Vietnam Self Storage Market Size, Share, Trends and Forecast by Self-Storage Type, and Region, 2026-2034

Vietnam Self Storage Market Size, Share, Trends & Forecast (2026-2034)

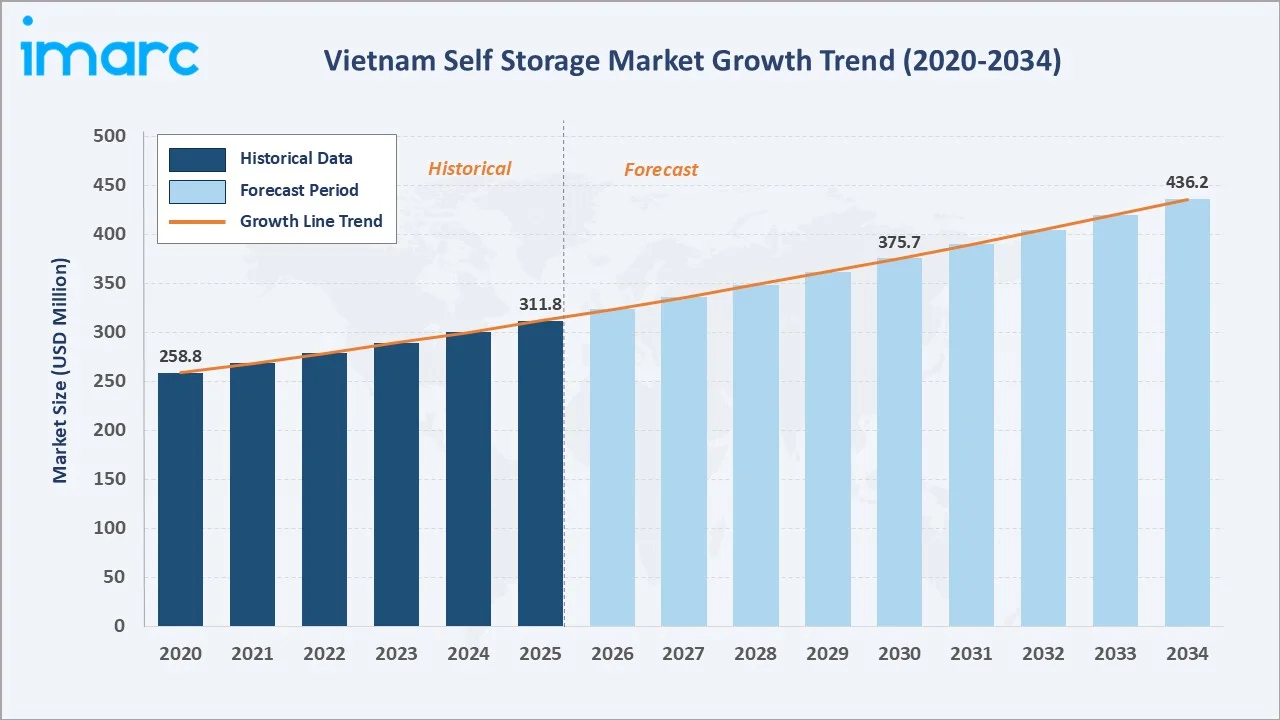

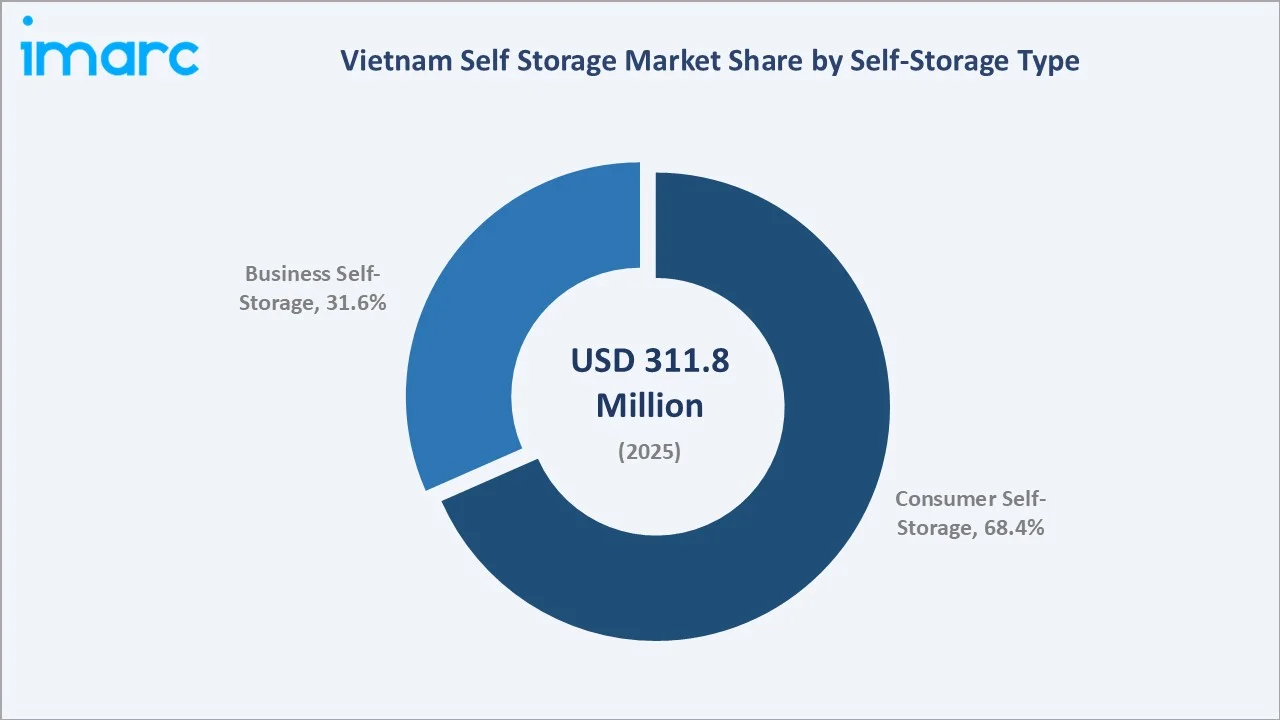

The Vietnam self storage market size reached USD 311.8 Million in 2025 and is projected to reach USD 436.2 Million by 2034, exhibiting a CAGR of 3.80% during 2026-2034. Increasing consumer demand for extra storage space driven by urbanization and smaller living apartments, the rise of e-commerce, and growing middle-class disposable income are the primary forces driving market growth.

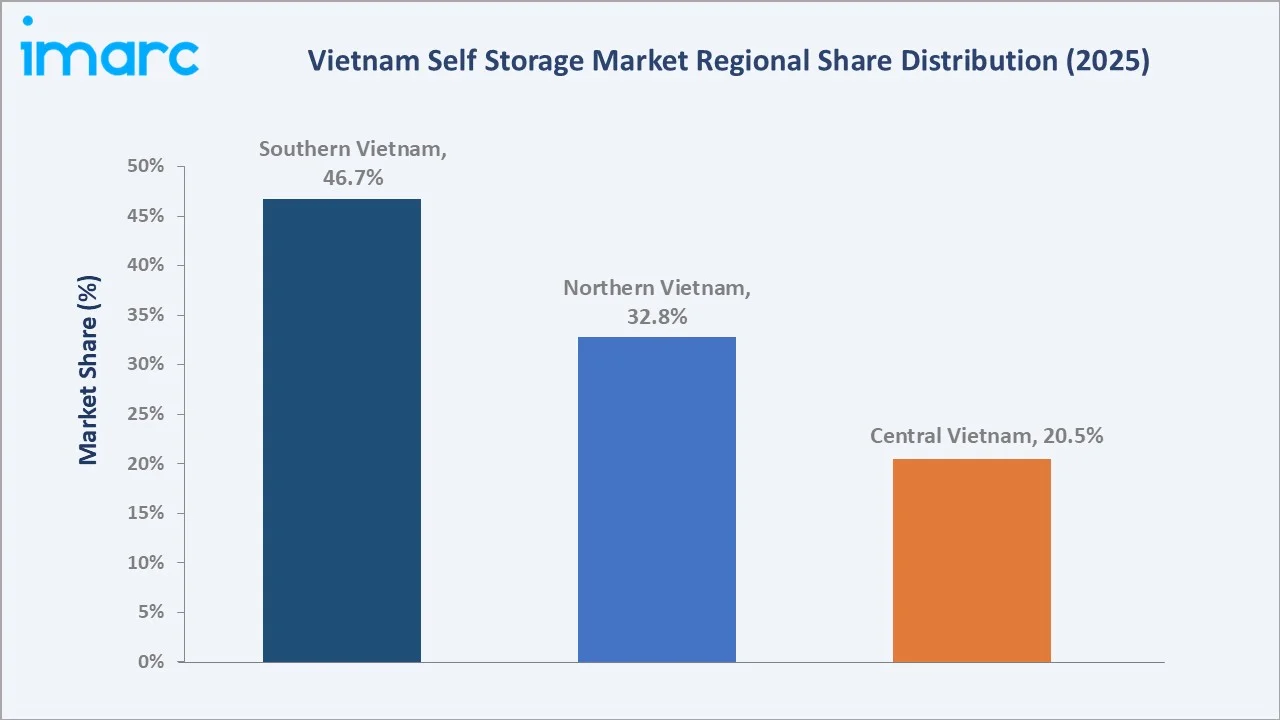

Consumer self-storage dominates at 68.4% in 2025, while Southern Vietnam commands a 46.7% regional share, reflecting Ho Chi Minh City's premier role as Vietnam's economic hub.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 311.8 Million |

|

Forecast Market Size (2034) |

USD 436.2 Million |

|

CAGR (2026-2034) |

3.80% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Southern Vietnam (46.7% share, 2025) |

|

Leading Self-Storage Type |

Consumer (68.4%, 2025) |

The Vietnam self storage market growth trajectory from 2020 through 2034, with historical expansion to USD 311.8 Million in 2025, reflects consistent urbanization-driven demand. The forecast to USD 436.2 Million captures accelerating e-commerce growth, increasing middle-class purchasing power, and digital adoption across storage booking platforms.

To get more information on this market, Request Sample

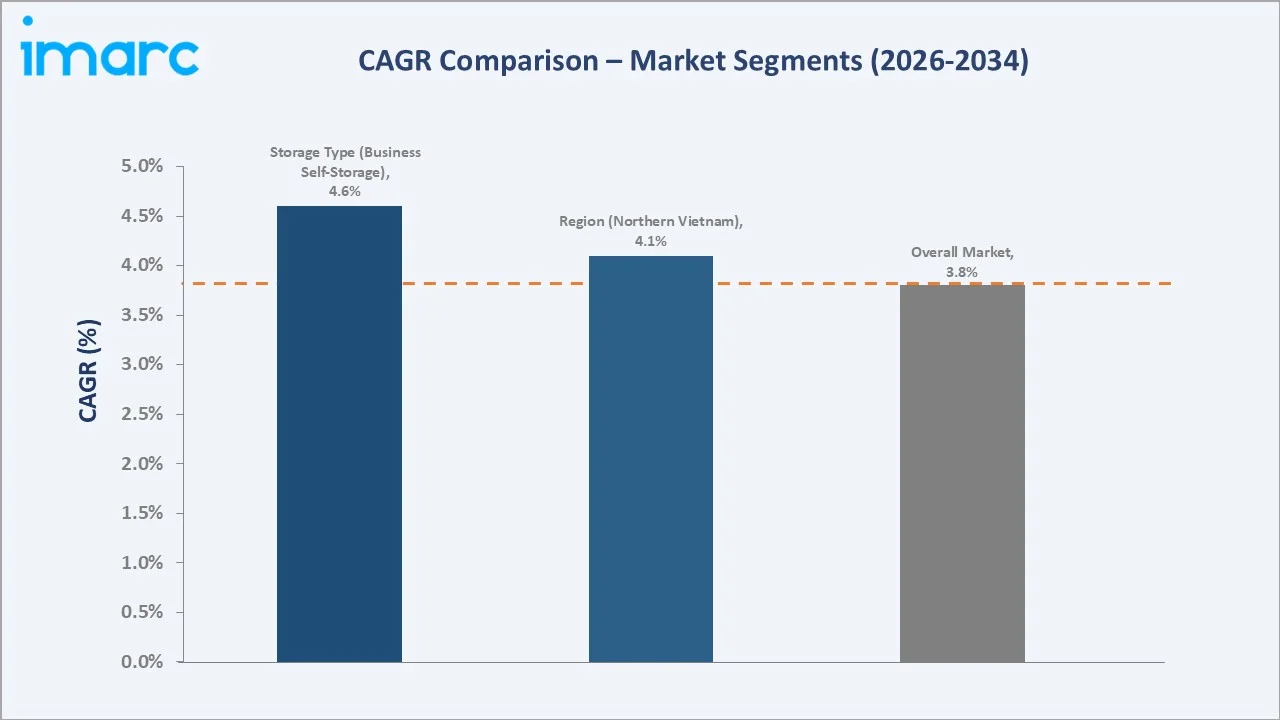

The CAGR trajectories across key self-storage type and regional sub-segments, with business self-storage at ~4.6% CAGR and Northern Vietnam at ~4.1% CAGR, represent the fastest-growing categories within the Vietnam self storage industry analysis through 2034.

Executive Summary

The Vietnam self storage market is on a sustained growth trajectory from USD 311.8 Million in 2025 to USD 436.2 Million by 2034. Self-storage, an essential service offering rented individual units or lockers within secure facilities, benefits from non-discretionary urbanization-linked demand and the expanding Vietnamese middle class.

Consumer self-storage dominates at 68.4% in 2025, driven by shrinking urban apartment sizes, expatriate population growth in Ho Chi Minh City and Hanoi, and lifestyle transitions among Vietnam's rapidly growing urban middle class. Business self-storage (31.6%) is the faster-growing segment at ~4.6% CAGR, driven by e-commerce sellers and SMEs requiring flexible, cost-effective warehousing alternatives.

Southern Vietnam commands 46.7% regional share in 2025, anchored by Ho Chi Minh City as Vietnam's dominant commercial center. Northern Vietnam (32.8%) follows, driven by Hanoi's expanding corporate base. Central Vietnam (20.5%) is the emerging frontier, with Da Nang's growing tourism and manufacturing sector creating incremental demand.

Key Market Insights

|

Insight |

Data |

|

Leading Self-Storage Type |

Consumer – 68.4% share (2025) |

|

Fastest-Growing Segment |

Business – ~4.6% CAGR (2026-2034) |

|

Largest Region |

Southern Vietnam – 46.7% (2025) |

|

Second Largest Region |

Northern Vietnam – 32.8% (2025) |

|

Smallest Region |

Central Vietnam – 20.5% (2025) |

|

Key Companies |

KingKho Storage Co., Ltd., Cube Self Storage Co. Ltd., V-Box Self Storage, MyStorage, Extra Space Asia, StorHub Group |

Key Analytical Observations Supporting the Above Data:

- Consumer self-storage, at 68.4% in 2025, dominates because of Vietnam's rapid urbanization and the proliferation of high-density micro-apartment developments in Ho Chi Minh City and Hanoi, where storage space per household is severely constrained and growing urban lifestyles generate increasing volumes of possessions.

- Business self-storage at 31.6% in 2025 is experiencing accelerated growth fueled by Vietnam's e-commerce sector, with SMEs and digital-native brands increasingly using self-storage as a cost-effective last-mile logistics and warehousing solution.

- Southern Vietnam's 46.7% dominance reflects Ho Chi Minh City's concentration of multinational companies, expatriates, and Vietnam's highest urban household incomes, generating dense, high-value storage demand within a constrained real estate market with limited affordable storage alternatives.

- Northern Vietnam's 32.8% share represents Hanoi's growing government, corporate, and diplomatic community alongside the city's rapid residential densification, creating structural consumer and business storage demand.

Vietnam Self Storage Market Overview

Self-storage refers to a service whereby individuals or businesses rent individual storage units or lockers within a secure, purpose-built facility on flexible short-to-medium-term leases. Units range from small locker-sized spaces to large rooms accommodating household furniture, vehicles, or significant business inventory. Facilities are equipped with security measures including CCTV surveillance, biometric access control, and on-site personnel.

The Vietnam self storage ecosystem integrates real estate developers, specialized storage facility operators, digital booking platforms, security technology providers, logistics partners, and a diverse base of consumer and business end users spanning residential households, SMEs, e-commerce sellers, expatriates, and multinational corporations operating across Vietnam's major urban centers.

Market Dynamics

To evaluate market opportunities, Request Sample

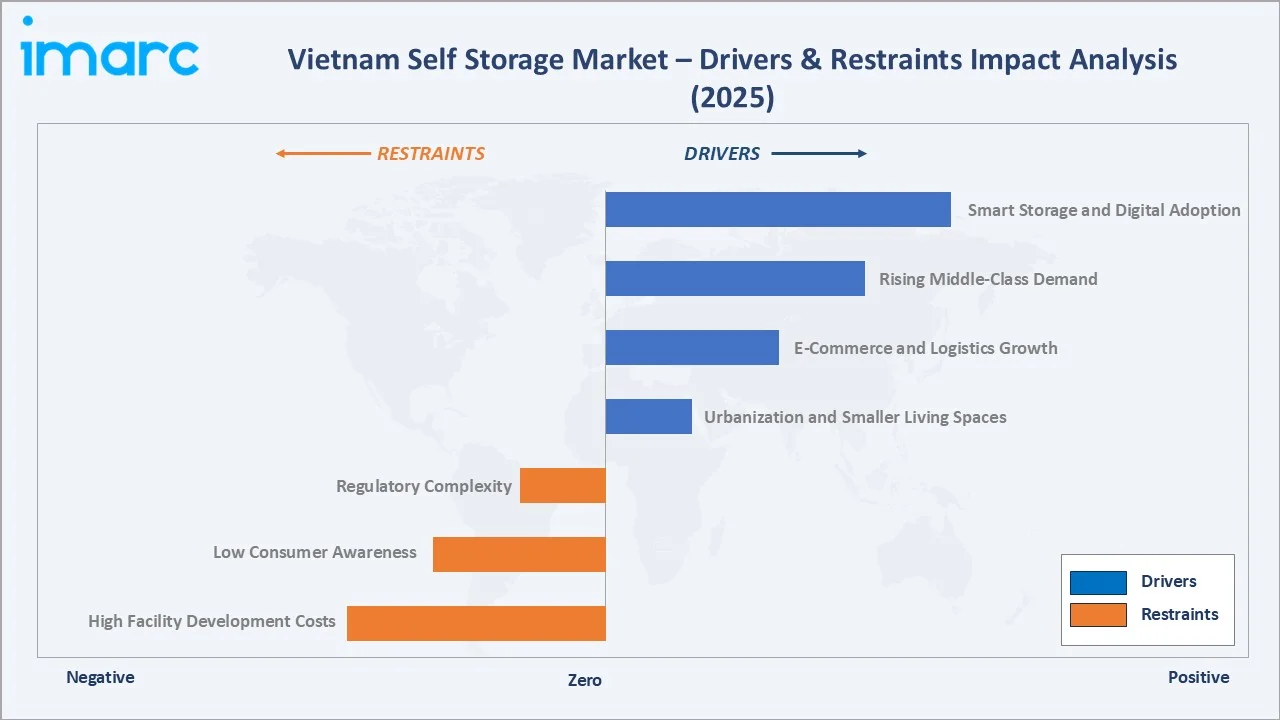

Market Drivers

- Urbanization and Smaller Living Spaces: Vietnam's urbanization rate exceeded 40% in 2021 with 868 urban areas, driving demand for high-density micro-apartments. Urban households in Ho Chi Minh City and Hanoi average below 50 sq m, creating structural demand for off-site storage solutions among growing middle-class families.

- E-Commerce and Logistics Growth: Vietnam's online retail sales exceeded USD 25 Billion in 2024, growing at approximately 20% annually. SMEs and e-commerce brands increasingly use business self-storage as a flexible, cost-effective warehousing and last mile fulfillment solution with no long-term lease commitments.

- Rising Middle-Class Demand: The middle class in Vietnam is expected to account for 26% of the country's population by 2026. Growing consumer spending on home furnishings, electronics, and seasonal goods is driving household storage demand among urbanizing Vietnamese families with increasing material possessions.

Market Restraints

- High Facility Development Costs: Purpose-built self-storage facilities require significant upfront capital for land acquisition, construction, and security technology installation in high-cost urban locations. Prime urban land scarcity in Ho Chi Minh City and Hanoi creates cost pressures that constrain supply expansion and raise rental price floors.

- Low Consumer Awareness: Self-storage is a relatively nascent concept in Vietnam beyond major urban centers. Consumer education and sustained marketing investment are required to build awareness and adoption outside Ho Chi Minh City and Hanoi, limiting addressable market growth in secondary cities.

- Regulatory Complexity: Vietnam lacks a clearly defined self-storage regulatory category, requiring operators to navigate warehouse, retail, and general-service regulations simultaneously. Approval timelines vary significantly by district and municipality, creating operational uncertainty for facility developers.

Market Opportunities

- Smart Storage and Digital Adoption: The integration of AI-driven occupancy forecasting, mobile booking applications, biometric access control, and smart environmental monitoring systems is creating differentiated premium storage products commanding higher rental rates and improving facility operational efficiency.

- Secondary City Expansion: Da Nang, Can Tho, Hai Phong, and Bien Hoa represent underserved markets with growing urban populations and limited self-storage supply. These markets offer first-mover advantages and above-average occupancy rates for operators willing to enter before competitive density increases.

- B2B E-Commerce Logistics Partnerships: Partnerships with Vietnamese e-commerce platforms and third-party logistics providers present significant revenue opportunities for business-oriented storage operators seeking to capture the growing SME and digital commerce inventory management market.

Market Challenges

- Price Sensitivity Among Users: A significant portion of potential self-storage customers in Vietnam remains price-sensitive, particularly among domestic SMEs and lower-income urban households. Operators must balance competitive pricing strategies with revenue requirements needed to sustain facility investment returns and expansion ambitions.

- Skilled Workforce Shortage: Vietnam's rapidly growing self-storage sector faces challenges in attracting and retaining qualified facility management and security personnel, particularly as multinational operators raise compensation standards and drive wage inflation across the sector.

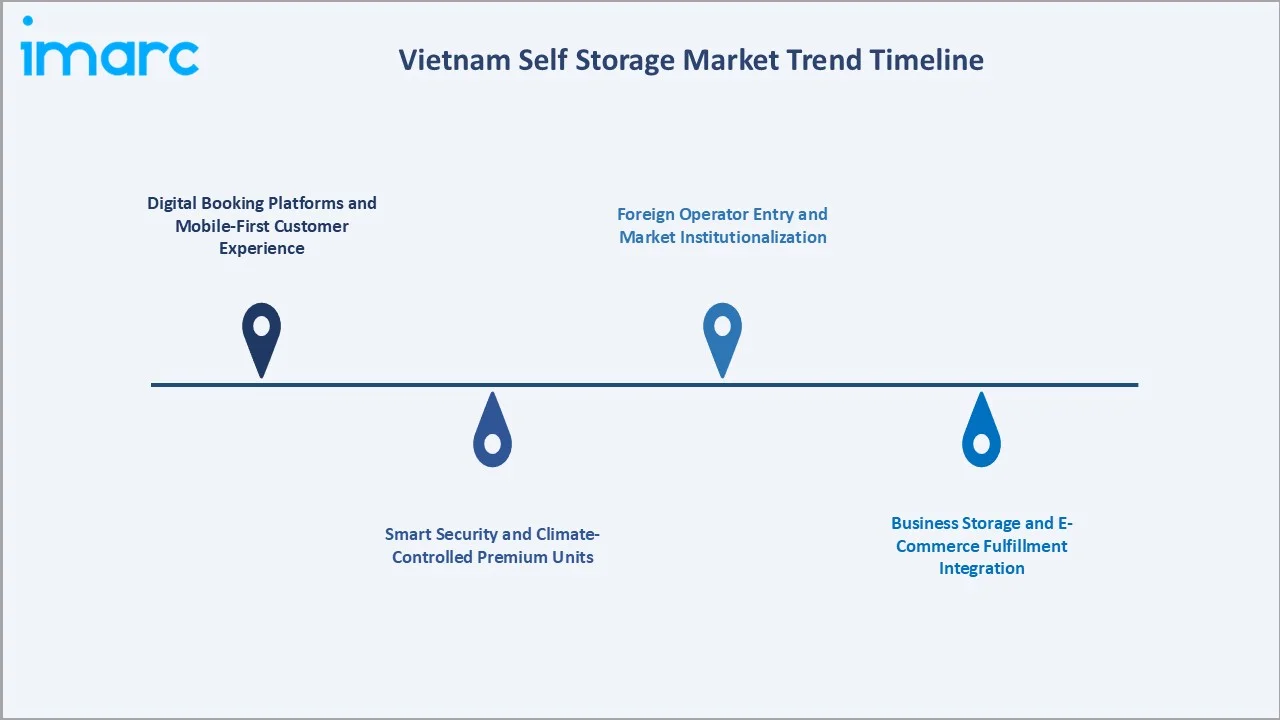

Emerging Market Trends

1. Digital Booking Platforms and Mobile-First Customer Experience

Online booking platforms and mobile applications are transforming self-storage accessibility in Vietnam. Operators deploying mobile-first reservation systems, digital payment rails including blockchain-based options introduced by BitcoinVN's investment in MyStorage, and real-time unit availability tracking are capturing disproportionate market share from technology-literate urban consumers and e-commerce businesses.

2. Smart Security and Climate-Controlled Premium Units

The incorporation of biometric access control, 24/7 CCTV surveillance, and IoT-enabled environmental monitoring is enabling premium-tier pricing for climate-controlled units. Expatriates and corporate clients demonstrate strong willingness-to-pay premiums for secure, monitored storage, with premium units commanding 40–60% rental rate premiums over standard consumer units in Ho Chi Minh City.

3. Business Storage and E-Commerce Fulfillment Integration

Self-storage operators are evolving beyond passive unit rental toward integrated fulfillment services for e-commerce businesses. Facilities offering inventory reception, pick-and-pack services, and same-day dispatch capabilities are commanding higher revenue per square meter and achieving structurally superior business tenant retention versus standard rental operators.

4. Foreign Operator Entry and Market Institutionalization

Regional self-storage leaders including Extra Space Asia and StorHub confirmed new facilities in Ho Chi Minh City and Hanoi in March 2025. Foreign operator entry is accelerating market formalization, introducing international operational standards, and validating institutional capital investment confidence in Vietnam's self-storage sector growth trajectory.

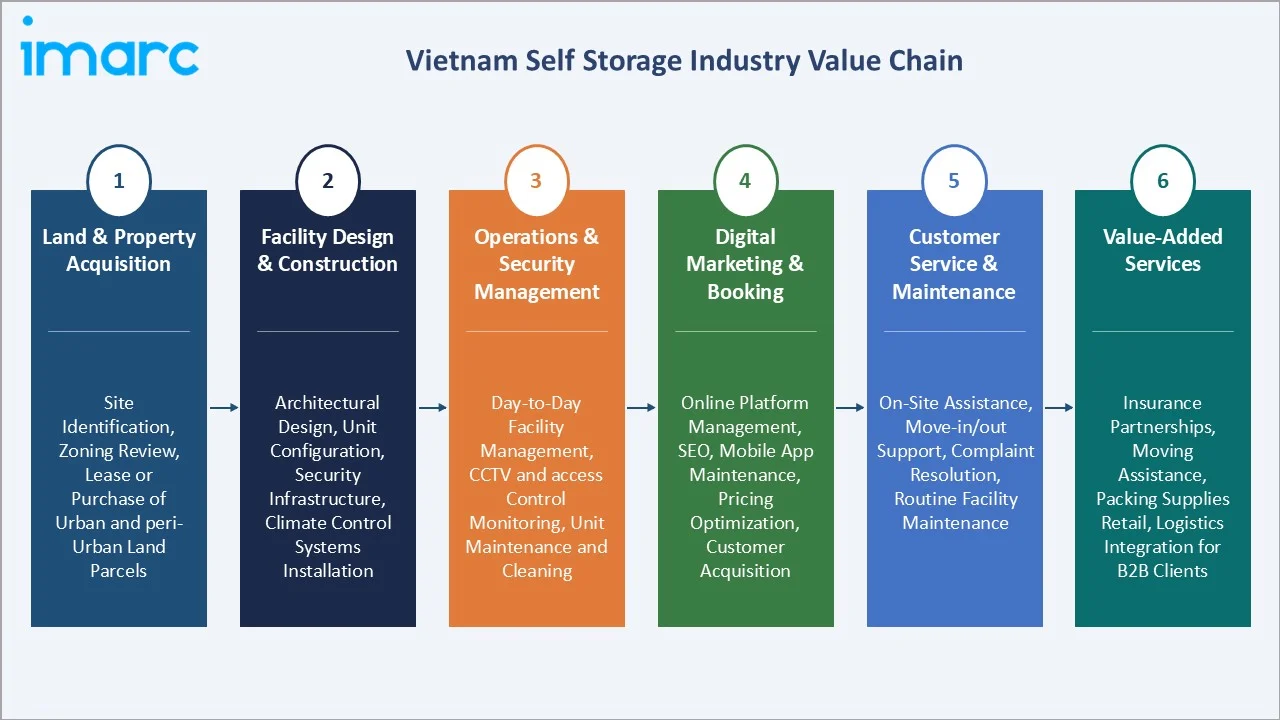

Industry Value Chain Analysis

The Vietnam self storage value chain spans six stages from land acquisition through value-added service delivery. Facility operations and digital marketing capture the highest ongoing revenue margins, while land acquisition and construction represent the highest capital deployment stages that determine long-term competitive positioning and barrier-to-entry levels.

|

Stage |

Key Activities / Examples |

|

Land & Property Acquisition |

Site identification, zoning review, lease or purchase of urban and peri-urban land parcels |

|

Facility Design & Construction |

Architectural design, unit configuration, security infrastructure, climate control systems installation |

|

Operations & Security Management |

Day-to-day facility management, CCTV and access control monitoring, unit maintenance and cleaning |

|

Digital Marketing & Booking |

Online platform management, SEO, mobile app maintenance, pricing optimization, customer acquisition |

|

Customer Service & Maintenance |

On-site assistance, move-in/out support, complaint resolution, routine facility maintenance |

|

Value-Added Services |

Insurance partnerships, moving assistance, packing supplies retail, logistics integration for B2B clients |

Integrated self-storage operators with proprietary digital booking platforms and in-house security monitoring capabilities achieve lower customer acquisition costs and higher occupancy utilization rates than operators relying entirely on third-party aggregators and manual management systems.

Digital platform ownership is becoming a meaningful competitive advantage in Vietnam's increasingly tech-driven urban storage market.

Technology Landscape in the Vietnam self storage Industry

Digital Platform and Mobile Booking Technology

Mobile-first booking platforms have become the standard customer acquisition channel for self-storage operators in Vietnam's urban markets. Operators deploying real-time inventory management systems, automated dynamic pricing algorithms, and digital contract execution are reducing customer acquisition costs while improving overall occupancy utilization across their facility portfolios.

Security Technology: Biometric and IoT-Enabled Systems

Advanced security systems incorporating biometric access controls, high-definition surveillance networks, and IoT environmental sensors are differentiating premium self-storage products and commanding occupancy premiums in competitive urban markets. BitcoinVN's 2025 investment in MyStorage introduced blockchain-based payment and real-time asset-tracking capabilities, establishing a new technology benchmark for the Vietnam market.

AI-Driven Occupancy Management and Revenue Optimization

Leading operators are deploying AI-driven occupancy forecasting models to dynamically adjust pricing, manage promotional discount ladders, and optimize revenue per square foot across their facility portfolios. These data-driven revenue management systems are enabling best-in-class operators to achieve sustained occupancy rates of 85–92% at optimized yield levels in high-demand urban locations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Self-Storage Type |

Consumer |

68.4% |

2025 |

|

Region |

Southern Vietnam |

46.7% |

2025 |

By Self-Storage Type

Consumer self-storage commands a 68.4% majority share in 2025, driven by structural demand from Vietnam's urbanizing population living in increasingly compact apartments. Consumer demand is underpinned by a non-discretionary storage requirement that is relatively insensitive to economic cycles, providing resilient occupancy floors for consumer-focused operators and predictable long-term revenue visibility.

To access detailed market analysis, Request Sample

Business self-storage at 31.6% in 2025, growing fastest at ~4.6% CAGR, serves e-commerce sellers, SMEs, retail brands, and multinationals requiring flexible inventory warehousing alternatives. The segment offers operators higher revenue per unit, lower seasonality variance, and longer average lease durations compared to residential consumer accounts, improving overall portfolio revenue stability.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Southern Vietnam |

46.7% |

HCMC commercial hub; expatriate demand; e-commerce logistics growth |

|

Northern Vietnam |

32.8% |

Hanoi government & corporate base; residential densification; SME growth |

|

Central Vietnam |

20.5% |

Da Nang tourism & manufacturing; emerging middle class; first-mover opportunity |

Southern Vietnam's 46.7% market dominance in 2025 is driven by Ho Chi Minh City's unparalleled concentration of multinationals, expatriates, and Vietnam's highest urban household incomes generating dense, high-value storage demand. The city's dense residential real estate market, with apartment sizes averaging below 60 sq m, creates persistent structural demand for off-site consumer storage that is expected to sustain above-average long-term occupancy.

Northern Vietnam, with 32.8% in 2025, is growing at ~4.1% CAGR, supported by Hanoi's expanding diplomatic community, rapid residential densification, and the growth of northern industrial zones generating business storage demand from manufacturing-linked SMEs and growing e-commerce fulfillment operations.

Competitive Landscape

The Vietnam Self Storage market is fragmented, with domestic operators holding strong local market positions and international operators beginning to scale their Vietnam presence. Local players leverage regulatory familiarity and location networks, while foreign operators bring institutional capital, tested technology platforms, and regional operational management expertise from established Southeast Asian markets.

|

Company Name |

Product Portfolio |

Market Position |

Strategic Focus |

|

KingKho Storage Co., Ltd. |

Personal storage, Business storage, Luggage storage, Storage for expats, Student storage, Document storage |

Leader |

Hanoi-based (Northern Vietnam); Vietnam's first self-storage company, internationally managed |

|

Cube Self Storage Co. Ltd. |

Self-Storage Solutions |

Leader |

Ho Chi Minh City leader; premium climate-controlled; urban consumer focus |

|

V-Box Self Storage |

Standard Self Storage Units, Climate Controlled Self-Storage Units, Shared Storage |

Leader |

Technology-enabled storage; mobile-first booking |

|

MyStorage |

Small, Medium, Large Self Storage |

Challenger |

HCMC; blockchain payment innovation; multi-site expansion with BitcoinVN investment |

|

Extra Space Asia |

Self-Storage Services |

Leader |

Regional leader; premium consumer & corporate; international brand |

|

StorHub Group |

Self-Storage Services |

Leader |

Regional playbook; digital-first operations; rapid scale-up |

Key players include KingKho Storage Co., Ltd., Cube Self Storage Co. Ltd., V-Box Self Storage, MyStorage, Extra Space Asia, StorHub Group, and others.

Key Company Profiles

KingKho Storage Co., Ltd.

KingKho Storage is one of Vietnam's leading domestic self-storage operators, with facilities concentrated in Northern Vietnam. The company has built a strong market position by combining competitive pricing, flexible lease terms, and deep understanding of local regulatory approval processes, providing a durable competitive moat against foreign entrants.

- Product Portfolio: Consumer self-storage units across multiple size tiers, SME business storage, document archiving, and others.

- Recent Developments: In December 2025, KingKho officially unveiled a new self-storage facility spanning 1,500 square meters, marking a significant step forward in its expansion of modern storage solutions across Vietnam. It offers a range of private storage units, each secured with individual locks, with sizes varying from 1 to 20 square meters to suit diverse needs.

- Strategic Focus: KingKho's strategy centers on leveraging home-field regulatory knowledge and established local client relationships to maintain occupancy leadership in Vietnam while selectively expanding into emerging second-tier markets with limited competitive supply and growing urbanizing populations.

Cube Self Storage Co. Ltd.

Cube Self Storage Co. Ltd. is a UK-origin self-storage operator established in 2003 as part of the Edward Baden Group Limited, with prior presence in the United Kingdom, Hong Kong, and Malaysia before entering Vietnam.

- Product Portfolio: Climate-controlled self-storage units, standard self-storage units, managed storage warehousing, luggage storage, and co-working space solutions integrated within storage facilities.

- Strategic Focus: Cube Self Storage's Vietnam strategy focuses on delivering international-grade, bespoke storage solutions across both consumer and business segments, differentiating on facility quality, climate-control technology, and service standards. The company targets expatriates, multinationals, and premium urban consumers in Ho Chi Minh City, leveraging its Edward Baden Group heritage and Southeast Asian operational experience to build a multi-facility network ahead of intensifying market competition.

V-Box Self Storage

V-Box Self Storage is a technology-forward Vietnamese operator offering mobile-first booking, smart access control, and transparent pricing across Ho Chi Minh City network. The company targets Vietnam's digitally active urban consumers and the rapidly growing base of e-commerce sellers requiring flexible, technology-enabled storage and fulfillment support.

- Product Portfolio: Consumer self-storage units, business storage with logistics integration capabilities, and smart locker solutions for urban high-density locations.

- Strategic Focus: V-Box positions itself at the intersection of technology and convenience, targeting younger urban consumers and tech-native e-commerce sellers who prioritize digital-first service experiences and operational transparency over price competition alone.

Market Concentration Analysis

The Vietnam Self Storage market is fragmented at both national and regional levels, with no single company holding more than 10–15% of total national revenue. Southern Vietnam is more concentrated, served primarily by KingKho, Saigon Storage, and V-Box, while Northern Vietnam has a more distributed competitive landscape with smaller independent operators alongside the larger national players.

