US Tractor Market Size, Share, Trends and Forecast by Power Output, Drive Type, Application, and Region, 2026-2034

US Tractor Market Size, Share, Trends & Forecast (2026-2034)

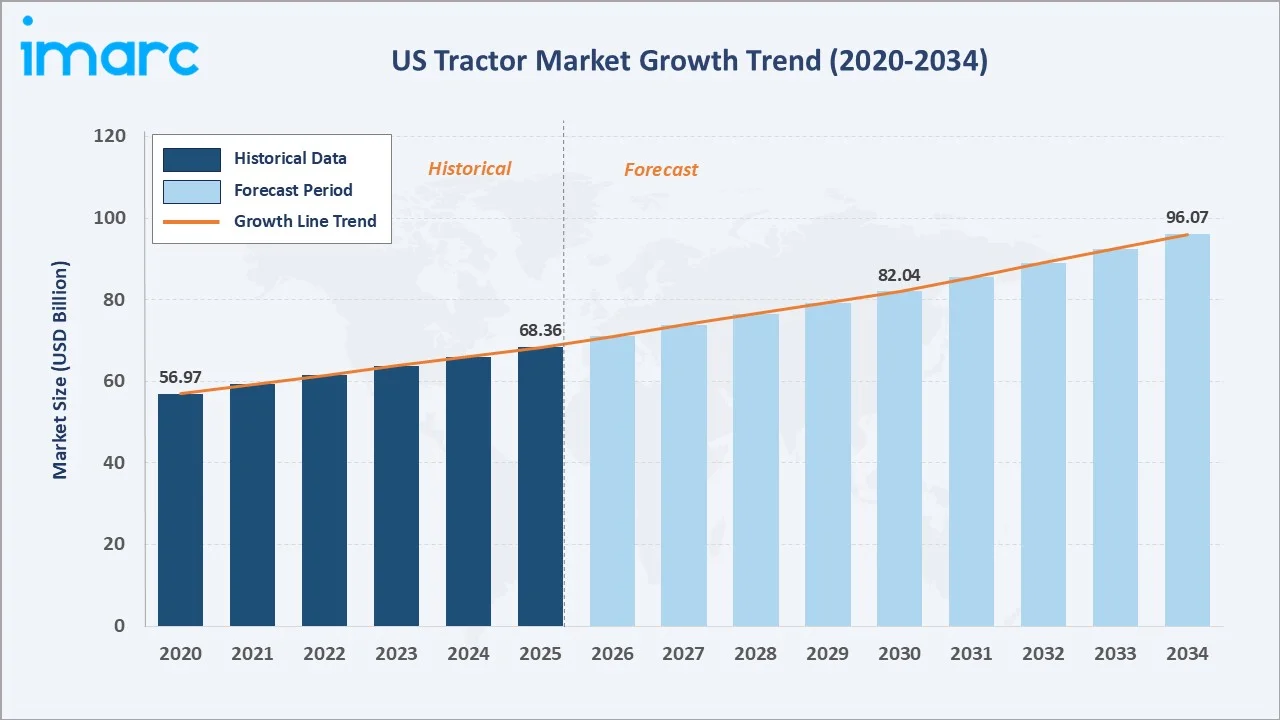

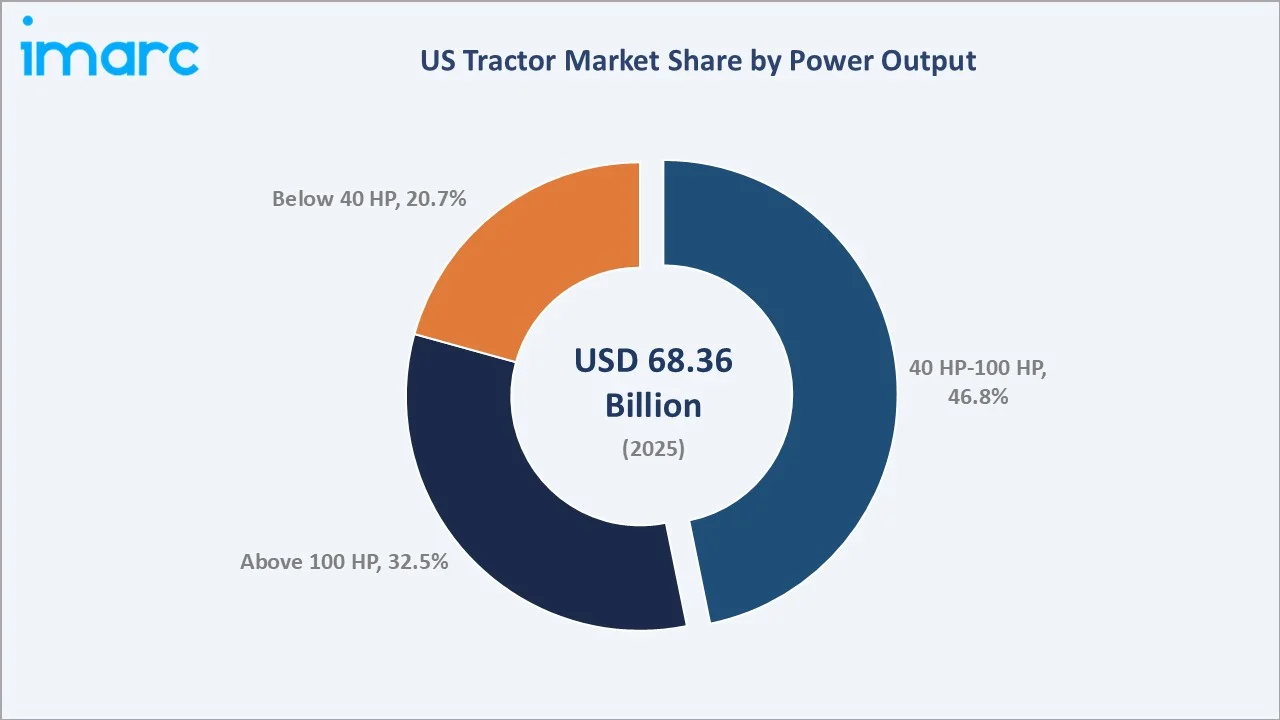

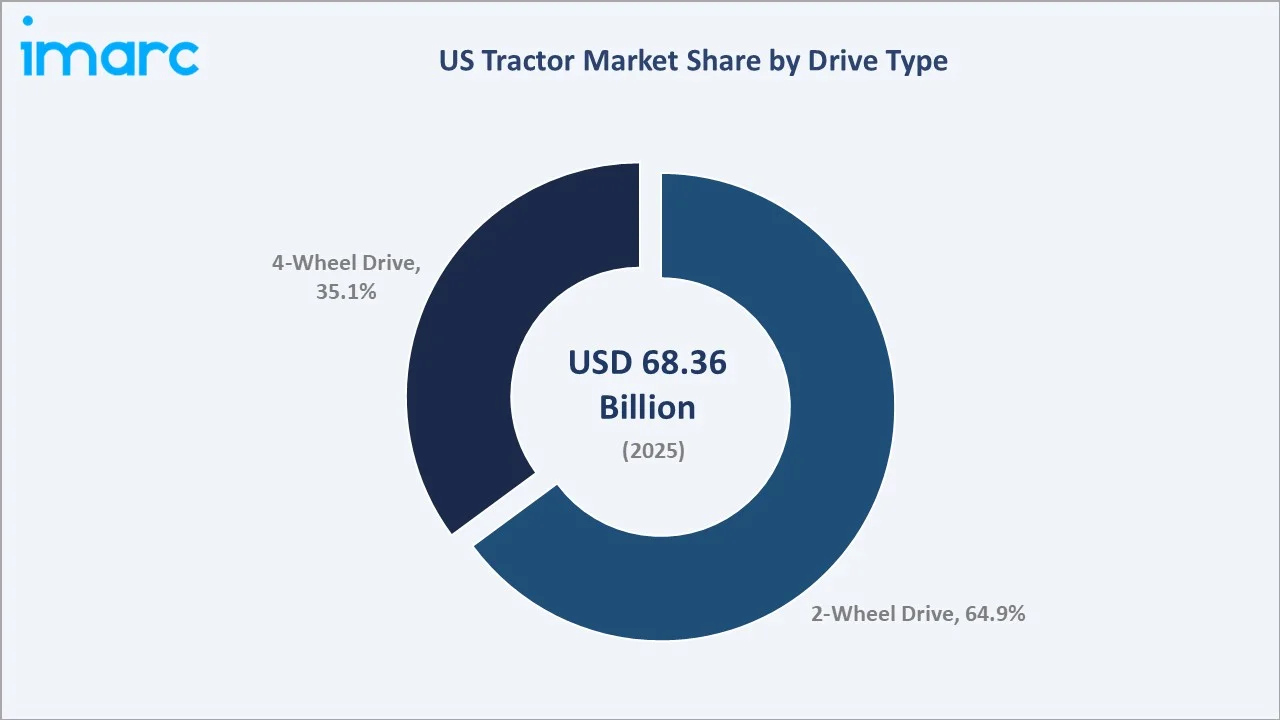

The US tractor market size was valued at USD 68.36 Billion in 2025 and is projected to reach USD 96.07 Billion by 2034, exhibiting a CAGR of 3.72% during the forecast period 2026-2034. The market is being driven by accelerating adoption of precision and autonomous farming technology, sustained federal loan and subsidy support, and rising large-scale farm consolidation.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 68.36 Billion |

|

Forecast Market Size (2034) |

USD 96.07 Billion |

|

CAGR (2026-2034) |

3.72% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

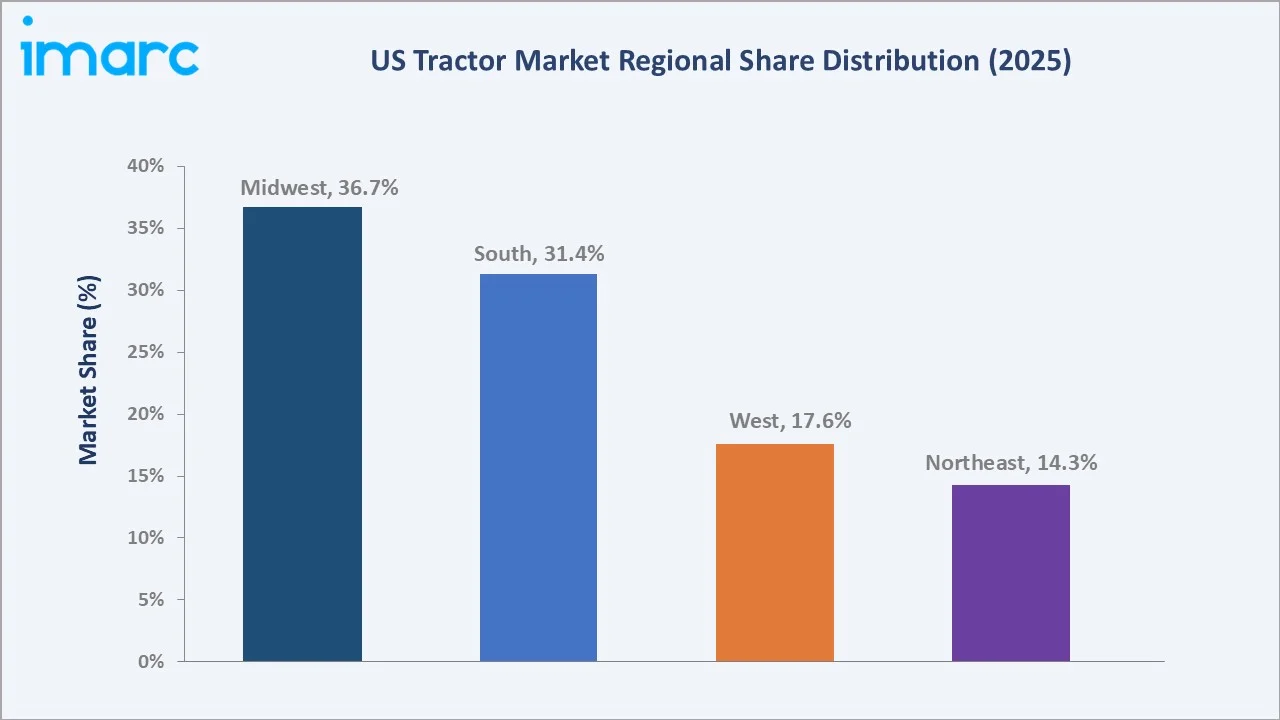

Largest Region |

Midwest (36.7% share, 2025) |

|

Fastest Growing Region |

South (CAGR ~4.3%) |

|

Leading Power Output |

40 HP-100 HP (46.8%, 2025) |

|

Leading Drive Type |

2-Wheel Drive (64.9%, 2025) |

The US tractor market growth trajectory from 2020 through 2034 reflects steady historical expansion of nearly USD 11.40 Billion between 2020 and 2025, followed by a sustained forecast curve supported by autonomous technology adoption and farm-equipment modernization cycles.

