Vietnam Electric Vehicle Charging Station Market Size, Share, Trends and Forecast by Charging Station Type, Vehicle Type, Installation Type, Charging Level, Connector Type, Application, and Region, 2026-2034

Vietnam Electric Vehicle Charging Station Market Size, Share, Trends & Forecast (2026-2034)

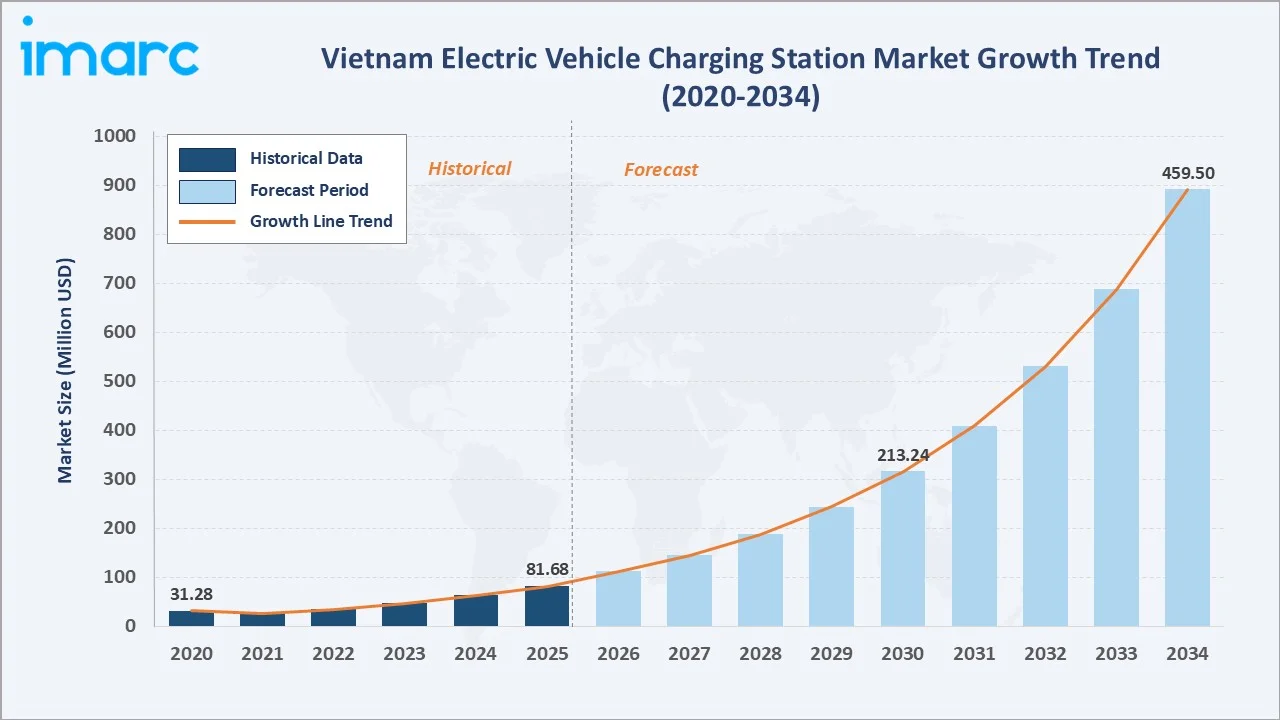

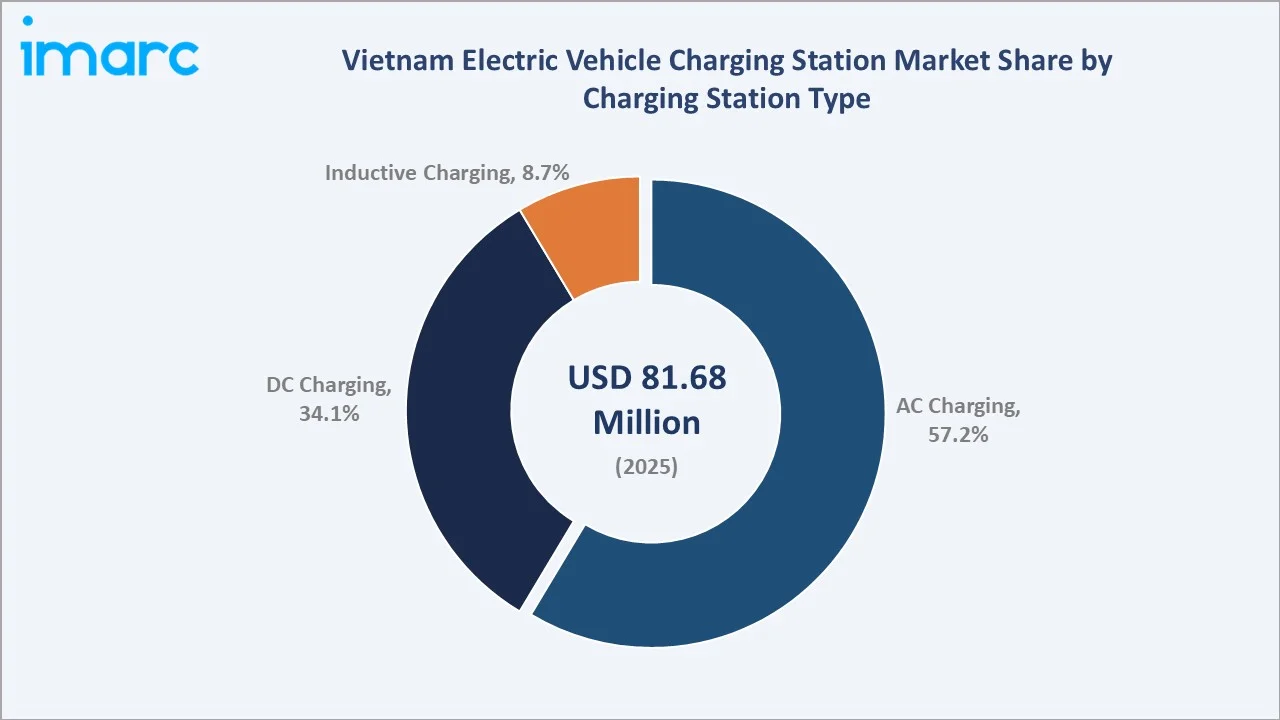

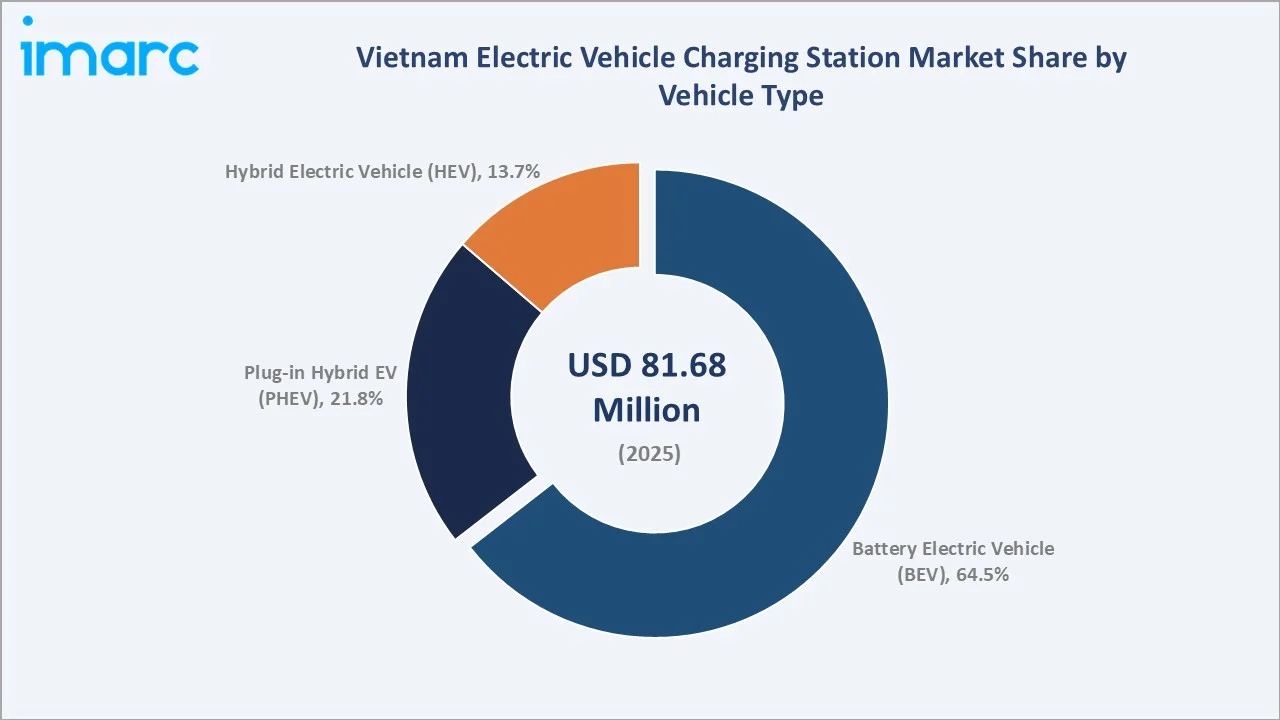

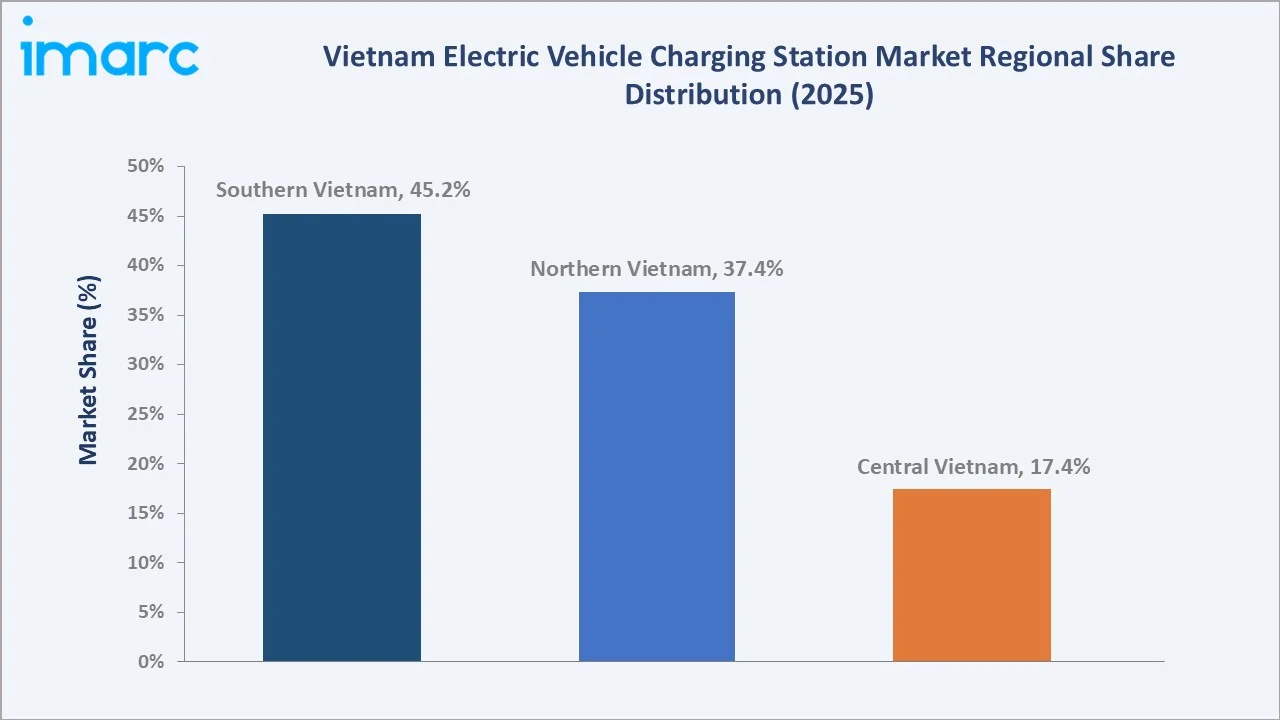

The Vietnam electric vehicle charging station market reached USD 81.68 Million in 2025 and is projected to reach USD 459.50 Million by 2034, growing at a CAGR of 21.16% during 2026-2034. The market is driven by rising EV adoption and strong domestic EV production. Vietnam is expected to have nearly 1 million EVs on the road by 2030, increasing to around 3.5 million by 2040. To support this growth, the International Energy Agency (IEA) recommended developing 100,000–350,000 charging stations over the next 15 years, equal to roughly one charger for every 10 EVs. This supports the market by highlighting the scale of infrastructure needed to match future EV adoption. AC charging leads at 57.2%. Battery electric vehicle (BEV) leads vehicle type at 64.5%. Southern Vietnam leads regionally at 45.2%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 81.68 Million |

|

Forecast Market Size (2034) |

USD 459.50 Million |

|

CAGR (2026-2034) |

21.16% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Charging Station Type |

AC Charging (57.2%, 2025) |

|

Dominant Vehicle Type |

Battery Electric Vehicle - BEV (64.5%, 2025) |

|

Leading Region |

Southern Vietnam (45.2%, 2025) |

Vietnam EV charging station market expanded from USD 31.28 Million in 2020 to USD 81.68 Million in 2025, anchored at USD 213.24 Million in 2030, and forecast to reach USD 459.50 Million by 2034, reflecting strong long-term expansion. This growth is supported by rising EV adoption, VinFast-led domestic EV production, government clean mobility goals, and increasing investment in public and fast-charging networks.

To get more information on this market, Request Sample

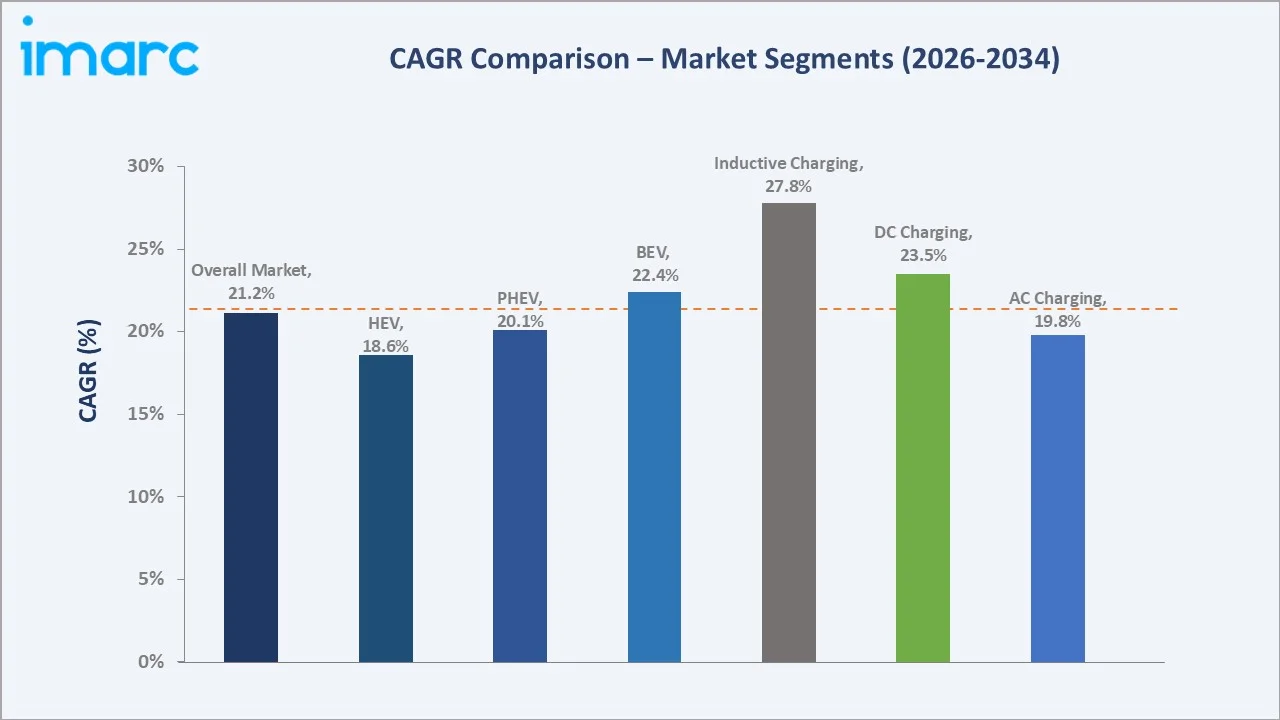

Inductive charging grows fastest at ~27.8% CAGR through VinFast electric taxi fleet wireless charging depot pilot and Vietnam's electric bus terminus inductive charging adoption. DC charging grows at ~23.5% CAGR through Vietnam's expressway DC fast charger deployment.

Executive Summary

Vietnam EV charging station market reached USD 81.68 Million in 2025. Increasing investment in public, residential, and fast-charging infrastructure is improving charging accessibility. Growing urban mobility demand and long-term EV fleet expansion are expected to strengthen market growth. The market is projected to reach USD 459.50 Million by 2034. AC charging at 57.2% leads the charging station type. BEV at 64.5% leads vehicle type through VinFast's BEV-only domestic production. Southern Vietnam leads regionally at 45.2% through EV concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Charging Station Type |

AC Charging - 57.2% share (2025) |

|

Dominant Vehicle Type |

Battery Electric Vehicle (BEV) - 64.5% market share (2025) |

|

Leading Region |

Southern Vietnam - 45.2% share (2025) |

|

Market Opportunity |

National Highway 1 DC fast charge corridor; solar EV charging hub Da Nang; VinFast V-Green residential smart charger; HCMC and Hanoi commercial property EVSE |

Key Analytical Observations Supporting The Above Data:

- AC Charging at 57.2%: The AC charging segment dominates due to its lower installation cost and suitability for residential, workplace, mall, and parking-based charging. Its ease of deployment makes it ideal for Vietnam’s urban EV adoption and routine daily charging needs.

- Battery Electric Vehicle (BEV) at 64.5%: The BEV segment dominates because fully electric vehicles depend entirely on external charging infrastructure. Rising BEV adoption, led by domestic EV production and expanding model availability, is increasing demand for public, residential, and fast-charging stations.

- Southern Vietnam at 45.2%: Southern Vietnam dominates regionally due to strong EV adoption, high urban density, and greater commercial activity in Ho Chi Minh City and surrounding industrial provinces. The region’s logistics hubs, malls, residential complexes, and transport corridors support faster charger deployment and higher utilization.

Vietnam Electric Vehicle Charging Station Market Overview

Vietnam EV charging station market operates within Vietnam's broader automotive transformation as the fastest-growing segment. The market’s commercial uniqueness lies in Vietnam’s strong domestic EV push led by VinFast, which is creating integrated demand for vehicles, charging networks, and mobility services. The market is also shaped by rapid urbanization, two-wheeler electrification potential, and the need for scalable charging infrastructure across dense cities and industrial corridors.

Vietnam EV charging station ecosystem integrates EVSE hardware importers, VinFast V-Green network, independent CPO, and regulatory frameworks. Macroeconomic factors include rapid urbanization, rising income levels, increasing fuel costs, and the government's focus on reducing transport emissions.

Market Dynamics

To evaluate market opportunities, Request Sample

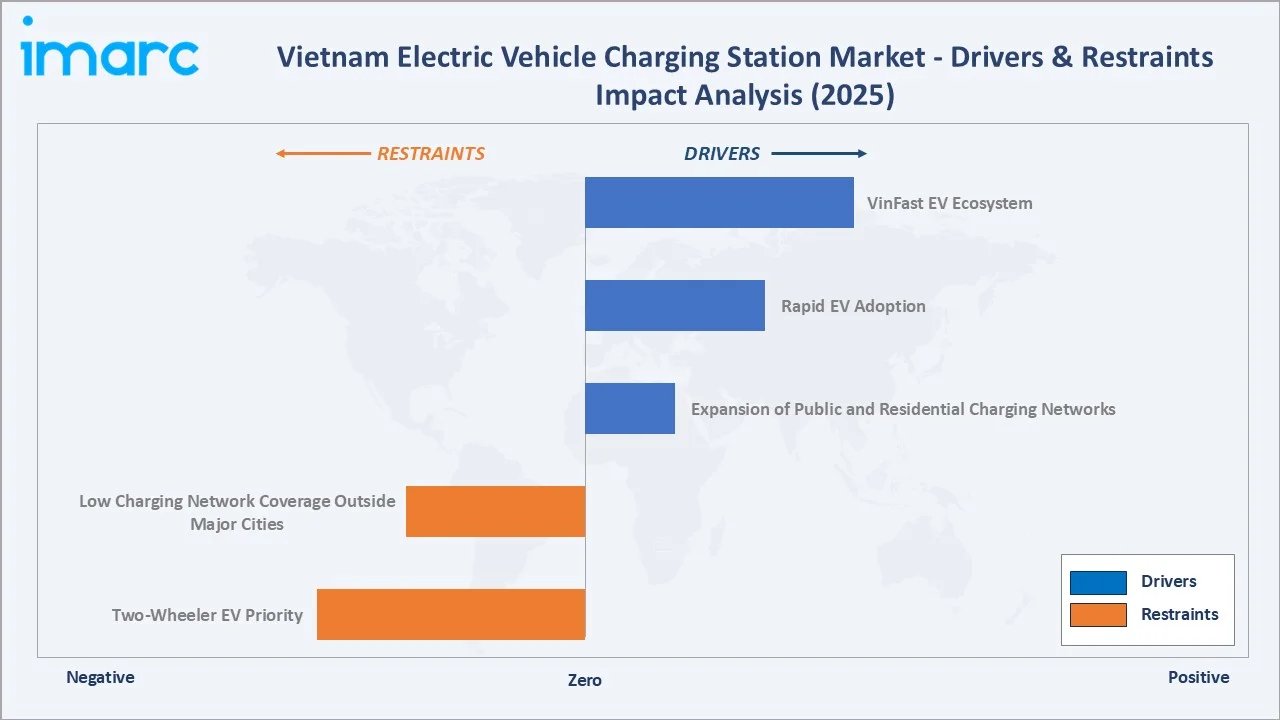

Market Drivers

- VinFast EV Ecosystem: VinFast delivered 175,099 electric vehicles in Vietnam in 2025. This strong performance lifted VinFast’s total deliveries during the first ten months of 2025 to 124,264 units, reinforcing its leading position in Vietnam’s fast-growing electric mobility sector. This VinFast EV ecosystem creates integrated demand for electric vehicles, charging infrastructure, and digital mobility services. As VinFast expands EV production and sales, the need for public, residential, and fast-charging networks is increasing. Its charging network development also improves consumer confidence and reduces range anxiety. This ecosystem-led approach is accelerating EV adoption and supporting nationwide charging infrastructure expansion.

- Rapid EV Adoption: By 2030, Vietnam is expected to have around 1 million EVs on the road, with the figure projected to rise to 3.5 million by 2040. This rapid EV adoption is increasing demand for reliable charging access across cities, residential areas, workplaces, and commercial hubs. As more consumers and fleets shift to electric vehicles, the need for public and private charging points continues to rise. Higher EV penetration also improves charger utilization, making infrastructure projects more attractive for investors. This is accelerating the rollout of AC chargers, fast chargers, and integrated charging networks across Vietnam.

- Expansion of Public and Residential Charging Networks: The expansion of public and residential charging networks improves charger availability for both daily commuters and private EV owners. Public chargers at malls, offices, parking areas, and transport hubs support convenient on-the-go charging. Residential chargers encourage home-based EV ownership by offering reliable overnight charging. Together, these networks reduce range anxiety and support wider EV adoption across Vietnam.

Market Restraints

- Two-Wheeler EV Priority: Two-wheeler EV priority is hampering the market because much of the electrification focus is on electric scooters and motorcycles rather than passenger cars. Two-wheelers often rely on home charging, removable batteries, or low-power charging points, reducing demand for large public EV charging stations. This limits utilization of AC and DC chargers designed for cars and fleets. As a result, investment in high-capacity charging infrastructure may grow more slowly outside major urban and commercial areas.

- Low Charging Network Coverage Outside Major Cities: Low charging network coverage outside major cities limits EV usability in smaller towns, rural areas, and intercity routes. Most chargers are concentrated in urban centers such as Ho Chi Minh City and Hanoi, creating access gaps in emerging regions. This increases range anxiety and discourages long-distance EV travel. As a result, EV adoption and charging infrastructure investment remain uneven across the country.

Market Opportunities

- Expansion of Intercity and Highway Fast-Charging Corridors: According to the Department for Roads of Vietnam, Petrolimex is developing nine rest stops across the country. At the Mai Son–National Highway 45 rest area, 10 EV charging points have been installed on each side of the expressway, with each point offering two ports. This provides 20 charging spaces on each side of the route. This expansion of intercity and highway fast-charging corridors enables convenient long-distance travel between major cities and economic zones. Fast chargers along national highways can reduce charging times and alleviate range anxiety, making EV ownership more practical. These corridors also support commercial fleets, logistics operators, and electric taxis that require reliable en-route charging. As EV adoption increases, highway charging networks can attract substantial investment from charging operators, utilities, and infrastructure developers.

- Fleet Charging Solutions for Logistics, Ride-Hailing, and Delivery Services: Fleet charging solutions for logistics, ride-hailing, and delivery services present a major opportunity as commercial operators increasingly electrify their vehicle fleets. These fleets require dedicated depot charging, fast-charging hubs, and reliable energy management systems to support continuous operations. Growing e-commerce activity and urban delivery demand are further increasing the need for fleet-focused charging infrastructure. This creates opportunities for charging operators, technology providers, and energy companies to develop scalable commercial charging networks across Vietnam.

Market Challenges

- Limited Grid Capacity in Certain Regions: Limited grid capacity in certain regions restricts the deployment of high-power AC and DC fast chargers. Areas with weak distribution networks may require costly upgrades, transformers, and load management systems before chargers can be installed. This raises project costs and delays rollout timelines for operators. As a result, charging infrastructure expansion may remain concentrated in major cities with stronger grid readiness.

- Interoperability and Charging Standardization Issues: Interoperability and charging standardization issues are creating compatibility concerns between different charging networks, connectors, software platforms, and payment systems. This can make charging less convenient for EV users and limit seamless access across multiple operators. For charging providers, supporting various standards increases operational complexity and costs. As the market expands, the lack of uniform standards may slow network integration and reduce overall charging efficiency.

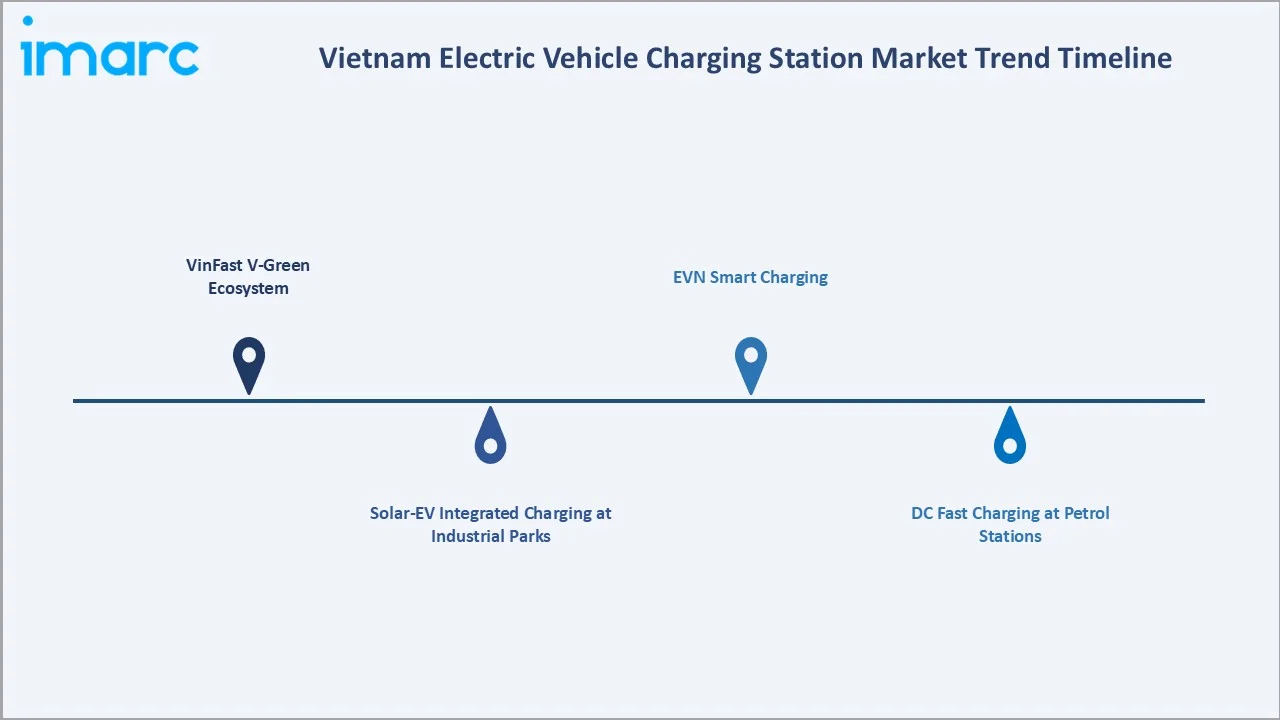

Emerging Market Trends

1. VinFast V-Green Ecosystem

In March 2026, V-GREEN planned to invest 10 trillion Vietnamese Dong (around $380 million) to expand Vietnam’s EV charging infrastructure. The company aims to develop 99 charging hubs along national and provincial highways by the end of 2026. Each hub is expected to include up to 100 charging points with a maximum capacity of 150 kW. The stations will use renewable energy supported by VinFast-produced battery energy storage systems. This VinFast V-Green ecosystem combines EV manufacturing, charging infrastructure, and digital mobility services. V-Green supports charging network expansion, while smart platform integration helps users locate chargers, monitor charging, and manage payments. This improves charging convenience and strengthens customer confidence in EV adoption. The integrated ecosystem also supports scalable infrastructure development across public, residential, and fleet charging applications.

2. Solar-EV Integrated Charging at Industrial Parks

Solar-EV integrated charging at industrial parks is emerging as factories and logistics hubs seek cleaner mobility solutions. Solar-backed charging can reduce electricity costs, ease pressure on local grids, and support corporate sustainability targets. Industrial parks can use these systems for employee EVs, delivery fleets, and electric logistics vehicles. This trend also aligns with Vietnam’s renewable energy growth and rising demand for low-carbon industrial operations.

3. EVN Smart Charging

EVN smart charging enables better coordination between charging demand and grid capacity. Smart charging solutions can help manage peak loads, optimize electricity use, and support reliable charger operation across public and residential networks. As EV adoption rises, EVN’s grid role becomes important for integrating charging infrastructure with power distribution planning. This trend supports scalable, efficient, and grid-friendly EV charging deployment across Vietnam.

4. DC Fast Charging at Petrol Stations

DC fast charging at petrol stations is emerging as fuel retailers use existing forecourt locations to serve EV users. Petrol stations already offer high visibility, road access, parking space, and convenience facilities, making them suitable for fast-charger deployment. This model supports intercity travel and reduces range anxiety for EV owners. It also allows fuel retailers to diversify their revenue streams as mobility shifts toward electric vehicles.