Market consolidation is expected to accelerate from 2026 through 2030 as well-capitalized regional players such as Extra Space Asia and StorHub scale their footprints across Ho Chi Minh City, Hanoi, and secondary cities. Domestic operators will face increasing pressure to differentiate on digital capabilities, location networks, and service depth as international operators raise competitive standards across the market.

Investment & Growth Opportunities

Fastest-Growing Segments

Business self-storage at ~4.6% CAGR through 2034 is the highest-growth segment, driven by Vietnam's booming e-commerce sector and the growing preference of SMEs for flexible, off-balance-sheet warehousing solutions. Technology-enhanced premium consumer units in Ho Chi Minh City command 40–60% rental premiums over standard units and are experiencing above-average occupancy growth rates.

Emerging Markets

Central Vietnam at ~3.9% CAGR represents the most significant greenfield expansion opportunity. Da Nang's rapidly growing tourist accommodation economy, expanding manufacturing base, and emerging urban middle class are generating incremental storage demand in a market with minimal competitive supply and relatively lower land acquisition costs than the major cities.

Venture & Investment Trends

Private capital interest in Vietnam's self-storage market is accelerating significantly. BitcoinVN's 2025 investment in MyStorage, SPX Express and Frasers Property Vietnam's USD 30 Million logistics infrastructure allocation in Binh Duong in 2024, and the institutional foreign operator entries by Extra Space Asia and StorHub collectively validate the sector's growing attractiveness to sophisticated investors.

Future Market Outlook (2026-2034)

The Vietnam Self Storage market is forecast to expand from USD 311.8 Million in 2025 to USD 436.2 Million by 2034 at a CAGR of 3.80%, adding USD 124.4 Million in incremental annual market value over the forecast period. This sustained, consistent growth reflects the market's urbanization-linked, structural demand characteristics and growing business storage adoption.

Three structural forces will shape the market through 2034: continued urban densification in Ho Chi Minh City and Hanoi sustaining consumer demand growth; Vietnam's e-commerce sector expansion driving business storage adoption among SMEs and digital brands; and the entry of regional institutional operators introducing technology and operational standards that expand the market's premium tier.

Secondary city expansion into Da Nang, Can Tho, Hai Phong, and Bien Hoa represents the most significant incremental market opportunity through 2034. Operators building multi-city networks in the near term will capture first-mover advantages in these underserved markets before competitive dynamics of the major cities replicate themselves in Vietnam's rapidly urbanizing secondary urban centers.

Research Methodology

Primary Research

Primary research encompassed structured interviews with Vietnam self-storage industry stakeholders, including facility operators, real estate developers, e-commerce logistics managers, and consumer storage users across Ho Chi Minh City, Hanoi, and Da Nang. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines across the forecast period.

Secondary Research

Key secondary sources include Vietnam Ministry of Industry and Trade e-commerce sector data, General Statistics Office of Vietnam urbanization and population statistics, IMARC Group proprietary industry databases, operator-reported performance metrics, and regional trade press including Vietnam Economic Times. International data sources include World Bank urbanization indices and ASEAN economic investment reports.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating Vietnam GDP growth rates, urbanization indices, household income data, and historical market evolution patterns. Scenario analysis covering base, optimistic, and conservative cases was performed to account for macroeconomic and regulatory uncertainty across the 2026–2034 forecast horizon.

Vietnam Self Storage Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Self-Storage Types Covered | Consumer, Business |

| Regions Covered | Northern Vietnam, Central Vietnam, Southern Vietnam |

| Companies Covered | KingKho Storage Co., Ltd., Cube Self Storage Co. Ltd., V-Box Self Storage, MyStorage, Extra Space Asia, StorHub Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Vietnam self storage market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Vietnam self storage market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Vietnam self storage industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Vietnam Self Storage Market Report

The Vietnam self storage market reached USD 311.8 Million in 2025 and is forecast to reach USD 436.2 Million by 2034, growing at a CAGR of 3.80% during 2026-2034.

Consumer self storage dominates with a 68.4% share in 2025, driven by urbanization, smaller urban apartments, and growing middle-class household goods ownership. Business self-storage (31.6%) is the fastest-growing segment at ~4.6% CAGR, driven by e-commerce and SME demand.

Southern Vietnam leads with a 46.7% share in 2025, anchored by Ho Chi Minh City's commercial density, expatriate population, and concentrated e-commerce logistics demand. Northern Vietnam (32.8%) and Central Vietnam (20.5%) follow.

Key players include KingKho Storage Co., Ltd., Cube Self Storage Co. Ltd., V-Box Self Storage, MyStorage, Extra Space Asia, StorHub Group, and others.

Key growth drivers include rapid urbanization with shrinking apartment sizes in Ho Chi Minh City and Hanoi, Vietnam's booming e-commerce sector generating B2B storage demand, rising middle-class disposable income, and the adoption of smart security and digital booking platforms expanding market accessibility.

The Vietnam self storage market is projected to grow at a CAGR of 3.80% during 2026–2034. The business self-storage segment is growing faster at approximately 4.6% CAGR, while Northern Vietnam is the fastest-growing region at approximately 4.1% CAGR over the same period.

Major challenges include high facility development costs due to urban land scarcity in Ho Chi Minh City and Hanoi, low consumer awareness outside major urban centers, regulatory complexity due to the absence of a defined self-storage regulatory framework, and price sensitivity among target customer segments.

Key investment opportunities include secondary city greenfield development in Da Nang, Can Tho, and Hai Phong with minimal existing competition, technology-enhanced premium unit development commanding rental premiums, B2B e-commerce logistics partnerships, and market consolidation plays as international operators accelerate expansion, and domestic operators seek strategic partnerships.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade