US Business Analytics Software Market Size, Share, Trends and Forecast by Component, Deployment Mode, Application, Organization Size, End User, and Region, 2026-2034

US Business Analytics Software Market Size, Share, Trends & Forecast (2026-2034)

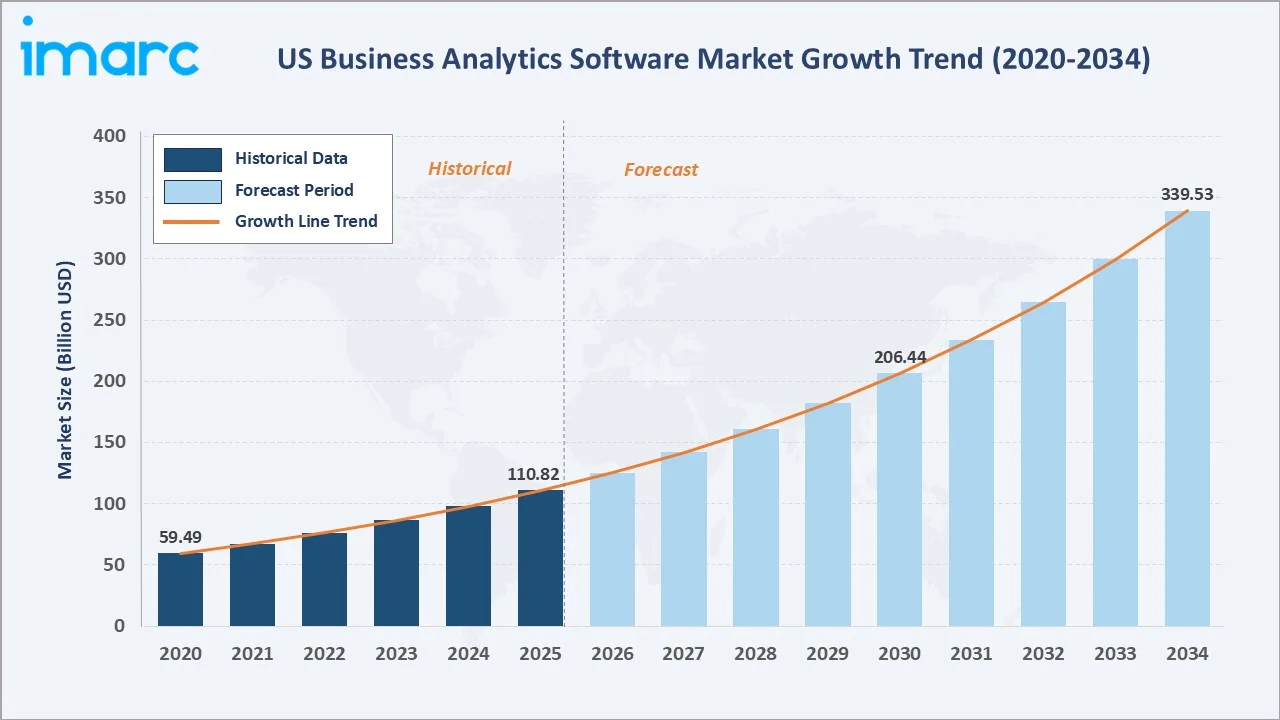

The US business analytics software market reached USD 110.82 Billion in 2025 and is projected to reach USD 339.53 Billion by 2034, growing at a CAGR of 13.25% during 2026-2034. The United States commands the world's dominant position in business analytics software, driven by the world's highest enterprise data generation volumes, the deepest concentration of analytics software vendors, and the accelerating integration of artificial intelligence and machine learning into every tier of the analytics software stack.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 110.82 Billion |

|

Forecast Market Size (2034) |

USD 339.53 Billion |

|

CAGR (2026-2034) |

13.25% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

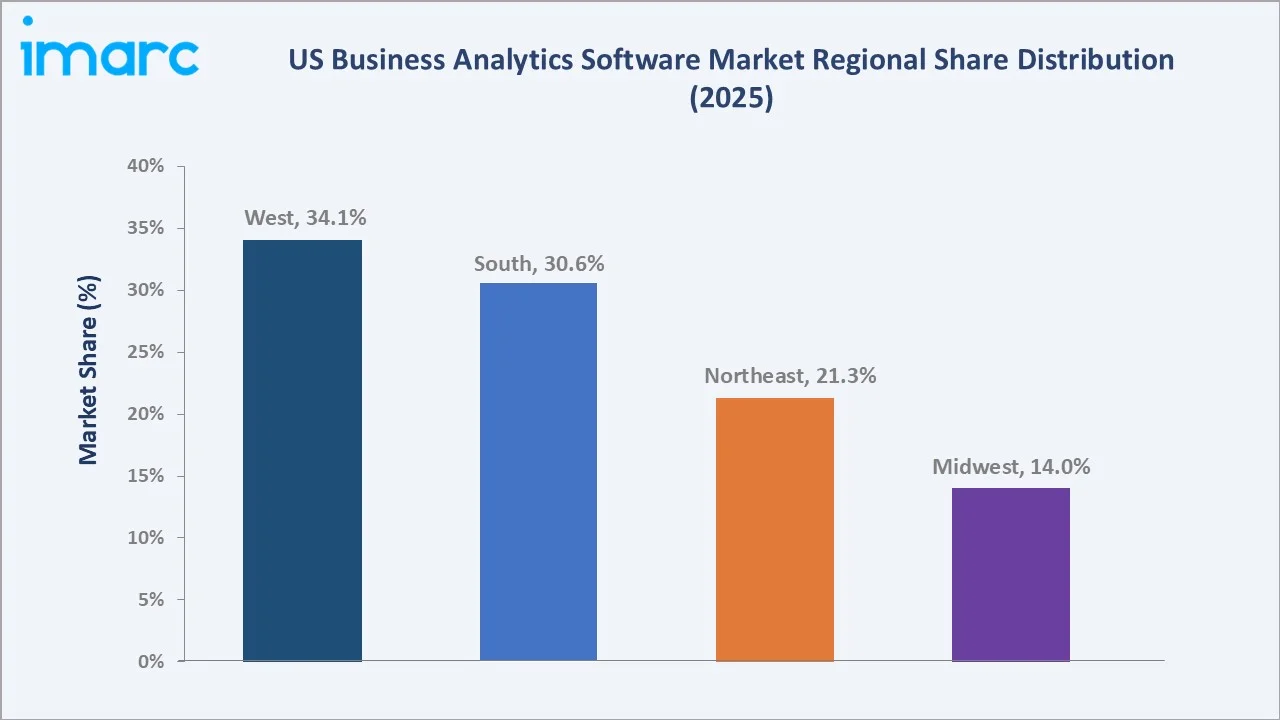

The West region leads with a 34.1% market share in 2025, anchored by Silicon Valley's technology sector, the world's highest concentration of analytics software vendors, hyperscale cloud infrastructure, and AI-driven enterprise adopters. Software dominates the component breakdown at 71.3%, while cloud deployment retains the largest share at 65.8% across deployment modes.

To get more information on this market, Request Sample

The US business analytics software market is underpinned by structural forces: the AI transformation of analytics platforms embedding large language model capabilities that automate insight generation at enterprise scale; and the competitive intelligence imperative, where US industry leaders across every sector are deploying advanced analytics to achieve the McKinsey-documented 23x customer acquisition and 19x profitability advantages associated with data-driven enterprise leadership.

Executive Summary

The US business analytics software market is experiencing accelerated expansion, driven by pervasive enterprise digital transformation, AI-augmented analytics adoption, and the cloud migration wave converting on-premises analytics deployments to subscription-based SaaS platforms. The market reached USD 110.82 Billion in 2025 and is forecast to reach USD 339.53 Billion by 2034, growing at a CAGR of 13.25%.

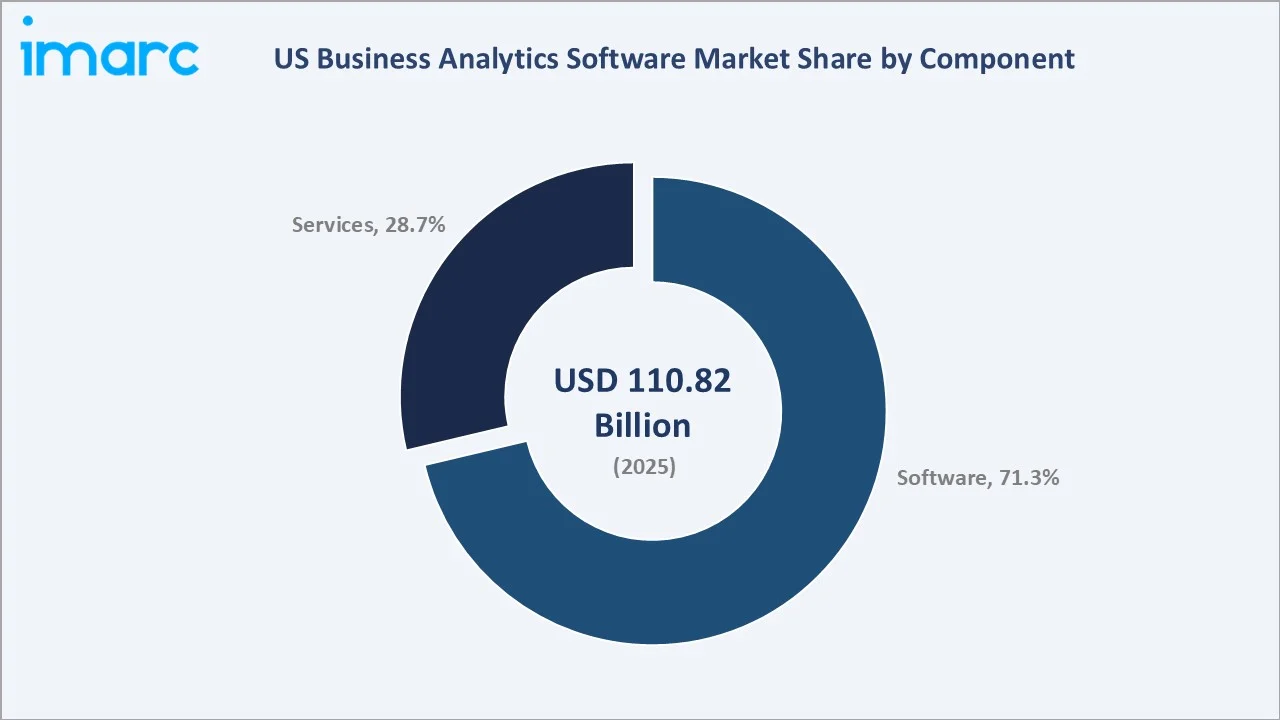

Software dominates the component segment with a 71.3% share in 2025, encompassing analytics platform licenses, cloud SaaS subscriptions, data visualization tools, predictive analytics engines, AI/ML model platforms, and embedded analytics SDKs.

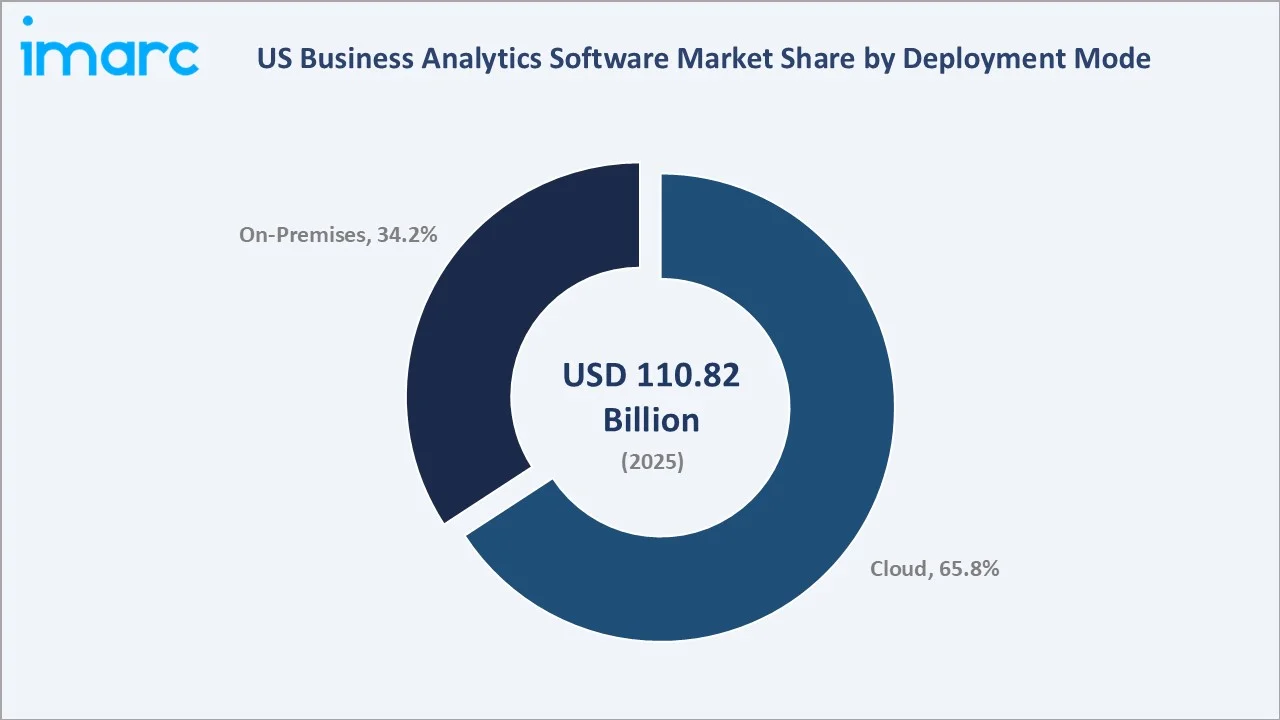

Cloud deployment commands a 65.8% majority share, driven by the enterprise migration from on-premises analytics deployments toward cloud-native platforms that provide elastic scalability, continuous capability updates, and consumption-based pricing aligned with actual usage rather than peak capacity provisioning.

The West region at 34.1% leads regionally, followed by the South at 30.6%, reflecting the geographic expansion of US enterprise technology adoption from Silicon Valley toward Texas's and Florida's growing technology sector concentrations. Leading vendors collectively represent the world's most competitive analytics software ecosystem.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Software – 71.3% share (2025) |

|

Fastest Growing Component |

Software – ~14.8% CAGR (2026-2034) |

|

Largest Deployment Mode |

Cloud – 65.8% share (2025) |

|

Fastest Growing Deployment |

Cloud – ~16.2% CAGR (2026-2034) |

|

Leading Region |

West – 34.1% share (2025) |

|

Top Companies |

Microsoft, Salesforce, Inc., SAP SE, SAS Institute Inc., Oracle |

Key Analytical Observations Supporting the Above Data:

- Software at 71.3% (2025) dominates as enterprise analytics software platforms generate high-margin recurring SaaS subscription revenue that creates durable revenue streams independent of services project cycles.

- Cloud deployment at 65.8% (2025) leads as the hyperscale cloud providers have made cloud-native analytics the default architecture for new enterprise deployments, with AWS QuickSight, Azure Synapse Analytics, and Google Looker providing fully managed analytics services that eliminate the infrastructure management overhead of on-premises analytics deployments.

- On-premise deployment at 34.2% (2025) persists among regulated industries that cannot migrate sensitive analytics workloads to public cloud due to compliance, data sovereignty, or security classification mandates requiring complete physical infrastructure control.

- The West's 34.1% share (2025) reflects Silicon Valley's dual role as both the primary analytics software vendor concentration and the most advanced enterprise analytics adoption market.

- Technology companies, including Alphabet, Meta, Netflix, and Apple, are simultaneously the most sophisticated analytics software users and the primary innovation drivers for next-generation analytics capabilities that subsequently propagate to mainstream enterprise adoption.

US Business Analytics Software Market Overview

Business analytics software encompasses the broad category of technology solutions that collect, process, analyze, and visualize enterprise data to support operational, tactical, and strategic decision-making. The US market spans descriptive analytics, diagnostic analytics, predictive analytics, prescriptive analytics, and cognitive analytics.

The market's macroeconomic foundation is the data economy transformation, where data has become the primary source of competitive advantage across all US industries, and the ability to generate superior insights from enterprise data faster than competitors determines market share, operational efficiency, and customer experience quality.