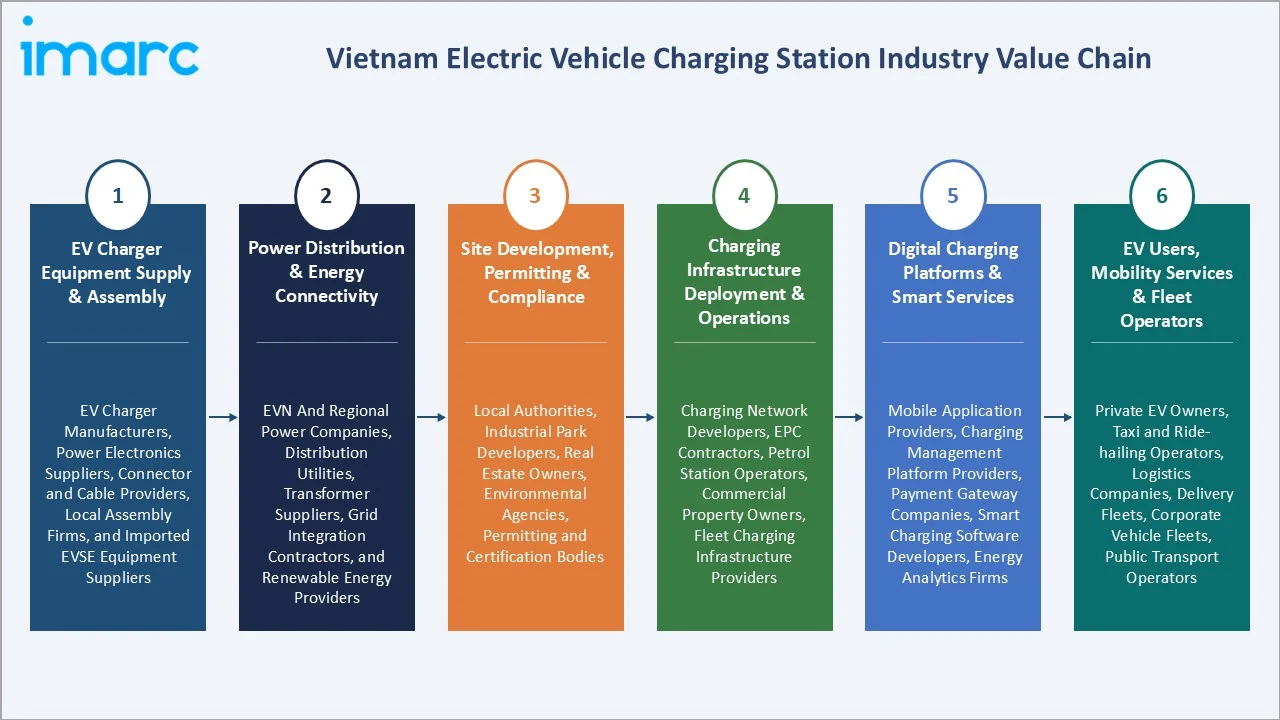

Industry Value Chain Analysis

Vietnam EV charging station value chain integrates EV charger equipment supply & assembly, power distribution & energy connectivity, site development, permitting & compliance, charging infrastructure deployment & operations, digital charging platforms & smart services, and EV users, mobility services & fleet operators.

|

Stage |

Key Participants |

|

EV Charger Equipment Supply & Assembly |

EV charger manufacturers, power electronics suppliers, connector and cable providers, local assembly firms, and imported EVSE equipment suppliers |

|

Power Distribution & Energy Connectivity |

EVN and regional power companies, distribution utilities, transformer suppliers, grid integration contractors, and renewable energy providers |

|

Site Development, Permitting & Compliance |

Local authorities, industrial park developers, real estate owners, environmental agencies, permitting and certification bodies |

|

Charging Infrastructure Deployment & Operations |

Charging network developers, EPC contractors, petrol station operators, commercial property owners, fleet charging infrastructure providers |

|

Digital Charging Platforms & Smart Services |

Mobile application providers, charging management platform providers, payment gateway companies, smart charging software developers, energy analytics firms |

|

EV Users, Mobility Services & Fleet Operators |

Private EV owners, taxi and ride-hailing operators, logistics companies, delivery fleets, corporate vehicle fleets, public transport operators |

Charging infrastructure deployment and operations represent the most value-added stage in Vietnam’s EV charging station value chain because it directly generates revenue and determine charger accessibility for end users. This stage involves selecting strategic locations, installing charging equipment, managing network performance, and ensuring reliable service availability. The effectiveness of deployment influences charger utilization rates, customer experience, and EV adoption.

Technology Landscape in the Vietnam Electric Vehicle Charging Station Industry

DC Fast-Charging and Ultra-Fast Charging Technology

DC fast-charging and ultra-fast charging technology significantly reduce charging times and improve convenience for EV users. In February 2025, Charge+ Vietnam opened an ultra-fast EV charging station at Crescent Mall in Phu My Hung City Center. The station includes both DC and AC chargers to serve different EV user needs and features Phu My Hung’s fastest EV charger, with a power capacity of 180 kW.These technologies support long-distance travel, commercial fleets, ride-hailing services, and high-traffic urban charging locations. Their deployment along highways, petrol stations, and transport corridors helps reduce range anxiety and increases charger utilization. As EV adoption accelerates, investment in high-power charging infrastructure is becoming a key focus for charging operators and infrastructure developers.

Cloud-based Charging Management Platforms

Cloud-based charging management platforms allow operators to monitor charger uptime, usage, energy consumption, and payments across multiple sites in real time. These platforms support remote diagnostics, dynamic pricing, user authentication, and digital payment integration. They also help operators optimize charger utilization and reduce maintenance downtime. As Vietnam expands public highway and fleet charging networks, cloud-based systems are becoming essential for scalable infrastructure management.

Vehicle-to-Grid (V2G) and Bidirectional Charging Technology

Vehicle-to-Grid (V2G) and bidirectional charging technology enable electric vehicles to both consume and supply electricity. This allows EVs to function as distributed energy storage assets, helping balance grid demand during peak periods. The technology also supports greater integration of renewable energy sources by storing excess power and feeding it back when needed. As Vietnam’s EV fleet and clean energy capacity expand, V2G solutions can enhance grid stability, energy efficiency, and the overall value of charging infrastructure.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Charging Station Type |

AC Charging |

57.2% |

2025 |

|

Vehicle Type |

Battery Electric Vehicle (BEV) |

64.5% |

2025 |

|

Installation Type |

🔒 |

🔒 |

2025 |

|

Charging Level |

🔒 |

🔒 |

2025 |

|

Connector Type |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

Southern Vietnam |

45.2% |

2025 |

By Charging Station Type

AC charging leads at 57.2% (2025). AC charging dominates due to its lower installation cost, simple setup, and suitability for daily charging needs. It is widely used in homes, offices, malls, residential complexes, and parking facilities. AC chargers are ideal for overnight and destination charging, where vehicles remain parked for longer periods. Their affordability and ease of deployment make them the preferred option for Vietnam’s expanding urban EV user base.

To access detailed market analysis, Request Sample

DC charging at 34.1% grows at ~23.5% CAGR through expressway DC corridor and fleet hub. Inductive charging at 8.7% grows fastest at ~27.8% CAGR through taxi depot wireless pilot and Vietnam's electric bus terminus inductive adoption.

By Vehicle Type

Battery electric vehicle (BEV) leads at 64.5% (2025). BEV sales in Vietnam reached 180,000 units in 2025, rising by 160.87% from 69,000 units in 2024. This strong growth supports the dominance of the BEV segment, as fully electric vehicles depend entirely on external charging infrastructure, increasing demand for public, residential, and fast-charging stations across the country.

Plug-in hybrid electric vehicle (PHEV) at 21.8%, creating demand for residential, workplace, and public charging infrastructure while offering the flexibility of a backup internal combustion engine. Hybrid electric vehicle (HEV) at 13.7% supports market growth by increasing consumer acceptance of electrified vehicles and promoting awareness of sustainable transportation.

Regional Market Insights

|

Region |

Share (2025) |

Key Vietnam EV Charging Station Market Drivers & Characteristics |

|

Southern Vietnam |

45.2% |

Supported by high EV adoption, strong commercial activity, dense urban development, and extensive charging infrastructure deployment. |

|

Northern Vietnam |

37.4% |

Reflects growing EV demand, increasing charger installations, and strong support from residential, commercial, and workplace charging applications. |

|

Central Vietnam |

17.4% |

Driven by expanding tourism activity, improving transport connectivity, and the gradual deployment of charging infrastructure along major highways, urban centers, and coastal economic corridors. |

Southern Vietnam's 45.2% supported by strong EV adoption, dense urban activity, and wider charger deployment across Ho Chi Minh City and nearby industrial provinces. Northern Vietnam's 37.4% driven by rising EV demand in Hanoi and surrounding economic zones.

