Vietnam Data Center Market Size, Share, Trends and Forecast by Data Center Size, Tier Type, Absorption, and Region, 2026-2034

Vietnam Data Center Market Summary:

The Vietnam data center market size was valued at USD 1.2 Billion in 2025 and is projected to reach USD 2.3 Billion by 2034, growing at a compound annual growth rate of 7.98% from 2026-2034.

The Vietnam data center market is accelerating as the country emerges as a strategic digital infrastructure hub in Southeast Asia. Rapid expansion in cloud computing demand, supportive regulatory reforms eliminating foreign ownership restrictions, and the growing enterprise digitalization are driving substantial investment inflows. Advancements in hyperscale facility development, increasing artificial intelligence (AI) workload requirements, and competitive construction cost advantages are reshaping the infrastructure landscape, positioning Vietnam as a leading destination for next-generation data center deployments.

Key Takeaways and Insights:

- By Data Center Size: Large leads the market with a share of 32% in 2025, driven by its ability to deliver scalable infrastructure to meet the growing enterprise and cloud service provider requirements while offering cost-efficient operations across Vietnamese industrial zones.

- By Tier Type: Tier 3 represents the largest segment with a market share of 60% in 2025, reflecting enterprise preference for concurrent maintainability standards that ensure uninterrupted operations for mission-critical banking, telecommunications, and government workloads across the country.

- By Absorption: Utilized dominates the market with a share of 71% in 2025, underscoring strong occupancy levels across Vietnamese colocation facilities as domestic and multinational enterprises expand their digital footprint in the country.

- Key Players: The Vietnam data center market features a competitive landscape with state-owned telecommunications operators, domestic technology firms, and international infrastructure providers vying for market share through hyperscale investments, strategic partnerships, and green data center initiatives.

The Vietnam data center market is being driven by rapid digital transformation across industries, as enterprises expand their reliance on cloud computing, digital banking, e-commerce, and online services. Rising connectivity and telecom infrastructure development are increasing data traffic, strengthening the demand for secure and scalable storage and processing capacity. Government initiatives focused on digital governance and data sovereignty are also accelerating domestic infrastructure growth. This direction was reinforced in 2025 when Vietnam officially launched its National Data Center under the new 2025 Data Law effective July 1, 2025. Built and managed by the Ministry of Public Security, the NDC serves as a centralized hub for storing, processing, and securing national data through advanced cloud infrastructure, high-performance computing, and an open National Data Portal. Alongside foreign investment, AI workload expansion, and cybersecurity priorities, these developments are sustaining strong market momentum.

Vietnam Data Center Market Trends:

Increasing Demand for Data Sovereignty and Local Hosting

The Vietnam data center market is being increasingly driven by the emphasis on data sovereignty and the need for secure domestic data hosting. Enterprises and government bodies are prioritizing local storage of sensitive information to strengthen compliance, security, and control over national data governance. This push is encouraging major investments in large-scale infrastructure. For example, in 2025, Vietnam officially launched National Data Center No. 1 at Hoa Lac Hi-Tech Park in Hanoi, spanning over 20 hectares and recognized with top international certifications for security and disaster resilience. The center was expected to serve as the “heart” of Vietnam’s digital transformation, supporting national databases, faster public services, and the growth of AI and the digital economy.

Growth of Foreign Direct Investment and Global Enterprise Presence

As multinational companies establish regional operations, there is a rise in the demand for internationally compliant infrastructure that can support enterprise IT workloads, cloud connectivity, and secure data management. This trend is encouraging partnerships and large-scale capacity development across the sector. For instance, in 2025, South Korea’s LG CNS announced plans to develop a hyperscale AI data center in Vietnam through an MoU with VNPT and Korea Investment Real Asset Management, covering facility construction, servers, storage, and advanced network connectivity. Such investments strengthen Vietnam’s position as an emerging regional digital infrastructure hub.

Rising Cloud Adoption Among Enterprises

The increasing shift of enterprises in Vietnam toward cloud computing is influencing the market, as organizations require scalable infrastructure to support remote operations, digital workloads, and secure service delivery. This transition is driving the demand for colocation, hybrid, and hyperscale environments capable of hosting cloud platforms efficiently. Investment activity reflects this momentum, as in 2025 Cyprus-based IPTP Networks announced the AIDC DeCenter project in Da Nang Hi-Tech Park, beginning with a USD 20 Million first phase delivering 10MW capacity within a broader USD 200 Million plan. Such developments highlight the expanding infrastructure needed to sustain Vietnam’s growing cloud and AI ecosystem.