Market Dynamics

To evaluate market opportunities, Request Sample

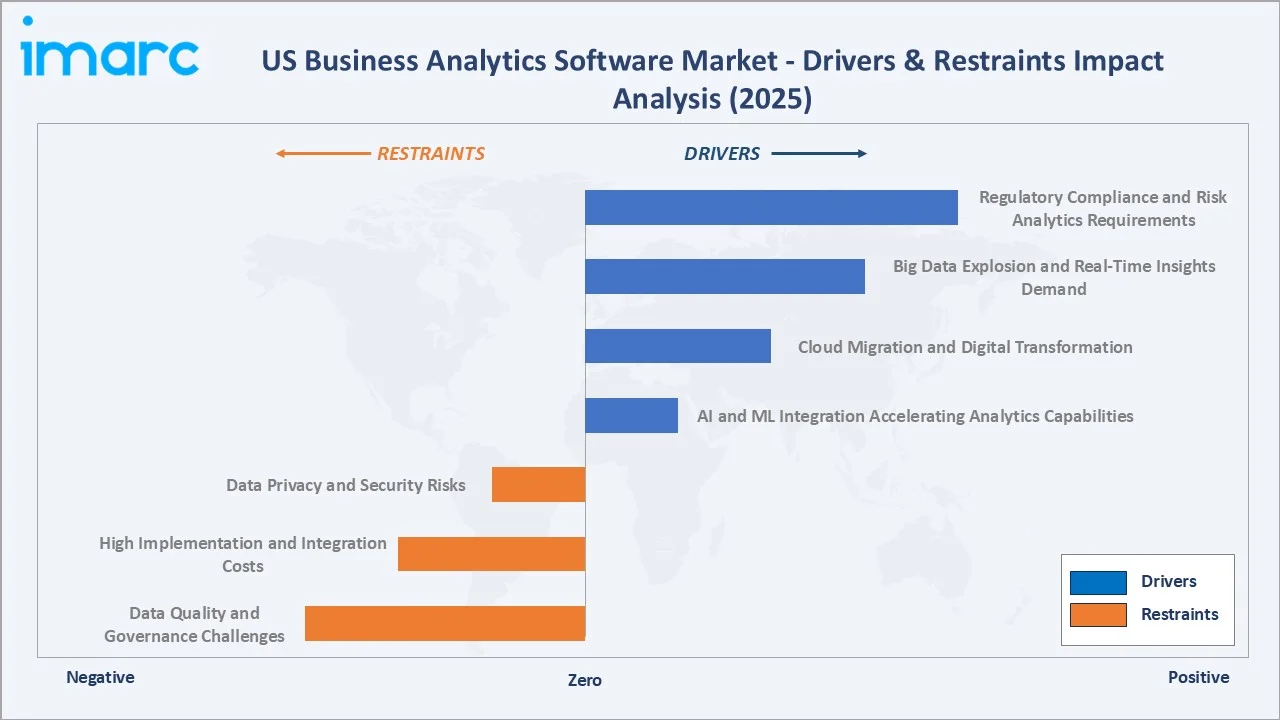

Market Drivers

- AI and ML Integration Accelerating Analytics Capabilities: The embedding of large language models and machine learning into analytics platforms is fundamentally transforming the value proposition of analytics software. AI-augmented analytics can process 100x more data variables than human analysts, identify non-linear relationships invisible to conventional reporting, and generate actionable recommendations within minutes versus weeks for traditional analytics projects.

- Cloud Migration and Digital Transformation: US enterprise digital transformation programs are systematically replacing legacy on-premises analytics infrastructure with cloud-native platforms. AWS's plans to boost capex to USD 100 billion in 2025 for investments in AI and Microsoft Azure's USD 80 billion AI infrastructure investment collectively create the cloud infrastructure foundation that makes cloud analytics economically superior to on-premises alternatives.

- Big Data Explosion and Real-Time Insights Demand: US IoT deployments are creating analytics workloads that exceed the processing capacity of traditional batch-reporting architectures. Real-time streaming analytics platforms are enabling sub-second insight generation from continuous data streams.

- Regulatory Compliance and Risk Analytics Requirements: US enterprises face an intensifying regulatory reporting landscape that creates non-discretionary analytics investment independent of enterprise IT budget constraints. Regulatory analytics software spending is estimated at USD 8–12 billion annually in the US, creating a captive analytics procurement market that sustains software revenue through economic cycles.

Market Restraints

- Data Privacy and Security Risks: The expansion of analytics software to process sensitive personal, financial, and health data creates significant cybersecurity exposure. The average US enterprise data breach cost reached USD 9.36 million in 2024, the highest globally, creating risk-averse procurement behavior that slows analytics adoption in industries handling sensitive consumer data.

- High Implementation and Integration Costs: Enterprise analytics platform deployments cost USD 1–20 million for large enterprise implementations spanning multiple data sources and business units. These costs create 18–36 month business case approval cycles that slow adoption velocity and create budget competition with other digital transformation priorities.

- Data Quality and Governance Challenges: A 2025 IBM Institute for Business Value (IBV) report found that 43% of chief operations officers consider data quality issues their top data priority. Poor data quality remains costly, with over one-fourth of organizations reporting annual losses above USD 5 million, and 7% losing USD 25 million or more.

Market Opportunities

- Augmented Analytics and AI-Generated Insights: The transition from analyst-driven insight generation to AI-automated insight delivery represents the next major commercial analytics software category. Microsoft Power BI Copilot, Salesforce Tableau Pulse, and ThoughtSpot's Spotter LLM analytics are pioneering this autonomous analytics paradigm.

- Industry Cloud Analytics Platforms: Major cloud providers are deploying industry-specific analytics platforms that pre-integrate analytics software with industry-standard data models, regulatory reporting templates, and sector-specific KPIs. These industry cloud analytics platforms compress implementation timelines from 18 months to 6 months by eliminating custom data model development.

Market Challenges

- Analytics Fragmentation and Platform Rationalization: US enterprises that deployed multiple point analytics tools during the 2010s self-service analytics wave are executing 'analytics rationalization' programs to consolidate to 2–3 enterprise-standard platforms. This rationalization creates large enterprise contract opportunities for winning platforms while generating displacement risk for specialized tools.

- Open Source Analytics Competition: The maturation of the open source analytics ecosystem is creating commercial analytics software pricing pressure as data science teams demonstrate that open source alternatives can perform core analytics functions at 80–90% of commercial platform capability at 10% of the cost.

Emerging Market Trends

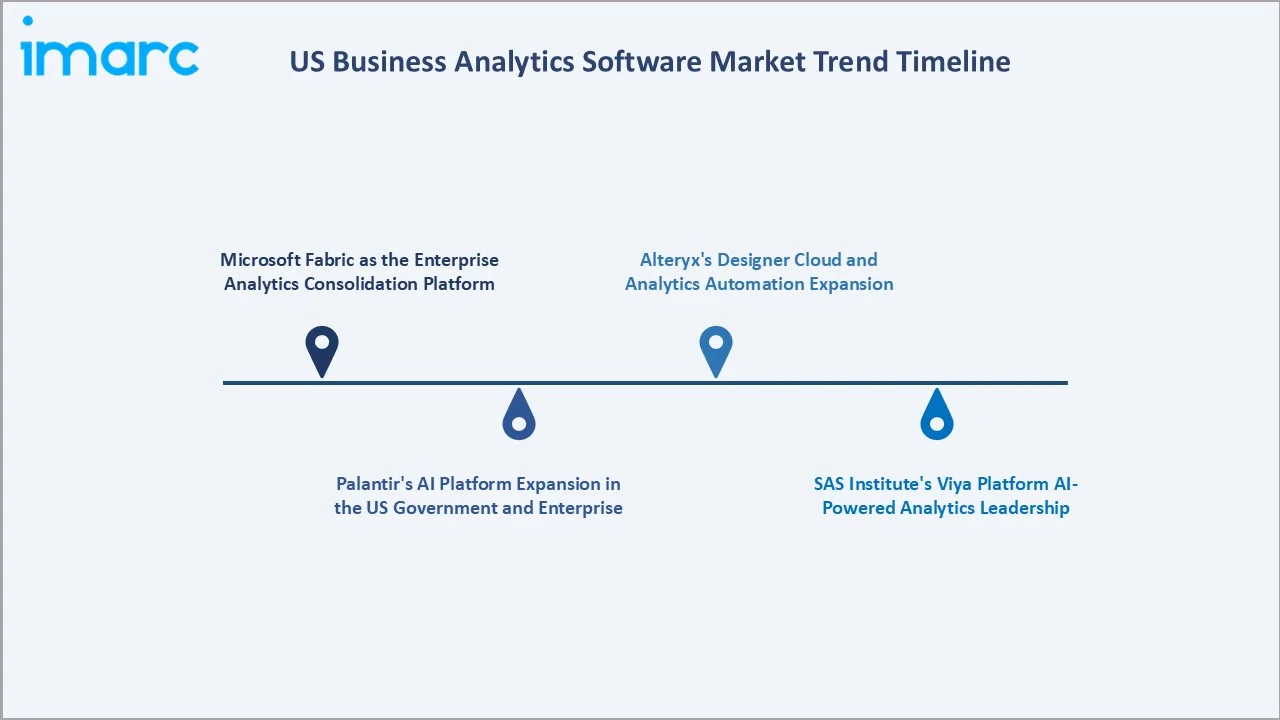

1. Microsoft Fabric as the Enterprise Analytics Consolidation Platform

Microsoft's unified analytics platform, Microsoft Fabric, achieved penetration in 70% of Fortune 500 companies by May 2025. Fabric's OneLake architecture combined with Copilot's natural language interface, is establishing Microsoft as the default enterprise analytics infrastructure for organizations already invested in the Microsoft cloud ecosystem.

2. Palantir's AI Platform Expansion in the US Government and Enterprise

Palantir Technologies' AI Platform (AIP) is transforming from a defense and intelligence analytics tool into a commercial enterprise analytics platform, with Palantir reporting U.S. commercial revenue reached USD 507 million, increasing 137% year-over-year and 28% quarter-over-quarter. Palantir's AIP boot camp deployment model is disrupting traditional analytics software procurement by demonstrating rapid time-to-value that justifies premium AIP pricing of USD 50,000–2 million per enterprise deployment.

3. SAS Institute's Viya Platform AI-Powered Analytics Leadership

In April 2026, SAS announced a refresh of SAS Data Management on the cloud-native SAS Viya platform to help enterprises prepare, govern, and activate data for trusted AI at scale. The update adds AI-ready data management, built-in governance, agentic AI/copilot capabilities, and cloud-native analytics acceleration to reduce data movement and improve automation.

4. Alteryx's Designer Cloud and Analytics Automation Expansion

Alteryx, acquired by Clearlake Capital Group, L.P. and Insight Partners L.P. in March 2024, is repositioning its analytics automation platform from desktop-centric data preparation to cloud-native analytics process automation. Alteryx Designer Cloud serves the rapidly growing analytics automation market, where organizations are replacing manual analytics processes with automated pipelines that continuously refresh insights on new data without analyst intervention.

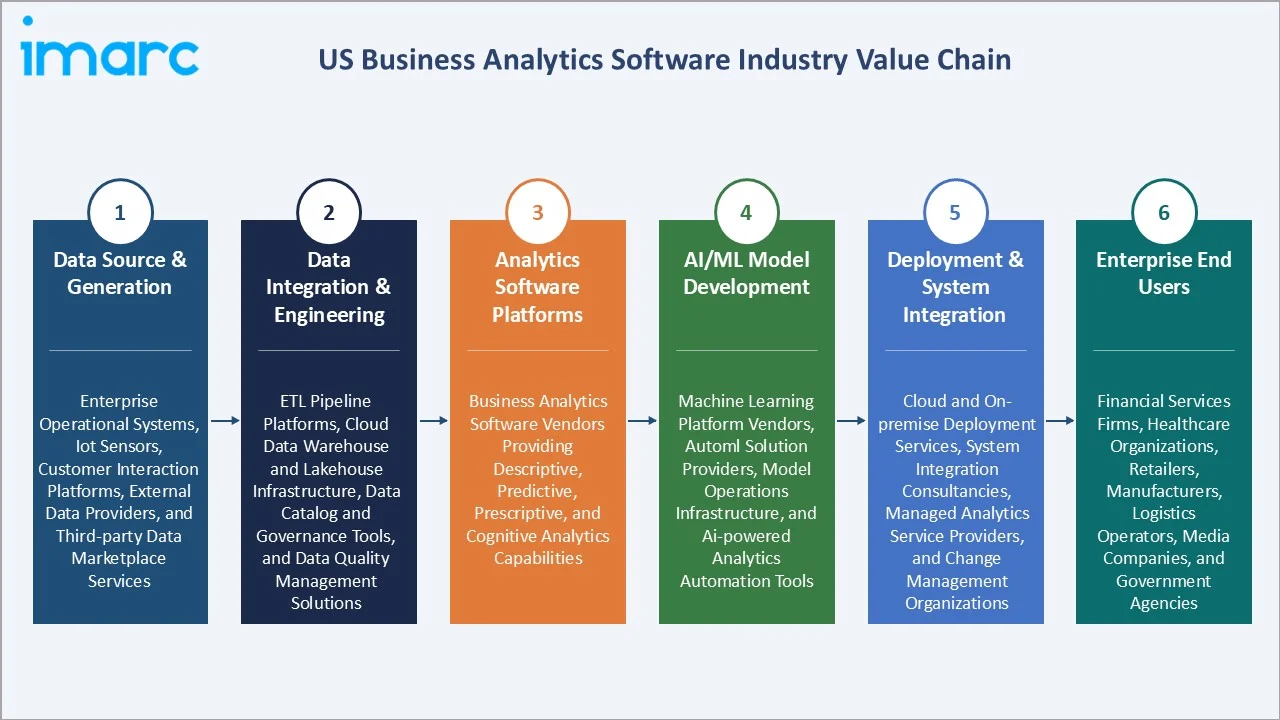

Industry Value Chain Analysis

The US business analytics software value chain spans enterprise data generation through decision-making action, with each stage occupied by specialized technology providers, platform vendors, system integrators, and consulting organizations whose collective performance determines the speed, accuracy, and economic value of enterprise analytics programs.

|

Stage |

Key Players / Examples |

|

Data Source & Generation |

Enterprise operational systems, IoT sensors, customer interaction platforms, external data providers, and third-party data marketplace services |

|

Data Integration & Engineering |

ETL pipeline platforms, cloud data warehouse and lakehouse infrastructure, data catalog and governance tools, and data quality management solutions |

|

Analytics Software Platforms |

Business analytics software vendors providing descriptive, predictive, prescriptive, and cognitive analytics capabilities |

|

AI/ML Model Development |

Machine learning platform vendors, AutoML solution providers, model operations infrastructure, and AI-powered analytics automation tools |

|

Deployment & System Integration |

Cloud and on-premise deployment services, system integration consultancies, managed analytics service providers, and change management organizations |

|

Enterprise End Users |

Financial services firms, healthcare organizations, retailers, manufacturers, logistics operators, media companies, and government agencies |

Technology Landscape in the US Business Analytics Software Industry

Cloud-Native Analytics Platforms and Data Lakehouse Architecture

The US analytics software market's technical foundation is transitioning to cloud-native data lakehouse architecture supported by Databricks' Lakehouse Platform, Snowflake's Data Cloud, and Microsoft Azure Synapse Analytics. These lakehouse platforms serve as the analytical data foundation upon which cloud analytics applications deliver business insights, with unified governance and ACID transaction support enabling reliable enterprise analytics on petabyte-scale data sets.

AI-Augmented Analytics and Automated Machine Learning

The integration of AutoML, natural language processing, and large language model capabilities into analytics software platforms is the primary technical differentiation vector in the US market. Microsoft Copilot for Power BI and SAS Viya's model management enables business analysts without data science training to build and deploy predictive models, reducing the time from business question to deployed predictive model from 6 months to 6 weeks.

Real-Time Streaming Analytics

The US analytics software market is rapidly expanding to encompass real-time streaming analytics. AWS Kinesis and Azure Event Hubs' streaming analytics platforms are enabling use cases, including algorithmic trading, real-time fraud detection, predictive maintenance alerts, and dynamic pricing optimization that require analytics latency measured in milliseconds rather than hours or days.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Software |

71.3% |

2025 |

|

Deployment Mode |

Cloud |

65.8% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Organization Size |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

West |

34.1% |

2025 |

By Component

The software segment dominates with a 71.3% share in 2025, reflecting the high-margin recurring subscription revenue model that analytics platform vendors have successfully transitioned to, with average gross margins of 75–85% on SaaS analytics subscriptions versus 30–45% for professional services engagements.

To access detailed market analysis, Request Sample

Services represent 28.7% share of the market (2025) and are projected to grow at approximately 9.6% CAGR as enterprises shift from one-time analytics implementations toward continuous analytics optimization engagements, where consulting firms provide ongoing data engineering, model retraining, and dashboard enhancement services under multi-year managed analytics contracts that provide stable recurring revenue complementary to software license streams.

By Deployment Mode

Cloud deployment commands a 65.8% share in 2025, reflecting the enterprise consensus that cloud-native analytics delivers superior economics versus maintaining dedicated on-premises analytics infrastructure. The 16.2% CAGR of cloud analytics exhibits both new deployments and the accelerating migration of on-premises analytics workloads to cloud platforms as legacy analytics system refresh cycles complete.

On-premise deployment represents 34.2%, sustained by its application in large manufacturing and energy sectors, where operational technology analytics require real-time access to plant-floor sensor data with millisecond latency that cannot be economically achieved over WAN connections to public cloud analytics platforms.

Regional Market Insights

The West region's market leadership (34.1%, 2025) reflects Silicon Valley's dual role as the world's primary analytics software vendor concentration and its most sophisticated enterprise analytics adopter market. The Bay Area hosts the headquarters of top players, creating the most concentrated analytics innovation ecosystem globally.

The South at 30.6% is growing fastest in absolute market value terms, driven by Texas's emergence as a major enterprise analytics hub and Virginia's Northern Virginia corridor serving as the US federal government's primary analytics technology procurement center.

|

Region |

Share (2025) |

Key Growth Drivers |

|

West |

34.1% |

Silicon Valley analytics software vendor concentration and advanced enterprise adopter density; hyperscale cloud infrastructure; high-growth technology startup analytics platform adoption |

|

South |

30.6% |

Texas Fortune 500 headquarters concentration driving large enterprise analytics procurement; Florida financial services, healthcare, and logistics sector analytics adoption |

|

Northeast |

21.3% |

Wall Street financial services analytics investment at the highest per-employee spend globally; Boston-Cambridge life sciences analytics adoption; New York media and advertising analytics platforms |

|

Midwest |

14.0% |

Manufacturing and automotive sector operational analytics at scale; major insurance and financial services analytics programs; healthcare analytics across major Midwest integrated delivery networks; growing state government digital transformation analytics investment |

Competitive Landscape

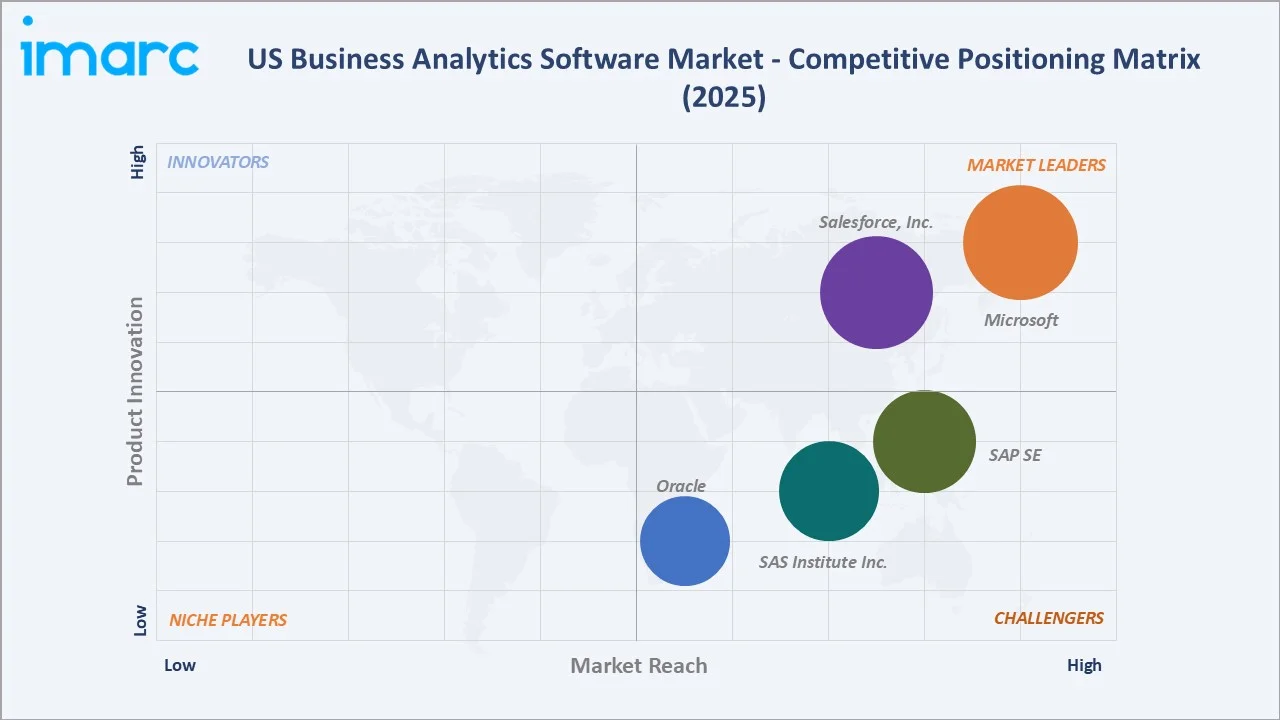

The US business analytics software market exhibits moderate concentration at the platform level, with Microsoft, Salesforce, Inc., and SAP SE collectively holding approximately 35–42% of total market revenue in 2025 based on analytics software revenue estimates.

|

Company Name |

Products/Solutions |

Market Position |

Core Strength |

|

Microsoft |

Power BI, Power BI Embedded, Azure Analysis Services, Azure Synapse Analytics, Microsoft Fabric |

Market Leader |

Microsoft Fabric unified analytics; Power BI and Copilot AI; Azure cloud ecosystem; Office 365 enterprise user distribution advantage |

|

Salesforce, Inc. |

Tableau Pulse, Embedded Analytics, Tableau Exchange, CRM Analytics, Revenue Intelligence, Data 360, Marketing Analytics, Sales Analytics |

Market Leader |

Tableau visual analytics leadership; Einstein AI integration; Tableau Pulse AI-generated insights |

|

SAP SE |

SAP Business Data Cloud, SAP HANA Cloud |

Strong Challenger |

Deep ERP integration; HANA in-memory analytics; enterprise finance and supply chain analytics leadership |

|

SAS Institute Inc. |

SAS Viya, Embedded Analytics, Automated Insights, Augmented Analytics for Data Scientists, Location Intelligence |

Strong Challenger |

Viya AI-powered analytics platform; statistical and regulatory analytics leadership; healthcare and financial services domain expertise |

|

Oracle |

Oracle Fusion Data Intelligence, Oracle Cloud Infrastructure (OCI) AI services |

Challenger |

Oracle Analytics Cloud; Fusion Data Intelligence; native ERP-to-analytics integration advantage |

Competition is intensifying as vendors differentiate through automation, real-time insights, embedded analytics, generative AI capabilities, and integration with enterprise data ecosystems.

Key Company Profiles

Microsoft

Microsoft is one of the US business analytics software market leaders, combining the world's most widely deployed analytics platform with Microsoft Fabric's unified analytics infrastructure and Copilot AI's natural language analytics democratization.

- Product Portfolio: Microsoft Power BI, Power BI Embedded, Microsoft Fabric, Azure Synapse Analytics, Azure Machine Learning, Power BI Copilot, Azure, and Azure Analysis Services.

- Strategic Focus: Microsoft Fabric ecosystem expansion; Copilot AI analytics democratization; real-time analytics via Fabric Real-Time Intelligence; data governance through Microsoft Purview; industry cloud analytics solutions for healthcare, financial services, and manufacturing.

SAS Institute Inc.

SAS Institute Inc. is one of the world's largest privately held analytics software companies and the longtime leader in advanced statistical analytics, regulatory reporting, and AI-powered enterprise analytics for regulated industries.

- Product Portfolio: SAS Viya, Embedded Analytics, Automated Insights, Augmented Analytics for Data Scientists, and Location Intelligence.

