US Coffee Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

US Coffee Market Size, Share, Trends & Forecast (2026-2034)

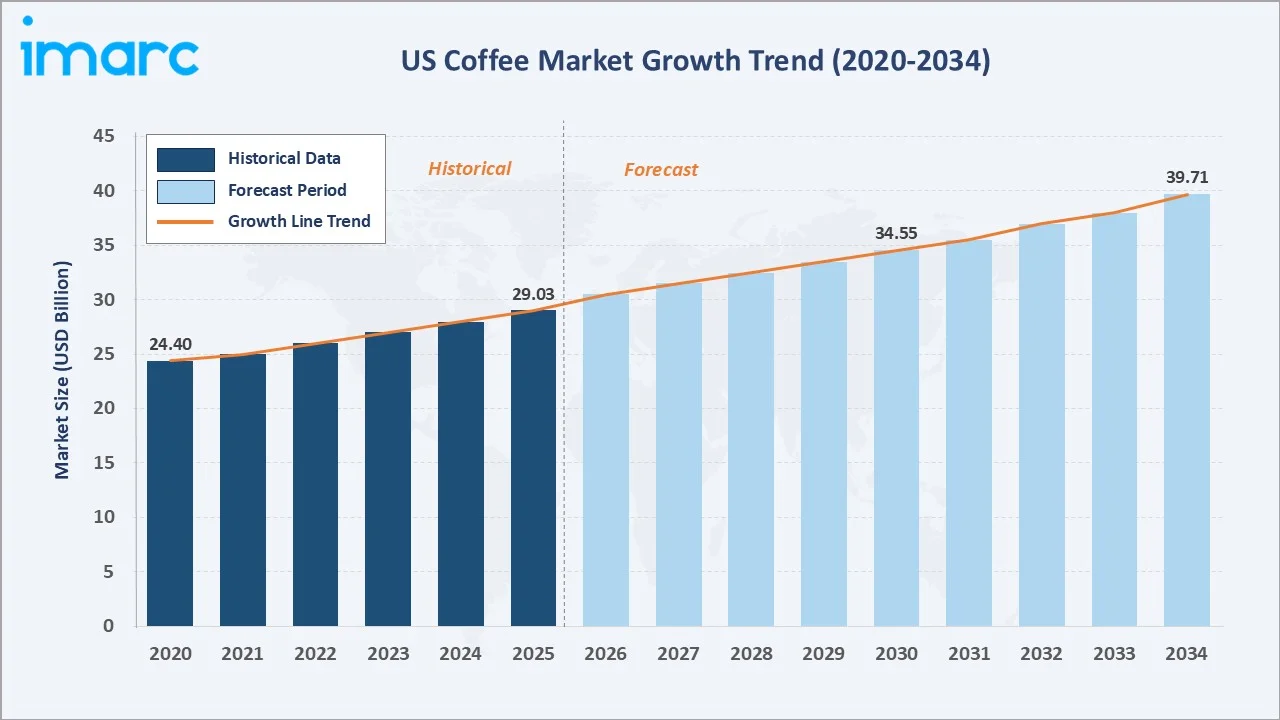

The US coffee market reached USD 29.03 Billion in 2025 and is projected to reach USD 39.71 Billion by 2034, growing at a CAGR of 3.54% during 2026-2034. Approximately 66% of adults in the United States consume coffee daily, while over 70% report drinking it at least once a week. Annual consumer spending on coffee in the U.S. exceeds $100 billion, reflecting its widespread popularity and strong market demand. Ground coffee leads at 38.4% product type share. Supermarkets and hypermarkets dominate distribution at 44.2%. The South region commands 31.6% of market revenues. High daily consumption rates, premiumization through coffee pods and specialty whole-bean, and online retail expansion anchor the market's steady growth trajectory.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 29.03 Billion |

|

Forecast Market Size (2034) |

USD 39.71 Billion |

|

CAGR (2026-2034) |

3.54% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Product Type |

Ground Coffee (38.4%, 2025) |

|

Leading Distribution Channel |

Supermarkets/Hypermarkets (44.2%, 2025) |

|

Dominant Region |

South Region (31.6%, 2025) |

The market grew from USD 24.40 Billion in 2020 to USD 29.03 Billion in 2025, anchored at USD 34.55 Billion in 2030, and is forecast to reach USD 39.71 Billion by 2034. The COVID-19 pandemic created a structural at-home coffee consumption surge, permanently increasing household coffee equipment investment and retail coffee purchasing that persists post-pandemic as a behavioral baseline.

To get more information on this market, Request Sample

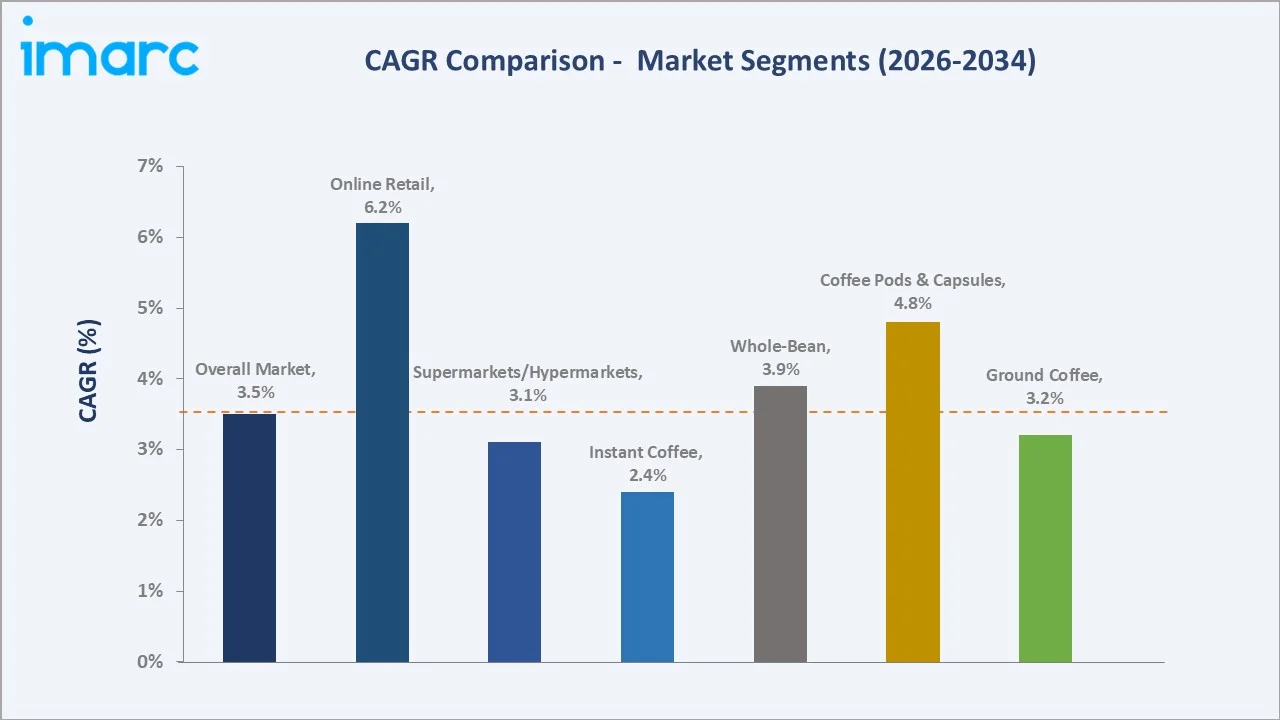

Online retail grows fastest at ~6.2% CAGR (2026-2034), driven by DTC subscription services, Amazon's expanding grocery, fresh coffee delivery, and brand websites offering subscription-based, freshly-roasted delivery. Coffee pods and capsules grow at ~4.8% CAGR, the fastest product type.

Executive Summary

The US coffee market reached USD 29.03 Billion in 2025, making it the world's largest national coffee market by value. The National Coffee Association's report found that 66% of American adults drink coffee daily, the highest daily consumption rate in the beverage category. This structural consumption foundation, combined with premiumization trends shifting consumers from commodity to specialty, creates a reliably growing market with strong brand loyalty dynamics. The market is projected to reach USD 39.71 Billion by 2034 at a 3.54% CAGR, reflecting the compounding of premiumization, RTD cold brew category expansion, functional coffee ingredient innovation, and e-commerce channel growth.

Ground coffee commands 38.4% market share (2025), anchored by the nation's highest-volume household brands. Supermarkets and hypermarkets at 44.2% remain the primary purchase channel. The South region at 31.6% leads with the largest consumer population base, while the West at 27.4% maintains the highest per-capita specialty coffee spending.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Ground Coffee - 38.4% share (2025) |

|

Leading Distribution Channel |

Supermarkets/Hypermarkets - 44.2% share (2025) |

|

Dominant Region |

South - 31.6% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Ground Coffee at 38.4% (2025): Ground coffee leads the market due to its affordability and easy availability across retail channels. Strong consumer preference for convenient, at-home brewing further supports its dominant position.

- Supermarkets/Hypermarkets at 44.2%: Supermarkets and hypermarkets lead the market due to their wide product assortment, competitive pricing, and strong private label presence. High consumer footfall and one-stop shopping convenience drive consistent sales across ground, instant, and specialty coffee segments.

- South region at 31.6% driven by Texas and Florida's large consumer populations: Texas is the second-largest state coffee market after California, with supermarkets being the primary coffee distribution channel and Starbucks' Texas stores representing one of the most concentrated US state markets.

US Coffee Market Overview

The US coffee market encompasses all retail and foodservice coffee products consumed domestically, ground coffee, whole-bean, instant coffee, coffee pods and capsules, and ready-to-drink (RTD) coffee, sold through retail, foodservice, office coffee service, and direct-to-consumer channels. The US is the world's largest coffee importer. In 2023, roughly 80% of U.S. unroasted coffee imports originated from Latin America, totaling about $4.8 billion, with Brazil contributing 35% and Colombia accounting for 27% of the supply.

The market ecosystem integrates global green coffee commodity traders, multinational roasters, specialty independent roasters, national distributors, and retail channels spanning supermarkets, convenience stores, and online retail. Macroeconomic drivers include US adult daily consumption, rising disposable income supporting premiumization, e-commerce normalization accelerating DTC subscription growth, and the functional beverage trend expanding coffee into health-positioned formats.

Market Dynamics

To evaluate market opportunities, Request Sample

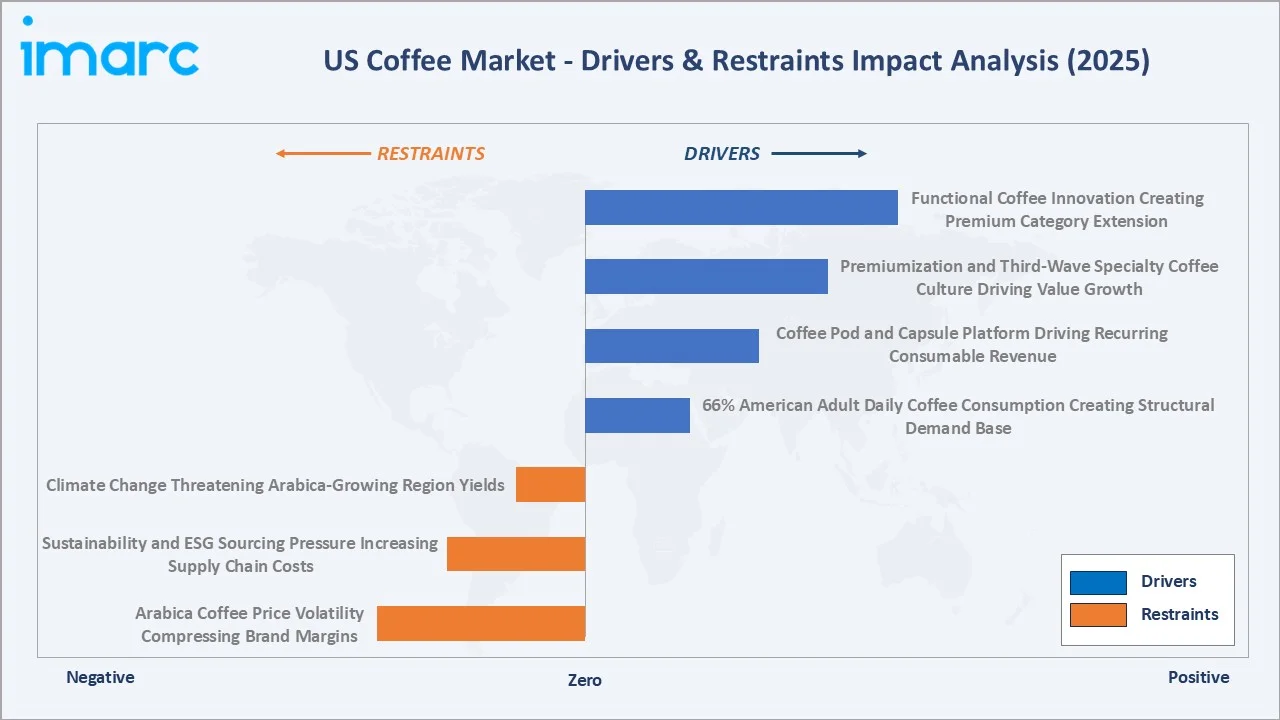

Market Drivers

- 66% American Adult Daily Coffee Consumption Creating Structural Demand Base: The NCA's survey found that 66% of American adults drink coffee daily. Coffee is the most widely consumed daily beverage among US adults, surpassing tap water and bottled water in daily consumption frequency. This structural consumption habit creates reliable market volume that is largely recession-resistant, as consumers maintain coffee consumption even during economic contractions.

- Coffee Pod and Capsule Platform Driving Recurring Consumable Revenue: In March 2024, Keurig Dr Pepper outlined an innovation roadmap focused on evolving coffee consumer preferences, emphasizing product variety, quality, value, and sustainability. The company’s near-term strategy highlights advancements in Keurig brewers and K-Cup pod offerings, aligning with its next-generation single-serve coffee system developments. The convenience and variety of single-serve systems align with US consumers' individualized beverage preferences, enabling different household members to brew different varieties without waste.

- Premiumization and Third-Wave Specialty Coffee Culture Driving Value Growth: The US specialty coffee market has grown, with premium whole-bean and single-origin ground coffee. Millennials and Gen-Z consumers demonstrate 2-3x higher price-per-cup tolerance for specialty coffee versus commodity brands, driving average revenue per unit upward across the ground and whole-bean segments.

Market Restraints

- Arabica Coffee Price Volatility Compressing Brand Margins: Arabica coffee bean futures surged 70%+ in 2024, driven by Brazilian drought conditions reducing the world's largest arabica origin's crop output. This commodity price shock compelled major branded manufacturers to implement 20-30% retail price increases in 2024, while partially protecting margin, which accelerated private label trade-down among budget-sensitive consumers and reduced volume growth.

- Sustainability and ESG Sourcing Pressure Increasing Supply Chain Costs: US consumers' increasing scrutiny of sustainability certifications is forcing major brands to invest in supply chain transparency, farmer income programs, and deforestation-free sourcing.

Market Opportunities

- Functional Coffee Innovation Creating Premium Category Extension: The functional beverage market's expansion into coffee formats is creating a premium coffee subcategory. These products command high serving prices versus traditional ground coffee, with distribution expanding from specialty and natural food channels into mainstream grocery.

- Cold Brew RTD Market Capturing Younger Consumer Demographics: The US ready-to-drink coffee market is growing, with cold brew as the fastest-growing subcategory. Cold brew's smoother taste profile appeals to Gen-Z consumers who prefer less acidic coffee, while its premium price point drives disproportionate revenue per unit.

Market Challenges

- Climate Change Threatening Arabica-Growing Region Yields: Climate scientists project that 50%+ of current arabica-suitable growing regions in Brazil, Colombia, and Central America will become unsuitable further due to rising temperatures and altered rainfall patterns.

- Foodservice Coffee Competition from Specialty Cafes Pressuring At-Home Premium Brands: The US specialty cafe sector provides consumers with convenient, away-from-home premium coffee access. As specialty cafe quality has improved and accessibility expanded, particularly in suburban areas and airports, the at-home premium coffee market must continuously justify price premiums through superior freshness, variety, and convenience against well-established away-from-home alternatives.

Emerging Market Trends

1. Coffee Pods and Capsules Gaining Ground on Traditional Ground Coffee

Coffee pods and capsules at 27.6% (2025) are growing fastest among product types at ~4.8% CAGR, driven by the US household installed base and boutique expansion. Coffee pods and capsules are gaining traction in the market due to their convenience, portion control, and compatibility with single-serve brewing systems. Rising demand for premium flavors and quick preparation is driving consumers to shift from traditional ground coffee to pod-based formats.

2. Direct-to-Consumer Subscriptions Redefining Coffee Retail Economics

Direct-to-consumer subscription models are reshaping coffee retail by enabling brands to build recurring revenue streams and stronger customer relationships. Personalized offerings, convenience, and cost efficiencies are helping companies bypass traditional retail channels and improve margins.

3. Functional and Adaptogenic Coffee Creating a New Market Tier

Functional coffee brands combining traditional coffee with adaptogens, nootropics, and protein are creating a new premium subcategory capturing health-conscious millennial and Gen-Z consumers. Ingredients like mushrooms, herbs, and botanicals are attracting wellness-focused consumers seeking more than just energy from their beverages. This shift is encouraging premiumization and product innovation across the coffee category.

4. RTD Cold Brew Expanding Coffee's Occasion Footprint

The RTD cold brew segment is redefining when and how Americans consume coffee, creating afternoon, evening, and exercise-adjacent consumption occasions previously not served by hot coffee. Ready-to-drink (RTD) cold brew is expanding coffee’s consumption occasions by offering convenient, on-the-go formats suited for busy lifestyles. Its smooth taste and premium positioning are appealing to younger consumers, encouraging coffee consumption beyond traditional morning routines. Wider availability across retail and convenience channels is further supporting its growth.

Industry Value Chain Analysis

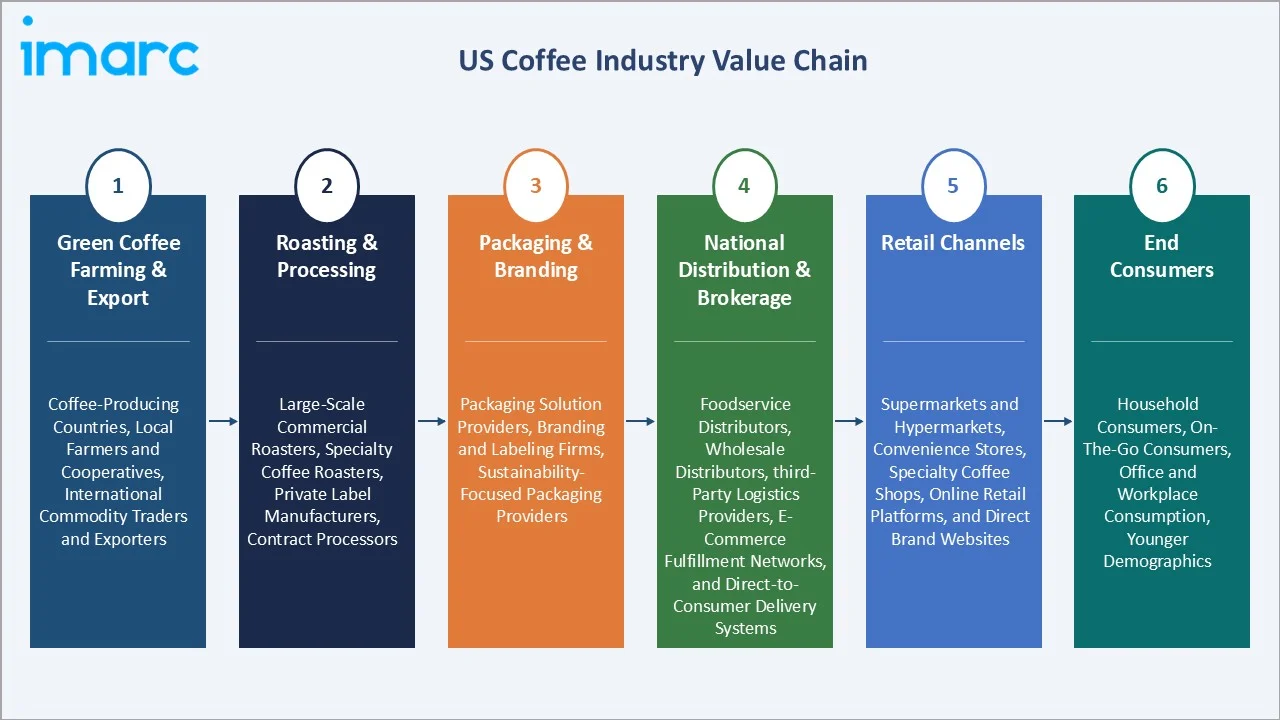

The US coffee market value chain spans green coffee origin farming across producing countries through roasting, packaging, national distribution, and retail dispensing to daily US consumers. The value chain is characterized by a commodity-to-premium bifurcation; commodity channel operators compete on price and volume, while premium operators compete on quality, sustainability narrative, and DTC channel economics.

|

Stage |

Key Participants |

|

Green Coffee Farming & Export |

Coffee-producing countries, local farmers and cooperatives, international commodity traders and exporters |

|

Roasting & Processing |

Large-scale commercial roasters, specialty coffee roasters, private label manufacturers, and contract processing companies |

|

Packaging & Branding |

Packaging solution providers (flexible packaging, pods/capsules, cans, bottles), branding and labeling firms, and sustainability-focused packaging providers |

|

National Distribution & Brokerage |

Foodservice distributors, wholesale distributors, third-party logistics providers, e-commerce fulfillment networks, and direct-to-consumer delivery systems |

|

Retail Channels |

Supermarkets and hypermarkets, convenience stores, specialty coffee shops, online retail platforms, and direct brand websites |

|

End Consumers |

Household consumers, on-the-go consumers, office and workplace consumption, and younger demographics are driving specialty and premium coffee demand |

Roasters capture the highest value-added margins, and premium specialty roasters earn 50-70% gross margins on finished packaged coffee versus raw green coffee costs. National distributors earn 8-15% margins on natural and specialty coffee distribution. Mass grocery retailers earn 25-35% retail markup on branded coffee, with private label providing 40-50% margins that incentivize shelf-space allocation decisions favoring private label growth.

Technology Landscape in the US Coffee Industry

Single-Serve Pod and Capsule Brewing Technology

Single-serve pod and capsule brewing technology is reshaping the coffee industry by enabling quick, consistent, and mess-free preparation. In September 2021, Bruvi, a single-serve coffee machine company, secured $7 million in new funding, increasing its total capital raised to $10.8 million. It is driving product innovation, premiumization, and ecosystem-based consumption through machine pod compatibility and diverse flavor offerings.

Cold Brew Processing and RTD Technology

Cold brew coffee production, steeping coarsely-ground coffee in cold or room-temperature water for 12-24 hours before filtration, requires significant production infrastructure for commercial scale. Cold brew processing and RTD technology enabling scalable production of smooth, shelf-stable beverages with extended freshness. Advanced extraction, filtration, and packaging innovations are supporting product diversification and expanding ready-to-drink coffee offerings across retail channels.

Sustainable Sourcing and Traceability Technology

Blockchain-based coffee traceability platforms enable US roasters to provide consumers with immutable farm-to-cup supply chain data accessible via QR code on packaging. These technologies enable premium brands to substantiate sustainability claims with verifiable data, supporting the price premiums that drive value growth above volume growth.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Ground Coffee |

38.4% |

2025 |

|

Distribution Channel |

Supermarkets/Hypermarkets |

44.2% |

2025 |

|

Region |

South |

31.6% |

2025 |

By Product Type

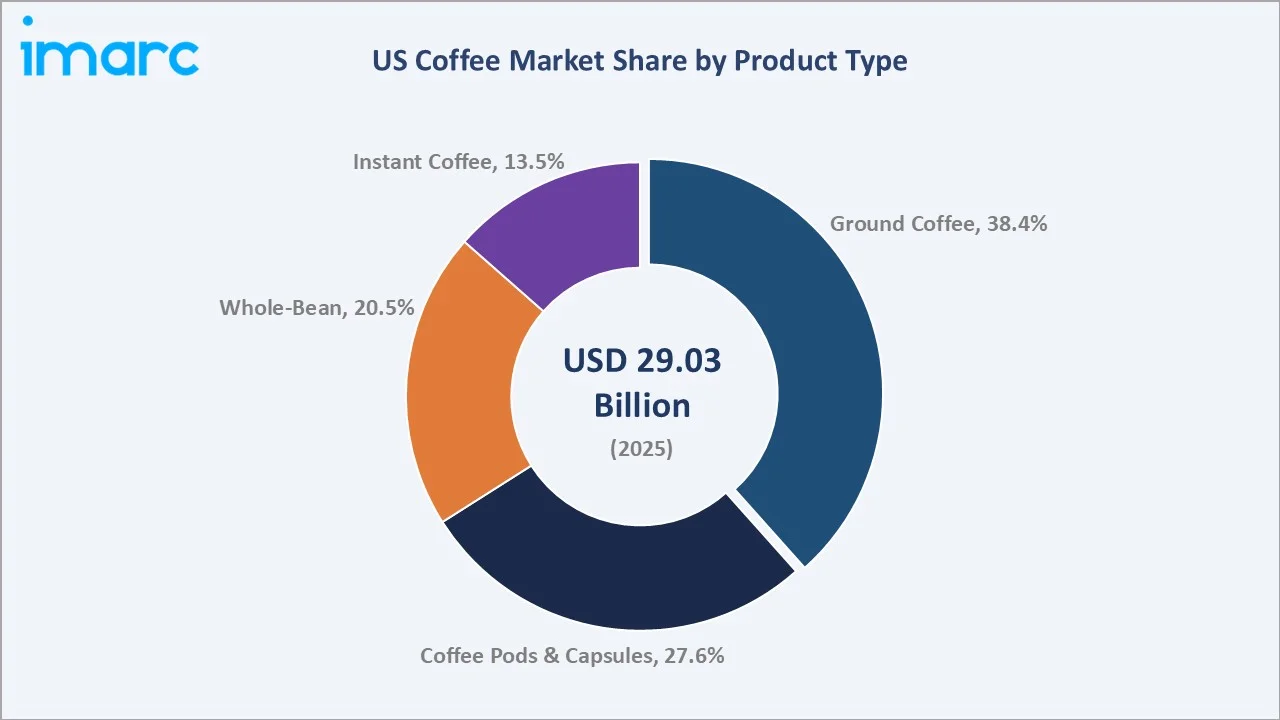

Ground coffee leads at 38.4% market share (2025). This segment encompasses commodity ground coffee and premium ground coffee. Ground coffee grows at ~3.2% CAGR (2026-2034), driven by premium brand premiumization, offsetting volume share losses to pods and capsules.

To access detailed market analysis, Request Sample

Coffee pods and capsules at 27.6% grow fastest at ~4.8% CAGR, anchored by machine installed base creating durable recurring demand. Whole-bean at 20.5% targets specialty and premium consumers growing at ~3.9% CAGR. Instant coffee at 13.5% is the slowest-growing segment at ~2.4% CAGR, serving value-conscious and convenience-oriented consumers with Nescafe and Starbucks as dominant brands.

By Distribution Channel

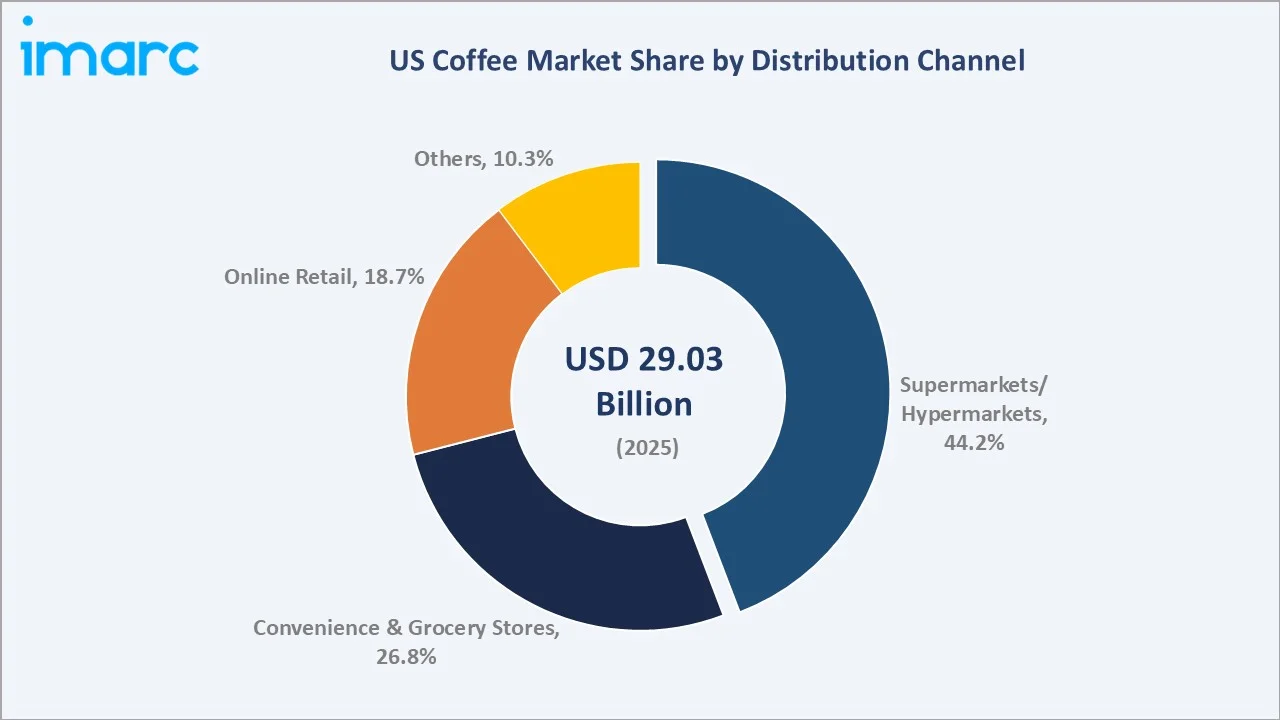

Supermarkets and hypermarkets lead at 44.2% market share (2025). High foot traffic and one-stop shopping convenience ensure consistent demand across ground, instant, and ready-to-drink coffee segments. Supermarket coffee category management has become increasingly sophisticated, with digital shelf-price optimization, personalized loyalty card purchase data, and growing private label investment, making the channel both the dominant and most competitive sales environment.

Convenience and grocery stores at 26.8% capture impulse and proximity purchases, with RTD coffee representing the fastest-growing convenience store SKU category at 15%+ CAGR. Online retail at 18.7% grows fastest at ~6.2% CAGR through Amazon, brand DTC subscription websites, and specialty e-commerce platforms. Others at 10.3% includes office coffee service, foodservice, and direct institutional supply channels.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

South |

31.6% |

Largest coffee-consuming population base, strong preference for at-home and on-the-go consumption, expanding retail and foodservice presence, and growing demand for affordable and convenient coffee formats |

|

West |

27.4% |

High adoption of specialty and premium coffee, strong café culture and innovation in cold brew and RTD segments, and health-conscious consumers driving organic and sustainable coffee demand |

|

Northeast |

22.3% |

High urban density supporting frequent coffee consumption, strong presence of premium coffee outlets, and high per capita spending on specialty coffee and subscription-based purchases |

|

Midwest |

18.7% |

Strong traditional coffee consumption habits, high demand for ground coffee and value-oriented products, and growing adoption of single-serve machines and pod-based formats in households |

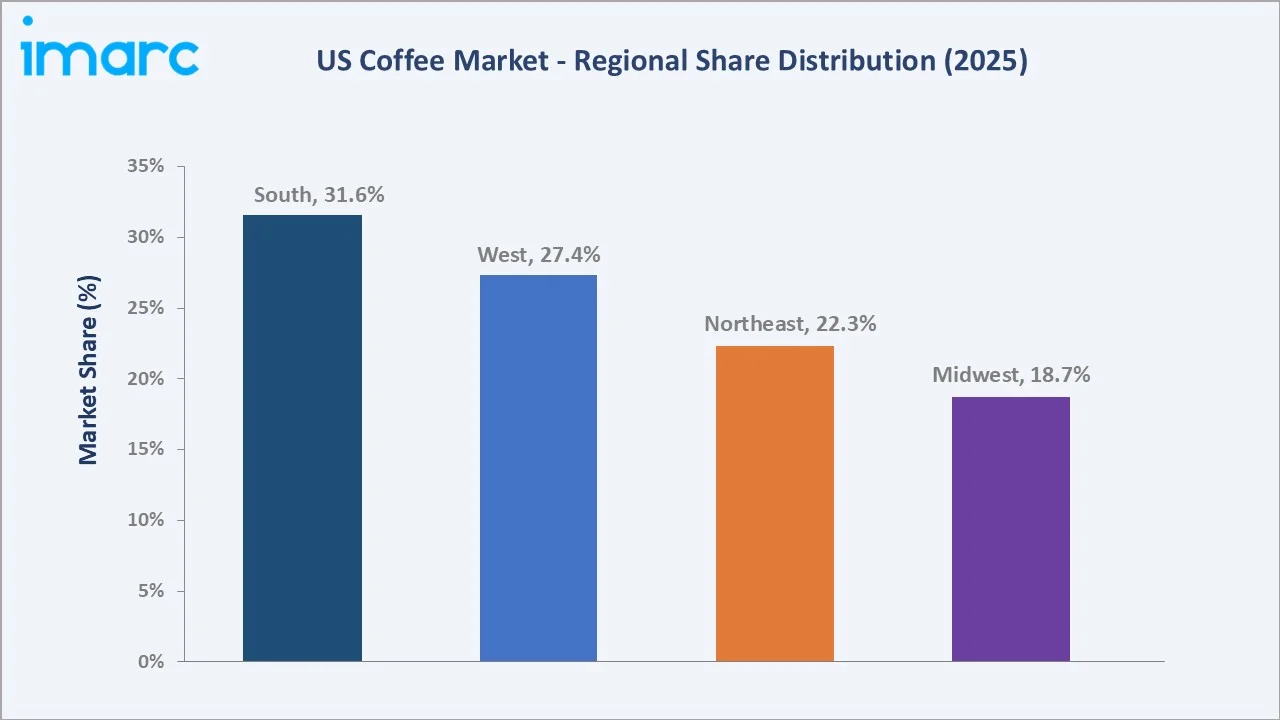

The South's 31.6% share reflects the combined population weight of Texas, Florida, and Georgia, three of the US's five largest states by population. Texas's supermarkets dominate coffee retail in the state, with store-brand and premium private-label coffee among the fastest-growing categories. The South's growing Hispanic consumer population creates above-average market demand.

The West's 27.4% reflects California's largest single-state coffee market and the modern US third-wave coffee movement. The West has the highest per-capita specialty coffee spending in the nation.

Competitive Landscape

The US coffee market exhibits moderate concentration at the branded retail level, with the top 5 companies collectively accounting for approximately 65-70% of US retail coffee revenues. The market's competitive structure bifurcates between commodity-oriented volume leaders competing on price and distribution scale, and premium brand leaders competing on product quality, sustainability narrative, and consumer loyalty ecosystems.

|

Company Name |

Brand / Product Line |

Market Position |

Core Strength |

|

Starbucks Coffee Company |

Starbucks |

Market Leader |

Starbucks is the largest coffee chain in the US |

|

Nestlé |

NESCAFÉ Clásico, NESCAFÉ GOLD Espresso |

Market Leader |

One of the world's largest food companies, Nescafe leadership globally and in the US |

|

The J.M. Smucker Co. |

Folgers, Cafe Bustelo, Dunkin', Medaglia D'oro |

Strong Challenger |

Folgers is one of America's #1 ground coffee brands, Cafe Bustelo espresso-style brand with the fastest-growing Hispanic consumer base |

|

Keurig Dr Pepper Inc. |

Keurig, Green Mountain Coffee Roasters |

Strong Challenger |

Keurig Dr Pepper brings specialty coffee and a variety of other specialty beverages in K-Cup pods for use with Keurig brewers. |

|

Kraft Heinz, Inc. |

Maxwell House, Gevalia |

Established Player |

Maxwell House is one of America's leading ground coffee brands; Gevalia premium Swedish-style coffee with a strong grocery store presence |

Private label grocery brands represent a third competitive tier, collectively holding 18-22% of US ground coffee retail volume and growing 3-4% annually as consumers trade down during inflationary periods. The fastest-growing competitive segment is DTC specialty brands using social media and subscription e-commerce to capture premium consumers at higher margins without traditional retail infrastructure.

Key Company Profiles

Starbucks Coffee Company

Starbucks is one of the world's largest coffeehouse companies and the US retail coffee market's most valuable brand.

- Product Portfolio: Starbuck’s Hot Coffee (Brewed Coffee, Americano, Latte, Cappuccino, Mocha, Macchiato, Cortado) and Cold Coffee (Cold Brew, Nitro Cold Brew, Iced Coffee, Iced Espresso, Iced Americano, Iced Latte).

- Recent Developments: In March 2026, Starbucks introduced a new range of ready-to-drink (RTD) Coffee & Protein beverages for retail, combining its premium coffee with 22 grams of complete protein, prebiotic fiber, added vitamins and minerals, and low sugar content.

- Strategic Focus: Loyalty program deepening; packaged grocery retail expansion.

Nestlé

Nestlé is one of the world's largest food and beverage companies, and the US coffee market's one of the largest players by value.

- Product Portfolio: NESCAFÉ Clásico, NESCAFÉ GOLD Espresso.

- Recent Developments: In January 2025, NESCAFÉ expanded its U.S. portfolio with its first-ever liquid concentrate line and newest innovation: NESCAFÉ Espresso Concentrate.

- Strategic Focus: Strengthening its US coffee presence through premiumization, innovation in single-serve and RTD formats.

Market Concentration Analysis

The US coffee market is moderately concentrated at the branded retail level. The top 5 companies collectively hold approximately 65-70% of US retail packaged coffee revenues. This concentration is highest in the ground coffee segment and lowest in the whole-bean specialty segment, where thousands of independent regional roasters collectively compete with national brands. Private label brands represent a significant competitive tier, collectively capturing 18-22% of US ground coffee volume and growing 3-4% annually. The DTC specialty brands represent a fragmented but growing competitive force that has bypassed traditional retail altogether.

Investment & Growth Opportunities

Fastest Growing Segments

Online retail (~6.2% CAGR), coffee pods & capsules (~4.8% CAGR), whole-bean specialty (~3.9% CAGR), RTD cold brew (~15% CAGR within beverages), and functional/adaptogenic coffee (~20%+ CAGR from small base) represent the US coffee market's highest-growth investment vectors through 2034. DTC subscription coffee platforms, combining freshly-roasted sourcing with AI personalization and recurring revenue models, represent the highest-margin commercial structure currently underexploited in a market still dominated by grocery retail economics.

Emerging Market Opportunities

The US Gen-Z adult consumer population drinks more than any previous generation at the same age. This demographic's preference for premium, sustainable, and functionally differentiated coffee formats versus commodity grounds creates an addressable premium market expansion opportunity. Functional coffee (adaptogenic, nootropic, protein-infused) is the segment most likely to capture this cohort's incremental spending, with DTC and social-commerce channels as the primary go-to-market routes.

Investment Themes

- DTC subscription coffee platforms: The US coffee subscription market, growing at 12%+ CAGR represents a superior margin structure versus grocery retail for quality-positioned brands.

- Functional and adaptogenic coffee brand development: The mainstream grocery entry phase of these brands represents the next 3-5x revenue expansion catalyst, creating investment entry points at current DTC-only valuations before retail distribution multiplication.

- Cold brew RTD production infrastructure: US cold brew production capacity is constrained by the 12-24 hour steeping process requiring large stainless steel vessel arrays. Co-manufacturing investment in cold brew production capacity serves the RTD cold brew category growth while enabling smaller craft brands to scale without capital-intensive equipment investment.

Future Market Outlook (2026-2034)

The US coffee market is projected to grow from USD 29.03 Billion in 2025 to USD 39.71 Billion by 2034, delivering a 3.54% CAGR. The market's anchor value of USD 34.55 Billion in 2030 reflects a structurally stable, premiumizing market where volume growth is modest but value growth is driven by price-per-cup increases from category trading-up toward specialty, pods, whole-bean, and functional formats.

Three structural forces define the US coffee market's trajectory with high visibility through 2034: the generational premiumization dynamic where Millennials and Gen-Z adults progressively replace Boomer value-brand loyalists as the market's primary revenue drivers; the household installed base creating durable pod consumable revenues that grow with household formation and machine upgrade cycles; and the e-commerce and DTC subscription channel's compounding margin advantage driving brand investment toward online-first commercial models.

Research Methodology

Primary Research

Primary research comprised structured interviews with 70+ industry stakeholders, including coffee category buyers; brand managers; specialty roaster founders from the Specialty Coffee Association's US member base; DTC coffee subscription platform operators; and National Coffee Association (NCA) research personnel providing access to their 2025 National Coffee Data Trends survey data.

Secondary Research

Secondary research encompassed National Coffee Association 2025 National Coffee Data Trends Report, USDA Foreign Agricultural Service green coffee import statistics 2024, ICE arabica and robusta commodity futures data, Nielsen and IRI retail scanner data for packaged coffee (2020-2025), Specialty Coffee Association US Market Report 2024, company investor presentations and earnings calls, and retail industry trade publications. Over 110 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using bottom-up product segment x retail channel x average retail price models, calibrated against Nielsen retail scanner data for verified baseline revenue estimates. Key inputs include NCA coffee consumption trend projections, Keurig pod platform growth model (installed base x average annual pod consumption x pod price trends), online retail adoption rate curves from USDA e-commerce grocery data, regional population growth projections from the US Census Bureau through 2034, and commodity Arabica price scenarios from ICE futures market forward curves.

US Coffee Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Whole-bean, Ground Coffee, Instant Coffee, Coffee Pods and Capsules |

| Distribution Channels Covered | Supermarkets/Hypermarkets, Convenience/Grocery Stores, Online Retail, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Starbucks Coffee Company, Nestlé, The J.M. Smucker Co., Keurig Dr Pepper Inc., Kraft Heinz, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, US coffee market outlook, and dynamics of the market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the US coffee market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the US coffee industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the US Coffee Market Report

The US coffee market reached USD 29.03 Billion in 2025, driven by 66% US adult daily consumption, premiumization trends, pod platform growth, and DTC subscription e-commerce expansion across daily coffee drinkers.

The market grows at 3.54% CAGR during 2026-2034, reaching USD 39.71 Billion by 2034, driven by premiumization, pods and capsule growth, online retail DTC subscription expansion, and functional coffee category development.

Ground coffee leads at 38.4% (2025), anchored by Folgers (J.M. Smucker) and Maxwell House (Kraft Heinz) as volume leaders, plus Starbucks packaged as the premium retail leader.

Supermarkets and hypermarkets lead at 44.2% (2025), anchored by Walmart, Costco, and Kroger's store national network.

Online retail grows fastest at ~6.2% CAGR (2026-2034), driven by DTC subscription services, Amazon Subscribe & Save processing premium online coffee sales, and brand DTC websites.

The South leads at 31.6% (2025), driven by Texas and Florida's large consumer populations, supermarket coffee dominance in Texas, and the highest Starbucks store density.

Leading companies include Starbucks Coffee Company, Nestlé, The J.M. Smucker Co., Keurig Dr Pepper Inc., and Kraft Heinz, Inc., among others.

The US coffee market is projected to reach approximately USD 34.55 Billion by 2030, with pods and capsules reaching 30%+ market share, online retail surpassing convenience stores as the second-largest channel, and cold brew RTD integrated into mass convenience distribution.

DTC subscription services offer freshly-roasted specialty coffee at a lower price with 65-75% gross margins versus 30-35% retail, using AI personalization to match consumers with roasters, creating a superior brand economics model.

Functional coffee combines traditional coffee with adaptogens (mushroom, ashwagandha), nootropics, and protein, creating premium SKUs growing at 20%+ CAGR.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)