Market Outlook 2026-2034:

The Vietnam data center market demonstrates strong growth potential throughout the forecast period, driven by irreversible digital transformation trends and expanding hyperscale investments. The market generated a revenue of USD 1.2 Billion in 2025 and is projected to reach a revenue of USD 2.3 Billion by 2034, growing at a compound annual growth rate of 7.98% from 2026-2034. Rising cloud adoption, AI infrastructure development, regulatory liberalization, and competitive cost advantages are expected to sustain robust revenue expansion across the Vietnamese data center ecosystem.

Vietnam Data Center Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Data Center Size |

Large |

32% |

|

Tier Type |

Tier 3 |

60% |

|

Absorption |

Utilized |

71% |

Data Center Size Insights:

To get detailed segment analysis of this market, Request Sample

- Large

- Massive

- Medium

- Mega

- Small

Large dominates with a market share of 32% of the total Vietnam data center market in 2025.

Large leads the market driven by the rapid growth in digital services, cloud adoption, and rising demand for high-capacity computing infrastructure. Enterprises, hyperscale cloud providers, and telecom operators require large scale facilities to support expanding workloads, data storage needs, and real time processing requirements. Large data center offers greater operational efficiency, economies of scale, and the ability to host multiple tenants. As Vietnam’s digital economy grows, demand continues to shift toward larger facilities capable of supporting advanced IT ecosystems.

The dominance of large Vietnam data center colocation market is further reinforced by increasing investments in e-commerce, fintech, streaming services, and government digital transformation programs. These sectors generate significant data volumes that require secure, reliable, and scalable infrastructure. Large facilities are also better positioned to integrate advanced cooling systems, energy management solutions, and redundancy frameworks that ensure uninterrupted service. As international technology firms expand their presence and local enterprises modernize IT operations, large data centers remain the preferred choice, supporting Vietnam’s long term data infrastructure development.

Tier Type Insights:

- Tier 1 and 2

- Tier 3

- Tier 4

Tier 3 leads with a market share of 60% of the total Vietnam data center market in 2025.

Tier 3 represents the largest segment because of its balance of high reliability, cost effectiveness, and operational flexibility. This facility provides multiple power and cooling distribution paths with redundancy, ensuring minimal downtime and strong service continuity. Enterprises, cloud providers, and telecom operators increasingly prefer Tier 3 infrastructure to support mission critical workloads without the higher costs associated with facilities. As Vietnam’s digital economy expands, Tier 3 data center offers an optimal standard for secure and resilient operations.

The dominance of Tier 3 is further supported by the growing demand from industries, such as banking, e-commerce, IT services, and government digital platforms that require dependable data hosting environments. Tier 3 enables concurrent maintainability, allowing equipment servicing without disrupting operations, which is essential for continuous service delivery. It also meets international expectations for uptime and security, making it attractive for foreign investment and regional data hub development. As data localization requirements and cloud adoption rise, Tier 3 continues to lead Vietnam’s data center market.

Absorption Insights:

- Non-Utilized

- Utilized

Utilized exhibits a clear dominance with a 71% share of the total Vietnam data center market in 2025.

Utilized holds the biggest marker share owing to the growing demand for operational space driven by rapid digitalization and increasing data usage. Enterprises, cloud providers, and telecom operators are actively leasing and filling available capacity to support expanding workloads, digital services, and online platforms. High utilization reflects the growing need for secure data storage, low latency connectivity, and scalable computing infrastructure. As Vietnam’s economy becomes more digitally connected, absorption rates remain high, reinforcing the dominance of utilized capacity within the market.

The dominance of utilized is further strengthened by rising investments in e-commerce, fintech, streaming services, and smart city initiatives, all of which generate significant data traffic. Businesses are prioritizing ready to deploy colocation and cloud environments rather than building in-house infrastructure, accelerating capacity take-up. Limited supply of high-quality facilities in key urban hubs also contributes to faster occupancy levels. As new capacity comes online, demand continues to absorb it quickly, supporting sustained growth in Vietnam’s data center sector.

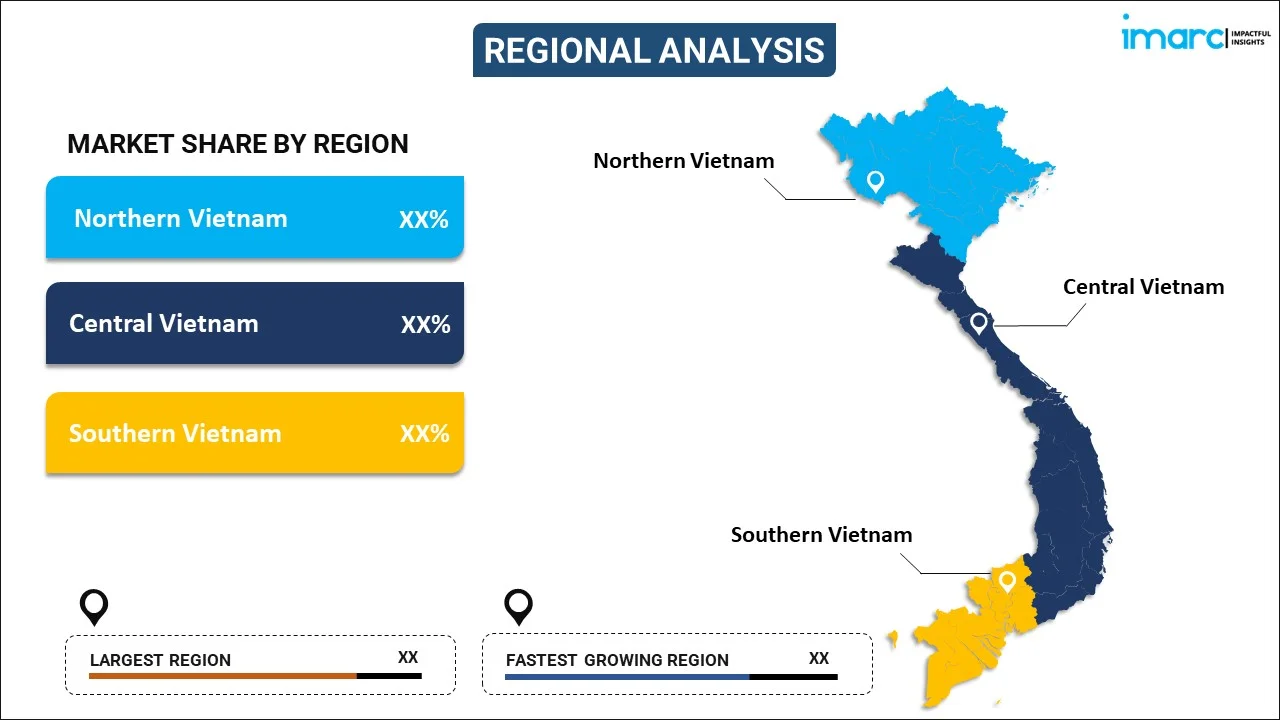

Regional Insights:

To get detailed regional analysis of this market, Request Sample

- Northern Vietnam

- Central Vietnam

- Southern Vietnam

Northern Vietnam is emerging as a crucial segment in the market, supported by expanding industrial activity and proximity to Hanoi’s digital economy. Rising demand from government platforms, financial institutions, and technology firms is encouraging new investments in reliable data infrastructure, strengthening the region’s role in national connectivity and cloud expansion. In 2025, Viettel broke ground on major projects including the An Khanh Data Center and a large-scale R&D Center at Hoa Lac Hi-Tech Park in Hanoi. The 60 MW An Khanh Data Center, expected to begin operations in Q2 2026, will strengthen Vietnam’s hyperscale digital infrastructure and accelerate national AI-driven transformation.

Central Vietnam benefits from its strategic geographic location and improving infrastructure. The region offers opportunities for future capacity development, supporting redundancy and network balance across the country. The growing tourism, logistics, and regional digitalization initiatives are contributing to the rising demand for modern data facilities.

Southern Vietnam remains a vital segment in the Vietnam data center market, driven by Ho Chi Minh City’s concentration of enterprises, cloud providers, and digital service companies. Strong commercial activity, high internet usage, and foreign investment are accelerating capacity expansion. The region benefits from advanced connectivity, making it a key center for scalable data infrastructure.

Market Dynamics:

Growth Drivers:

Why is the Vietnam Data Center Market Growing?

Increasing Energy Efficiency and Green Infrastructure Requirements

The growing focus on energy efficiency and sustainable infrastructure development, as operators seek to manage high power usage while reducing long-term operating costs, is influencing the market. Data center developers are investing in advanced cooling technologies, optimized power management, and renewable energy integration to meet performance and sustainability expectations. This shift is reflected in major investments, including CMC Corporation’s announcement in 2025 of a USD 250 Million hyperscale green data center in Ho Chi Minh City, designed to scale from 30 MW to 120 MW using renewable energy. Such initiatives reinforce the importance of energy-efficient data center models in shaping future capacity expansion and market growth.

Expansion of Domestic Data Center Capacity

The Vietnam data center market is driven by active capacity expansion from established domestic technology companies seeking to strengthen national digital infrastructure. Local operators are investing in large, modern facilities to support the growing enterprise demand for secure hosting, flexible connectivity, and scalable workloads. This trend is reflected in 2025 when FPT Corporation inaugurated the FPT Fornix HCM02 Data Center at Ho Chi Minh City High-Tech Park, its fourth facility nationwide, spanning 10,000 square meters and capable of hosting 3,600 racks. Such investments enhance carrier-neutral connectivity, improve cost efficiency, and reinforce Vietnam’s digital sovereignty, supporting the market growth.

Rapid Growth in Digital Economy and Online Services

The Vietnam data center market is driven by the rapid expansion of the country’s digital economy, fueled by rising adoption of e-commerce, digital banking, online education, and cloud-based services. As businesses increasingly depend on digital platforms, there is a rise in the demand for secure, high-capacity infrastructure to support data storage and processing needs. This momentum is reflected in major hyperscale investments, including G42’s 2025 announcement with Vietnamese partners, such as FPT, VinaCapital, and Viet Thai Group to develop a USD 2 Billion data center in Ho Chi Minh City. Designed as an “AI factory,” the project aimed to deliver advanced cloud and AI infrastructure for customers across Asia while boosting Vietnam’s digital economy. Such projects reinforce the need for scalable facilities supporting Vietnam’s digital competitiveness.

Market Restraints:

What Challenges the Vietnam Data Center Market is Facing?

Power Grid Reliability and Energy Supply Constraints

Vietnam's electricity grid faces capacity and reliability challenges that pose operational risks for power-intensive data center operations. Periodic power shortages, particularly in southern regions, including Ho Chi Minh City, can disrupt service continuity. Meeting the surging energy demands of hyperscale facilities requires substantial grid modernization investments, creating uncertainty for operators dependent on stable, uninterrupted power supply for mission-critical workloads.

Complex Regulatory and Licensing Frameworks

Data center developers face a multi-layered regulatory environment involving intricate licensing procedures, land use restrictions, and zoning approval processes. Foreign investors can lease land only through industrial parks or designated zones, limiting site selection flexibility. Environmental permitting requirements and evolving cybersecurity compliance mandates add procedural complexity, potentially extending project timelines and increasing pre-development costs for domestic and international operators.

Limited International Connectivity Infrastructure

Vietnam's reliance on a limited number of operational submarine cable routes creates vulnerability to service disruptions that can affect data center operations and client confidence. Cable outages have historically caused significant connectivity degradation, impacting latency-sensitive applications. While the government is actively addressing this limitation, current infrastructure constraints may deter latency-critical deployments by global hyperscalers until additional capacity becomes operational.

Competitive Landscape:

The Vietnam data center market features a dynamic competitive landscape characterized by the participation of state-owned telecommunications operators, domestic technology conglomerates, and international infrastructure providers. Competition is intensifying as operators pursue hyperscale development, green data center certifications, and AI-ready infrastructure capabilities to differentiate their offerings. Strategic partnerships between domestic enterprises and international technology companies are reshaping market dynamics, enabling knowledge transfer and accelerating deployment timelines. The market is witnessing increasing investment from foreign operators leveraging Vietnam's cost advantages, regulatory liberalization, and strategic geographic positioning as an alternative to capacity-constrained hubs in the region.

Recent Developments:

- December 2025: HITC International Telecommunication JSC partnered with Evolution Data Centers through a joint venture to develop AI and hyperscale data centers in Ho Chi Minh City and Hanoi. The collaboration aimed to deliver sustainable, high-performance digital infrastructure to meet Vietnam’s fast-rising demand for cloud and AI services.

- November 2025: Vietnamese industrial park developer Kinh Bac City Development Holding (KBC) signed an MoU with Accelerated Infrastructure Capital (AIC) and VietinBank to build a massive $2 billion AI-focused data center campus in Ho Chi Minh City. Planned across 10 hectares in Tan Phu Trung Industrial Park, the facility will have an IT load capacity of up to 200 MW and support around 100,000 GPUs. The project was expected to strengthen HCMC’s digital infrastructure and position Vietnam as a rising regional hub for hyperscale data centers and AI development.

Vietnam Data Center Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Data Center Sizes Covered | Large, Massive, Medium, Mega, Small |

| Tier Types Covered | Tier 1 and 2, Tier 3, Tier 4 |

| Absorptions Covered | Non-Utilized, Utilized |

| Regions Covered | Northern Vietnam, Central Vietnam, Southern Vietnam |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Vietnam Data Center Market Report

The Vietnam data center market size was valued at USD 1.2 Billion in 2025.

The Vietnam data center market is expected to grow at a compound annual growth rate of 7.98% from 2026-2034 to reach USD 2.3 Billion by 2034.

Tier 3 holds the largest revenue share of 60% in 2025, driven by enterprise demand for concurrent maintainability standards that ensure reliable operations for mission-critical banking, telecommunications, and government applications across the country.

Key factors driving the Vietnam data center market include rising multinational expansion, which is driving the demand for internationally compliant infrastructure to support enterprise IT, cloud connectivity, and secure data management. In 2025, LG CNS signed an MoU with VNPT to develop a hyperscale AI data center.

Major challenges include power grid reliability constraints and periodic energy supply shortages, complex regulatory and licensing frameworks involving land use restrictions and zoning approvals, limited international submarine cable connectivity creating service disruption risks, and high upfront capital requirements for hyperscale facility development.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade