Vehicle Recycling Market Size, Share, Trends and Forecast by Type, Material, Application and Region, 2026-2034

Global Vehicle Recycling Market Size, Share, Trends & Forecast (2026-2034)

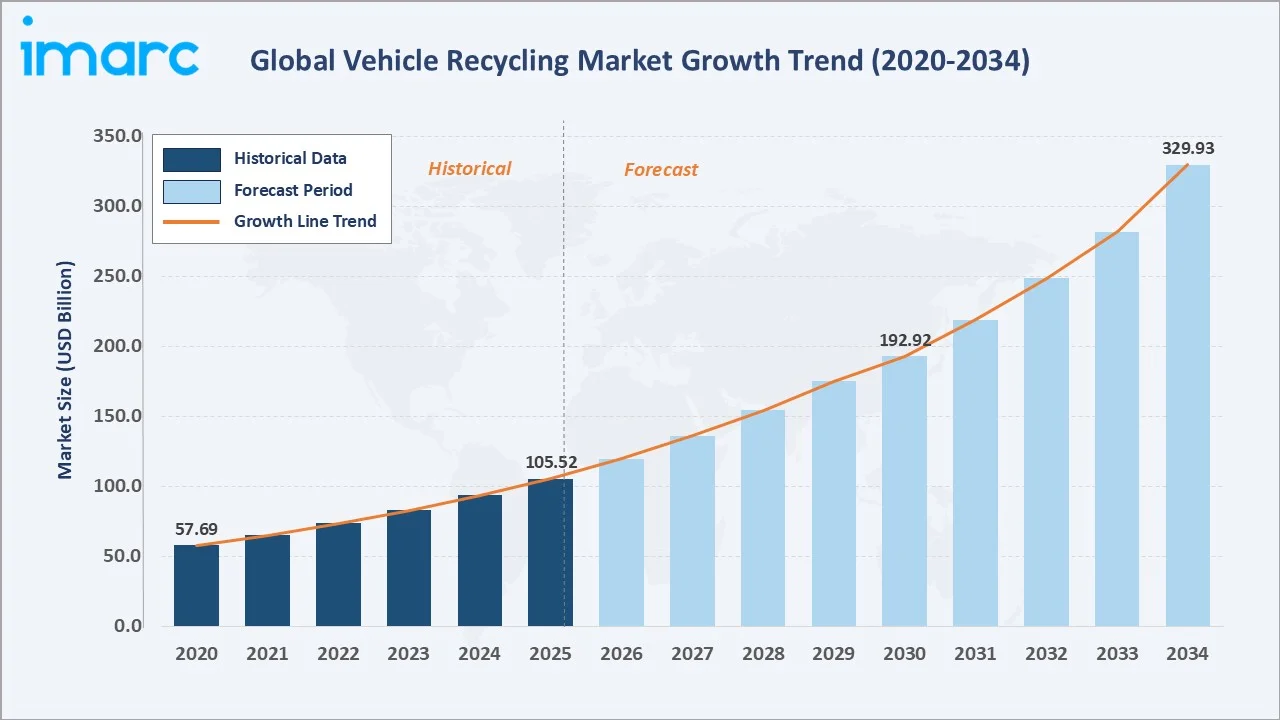

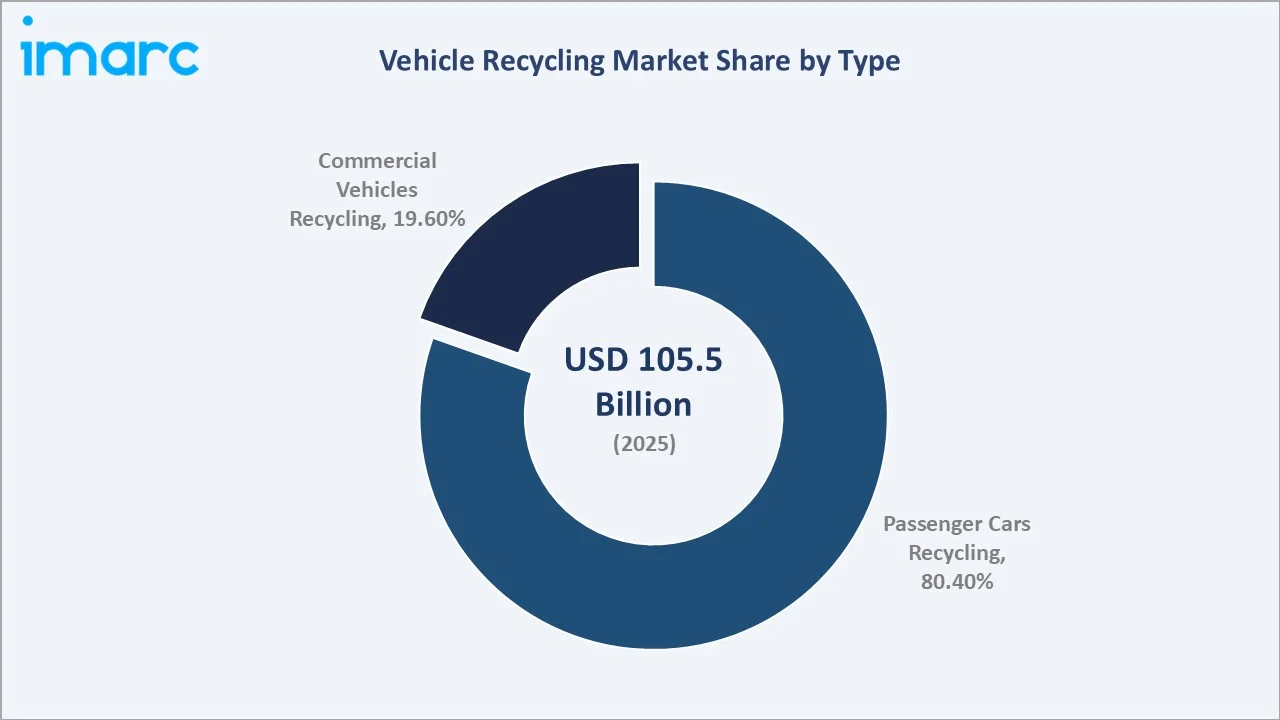

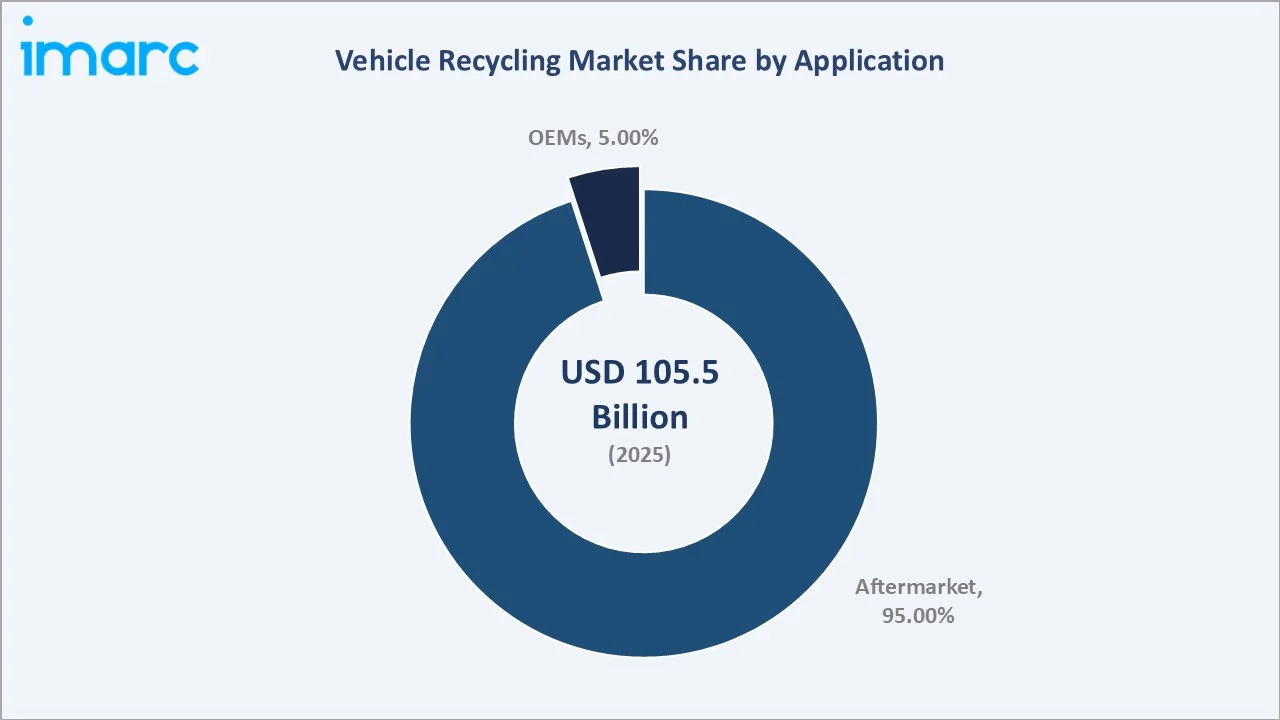

The global vehicle recycling market was valued at USD 105.5 Billion in 2025 and is projected to reach USD 329.9 Billion by 2034, expanding at a CAGR of 12.83% during the forecast period. Growth is driven by rapid industrialization, stringent end-of-life vehicle (ELV) regulations, and widespread adoption of recycled steel and aluminum in vehicle manufacturing.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 105.5 Billion |

|

Forecast Market Size (2034) |

USD 329.9 Billion |

|

CAGR (2026-2034) |

12.83% |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Largest Segment (Type) |

Passenger Cars Recycling - 80.4% (2025) |

|

Largest Segment (Application) |

Aftermarket - 95.1% (2025) |

|

Largest Region |

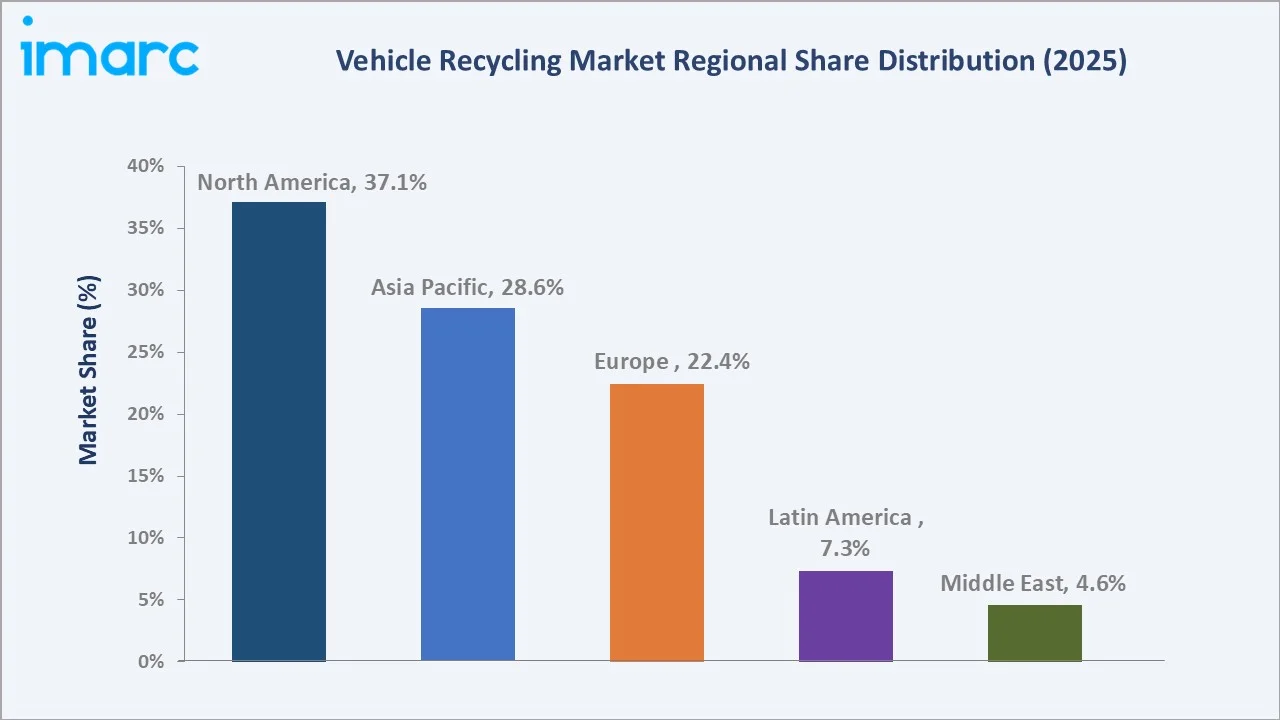

North America - 37.1% (2025) |

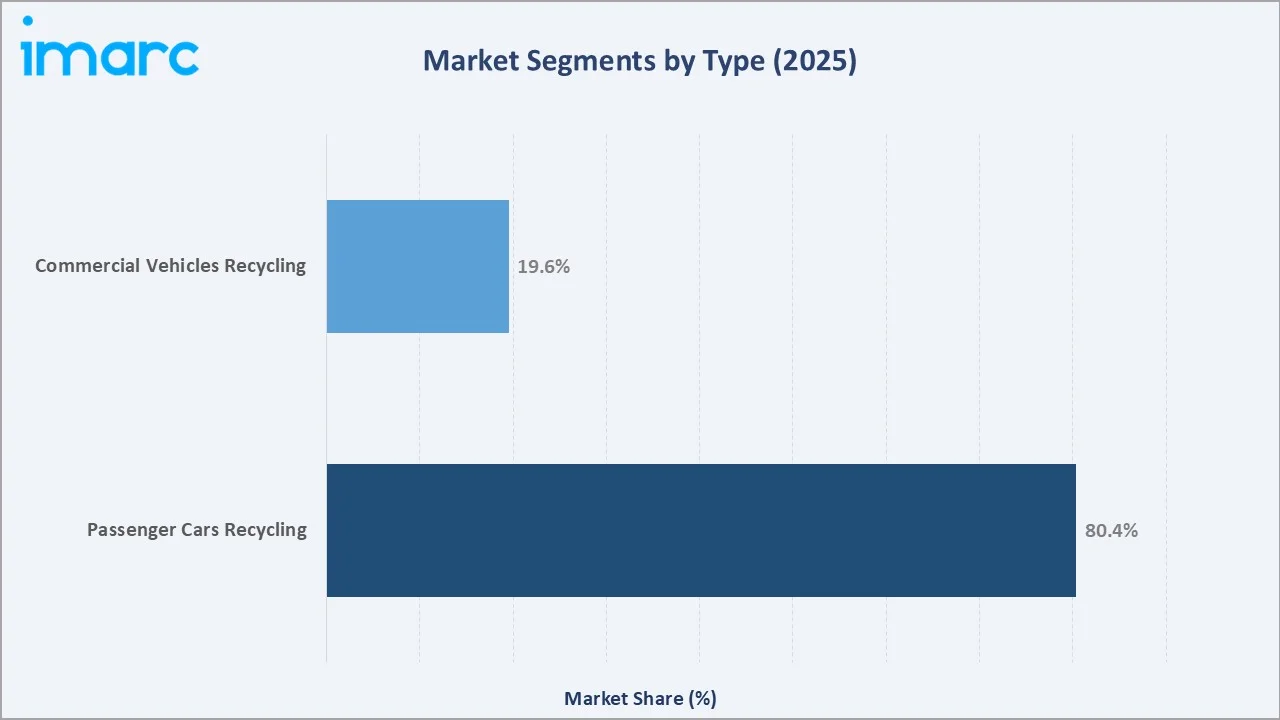

Passenger Cars Recycling dominates by type at 80.4% share, while the Aftermarket segment leads application with 95.1% share. North America remains the dominant region, accounting for 37.1% of global revenue in 2025. Key industry participants include LKQ Corporation, Radius Recycling Inc., Sims Limited, and ASM Auto Recycling.

To get more information on this market, Request Sample

The vehicle recycling market is an essential component of the global circular economy, focused on recovering valuable materials such as metals, plastics, and components from end-of-life vehicles (ELVs). Driven by increasing environmental regulations, rising scrap metal demand, and the need to reduce automotive waste, the market has witnessed steady growth across developed and emerging economies.

Executive Summary

The global vehicle recycling market continues to demonstrate robust expansion, underpinned by tightening ELV regulations, surging demand for recycled metals, and the rapid growth of the electric vehicle sector, which is creating entirely new high-value recycling streams. Valued at USD 105.5 Billion in 2025, the market is forecasted to exceed USD 329.9 Billion by 2034 at a CAGR of 12.83%.

Among the key growth drivers, the widespread adoption of recycled steel and aluminum in vehicle manufacturing remains a primary catalyst. Approximately 85% of vehicle components by weight are recyclable (2025), with steel and non-ferrous metals constituting around 75% of total vehicle mass. The passenger car recycling segment dominates with an 80.4% share of the market in 2025, reflecting the overwhelming size of the global passenger vehicle fleet.

North America retains its market leadership with a 37.1% share (2025), while Asia Pacific emerges as the fastest-growing region, registering significant CAGR growth owing to expanding vehicle scrappage policies and EV battery recycling mandates in China, India, and South Korea. Leading market players are investing in advanced shredding technology, automated dismantling systems, and EV battery pre-treatment capabilities - all key areas reshaping the competitive landscape through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Passenger Cars Recycling – 80.4% share (2025) |

