Vietnam Containerized Data Center Market Size, Share, Trends and Forecast by Type of Container, Organization Size, Application, End Use Industry, and Region, 2026-2034

Vietnam Containerized Data Center Market Summary:

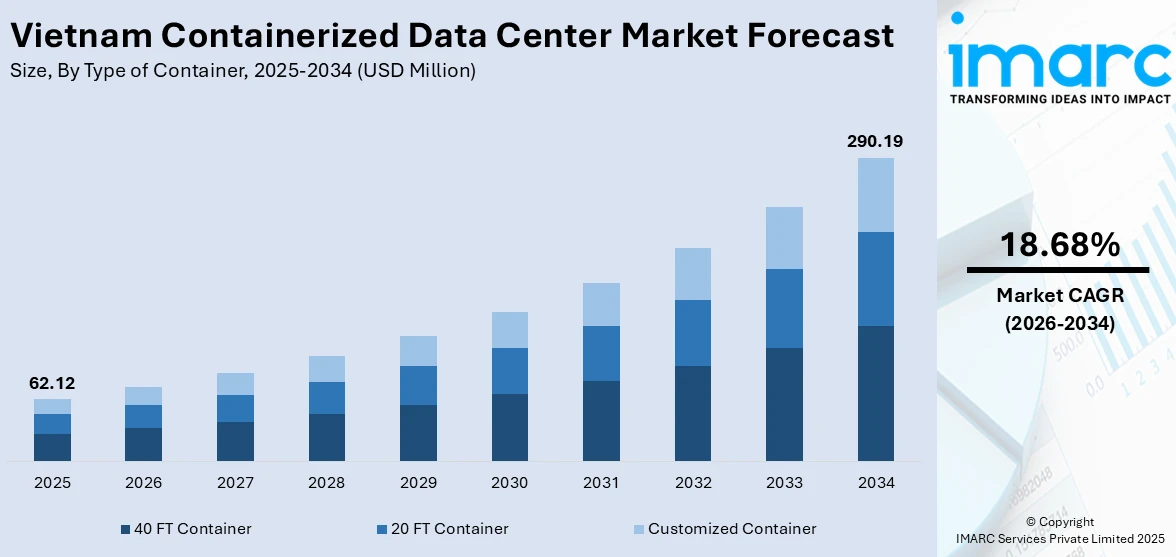

The Vietnam containerized data center market size was valued at USD 62.12 Million in 2025 and is projected to reach USD 290.19 Million by 2034, growing at a compound annual growth rate of 18.68% from 2026-2034.

The market is driven by the rapid adoption of modular and portable data infrastructure solutions that enable swift deployment across diverse geographic locations in Vietnam. Rising demand for edge computing capabilities, increasing digital transformation initiatives by enterprises, and favorable government policies supporting information and communication technology infrastructure development are fueling robust expansion. The growing preference for scalable, energy-efficient, and cost-effective alternatives to traditional brick-and-mortar facilities is further accelerating adoption, contributing to a rising Vietnam containerized data center market share.

Key Takeaways and Insights:

- By Type of Container: 40 FT container dominates the market with a share of 46.8% in 2025, driven by its superior capacity to house comprehensive IT infrastructure, networking equipment, and integrated cooling systems within a standardized unit.

- By Organization Size: Large organization leads the market with a share of 52.4% in 2025, owing to substantial capital investment capabilities and the need for high-density computing resources supporting complex enterprise workloads.

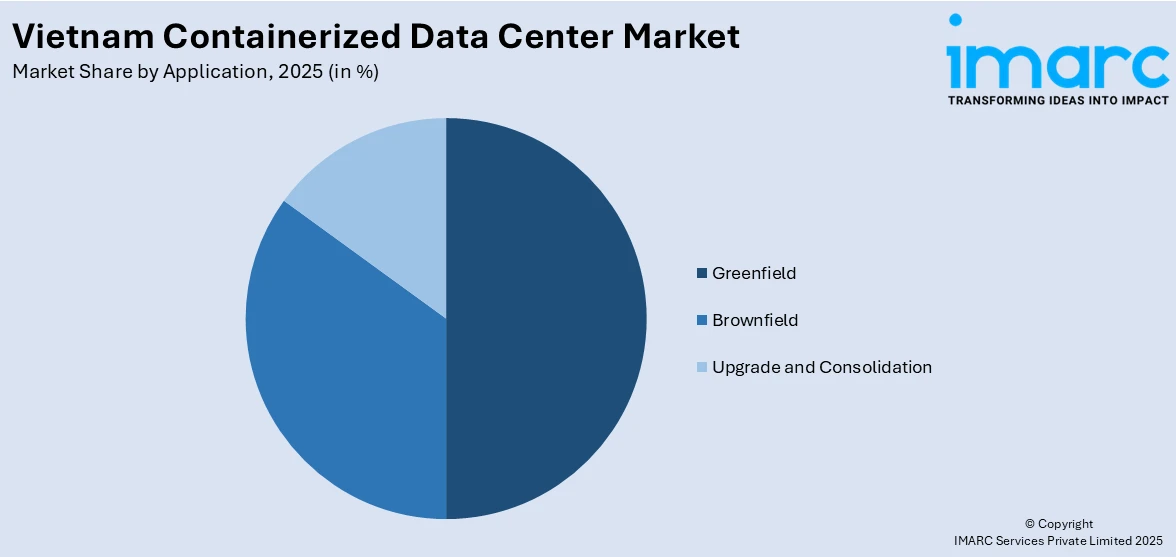

- By Application: Greenfield represents the largest segment with a market share of 44.6% in 2025, driven by the increasing establishment of entirely new data center facilities in industrial zones and emerging technology parks.

- By End Use Industry: IT and telecommunications dominate the market with a share of 36.9% in 2025, owing to explosive growth in data traffic from expanding mobile networks and cloud service adoption.

- By Region: Southern Vietnam leads the market with a share of 41.3% in 2025, driven by the concentration of major economic and industrial hubs, superior connectivity infrastructure, and established technology ecosystems.

- Key Players: The Vietnam containerized data center market exhibits a moderately fragmented competitive landscape, with domestic technology infrastructure providers and international modular data center specialists competing through rapid deployment capabilities and energy-efficient technologies.

To get more information on this market Request Sample

The Vietnam containerized data center market is experiencing significant momentum as organizations across the country seek agile, rapidly deployable computing infrastructure to address escalating digital demands. The proliferation of cloud computing services, coupled with the government's ambitious digital transformation agenda and data localization mandates, is compelling enterprises to establish domestic data processing capabilities swiftly. In April 2025, Viettel Group broke ground on its largest data center to date in Ho Chi Minh City’s Tan Phu Trung Industrial Park, a 140 MW of capacity with approximately 10,000 racks, designed to support advanced digital services and national infrastructure needs, expected to be operational by 2026. Containerized data centers offer a compelling solution by providing pre-engineered, factory-tested modular units that can be transported and commissioned within significantly shorter timeframes compared to conventional facilities. The rising penetration of advanced mobile networks and the expansion of edge computing requirements in manufacturing zones, logistics corridors, and urban centers are further amplifying demand.

Vietnam Containerized Data Center Market Trends:

Rising Adoption of Edge Computing Driving Distributed Containerized Deployments

The growing demand for low-latency data processing at the network edge is reshaping infrastructure deployment strategies across Vietnam. As enterprises increasingly rely on real-time analytics for manufacturing automation, logistics optimization, and smart city applications, containerized data centers are emerging as the preferred solution for distributed edge deployments. In 2025, CMC Telecom partnered with BBIX to launch two new Internet Exchange (IX) points at data centers in Hanoi and Ho Chi Minh City, boosting connectivity options and enhancing low‑latency services crucial for edge computing deployments. These modular units bring computing closer to data sources in industrial, logistics, and urban areas, while telcos extend services with containerized deployments.

Sustainability and Energy Efficiency Shaping Next-Generation Container Designs

Environmental sustainability has become a defining characteristic of new containerized data center deployments in Vietnam. Operators are incorporating advanced thermal management solutions, including liquid cooling systems and intelligent airflow optimization, to achieve superior power usage effectiveness suited to the tropical climate. In December 2025, BIM Energy and Evolution Data Centres signed a Memorandum of Understanding to supply 50 to 100 MW of renewable electricity via DPPA to a large-scale Ho Chi Minh City data center, supporting cloud and AI infrastructure. Government sustainability targets are further encouraging containerized solutions that inherently offer improved energy efficiency through compact, purpose-built designs.

Convergence of Artificial Intelligence Workloads and Modular Infrastructure

The rapid expansion of artificial intelligence and machine learning applications across Vietnamese enterprises is creating specialized demand for high-density containerized computing environments. Organizations are deploying purpose-built container units equipped with advanced graphics processing capabilities and enhanced cooling architectures to support training and inference workloads. In August 2025, FPT Corporation inaugurated the FPT Fornix HCM02 data center in Ho Chi Minh City, built to international standards to support AI, cloud computing and digital transformation workloads, highlighting enterprise demand for high‑performance infrastructure. This trend is strong in financial services, e-commerce, and telecom, as modular containerized solutions enable scalable, incremental intelligent automation deployment.

Market Outlook 2026-2034:

The Vietnam containerized data center market is poised for sustained expansion over the forecast period, underpinned by accelerating digital transformation across government and private sectors, stringent data sovereignty regulations, and the country's emergence as a strategic technology infrastructure destination in Southeast Asia. The convergence of expanding cloud adoption, edge computing proliferation, and increasing foreign direct investment in digital infrastructure is expected to generate substantial revenue opportunities. Growing enterprise demand for rapidly deployable, scalable modular solutions will continue driving adoption across diverse industry verticals and geographic regions throughout the forecast period. The market generated a revenue of USD 62.12 Million in 2025 and is projected to reach a revenue of USD 290.19 Million by 2034, growing at a compound annual growth rate of 18.68% from 2026-2034.

Vietnam Containerized Data Center Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type of Container |

40 FT Container |

46.8% |

|

Organization Size |

Large Organization |

52.4% |

|

Application |

Greenfield |

44.6% |

|

End Use Industry |

IT and Telecommunications |

36.9% |

|

Region |

Southern Vietnam |

41.3% |

Type of Container Insights:

- 20 FT Container

- 40 FT Container

- Customized Container

40 FT container dominates with a market share of 46.8% of the total Vietnam containerized data center market in 2025.

The 40 FT container dominates the Vietnam containerized data center market, primarily attributed to its optimal balance between physical capacity and deployment versatility. These standardized units provide sufficient internal volume to accommodate comprehensive IT rack configurations, redundant power distribution systems, and integrated precision cooling infrastructure within a single transportable enclosure. In August 2025, Schneider Electric showcased a prefabricated containerized data center at Vietnam’s National Achievements Exhibition, demonstrating rapid deployment, flexible scalability, and AI-ready infrastructure for national digital transformation.

Furthermore, the 40 FT container supports high-density computing configurations that are increasingly essential for cloud hosting, artificial intelligence workloads, and telecommunications backbone operations. The ability to configure these units with advanced fire suppression, environmental monitoring, and remote management systems enables operators to achieve reliable uptime standards without extended construction timelines associated with traditional facilities. As Vietnam's digital economy continues to mature, this segment is expected to maintain its leading position due to proven operational efficiency.

Organization Size Insights:

- Small Organization

- Midsize Organization

- Large Organization

Large organization leads with a share of 52.4% of the total Vietnam containerized data center market in 2025.

Large organizations represent the dominant adopter segment within the Vietnam containerized data center market, driven by their substantial data processing requirements and the strategic imperative to maintain robust, geographically distributed computing infrastructure. These enterprises, spanning telecommunications, banking, e-commerce, and government sectors, generate enormous volumes of transactional and operational data necessitating reliable, high-availability processing environments. As per sources, Vietnam’s Ministry of Public Security commissioned National Data Center No. 1 in Hoa Lac, a national‑level facility supporting government and enterprise digital services with 1,300 server racks and high‑security infrastructure.

The preference among large organizations for containerized deployments is further reinforced by their operational scale and the need for standardized, repeatable infrastructure solutions across multiple sites. By adopting modular container-based architectures, these enterprises achieve greater consistency in performance benchmarks, security configurations, and maintenance procedures across their entire data center portfolio. The ability to pre-test and validate complete containerized units in factory environments before shipment significantly reduces deployment risks and accelerates time-to-service for complex technology ecosystems.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Greenfield

- Brownfield

- Upgrade and Consolidation

Greenfield exhibits a clear dominance with a 44.6% share of the total Vietnam containerized data center market in 2025.

Greenfield leads the Vietnam containerized data center market as organizations increasingly establish entirely new data center facilities to address the country's growing digital infrastructure deficit. Vietnam's expanding industrial zones, special economic areas, and newly developed technology parks provide ideal locations for greenfield containerized deployments, where the absence of existing legacy infrastructure allows for optimal site planning and modern design implementation. Government initiatives promoting digital economy development and data sovereignty are encouraging new facility development from the ground up.

Greenfield deployments also benefit from the flexibility to incorporate the latest energy-efficient technologies and cooling solutions from inception, avoiding the retrofit complexities associated with existing facilities. Organizations selecting greenfield sites can optimize their power distribution architectures, network connectivity, and physical security arrangements specifically for containerized configurations, resulting in superior operational efficiency and lower total cost of ownership. The ability to phase construction by deploying additional container units incrementally makes greenfield projects particularly attractive for operators managing capital expenditure prudently.

End Use Industry Insights:

- BFSI

- IT and Telecommunications

- Government

- Education

- Healthcare

- Defense

- Entertainment and Media

- Others

IT and telecommunications lead with a market share of 36.9% of the total Vietnam containerized data center market in 2025.

IT and telecommunications represent the largest end-use industry for containerized data centers in Vietnam, reflecting the sector's central role in driving the country's digital infrastructure buildout. Telecommunications operators are deploying containerized units to support the rapid expansion of advanced mobile network infrastructure, requiring distributed computing nodes positioned at cell tower sites, aggregation points, and network backbone locations. According to reports, in 2025, Vietnam launched the first international terrestrial cable line (VSTN) linking Danang to Singapore via Laos, Thailand, and Malaysia, enhancing cross‑border telecom connectivity crucial for data centers and edge deployments.

The convergence of increasing internet penetration, expanding digital service consumption, and enterprise migration to software-as-a-service applications is generating sustained demand for scalable telecommunications infrastructure across Vietnam. Containerized data centers provide IT and telecom operators with the agility to respond to localized demand surges, deploy capacity in underserved regions, and support content delivery requirements of a rapidly growing online user base. The sector's inherent need for standardized, remotely manageable infrastructure makes containerized solutions operationally superior for network-edge deployment scenarios.

Regional Insights:

- Northern Vietnam

- Central Vietnam

- Southern Vietnam

Southern Vietnam dominates with a market share of 41.3% of the total Vietnam containerized data center market in 2025.

Southern Vietnam maintains its leading position in the containerized data center market due to the region's unmatched economic dynamism and its role as the country's primary commercial and technology hub. The concentration of multinational enterprises, financial institutions, e-commerce platforms, and technology companies in the southern economic corridor creates substantial demand for proximate, high-performance computing infrastructure. The region's well-developed industrial zones and special economic areas offer suitable sites for containerized deployments with established power grid connectivity and fiber-optic network infrastructure.

Additionally, Southern Vietnam benefits from its strategic position as a gateway for international connectivity, with proximity to major submarine cable landing stations enabling low-latency connections to regional and global networks. The concentration of foreign direct investment in the southern provinces, particularly in technology manufacturing and digital services, generates sustained demand for enterprise-grade data center capacity. Containerized solutions are particularly well-suited to this environment, enabling operators to deploy capacity quickly in response to investment-driven demand fluctuations while maintaining operational flexibility.

Market Dynamics:

Growth Drivers:

Why is the Vietnam Containerized Data Center Market Growing?

Accelerating Data Sovereignty Regulations and Localization Mandates

Vietnam's enactment of comprehensive data protection and localization legislation is compelling organizations to establish domestically located data processing infrastructure at an unprecedented pace. These regulatory frameworks require enterprises operating within Vietnam to store and process personal data within national boundaries, driving multinational corporations and domestic businesses alike to rapidly deploy local computing facilities. According to reports, Vietnam’s Parliament adopted the Law on Data (No. 60/2024/QH15) including data localization requirements that mandate core and important data be stored within Vietnam, particularly in the National Data Center, to ensure security and compliance. Moreover, containerized data centers provide the fastest pathway to regulatory compliance, enabling organizations to commission fully operational infrastructure within weeks rather than the extended timelines required for conventional facility construction, significantly accelerating market adoption across all industry sectors.

Rapid Cloud Computing Adoption Fueling Infrastructure Demand

The exponential growth of cloud service adoption across Vietnamese enterprises is fundamentally reshaping infrastructure investment patterns and driving substantial demand for containerized solutions. As organizations migrate applications and workloads to cloud-based platforms, service providers must establish distributed points of presence to deliver acceptable performance levels across the country's geographically dispersed user base. As per sources in August 2024, Cloud4C launched a high‑availability data center in Hanoi in partnership with Viettel IDC to boost locally compliant cloud solutions for Vietnamese enterprises, reflecting rising enterprise demand for on‑shore cloud and infrastructure capacity.

Competitive Cost Structure Attracting Foreign Investment Inflows

Vietnam's significantly lower construction and operational costs compared to established regional technology hubs are creating a compelling economic proposition for containerized data center investment. The country's favorable cost environment for land acquisition, labor, and power consumption provides substantial savings for infrastructure developers compared to markets across Southeast Asia. This cost advantage, combined with government incentives targeting foreign direct investment in digital infrastructure and the removal of foreign ownership restrictions for data center operations, is attracting considerable international capital into the containerized segment and accelerating the pace of new facility deployments nationwide.

Market Restraints:

What Challenges the Vietnam Containerized Data Center Market is Facing?

Power Grid Infrastructure Limitations and Reliability Concerns

The capacity and reliability of Vietnam's electrical power distribution network present a significant constraint for containerized data center expansion, particularly in secondary cities and emerging industrial zones where grid infrastructure has not kept pace with digital economy growth. Inconsistent power quality and limited availability of high-capacity electrical feeds force operators to invest in substantial backup generation equipment.

Regulatory Complexity and Multi-Agency Permitting Delays

The evolving regulatory landscape governing data center operations in Vietnam, encompassing licensing, environmental compliance, foreign investment approvals, and telecommunications permits, creates administrative complexity that can delay containerized deployment timelines. The practical execution of multi-agency approval processes often introduces uncertainty, particularly for operators establishing facilities in new geographic locations across different provincial jurisdictions.

Skilled Workforce Shortages for Specialized Modular Operations

The limited availability of technically qualified professionals with expertise in data center operations, advanced cooling systems, and modular infrastructure management constrains the pace of market expansion in Vietnam. While the country possesses a growing information technology talent pool, specialized skill sets required for deploying and maintaining high availability containerized environments remain scarce, increasing operational costs.

Competitive Landscape:

The Vietnam containerized data center market features a dynamic competitive landscape characterized by the participation of both established domestic technology infrastructure providers and international modular data center specialists seeking to capitalize on the country’s growth trajectory. Market participants are differentiating through advanced container design innovations, superior energy efficiency performance, comprehensive managed service offerings, and strategic partnerships with cloud service platforms. Competition is intensifying as operators expand beyond traditional metropolitan deployments into secondary cities and industrial zones, leveraging containerized solutions to establish first-mover advantages in underserved markets.

Recent Developments:

-

In August 2025, Cyprus-based IPTP Networks announced the AIDC DeCenter project at Da Nang Hi-Tech Park, Vietnam. The $200m AI-ready facility, developed with DeCenter AI and MCB Ventures, will be built in phases starting Q4 2025, offering scalable capacity and advanced digital infrastructure solutions.

Vietnam Containerized Data Center Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types of Containers Covered |

20 FT Container, 40 FT Container, Customized Container |

|

Organization Sizes Covered |

Small Organization, Midsize Organization, Large Organization |

|

Applications Covered |

Greenfield, Brownfield, Upgrade and Consolidation |

|

End Use Industries Covered |

BFSI, IT and Telecommunications, Government, Education, Healthcare, Defense, Entertainment and Media, Others |

|

Regions Covered |

Northern Vietnam, Central Vietnam, Southern Vietnam |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Vietnam Containerized Data Center Market Report

The Vietnam containerized data center market size was valued at USD 62.12 Million in 2025.

The Vietnam containerized data center market is expected to grow at a compound annual growth rate of 18.68% from 2026-2034 to reach USD 290.19 Million by 2034.

40 FT container held the largest share, driven by its superior capacity to accommodate comprehensive IT infrastructure, integrated cooling, and power systems within a standardized, transportable unit that aligns with global logistics frameworks.

Key factors driving the Vietnam containerized data center market include accelerating digital transformation mandates, stringent data sovereignty regulations requiring domestic data processing, rapid cloud computing adoption, expanding edge infrastructure requirements, and competitive deployment cost advantages.

Major challenges include power grid infrastructure limitations in emerging deployment locations, regulatory complexity involving multi-agency licensing and permitting processes, skilled workforce shortages for specialized modular operations, and evolving compliance frameworks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)