Central Vietnam's 17.4% emerging gradually, supported by tourism, highway connectivity, and charging infrastructure along coastal corridors.

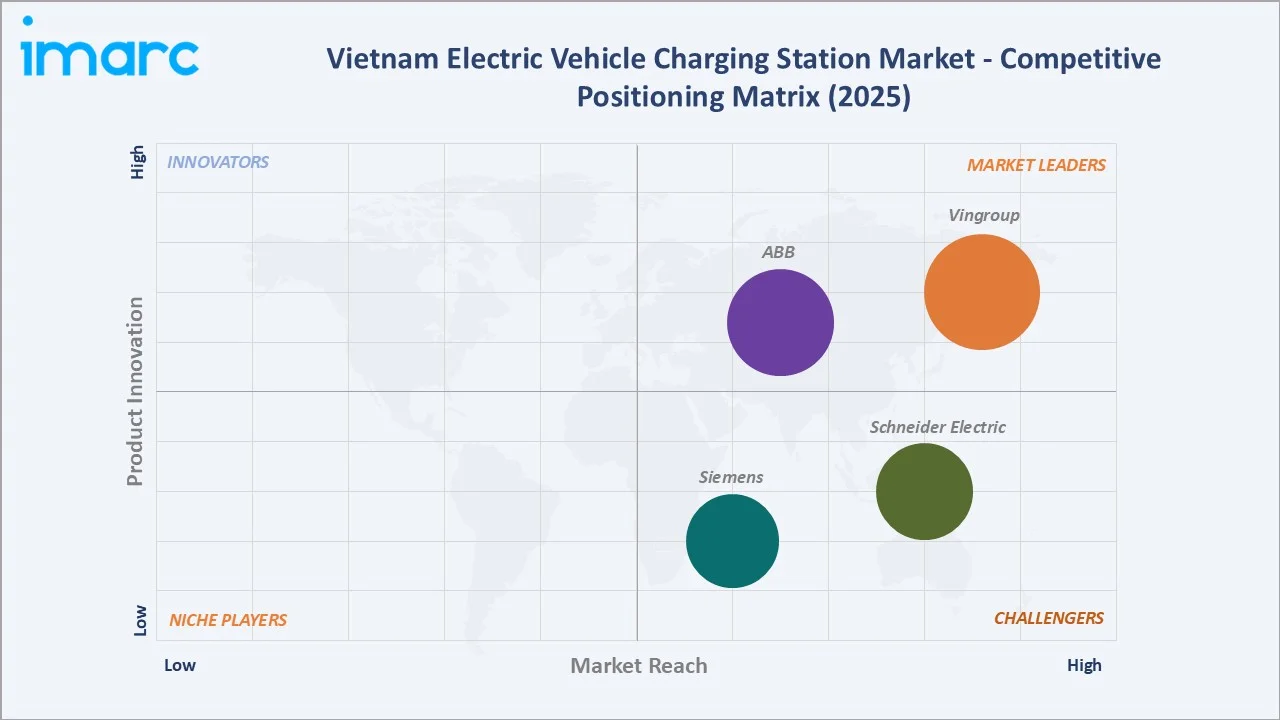

Competitive Landscape

Vietnam EV charging station competitive landscape is commercially dominated by VinFast’s V-GREEN ecosystem, which benefits from strong integration with domestic EV production and nationwide charging network expansion. Other participants include energy utilities, petrol station operators, commercial property owners, and emerging charging network providers. Competition is increasingly centered on fast-charging deployment, highway charging hubs, renewable-energy integration, and digital charging platforms.

|

Company |

Key Products |

Market Position |

Core Strength |

|

Vingroup |

250kW DC super-fast charging, 150kW DC super-fast charging, 60kW DC fast charging, 30kW DC fast charging |

Market Leader |

Vingroup acts as the primary driver of EV infrastructure in Vietnam through its dedicated subsidiary, VinFast. |

|

ABB |

A400, C50, HVC360, HVC150 |

Market Leader |

ABB plays a key role in developing Vietnam's electric vehicle (EV) charging infrastructure by supplying advanced DC fast chargers, notably partnering with AEON MALL Vietnam to support sustainable urban mobility. |

|

Schneider Electric |

Schneider Charge, Schneider Charge Pro, EVLink Pro DC, EVLink Pro AC |

Strong Challenger |

Schneider Electric plays a significant role in Vietnam's EV charging infrastructure market by providing smart, scalable, and sustainable charging solutions (AC and DC) for homes, commercial buildings, and industrial fleets. |

|

Siemens |

SICHARGE D |

Strong Challenger |

Siemens plays a significant role in Vietnam's growing Electric Vehicle (EV) charging infrastructure by providing technology, hardware, and smart solutions that support the country's shift to electric mobility. |

Vietnam EV charging competitive landscape is evolving through rapid charging network expansion, increasing investments by the V-GREEN ecosystem, and growing participation from energy companies, petrol station operators, and technology providers. Competition is increasingly focused on fast-charging deployment, digital charging platforms, renewable energy integration, and nationwide infrastructure coverage.

Key Company Profiles

Vingroup

Vingroup is one of Vietnam’s largest private conglomerates, with operations spanning real estate, technology, industrial manufacturing, healthcare, education, and mobility solutions. Through its electric vehicle subsidiary, VinFast, Vingroup plays a leading role in Vietnam’s EV charging station market.

- Key Products: 250kW DC super-fast charging, 150kW DC super-fast charging, 60kW DC fast charging, 30kW DC fast charging.

- Recent Developments: In March 2026, V-GREEN planned to invest VND 10 trillion (USD 380 million) to expand EV charging infrastructure across Vietnam. According to the Vietnam News Agency, the company aims to build 99 EV charging hubs along national and provincial highways by the end of the year. Each hub will feature up to 100 charging points with a maximum capacity of 150 kW. The stations will be powered by renewable energy, supported by VinFast-developed battery energy storage systems.

- Strategic Focus: Expanding Vietnam’s EV charging infrastructure through its charging platform, by deploying charging stations across cities, highways, residential complexes, commercial properties, and industrial zones.

ABB

ABB is a technology leader specializing in electrification, automation, robotics, and digital solutions. Through its ABB E-mobility division, the company provides a comprehensive portfolio of EV charging solutions, including AC chargers, DC fast chargers, ultra-fast charging systems, and charging management software.

- Key Products: A400, C50, HVC360, HVC150.

- Strategic Focus: Focused on deployment of DC fast-charging and ultra-fast charging solutions for public charging networks, commercial sites, and fleet operators.

Market Concentration Analysis

The Vietnam EV charging station market exhibits a moderately concentrated structure. The market also includes global technology providers, utilities, fuel retailers, and emerging charging network operators. Competition is increasingly focused on fast-charging deployment, highway charging hubs, battery-swapping solutions, and smart charging platforms. Strategic partnerships between charging providers, energy companies, and commercial property owners are accelerating infrastructure expansion. As EV adoption grows, new entrants are expected to increase competition, although large-scale network operators are likely to retain a significant market presence due to their infrastructure advantages.

Investment & Growth Opportunities

Highest Growth Segments

Inductive charging (~27.8% CAGR), DC charging (~23.5% CAGR through expressway corridor), BEV vehicle type (~22.4% CAGR), solar-EV integrated hub (~30-35% CAGR), fleet hub charging (~25-28% CAGR), and Central Vietnam tourism EVSE (~20-22% CAGR) represent Vietnam's highest-growth EV charging investment vectors through 2034.

Investment Themes

National Highway DC fast charging: Investors are focusing on deploying high-power chargers along national highways to reduce charging times and alleviate range anxiety. These corridors support passenger vehicles, logistics fleets, intercity transport, and commercial mobility services. As EV adoption accelerates, highway charging infrastructure is expected to attract significant investment from charging operators, energy companies, and infrastructure developers.

Future Market Outlook (2026-2034)

Vietnam EV charging station market is projected to grow from USD 81.68 Million in 2025 to USD 459.50 Million by 2034, delivering a 21.16% CAGR over the forecast period, driven by rapid EV adoption, expanding domestic EV production, and increasing government support for clean transportation. Large-scale investments in public charging networks, highway fast-charging corridors, and renewable-energy-powered charging hubs are expected to strengthen infrastructure coverage nationwide. The market is also likely to benefit from growing fleet electrification, smart charging technologies, and integration with energy storage systems. As EV ownership continues to rise, charging infrastructure deployment is expected to accelerate across urban centers, industrial zones, and intercity transport routes.

Three structural forces define Vietnam's EV charging growth through 2034. First, the continued expansion of the VinFast-led EV ecosystem will drive demand for nationwide charging infrastructure and integrated mobility services. Second, large-scale investments in highway fast-charging corridors and urban charging networks will improve accessibility and support long-distance EV travel. Third, increasing focus on renewable energy integration, smart charging technologies, and grid modernization will enhance the efficiency and sustainability of the charging ecosystem. Together, these factors will accelerate EV adoption and infrastructure deployment across the country.

Research Methodology

Primary Research

Primary research comprised detailed interviews with EV charging network operators, EV manufacturers, utility companies, government agencies, fleet operators, technology providers, and industry experts across Vietnam. Discussions focused on charging infrastructure deployment, EV adoption trends, investment priorities, technology developments, and regulatory support. These interactions provided firsthand insights into market dynamics, competitive positioning, and future growth opportunities.

Secondary Research

Secondary research encompassed a review of company websites, annual reports, press releases, government publications, EV policy documents, and industry association data. It also included charging network updates, utility reports, infrastructure announcements, and credible news sources. These sources helped assess market size, technology trends, competitive landscape, regulatory developments, and investment activity. The information was cross-checked with primary inputs to ensure consistency and reliability.

Forecasting Models

Market revenue forecasts developed using EV fleet EVSE penetration model: Vietnam new EV registrations by vehicle type multiplied by EVSE-to-EV ratio multiplied by average EVSE installed cost and lifecycle by type.

Vietnam Electric Vehicle Charging Station Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Charging Station Types Covered | AC Charging, DC Charging, Inductive Charging |

| Vehicle Types Covered | Battery Electric Vehicle (BEV), Plug-in Hybrid Electric Vehicle (PHEV), Hybrid Electric Vehicle (HEV) |

| Installation Types Covered | Portable Charger, Fixed Charger |

| Charging Levels Covered | Level 1, Level 2, Level 3 |

| Connector Types Covered | Combines Charging Station (CCS), CHAdeMO, Normal Charging, Tesla Supercharger, Type-2 (IEC 621196), Others |

| Applications Covered | Residential, Commercial |

| Regions Covered | Northern Vietnam, Central Vietnam, Southern Vietnam |

| Companies Covered | Vingroup, ABB, Schneider Electric, Siemens, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Vietnam electric vehicle charging station market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Vietnam electric vehicle charging station market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Vietnam electric vehicle charging station industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Vietnam Electric Vehicle Charging Station Market Report

The Vietnam EV charging station market reached USD 81.68 Million in 2025, driven by rapid EV adoption, supported by strong domestic EV production led by VinFast and expanding consumer acceptance of electric mobility. Growing investments in public, residential, and highway fast-charging networks are improving charging accessibility across major cities and transport corridors. Government clean mobility goals, rising fuel costs, and urbanization are further encouraging the shift toward EVs. Fleet electrification in logistics, taxis, and delivery services is also creating demand for dedicated charging infrastructure.

The Vietnam EV charging station market grows at 21.16% CAGR during 2026-2034, reaching USD 459.50 Million by 2034. The CAGR reflects VinFast production scale-up, Green Growth Strategy 2030 mandate, expressway DC corridor, and solar-EV integration.

AC charging leads at 57.2% due to its lower installation and operating costs compared to DC fast chargers. AC chargers are widely deployed in homes, apartment complexes, offices, shopping centers, and parking facilities, where vehicles remain parked for extended periods. Their ease of installation and suitability for overnight and destination charging make them the preferred choice for daily EV users.

BEVs lead at 64.5% because BEVs rely entirely on external charging infrastructure for operation, unlike hybrid vehicles that can use conventional fuels. Strong growth in BEV sales, led by VinFast and supported by expanding model availability, is increasing demand for public, residential, and fast-charging stations. The rapid expansion of charging networks and government support for zero-emission mobility further reinforces the dominance of the BEV segment.

Southern Vietnam leads at 45.2% due to its high concentration of EV users, strong commercial activity, and extensive urban development centered around Ho Chi Minh City. The region benefits from greater charging infrastructure deployment, higher disposable incomes, and strong demand from residential, commercial, and fleet applications. Its dense transportation network and industrial base further support higher charger utilization and continued infrastructure investment.

Leading companies include Vingroup, ABB, Schneider Electric, and Siemens, among others.

The market is projected to reach approximately USD 213.24 Million by 2030, with VinFast production and Vietnam's North-South Expressway DC fast chargers.

Three priority investment opportunities: National Highway 1 DC fast charging, high fleet charging hubs, and solar-EV integrated hubs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade