Vegetable Seed Market Size, Share, Trends and Forecast by Type, Crop Type, Cultivation Method, Seed Type, and Region, 2026-2034

Vegetable Seed Market Size, Share, Trends & Forecast (2026-2034)

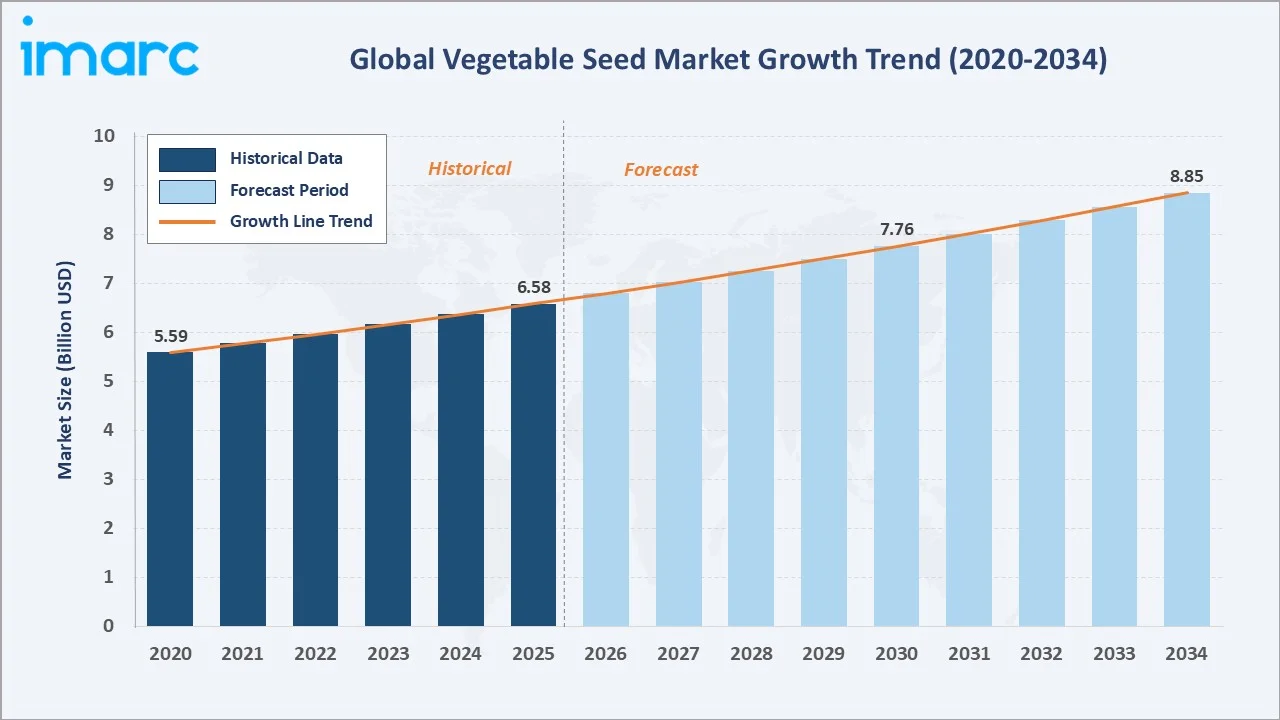

The global vegetable seed market reached USD 6.58 Billion in 2025 and is projected to reach USD 8.85 Billion by 2034, growing at a CAGR of 3.34% during 2026-2034. The market is driven by rising demand for high-yielding, disease-resistant seed varieties, expanding food security imperatives, and advancements in precision breeding technology.

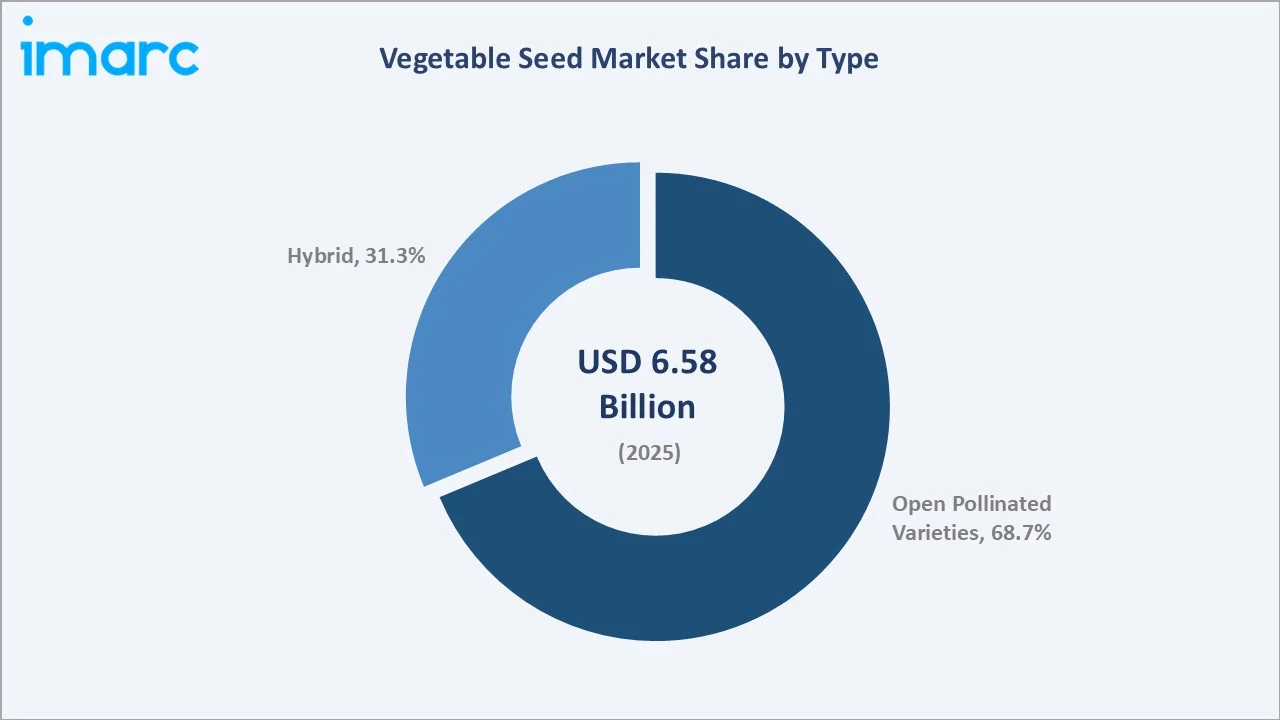

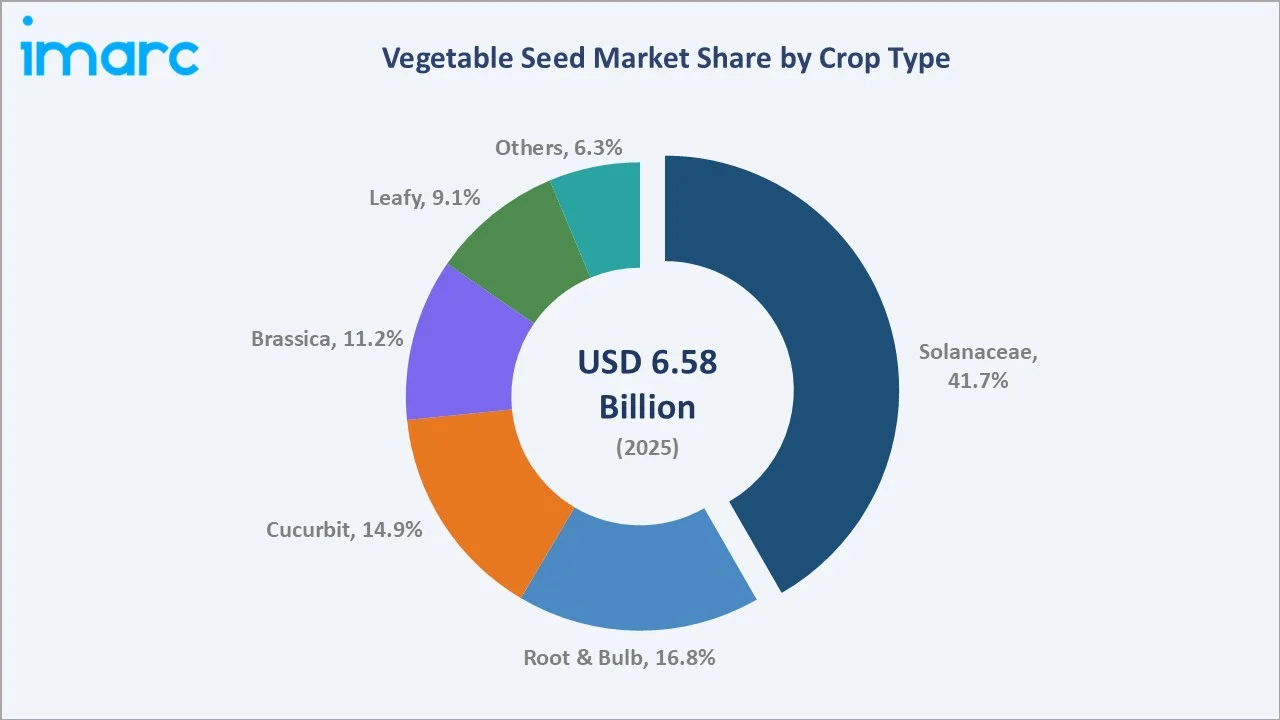

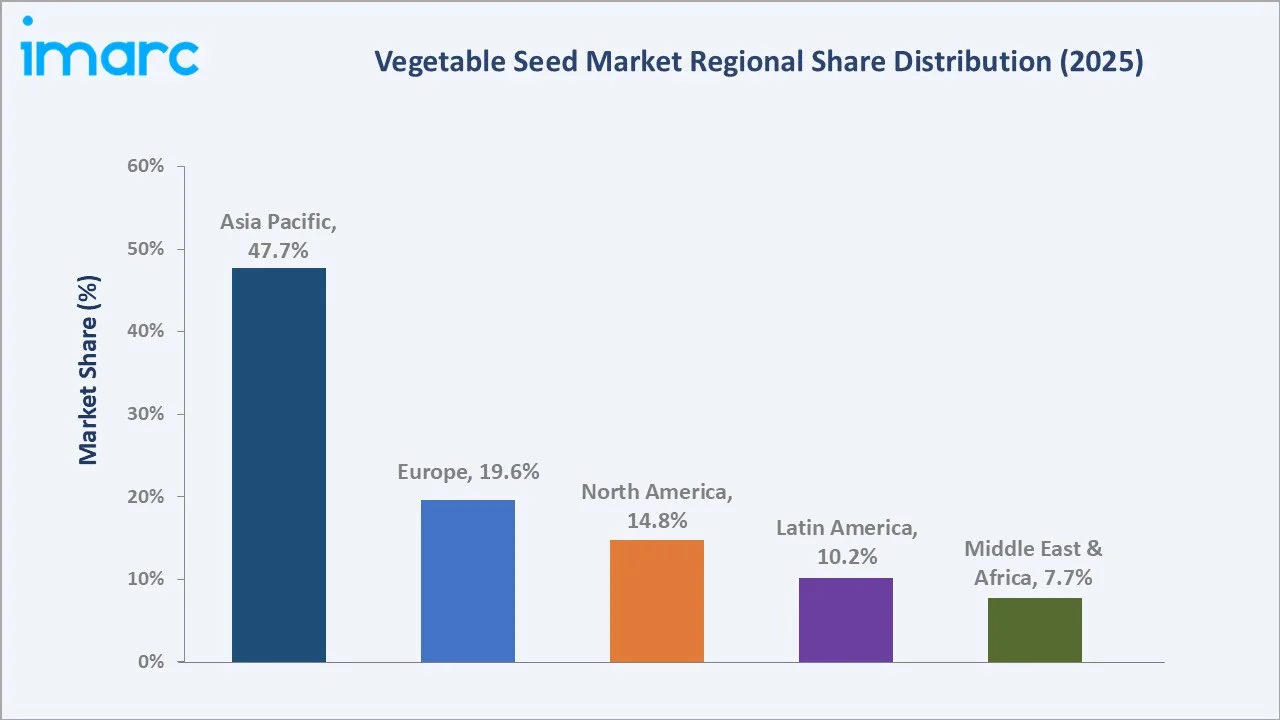

Open Pollinated Varieties dominate at 68.7%. Solanaceae leads crop type at 41.7%. Asia Pacific commands 47.7% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.58 Billion |

|

Forecast Market Size (2034) |

USD 8.85 Billion |

|

CAGR (2026-2034) |

3.34% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Open Pollinated Varieties (68.7%, 2025) |

|

Dominant Crop Type |

Solanaceae (41.7%, 2025) |

|

Leading Region |

Asia Pacific (47.7%, 2025) |

The market expanded from USD 5.59 Billion in 2020 to USD 6.58 Billion in 2025, anchored at USD 7.76 Billion in 2030 and forecast to reach USD 8.85 Billion by 2034. Growing farmer awareness of hybrid seed benefits and rising adoption of biotech-enhanced varieties sustained steady growth throughout the historical period and continues to support the forecast trajectory.

To get more information on this market, Request Sample

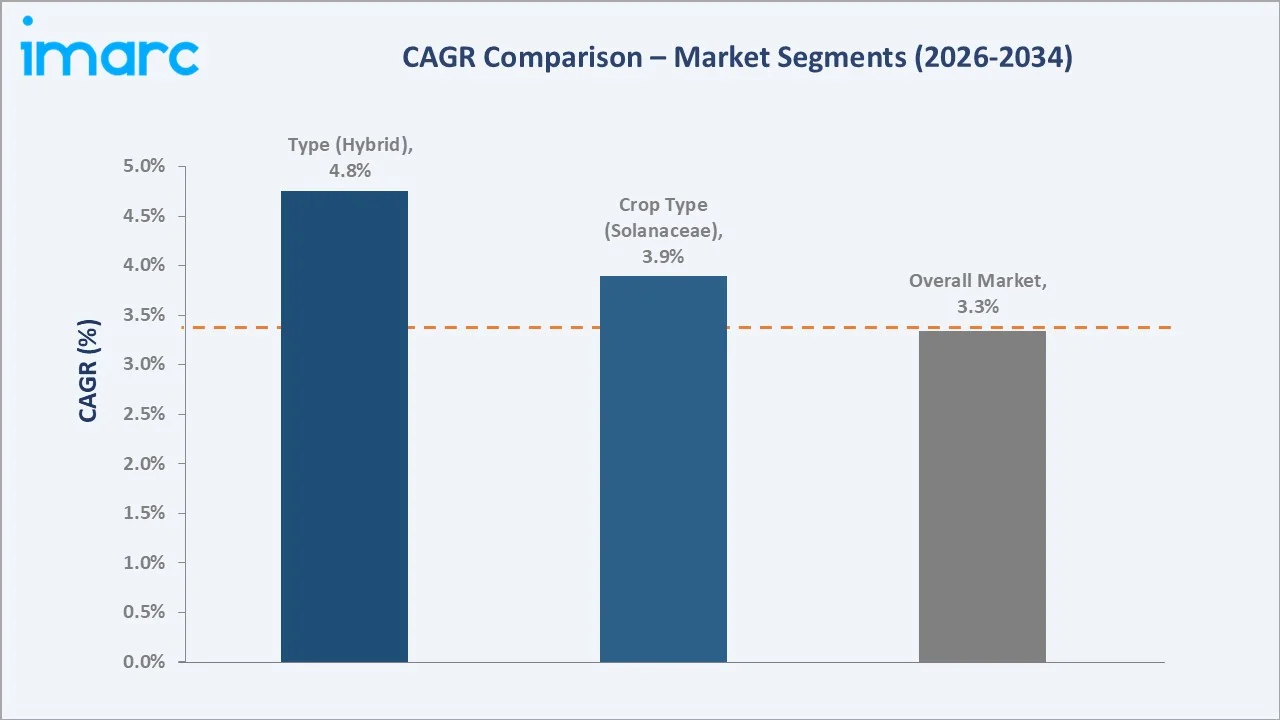

The Hybrid type segment is projected to grow at ~4.75% CAGR, outpacing Open Pollinated Varieties (~2.65% CAGR), as commercial farms intensify adoption for yield premiums. Solanaceae leads segment growth at ~3.90% CAGR, driven by global tomato and pepper demand expansion across fresh produce and food processing industries.

Executive Summary

The global vegetable seed market reached USD 6.58 Billion in 2025 and represents a foundational segment of the global agricultural ecosystem, underpinning food security, crop diversity, and commercial farming at scale. The market is projected to reach USD 8.85 Billion by 2034, driven by population growth, dietary evolution, and continuous seed technology innovation across all major vegetable crop categories.

Open Pollinated Varieties at 68.7% dominate through widespread farmer acceptance in smallholder-driven economies. Solanaceae at 41.7% leads crop type through the global commercial importance of tomatoes, peppers, and eggplants. Asia Pacific at 47.7% leads globally through its vast agricultural base, government seed modernization programs, and rapid hybrid adoption across China, India, and Southeast Asia.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Open Pollinated Varieties – 68.7% share (2025) |

|

Dominant Crop Type |

Solanaceae – 41.7% market share (2025) |

|

Leading Region |

Asia Pacific – 47.7% market share (2025) |

|

Market Opportunity |

Hybrid seed innovation; precision breeding; climate-resilient varieties; organic seed expansion; biofortification |

Key Analytical Observations Supporting the Above Data:

- Open Pollinated Varieties at 68.7%: Open pollinated varieties dominate as they are cost-accessible, seed-saving compatible, and deeply embedded in traditional farming systems across Asia, Africa, and Latin America. Their adaptability to local conditions and low input costs sustain farmer preference in smallholder-dominant agricultural economies globally.

- Solanaceae at 41.7%: Solanaceae leads as tomatoes, peppers, and eggplants are among the most globally cultivated and commercially valuable vegetables, with high per-unit seed value and strong demand from fresh produce and food processing industries, driving sustained procurement across all geographies.

- Asia Pacific at 47.7%: Asia Pacific commands the highest share through its vast agricultural base, dense rural farming population, rapid adoption of improved seed varieties, and strong government investment in agricultural productivity across China, India, Southeast Asia, and Japan.

Vegetable Seed Market Overview

The global vegetable seed market encompasses the research, development, production, and commercial distribution of seeds used for cultivating all major vegetable crops worldwide. The ecosystem integrates seed breeding companies, biotechnology firms, agri-input distributors, contract seed growers, regulatory certification bodies, and end farmers across all cultivation systems.

Macroeconomic drivers include population growth, urbanization, rising dietary preference for fresh vegetables, and increasing demand for processed vegetable products. Climate change is creating new demand for stress-tolerant and climate-adaptive seed varieties. Government food security programs and agricultural subsidies are incentivizing seed sector investment across emerging markets globally.

Market Dynamics

To evaluate market opportunities, Request Sample

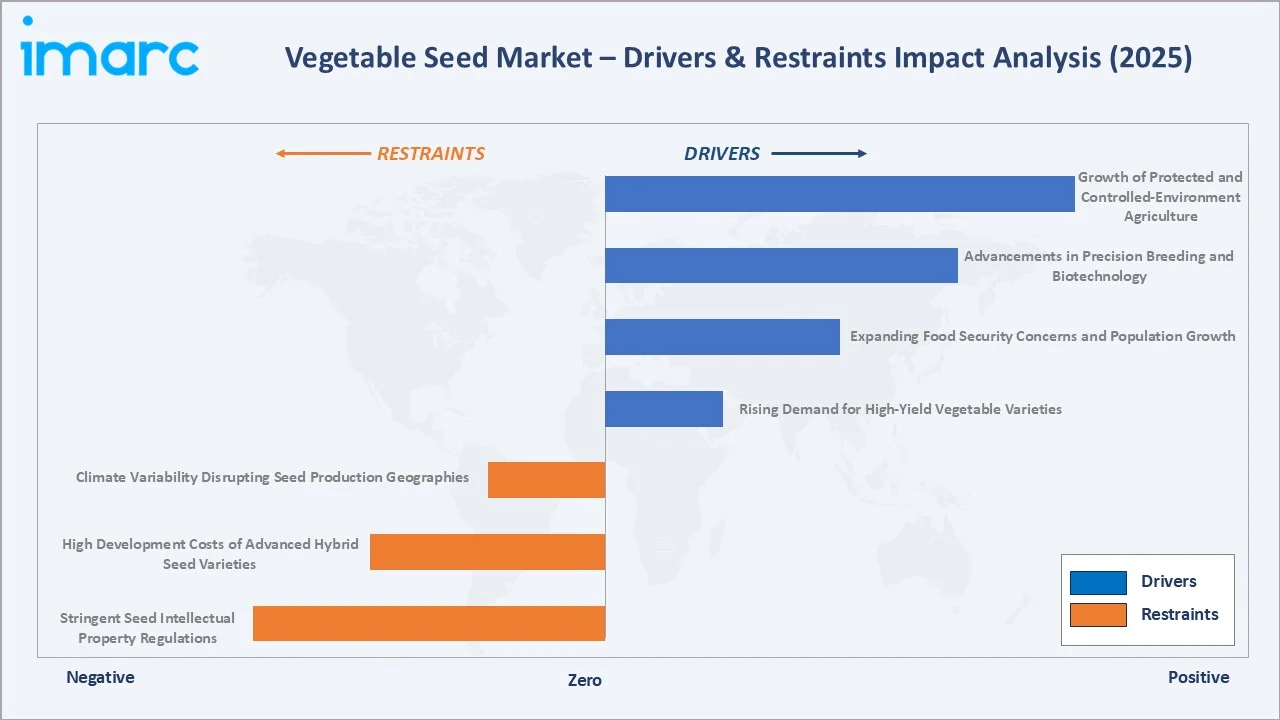

Market Drivers

- Rising Demand for High-Yield Vegetable Varieties: Growing farmer awareness about yield optimization is accelerating adoption of improved vegetable seeds. High-yielding hybrid varieties offering disease resistance, climate adaptability, and uniform produce quality are commanding premium procurement across commercial farms. Hybrid seeds offer up to 30% higher yields versus conventional open-pollinated varieties, directly driving market revenue growth.

- Expanding Food Security Concerns and Population Growth: Rising global population, projected to exceed 9.7 billion by 2050, is intensifying food production pressure. Governments and agri-input companies are investing in advanced vegetable seed development to increase crop productivity per unit area, directly driving procurement of high-performance seed varieties across Solanaceae, Cucurbit, and Brassica crop categories globally.

- Advancements in Precision Breeding and Biotechnology: Precision breeding technologies including CRISPR, marker-assisted selection, and genomic sequencing are enabling faster development of disease-resistant and climate-resilient vegetable seed varieties. These innovations reduce R&D timelines by 30-40% and expand commercially viable seed portfolios, attracting investment and broadening market growth opportunities across all major vegetable crop categories.

- Growth of Protected and Controlled-Environment Agriculture: Rapid expansion of greenhouse, hydroponic, and controlled-environment farming is creating structured demand for specialized vegetable seeds optimized for indoor cultivation. Protected agriculture requires seeds with uniform germination and high productivity under artificial conditions, supporting premium seed segment expansion across Europe, North America, and East Asia.

Market Restraints

- Stringent Seed Intellectual Property Regulations: Complex IP frameworks, patent restrictions, and variety protection laws governing hybrid and biotech-derived seeds create compliance burdens. These regulations limit farmer seed-saving practices and increase procurement dependency, potentially constraining adoption of improved varieties in cost-sensitive smallholder markets across Asia and Africa.

- High Development Costs of Advanced Hybrid Seed Varieties: Developing commercial hybrid vegetable seed varieties requires substantial multi-year investment in breeding programs, field trials, quality testing, and regulatory approvals. High R&D expenditure translates into elevated seed prices, limiting adoption rates among smallholder farmers in price-sensitive emerging markets globally.

- Climate Variability Disrupting Seed Production Geographies: Irregular rainfall, temperature extremes, and unpredictable growing seasons are disrupting traditional seed production regions. Seed yield losses and quality degradation from climate stress increase production costs and create supply volatility, presenting procurement challenges for seed companies and commercial buyers dependent on consistent annual seed supply.

Market Opportunities

- Biofortified and Nutritionally Enhanced Seed Development: Growing consumer demand for nutritionally dense vegetables is creating commercial opportunities for biofortified seed varieties with enhanced vitamin, mineral, and antioxidant profiles. Biofortified vegetable seeds command premium pricing and attract institutional procurement from government food security programs, particularly across Sub-Saharan Africa and South Asia.

- Organic and Non-GMO Seed Market Expansion: Rising consumer preference for organic and non-GMO produce is stimulating dedicated organic vegetable seed market expansion. Specialty seed companies serving organic farming segments are achieving above-market growth rates as retail demand for certified organic vegetables intensifies across North America and European markets.

Market Challenges

-

- Counterfeit and Low-Quality Seed Proliferation in Developing Markets: Widespread circulation of counterfeit, mislabelled, and substandard seeds in developing markets undermines farmer trust in commercial seed products. Quality control failures reduce adoption of improved varieties and damage brand equity for genuine seed manufacturers, requiring increased regulatory enforcement investment across South Asia and Sub-Saharan Africa.

- Supply Chain Complexity in Cross-Border Seed Distribution: International seed trade involves complex phytosanitary certifications, quarantine requirements, and import/export regulations that vary significantly by country. Compliance complexity increases logistics costs and delays market access for new varieties, particularly for smaller companies entering high-growth emerging markets.

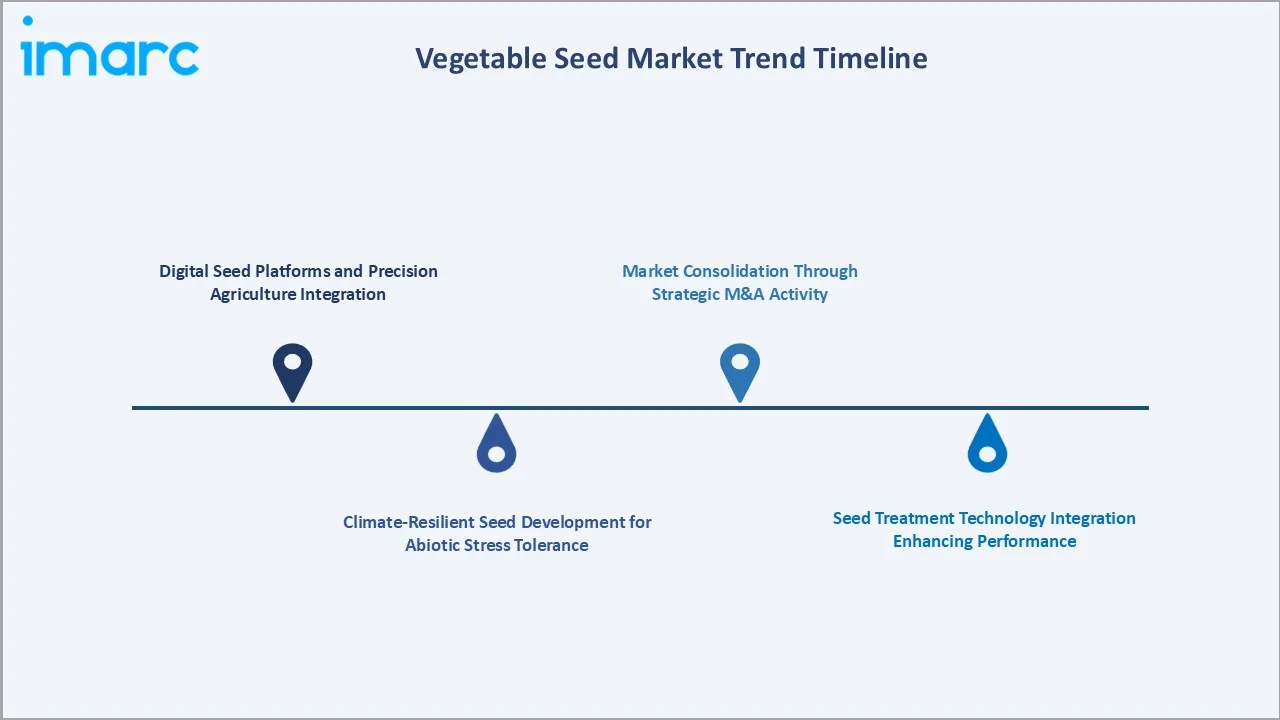

Emerging Market Trends

1. Digital Seed Platforms and Precision Agriculture Integration

Digital platforms connecting seed companies directly with farmers are transforming seed procurement and advisory services. AI-powered crop management tools integrated with seed variety databases enable precision planting recommendations, improving adoption of high-performance seed varieties and building direct commercial relationships between manufacturers and farmers.

2. Climate-Resilient Seed Development for Abiotic Stress Tolerance

Accelerating climate variability is driving focused investment in heat-tolerant, drought-resistant, and flood-adapted vegetable seed varieties. Breeding programs are prioritizing stress resilience traits, creating new commercial categories of climate-adaptive seeds commanding premium pricing and institutional procurement contracts from government food security programs globally.

3. Seed Treatment Technology Integration Enhancing Performance

Advanced seed treatment technologies, including biological coatings, priming treatments, and micronutrient enrichment, are being integrated with commercial vegetable seed products. Treated seeds offer superior germination rates, pest protection, and early establishment advantages, increasing per-unit value and supporting farmer yield improvements across diverse agro-climatic conditions.

4. Market Consolidation Through Strategic M&A Activity

Strategic acquisitions are reshaping competitive dynamics as major agrochemical companies acquire specialty vegetable seed firms to expand product portfolios and geographical reach. Consolidation is particularly active in Asia Pacific and African markets where smallholder seed modernization is accelerating, and distribution network ownership provides sustainable competitive advantages.

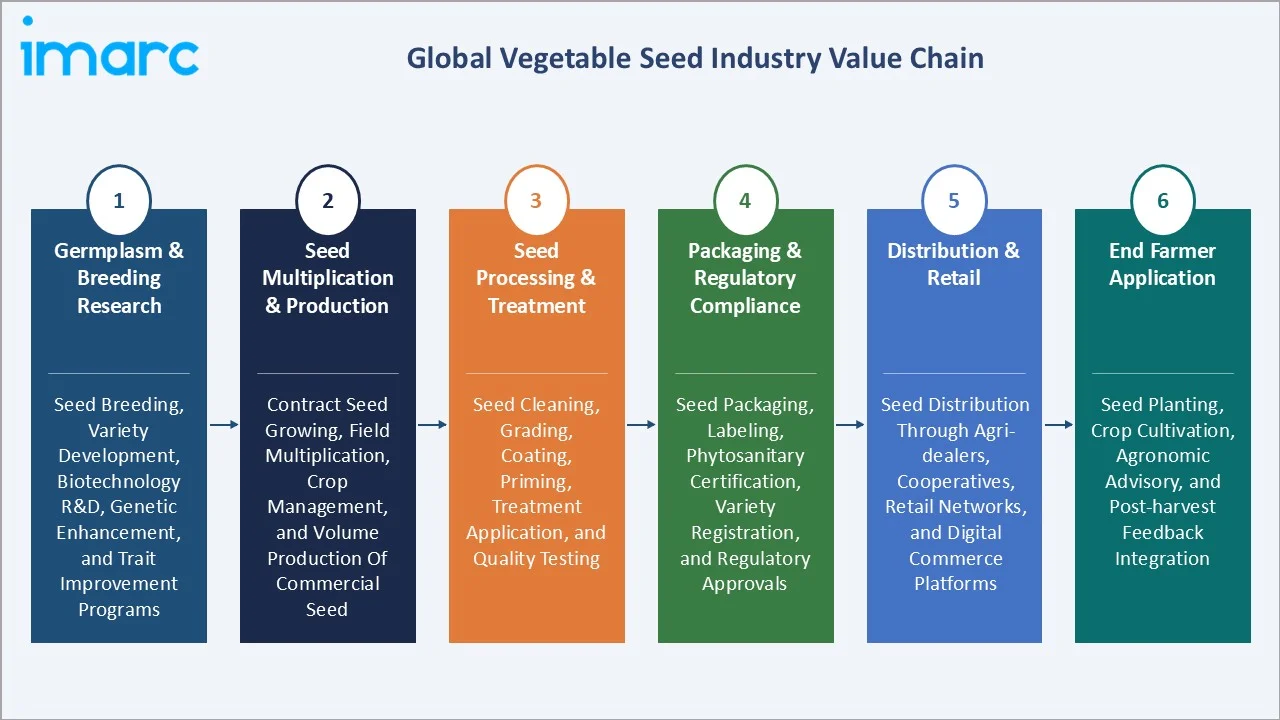

Industry Value Chain Analysis

The vegetable seed value chain integrates germplasm sourcing, breeding research, seed multiplication, processing and treatment, distribution, and end-farmer application. Commercial consolidation is progressively integrating upstream breeding with digital agri-services as the primary commercial format, replacing the former segmented structure between breeding, processing, and distribution stages.

|

Stage |

Key Activities |

|

Germplasm & Breeding Research |

Seed breeding, variety development, biotechnology R&D, genetic enhancement, and trait improvement programs |

|

Seed Multiplication & Production |

Contract seed growing, field multiplication, crop management, and volume production of commercial seed |

|

Seed Processing & Treatment |

Seed cleaning, grading, coating, priming, treatment application, and quality testing |

|

Packaging & Regulatory Compliance |

Seed packaging, labeling, phytosanitary certification, variety registration, and regulatory approvals |

|

Distribution & Retail |

Seed distribution through agri-dealers, cooperatives, retail networks, and digital commerce platforms |

|

End Farmer Application |

Seed planting, crop cultivation, agronomic advisory, and post-harvest feedback integration |

The germplasm and breeding research tier is the vegetable seed value chain's most strategically critical stage, with seed company IP portfolios representing the primary commercial differentiator. The distribution tier is experiencing the most rapid transformation as digital platforms and e-commerce channels disrupt traditional agri-dealer networks across emerging markets.

Technology Landscape in the Vegetable Seed Industry

Hybrid Seed Technology

Hybrid seed technology produces superior commercial varieties through controlled cross-pollination of distinct parent lines, delivering heterosis advantages including higher yield, disease resistance, and uniformity. Hybrid vegetable seeds command premium market pricing and represent the highest-value commercial seed category, with growing adoption particularly among Solanaceae and Cucurbit crop producers globally.

Marker-Assisted Selection (MAS)

Marker-assisted selection accelerates vegetable seed breeding by enabling genetic screening for desired traits at the DNA level, reducing multi-year field trial dependency. MAS-developed varieties deliver faster commercial pipeline times and more precise trait combinations, improving R&D efficiency and variety performance while reducing per-variety development costs for leading seed companies globally.

CRISPR Gene Editing in Vegetable Seed Development

CRISPR-based gene editing enables precise modification of vegetable seed genomes to introduce disease resistance, nutritional enhancement, and climate resilience traits. In 2025, multiple regulatory jurisdictions advanced CRISPR seed product approvals, creating new commercial pathways for next-generation precision-bred vegetable seed varieties across Solanaceae and leafy vegetable categories.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Open Pollinated Varieties |

68.7% |

2025 |

|

Crop Type |

Solanaceae |

41.7% |

2025 |

|

Cultivation Method |

🔒 |

🔒 |

2025 |

|

Seed Type |

🔒 |

🔒 |

2025 |

|

Region |

Asia Pacific |

47.7% |

2025 |

By Type

Open Pollinated Varieties dominate at 68.7% in 2025, maintaining widespread adoption through affordability, seed-saving compatibility, and proven performance across diverse agro-climatic conditions. OPV dominance is particularly strong in Asia Pacific and Africa, where smallholder farmers represent the largest procurement base and cost-accessibility drives variety selection decisions.

To access detailed market analysis, Request Sample

Hybrid seeds at 31.3% represent the market's highest-growth segment at ~4.75% CAGR, driven by commercial farms' demand for uniform, high-yield produce. Hybrid adoption is accelerating across Solanaceae crops, particularly processing tomatoes, where yield premiums justify higher seed investment for large-scale commercial growers across North America and Europe.

By Crop Type

Solanaceae leads at 41.7% in 2025, encompassing tomatoes, peppers, and eggplants, which are among the most globally cultivated and commercially valuable vegetables. Their high per-unit seed value, global processing industry demand, and broad cultivar diversity across open-field and greenhouse production systems maintain segment leadership through the forecast period.

Root & Bulb crops at 16.8% include onions, carrots, and beets, supported by consistent global demand and expanding processed food applications. Cucurbit at 14.9% captures cucumber, melon, and squash cultivation. Brassica at 11.2% benefits from rising health-food consumption trends. Leafy vegetables at 9.1% are growing through urban farming and ready-to-eat salad market expansion globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

Asia Pacific |

47.7% |

Driven by large agricultural base, rising food demand, rapid hybrid adoption, and government seed modernization programs |

|

Europe |

19.6% |

Driven by food quality standards, organic seed demand, greenhouse cultivation growth, and biotechnology seed innovation |

|

North America |

14.8% |

Supported by large-scale commercial farming, high hybrid adoption, precision agriculture integration, and organic seed demand |

|

Latin America |

10.2% |

Driven by expanding vegetable export sectors, rising hybrid adoption, and investment in modern seed distribution networks |

|

Middle East and Africa |

7.7% |

Emerging through food security investment, greenhouse expansion, and government-supported seed modernization programs |

Asia Pacific at 47.7% leads through the region's large-scale vegetable production, expanding hybrid seed adoption, and strong government investment in agricultural productivity. Europe at 19.6% reflects robust regulatory infrastructure supporting certified seed markets and innovation-led specialty seed development.

North America at 14.8% reflects large-scale commercial vegetable farming and high hybrid seed penetration. Latin America at 10.2% and Middle East and Africa at 7.7% represent high-growth early-stage markets primarily driven by export-oriented vegetable production investment and government food security procurement programs.

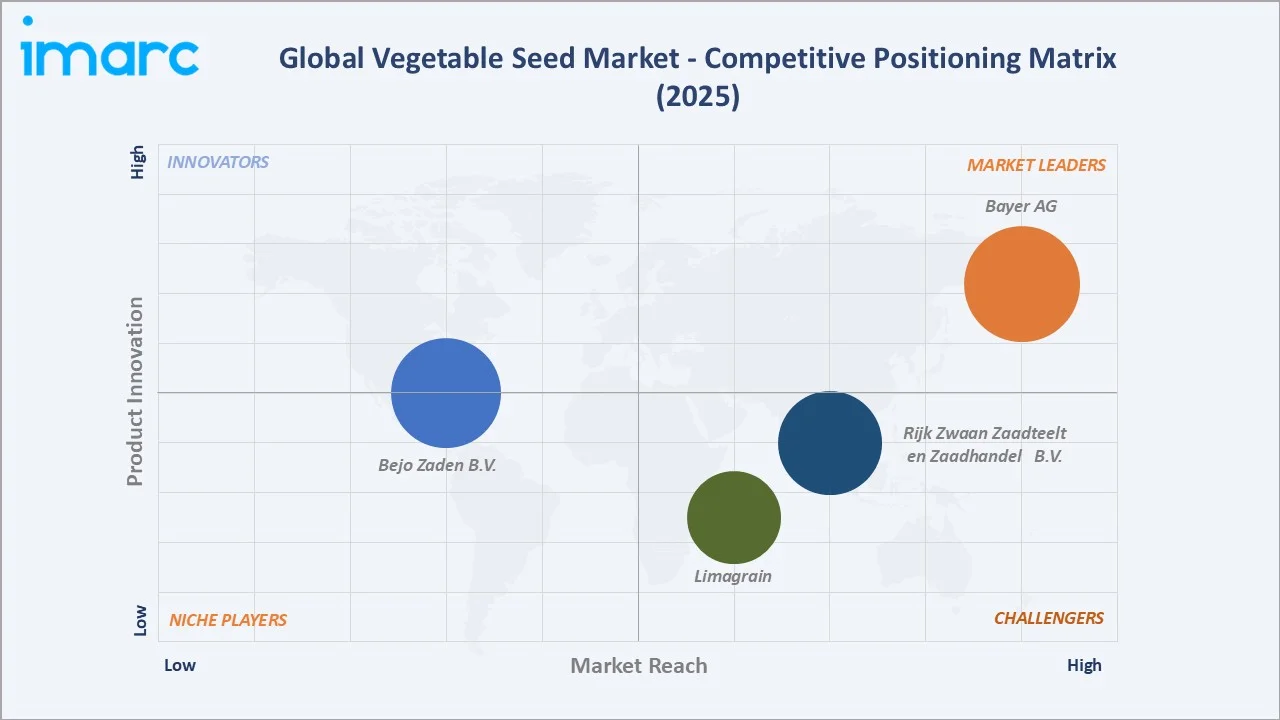

Competitive Landscape

The global vegetable seed market competitive landscape is moderately concentrated with three competitive tiers: global diversified agri-input leaders holding broad IP portfolios, dedicated vegetable seed specialists with deep crop-specific breeding expertise, and regional companies serving local smallholder markets with locally adapted varieties.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Bayer AG |

De Ruiter, Seminis |

Market Leader |

Delivering high-yield vegetable seed solutions across global markets |

|

Limagrain |

Carrot, Tomato, Pumpkins, Lettuce, Beetroot, Eggplant, Broccoli, Brussels sprouts, Cauliflower, Cabbage, Kabocha squash |

Strong Challenger |

Farmer-owned cooperative with specialized breeding and global commercial network |

|

Rijk Zwaan Zaadteelt en Zaadhandel B.V. |

Tomato, lettuce, cucumber, pepper hybrids |

Strong Challenger |

Specialist vegetable seed breeder with strong European roots and global penetration |

|

Bejo Zaden B.V. |

Carrot, onion, cabbage, beet seed varieties |

Established Player |

Root, bulb, and Brassica specialist with dedicated breeding and distribution programs |

Key players include Bayer AG, Limagrain, Rijk Zwaan Zaadteelt en Zaadhandel B.V., Bejo Zaden B.V., and others.

Key Company Profiles

Bayer AG

Bayer AG is a Germany-based global life sciences company with strong vegetable seed market presence, delivering high-performance hybrid seed varieties across Solanaceae, Cucurbit, and root vegetable categories to commercial producers globally.

- Key Products: De Ruiter, Seminis

- Recent Developments: In January 2026, Bayer commenced operations of a new vegetable seeds production center in Khon Kaen, Thailand, reinforcing the company’s presence in Asia and expanding its global vegetable seed supply capabilities. The Khon Kaen hub will supply vegetable seeds under Bayer’s Seminis and De Ruiter brands to key markets across Asia-Pacific and internationally, including the US, Europe, China, Japan, South Korea, Australia, and New Zealand.

- Strategic Focus: Strengthening genomic breeding capabilities and digital farming integration to deliver precision vegetable seed solutions for large-scale commercial producers across Europe, North America, and Asia Pacific markets.

Limagrain

Limagrain is a France-based, farmer-owned agricultural cooperative and global seed group, serving commercial vegetable producers.

- Key Products: Carrot, Tomato, Pumpkins, Lettuce, Beetroot, Eggplant, Broccoli, Brussels sprouts, Cauliflower, Cabbage, Kabocha squash

- Strategic Focus: Expanding hybrid vegetable seed portfolio through precision breeding innovations and deepening direct farmer partnership programs across high-growth markets in Asia, Latin America, and Sub-Saharan Africa.

Market Concentration Analysis

The vegetable seed market is moderately concentrated at the global Tier-1 level, with top 4-5 companies collectively accounting for approximately 45-55% of global commercial vegetable seed revenue. Dedicated specialist seed companies account for an estimated 20-30% of market revenue, with regional and domestic seed companies serving the remaining share predominantly across Asia and Africa. Market concentration is expected to gradually decline as regional companies strengthen breeding capabilities and digital distribution platforms over the forecast period.

Investment & Growth Opportunities

Highest Growth Segments

Hybrid vegetable seed segment (~4.75% CAGR), Solanaceae crop type (~3.90% CAGR), Asia Pacific region (~3.65% CAGR), greenhouse/protected agriculture seeds (~5-6% CAGR), biofortified seed varieties (~6-8% CAGR from smaller base), organic and non-GMO seed segment (~5-7% CAGR), and digital seed advisory integrated products represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Climate-resilient seed development for heat and drought tolerance represents the vegetable seed market's most strategically critical emerging investment priority. Seeds combining yield performance with abiotic stress tolerance are commanding increasing institutional procurement from food security programs in South Asia, Sub-Saharan Africa, and the Middle East, creating structurally growing demand pools through 2034.

Investment Themes

- Precision breeding technology investment for accelerated hybrid variety development: Genomic selection and high-throughput phenotyping investments can reduce commercial variety development timelines by 30-40%, creating sustainable competitive advantages for seed companies capable of faster innovation cycles to meet shifting farmer and climate demands.

- Tropical and subtropical market seed portfolio expansion: Asia Pacific and Sub-Saharan Africa smallholder vegetable market growth represents the vegetable seed industry's largest addressable expansion opportunity, requiring localized breeding for tropical crop types, distribution network investment, and farmer extension program development.

Future Market Outlook (2026-2034)

The global vegetable seed market is projected to grow from USD 6.58 Billion in 2025 to USD 8.85 Billion by 2034, delivering a 3.34% CAGR across the forecast period. The market's anchor value of approximately USD 7.76 Billion in 2030 reflects steady structural demand growth driven by population expansion, dietary shifts toward fresh vegetables, and continuous seed technology advancement globally.

Hybrid seed adoption will progressively increase its market share from 31.3% in 2025 toward 38-40% by 2034 as commercial farming scale intensifies and precision breeding reduces hybrid seed pricing premiums. Digital seed platforms will become integrated commercial channels, reshaping seed distribution and farmer advisory relationships across emerging markets.

Three structural forces define vegetable seed market growth through 2034. Population-driven food demand creates compounding procurement needs for higher-yield seed varieties. Urbanization and dietary shift toward vegetables expand per-capita consumption, driving crop volume growth. Climate change accelerates investment in stress-resilient seed innovation delivering premium commercial returns globally through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including senior seed company executives, commercial vegetable farm operators, agri-input distributors, seed industry regulatory specialists, and precision breeding technology researchers across key markets in Asia, Europe, and North America.

Secondary Research

Secondary research encompassed company annual reports; FAO agricultural production databases; OECD-FAO Agricultural Outlook 2025-2034; seed industry association publications; government agricultural ministry seed sector reports; and academic journals on plant breeding and agricultural biotechnology.

Forecasting Models

Market revenue forecasts developed using crop area-based bottom-up model: (i) global vegetable crop area forecast by crop type; (ii) seed application rate per hectare by crop category; (iii) average seed value per hectare by variety type; (iv) technology premium adjustment for treated and biofortified seed pricing through 2034.

Vegetable Seed Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Open Pollinated Varieties, Hybrid |

| Crop Types Covered | Solanaceae, Root & Bulb, Cucurbit, Brassica, Leafy, Others |

| Cultivation Methods Covered | Protected, Open Field |

| Seed Types Covered | Conventional, Genetically Modified Seeds |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Bayer AG, Limagrain, Rijk Zwaan Zaadteelt en Zaadhandel B.V., Bejo Zaden B.V., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the vegetable seed market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global vegetable seed market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the vegetable seed industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Vegetable Seed Market Report

The global vegetable seed market reached USD 6.58 Billion in 2025, with Open Pollinated Varieties dominating at 68.7%, Solanaceae leading crop type at 41.7%, and Asia Pacific commanding 47.7% global share through the region's large agricultural base and rapid hybrid adoption.

The vegetable seed market grows at 3.34% CAGR during 2026-2034, reaching USD 8.85 Billion by 2034. Growth reflects hybrid adoption expansion, climate-resilient variety demand, precision breeding advancements, and rising vegetable consumption driven by global population growth and dietary evolution.

Open Pollinated Varieties lead at 68.7%, capturing smallholder-dominated markets through cost-accessibility, seed-saving compatibility, and adaptability to local agro-climatic conditions across Asia, Africa, and Latin America.

Solanaceae leads at 41.7% through the global commercial importance of tomatoes, peppers, and eggplants. High per-unit seed value, processing industry demand, and cultivar diversity across growing systems maintain Solanaceae's dominant position through 2034.

Asia Pacific leads at 47.7% through large-scale vegetable cultivation, expanding hybrid adoption, and strong government investment in agricultural productivity across China, India, and Southeast Asia.

Leading companies include Bayer AG, Limagrain, Rijk Zwaan Zaadteelt en Zaadhandel B.V., and Bejo Zaden B.V., among others.

The vegetable seed market is projected to reach approximately USD 7.76 Billion by 2030, with hybrid seed adoption accelerating, climate-resilient varieties entering mainstream commercial use, and Asia Pacific consolidating regional market leadership.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)