- Strategic Focus: SAS Viya cloud adoption acceleration; healthcare and life sciences AI analytics; financial services regulatory analytics and model risk management; government analytics modernization; AI governance and responsible AI differentiation.

Market Concentration Analysis

The US business analytics software market is moderately concentrated at the platform level, with Microsoft, Salesforce, Inc., and SAP SE collectively holding approximately 35–42% of software revenue. The remaining 58–65% is distributed across IBM Corporation, Oracle, SAS Institute Inc., Qlik, Adobe Analytics, Palantir, Alteryx, Strategy, and 300+ specialized analytics software vendors serving specific industries, use cases, or analytical disciplines.

The market's structural dynamics favor platform consolidation, while simultaneously expanding per-platform usage depth through AI capabilities, embedded analytics modules, and industry-specific analytics applications. This consolidation benefits integrated platform vendors while creating displacement pressure on specialized point analytics tools.

Investment & Growth Opportunities

Fastest Growing Segments

Cloud analytics (~16.2% CAGR), AI-powered automated machine learning (~30% CAGR), real-time streaming analytics (~28% CAGR), and industry-specific analytics cloud platforms (~22% CAGR) represent the highest-growth investment vectors through 2034. Together, these subcategories address a combined USD 100+ billion incremental addressable market opportunity within the US business analytics software ecosystem by 2030.

Emerging Market Expansion

US business analytics software vendors are expanding into emerging markets by offering cloud-based, scalable, and cost-efficient analytics platforms for enterprises undergoing digital transformation. Rising demand for real-time insights, data visualization, predictive analytics, and AI-enabled decision-making across Asia Pacific, Latin America, and the Middle East is creating new growth opportunities for US providers.

Venture and Institutional Investment Trends

- AI-native analytics startups are raising substantial growth rounds as they demonstrate superior performance versus incumbent analytics platforms in specific use cases: ThoughtSpot, Hex, Sigma Computing, and Lightdash collectively represent approximately USD 15 billion in venture-backed analytics software innovation funded since 2020.

Future Market Outlook (2026-2034)

The US business analytics software market is positioned for sustained, above-average expansion through 2034. From a base of USD 110.82 Billion in 2025, the market is projected to reach USD 339.53 Billion by 2034, representing total incremental value creation of USD 228.71 billion at a CAGR of 13.25%.

This growth is underpinned by the inexorable data economy transformation of the US economy, the non-discretionary nature of regulatory analytics investment, and the competitive necessity of AI-powered analytics capabilities that are converting analytics from a discretionary IT investment to a strategic competitive necessity for US market leaders across all industries.

By 2034, the market's composition will shift toward autonomous analytics—where AI agents continuously monitor business metrics, generate insights, and recommend actions without analyst intervention. Cloud deployment will reach 80%+ share as on-premises analytics completes its lifecycle transition for non-regulated workloads.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 105 industry participants in 2024–2025, including analytics software executives, enterprise analytics directors, data science managers, BI consulting principals, and institutional investors across California, Texas, New York, and Virginia.

Secondary Research

Secondary research encompassed vendor annual reports and investor presentations, IDC Worldwide Analytics and Data Management Software Tracker, Gartner Magic Quadrant for Analytics and Business Intelligence Platforms (2024, 2025), Forrester Wave Analytics Platforms, and industry publications (Information Management, TDWI Research, Data Science Weekly).

Forecasting Models

Market size estimations incorporated US enterprise data and analytics software spending surveys, cloud migration velocity data, AI analytics adoption projections, and vendor software revenue growth disclosures. A base-case CAGR of 13.25% reflects consensus estimates validated against vendor revenue trajectories, IDC market share data, and enterprise IT budget allocation surveys from FY2020 to FY2025.

US Business Analytics Software Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Software, Service |

| Deployment Modes Covered | On-premise, Cloud |

| Applications Covered | Customer Analytics, Supply Chain Analytics, Marketing Analytics, Pricing Analytics, Risk and Credit Analytics, Others |

| Organization Sizes Covered | Large Enterprises, Small and Medium-sized Enterprises |

| End Users Covered | IT & Telecom, Retail & E-commerce, BFSI, Manufacturing, Healthcare, Government, Education, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Microsoft, Salesforce, Inc., SAP SE, SAS Institute Inc., Oracle, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the US business analytics software market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the US business analytics software market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the US business analytics software industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the US Business Analytics Software Market Report

The US business analytics software market reached USD 110.82 Billion in 2025 and is projected to reach USD 339.53 Billion by 2034.

The market is expected to grow at a CAGR of 13.25% during 2026-2034, driven by AI/ML integration, cloud migration, big data analytics adoption, and regulatory compliance analytics requirements.

The West region leads with a 34.1% share in 2025, anchored by Silicon Valley's analytics software vendor concentration, hyperscale cloud infrastructure, and the most advanced enterprise analytics adoption in the US economy.

Software dominates with a 71.3% share in 2025, encompassing analytics platform licenses, cloud SaaS subscriptions, data visualization tools, predictive analytics engines, and AI/ML model platforms.

Cloud deployment holds the largest share at 65.8%, reflecting enterprise migration from legacy on-premises analytics deployments to cloud-native platforms delivering elastic scalability, continuous updates, and consumption-based pricing.

Some of the key players include Microsoft, Salesforce, Inc., SAP SE, SAS Institute Inc., and Oracle.

Cloud analytics is growing at ~16.2% CAGR as enterprises are systematically migrating on-premises analytics to Microsoft Fabric, Salesforce Tableau Cloud, and SAP Analytics Cloud, reducing infrastructure costs and enabling automatic AI feature updates.

Key challenges include data privacy and security risks for cloud analytics deployments, high implementation costs for enterprise analytics projects, data quality and governance challenges degrading analytics reliability, analytics talent shortages, and the open source analytics competition providing commodity capabilities at zero license cost.

AI-powered automated machine learning, real-time streaming analytics for IoT, industry-specific analytics cloud platforms, edge analytics for manufacturing, and analytics process automation represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)