Vietnam Energy as a Service (EaaS) Market Size, Share, Trends and Forecast by Service Type, End User, and Region, 2026-2034

Vietnam Energy as a Service (EaaS) Market Summary:

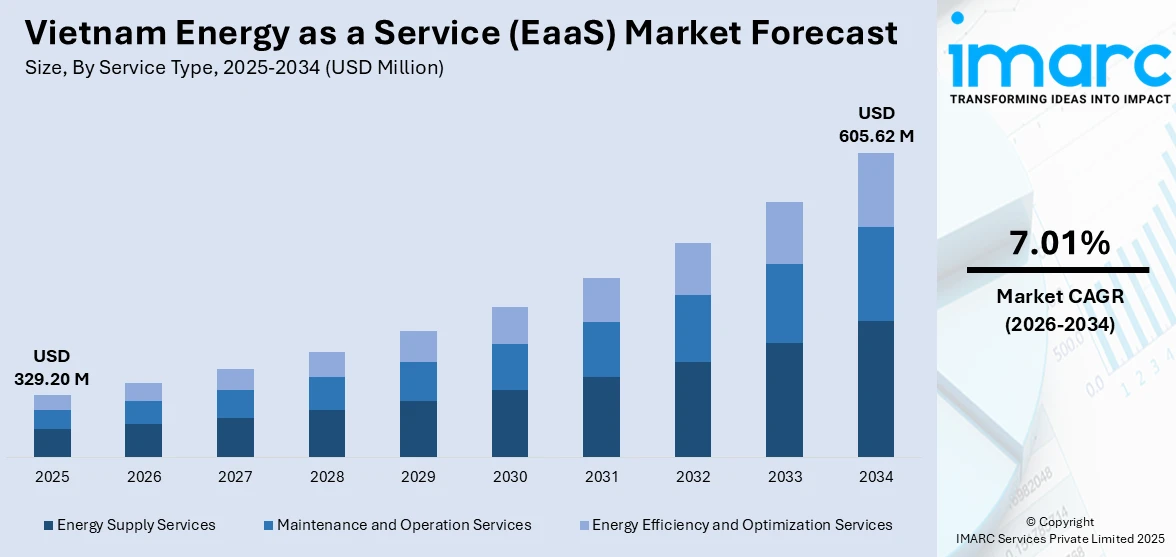

The Vietnam energy as a service (EaaS) market size was valued at USD 329.20 Million in 2025 and is projected to reach USD 605.62 Million by 2034, growing at a compound annual growth rate of 7.01% from 2026-2034.

The Vietnam energy as a service market is expanding steadily, underpinned by the country’s accelerating energy transition, rising industrial electricity demand, and supportive government policies promoting renewable energy adoption. The shift toward outsourced energy management, on-site power generation, and efficiency optimization is enabling businesses to reduce operational costs while meeting sustainability mandates. Growing foreign direct investment in manufacturing and technology sectors further amplifies demand for reliable, scalable, and cost-effective energy service solutions across the country.

Key Takeaways and Insights:

- By Service Type: Energy supply services dominate the market with a share of 46.8% in 2025, driven by increasing demand for on-site renewable energy generation and distributed power solutions across industrial and commercial facilities.

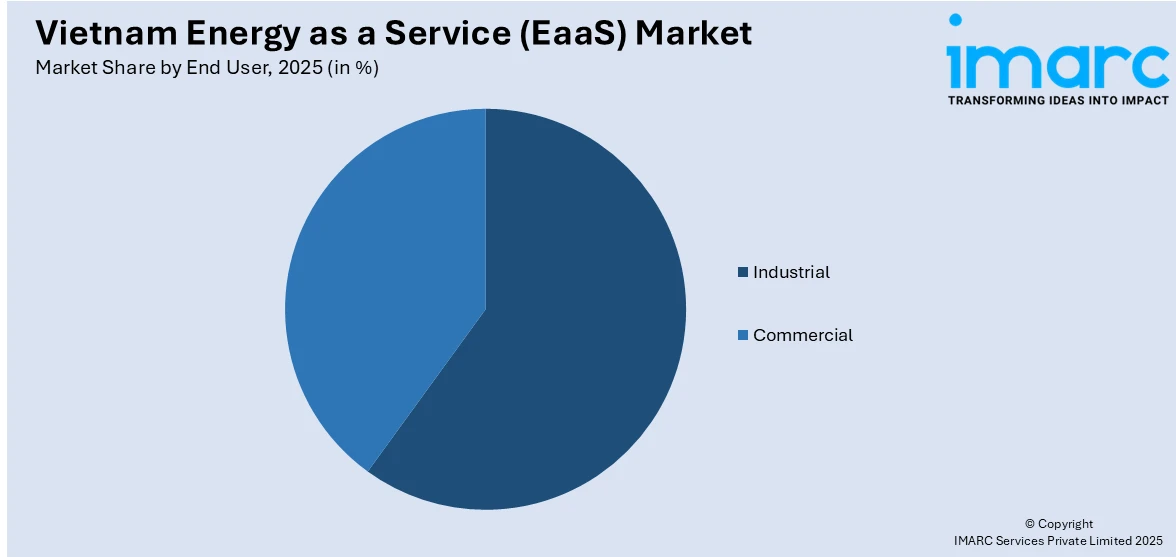

- By End User: Industrial leads the market with a share of 58.9% in 2025, owing to the concentration of energy-intensive manufacturing operations and multinational facilities requiring reliable, uninterrupted power supply.

- By Region: Southern Vietnam represents the largest segment with a market share of 39.6% in 2025, supported by Ho Chi Minh City’s dense industrial park ecosystem, high FDI inflows, and the region’s significant contribution to national GDP.

- Key Players: The Vietnam energy as a service market features a moderately fragmented competitive landscape, with international energy service providers competing alongside regional players and emerging domestic firms. Market participants leverage technology partnerships, long-term service agreements, and renewable energy integration capabilities to differentiate their offerings.

To get more information on this market Request Sample

Vietnam’s energy-as-a-service market is gaining momentum as industrial expansion, policy reforms, and corporate sustainability priorities increasingly intersect. Ongoing power sector liberalization has created new avenues for large commercial and industrial users to source cleaner energy solutions beyond traditional utility supply, supporting greater flexibility and reliability. At the same time, multinational manufacturers operating in Vietnam are accelerating the adoption of on-site and contract-based renewable energy models to align with global environmental commitments and manage long-term energy costs. These shifts are encouraging wider deployment of distributed generation, energy management services, and performance-based energy contracts. Together, regulatory openness and rising ESG expectations are reshaping how enterprises approach energy procurement, positioning energy-as-a-service as a strategic tool for operational efficiency, sustainability compliance, and risk mitigation across Vietnam’s industrial landscape. Additionally, Vietnam’s revised Power Development Plan VIII, approved in April 2025, targets a total investment of USD 136.3 billion for power generation and transmission development through 2030, significantly expanding opportunities for energy service providers across the value chain.

Vietnam Energy as a Service (EaaS) Market Trends:

Expansion of Direct Power Purchase Agreements Reshaping Energy Procurement

The rapid rollout and ongoing refinement of the DPPA framework is reshaping energy procurement practices in Vietnam. Recent regulatory changes have expanded participation to a wider range of renewable energy sources and energy-related businesses, giving large electricity consumers greater flexibility in how they source power. This approach allows enterprises to contract electricity directly from renewable producers, either through dedicated infrastructure or the broader power market. The model is especially appealing to multinational manufacturers aiming to meet sustainability and ESG objectives, as it reduces reliance on traditional utility channels and simplifies access to clean energy solutions.

Rapid Adoption of Rooftop Solar in Industrial Parks

Rooftop solar installations in Vietnam’s industrial parks have emerged as a defining trend in the energy service landscape. Statistics from the Ministry of Industry and Trade indicate that total rooftop solar capacity in Vietnamese industrial parks exceeded 3,200 MWp by late 2024, with deployment accelerating across all three regions. The momentum is largely shaped by global supply chain expectations, as export-focused manufacturers must comply with tougher environmental and sustainability standards imposed by key international markets. Industrial hubs with a strong concentration of electronics and advanced manufacturing are increasingly prioritizing rooftop solar adoption to align with these requirements. Local authorities are encouraging the use of existing factory rooftops within established industrial zones to host distributed solar systems, enabling manufacturers to integrate clean energy into operations, lower carbon footprints, and strengthen compliance with international buyer expectations while optimizing the use of available industrial infrastructure.

Integration of Battery Energy Storage Systems with Renewable Energy Projects

Vietnam is experiencing a significant push toward battery energy storage system deployment to support the growing share of intermittent renewable energy in the national grid. The revised Power Development Plan VIII dramatically increased BESS targets from the initial 300 MW to between 10,000 and 16,300 MW by 2030, reflecting the government’s recognition of storage as critical infrastructure. The European Union also announced a comprehensive 430 million euro package in October 2025 to advance the Bac Ai Pumped Hydro Storage Project, a flagship investment under Vietnam’s Just Energy Transition Partnership aimed at enhancing grid stability.

Market Outlook 2026-2034:

Vietnam’s energy as a service market is set for steady growth over the coming years, supported by long-term infrastructure development priorities, increasing involvement from private renewable energy providers, and rising industrial demand for affordable and sustainable power solutions. Ongoing electricity market reforms are fostering greater competition and flexibility in power procurement, encouraging innovative service models. Clear policy direction favoring environmentally responsible, efficient, and market-driven energy development further strengthens confidence among investors and accelerates the evolution of a diversified energy services ecosystem. The market generated a revenue of USD 329.20 Million in 2025 and is projected to reach a revenue of USD 605.62 Million by 2034, growing at a compound annual growth rate of 7.01% from 2026-2034.

Vietnam Energy as a Service (EaaS) Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Service Type |

Energy Supply Services |

46.8% |

|

End User |

Industrial |

58.9% |

|

Region |

Southern Vietnam |

39.6% |

Service Type Insights:

- Energy Supply Services

- Maintenance and Operation Services

- Energy Efficiency and Optimization Services

Energy supply services dominates with a market share of 46.8% of the total Vietnam energy as a service market in 2025.

Energy supply services include on-site power generation, distributed energy solutions, and renewable electricity sourcing models that allow businesses to access dependable power without large upfront investments. This segment leads the market as industrial and commercial users increasingly favor outsourced energy generation to improve cost control and operational reliability. Rooftop solar systems and combined heat and power solutions are especially attractive, as they reduce exposure to grid volatility. Supportive procurement mechanisms have further encouraged businesses to source clean power directly from private providers rather than relying solely on traditional utility supply.

The segment is further supported by Vietnam’s strong renewable resource potential, particularly favorable solar conditions in central and southern regions and robust wind availability along coastal areas. Manufacturing hubs and industrial parks are increasingly engaging specialized energy service providers to design, operate, and maintain on-site generation assets. This approach allows companies to shift technical, operational, and performance risks to experienced operators while securing stable energy supply. The resulting improvements in cost efficiency, sustainability performance, and energy reliability continue to accelerate adoption across export-oriented manufacturing clusters.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Commercial

- Industrial

Industrial leads with a share of 58.9% of the total Vietnam energy as a service market in 2025.

The industrial end-user segment’s dominance reflects Vietnam’s position as one of Southeast Asia’s fastest-growing manufacturing hubs, with industrial production recording growth of 8.4 percent in 2024. Energy-intensive activities such as electronics manufacturing, textiles, automotive components, and semiconductor production depend on reliable and affordable electricity to maintain operational efficiency. This makes Energy as a Service solutions especially appealing, as they help industrial users manage power costs, ensure supply stability, and optimize energy usage. The industrial sector’s dominant role in overall energy demand highlights the strong and sustained need for specialized energy supply, efficiency, and management services tailored to complex manufacturing environments.

Multinational companies active in Vietnam are increasingly requiring the use of renewable energy across their production and sourcing networks, pushing manufacturers and industrial park occupants toward Energy as a Service models. At the same time, national industrial development priorities emphasize manufacturing-led economic growth, making dependable power supply a critical consideration for foreign investors. Rising electricity needs from energy-intensive activities such as data centers and logistics operations in southern industrial zones further highlight the importance of flexible, scalable energy service partnerships tailored to industrial users.

Regional Insights:

- Northern Vietnam

- Central Vietnam

- Southern Vietnam

Southern Vietnam represents the largest share with 39.6% of the total Vietnam energy as a service market in 2025.

Southern Vietnam’s leading position in the energy as a service market stems from its role as the country’s main economic and industrial hub. Ho Chi Minh City and nearby provinces host a dense concentration of manufacturing plants, logistics operations, data facilities, and commercial developments. This clustering of high-value economic activity generates sustained and diversified electricity demand. Strong integration into global trade networks and continued industrial expansion further reinforce the region’s need for reliable, scalable, and efficiently managed energy solutions, supporting its market leadership.

The large number of industrial parks and export processing zones in the region gives rise to a natural need for the supply of energy and its maintenance services, as well as efficiency optimization. The southern provinces have high levels of solar irradiation, which can be used to promote the deployment of rooftop solar systems, and the advanced infrastructure in the region facilitates the incorporation of advanced energy management systems. The function of clustering multinational manufacturers that have corporate sustainability objectives has placed Southern Vietnam in the spotlight of EaaS suppliers in their quest to provide holistic energy services that include renewable generation, demand management, and long-term performance guarantees.

Market Dynamics:

Growth Drivers:

Why is the Vietnam Energy as a Service (EaaS) Market Growing?

Government-Led Energy Reforms and Policy Support for Renewable Energy Adoption

Vietnam’s regulatory landscape has undergone transformative changes that directly support the market expansion. The Electricity Law, enacted in November 2024 and effective from February 2025 established the legal foundation for competitive electricity markets and private sector participation in energy generation and distribution. Subsequent regulatory actions have institutionalized mechanisms that allow renewable power producers to supply electricity directly to large industrial users, either through dedicated connections or market-based trading platforms. Broader national power planning policies emphasize long-term investment in generation and transmission infrastructure to support reliable supply. At the same time, high-level policy direction continues to promote a greener, more competitive, and market-driven energy sector. Together, these measures encourage private participation, improve regulatory clarity, streamline project development, and create a more supportive environment for renewable energy deployment and innovative energy service models.

Rapid Industrialization and Escalating Energy Demand from Manufacturing Sectors

Vietnam’s rapid industrial expansion is intensifying demand for energy service solutions capable of supplying stable, flexible, and economically efficient power to manufacturing facilities. Rising production activity is placing growing pressure on the national electricity system, encouraging utilities and businesses to explore alternative supply and demand management approaches. Ambitious economic and industrial development goals, particularly in manufacturing and high-technology segments, require continuous strengthening of power generation and distribution capacity. Expanding data centers, logistics hubs, and advanced manufacturing clusters are further elevating electricity needs, while periodic supply constraints in key regions highlight the importance of diversified, decentralized, and professionally managed energy service models.

Growing Corporate Sustainability Mandates and ESG-Driven Energy Procurement

The growing emphasis on environmental, social, and governance commitments among multinational companies operating in Vietnam is acting as a powerful catalyst for energy as a service adoption. Global manufacturers, technology firms, and data infrastructure operators increasingly require renewable energy use across their supply chains, pushing local facilities and contract manufacturers to shift toward cleaner power sources. Vietnam’s evolving regulatory framework supports this transition by allowing companies to procure green electricity more directly and encouraging on-site renewable generation within industrial zones. As a result, manufacturing hubs are increasingly integrating professionally managed renewable energy solutions to align operations with global sustainability expectations and corporate decarbonization goals.

Market Restraints:

What Challenges the Vietnam Energy as a Service (EaaS) Market is Facing?

Grid Infrastructure Constraints and Transmission Bottlenecks

Vietnam’s transmission network has not kept pace with the rapid expansion of renewable energy capacity, leading to significant curtailment in key generation provinces and limiting the ability of energy service providers to deliver a reliable supply. Northern provinces experienced power shortfalls during peak demand periods in 2024, necessitating emergency electricity imports, while only a fraction of mandated grid projects met their scheduled timelines. These infrastructure constraints create uncertainty for EaaS providers relying on grid connectivity for power delivery and management services.

Regulatory Uncertainty and Policy Implementation Challenges

Despite significant legislative progress, the rapid pace of regulatory change and instances of retroactive policy adjustments have introduced uncertainty for energy market participants. The government’s review of feed-in tariff eligibility for multiple solar and wind projects, with potential revenue reductions, has raised concerns about policy predictability. Frequent revisions to key decrees and the evolving implementation framework for DPPAs require market participants to continuously adapt their business models and investment strategies.

High Upfront Costs and Financing Barriers for Small and Medium Enterprises

The initial investment required for renewable energy installations, battery storage systems, and advanced energy management infrastructure presents a significant barrier for adoption among smaller businesses. Small and medium-sized enterprises in industrial parks often lack the financial capacity for direct investment in solar panels and storage solutions, while loan interest rates and project guarantee conditions remain unfavorable. This financing gap limits the addressable market for EaaS providers seeking to serve beyond large multinational clients.

Competitive Landscape:

The Vietnam energy-as-a-service market features a dynamic, competitive landscape characterized by participation from international energy companies, regional service providers, and emerging domestic players. Market participants compete across service offerings including on-site renewable energy generation, energy management systems, maintenance and operations, and comprehensive efficiency optimization solutions. Strategic differentiation is driven by technological capabilities, particularly in smart grid integration, artificial intelligence-powered monitoring systems, and battery storage solutions. Long-term service agreements, performance-based contracts, and partnerships with industrial park developers serve as key competitive strategies. The evolving regulatory environment, particularly the DPPA framework, is enabling new market entrants to offer innovative energy procurement models, intensifying competition and driving service quality improvements across the value chain.

Recent Developments:

- July 2025: Samsung Electronics Vietnam officially commissioned a rooftop solar power system with a capacity of 2.38 MWp at its factory in Yen Phong Industrial Park, Bac Ninh, marking the company’s first step toward its Net Zero ambition in Vietnam and expected to generate approximately 2.59 million kWh of clean electricity annually.

- March 2025: The Government of Vietnam issued Decree 57/2025/ND-CP, replacing Decree 80/2024 after eight months, to establish the comprehensive regulatory framework for Direct Power Purchase Agreements between renewable energy generators and large electricity consumers, broadening eligibility to include biomass generators and electric vehicle charging businesses.

Vietnam Energy as a Service (EaaS) Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Service Types Covered |

Energy Supply Services, Maintenance and Operation Services, Energy Efficiency and Optimization Services |

|

End Users Covered |

Commercial, Industrial |

|

Regions Covered |

Northern Vietnam, Central Vietnam, Southern Vietnam |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Vietnam Energy as a Service (EaaS) Market Report

The Vietnam energy as a service (EaaS) market size was valued at USD 329.20 Million in 2025.

The Vietnam energy as a service (EaaS) market is expected to grow at a compound annual growth rate of 7.01% from 2026-2034 to reach USD 605.62 Million by 2034.

Energy supply services dominated the market with a share of 46.8% in 2025, driven by growing demand for on-site renewable energy generation, distributed power solutions, and the expanding DPPA framework enabling direct renewable energy procurement by industrial consumers.

Key factors driving the Vietnam energy as a service (EaaS) market include government-led energy reforms such as the DPPA framework and revised PDP8, rapid industrialization with escalating energy demand from manufacturing sectors, and growing corporate ESG mandates requiring renewable energy adoption.

Major challenges include grid infrastructure constraints and transmission bottlenecks that limit reliable power delivery, regulatory uncertainty stemming from frequent policy revisions and retroactive tariff adjustments, and high upfront investment costs that restrict EaaS adoption among small and medium enterprises.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)