US Pharmaceutical Market Size, Share, Trends and Forecast by Prescription Type, Therapeutic Category, and Region, 2026-2034

US Pharmaceutical Market Size, Share, Trends & Forecast (2026-2034)

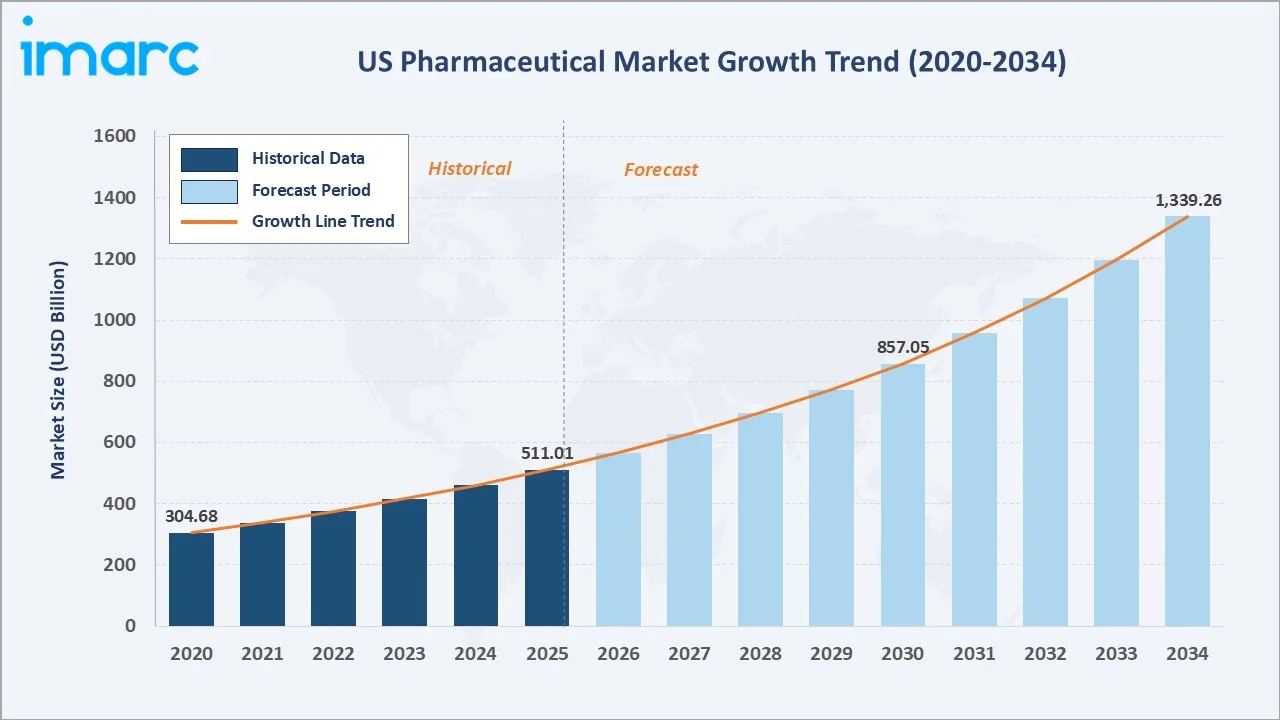

The US pharmaceutical market size was valued at USD 511.01 Billion in 2025 and is projected to reach USD 1,339.26 Billion by 2034, exhibiting a CAGR of 10.90% during the forecast period 2026-2034. An aging population, rapid digital integration across the value chain, and rising R&D investment are driving the US pharmaceutical market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 511.01 Billion |

|

Forecast Market Size (2034) |

USD 1,339.26 Billion |

|

CAGR (2026-2034) |

10.90% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

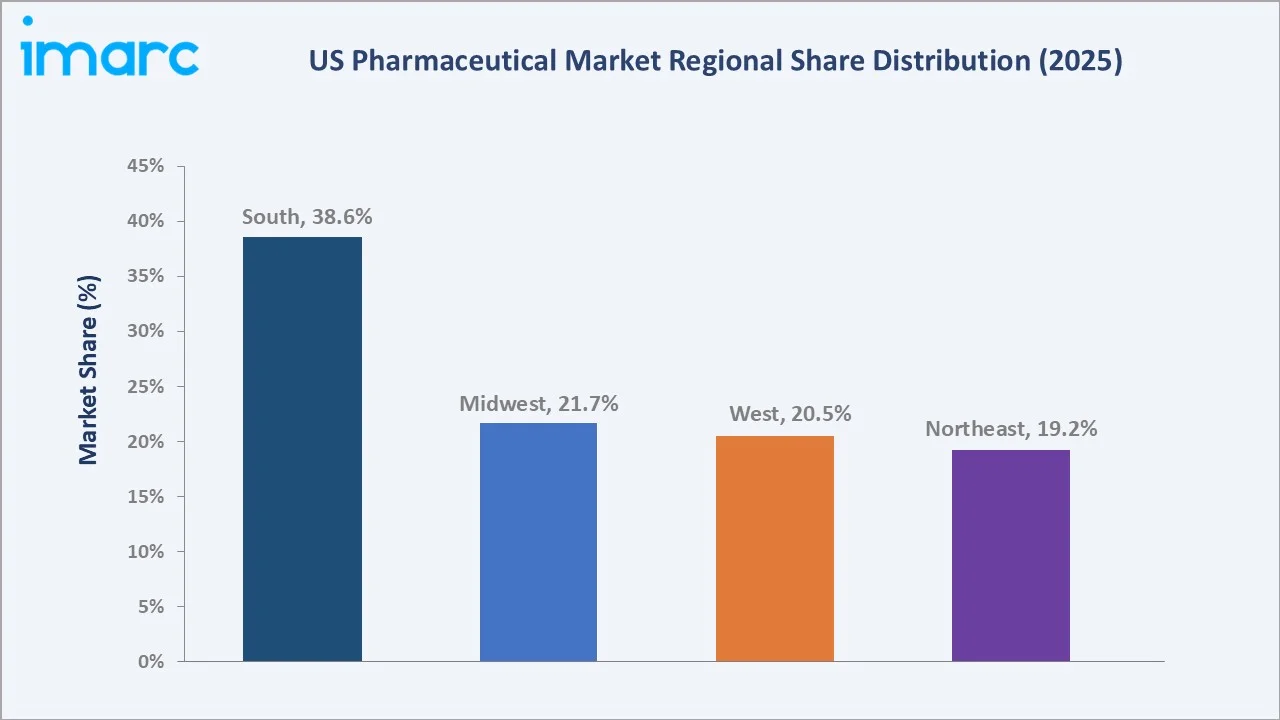

South (38.6% share, 2025) |

|

Fastest Growing Region |

South (~11.4% CAGR through 2034) |

|

Leading Prescription Type |

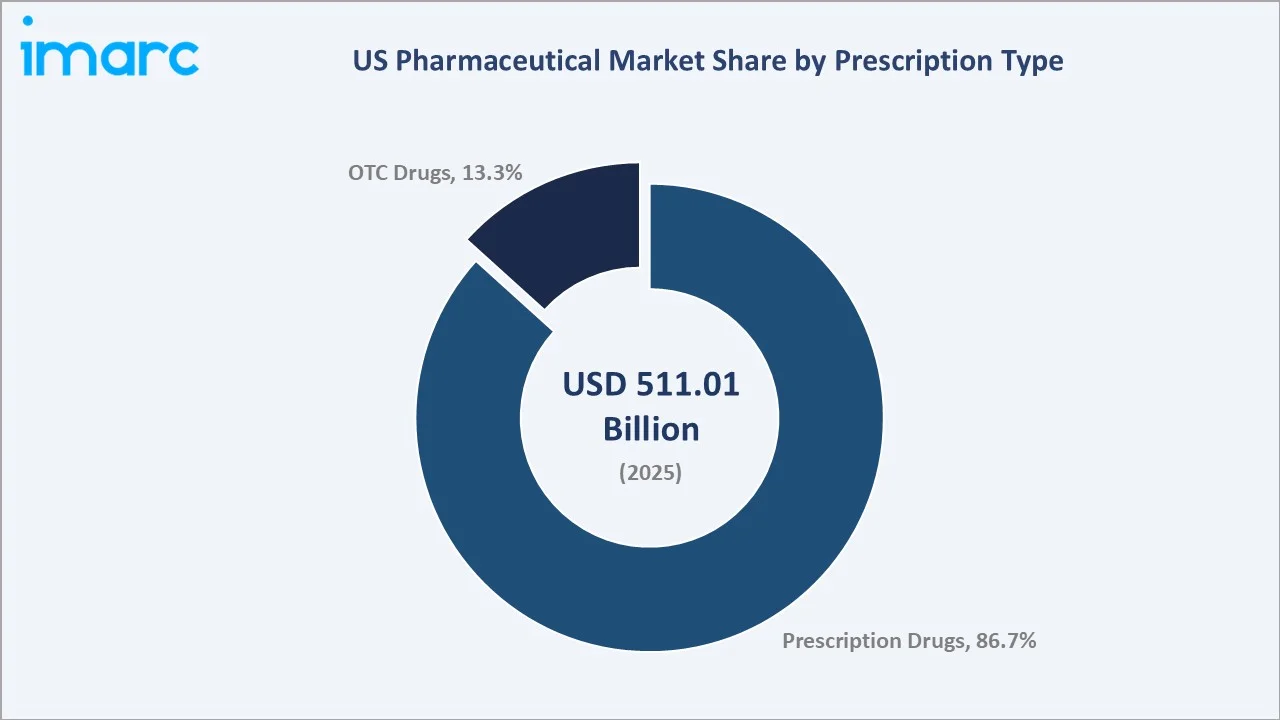

Prescription Drugs (86.7%, 2025) |

|

Leading Therapeutic Category |

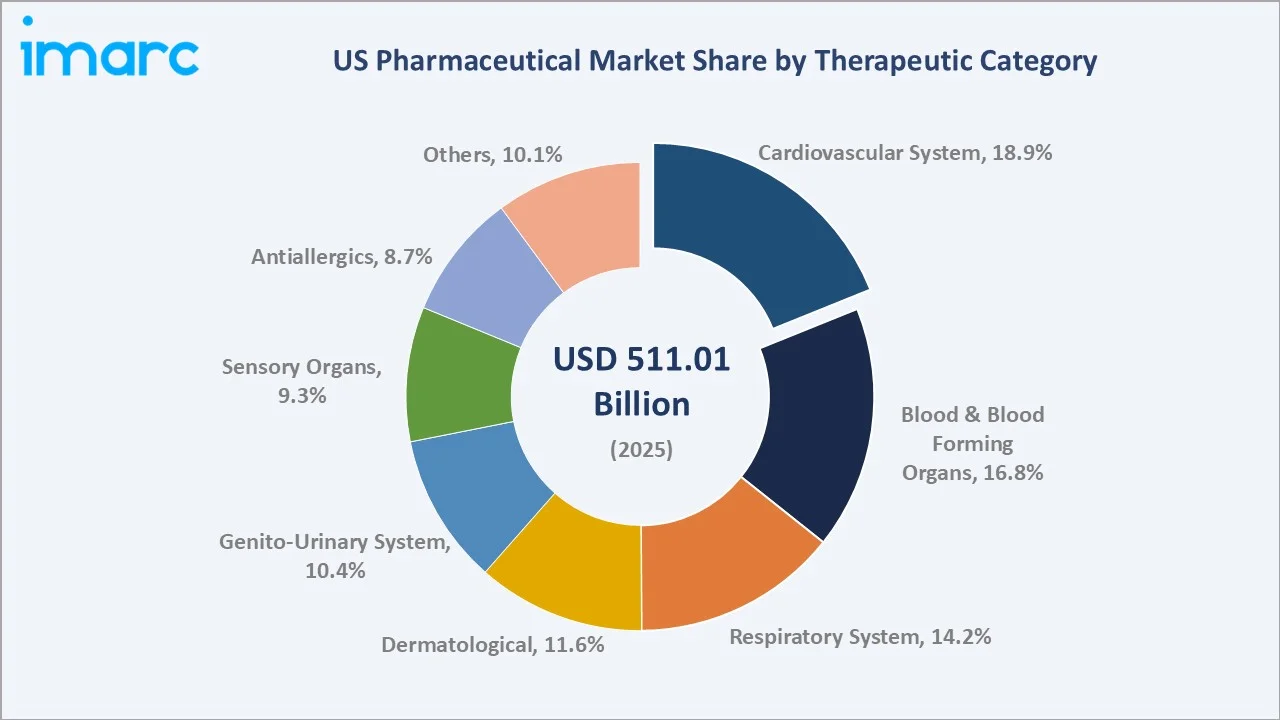

Cardiovascular System (18.9%, 2025) |

The US pharmaceutical market growth trajectory from 2020 through 2034 contrasts steady historical expansion against a stronger forecast curve. This curve is fueled by demographic shifts, biologic and specialty drug adoption, and accelerating digital transformation across drug discovery and delivery.

To get more information on this market, Request Sample

Segment-level CAGR comparisons reveal cardiovascular and blood-related therapies as the fastest-expanding categories. They reflect rising chronic disease prevalence and continued biologic launches across the US pharmaceutical market forecast through 2034.

Executive Summary

The US pharmaceutical market is undergoing a structural transformation. It is shaped by demographic aging, digital innovation, and heavier strategic collaboration across the value chain. Valued at USD 511.01 Billion in 2025, the market is forecast to reach USD 1339.26 Billion by 2034 at a CAGR of 10.90%.

Prescription drugs command 86.7% share in 2025, anchored by branded biologics and the rapid expansion of generic substitutes. The cardiovascular system therapeutic category leads at 18.9%, followed by blood and blood forming organs at 16.8%. Aging-population diseases continue to widen prescription volume across most therapy areas through 2030.

The South region commands 38.6% of national revenue in 2025, supported by population growth in Texas and Florida and large hospital networks. The Midwest holds 21.7%, the West 20.5%, and the Northeast 19.2%. The US pharmaceutical market outlook stays positive as personalized medicine, AI-led drug discovery, and biologics scale across all major regions.

Key Market Insights

|

Insight |

Data |

|

Largest Prescription Type |

Prescription Drugs - 86.7% share (2025) |

|

Second Prescription Type |

OTC Drugs - 13.3% share (2025) |

|

Largest Therapeutic Category |

Cardiovascular System - 18.9% share (2025) |

|

Fastest Growing Therapeutic Category |

Cardiovascular System - ~12.3% CAGR (2026-2034) |

|

Leading Region |

South - 38.6% revenue share (2025) |

|

Top Companies |

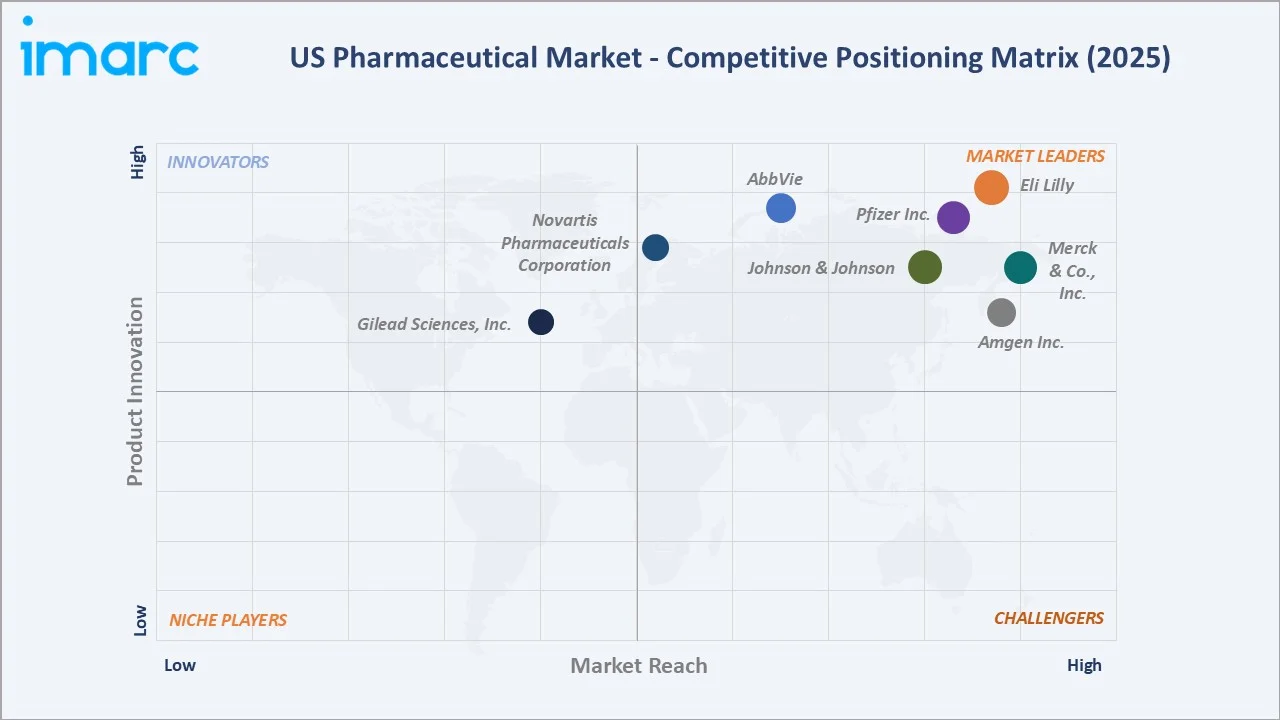

Pfizer Inc., Johnson & Johnson, Merck & Co., Inc., AbbVie, Eli Lilly, Amgen Inc., Gilead Sciences, Inc., Novartis Pharmaceuticals Corporation |

|

Key Opportunities |

Rising adoption of biologics, gene therapies, and increasing prevalence of chronic and rare diseases |

Key Analytical Observations Supporting the Above Data:

- Prescription drugs' 86.7% dominance in 2025 reflects the combined weight of branded biologics, specialty therapies, and rapidly expanding generic prescriptions, with branded prescription volumes showing steady growth in recent years.

- OTC drugs' 13.3% share is supported by rising self-medication trends, expanded Rx-to-OTC switches, and strong consumer demand for cold, pain, and digestive remedies, with the market continuing to see robust sales growth.

- Cardiovascular's 18.9% therapeutic lead driven by the high burden of heart disease, which remains the leading cause of death in the US. This sustains strong demand for treatments such as statins, anticoagulants, and PCSK9 inhibitors.

- South region's 38.6% dominance is underpinned by population scale across Texas, Florida, Georgia, and the Carolinas, plus expanding hospital networks and a higher prevalence of chronic conditions like diabetes and hypertension.

- Aging population pressure is structural, with the number of older adults steadily increasing over time, driving higher prescription volumes across cardiovascular, blood, and sensory organ therapies.

- Digital transformation in drug discovery is accelerating - leading firms now apply AI/ML across target identification, clinical trial design, and post-market pharmacovigilance, reducing development timelines and improving trial success rates.

US Pharmaceutical Market Overview

The US pharmaceutical industry covers the discovery, development, manufacture, and distribution of prescription drugs, OTC medicines, biologics, vaccines, and specialty therapies. Products include small-molecule tablets, injectables, biologics, gene and cell therapies, and digital therapeutics. They are delivered through hospitals, retail and mail-order pharmacies, specialty distributors, and increasingly through telehealth-linked direct-to-patient channels.

The industry sits at the convergence of healthcare demand, regulatory oversight, and technological advancement. Macroeconomic drivers include an aging population, rising chronic disease prevalence, expanding insurance coverage, and federal R&D incentives. At the same time, the structural shift toward biologics, personalized medicine, AI-enabled drug discovery, and digital health is reshaping innovation and procurement strategies across the country pharmaceutical landscape.

Market Dynamics

To evaluate market opportunities, Request Sample

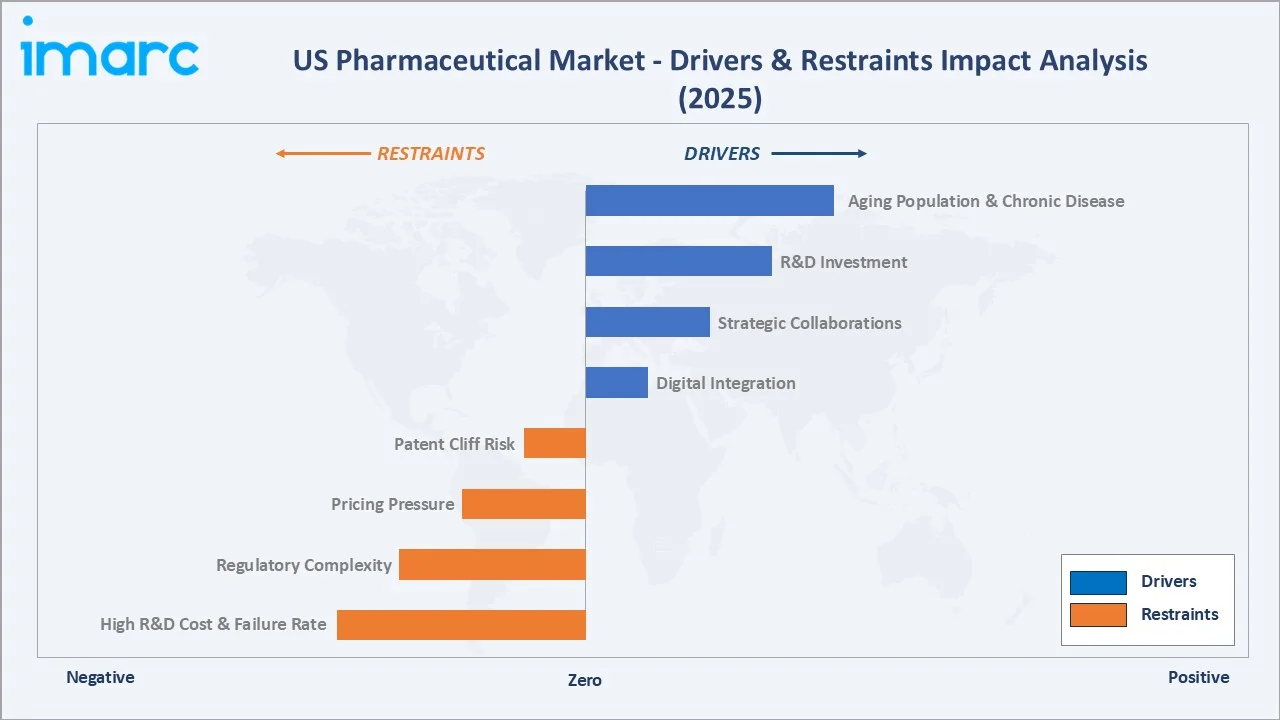

Market Drivers

- Aging Population and Chronic Disease Burden: The US population aged 65 and above is projected to grow significantly over the coming decades, increasing its share of the total population. This demographic shift is driving sustained demand for cardiovascular, anticoagulant, anti-diabetic, and neurology therapies, while lifestyle-related conditions continue to raise the prevalence of non-communicable diseases and overall prescription volumes.

- Rising R&D Investment: PhRMA member companies invested approximately USD 102 billion in R&D in 2021. Sustained investment in biologics, oncology, and rare-disease therapies is expanding the new-product pipeline. As of late 2024, the FDA approved 50 novel drugs, sustaining innovation-led volume growth across specialty categories.

- Strategic Collaborations and Partnerships: Cross-company partnerships are accelerating product launches and de-risking capital outlays. In 2025, Zydus Lifesciences partnered with Synthon BV to launch a generic Ozanimod for multiple sclerosis in the US, with Synthon handling regulatory and manufacturing while Zydus led commercialization. These structured alliances widen therapeutic coverage and shorten time-to-market.

- Digital Integration and AI in Drug Discovery: AI, machine learning, big data, and automation are reshaping every phase of the pharmaceutical value chain - from early discovery to post-market surveillance. Cloud-based collaboration, real-world data systems, and digital therapeutics are improving trial efficiency, pharmacovigilance, and personalized treatment pathways across the country pharmaceutical market.

Market Restraints

- High R&D Cost and Failure Rate: The cost of developing and bringing a new drug to market is extremely high, with most candidates failing during clinical trials. This financial burden constrains smaller players and extends payback periods, particularly for emerging therapies such as gene therapy.

- Regulatory Complexity: Evolving FDA, CMS, and state-level pricing reforms - including Medicare Drug Price Negotiation under the Inflation Reduction Act - introduce continuous compliance overhead. Smaller manufacturers face disproportionate cost pressure on quality, safety, and post-market reporting.

- Pricing Pressure and Generic Erosion: Insurer formulary controls, PBM rebates, and biosimilar entry are compressing margins for blockbuster brands, particularly post loss-of-exclusivity. The US pharmaceutical market share for branded products faces sustained pricing scrutiny through 2030.

Market Opportunities

- Personalized and Precision Medicine: Biomarker-led therapies and gene-editing platforms (CRISPR, mRNA) are unlocking new addressable populations across oncology, rare diseases, and cardiovascular care. CMS coverage expansion for cell and gene therapies is opening reimbursement runway through 2030.

- Biosimilars and Generic Expansion: The US biosimilars market is forecast to triple by 2030 as patents on multiple blockbuster biologics expire. Lupin's October 2025 launch of generic Rivaroxaban for pediatric VTE and Natco Pharma's August 2025 launch of generic Bosentan illustrate the ongoing expansion of cost-efficient therapy options.

- Digital Therapeutics and Telehealth Integration: FDA-cleared digital therapeutics, wearable monitoring tools, and tele-prescription platforms are reshaping patient engagement and adherence. Combined with companion diagnostics, they are creating new revenue layers beyond traditional pill-based therapy.

Market Challenges

- Patent Cliff Risk: Several blockbuster biologics face loss of exclusivity through 2030, creating a sizeable revenue headwind for incumbent leaders. Replacing this revenue requires consistent late-stage pipeline delivery and disciplined business development.

- Supply Chain Resilience: API and excipient supply remains heavily concentrated in Asia. Geopolitical tensions, tariffs, and quality-control incidents continue to drive efforts toward US and near-shore reshoring of critical drug manufacturing.

- Workforce and Talent Constraints: Specialized capabilities in biologics manufacturing, AI/ML drug discovery, and clinical regulatory affairs remain scarce. Talent shortages can delay program timelines and inflate operating costs across mid-tier biotechs.

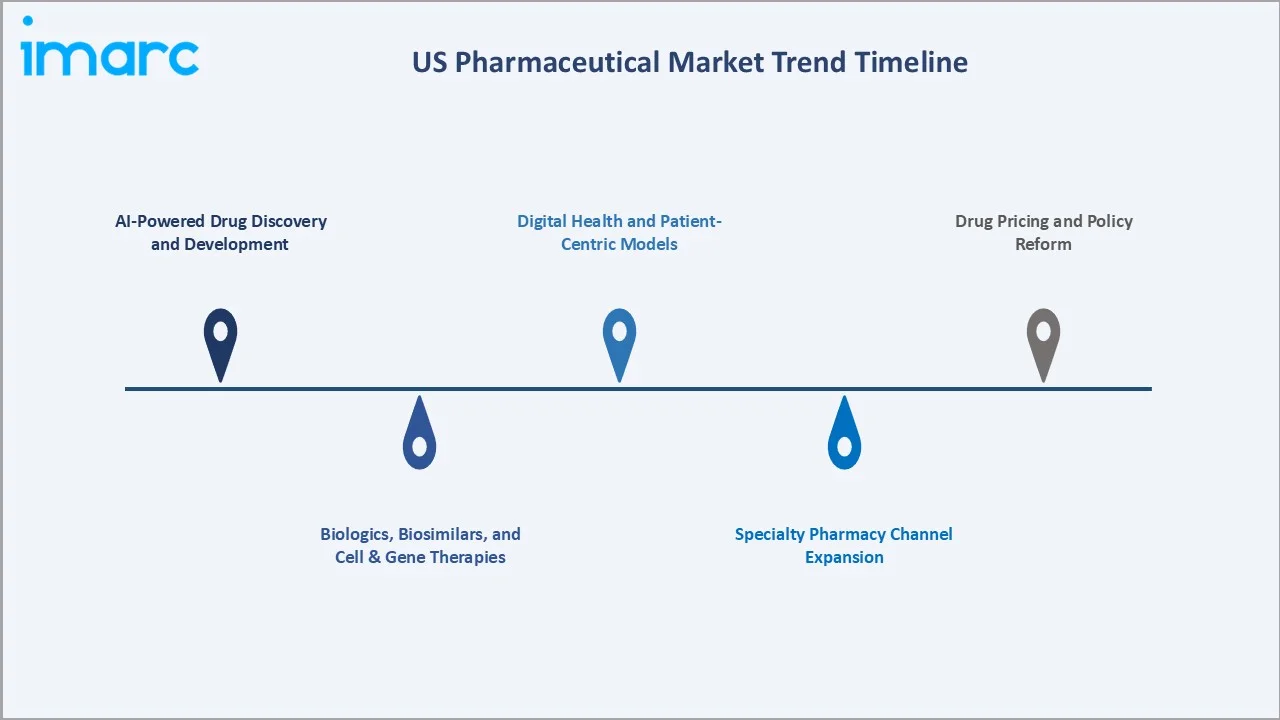

Emerging Market Trends

1. AI-Powered Drug Discovery and Development

AI and ML are compressing early-stage drug discovery cycles from years to months by accelerating target identification, molecule design, and trial site selection. Leading firms now embed AI across translational research, predictive pharmacology, and adaptive trial design, sharply improving Phase II success rates.

2. Biologics, Biosimilars, and Cell & Gene Therapies

Biologics now account for nearly half of US prescription drug spending. Biosimilar approvals continue to widen, while cell and gene therapy launches in oncology, hemophilia, and rare diseases are unlocking premium-priced curative therapies.

3. Specialty Pharmacy Channel Expansion

Specialty pharmacy networks, integrated benefit management, and limited-distribution drug models are expanding, supported by the rapid scaling of high-cost biologic and cell therapy launches.

4. Digital Health and Patient-Centric Models

Telehealth, digital therapeutics, and remote patient monitoring are restructuring patient engagement, especially in mental health, diabetes, and cardiovascular care. Wearables and connected adherence tools are improving real-world outcomes data flow and supporting value-based contracts.

5. Drug Pricing and Policy Reform

The Inflation Reduction Act has activated Medicare price negotiation for selected high-cost drugs from 2026 onward. Manufacturers are recalibrating launch pricing, lifecycle strategy, and indication sequencing to balance access goals with sustained R&D return economics.

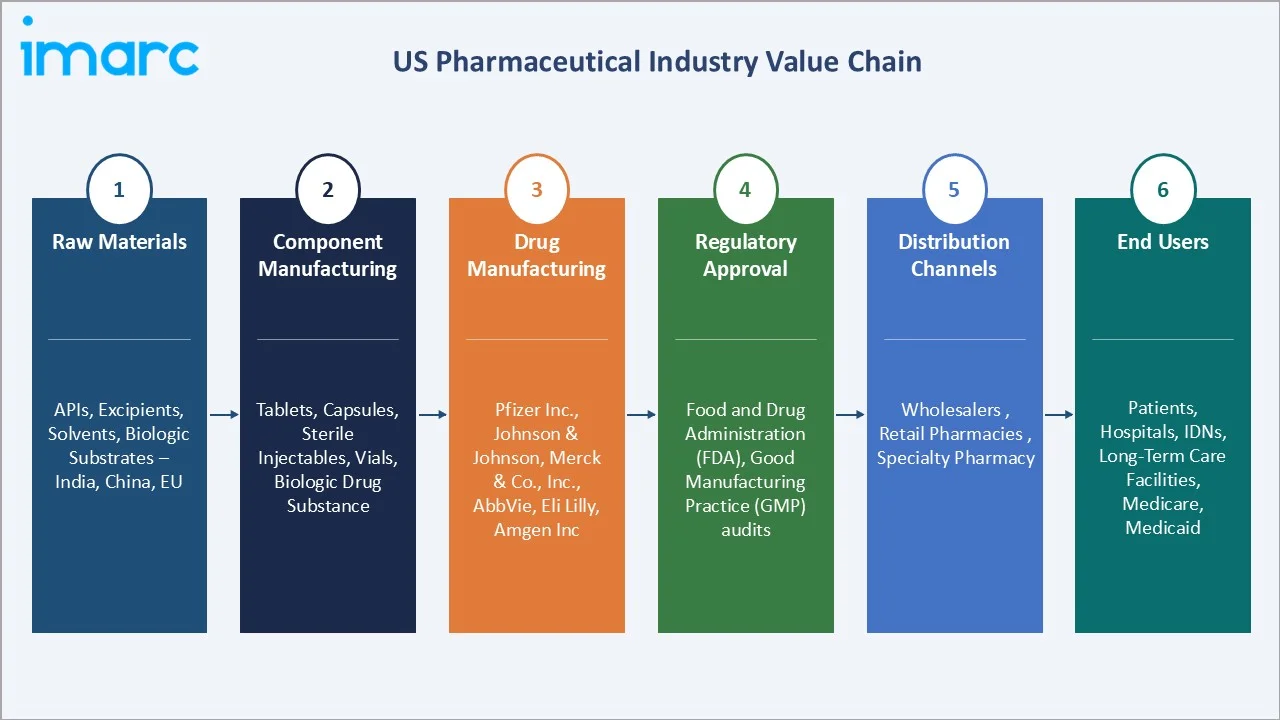

Industry Value Chain Analysis

The US pharmaceutical value chain spans six integrated stages from raw material sourcing through patient delivery. Each stage carries distinct competitive dynamics, margin profiles, and regulatory requirements, all relevant to a complete US pharmaceutical market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

APIs, excipients, solvents, biologic substrates - sourced largely from India, China, and selected EU and US producers |

|

Component Manufacturing |

Tablets, capsules, sterile injectables, vials, prefilled syringes, biologic drug substance produced by CDMOs and OEM sites |

|

Drug Manufacturing |

Pfizer Inc., Johnson & Johnson, Merck & Co., Inc., AbbVie, Eli Lilly, Amgen Inc., Gilead Sciences, Inc., and Novartis Pharmaceuticals Corporation |

|

Regulatory Approval |

FDA (CDER, CBER), USP, DEA - NDA/BLA/ANDA pathways, REMS, post-market commitments, GMP audits |

|

Distribution Channels |

Wholesalers, retail pharmacies, mail-order, specialty pharmacy |

|

End Users |

Patients, hospitals, integrated delivery networks, long-term care facilities, payers, government health programs |

Innovator pharmaceutical companies retain the highest strategic value by integrating R&D, regulatory science, and commercial scale into branded therapy launches. Meanwhile, specialty pharmacy and direct-to-patient digital channels are reshaping distribution, allowing manufacturers to strengthen patient relationships and improve adherence economics.

Technology Landscape in the US Pharmaceutical Industry

AI, Machine Learning, and Drug Discovery

AI and ML are now embedded across target identification, lead optimization, predictive toxicology, and adaptive trial design. Cloud-based research platforms enable distributed teams to collaborate in real time, while generative chemistry models are screening millions of compound candidates faster than traditional in-silico methods.

Biologics, mRNA, and Cell & Gene Therapies

mRNA platforms scaled rapidly through the COVID-19 vaccine cycle and are now extending into oncology and rare diseases. CRISPR-based gene-editing therapies and CAR-T cell therapies are entering wider commercial use, supported by purpose-built single-use bioreactor manufacturing capacity in the US.

Digital Therapeutics and Connected Devices

FDA-cleared digital therapeutics for diabetes, ADHD, substance use, and insomnia are gaining payer reimbursement traction. Combined with smartphone apps, wearables, and connected drug delivery devices, they are improving adherence, generating real-world evidence, and unlocking value-based contracting models.

Manufacturing Innovation and Continuous Processing

Continuous manufacturing, single-use bioreactors, and modular fill-finish lines are improving cycle times, yield, and quality consistency. Several large US manufacturers are investing in domestic biologics capacity to reduce supply chain risk and meet onshoring policy expectations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Prescription Type |

Prescription Drugs |

86.7% |

2025 |

|

Therapeutic Category |

Cardiovascular System |

18.9% |

2025 |

|

Region |

South |

38.6% |

2025 |

By Prescription Type

To access detailed market analysis, Request Sample

Prescription drugs lead the US pharmaceutical market with an 86.7% share in 2025. Demand is driven by branded biologics, specialty therapies, and rapidly expanding generic prescriptions across chronic and acute disease areas. The branded segment is anchored by oncology, immunology, diabetes, and cardiovascular blockbusters, while generics absorb post-patent volume at lower price points. PBMs and insurer formularies remain the gatekeepers shaping prescription drug volume and net pricing.

By Therapeutic Category

The cardiovascular system is the largest therapeutic category at 18.9% share in 2025. Demand is driven by hypertension, dyslipidemia, atrial fibrillation, and heart failure prevalence across the aging population. Statins, anticoagulants (DOACs), antihypertensives, and PCSK9 inhibitors anchor volume, while new lipid-lowering and heart failure agents are extending value.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

38.6% |

Population growth in TX, FL, GA, NC; large hospital networks; high chronic disease prevalence; biotech expansion in NC and GA |

|

Midwest |

21.7% |

Strong manufacturing base (Indiana, Illinois); concentration of CDMOs; stable insured population |

|

West |

20.5% |

California biotech cluster; large biopharma R&D footprint; San Diego biologics ecosystem; Pacific Northwest specialty pharma growth |

|

Northeast |

19.2% |

Academic medical centers; high specialty drug spend per capita |

South commands 38.6% national revenue share in 2025. Texas and Florida together represent more than half of the regional opportunity, supported by population growth and large hospital networks like HCA and Tenet. Higher prevalence of cardiovascular, diabetes, and respiratory conditions reinforces sustained demand. Research Triangle in North Carolina and Atlanta's biotech corridor are expanding the region's manufacturing and clinical research footprint, with the South forecast to remain the fastest-growing region at approximately 11.4% CAGR through 2034.

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Pfizer Inc. |

Eliquis, Prevnar, Ibrance |

Leader |

Vaccines, oncology, cardiovascular scale; strong COVID-era cash position |

|

Johnson & Johnson |

Stelara, Darzalex, Tremfya |

Leader |

Immunology and oncology biologics; broad innovative medicine pipeline |

|

Merck & Co., Inc. |

Keytruda, Gardasil |

Leader |

Oncology immunotherapy leader, vaccines, anti-infectives breadth |

|

AbbVie |

Humira, Skyrizi, Rinvoq |

Leader |

Immunology franchise leadership and rapid Skyrizi/Rinvoq scaling |

|

Eli Lilly |

Mounjaro, Zepbound |

Leader |

GLP-1 / obesity blockbusters, diabetes, oncology pipeline |

|

Amgen Inc. |

Enbrel, Repatha, Prolia |

Challenger |

Biologics manufacturing scale, biosimilars, bone health portfolio |

|

Gilead Sciences, Inc. |

Biktarvy, Gilead Sciences, Inc. |

Challenger |

HIV franchise leadership, oncology expansion via Gilead Sciences, Inc. |

|

Novartis Pharmaceuticals Corporation |

Cosentyx, Entresto, Pluvicto |

Challenger |

Immunology, cardiovascular, radioligand oncology innovation |

The US pharmaceutical market's competitive landscape is moderately concentrated at the innovator tier, while the generic and specialty segments remain highly fragmented. Leading players compete on pipeline depth, biologics manufacturing scale, payer access, and digital engagement. Strategic acquisitions are a recurring competitive lever - large pharma continues to in-license oncology, obesity, and rare-disease assets to refresh growth profiles ahead of upcoming patent cliffs.

Key Company Profiles

Pfizer Inc.

Pfizer Inc., headquartered in New York City, is one of the world's largest research-based biopharmaceutical companies. Founded in 1849, it operates across cardiovascular, oncology, immunology, vaccines, and rare diseases with a presence in over 125 countries.

- Product & Platform Portfolio: Pfizer's US pharmaceutical portfolio includes Eliquis Prevnar pneumococcal vaccines, Ibrance for breast cancer, Vyndaqel for ATTR-CM, and the Comirnaty COVID-19 mRNA vaccine portfolio.

- Recent Developments: In 2023, Pfizer Inc. completed the acquisition of Seagen Inc. for $43 billion. The deal significantly expands Pfizer’s oncology pipeline, especially in antibody-drug conjugates (ADCs), a fast-growing cancer therapy segment. It positions Pfizer to offset declining COVID-related revenues with long-term cancer drug growth.

- Strategic Focus: Pfizer's strategy centers on rebuilding pipeline strength via oncology bolt-ons, expanding ADC and mRNA platforms, and managing the post-COVID revenue normalization through cost discipline and selective in-licensing.

Johnson & Johnson

Johnson & Johnson is one of the world’s largest and most diversified healthcare companies, operating across pharmaceuticals and medical technology, headquartered in New Brunswick, New Jersey.

- Product & Platform Portfolio: Johnson & Johnson's portfolio includes Stelara, Tremfya, and Darzalex in immunology and oncology. The company also produces Invega Hafyera for schizophrenia and is expanding cell therapy via Carvykti for multiple myeloma in partnership with Legend Biotech.

- Recent Developments: In 2025, Johnson & Johnson plans to invest over USD 55 billion in US manufacturing, R&D, and technology over the next four years, marking a significant increase in domestic investment. The strategy includes new advanced manufacturing facilities, expansion of existing plants, and a focus on high-value therapies such as oncology, neuroscience, and immunology.

- Strategic Focus: J&J's strategy emphasizes immunology and oncology pipeline depth, biosimilar defense via lifecycle management, and selective bolt-on acquisitions to offset Stelara's loss of exclusivity.

Merck & Co.

Merck & Co., headquartered in Rahway, New Jersey, is a leading research-driven biopharmaceutical company with a strong franchise in oncology, vaccines, and animal health. The company operates across more than 140 countries.

- Product & Platform Portfolio: Merck's portfolio is anchored by Keytruda, the world's leading PD-1 immuno-oncology agent, alongside Gardasil HPV vaccines, the pneumococcal franchise, and Januvia for type 2 diabetes.

- Recent Developments: In 2025, Merck & Co. has announced the groundbreaking of a new USD 3 billion “Center of Excellence” for pharmaceutical manufacturing in Elkton, Virginia. The facility is designed to expand the company’s small-molecule production capabilities, covering both active pharmaceutical ingredients and finished drug products.

- Strategic Focus: Merck's strategy focuses on extending Keytruda's lifecycle through subcutaneous formulations, building cardiovascular and rare-disease pillars, and maintaining vaccine franchise leadership in pediatric and adult immunization.

Market Concentration Analysis

The US pharmaceutical market exhibits moderate concentration at the innovator tier and high fragmentation in generics. The top five players - Pfizer Inc., Johnson & Johnson, Merck & Co., Inc., AbbVie, Eli Lilly - collectively account for approximately 35-42% of US pharmaceutical revenue in 2025.

The market is experiencing two structural shifts. At the innovator tier, consolidation is accelerating around oncology, obesity, immunology, and rare-disease pipelines via M&A and licensing. Through 2034, biosimilar adoption and the entry of cell and gene therapy specialists will further reshape concentration dynamics across therapy areas.

Investment & Growth Opportunities

Fastest-Growing Segments

Cardiovascular and blood-forming organ therapies are the highest-CAGR therapeutic categories, with cardiovascular projected at approximately 12.3% CAGR through 2034 and blood and blood forming organs at 11.6%. Within prescription drugs, GLP-1 obesity and diabetes therapies, oncology biologics, and cell and gene therapies represent the most attractive growth pockets.

Emerging Opportunity Pockets

The South region offers the strongest demographic and infrastructure growth runway, supported by Texas and Florida population gains and the Research Triangle's biopharmaceutical expansion. Specialty pharmacy networks, AI-led drug discovery startups, and US-based biologic manufacturing reshoring also represent high-conviction investment themes through 2030.

Venture and Strategic Investment Trends

Strategic acquisitions continue to reshape the competitive landscape. Recent moves include AbbVie's Cerevel and ImmunoGen acquisitions and Pfizer's integration of Seagen. Venture investment in 2024-2025 has concentrated on AI drug discovery (Insilico, Recursion peers), GLP-1 next-generation candidates, radioligand oncology therapies, and obesity-adjacent metabolic platforms - all expected to attract further capital through 2030.

Future Market Outlook (2026-2034)

The US pharmaceutical market forecast projects sustained value expansion from USD 511.01 Billion in 2025 to USD 1339.26 Billion by 2034 at a CAGR of 10.90%. The market is expected to cross USD 857 billion by 2030.

Three structural shifts will shape the market through 2034. First, AI-led drug discovery and digital therapeutics will redefine the cost and timeline economics of new drug development, compressing average time-to-market by an estimated 18-24 months for AI-native programs. Second, biosimilars and generic erosion will reset the branded pricing curve - particularly for blockbuster biologics losing exclusivity by 2030. Third, the integration of personalized medicine, gene editing, and value-based contracting will rewire payer-manufacturer economics.

Research Methodology

Primary Research

Primary research involved structured interviews conducted in 2024-2025 with US pharmaceutical industry stakeholders, including R&D directors at large biopharma firms, regulatory leaders at CDMOs, formulary directors at PBMs and health plans, and senior buyers at specialty pharmacy networks. Primary inputs validated market sizing, segmentation estimates, and adoption timelines for biologics, biosimilars, and digital therapeutics.

Secondary Research

Secondary sources include FDA approval databases, CMS Medicare Part B and Part D spend data, PhRMA annual industry reports, IQVIA Institute publications, US Census Bureau demographic projections, CDC chronic disease prevalence data, USPTO patent filings, and SEC 10-K filings of leading manufacturers. Trade publications, including BioPharma Dive, FiercePharma, Endpoints News, and STAT, also informed the analysis.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models. Inputs include US GDP growth, population aging trajectories, prescription volume by therapy area, and historical adoption patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for IRA pricing reform, biosimilar uptake, and macroeconomic uncertainty.

US Pharmaceutical Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Prescription Types Covered |

|

| Therapeutic Categories Covered | Antiallergics, Blood and Blood Forming Organs, Cardiovascular System, Dermatological, Genito Urinary System, Respiratory System, Sensory Organs, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Pfizer Inc., Johnson & Johnson, Merck & Co., Inc., AbbVie, Eli Lilly, Amgen Inc., Gilead Sciences, Inc., Novartis Pharmaceuticals Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the US pharmaceutical market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the US pharmaceutical market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the US pharmaceutical industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the US Pharmaceutical Market Report

The US pharmaceutical market was valued at USD 511.01 Billion in 2025, driven by an aging population, rising chronic disease burden, expanding biologics use, and digital integration across the value chain.

The market is projected to reach USD 1,339.26 Billion by 2034, growing at a CAGR of 10.90% during 2026-2034, supported by R&D investment, biologics scaling, and personalized medicine adoption.

Prescription drugs lead with an 86.7% share in 2025, anchored by branded biologics, oncology, immunology, and rapidly expanding generic substitutes for blockbuster molecules across multiple therapeutic categories.

The cardiovascular system is the largest therapeutic category with 18.9% share in 2025, followed by blood and blood forming organs (16.8%) and respiratory system (14.2%) - reflecting chronic disease prevalence.

The South region dominates with 38.6% share in 2025. Texas and Florida population growth, large hospital networks, and the Research Triangle biotech corridor underpin its national leadership position.

Key drivers include population aging, rising R&D investment, AI-led drug discovery, strategic collaborations, biologics expansion, and continued digital therapeutics integration into care delivery.

Major players include Pfizer Inc., Johnson & Johnson, Merck & Co., Inc., AbbVie, Eli Lilly, Amgen Inc., Gilead Sciences, Inc., and Novartis Pharmaceuticals Corporation.

The cardiovascular system therapeutic category is among the fastest growing, advancing at approximately 12.3% CAGR through 2034, driven by chronic disease burden and innovative lipid and heart failure agents.

Key opportunities include GLP-1 obesity and diabetes therapies, oncology biologics and ADCs, cell and gene therapies, AI-driven drug discovery platforms, biosimilars, and US-based biologic manufacturing reshoring through 2030.

AI, ML, big data, and cloud platforms are now embedded across drug discovery, clinical trial design, and post-market surveillance. They are compressing development timelines and improving real-world evidence collection significantly.

The IRA introduces Medicare drug price negotiation for selected high-cost drugs starting 2026, recalibrating launch pricing, lifecycle strategy, and indication sequencing across the branded segment through 2030.

Biosimilars are central to the cost trajectory. As patents on multiple blockbuster biologics expire by 2030, biosimilar adoption is forecast to triple, reshaping the prescription drug pricing curve and competitive intensity.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)