To get more information on this market, Request Sample

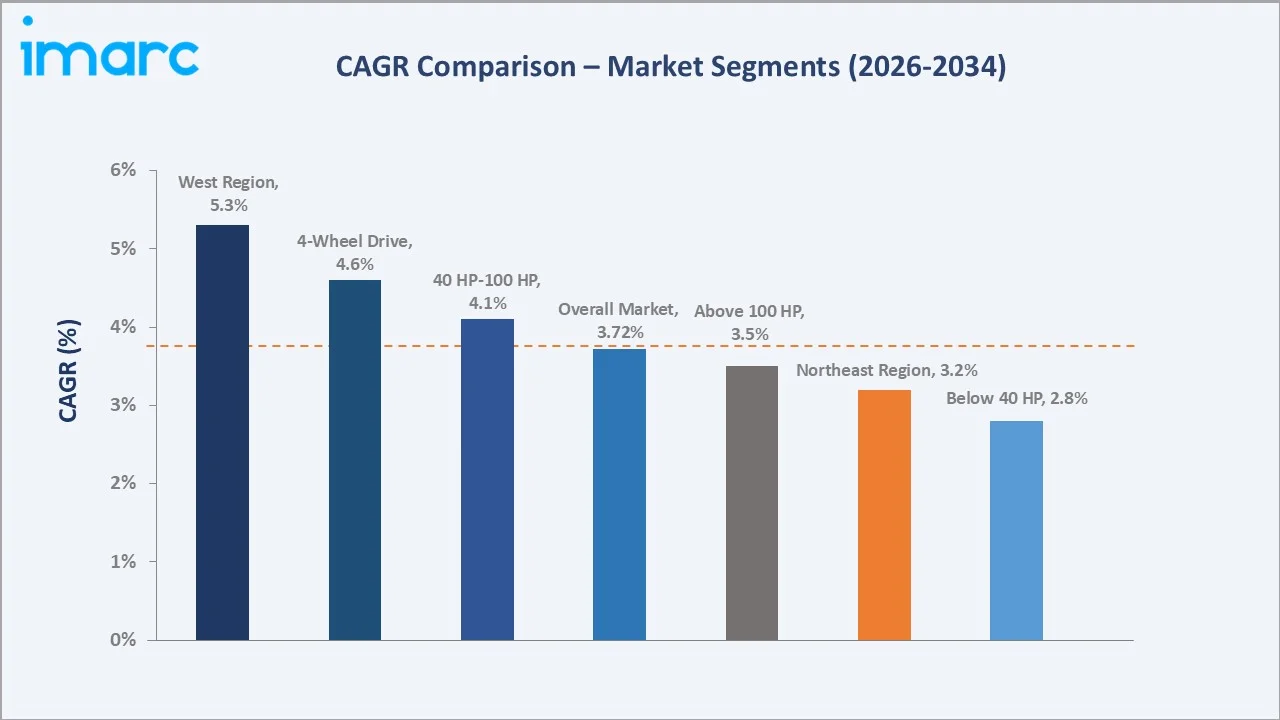

Segment-level CAGR comparisons highlight construction-application tractors and 4-wheel drive units as the fastest-growing sub-categories within the US tractor market forecast through 2034, both outpacing the overall industry growth rate of 3.72%.

Executive Summary

The US tractor market is undergoing a structural transformation driven by precision agriculture, persistent farm labor shortages, and federal financing programs that lower the cost of equipment ownership. Valued at USD 68.36 Billion in 2025, the market is forecast to reach USD 96.07 Billion by 2034 at a CAGR of 3.72%, adding nearly USD 27.7 Billion in incremental value over the period.

The 40 HP-100 HP utility tractor category commands a 46.8% share in 2025, supported by mid-sized row-crop and livestock farms. Above 100 HP units hold 32.5% as large-acreage operations adopt high-horsepower autonomous platforms. 2-wheel drive systems represent 64.9% of demand because they remain cost-effective for flat, well-drained terrain. The 4-wheel drive segment is the fastest-growing drive-type category at an estimated CAGR of 4.6% through 2034.

The Midwest leads with a 36.7% revenue share in 2025, followed by the South at 31.4% and the West at 17.6%. The US tractor market outlook remains constructive as autonomous platforms move from pilot to commercial scale, federal loan disbursements continue to support equipment refresh, and OEMs commit multi-billion-dollar investments in domestic manufacturing capacity.

Key Market Insights

|

Insight |

Data |

|

Largest Power Output |

40 HP-100 HP – 46.8% share (2025) |

|

Second Power Output |

Above 100 HP – 32.5% share (2025) |

|

Largest Drive Type |

2-Wheel Drive – 64.9% share (2025) |

|

Fastest Growing Drive Type |

4-Wheel Drive – ~4.6% CAGR (2026-2034) |

|

Leading Region |

Midwest – 36.7% revenue share (2025) |

|

Top Companies |

Deere & Company, CNH Industrial N.V, AGCO Corporation, Kubota Corporation, Mahindra&Mahindra Ltd., YANMAR HOLDINGS CO., LTD., and LS MTRON LTD. |

|

Autonomous Tractor Adoption |

USD 20 Billion John Deere investment (2025) |

Key Analytical Observations Supporting the Above Data:

- 40 HP-100 HP dominance at 46.8% in 2025 reflects the breadth of mid-sized US farms, where utility horsepower aligns with row-crop, livestock, and orchard workloads across the Corn Belt and Southern Plains.

- Above 100 HP tractors' 32.5% share is driven by large-acreage operations in Iowa, Illinois, Kansas, and Texas, where high-horsepower units now ship with autonomous kits, GPS guidance, and 360-degree camera arrays.

- 2-wheel drive leadership at 64.9% is supported by relatively flat terrain in key agricultural regions and its lower upfront cost, which makes it a practical choice for farmers. Strong overall farm income levels continue to sustain steady replacement demand in the market.

- Midwest's 36.7% regional dominance driven by key states such as Iowa, Illinois, Nebraska, Minnesota, and Indiana, which form the core of US corn and soybean production and have the highest tractor density per farm in the country.

- John Deere's USD 20 Billion commitment announced in May 2025 for US manufacturing expansion over the next decade signals long-term confidence and is expected to add domestic capacity across autonomous and electric platforms.

US Tractor Market Overview

Tractors are the foundational power units of US agriculture, construction, and forestry. The market spans utility, compact, sub-compact, and high-horsepower row-crop tractors across 2-wheel and 4-wheel drive configurations, supported by attachments such as loaders, mowers, balers, and tillage tools. Modern units integrate GPS guidance, telematics, and AI-driven autonomy.

The industry sits at the intersection of farm income cycles, federal policy, commodity prices, and labor availability. Growth is supported by USDA loan programs, Inflation Reduction Act provisions, persistent farm labor shortages, and rising capital deployment by OEMs in autonomous platforms, electric powertrains, and connected-fleet technology.

Market Dynamics

To evaluate market opportunities, Request Sample

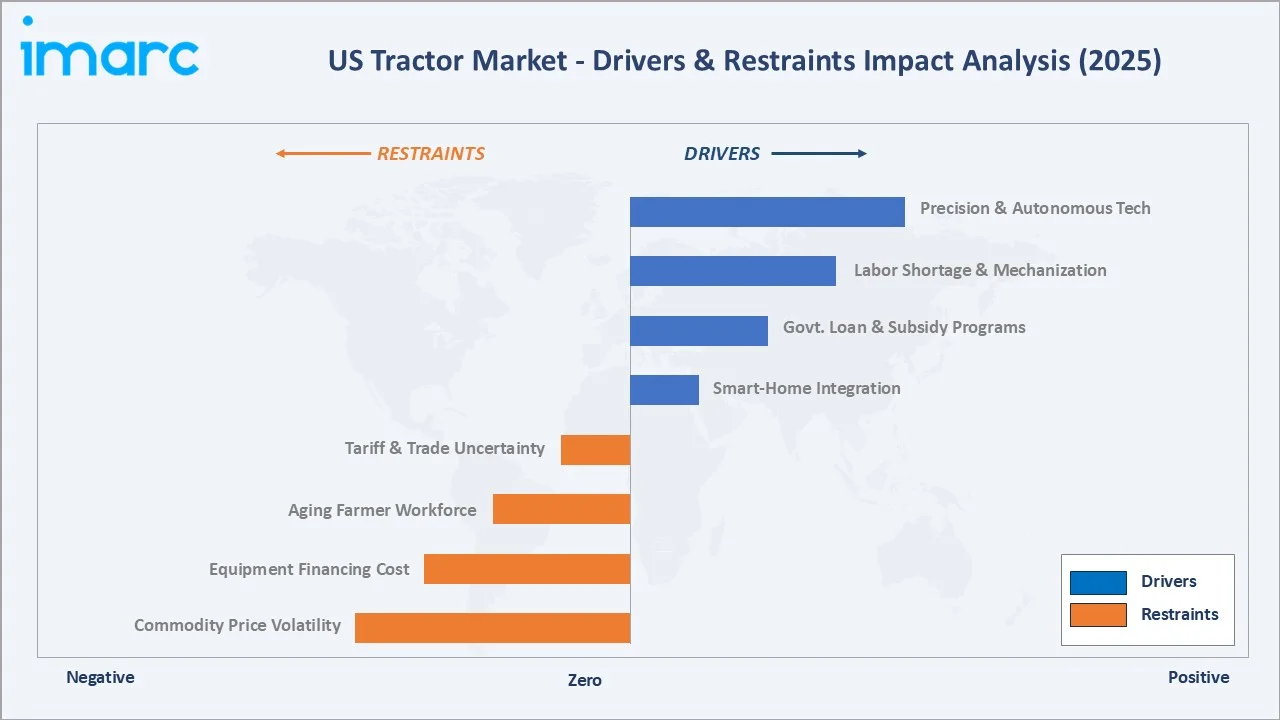

Market Drivers

- Precision and Autonomous Technology Adoption: Modern tractors now integrate GPS guidance, machine vision, and AI-based control systems. Second-generation autonomy with 360-degree camera arrays enables the use of wider implements at higher field speeds, helping address a persistent labor shortage impacting a significant share of farms.

- Government Loan and Subsidy Programs: The USDA Farm Service Agency has provided substantial assistance to distressed borrowers under recent programs, with cumulative support reaching significant levels. These initiatives help lower the effective cost of new tractor acquisition and support ongoing fleet modernization.

- Farm Labor Shortage and Mechanization: Persistent labor scarcity has accelerated mechanization across US farms. Higher wages and shrinking H-2A guest-worker availability are pushing operators toward autonomous and high-horsepower units that compress field operations into narrower weather windows.

- Major Manufacturing Investment: John Deere announced a USD 20 Billion US manufacturing investment in May 2025. These commitments are expanding domestic capacity for autonomous, electric, and connected platforms through 2034.

Market Restraints

- Commodity Price Volatility: Corn, soybean, and wheat prices directly determine farm purchasing power. Sharp swings in commodity revenue compress equipment-purchase budgets and delay replacement cycles, particularly for non-essential horsepower upgrades.

- Equipment Financing Costs: Sustained elevated interest rates have increased floor-plan and equipment loan costs. Higher monthly payments on mid- to high-value units are extending ownership cycles and reducing dealer trade-in volumes.

- Aging Farmer Workforce: USDA Census of Agriculture data show the average US farmer age now exceeds 58 years. Older operators tend to defer high-tech equipment investment, slowing the diffusion of autonomous and connected platforms across smaller operations.

Market Opportunities

- Autonomous Retrofit Kits: OEM-developed retrofit autonomy kits compatible with installed-base tractors create incremental revenue streams and lower the financial barrier to autonomous adoption for mid-sized farms unwilling to replace functioning equipment.

- Electric and Hybrid Powertrains: Compact and utility electric tractors are emerging for orchards, vineyards, and dairy operations where noise and emissions matter. The IRA's Section 45W and 30C provisions create installation and purchase incentives for low-emission farm equipment.

- Specialty and Vineyard Tractors: California’s large specialty crop sector and growing domestic wine production are driving demand for narrow-track, low-profile tractors. Recent collaborations between major equipment manufacturers and agtech firms have accelerated the adoption of autonomous solutions in specialty-crop farming across the Western US.

Market Challenges

- Tariff and Trade Uncertainty: US–China tariff actions on agricultural exports compress farm income and indirectly delay tractor purchases. Tariffs on steel and components also increase OEM input costs, putting upward pressure on pricing across major equipment platforms.

- Right-to-Repair Legislation: State-level right-to-repair laws, including Colorado's 2023 Consumer Right to Repair Agricultural Equipment Act, force OEMs to redesign software access and warranty structures, creating compliance costs and dealer-channel friction.

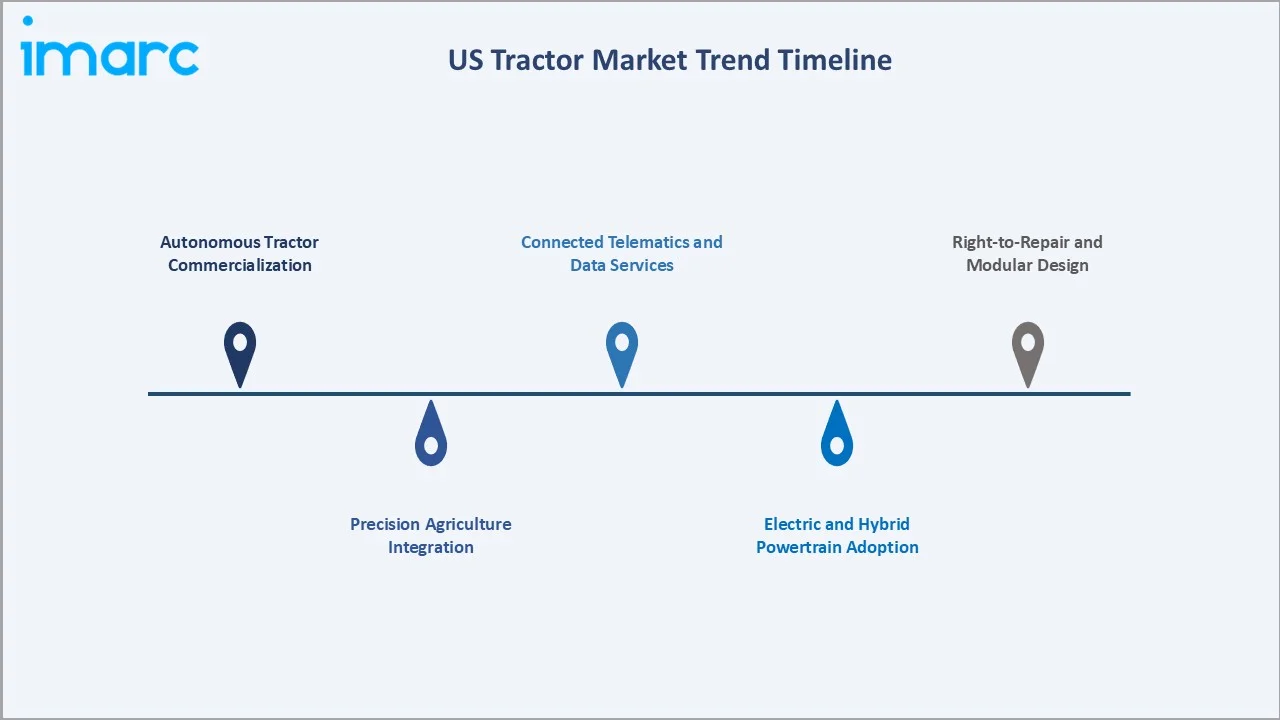

Emerging Market Trends

1. Autonomous Tractor Commercialization

Driverless tractors with multi-camera vision and sensor fusion are moving from pilot deployments to commercial scale. Major OEMs introduced second-generation autonomy in 2025, enabling wider implements, higher field speeds, and 24-hour operation that compress planting and tillage windows.

2. Precision Agriculture Integration

GPS guidance, variable-rate application, and ISOBUS connectivity are now standard on higher-horsepower tractors. Ongoing partnerships between major equipment manufacturers and precision agriculture technology providers are further consolidating mixed-fleet platforms and improving cross-brand interoperability.

3. Electric and Hybrid Powertrain Adoption

Compact electric tractors targeting orchards, vineyards, and small farms are being launched by John Deere, and Kubota. IRA tax credits for clean-energy farm equipment are accelerating early adoption, particularly in California and the Pacific Northwest.

4. Connected Telematics and Data Services

Subscription-based telematics platforms now generate recurring revenue for OEMs. John Deere Operations Center, AGCO FarmerCore, and CNH AFS Connect are tracking machine health, fuel use, and field operations across millions of US acres.

5. Right-to-Repair and Modular Design

Pressure from farm associations and state legislatures is driving OEMs to publish diagnostic codes and offer self-repair tools. This is reshaping aftermarket service economics and forcing modular design changes through the 2026-2034 forecast period.

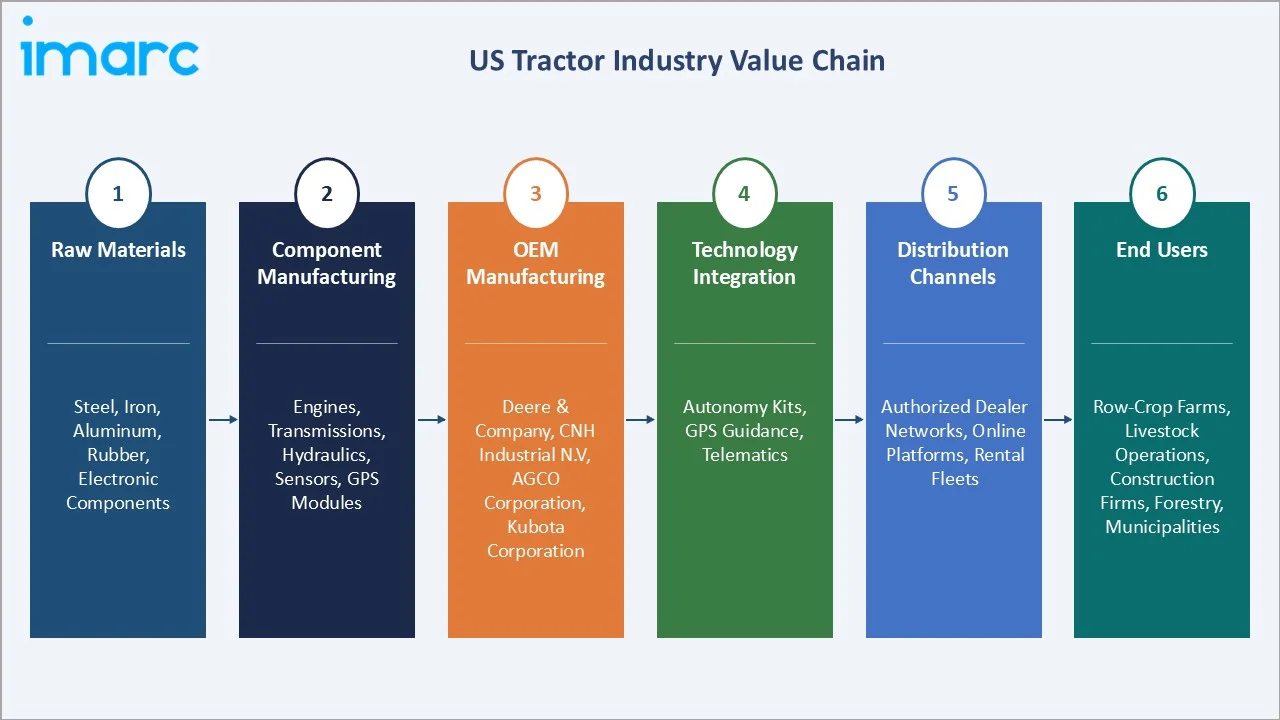

Industry Value Chain Analysis

The US tractor industry value chain spans six stages from raw materials to end-user operations. Each stage carries distinct margin profiles, capital intensity, and technology investment requirements relevant to the overall US tractor market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Steel, iron, aluminum, rubber, electronic components |

|

Component Manufacturing |

Engines, transmissions, hydraulics, sensors, GPS modules |

|

OEM Manufacturing |

Deere & Company, CNH Industrial N.V, AGCO Corporation, Kubota Corporation, Mahindra&Mahindra Ltd., YANMAR HOLDINGS CO., LTD., and LS MTRON LTD. |

|

Technology Integration |

Autonomy kits, GPS guidance, telematics, ISOBUS |

|

Distribution Channels |

Authorized dealer networks, online platforms, rental fleets – Titan Machinery, RDO Equipment, United Rentals |

|

End Users |

Row-crop farms, livestock operations, construction firms, forestry contractors, municipalities |

OEMs hold the highest strategic value by integrating engines, electronics, and software into turnkey solutions. Dealer networks, however, are increasingly the gatekeepers of customer relationships, supported by service revenue and used-equipment trade economics.

Technology Landscape in the US Tractor Industry

Autonomy and Machine Vision

Second-generation autonomous tractors feature 360-degree multi-camera arrays, LiDAR fusion, and AI-based obstacle detection. These platforms operate continuously across tillage, planting, and spraying tasks, with John Deere, CNH, and AGCO leading commercial deployment.

Precision Components and Hydraulics

Variable-rate hydraulic systems, electronic fuel injection, and CVT transmissions are now standard on premium tractors. These technologies improve fuel efficiency compared to older mechanical units while enhancing operator comfort during long working hours.

Connectivity and IoT Integration

4G/5G modems, Wi-Fi, and satellite uplinks are enabling continuous machine-to-cloud data flow. OEM platforms such as Operations Center and AFS Connect now support fleet-wide visibility, predictive maintenance alerts, and remote diagnostics.

Electrification and Alternative Powertrains

Battery-electric utility tractors from, John Deer Tractor target compact and orchard segments. Hybrid powertrains and biofuel-compatible engines are also expanding, supported by IRA Section 45W incentives for low-emission farm equipment.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Power Output | 40 HP - 100 HP | 46.8% | 2025 |

| Drive Type | 2-Wheel Drive | 64.9% | 2025 |

| Application | 🔒 | 🔒 | 2025 |

| Region | Midwest | 36.7% | 2025 |

By Power Output

To access detailed market analysis, Request Sample

The 40 HP–100 HP utility category leads the US tractor market by power output, serving a broad base of farms ranging from row-crop operations to livestock and dairy. Demand is supported by ongoing replacement cycles of aging equipment and increasing attachment versatility, with implements such as loaders, mowers, and balers driving additional purchases. Key demand centers include major agricultural states across the Midwest, South, and Northeast regions.

By Drive Type

2-wheel drive tractors dominate the US market with a 64.9% share in 2025. The configuration remains the cost-efficient default for flat, well-drained terrain across the Midwest and South, where most US row-crop production occurs. Lower acquisition cost 2WD attractive for utility, mid-horsepower, and replacement applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Midwest |

36.7% |

Corn Belt row-crop operations, Iowa/Illinois/Nebraska scale, high tractor density |

|

South |

31.4% |

Texas livestock, Florida specialty crops, Arkansas/Mississippi row-crop expansion |

|

West |

17.6% |

California specialty crops, Pacific Northwest forestry, vineyard mechanization |

|

Northeast |

14.3% |

Dairy operations, hobby farms, landscaping, municipal applications |

The Midwest commands a 36.7% share of the US tractor market in 2025, reflecting the Corn Belt's structural dominance in US agriculture. The South holds 31.4% of demand, with Texas leading on livestock and cotton operations, Florida on specialty crops, and Arkansas, Mississippi, and Louisiana on row-crop and rice production.

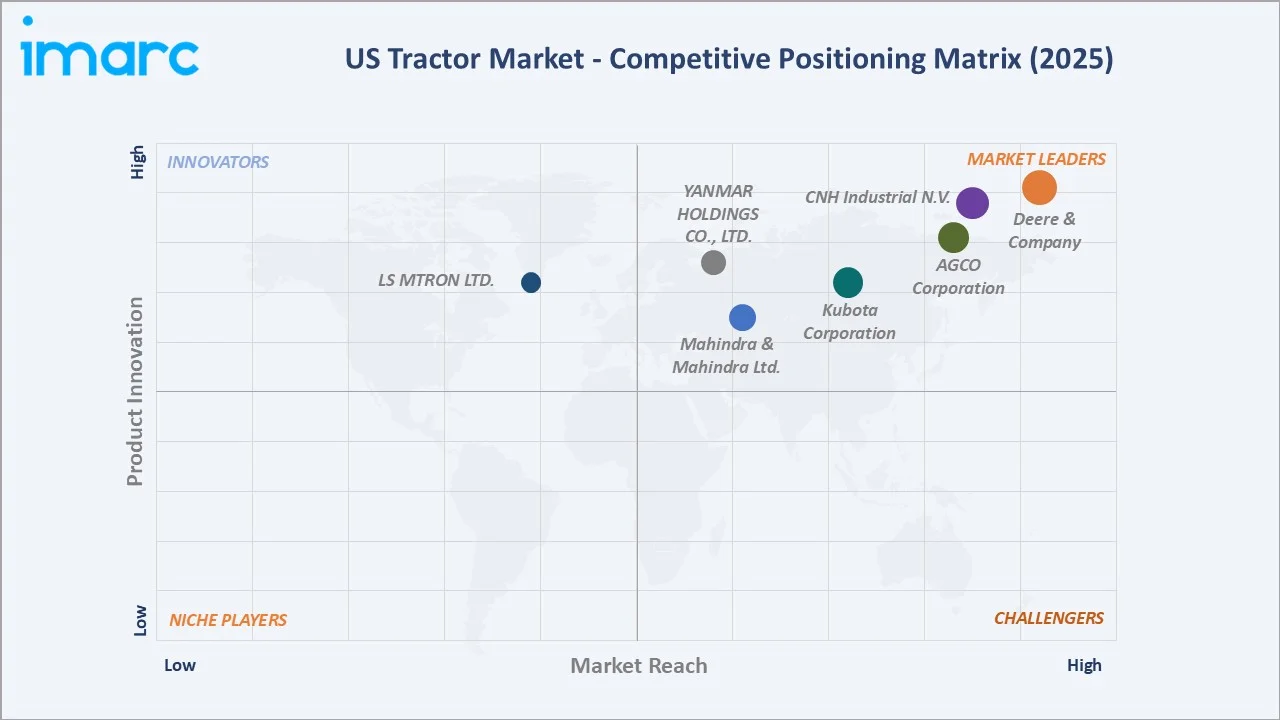

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Deere & Company |

John Deere |

Leader |

Autonomous platform, dealer network, US manufacturing scale |

|

CNH Industrial N.V. |

Case IH, New Holland |

Leader |

Multi-brand strategy, Bluewhite alliance, mid-horsepower depth |

|

AGCO Corporation |

Massey Ferguson, Fendt |

Leader |

PTx Trimble JV, precision agriculture, premium European brands |

|

Kubota Corporation |

Kubota |

Leader |

Compact and sub-compact dominance, Southern US strength |

|

Mahindra&Mahindra Ltd. |

Mahindra |

Challenger |

Value-tier 25-100 HP platform, rural lifestyle market |

|

YANMAR HOLDINGS CO., LTD. |

Yanmar America |

Challenger |

Compact diesel tractors, US dealer expansion |

|

LS MTRON LTD. |

LS Tractor USA |

Challenger |

Korean-engineered utility tractors, value pricing |

The US tractor market's competitive landscape is highly concentrated at the top, with John Deere, CNH, AGCO, and Kubota collectively holding the majority of revenue. Competition is intensifying around autonomy, precision agriculture, and connected services.

Key Company Profiles

Deere & Company

Deere & Company, headquartered in Moline, Illinois, is the largest agricultural equipment manufacturer in the world and the dominant player in the US tractor market. Founded in 1837, the company operates production facilities across Iowa, Illinois, Tennessee, and North Carolina.

- Product & Platform Portfolio: John Deere's tractor portfolio spans the 1 Family compact line through the 9R series above 700 HP, supported by autonomous-ready platforms, the Operations Center telematics suite, and the See & Spray precision-spraying system.

- Recent Developments: In May 2025, John Deere has announced a USD 20 billion investment in the United States over the next decade, including expansion of production capacity for its high-horsepower John Deere 9RX tractors at its Waterloo, Iowa facility, with new assembly lines to meet rising demand for advanced large-scale farming equipment.

- Strategic Focus: Deere's strategy centers on autonomous platform leadership, recurring software and data revenue through Operations Center, and US manufacturing scale that protects against import tariffs and component-supply disruptions.

CNH Industrial N.V.

CNH Industrial N. V., headquartered in London with North American operations in Racine, Wisconsin, owns Case IH and New Holland, two of the most established US tractor brands. The company operates manufacturing in Wisconsin, Pennsylvania, and Kansas.

- Product & Platform Portfolio: CNH's portfolio spans Case IH Magnum, Steiger, and Farmall lines as well as New Holland T-series and Workmaster utility tractors, complemented by AFS Connect telematics and the Raven precision-agriculture platform.

- Recent Developments: In June 2025, CNH Industrial N.V., through its New Holland brand, is advancing sustainable tractor technology with its methane-powered models, enabling farmers to run tractors on biogas derived from agricultural waste. The New Holland T7 Methane Power tractor delivers diesel-equivalent performance while supporting on-farm energy independence and lower emissions, marking a shift toward alternative-fuel tractors in modern agriculture.

- Strategic Focus: CNH is consolidating around autonomous specialty-crop solutions, mid-horsepower depth, and expansion of AFS Connect subscriptions across its installed base.

AGCO Corporation

AGCO Corporation is headquartered in Duluth, Georgia, and operates across the Massey Ferguson, Fendt, Challenger, and Valtra brands.

- Product & Platform Portfolio: AGCO's tractor portfolio includes Massey Ferguson utility tractors, Fendt premium row-crop platforms above 200 HP, and Challenger track tractors, all integrated with PTx Trimble precision technologies.

- Recent Developments: In April 2026, AGCO Corporation showcased its advanced tractor innovation at the Great American Agriculture Celebration in Washington, D.C., featuring a symbolic Fendt 1167 Vario MT tractor. The display highlighted modern high-horsepower tractor technology and AGCO’s continued focus on precision farming and equipment innovation.

- Strategic Focus: AGCO is focused on Fendt premium expansion in North America, mixed-fleet precision platforms through PTx Trimble, and growing Massey Ferguson dealer coverage in the South and Midwest.

Market Concentration Analysis

The US tractor market is highly concentrated. The top five players - Deere & Company, CNH Industrial N.V, AGCO Corporation, Kubota Corporation, Mahindra&Mahindra Ltd. - collectively account for an estimated 75-82% of total US tractor revenue in 2025.

The market is bifurcating - premium platforms above 100 HP are consolidating around the top three OEMs, while compact and sub-compact tiers remain more contestable. Through 2034, autonomous platform investment, telematics scale, and dealer-network depth are expected to deepen concentration at the top tier.

Investment & Growth Opportunities

Fastest-Growing Segments

Construction-application tractors are the fastest-growing application sub-segment at an estimated 5.3% CAGR through 2034, driven by US infrastructure spending under the IIJA. The 4-wheel drive segment is growing at 4.6% CAGR, while autonomous-ready high-horsepower units represent the premium-technology growth opportunity, with US deployments projected to expand significantly through 2030.

Emerging Market Expansion

The Southern US is the highest-potential expansion region, projected to grow at 4.3% CAGR through 2034, driven by Texas livestock expansion, Florida specialty crops, and Arkansas/Mississippi row-crop investment. California's specialty crop sector represents the strongest near-term opportunity for autonomous narrow-track and electric tractors.

Strategic Investment Trends

Strategic acquisitions and joint ventures are reshaping the competitive landscape. Large-scale manufacturing investments and partnerships between major OEMs and technology firms are anchoring long-term capital deployment. At the same time, venture capital is increasingly focused on autonomous retrofit kits, electric powertrains, and AI-driven crop monitoring platforms over the coming decade.

Future Market Outlook (2026-2034)

The US tractor market forecast projects steady value expansion from USD 68.36 Billion in 2025 to USD 96.07 Billion by 2034 at a CAGR of 3.72%. The Midwest will retain regional leadership while the South captures the highest growth rate. Premium high-horsepower platforms and 4-wheel drive units will outpace overall market growth.

Three major shifts will reshape the market through 2034. Autonomous tractors will move from premium niches to mainstream Corn Belt deployment by 2028-2030, with retrofit kits expanding access for installed-base owners. Electric and hybrid powertrains will achieve commercial traction in compact and specialty-crop tractors, supported by IRA incentives. Right-to-repair legislation and digital service platforms will redefine aftermarket economics, opening new revenue lines for OEMs and independent service providers alike.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024-2025 with tractor industry stakeholders such as OEM product directors, dealer principals, large-acreage farm operators, USDA program administrators, and equipment finance lenders. Primary insights validated market sizing, segment shares, and autonomous adoption timelines.

Secondary Research

Secondary sources include USDA Census of Agriculture, USDA Economic Research Service farm income reports, Association of Equipment Manufacturers (AEM) shipment data, US Bureau of Labor Statistics agricultural labor data, OEM annual reports and SEC filings, and trade publications such as Farm Equipment Magazine, Successful Farming, and Farm Industry News.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating US farm income outlook, commodity price trajectories, IIJA infrastructure spending, and historical equipment replacement cycles. Scenario analysis - base, upside, and downside - was performed to capture macroeconomic and policy uncertainty.

US Tractor Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Power Outputs Covered | Below 40 HP, 40 HP - 100 HP, Above 100 HP |

| Drive Types Covered | 2-Wheel Drive, 4-Wheel Drive |

| Applications Covered | Agriculture, Construction, Mining, Forestry, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, Mahindra&Mahindra Ltd., YANMAR HOLDINGS CO., LTD., LS MTRON LTD., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the US tractor market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the US tractor market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the US tractor industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the US Tractor Market Report

The US tractor market was valued at USD 68.36 Billion in 2025, supported by precision technology adoption, USDA loan programs, persistent farm labor shortages, and OEM manufacturing investment.

The market is projected to reach USD 96.07 Billion by 2034, growing at a CAGR of 3.72% during 2026-2034, driven by autonomous platforms, IRA incentives, and infrastructure-led construction demand.

The 40 HP-100 HP utility category leads with a 46.8% share in 2025, driven by its alignment with mid-sized US row-crop, livestock, and dairy farm workloads across the Corn Belt.

2-wheel drive systems dominate with a 64.9% share in 2025, supported by lower acquisition cost and the flat, well-drained terrain of the Midwest where most US row-crop production takes place.

The Midwest leads with a 36.7% share in 2025, anchored by Iowa, Illinois, Nebraska, and Indiana, which together account for the majority of US corn and soybean production.

The South is the fastest-growing region at an estimated 4.3% CAGR through 2034, driven by Texas livestock expansion, Florida specialty crops, and rising mid-sized operator demand.

Key drivers include precision and autonomous technology adoption, USDA loan and subsidy programs, persistent farm labor shortages, and major OEM investments in domestic manufacturing capacity.

Leading companies include Deere & Company, CNH Industrial N.V, AGCO Corporation, Kubota Corporation, Mahindra&Mahindra Ltd., YANMAR HOLDINGS CO., LTD., and LS MTRON LTD.

Autonomous adoption is driven by farm labor shortages, narrow planting and tillage windows, and OEM investment in 360-degree camera arrays, sensor fusion, and AI-based obstacle detection.

USDA Farm Service Agency loan programs and related policy support have provided substantial assistance to distressed borrowers, helping sustain tractor purchase capacity across the market.

Construction-application tractors at 5.3% CAGR and 4-wheel drive units at 4.6% CAGR are the fastest-growing segments, supported by infrastructure spending and high-horsepower row-crop demand.

Key opportunities include autonomous retrofit kits, electric and hybrid compact tractors, specialty-crop and vineyard platforms, and connected telematics services targeting installed fleets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)