US Clinical Trials Management System Market Size, Share, Trends and Forecast by Component, Deployment Mode, End User, and Region, 2026-2034

US Clinical Trials Management System Market Size, Share, Trends & Forecast (2026-2034)

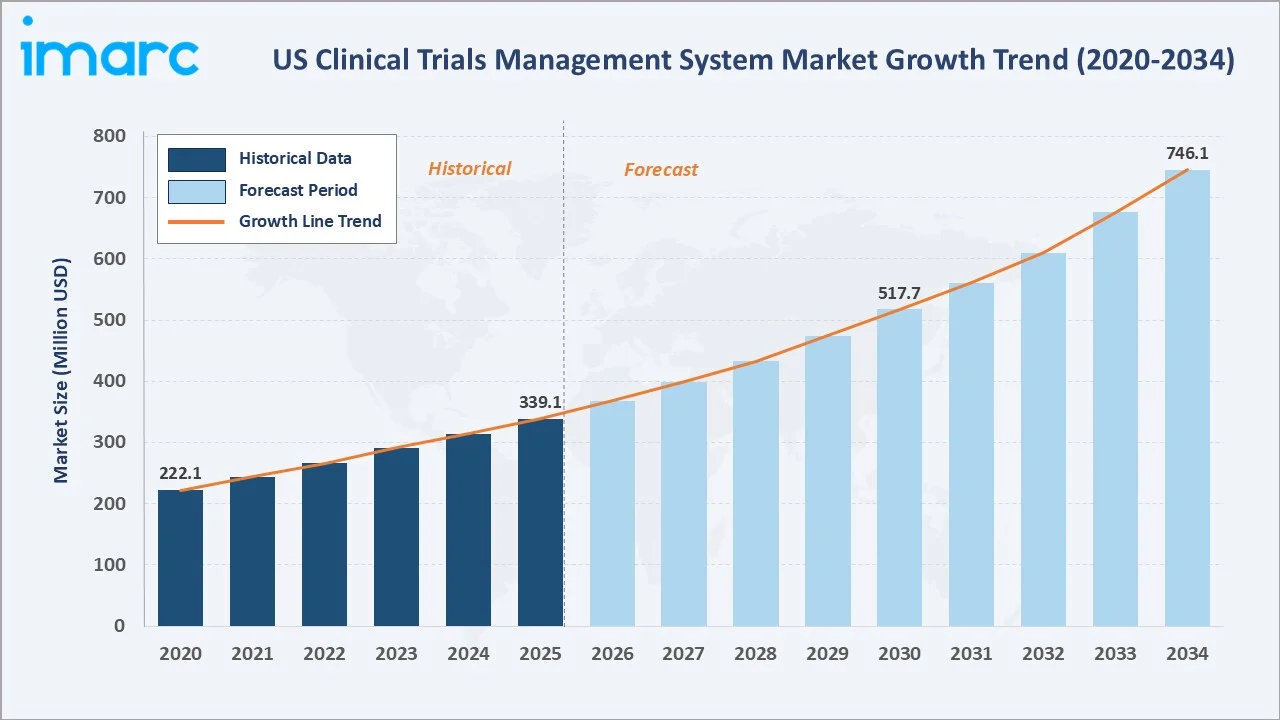

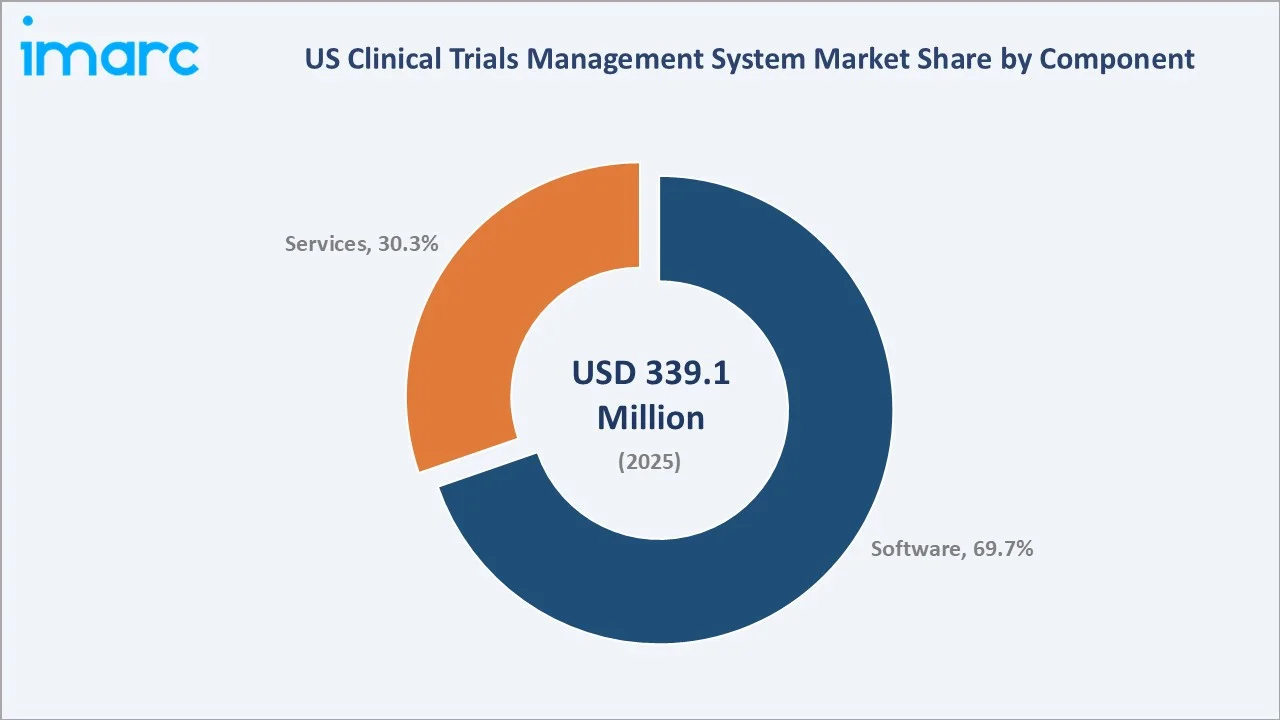

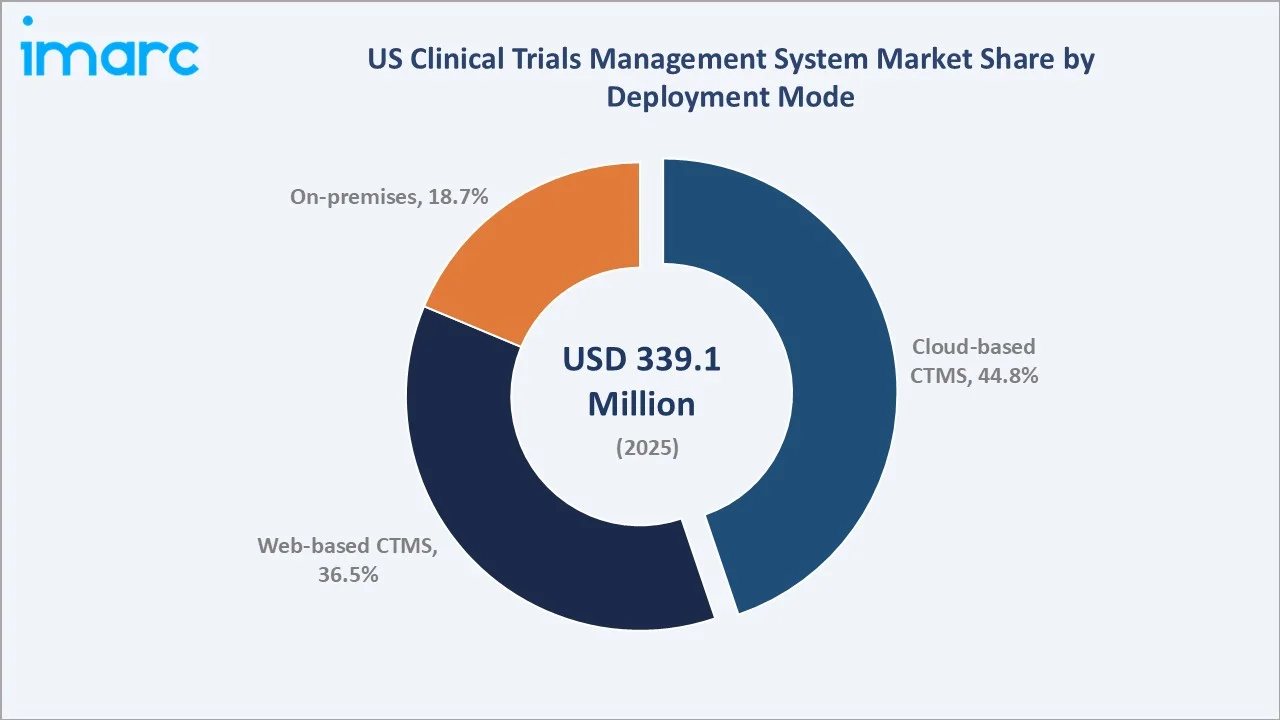

The US clinical trials management system market was valued at USD 339.1 Million in 2025 and is projected to reach USD 746.1 Million by 2034, exhibiting a CAGR of 8.83% during 2026-2034. The Center for Drug Evaluation and Research (CDER) approved 55 novel drugs in 2023, underscoring the expanding pharmaceutical pipeline that is amplifying demand for robust clinical trials management system platforms.

Software accounts for 69.7% of the component segment, cloud-based CTMS leads deployment mode at 44.8%, and Northeast holds 32.1% of the regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 339.1 Million |

|

Forecast Market Size (2034) |

USD 746.1 Million |

|

CAGR (2026-2034) |

8.83% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Northeast (32.1%, 2025) |

|

Second Largest Region |

West (27.8%, 2025) |

|

Leading Component |

Software (69.7%, 2025) |

|

Leading Deployment Mode |

Cloud-based CTMS (44.8%, 2025) |

The US clinical trials management system market expanded from USD 222.1 Million in 2020 to USD 339.1 Million in 2025, propelled by increasing clinical trial activity, heightened regulatory compliance requirements, and widening adoption of cloud-native platforms across pharmaceutical sponsors, contract research organizations (CROs), and academic medical centers. Anchored at USD 517.7 Million in 2030, the forecast to USD 746.1 Million by 2034 is supported by accelerating decentralized trial adoption and artificial intelligence (AI)-enabled protocol management.

To get more information on this market, Request Sample

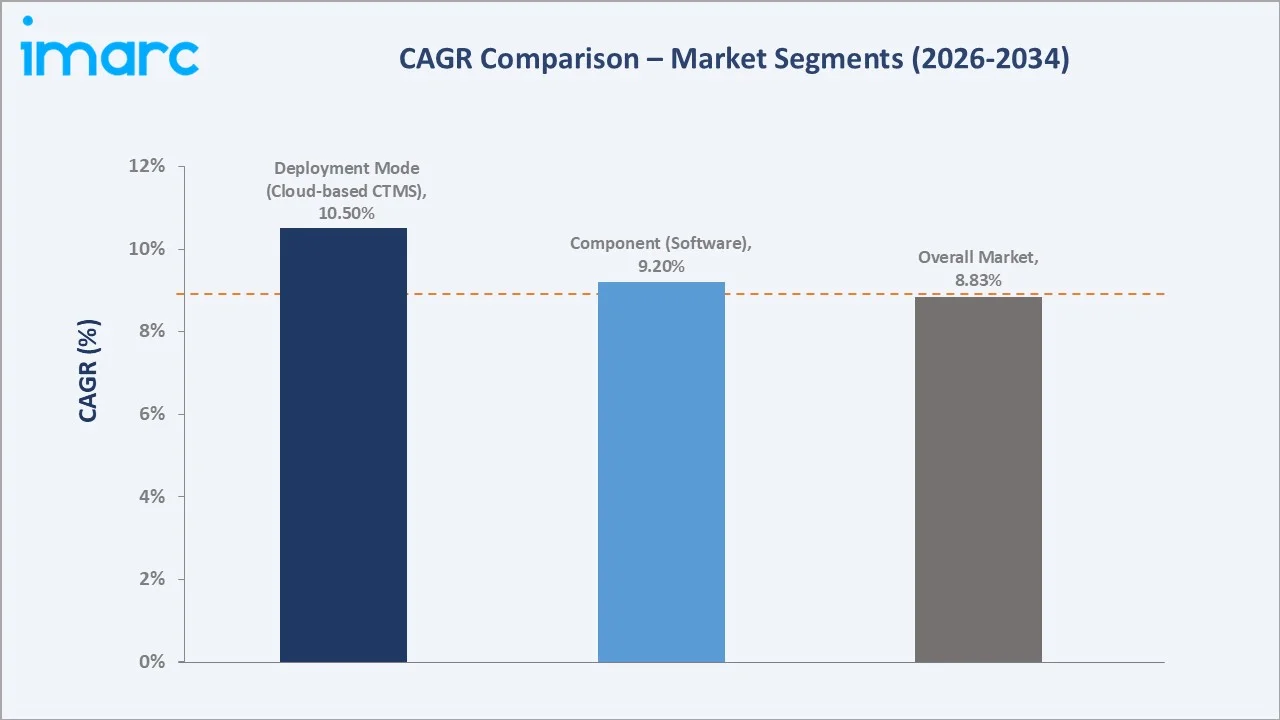

CAGR trajectories across component and deployment mode sub-segments show cloud-based CTMS and software expanding faster than the overall 8.83% market CAGR, driven by pharmaceutical sponsors prioritizing scalable, subscription-based platforms and CROs demanding real-time multi-site visibility.

Executive Summary

The US clinical trials management system market is on a sustained growth trajectory from USD 222.1 Million in 2020 to USD 746.1 Million by 2034. The segment has evolved from paper-based and fragmented electronic tracking to fully integrated, cloud-enabled platforms that manage trial planning, patient enrollment, regulatory documentation, site performance, and financial reconciliation within a unified digital environment.

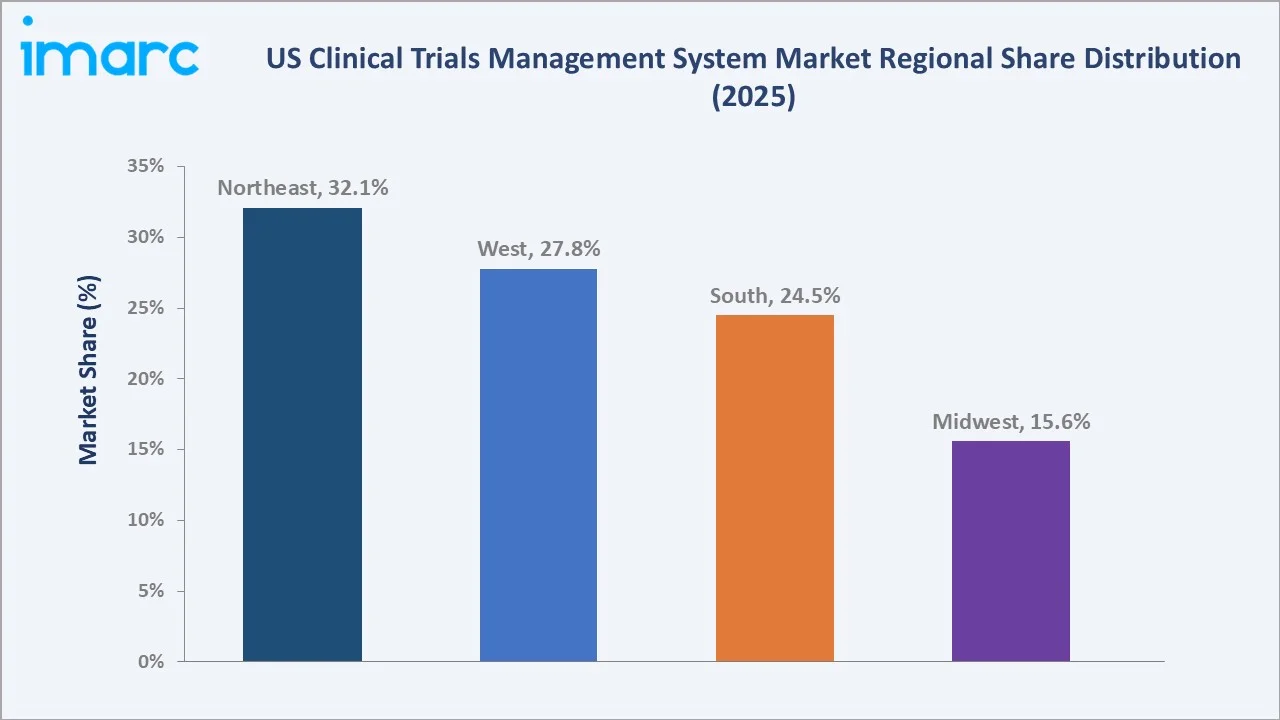

Software commands 69.7% of the component segment in 2025, reflecting the depth of functionality required for end-to-end trial lifecycle management. Cloud-based CTMS leads deployment mode at 44.8%, supported by lower total cost of ownership, faster deployment cycles, and native support for remote monitoring and decentralized trial workflows. Northeast holds 32.1% of the regional share, anchored by high concentration of academic medical centers, pharmaceutical headquarters, and CRO hubs in the country.

Key Market Insights

|

Insight |

Data |

|

Leading Component |

Software – 69.7% share (2025) |

|

Second Largest Component |

Services – 30.3% share (2025) |

|

Leading Deployment Mode |

Cloud-based CTMS – 44.8% share (2025) |

|

Second Largest Deployment Mode |

Web-based CTMS – 36.5% share (2025) |

|

Leading Region |

Northeast – 32.1% share (2025) |

|

Second Largest Region |

West – 27.8% share (2025) |

|

Top Companies |

Dassault Systèmes, Veeva Systems Inc., Valsoft, Florence Healthcare |

Key Analytical Observations Expanding On The Data Above:

- Software leadership at 69.7% reflects the high-value functionality embedded in clinical trials management system platforms, encompassing protocol management, regulatory document tracking, adverse event reporting, and financial reconciliation, all of which require continuous licensing and upgrade investment.

- Services at 30.3% covers implementation, validation, training, and ongoing managed services that sponsors and CROs procure alongside software licenses to ensure GCP compliance and operational readiness.

- Cloud-based CTMS at 44.8% is the largest and fastest-growing deployment mode, driven by faster deployment cycles, scalable multi-site access, and native support for remote monitoring and source data review.

- Web-based CTMS at 36.5% continues to serve mid-sized sponsors and investigator-led sites that require browser-based access without full cloud migration, particularly in community hospital and academic settings.

- Northeast dominance at 32.1% is anchored by the high density of academic medical centers, biopharma headquarters, and top-tier CROs along the Boston-New York-Philadelphia corridor.

US Clinical Trials Management System Market Overview

A clinical trials management system is an enterprise-grade software platform designed to manage the operational, regulatory, financial, and logistical aspects of clinical research across the full trial lifecycle. Clinical trials management system solutions support study startup activities, including protocol development and IRB tracking, patient recruitment and enrollment monitoring, investigational product accountability, regulatory document management, site performance reporting, and study closeout processes.

The US ecosystem integrates clinical trials management system software vendors, CRO platforms, electronic data capture providers, regulatory technology specialists, laboratory information management systems, clinical supply chain vendors, and site management organizations. Together, these stakeholders enable pharmaceutical sponsors, biotech firms, device manufacturers, and academic research centers to execute compliant and efficient clinical trials under FDA oversight frameworks.

Market Dynamics

To evaluate market opportunities, Request Sample

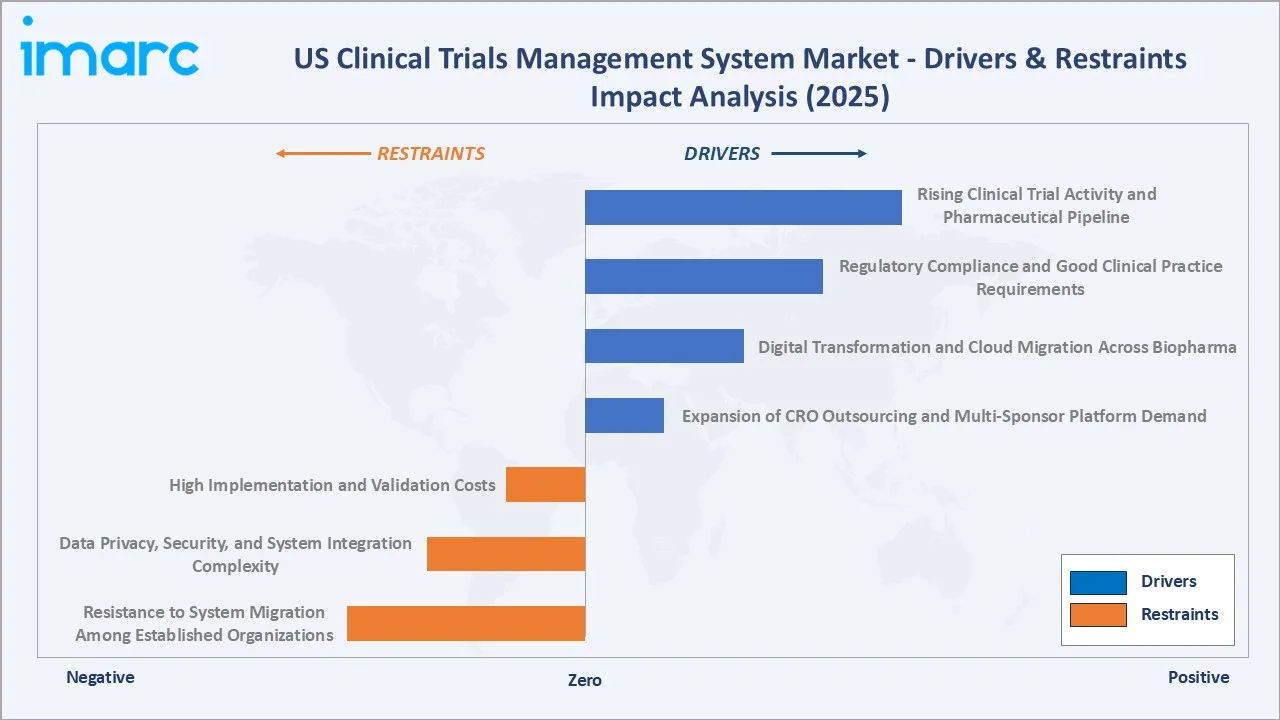

Market Drivers

- Rising Clinical Trial Activity and Pharmaceutical Pipeline: The US continues to lead global clinical research activity, with the FDA receiving a growing number of Investigational New Drug (IND) applications each year across oncology, rare disease, immunology, and gene therapy indications. In May 2026, Oorja Bio obtained IND approval from the FDA for the clinical progression of ORJ-001 and intends to commence a Phase 2 clinical study this year in IPF patients. The sustained volume of trial activity creates continuous demand for clinical trials management system platforms capable of managing complex multi-site study operations and regulatory submission workflows within tight sponsor timelines.

- Regulatory Compliance and Good Clinical Practice Requirements: Adherence to FDA regulations and Good Clinical Practice guidelines requires sponsors and investigative sites to maintain meticulous documentation, complete audit trails, and version-controlled regulatory files throughout every stage of a clinical trial. Clinical trials management system platforms address this requirement by providing structured, role-based workflows for IRB submissions, informed consent tracking, adverse event reporting, and electronic trial master file management.

- Digital Transformation and Cloud Migration Across Biopharma: Pharmaceutical sponsors and CROs are systematically retiring fragmented, on-premises trial tracking tools in favor of cloud-native clinical trials management system platforms that support real-time collaboration across geographically distributed study teams. The move toward cloud-based deployment reflects broader enterprise technology modernization strategies, with sponsors seeking lower infrastructure overhead and faster vendor-managed compliance updates.

- Expansion of CRO Outsourcing and Multi-Sponsor Platform Demand: Growing reliance on CROs for end-to-end trial execution across all development phases is creating structured demand for clinical trials management system platforms capable of supporting multiple concurrent sponsors, configurable client-specific workflows, and granular study-level access controls.

Market Restraints

- High Implementation and Validation Costs: Enterprise clinical trials management system deployment involves substantial investment in software licensing, computer system validation, staff training, and technical integration with existing electronic data capture and regulatory document management systems. For smaller sponsors and emerging biotech companies, the upfront cost and timeline associated with validated clinical trials management system implementation represent a meaningful barrier, often leading organizations to defer adoption or rely on manual and semi-automated workarounds that limit operational efficiency.

- Data Privacy, Security, and System Integration Complexity: Clinical trial management platforms handle sensitive investigator, patient, and protocol data, requiring robust security measures, such as encryption, access controls, and audit trails. In addition, integrating these platforms with other clinical and research systems remains a complex challenge, especially across multi-vendor technology environments.

- Resistance to System Migration Among Established Organizations: Many large pharmaceutical companies and academic medical centers have operated the same clinical trials management system or internally developed tracking platforms for extended periods, creating deeply embedded operational processes and institutional dependencies that are difficult to unwind. The prospect of migrating historical trial data and managing transition risk during active studies creates organizational inertia that slows adoption of modern platforms.

Market Opportunities

- AI Integration for Operational Efficiency: The embedding of AI and machine learning (ML) capabilities within clinical trials management system platforms for site feasibility scoring, enrollment trajectory modeling, protocol deviation detection, and automated document classification represents a meaningful opportunity to expand the functional value proposition beyond core trial tracking.

- Rare Disease and Specialty Therapy Trial Growth: The accelerating development of therapies for rare and ultra-rare conditions is generating a growing pipeline of specialized trials that involve small patient populations, complex eligibility criteria, multi-modal data collection, and adaptive design frameworks. These studies place premium demands on clinical trials management system configurability, data flexibility, and regulatory workflow support.

Market Challenges

- Multi-System Integration in Complex Technology Environments: Clinical trial management platforms must integrate seamlessly with various research and healthcare systems. Maintaining reliable and validated data exchange across these platforms increases operational complexity and costs.

- Workforce Capability and Clinical Research Technology Expertise: Effective use of clinical trial management platforms requires expertise in clinical research, regulatory compliance, and enterprise software. The shortage of skilled professionals can delay implementation and limit platform utilization.

Emerging Market Trends

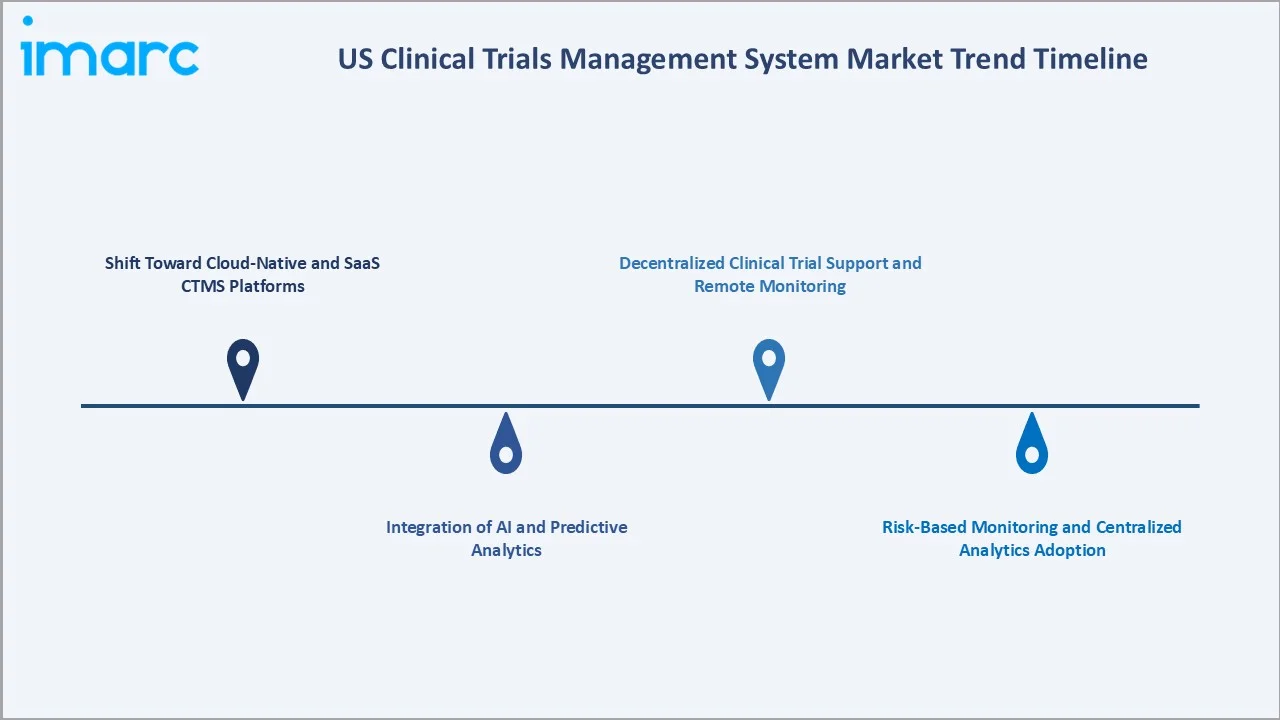

1. Shift Toward Cloud-Native and SaaS Clinical Trials Management System Platforms

Pharmaceutical sponsors and CROs are accelerating migration from on-premises to cloud-native and SaaS clinical trials management system deployments to reduce IT infrastructure burden, enable real-time global collaboration, and improve disaster recovery readiness.

2. Integration of AI and Predictive Analytics

Leading clinical trials management system vendors are embedding AI and ML capabilities for site feasibility scoring, patient enrollment prediction, protocol deviation early warning, and automated safety narrative generation.

3. Decentralized Clinical Trial Support and Remote Monitoring

Following the FDA's 2024 decentralized clinical trial guidance, clinical trials management system platforms are incorporating native support for remote site visits, electronic patient-reported outcomes, wearable data ingestion, and home health worker coordination. This structural shift toward hybrid and fully decentralized models is creating new module categories within clinical trials management system platforms.

4. Risk-Based Monitoring and Centralized Analytics Adoption

The shift toward risk-based and centralized monitoring is driving demand for clinical trial management platforms with advanced analytics, remote oversight, and integrated risk management capabilities. These features help improve data quality, streamline monitoring activities, and support more efficient multi-site trial operations.

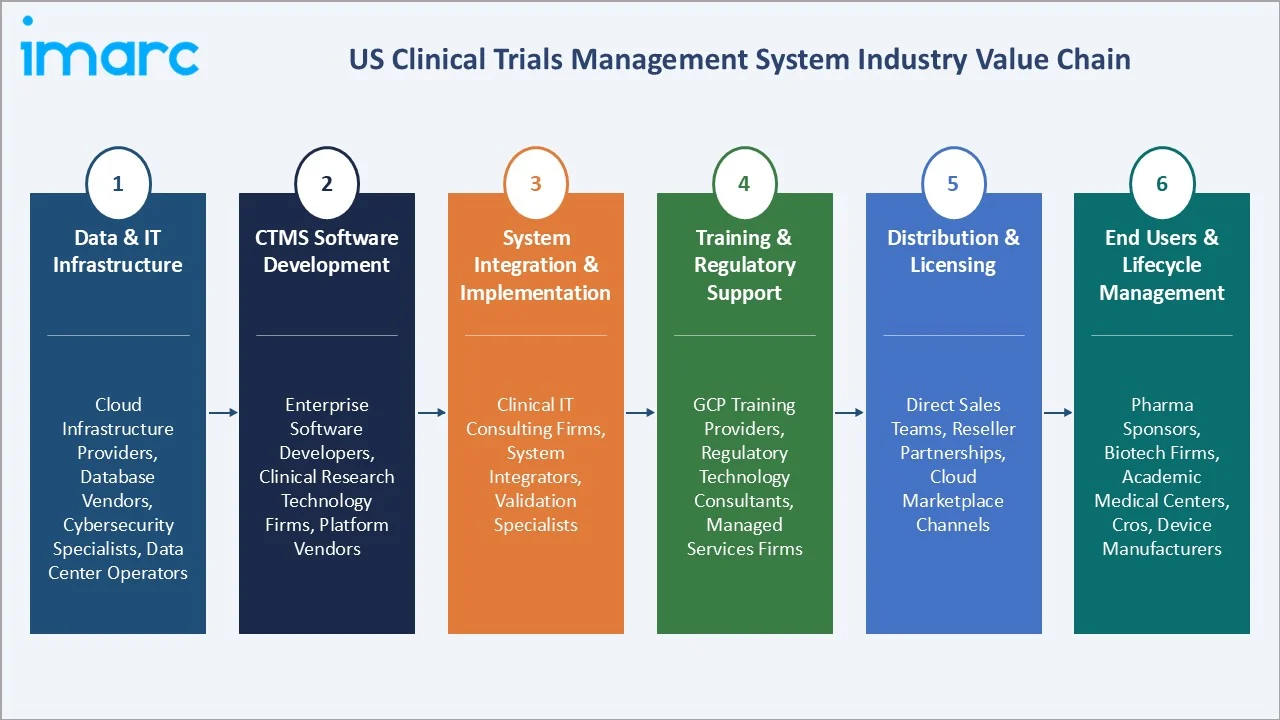

Industry Value Chain Analysis

The US clinical trials management system market value chain spans six stages from data and IT infrastructure supply through end-user engagement and lifecycle management. Software development, system implementation, and compliance services capture the highest value-add, while interoperability and post-deployment support capabilities increasingly determine sustainable competitive position in this regulated technology segment.

|

Stage |

Key Players / Examples |

|

Data & IT Infrastructure |

Cloud infrastructure providers, database management vendors, cybersecurity specialists, and data center operators enabling compliant clinical trials management system hosting environments |

|

Clinical Trials Management System Software Development |

Enterprise software developers, specialized clinical research technology firms, and platform vendors building core clinical trials management system functionality across protocol, site, and financial management modules |

|

System Integration & Implementation |

Clinical IT consulting firms, system integrators, and validation specialists managing clinical trials management system deployment, computer system validation, and integration with EDC and regulatory document management systems |

|

Training & Regulatory Support |

GCP training providers, regulatory technology consultants, and managed services firms supporting user onboarding |

|

Distribution & Licensing |

Direct sales teams, reseller partnerships, and cloud marketplace channels delivering software licenses, SaaS subscriptions, and managed service agreements to sponsors and CROs |

|

End Users & Lifecycle Management |

Pharmaceutical sponsors, biotech firms, academic medical centers, CROs, site management organizations, and device manufacturers operating clinical trials management system platforms throughout the clinical trial lifecycle |

Vertically integrated vendors that own proprietary trial management software stacks, AI-powered protocol optimization and enrollment analytics engines, and direct relationships with pharmaceutical sponsors and investigative sites are positioned to capture greater value than those reliant on third-party electronic data capture platforms, outsourced regulatory document infrastructure, or indirect channel distribution models.

Technology Landscape in the US Clinical Trials Management System Industry

Cloud and SaaS Platform Architecture

Modern clinical trial management platforms are increasingly built on multi-tenant cloud architectures, providing scalable, secure, and high-availability environments for managing clinical research operations. Containerization, microservices design, and continuous integration pipelines enable rapid feature deployment and regulatory patch management, supporting sponsor demands for frequent compliance updates without operational disruption.

AI and ML

AI and ML models are integrated into leading clinical trials management system platforms for site feasibility scoring, patient enrollment prediction, protocol deviation early detection, and automated safety reporting assistance. Natural language processing capabilities are being deployed to automate protocol synopsis extraction, regulatory document classification, and adverse event narrative drafting, materially reducing manual workload across study startup and ongoing monitoring activities.

Interoperability and Electronic Health Record Integration

Growing adoption of standardized data exchange frameworks is enabling seamless integration between clinical trial management platforms and electronic health record systems. This supports more efficient patient recruitment, real-world data collection, and streamlined clinical research workflows.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Software |

69.7% |

2025 |

|

Deployment Mode |

Cloud-based CTMS |

44.8% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Northeast |

32.1% |

2025 |

By Component

Software commands a 69.7% majority share in 2025, driven by the breadth and depth of functionality required across protocol management, site management, patient enrollment tracking, regulatory document management, adverse event reporting, and financial reconciliation workflows.

To access detailed market analysis, Request Sample

Services at 30.3% in 2025 encompasses implementation consulting, computer system validation, user training, data migration, ongoing technical support, and managed services engagements.

By Deployment Mode

Cloud-based CTMS dominates with 44.8% share in 2025, reflecting sponsor preference for scalable, subscription-based platforms that reduce upfront capital expenditure, enable real-time global team access, and provide native support for remote monitoring and decentralized trial workflows.

Web-based CTMS at 36.5% serves the substantial mid-market of sponsors and academic research centers that require browser-accessible trial management without committing to full cloud migration.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Northeast |

32.1% |

High concentration of academic medical centers, pharmaceutical headquarters, and CRO hubs; strong regulatory expertise; dense biopharma ecosystem |

|

West |

27.8% |

Rapidly expanding biotech cluster in San Francisco Bay Area and San Diego; high venture capital investment; growing cell and gene therapy trial activity |

|

South |

24.5% |

Expanding clinical research infrastructure in Texas and Florida; growing number of investigator-initiated and sponsor-funded trial sites; rising patient diversity |

|

Midwest |

15.6% |

Strong academic research hospital network; established medical device and pharmaceutical manufacturing presence; growing CRO operations in the Chicago metro area |

Northeast at 32.1% in 2025 leads the regional landscape, anchored by Boston, New York City, and Philadelphia. Dense regulatory talent and a mature CRO ecosystem sustain leadership across both software and services segments.

West at 27.8% is the second largest region. San Francisco Bay Area and San Diego biotech clusters, supported by a high concentration of venture capital investment in life sciences, are generating a rapidly expanding pipeline of Phase I and Phase II oncology, immunology, and gene therapy trials that require sophisticated clinical trials management system capabilities.

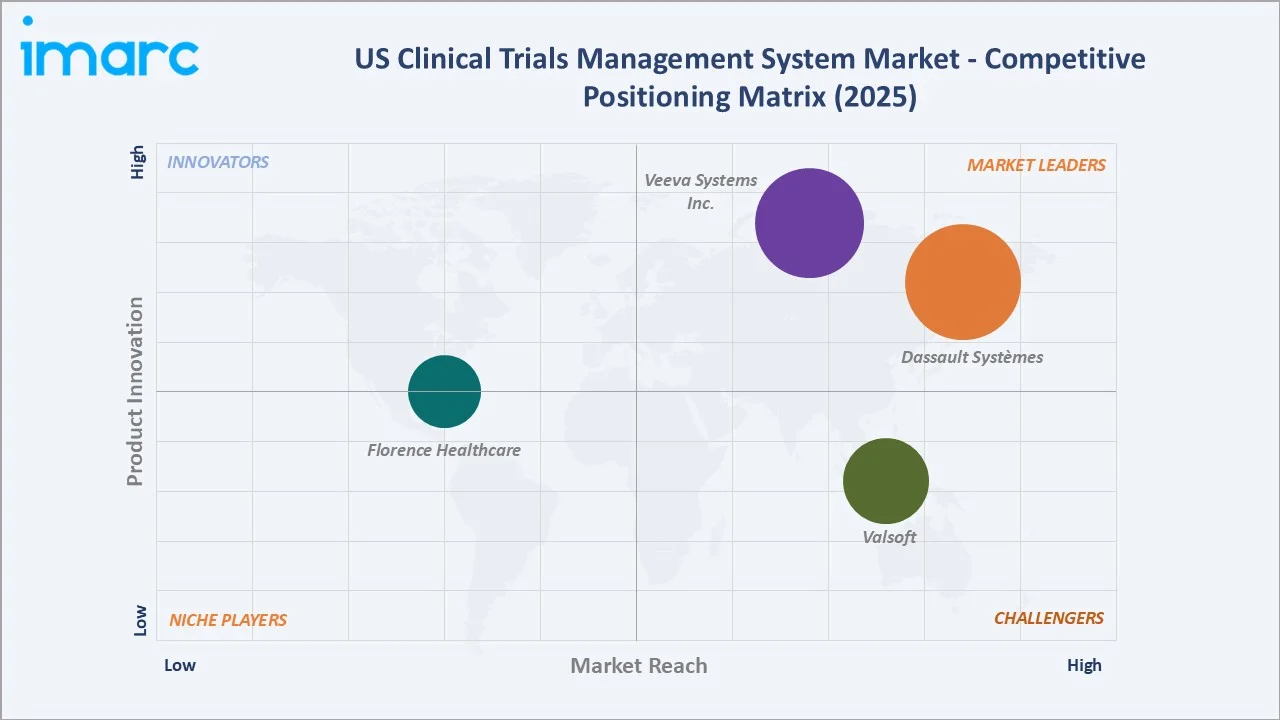

Competitive Landscape

The US clinical trials management system market is moderately concentrated, with established enterprise software vendors leading on product breadth and regulatory compliance depth while emerging point solution providers compete on usability, niche workflow support, and integration flexibility.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Dassault Systèmes |

Medidata Rave CTMS |

Leader |

End-to-end clinical data and trial management platform |

|

Veeva Systems Inc. |

Veeva CTMS |

Leader |

Cloud-native unified clinical operations platform |

|

Valsoft |

Anju Software |

Challenger |

Site-level and sponsor clinical trials management system for mid-market sponsors |

|

Florence Healthcare |

Florence eBinders |

Emerging |

Regulatory binder and site document management integration |

Key players include Dassault Systèmes, Veeva Systems Inc., Valsoft, and Florence Healthcare, among others.

Key Company Profiles

Dassault Systèmes

Dassault Systèmes is a France-based multinational software company. Through Medidata, Dassault Systèmes serves the global life sciences industry with an integrated cloud platform spanning clinical trial management, electronic data capture, patient engagement, and real-world evidence analytics.

- Product Portfolio: Medidata Rave CTMS, providing end-to-end trial management covering study startup, site and patient management, financial tracking, and regulatory document management.

- Recent Developments: The firm has been expanding its clinical research platform with enhanced digital and AI-enabled capabilities to improve trial planning, execution, and data management.

- Strategic Focus: Delivering a fully unified clinical data and operations platform that reduces technology fragmentation for large pharmaceutical sponsors and supports end-to-end trial execution from study design through regulatory submission.

Veeva Systems Inc.

Veeva Systems Inc. is a publicly listed cloud computing company specializing in life sciences software applications. The company offers an integrated suite of clinical, regulatory, quality, and commercial cloud solutions, serving pharmaceutical, biotech, and medical device organizations globally.

- Product Portfolio: Veeva CTMS providing end-to-end study and site management, financial tracking, patient enrollment monitoring, milestone management, and issue resolution.

- Recent Developments: Veeva Systems Inc. has been expanding its clinical operations capabilities, with ongoing enhancements to monitoring workflows, CRO collaboration tools, and decentralized trial support functionalities.

- Strategic Focus: Building an industry-leading cloud-native clinical suite by unifying trial management, document management, and clinical data within a single platform to create a single source of truth across clinical operations.

Florence Healthcare

Florence Healthcare is an independent clinical research technology company focused on enabling research sites and connecting them with sponsors and contract research organizations. The company provides a site enablement platform that digitizes regulatory document management, automates clinical trial workflows, and facilitates real-time collaboration across the clinical trial ecosystem.

- Product Portfolio: Florence eBinders providing digital regulatory binder management, electronic investigator site file capabilities, remote source document access, and sponsor-site document exchange.

- Recent Developments: Florence Healthcare has been broadening its site network and deepening integrations with clinical trial management, while growing its connectivity capabilities to support an increasing number of sponsors and sites operating across decentralized and hybrid trial models.

- Strategic Focus: Improving investigational site operational efficiency and sponsor-site document exchange to accelerate study startup, reduce inspection risk, and support research sites across all phases of clinical trial management.

Market Concentration Analysis

The US clinical trials management system market is moderately concentrated, with the top two vendors (Dassault Systèmes and Veeva Systems Inc.) collectively accounting for a significant share of total market revenue through their enterprise clinical trials management system deployments across major pharmaceutical sponsors and CROs.

Barriers to entry in the enterprise clinical trial management system market are high due to strict regulatory compliance requirements, complex system validation, and the need for seamless integration with other clinical technologies. These factors favor established vendors with strong compliance capabilities and mature integration ecosystems.

Consolidation is accelerating as larger technology vendors acquire specialized clinical trials management system and clinical research software firms to expand functional breadth and integration depth. Strategic acquisitions illustrate the trend toward platform aggregation reshaping competitive dynamics. Smaller vendors are increasingly differentiated through deep vertical specialization rather than competing directly with enterprise platform leaders on breadth.

Investment & Growth Opportunities

Fastest-Growing Segments

Cloud-based CTMS expands fastest among deployment modes, driven by SaaS economics, faster deployment timelines, and native support for decentralized trial monitoring. Software continues to capture the largest and fastest-growing revenue pool, supported by expanding platform functionality, compliance update subscription requirements, and increasing module adoption beyond core clinical trials management system capabilities.

Emerging Markets

West is the fastest-growing region, anchored by rapid biotech cluster expansion in San Francisco Bay Area and San Diego, high venture capital investment in cell and gene therapy, and a growing pipeline of investigator-initiated and sponsor-funded Phase I and Phase II trials. These markets represent significant growth opportunity for clinical trials management system vendors with configurable platforms suited to early-phase and adaptive trial designs.

Venture & Investment Trends

Investment is concentrated in AI-enabled clinical trials management system platform development and decentralized trial technology integration. Capital is also flowing into site-facing clinical trials management system tools that improve site efficiency, reduce startup timelines, and support investigator-initiated trial management. Strategic mergers and acquisitions are expected to continue reshaping the competitive landscape as large enterprise software vendors acquire clinical research technology specialists.

Future Market Outlook (2026-2034)

The US clinical trials management system market is forecast to expand from USD 339.1 Million in 2025 to USD 746.1 Million by 2034 at a CAGR of 8.83%, adding approximately USD 407 Million in incremental market value over the forecast period.

Four key trends are expected to shape the market through 2034: wider adoption of cloud-native and AI-enabled clinical trial management platforms, growing use of decentralized and hybrid trial models, increasing interoperability with electronic health record systems, and rising outsourcing of clinical operations to contract research organizations requiring scalable, multi-sponsor platforms.

By 2034, clinical trials management system platforms in the US are expected to be defined by highly automated study startup workflows, predictive enrollment analytics, seamless decentralized trial support, and real-time centralized monitoring capabilities. Regulatory evolution at the FDA, including ongoing guidance development for decentralized clinical trials and real-world evidence integration, will continue to drive demand for platform upgrades and new module adoption across the commercial and academic trial management ecosystem.

Research Methodology

Primary Research

Primary research included structured interviews with clinical operations executives, clinical trials management system platform administrators, CRO technology leaders, pharmaceutical clinical technology directors, and academic research center administrators, validating market sizing, deployment mode evolution, regional demand patterns, and competitive positioning.

Secondary Research

Secondary sources included FDA Clinical Trials Guidance documents, annual reports and investor presentations from publicly listed clinical trials management system vendors, industry associations including the Association of Clinical Research Professionals and the Society of Clinical Research Associates, and technology analyst reports covering clinical research software markets.

Forecasting Models

Market forecasts used top-down and bottom-up models combining registered active clinical trial volumes, clinical trials management system adoption rates by sponsor type, average revenue per site and per study, deployment mode transition rates, and macroeconomic variables influencing pharmaceutical R&D investment. Scenario analysis addressed FDA regulatory pace, AI integration timelines, and CRO outsourcing trajectory assumptions.

US Clinical Trials Management System Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Software, Services |

| Deployment Modes Covered | Web-based CTMS, On-premises, Cloud-based CTMS |

| End Users Covered | Pharmaceutical and Biotechnology Firms, Contract Research Organizations, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Dassault Systèmes, Veeva Systems Inc., Valsoft, Florence Healthcare, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the US clinical trials management system market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the US clinical trials management system market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the US clinical trials management system industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the US Clinical Trials Management System Market Report

The US clinical trials management system market was valued at USD 339.1 Million in 2025, driven by expanding pharmaceutical trial pipelines, rising compliance requirements, and accelerating cloud-native platform adoption across sponsors and CROs.

The market is projected to grow at a CAGR of 8.83% from 2026 to 2034, reaching USD 746.1 Million, supported by cloud adoption, AI integration, and growing demand for decentralized trial management capabilities.

Software leads with a 69.7% share in 2025, driven by broad functionality requirements across the trial lifecycle and recurring SaaS licensing models that support continuous compliance updates.

Cloud-based CTMS leads at 44.8% in 2025, supported by lower total cost of ownership, faster deployment, and native decentralized trial support.

Northeast commands 32.1% in 2025, led by the highest concentration of academic medical centers, pharmaceutical headquarters, and CRO operations along the Boston-New York-Philadelphia corridor.

Leading players include Dassault Systèmes, Veeva Systems Inc., Valsoft, and Florence Healthcare, among others.

Decentralized clinical trial adoption is expanding clinical trials management system functionality requirements to include remote visit management, patient engagement integration, wearable data ingestion, and home nursing coordination, creating new module demand and upgrade cycles.

AI and ML are being integrated for site feasibility scoring, enrollment prediction, protocol deviation early warning, and safety narrative automation, materially reducing manual workload and improving trial execution efficiency.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)