Vietnam Digital Banking Platform Market Size, Share, Trends and Forecast by Component, Type, Deployment Mode, Banking Mode, and Region, 2026-2034

Vietnam Digital Banking Platform Market Overview:

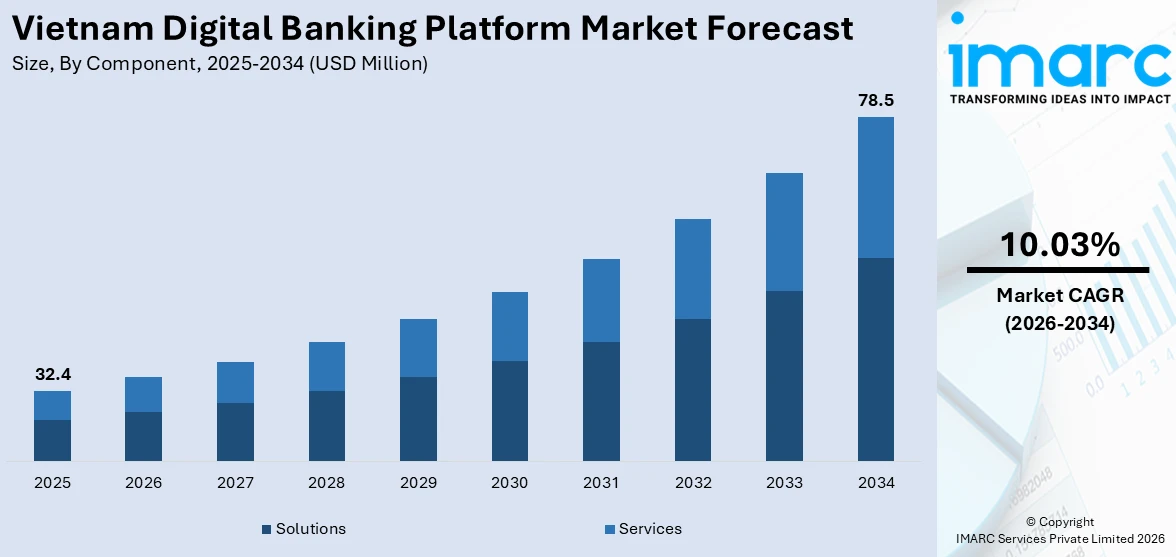

The Vietnam digital banking platform market size reached USD 32.4 Million in 2025. The market is projected to reach USD 78.5 Million by 2034, exhibiting a growth rate (CAGR) of 10.03% during 2026-2034. The market is driven by the rising smartphone and internet penetration, increasing consumer preference for cashless transactions, and a young, tech-savvy population open to innovative financial services. Supportive government policies, such as the national e-payment strategy, along with fintech partnerships, encourage digital banking adoption. Enhanced convenience, faster services, and competitive offerings from both traditional banks and neobanks further Vietnam digital banking platform market share. Additionally, the COVID-19 pandemic accelerated digital payment usage, solidifying digital banking as a mainstream financial channel.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 32.4 Million |

| Market Forecast in 2034 | USD 78.5 Million |

| Market Growth Rate 2026-2034 | 10.03% |

Vietnam Digital Banking Platform Market Trends:

Rapid Smartphone and Internet Penetration

Vietnam has witnessed remarkable growth in smartphone adoption and internet connectivity, laying a strong foundation for digital banking platforms. By early 2024, the country had 100.7 million smartphone subscriptions, with a penetration rate exceeding 84%, surpassing the global average of 63%. High-speed internet is widely available in urban areas and expanding in rural regions, enabling consumers to access banking services via apps and web platforms with ease. This digital infrastructure supports convenient, anytime, anywhere transactions, appealing especially to younger generations and urban professionals. Banks and fintechs make use of this interconnection to provide frictionless services, such as online account opening, instant fund transfer, QR-based payments, and digital wallets, leading to mass adoption and increased transaction volumes. Mobile banking has thereby become more convenient, secure, and preferable than branch-based banking, towards a digital-first financial ecosystem thereby contributing to the Vietnam digital banking platform market growth.

To get more information on this market Request Sample

Government Policies and Regulatory Support

Vietnam’s digital banking sector is poised for strong growth, projected to generate over $1 billion in revenue by 2025, driven by a tech-savvy population seeking convenience and innovation. This expansion aligns with robust government initiatives, such as the National Digital Transformation Program 2025 and the push for a cashless economy, which encourage banks and fintechs to develop advanced digital platforms. The State Bank of Vietnam has implemented regulations enabling e-KYC, digital signatures, and secure mobile transactions, simplifying onboarding and building consumer trust. Public-private collaborations further support innovation through fintech partnerships, open banking, and e-wallet integration. By reducing fraud and cybersecurity risks, these policies foster confidence in digital financial services. Collectively, Vietnam’s supportive regulatory environment and growing consumer demand create a fertile ecosystem for technology-driven banking solutions, accelerating digital adoption and enabling banks to compete effectively in a rapidly evolving market.

Changing Consumer Behavior and Tech-Savvy Population

Another important Vietnam digital banking platform market trend is a young, technology-literate, and increasingly comfortable population with technology-based services. Convenience, speed, and smooth customer experiences are valued by Gen Z and millennials, with mobile apps being their go-to, and they are less inclined towards physical branches. Consumer behavior is also driven by urbanization, increasing incomes, and a growing e-commerce segment, which necessitate seamless payment and banking solutions. Digital banking platforms accommodate these tastes with functions such as instant transfers, bill payments, investment and savings features, and rewards programs. Fintech technologies, gamified interfaces, and customized financial services add further drivers of engagement. The COVID-19 pandemic accelerated this process by encouraging contactless payments, building confidence in digital channels. With customers increasingly demanding efficiency and digital convenience, banks providing solid, easy-to-use platforms command competitive positions in Vietnam's changing financial scene.

Vietnam Digital Banking Platform Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on component, type, deployment mode, and banking mode.

Component Insights:

- Solutions

- Services

The report has provided a detailed breakup and analysis of the market based on the component. This includes solutions and services.

Type Insights:

Access the comprehensive market breakdown Request Sample

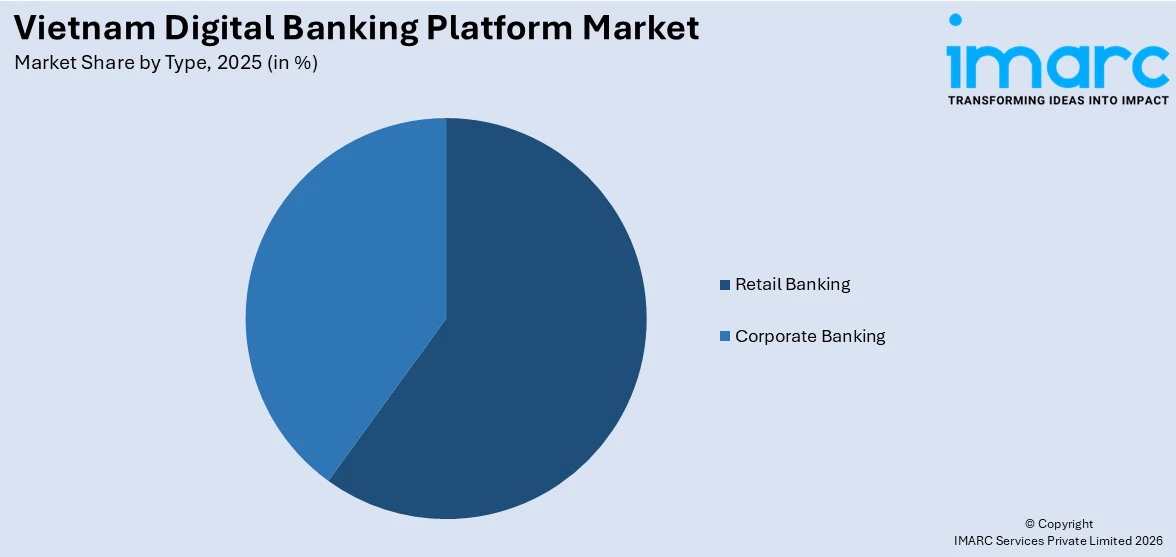

- Retail Banking

- Corporate Banking

A detailed breakup and analysis of the market based on the type have also been provided in the report. This includes retail banking and corporate banking.

Deployment Mode Insights:

- On-Premises

- Cloud-Based

A detailed breakup and analysis of the market based on the deployment mode have also been provided in the report. This includes On-premises, and cloud-based.

Banking Mode Insights:

- Online Banking

- Mobile Banking

The report has provided a detailed breakup and analysis of the market based on the banking mode. This includes online banking and mobile banking.

Regional Insights:

- Northern Vietnam

- Central Vietnam

- Southern Vietnam

The report has also provided a comprehensive analysis of all the major regional markets, which include Northern Vietnam, Central Vietnam, and Southern Vietnam.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Vietnam Digital Banking Platform Market News:

- In June 2025, Eximbank Vietnam launched a next-generation card management system using OpenWay’s Way4 platform, enhancing digital payments and customer experience. The system enables real-time processing, personalized card products, improved security, and operational efficiency, integrating global and domestic payment networks and e-wallets. It supports Eximbank’s retail and corporate banking platforms, automates card management, and scales with growing transaction volumes, strengthening the bank’s position as an innovator in Vietnam’s digital banking and payments sector.

- In June 2025, Saigon – Hanoi Commercial Bank (SHB) has launched SHB SAHA, its next-generation digital banking app, upgrading SHB Mobile with advanced technology, a user-friendly interface, and smart features. The app offers seamless omnichannel services, including transfers, bill payments, virtual cards, loans, and investments. Designed for speed, security, and convenience, SHB SAHA targets tech-savvy users, supports long-term financial planning, and represents a strategic step in SHB’s digital transformation toward becoming Vietnam’s leading “Bank of the Future.”

- In January 2025, Vietnam’s ABBANK launched ABBANK Business, a digital banking platform built on Backbase Engagement Banking Platform, aimed at enhancing SME banking experiences. The app offers fast, secure, and customizable services, including account management, bill payments, international transfers, and asset dashboards. Following a smooth three-month migration, 88% of active business clients now use the app as their main channel. The platform exemplifies ABBANK’s customer-centric strategy, improving efficiency, user experience, and digital transformation capabilities for corporate clients.

Vietnam Digital Banking Platform Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Solutions, Services |

| Types Covered | Retail Banking, Corporate Banking |

| Deployment Modes Covered | On-Premises, Cloud-Based |

| Banking Modes Covered | Online Banking, Mobile Banking |

| Regions Covered | Northern Vietnam, Central Vietnam, Southern Vietnam |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Vietnam digital banking platform market performed so far and how will it perform in the coming years?

- What is the breakup of the Vietnam digital banking platform market on the basis of component?

- What is the breakup of the Vietnam digital banking platform market on the basis of type?

- What is the breakup of the Vietnam digital banking platform market on the basis of deployment mode?

- What is the breakup of the Vietnam digital banking platform market on the basis of banking mode?

- What is the breakup of the Vietnam digital banking platform market on the basis of region?

- What are the various stages in the value chain of the Vietnam digital banking platform market?

- What are the key driving factors and challenges in the Vietnam digital banking platform market?

- What is the structure of the Vietnam digital banking platform market and who are the key players?

- What is the degree of competition in the Vietnam digital banking platform market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Vietnam digital banking platform market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Vietnam digital banking platform market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Vietnam digital banking platform industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)