Vacuum Insulation Panel Market Report by Type (Flat Panel, Special Shape Panel), Raw Material (Plastics, Metal), Core Material (Silica, Fiberglass, and Others), Application (Construction, Cooling and Freezing Devices, Logistics, and Others), and Region 2026-2034

Vacuum Insulation Panel Market Size:

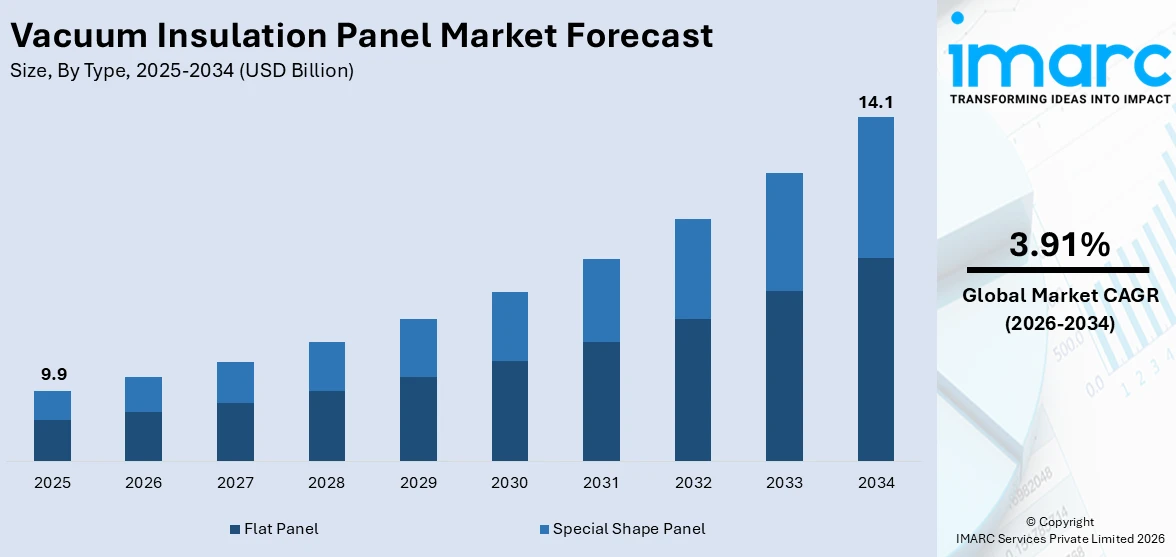

The global vacuum insulation panel market size reached USD 9.9 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 14.1 Billion by 2034, exhibiting a growth rate (CAGR) of 3.91% during 2026-2034. The increasing awareness of sustainable building practices, stringent regulations promoting energy efficiency, advancements in manufacturing technologies, rising demand for cold chain logistics, the shift towards electric vehicles, the trend of modular construction, and the significant growth in the pharmaceutical industry are some of the factors creating a positive outlook for the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 9.9 Billion |

|

Market Forecast in 2034

|

USD 14.1 Billion |

| Market Growth Rate 2026-2034 | 3.91% |

Vacuum Insulation Panel Market Analysis:

- Major Market Drivers: As per the vacuum insulation panel market analysis, the market is largely fueled by rapid urbanization, which has surged the need for energy-efficient, spatially conservative insulation solutions in building construction. Consequently, the market benefits from the stringent regulations designed to cut down the energy utilization. Additionally, there is a significant demand for high-performance insulation, especially with the expansion of the cold chain sector for pharmaceutical distribution and perishable food transportation. Moreover, the development in material absorbing technology, such as nanoporous materials, improves the thermal performance of vacuum insulation panels (VIPs), which is further creating a positive outlook for the vacuum insulation panel market growth. Apart from this, the widening consumer base of the electric vehicle (EV) also fuels a strong market for VIPs due to their application in insulating battery compartments, enhancing efficiency and safety.

- Key Market Trends: The vacuum insulation panel market trends include the surging product utilization into smart buildings that use numerous sensors and the Internet of Things (IoT) devices to dynamically optimize the consumption of electricity depending on structural and human behavior. Moreover, there is a trend from the vacuum insulation panel (VIP) market to environmentally friendly and sustainable generation of insulation materials, which has led to the development of recyclable and biodegradable VIPs. Furthermore, the rising demand for thinner, flexible panels for various construction and application materials in order to save space and perform efficiently is supporting the market growth. Apart from this, the increasing focus on improving the fire resistance of VIPs to meet building safety regulations is also driving the vacuum insulation panel market share.

- Geographical Trends: The Asia-Pacific region holds the leading position in the global vacuum insulation panel market. This is primarily because the countries in the region, such as China and India, are experiencing rapid urbanization and industrialization. These factors are responsible for extensive construction in the region, and many projects require high-performance insulation to suit energy efficiency criteria. In addition, the region boasts a highly developed manufacturing industry of consumer appliances, which widely adopt VIPs for thermal management. As per the vacuum insulation panel market report, the next region by the volume of the market is Europe, where energy efficiency is strongly regulated, and sustainable construction is prevalent. North America is also a large part of the market due to the presence of well-established cold chain logistics and transport.

- Competitive Landscape: As per the market statistics, some of the key vacuum insulation panel companies include Avery Dennison Corporation, Etex Group, Kingspan Group, Knauf Insulation, Morgan Advanced Materials, Panasonic Corporation of North America, Recticel Insulation UK, Turvac Vacuum Insulation, va-Q-tec Thermal Solutions GmbH, etc.

- Challenges and Opportunities: The vacuum insulation panel market faces several challenges, including high manufacturing costs and the complexity of installation, which can hinder widespread product adoption. The sensitivity of VIPs to puncture and their performance degradation over time due to gas permeation also pose significant challenges. However, these challenges present substantial opportunities for market players. There is a growing opportunity for the development of more robust and puncture-resistant panels, as well as materials that offer longer lifespans. Innovations in barrier technologies that reduce gas permeation could greatly extend the usable life of VIPs. Additionally, the market can capitalize on the increasing demand for sustainable and energy-efficient insulation solutions across various sectors, including automotive, building and construction, and refrigeration, which is further accelerating the vacuum insulation panel market outlook.

Vacuum Insulation Panel Market Trends:

Surging awareness regarding sustainable building practices

Growing awareness and integration of sustainable building practices are driving the global vacuum insulation panel market. Due to their superior thermal insulation properties, VIPs are increasingly being preferred in the construction industry to allow buildings to comply with higher energy efficiency standards. Global concern for long-term sustainability ensures policies and projects aimed at promoting energy-efficient construction drive the market for vacuum insulation panels all over the world. By using these panels, energy consumption in heating and cooling is also reduced, which translates to lower carbon emissions. As a result, in an effort to achieve green building certification and comply with strict environmental regulations, architects, builders, and developers are embracing these materials.

To get more information on this market Request Sample

Stringent government regulations

As per the vacuum insulation panel market overview, governments and international bodies have enforced stringent regulation and energy efficiency standards that have significantly supported the growth of our global market over the last several years. Given the increasing concern over greenhouse gas emissions and mitigating climate change, the energy efficiency of buildings, appliances, and industrial processes is at a premium. VIPs are one of the few materials capable of meeting these stringent standards because of their thermal insulation capabilities. Governments around the world have initiated initiatives for promoting adoption of energy efficient technologies, including VIPs, in several sectors, including construction, refrigeration, and transportation.

Burgeoning advancement in technology

Advancements in manufacturing technology support the growth of the global vacuum insulation panel market. Since the first introduction of VIPs in the 20th century, manufacturing techniques and materials have significantly evolved to enhance panel performance, durability, and affordability. Advanced manufacturing procedures, including vacuum sealing, core material and barrier film selection, have allowed producers to manufacture VIPs with an increased thermal profile while concurrently decreasing their thickness. Both factors have driven their increased prevalence in various sectors. In addition, manufacturing economies of scale and automation have lowered overall VIP expenses and rendered them competitive with traditional insulation materials.

Vacuum Insulation Panel Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional and country levels for 2026-2034. Our report has categorized the market based on the type, raw material, core material, and application.

Breakup by Type:

- Flat Panel

- Special Shape Panel

Flat panel accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the type. This includes flat panel and special shape panel. According to the report, flat panel represented the largest segment.

The flat panel segment is driven by the increasing demand for sleek, space-saving display solutions across various industries, including consumer electronics, automotive, healthcare, and retail. Consumers are increasingly gravitating towards flat panel displays due to their slim profiles, lightweight design, and superior visual performance, driving manufacturers to innovate and expand their product offerings. Furthermore, advancements in display technologies have revolutionized the flat panel segment, offering enhanced brightness, contrast, and color accuracy, thereby attracting consumers seeking immersive viewing experiences. Additionally, the integration of touch-screen capabilities and interactive features in flat panel displays has spurred their adoption in applications ranging from interactive kiosks and digital signage to smart appliances and automotive infotainment systems. Moreover, the growing trend of remote work and virtual collaboration has fueled the demand for large-format flat panel displays in conference rooms and home offices, driving the market growth. Apart from this, the automotive industry’s emphasis on in-vehicle entertainment and connectivity solutions has propelled the integration of flat panel displays in dashboard systems, rear-seat entertainment, and navigation displays, further expanding the market.

Breakup by Raw Material:

- Plastics

- Metal

The report has provided a detailed breakup and analysis of the market based on the raw material. This includes plastics and metal.

The plastics segment is driven by the increasing demand for lightweight and durable materials across various industries. Plastics offer versatility in applications, ranging from packaging and automotive components to construction materials and consumer goods. The demand for plastics is further propelled by their cost-effectiveness, corrosion resistance, and ability to be molded into complex shapes, catering to diverse end-use requirements. Additionally, technological advancements in polymer chemistry and processing techniques enhance the performance and sustainability of plastics, driving their adoption in new applications and markets.

On the other hand, the metal segment is driven by its inherent strength, durability, and conductivity properties, making it indispensable across multiple sectors. Metals find extensive applications in construction, transportation, electronics, and machinery manufacturing due to their reliability and performance under extreme conditions. The demand for metals is further fueled by urbanization, infrastructure development, and industrialization in emerging economies, driving the need for raw materials in construction projects, automotive production, and industrial machinery.

Breakup by Core Material:

- Silica

- Fiberglass

- Others

Silica accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the core material. This includes silica, fiberglass, and others. According to the report, silica represented the largest segment.

The silica segment is driven by the increasing demand across various industries due to its versatile properties and wide-ranging applications. For instance, in the construction sector, silica finds extensive use in the production of concrete, mortar, and other construction materials due to its ability to enhance strength, durability, and workability. Additionally, silica-based products are crucial in the manufacturing of glass, ceramics, and refractories, catering to the growing demand from the automotive, electronics, and architectural industries. Furthermore, in the chemical industry, silica serves as a key ingredient in the production of various chemicals, including silicones, silicates, and zeolites, supporting diverse applications in adhesives, coatings, and catalysts. Moreover, the healthcare sector relies on silica for pharmaceutical formulations, dental materials, and medical devices, driven by the increasing demand for healthcare products worldwide. Apart from this, the cosmetics and personal care industry utilizes silica in skincare and cosmetic formulations due to its absorbent and mattifying properties.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

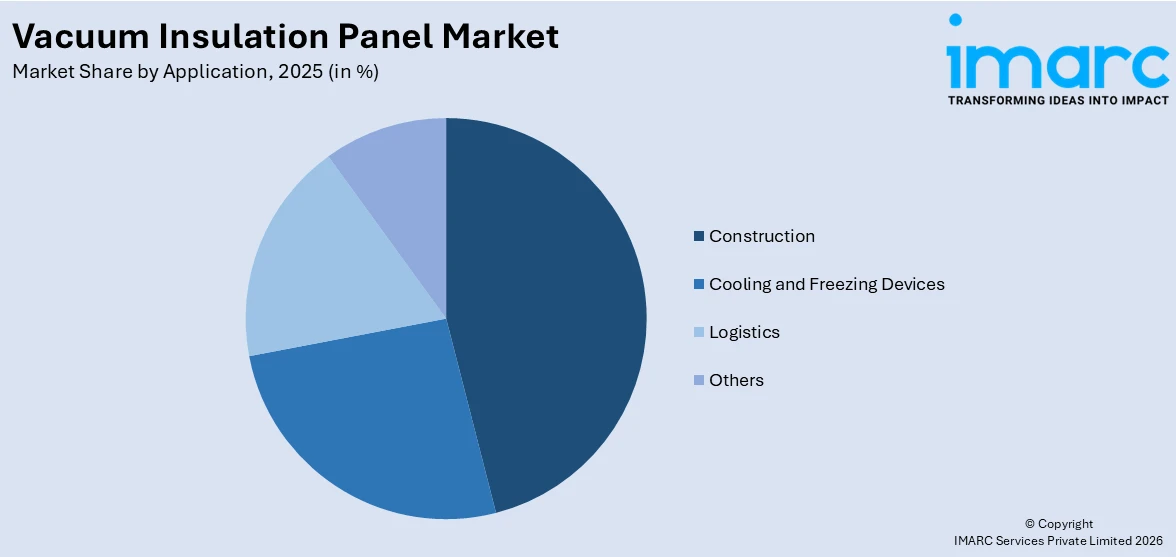

- Construction

- Cooling and Freezing Devices

- Logistics

- Others

Construction accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the application. This includes construction, cooling and freezing devices, logistics, and others. According to the report, construction represented the largest segment.

The construction segment is driven by the increasing emphasis on sustainable building practices, which has propelled the demand for vacuum insulation panels (VIPs). VIPs offer superior thermal insulation properties compared to traditional materials, enabling buildings to achieve higher energy efficiency standards and reduce carbon emissions. Additionally, stringent regulations and green building certifications incentivize architects, builders, and developers to incorporate VIPs into their designs to meet environmental standards. Moreover, the rising awareness of energy conservation and the need for cost-effective solutions contribute to the adoption of VIPs in construction projects. Furthermore, advancements in manufacturing technologies have led to the production of thinner and more efficient VIPs, making them increasingly viable for use in walls, roofs, and floors of both residential and commercial buildings. The durability and longevity of VIPs also appeal to construction stakeholders, as they offer long-term insulation performance without degradation.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific leads the market, accounting for the largest vacuum insulation panel market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific represents the largest regional market for vacuum insulation panels.

The Asia Pacific region is driven by the increasing urbanization and infrastructure development, particularly in emerging economies like China and India, fostering demand for vacuum insulation panels (VIPs) in the construction sector to meet stringent energy efficiency regulations and address sustainability concerns. Additionally, the rapid expansion of the cold chain logistics industry in countries such as Japan, South Korea, and Australia, fueled by the growth of e-commerce and the food and beverage (F&B) sector, boosts the adoption of VIPs in insulated packaging solutions, maintaining product integrity during transit. Moreover, the region's automotive sector's shift towards electric vehicles to combat pollution and reduce reliance on fossil fuels drives the demand for lightweight and efficient insulation materials like VIPs to optimize battery performance and extend driving range. Apart from this, the emphasis on energy conservation and the adoption of green building standards by governments and organizations across the Asia Pacific region propel the integration of VIPs into residential and commercial constructions, stimulating market growth.

Competitive Landscape:

Key players in the vacuum insulation panel (VIP) market are actively engaged in several strategies to strengthen their market position and gain a competitive edge. Companies are investing significantly in research and development to innovate and improve the performance, durability, and cost-effectiveness of VIPs. This includes developing advanced manufacturing techniques, exploring new core materials, and enhancing barrier film technology to produce VIPs with higher thermal resistance and thinner profiles. Moreover, players are focusing on expanding their product portfolios to cater to diverse industry verticals, such as construction, refrigeration, automotive, and packaging. This involves developing customized solutions to meet specific customer requirements and address emerging market trends, such as the growing demand for sustainable building materials and eco-friendly packaging solutions. Additionally, key players are actively pursuing strategic partnerships, collaborations, and acquisitions to broaden their geographic presence, access new markets, and leverage complementary capabilities.

The report provides a comprehensive analysis of the competitive landscape in the global vacuum insulation panel market with detailed profiles of all major companies, including:

- Avery Dennison Corporation

- Etex Group

- Kingspan Group

- Knauf Insulation

- Morgan Advanced Materials

- Panasonic Corporation of North America

- Recticel Insulation UK

- Turvac Vacuum Insulation

- va-Q-tec Thermal Solutions GmbH

Vacuum Insulation Panel Market News:

- In 2023: Kingspan Group plc announced the launch of a new range of vacuum insulation panels (VIPs) designed specifically for the construction industry. These VIPs boast enhanced thermal performance and durability, catering to the increasing demand for sustainable building materials.

- In March 2023: Hutchinsonand va-Q-tec, pioneer of highly efficient vacuum insulation panels (VIPs), announced their partnership. The aim of this strategic partnership is to jointly develop high-performance, scalable insulation solutions to improve the thermal management of eMobility vehicles.

Vacuum Insulation Panel Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Flat Panel, Special Shape Panel |

| Raw Materials Covered | Plastics, Metal |

| Core Materials Covered | Silica, Fiberglass, Others |

| Applications Covered | Construction, Cooling and Freezing Devices, Logistics, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Avery Dennison Corporation, Etex Group, Kingspan Group, Knauf Insulation, Morgan Advanced Materials, Panasonic Corporation of North America, Recticel Insulation UK, Turvac Vacuum Insulation, va-Q-tec Thermal Solutions GmbH, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the vacuum insulation panel market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global vacuum insulation panel market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the vacuum insulation panel industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Vacuum Insulation Panel Market Report

The global vacuum insulation panel market was valued at USD 9.9 Billion in 2025.

We expect the global vacuum insulation panel market to exhibit a CAGR of 3.91% during 2026-2034.

The widespread utilization of vacuum insulation panels in detached houses, apartment buildings, nurseries, office buildings, etc., is primarily driving the global vacuum insulation panel market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations resulting in temporary closure of numerous end use industries, thereby negatively impacting the demand for vacuum insulation panel.

Based on the type, the global vacuum insulation panel market can be categorized into flat panel and special shape panel, where flat panel exhibits the clear dominance in the market.

Based on the core material, the global vacuum insulation panel market has been segmented into silica, fiberglass, and others. Currently, silica represents the largest market share.

Based on the application, the global vacuum insulation panel market can be bifurcated into construction, cooling and freezing devices, logistics, and others. Among these, the construction sector accounts for the majority of the total market share.

On a regional level, the market has been classified into North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America, where Asia-Pacific currently dominates the global market.

Some of the major players in the global vacuum insulation panel market include Avery Dennison Corporation, Etex Group, Kingspan Group, Knauf Insulation, Morgan Advanced Materials, Panasonic Corporation of North America, Recticel Insulation UK, Turvac Vacuum Insulation, and va-Q-tec Thermal Solutions GmbH.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)