|

Largest Segment (Application) |

Aftermarket – 95.1% share (2025) |

|

Leading Region |

North America – 37.1% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific – driven by China's EV battery recycling mandates. |

|

Top Companies |

LKQ Corporation, Radius Recycling, Sims Limited, ASM Auto Recycling |

|

Market Opportunity |

EV battery recycling projected at USD 40B+ globally by 2034 |

Key Analytical Observations Supporting the Above Data:

- Passenger Cars Recycling dominates at 80.4% (2025). Global passenger vehicle sales totaled around 82 million units in 2024, reflecting a 3% increase compared to 2023. The total number of end-of-life vehicles (ELVs) is projected to approach 50 million by 2030 in India, providing a continuous and predictable ELV supply pipeline.

- Commercial Vehicles Recycling at 19.6% (2025) delivers disproportionately high metal recovery volumes per unit processed. Nearly 75% of vehicles’ mass consists of recyclable steel and aluminum, making commercial ELVs particularly valuable inputs for secondary metal processors.

- Aftermarket application dominates at 95.1% (2025), driven by global demand for recycled spare parts offering 40-70% cost savings versus new OEM components.

- North America leads at 37.1% (2025), anchored by the US’ highly organized network of licensed dismantlers and shredder operators, comprehensive ELV regulatory frameworks, and the presence of major industry players with extensive multi-state processing capacity.

- EV battery recycling is emerging as a major new revenue stream, as growing EV adoption creates a growing pipeline of high-value battery packs requiring specialized hydrometallurgical and pyrometallurgical processing to recover lithium, cobalt, nickel, and manganese.

- Circular economy and Extended Producer Responsibility (EPR) mandates are fundamentally expanding organized recycling volumes globally. The EU's revised ELV Regulation targets 25% recycled content in new vehicles by 2030, creating unprecedented downstream demand for certified recycled automotive materials.

Global Vehicle Recycling Market Overview

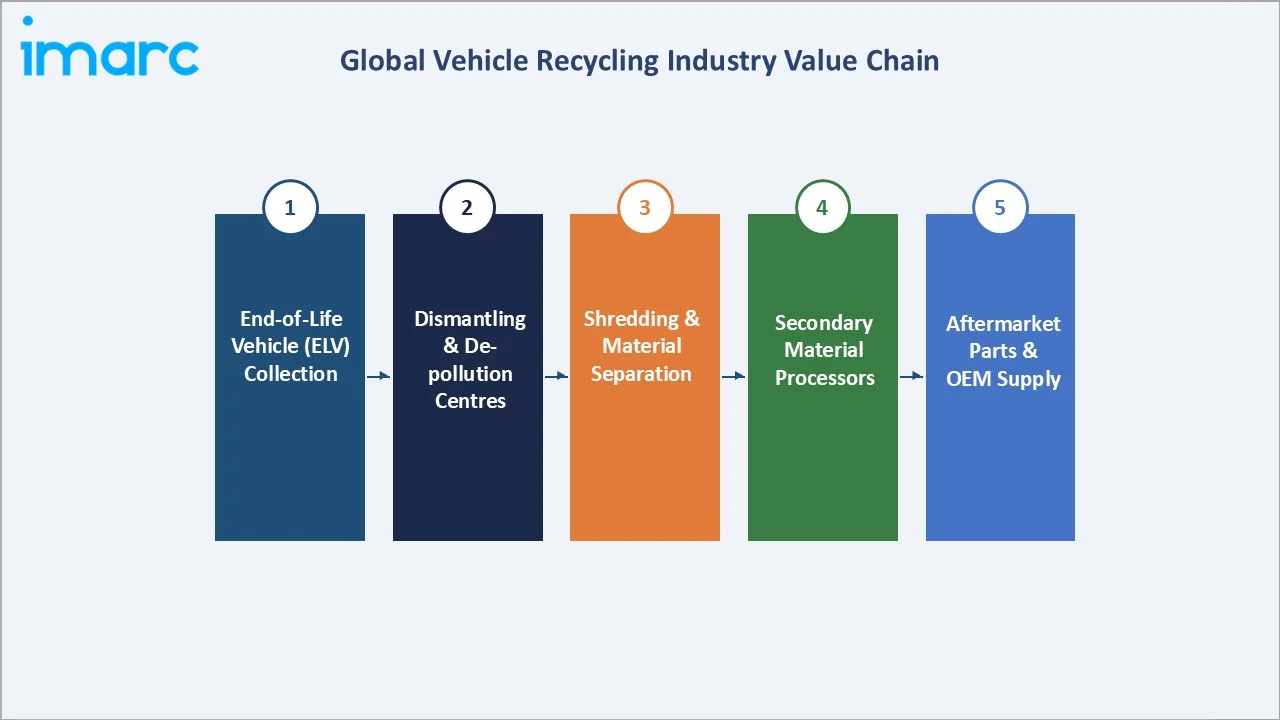

Vehicle recycling constitutes one of the most established and commercially significant segments within the broader circular economy and secondary materials industry. The process involves the systematic disassembly of end-of-life automobiles to recover spare parts, metals, fluids, and other materials for reuse and remanufacturing. This involves dismantling, crushing, shredding, and material recovery operations through which magnetic pieces, sheet metals, seats, wheels, batteries, and other components are retrieved and directed to appropriate downstream markets.

The global vehicle recycling ecosystem encompasses end-of-life vehicle collectors, licensed dismantlers, shredder operators, secondary metal processors, aftermarket parts distributors, and specialty recyclers for batteries, rubber, glass, and plastics. The market's versatile value proposition - spanning steel supply for manufacturing, affordable spare parts for repair markets, and hazardous material management - makes it a structurally resilient and commercially diverse industry.

Macroeconomic influences, including rising raw material costs, urbanization rates, vehicle fleet expansion, and increasing regulatory pressure, are all positively reinforcing the vehicle recycling market. By 2034, vehicle recycling is expected to represent a critical pillar of global automotive sustainability strategies, as automakers embed recycled content requirements into vehicle design and procurement to meet carbon neutrality targets and circular economy commitments.

Market Dynamics

To evaluate market opportunities, Request Sample

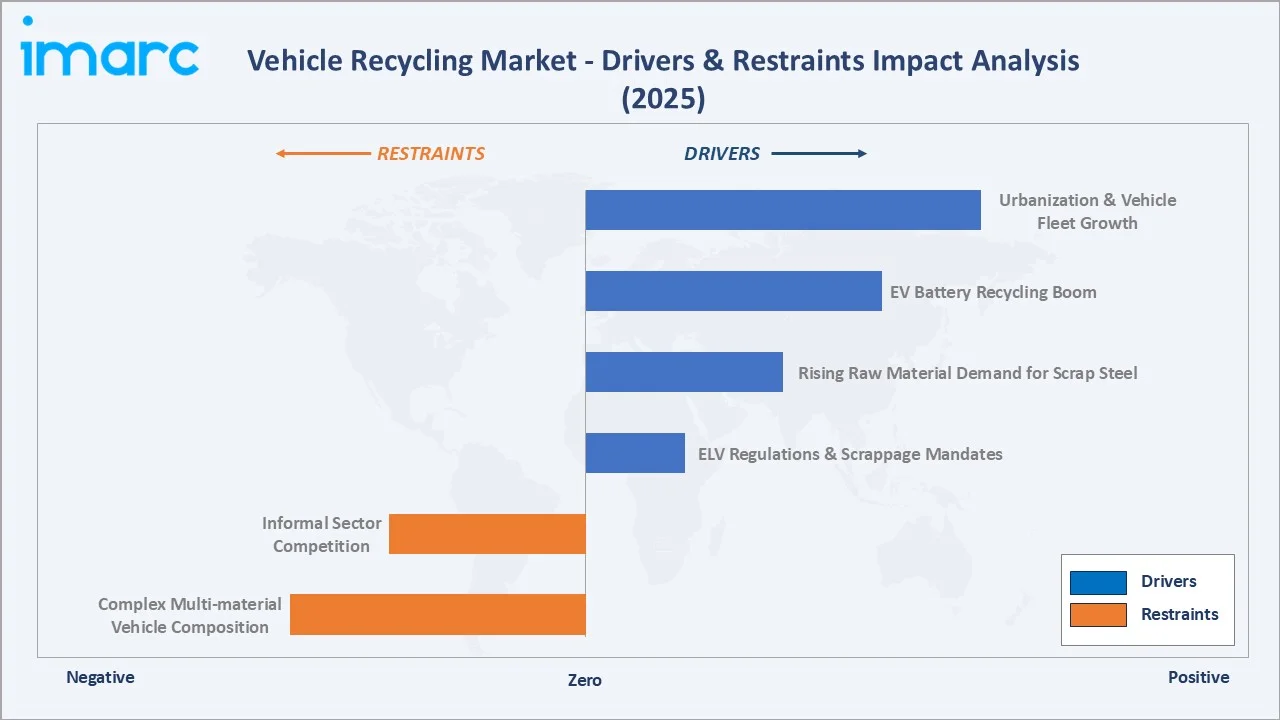

Market Drivers

- Stringent ELV Regulations and Scrappage Policy Mandates: Governments across the European Union, Japan, South Korea, China, and India have enacted comprehensive end-of-life vehicle regulations mandating formal recycling and minimum recyclability thresholds. The EU ELV Directive requires 85% by weight recyclability, compelling automakers and dismantlers to invest in advanced recovery infrastructure.

- Rising Demand for Recycled Steel, Aluminum, and Non-Ferrous Metals: Escalating costs of virgin raw materials are incentivizing manufacturers to prioritize recycled feedstocks. Vehicle-derived recycled steel accounts for a substantial portion of secondary steel inputs for automotive and construction manufacturers globally (2025).

- EV Battery Recycling Boom Creating High-Value New Revenue Streams: More than 17 million electric vehicles were sold globally in 2024, generating a growing pipeline of end-of-life battery packs. EV batteries contain high-value metals, making EV recycling substantially more lucrative per unit than conventional ICE vehicle processing.

- Rapid Urbanization and Global Vehicle Fleet Expansion: The global car parc is estimated to reach approximately 1.644 billion vehicles in 2025, with emerging economies in the Asia Pacific and Latin America seeing rapid motorization. This structural fleet growth directly expands the future ELV supply pipeline, underpinning long-term recycling volume growth across all major regions.

These drivers collectively reinforce a virtuous cycle of market expansion - regulatory compliance drives organized recycling investment, which improves recovery rates and economics, which attracts greater capital and technology deployment, which in turn enables broader market formalization and volume growth.

Market Restraints

- Complex Multi-material Vehicle Composition: Modern vehicles increasingly incorporate advanced high-strength steels, carbon fiber composites, multi-layer adhesives, and specialty polymers that are difficult and costly to separate and recover, reducing shredder profitability and material purity for downstream processors.

- Informal Sector Competition: In emerging markets across Asia, Africa, and Latin America, informal vehicle dismantling operations process significant ELV volumes without regulatory compliance, environmental safeguards, or hazardous material controls, undercutting formal recyclers on cost and distorting market pricing.

- High Capital Investment Requirements for Advanced Facilities: Establishing technologically advanced vehicle recycling infrastructure, including automated dismantling lines, advanced shredders, and EV battery pre-treatment systems, requires substantial upfront capital investment that can constrain market entry and capacity expansion.

Market Opportunities

- Expansion of Organized Vehicle Scrapping Infrastructure in Emerging Markets: India's Vehicle Scrappage Policy, China's expanded ELV regulations, and Brazil's emerging scrappage incentive programs are collectively catalyzing the construction of hundreds of formally registered vehicle scrapping facilities, creating major greenfield investment opportunities.

- EV Battery and Critical Materials Recycling: Specialized hydrometallurgical and pyrometallurgical processing for EV battery materials represents a USD 40 Billion+ global opportunity by 2034. Companies investing early in EV battery pre-treatment capabilities are positioning for a dominant share of this high-margin emerging segment.

- Digital Platforms and Aftermarket Parts Marketplaces: Online platforms enabling certified recycled parts trading are digitalizing the aftermarket supply chain, broadening buyer access globally and improving price discovery for salvaged components, directly expanding the commercial value captured per processed ELV.

Market Challenges

- Shredder Residue Management and Landfill Costs: Automotive shredder residue (ASR), comprising textiles, plastics, glass, and residual metals, represents 20-25% of vehicle weight and requires expensive disposal or specialized downstream processing, creating a persistent cost challenge for shredder operators across all markets.

- Hazardous Material Handling Compliance: The removal and safe disposal of fluids including engine oil, brake fluid, coolant, fuel, and airbag chemicals requires certified handling facilities and skilled labor, raising operational complexity and compliance costs for formal recycling operators.

- Price Volatility of Recycled Metal Commodities: Recycled steel scrap and non-ferrous metal prices are subject to global commodity market fluctuations, creating revenue uncertainty for vehicle recyclers and making long-term investment planning and facility financing more challenging.

Emerging Market Trends

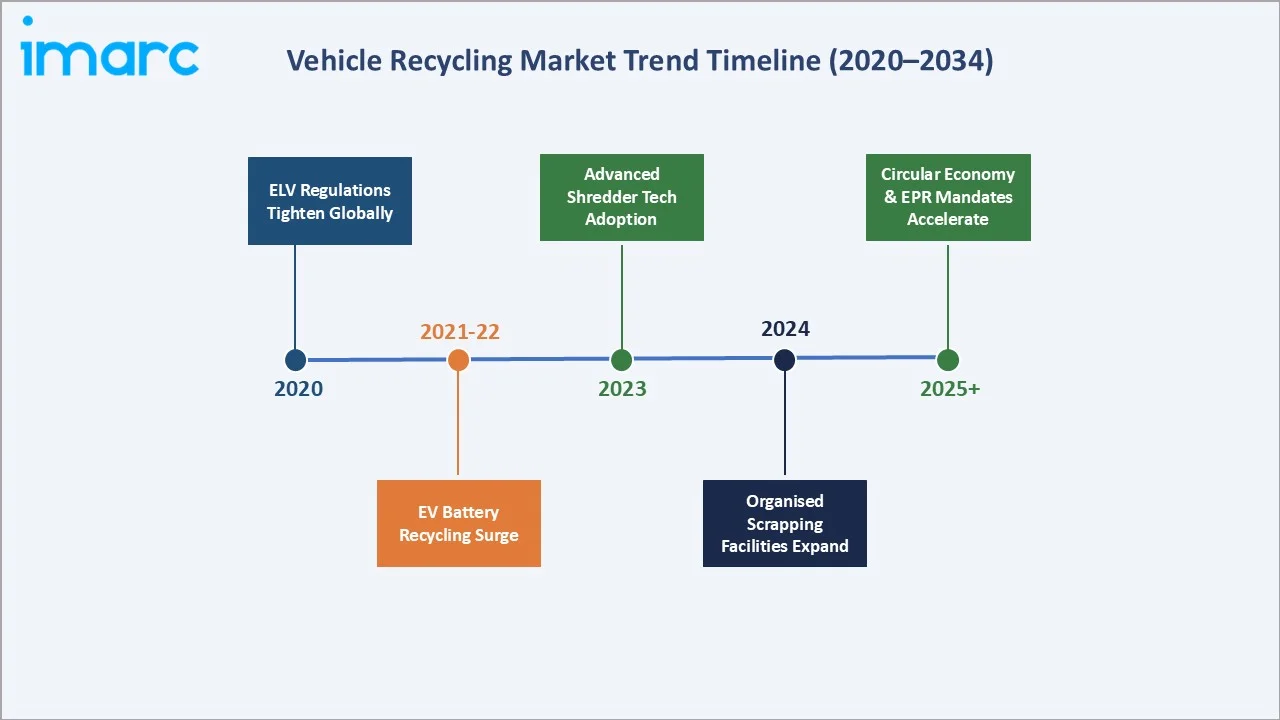

1. Expansion of Organized and Technologically Advanced Scraping Facilities

In India, the Vehicle Scrappage Policy launched in 2021 has catalyzed dozens of greenfield Registered Vehicle Scrapping Facilities (RVSFs). In November 2024, Tata Motors and Tata International launched Re.Wi.Re, an advanced registered vehicle scrapping facility in Pune, reflecting the accelerating momentum behind organized vehicle recycling investment across emerging economies.

2. Electric Vehicle Battery Recycling as a High-Value Growth Segment

Major recycling operators in China, South Korea, Germany, and North America are investing heavily in EV battery pre-treatment and hydrometallurgical processing capabilities, forming strategic partnerships with automakers to establish closed-loop battery material supply chains that re-enter vehicle manufacturing.

3. Circular Economy Frameworks and Extended Producer Responsibility

Extended producer responsibility mandates, now operative across 40+ countries, are placing end-of-life management costs directly on vehicle manufacturers, incentivizing vehicles designed for higher recyclability. The EU's revised ELV Regulation targeting 25% recycled content in new vehicles by 2030 is creating unprecedented downstream demand for certified recycled automotive-grade steel and aluminum, enhancing commercial visibility and contract stability for leading recycling operators.

4. Digital Transformation of Aftermarket Parts Trading

LKQ Corporation digital auction platforms have expanded global buyer reach for certified salvage parts, improving price realization and inventory turnover for dismantlers. A recent survey of Tier-1 automotive suppliers confirms that AI-driven automation is delivering consistent and measurable productivity gains, with facilities reporting an average 25% improvement in overall productivity.

5. Adoption of Advanced Material Separation Technologies

Next-generation separation technologies, including sensor-based optical sorting, laser ablation, and advanced eddy current systems, are enabling recyclers to achieve significantly higher non-ferrous metal recovery rates from shredder output. Facilities adopting advanced separation technology are reporting 15-25% improvements in total revenue per ton of processed material.

Industry Value Chain Analysis

The vehicle recycling industry value chain spans multiple interconnected stages, from end-of-life vehicle acquisition through to secondary material delivery to downstream manufacturing customers. Each stage is populated by specialized operators whose performance directly influences material recovery yield, environmental compliance, and overall market profitability.

|

Stage |

Key Players / Examples |

|

ELV Collection & Acquisition |

Insurance salvage, municipal programs, dealership trade-in schemes, and direct consumer drop-off |

|

Licensed Dismantlers |

ASM Auto Recycling (UK), INDRA (Europe), Keiaisha Co. (Japan), and independent certified dismantlers globally |

|

De-pollution Centers |

Specialist hazardous fluid removal, airbag neutralization, battery disconnection (EU-certified operators) |

|

Vehicle Shredders |

Radius Recyling, Inc., Sims Limited, Scholz Recycling, Hensel Recycling Group |

|

Material Separation & Processing |

Non-ferrous metal processors, steel mills, rubber recyclers, glass cullet processors, plastic reclaimers |

|

EV Battery Recyclers |

Eco-Bat Technologies (lead-acid), Li-Cycle, Umicore, Redwood Materials (lithium-ion) |

|

Secondary Material Buyers |

Steel mills, aluminum smelters, copper refineries, OEM material purchasing departments |

|

Aftermarket Parts Distributors |

LKQ Corporation, online platforms (Car-Part.com, Row52), and independent regional distributors |

Technology Landscape in the Vehicle Recycling Industry

Advanced Shredding and Separation Technology

The world’s largest industrial shredder, operating in Newport, Wales since 2006, can process up to 450 end-of-life vehicles per hour, making it one of the largest facilities of its kind globally. that processes up to 450 vehicles per hour, equivalent to around 350 tons of metal. These integrated shredder-separation systems are enabling facilities to profitably recover specialty alloys, copper wiring, and aluminum cast components that previously ended up in shredder residue.

Electric Vehicle Battery Dismantling and Hydrometallurgy

EV battery pre-treatment technologies, including robotic module disassembly, thermal pre-treatment for electrode material liberation, and direct hydrometallurgical leaching, are maturing rapidly as global EV recycling volumes ramp up. Umicore’s pyro-hydro recycling technology achieves recovery rates exceeding 95% for cobalt, copper, and nickel, and over 90% for lithium, enabling the production of high-purity, battery-grade materials that are reintegrated directly into the battery value chain.

AI-Powered Parts Identification and Inventory Management

Artificial intelligence-based computer vision systems are transforming dismantled parts grading, pricing, and inventory management at major auto recycling facilities. These systems can identify, condition-assess, and price a recovered component in seconds versus minutes for manual grading. LKQ North America partnered with Tractable to deploy AI-powered computer vision technology that analyzes vehicle damage and identifies reusable parts, helping accelerate and optimize salvage vehicle recycling.

Digital Traceability and Sustainability Reporting

Blockchain and IoT-enabled material traceability systems are enabling recycled steel and aluminum producers to provide certified chain-of-custody documentation to automotive OEM customers, a critical requirement as automakers embed recycled content targets into their sustainability reporting frameworks.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Passenger Cars Recycling |

80.4% |

2025 |

|

Material |

Steel |

53.2% |

2025 |

|

Application |

Aftermarket |

95.0% |

2025 |

|

Region |

North America |

37.1% |

2025 |

By Type

Passenger cars recycling dominates the market with an 80.4% share (2025), driven by the overwhelming size of the global passenger vehicle fleet and the comparatively shorter average vehicle service life of passenger automobiles. Commercial vehicles recycling accounts for 19.6% of market share, delivering disproportionately high metal recovery volumes per unit due to larger structural mass.

To access detailed market analysis, Request Sample

India's end-of-life vehicles (ELVs), with a NITI Aayog report projecting volumes to grow from nearly 23 million by 2025 to around 50 million by 2030. This surge underscores the urgent need for a scaled and formal vehicle scrappage ecosystem, shifting it from a policy goal to an operational necessity. Recycled steel from passenger cars constitutes a major share of secondary steel inputs for automotive and construction manufacturers.

By Application

The aftermarket segment dominates at 95.1% share (2025), reflecting massive global demand for cost-effective recycled spare parts for vehicle maintenance and repair. The OEMs segment accounts for 4.9% but is the fastest-growing application as automakers embed certified recycled material procurement into vehicle manufacturing supply chains to meet circular economy targets.

Independent repair shops, fleet operators, and cost-conscious consumers across all major markets rely heavily on certified recycled parts for collision repair, mechanical servicing, and vehicle maintenance. The OEMs segment is projected to grow at an above-average rate through 2034, as the EU End-of-Life Vehicle regulation, which includes a minimum 15% recycled content within six years, creates structured, long-term procurement contracts between automakers and certified recycled material suppliers.

Regional Market Insights

North America's market leadership at 37.1% (2025) is deeply entrenched, anchored by the US’s highly organized network of licensed vehicle dismantlers and major shredder operators. With more than 290.9 million registered vehicles in the US alone in 2026 and an average vehicle age of 12.8 years, North America generates one of the largest and most consistent ELV supply streams globally.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Companies |

|

North America |

37.1% |

Mature ELV infrastructure; large aging vehicle fleet; strong aftermarket demand |

RCRA; state ELV laws; EPA hazardous material standards |

LKQ, Radius Recycling, Sims Limited |

|

Asia Pacific |

28.6% |

China & India scrappage policies; EV battery recycling surge; rapid fleet growth |

China ELV Regulation; India Scrappage Policy 2021; Japan End-of-Life Vehicle Law |

Keiaisha Co., Toyota Metal |

|

Europe |

22.4% |

EU ELV Directive compliance; circular economy targets; advanced shredder residue recovery |

EU ELV Directive (95% recyclability); REACH; EU Battery Regulation |

INDRA, Hensel Recycling, Scholz, ASM Auto |

|

Latin America |

7.3% |

Growing vehicle parc; informal sector formalization; Brazil & Mexico policy development |

Local scrappage incentives, developing EPR frameworks |

Regional operators; Sims Limited |

|

Middle East & Africa |

4.6% |

Rising vehicle imports are driving ELV volumes and circular economy policy adoption. |

Nascent ELV regulation; GCC sustainability mandates |

Local dismantlers; emerging formal operators |

Asia Pacific emerges as the clear growth engine with a 28.6% share (2025) and represents the fastest-growing major region within the global vehicle recycling market. China is the dominant contributor, supported by a rapidly maturing ELV policy framework, a fleet of over 300 million registered vehicles, and strategic government investments in organized recycling infrastructure. India's Vehicle Scrappage Policy is catalyzing the construction of registered vehicle scrapping facilities across multiple states, while Japan and South Korea bring advanced recycling technologies and high-yield processing systems to the regional landscape.

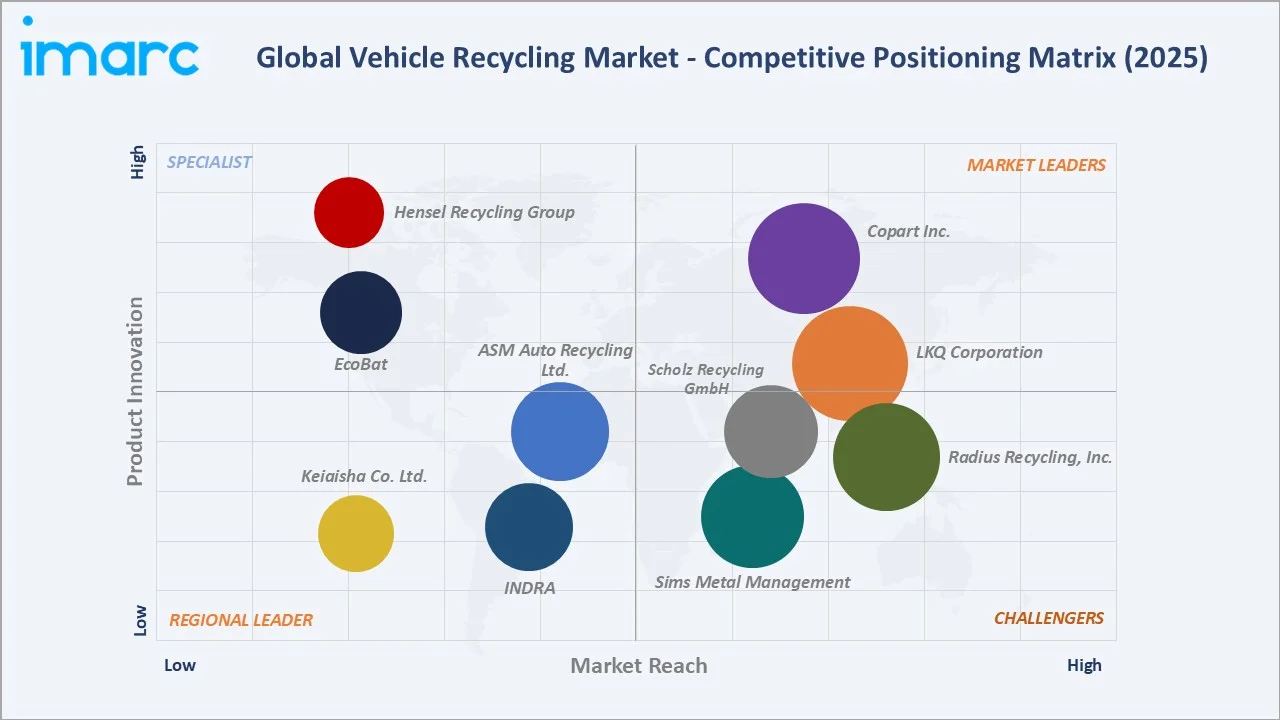

Competitive Landscape

The global vehicle recycling market exhibits a moderately consolidated competitive structure. The top five players, LKQ Corporation, Radius Recycling Inc., Sims Limited, and INDRA, collectively account for approximately 35-40% of organized global recycling revenues in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

LKQ Corporation |

LKQ / Euro Car Parts |

Market Leader |

North America's largest aftermarket parts supplier; global salvage network |

|

Radius Recycling, Inc. |

Radius Recycling / Pick-N-Pull |

Strong Challenger |

US scrap metal processing leader; significant ferrous & non-ferrous recovery |

|

Sims Limited |

Sims Limited |

Strong Challenger |

Global metals recycler; advanced ELV shredding and downstream processing |

|

ASM Auto Recycling Ltd. |

ASM Auto Recycling |

Regional Leader |

UK-certified green dismantling, de-pollution, and parts re-use specialist |

|

INDRA |

INDRA Automobile Recycling |

Regional Leader |

European ELV dismantling pioneer; France, Spain, Portugal network |

|

Hensel Recycling Group |

Hensel Recycling |

Specialist |

German multi-material recycler; non-ferrous metal recovery specialist |

|

EcoBat |

EcoBat |

Specialist |

One of world's largest lead-acid battery recyclers; ELV battery specialist |

|

Keiaisha Co. Ltd. |

Keiaisha |

Regional Specialist |

Japan-based ELV specialist; advanced hazardous material removal technology |

|

Scholz Recycling GmbH |

Scholz |

Challenger |

European multi-material recycler; automotive scrap processing & steel trading |

The remainder is distributed among thousands of regional operators, independent dismantlers, and specialist recyclers across ferrous metals, non-ferrous metals, EV batteries, and aftermarket parts segments.

Key Company Profiles

LKQ Corporation

LKQ Corporation is North America's largest provider of alternative and specialty parts to repair and accessorize automobiles and other vehicles, with annual revenues exceeding USD 14.4 Billion (2025). The company operates an extensive network of self-service and full-service used vehicle parts facilities across North America and Europe.

- Product Portfolio: Recycled OEM parts, aftermarket collision replacement parts, refurbished parts, and specialty accessories for passenger vehicles, light trucks, and recreational vehicles.

- Recent Developments: Expanded European recycling and salvage operations in 2024; launched AI-powered parts identification and digital inventory systems to improve throughput and pricing accuracy.

- Strategic Focus: Omnichannel parts distribution, digital platform enhancement, European market consolidation, and sustainable parts lifecycle solutions for insurance and collision repair customers.

Radius Recycling, Inc.

Radius Recycling, Inc., formerly known as Schnitzer Steel Industries, is one of the largest recyclers of ferrous and non-ferrous scrap metal in North America, operating auto parts stores (Pick-N-Pull) and shredding facilities. The company processed over 660,000 units of end-of-life vehicles through its network in FY2024.

- Product Portfolio: Recycled ferrous scrap, non-ferrous metals, finished steel products, and salvage auto parts through its retail Pick-N-Pull consumer brand.

- Recent Developments: Commissioned a new advanced shredder line in 2024, increasing non-ferrous recovery capacity by approximately 15%; expanded Pick-N-Pull self-service parts stores in growing Sun Belt markets.

- Strategic Focus: Technology investment in shredding and separation efficiency, growing the consumer-facing Pick-N-Pull aftermarket brand, and steel product quality improvement for automotive OEM customers.

Sims Limited

Sims Limited is a leading global metals and electronics recycler operating across 200+ locations in North America, Australasia, and the UK. The company reported annual revenues of approximately AUD 7.195 billion in FY2024, with automotive scrap representing a major portion of processed volumes.

- Product Portfolio: Ferrous scrap, non-ferrous metals (aluminum, copper, zinc), electronics recycling, and processed metal products for steel mill and foundry customers.

- Recent Developments: Advanced its digital trading platform in 2024 for improved scrap procurement and sales; invested in sensor-based non-ferrous sorting upgrades at multiple North American facilities.

- Strategic Focus: Operational efficiency through technology, sustainable material flows for low-carbon steel production, and strategic positioning for EV battery material recovery as volumes ramp through 2030.

Market Concentration Analysis

The global vehicle recycling market exhibits moderate concentration at the top end, with the leading five players, including LKQ Corporation, Radius Recyling, Inc., Sims Limited, and INDRA, collectively accounting for approximately 35-40% of organized global recycling revenues in 2025. However, the presence of thousands of independent regional operators and informal dismantlers globally ensures a highly fragmented long tail that characterizes the broader market structure.

The aftermarket parts segment is notably more fragmented than the shredded scrap metals segment. In the organized shredded scrap category, the top three operators, Radius Recyling, Inc., Sims Limited, and Scholz Recycling GmbH, command a significant share of processed volumes in their respective regions, demonstrating higher concentration in industrial metal recovery relative to the broader vehicle dismantling landscape.

Consolidation activity has accelerated since 2021. Notable M&A transactions include LKQ Corporation's ongoing European consolidation program and private equity-backed roll-ups of regional dismantling networks in North America and Europe. The market is expected to see significant M&A transactions annually through 2034, as larger operators pursue scale advantages in technology investment, EV battery processing capabilities, and digital platform development.

Investment & Growth Opportunities

Fastest Growing Segments

EV battery recycling is projected to grow at a CAGR exceeding 25% from 2025 to 2034, driven by the exponential growth in end-of-life EV battery volumes. Advanced shredder residue processing technologies capable of recovering previously landfilled materials are attracting increasing capital. These segments collectively address a total addressable market of approximately USD 80 Billion+ by 2034.

Emerging Market Expansion

Asia Pacific and Latin America present the most compelling geographic investment opportunities. The government of India is targeting an annual scrappage of over 500,000 vehicles by 2026. Entry via joint ventures with local operators, government-approved registered vehicle scrapping facility operators, and technology licensing partnerships is the dominant preferred strategy for international players entering these high-growth emerging markets.

Venture Investment Trends

Key investment themes include AI-powered dismantling robotics, EV battery hydrometallurgical processing, digital aftermarket parts marketplaces, and IoT-enabled scrap traceability platforms.

- Key growth bets: EV battery pre-treatment automation, sensor-based non-ferrous metal sorting, and certified recycled material supply chain traceability.

- ESG-aligned investors are increasingly targeting circular economy-compliant vehicle recycling operators as sustainable infrastructure investments aligned with net-zero automotive supply chain commitments.

- Institutional PE interest in multi-facility vehicle recycling roll-ups remains elevated, particularly in Southeast Asia, India, and the GCC region, where formal recycling infrastructure is nascent but regulatory pressure is accelerating.

Future Market Outlook (2026-2034)

From a base of USD 105.5 Billion in 2025, the market is forecast to reach USD 329.9 Billion by 2034, representing absolute incremental value addition of approximately USD 224.4 Billion over the forecast decade - reflecting nearly tripling of market scale.

Operators achieving 20-30% cost efficiency gains through automation and AI-driven processing optimization will gain a decisive competitive advantage in high-volume markets by 2028-2030. The growing share of EVs in total ELV volumes, projected to exceed 15% of annual end-of-life vehicles by 2034, will fundamentally alter per-vehicle revenue profiles, with battery-derived materials contributing significantly to overall recycling economics.

The next decade will also witness a fundamental shift in regulatory expectations. Extended Producer Responsibility frameworks, recycled content mandates for new vehicles, and carbon border adjustment mechanisms are expected to transition from voluntary to mandatory across major markets. Operators that fail to achieve certified circular material flows and measurable carbon reduction outcomes risk losing OEM supply contracts and regulatory operating licenses, particularly in the EU and increasingly across Asian markets.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 180 industry participants in 2024-2025, comprising vehicle recycling facility operators, scrap metal processors, OEM sustainability executives, EV battery recycling specialists, and regulatory affairs representatives across North America, Europe, and the Asia Pacific.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, regulatory filings, trade publications (Recycling Today, Scrap Magazine, Automotive Recycling), industry databases, government ELV registration data, and publicly available automotive industry statistics. Over 300 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating ELV volume projections, metal commodity price trends, vehicle fleet age distribution data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for commodity price volatility and regulatory timing uncertainty.

Vehicle Recycling Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Passenger Cars Recycling, Commercial Vehicles Recycling |

| Material Covered | Iron, Aluminium, Steel, Rubber, Copper, Glass, Plastic, Others |

| Application Covered | OEMs, Aftermarket |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | LKQ Corporation, Radius Recycling, Inc., Sims Limited, ASM Auto Recycling Ltd., INDRA, Hensel Recycling Group, EcoBat, Keiaisha Co. Ltd., Scholz Recycling GmbH |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Vehicle Recycling Market Report

The global vehicle recycling market was valued at USD 105.5 Billion in 2025 and is projected to reach USD 329.9 Billion by 2034.

The market is expected to grow at a CAGR of 12.83% during the forecast period 2026-2034, reflecting strong demand for recycled metals, tightening ELV regulations, and the emerging EV battery recycling segment.

North America is the dominant region, accounting for 37.1% of global revenues in 2025, driven by mature recycling infrastructure, a large and aging vehicle fleet, and comprehensive ELV regulatory frameworks.

Asia Pacific is the fastest-growing region, led by China's ELV policy expansion, India's Vehicle Scrappage Policy, and the region's dominant role in global EV adoption and battery recycling volumes.

Key drivers include stringent ELV regulations, rising demand for recycled steel and non-ferrous metals, the EV battery recycling boom, rapid urbanization, fleet expansion in emerging markets, and circular economy mandates.

Passenger cars recycling leads with an 80.4% market share in 2025, driven by the global passenger car fleet exceeding 1.4 billion units, with approximately 80 million vehicles reaching end-of-life annually.

The aftermarket segment dominates at 95.1% share in 2025, reflecting global demand for recycled auto parts offering 40-70% cost savings versus new OEM components for vehicle maintenance and repair.

EV growth is creating high-value battery recycling streams containing lithium, cobalt, and nickel. EV battery recycling is projected to grow at over 25% CAGR through 2034, representing a major new revenue segment.

Key trends include organized scrapping facility expansion, EV battery recycling investment, circular economy EPR mandates, AI-powered parts identification, digital aftermarket platforms, and advanced material separation technology.

Key players in the vehicle recycling market include LKQ Corporation, Radius Recycling, Inc., Sims Limited, ASM Auto Recycling Ltd., INDRA, Hensel Recycling Group, EcoBat, Keiaisha Co. Ltd., and Scholz Recycling GmbH.

High-growth opportunities include EV battery hydrometallurgy facilities, AI-powered dismantling automation, digital aftermarket parts marketplaces, and organized scrapping facility development in India, China, Brazil, and GCC countries.

Key challenges include complex multi-material vehicle composition, informal sector competition in emerging markets, automotive shredder residue disposal costs, hazardous material handling compliance, and commodity price volatility.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)