Vinyl Record Market Size, Share, Trends and Forecast by Product, Feature, Gender, Age Group, Application, Distribution Channel, and Region, 2026-2034

Vinyl Record Market Size, Share, Trends & Forecast (2026-2034)

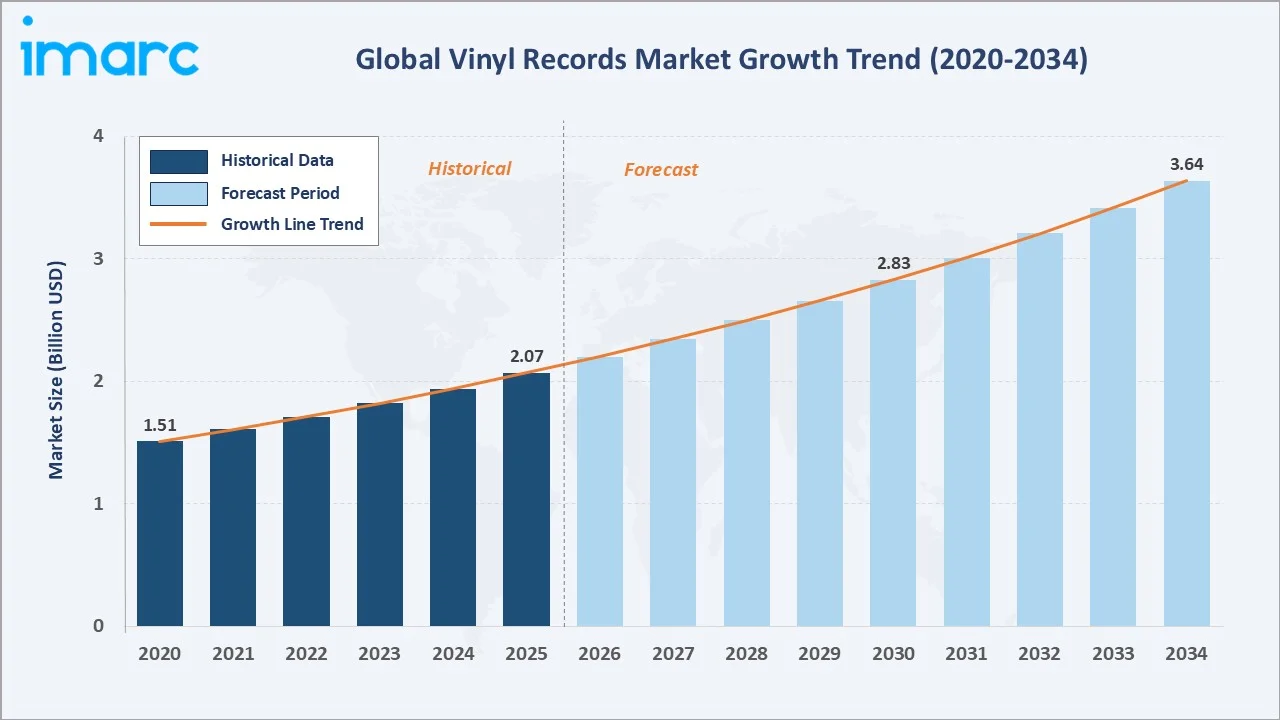

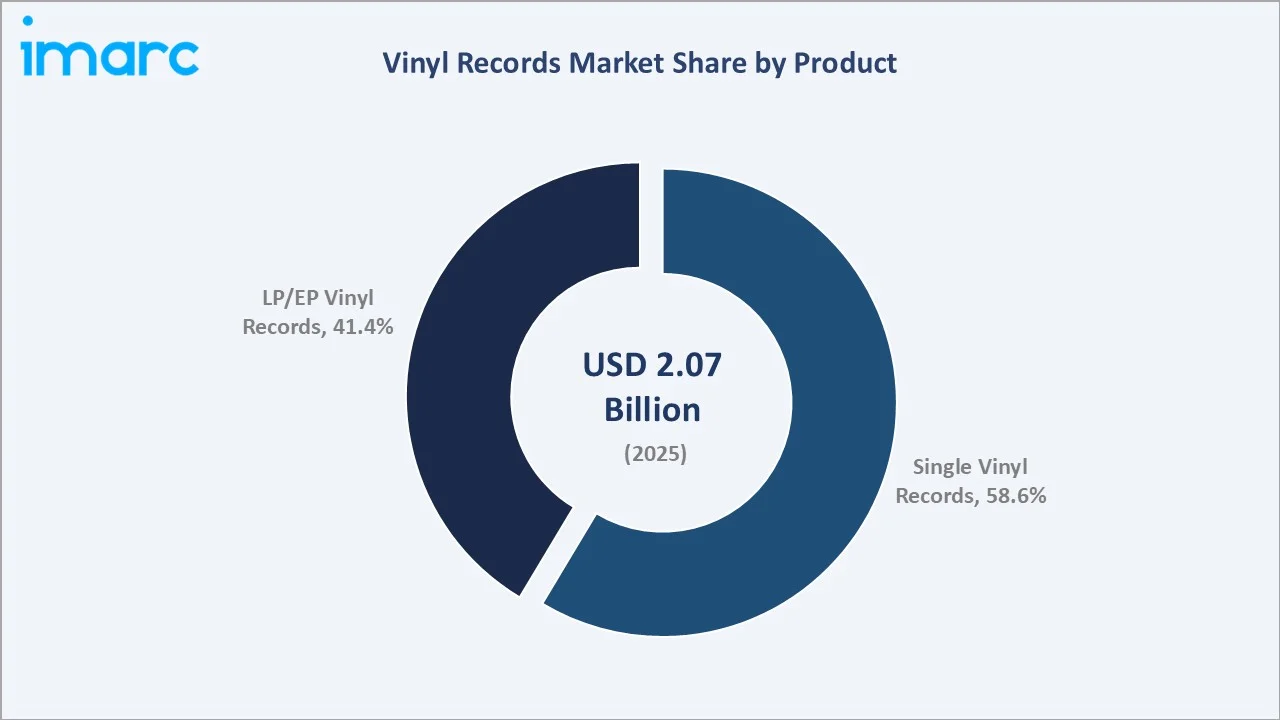

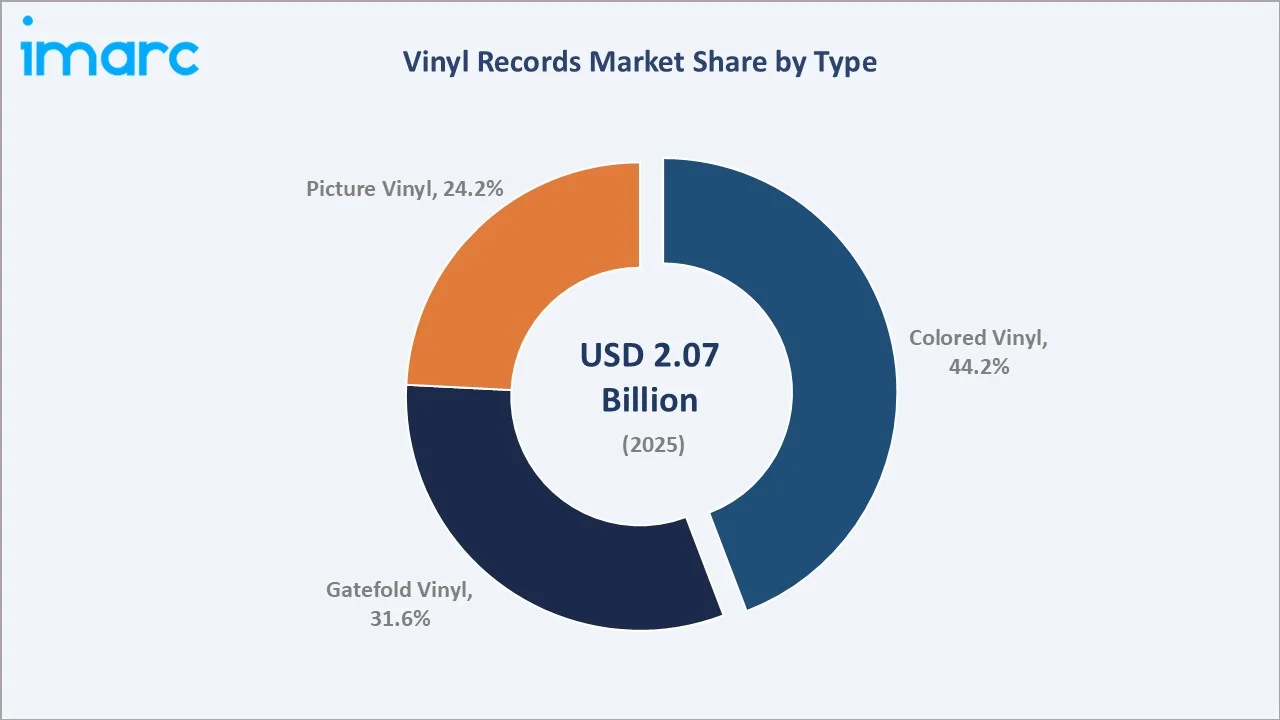

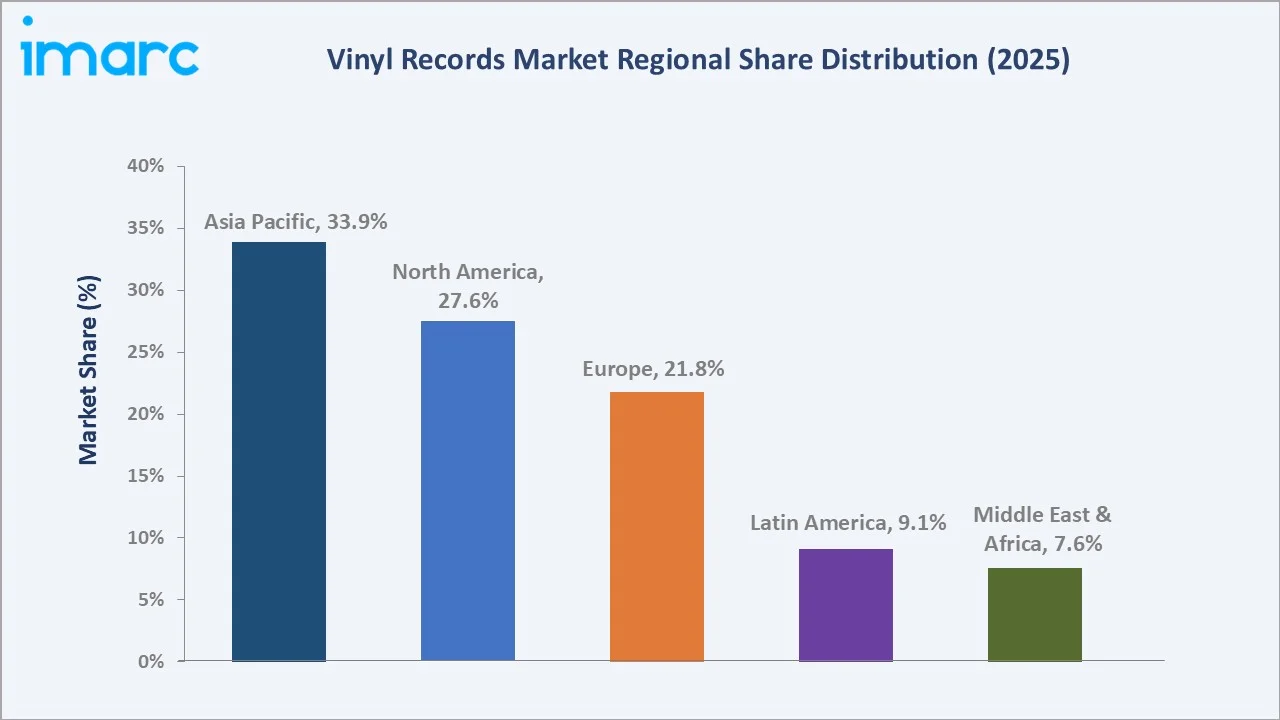

The global vinyl record market size was valued at USD 2.07 Billion in 2025 and is projected to reach USD 3.64 Billion by 2034, exhibiting a CAGR of 6.48% during the forecast period 2026-2034. The renewed cultural fascination with analog audio, artist-led vinyl exclusives, and a thriving collector economy are powering vinyl record market growth. Single Vinyl Records dominate with a 58.6% share in 2025, while Colored Vinyl leads by type at 44.2%. Asia Pacific commands the largest regional position at 33.9%, supported by Japan, South Korea, and Australia, alongside expanding e-commerce penetration.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.07 Billion |

|

Forecast Market Size (2034) |

USD 3.64 Billion |

|

CAGR (2026-2034) |

6.48% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (33.9% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (Premium audio + young collectors) |

|

Leading Segment (by Product) |

Single Vinyl Records (58.6%, 2025) |

|

Leading Segment (by Type) |

Colored Vinyl (44.2%, 2025) |

The vinyl record market growth trajectory from 2020 through 2034 reflects a steady pre-2025 climb from USD 1.51 Billion to USD 2.07 Billion, followed by a sustained forecast curve driven by indie label resurgence, artist-led exclusive drops, and premium pressing demand across collector segments.

To get more information on this market, Request Sample

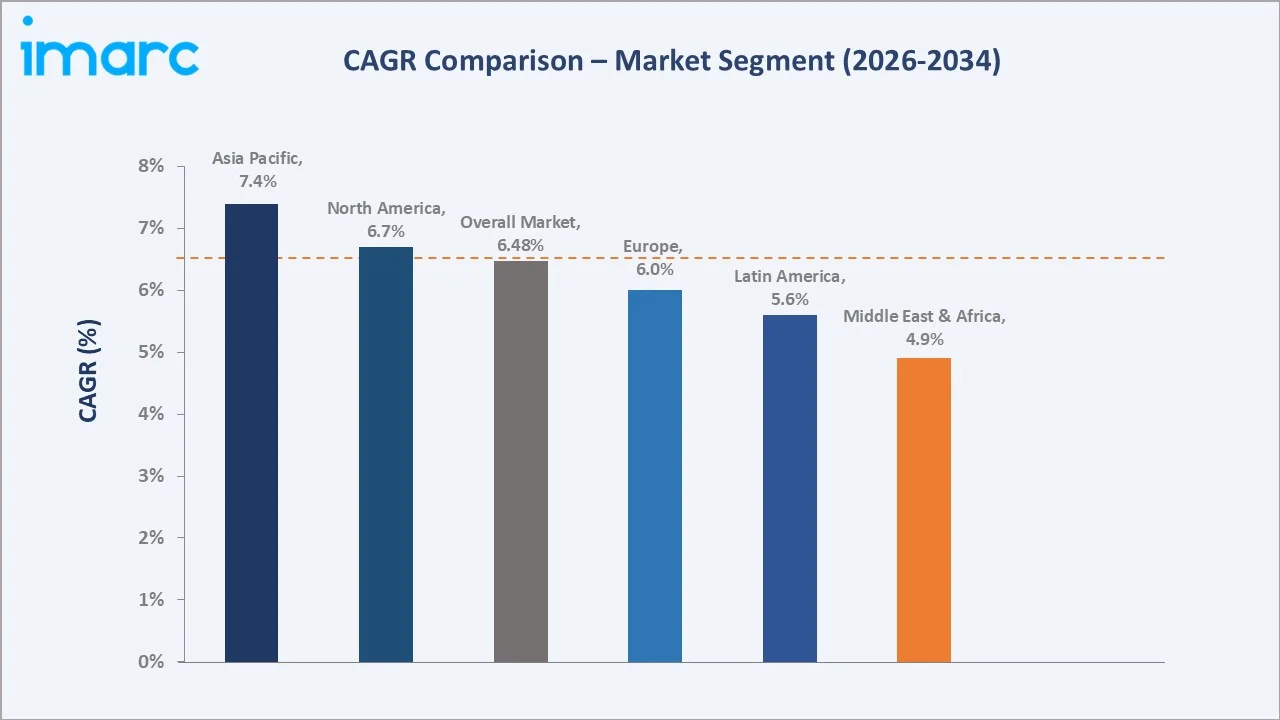

Regional CAGR analysis highlights Asia Pacific and North America as the fastest-growing engines within the vinyl record market forecast through 2034, fueled by digital-era nostalgia and audiophile-led premiumization across both mature and emerging markets.

Executive Summary

The vinyl record market is undergoing a remarkable cultural revival, driven by collector demand, artist-led exclusive pressings, and the broader analog renaissance among younger consumers. Valued at USD 2.07 Billion in 2025, the market is forecast to reach USD 3.64 Billion by 2034 at a CAGR of 6.48%. Vinyl is no longer a legacy format. It is a lifestyle product, with global LP sales recording double-digit growth annually since 2020.

Single Vinyl Records lead the product mix at 58.6% in 2025, supported by short-run artist drops, anniversary editions, and viral chart hits being pressed for collector audiences. Colored Vinyl commands 44.2% by type, followed by Gatefold at 31.6% and Picture discs at 24.2%. Premium variants are driving 1.5x to 2x the price of standard black vinyl.

Asia Pacific holds 33.9% of the global market, anchored by Japan, South Korea, and Australia. North America follows at 27.6%, while Europe accounts for 21.8%. The vinyl record market outlook remains positive as Gen Z adoption, cross-border e-commerce, and limited-edition pressings continue to expand revenue pools through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product) |

Single Vinyl Records – 58.6% share (2025) |

|

Second Segment (Product) |

LP/EP Vinyl Records – 41.4% share (2025) |

|

Largest Segment (Type) |

Colored Vinyl – 44.2% share (2025) |

|

Second Segment (Type) |

Gatefold Vinyl – 31.6% share (2025) |

|

Leading Region |

Asia Pacific – 33.9% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific – Accelerating at ~7.4% CAGR |

|

Top Companies |

Sony Music Entertainment, Universal Music Group, Warner Music Group, GZ Media, United Record Pressing |

|

Market Opportunity |

Artist-led exclusive drops and Gen Z collector economy |

Key Analytical Observations Supporting the Above Data:

- Single Vinyl Records' 58.6% dominance in 2025 reflects the rise of artist-driven 7-inch drops, viral chart hits, and short-run pressings. The global indie music ecosystem continues to drive vinyl output, with thousands of new titles released annually, supported by the resurgence of physical formats and direct-to-consumer channels.

- LP/EP Vinyl Records' 41.4% share is anchored by full-album releases, deluxe reissues, and audiophile editions. Vinyl sales hit $1 Billion in the United States in 2025, marking the 18th consecutive year of growth.

- Colored Vinyl's 44.2% lead reflects the format's transformation into a visual-first collectible. Limited-edition colored variants typically command price premiums over standard black pressings, fuelling margin expansion.

- Gatefold Vinyl at 31.6% continues to attract premium buyers seeking elaborate cover art, lyric inserts, and double-LP packaging. Major reissue programs are pushing gatefold pressings into the mainstream.

- Asia Pacific's 33.9% regional leadership is anchored by Japan's mature audiophile base, South Korea's K-pop vinyl exclusives, and Australia's strong indie scene. Japan alone represents a fractional amount of regional vinyl sales.

- Asia Pacific is the fastest-growing region at an estimated 7.4% CAGR through 2034, supported by K-pop collector culture, J-pop reissues, and rapidly expanding online vinyl retail in India, China, and Southeast Asia.

Global Vinyl Record Market Overview

Vinyl records are analog sound storage discs pressed on polyvinyl chloride (PVC) and played using turntables. The global vinyl records industry spans single records, LPs, EPs, and a growing range of colored, gatefold, and picture variants. Major end users include collectors, audiophiles, DJs, music retailers, and indie record stores.

The market sits at the crossroads of music streaming's digital fatigue, the broader vintage revival, and the post-pandemic surge in physical music ownership. Macroeconomic factors such as rising disposable incomes among Gen Z, social media-driven aesthetic culture, and the over 1,400 active independent record stores worldwide collectively shape vinyl record market trends and growth patterns.

Market Dynamics

To evaluate market opportunities, Request Sample

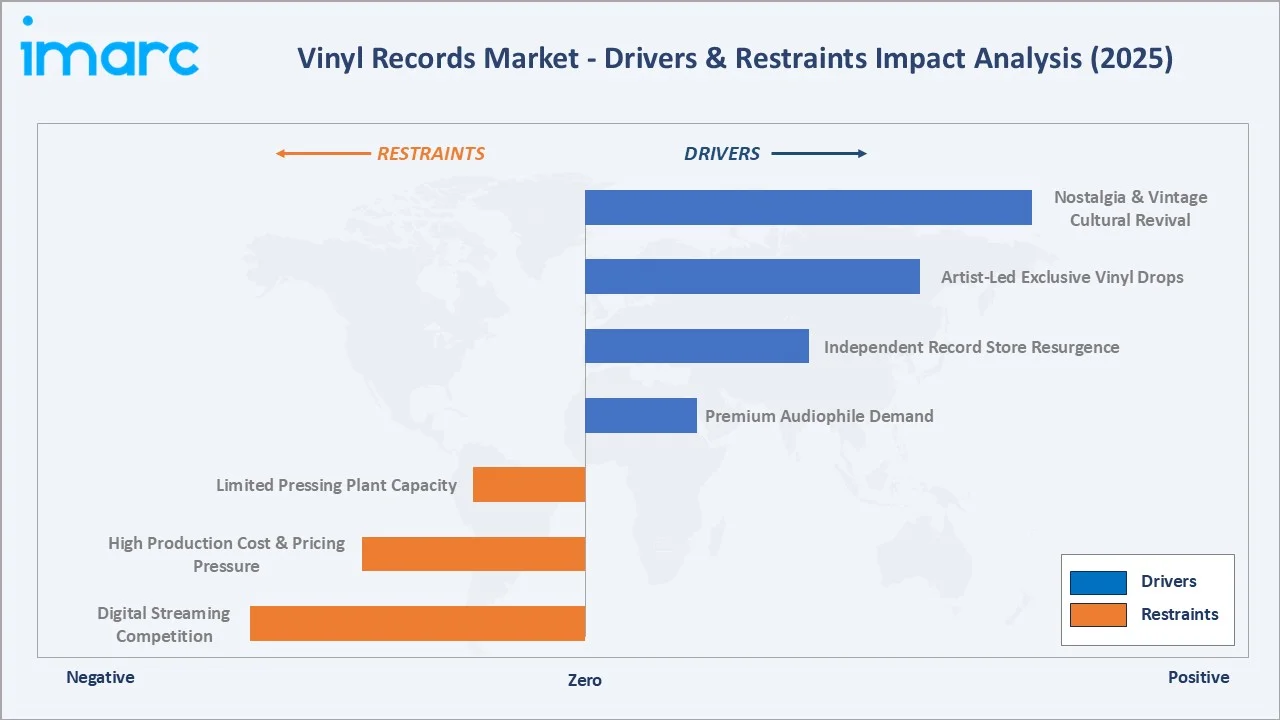

Market Drivers

- Nostalgia and Vintage Cultural Revival: The post-2020 cultural shift toward analog experiences has created an enduring demand for vinyl. Vinyl LP sales reached over $1 Billion units in the US alone in 2025, the 18th straight year of growth, highlighting how nostalgia continues to convert into recurring purchases.

- Artist-Led Exclusive Vinyl Drops: Major artists including Taylor Swift, Olivia Rodrigo, and BTS routinely launch vinyl-only variants with bonus tracks, alternate covers, and signed editions. Taylor Swift was responsible for 7% vinyl units in 2023, more than any artist in modern history, reshaping label release strategies.

- Premium Audiophile Demand: High-end pressings on 180-gram and 200-gram heavyweight vinyl, along with half-speed mastered editions, are commanding price points of USD 40-80 per unit. This audiophile-grade segment is growing at roughly 1.5x the broader vinyl market rate.

- Independent Record Store Resurgence: Record Store Day, observed annually since 2008, generated over USD 80 Million in vinyl sales in 2024 alone. More than 1,500 independent stores worldwide now anchor a vibrant retail ecosystem, supporting niche releases and limited pressing.

Market Restraints

- High Production Cost and Pricing Pressure: Vinyl pressing costs have risen since 2020 due to PVC raw material inflation and energy expenses. The average new vinyl LP retails for USD 25-35, limiting mass-market adoption among price-sensitive listeners.

- Limited Pressing Plant Capacity: Global vinyl pressing capacity is concentrated among roughly 50 major plants, leading to lead times of 6-9 months for new releases. This creates supply bottlenecks that constrain how quickly labels can respond to spike demand.

- Digital Streaming Competition: Spotify, Apple Music, and YouTube Music collectively serve over 700 Million paying subscribers in 2025. Streaming's convenience and library breadth continue to limit vinyl's mass-market share to under 8% of total recorded music revenue globally.

Market Opportunities

- Gen Z and Young Collector Economy: Roughly 50% of new vinyl buyers in 2024 were aged 18-34, signalling a structural generational shift. Younger consumers are driving vinyl’s resurgence, with social-media-led discovery and platform-driven trends accelerating demand and shaping the growth of the format.

- Direct-to-Consumer Artist Stores: Platforms such as Bandcamp, Shopify, and artist-owned stores have unlocked direct vinyl sales bypassing traditional retail. Bandcamp alone reported USD 150+ Million in artist payouts in 2024, with vinyl as the highest-margin format.

- Sustainable and Bio-Based Vinyl: Companies such as Green Vinyl Records and Evolution Music are commercializing PVC-free and bio-resin alternatives. The sustainable vinyl segment is forecast to expanded CAGR through 2034 as eco-conscious consumers seek lower-carbon pressings.

Market Challenges

- Quality Control in Mass Pressing: Surface noise, warping, and mispressing complaints have risen as plants run at full capacity. Customer return rates at major retailers in 2024, creating reputational and margin pressure across the value chain.

- Environmental Impact of PVC: Traditional vinyl production relies on PVC, a non-biodegradable polymer. Regulatory scrutiny in the EU under proposed plastics directives could increase compliance costs over the next five years for major pressing plants.

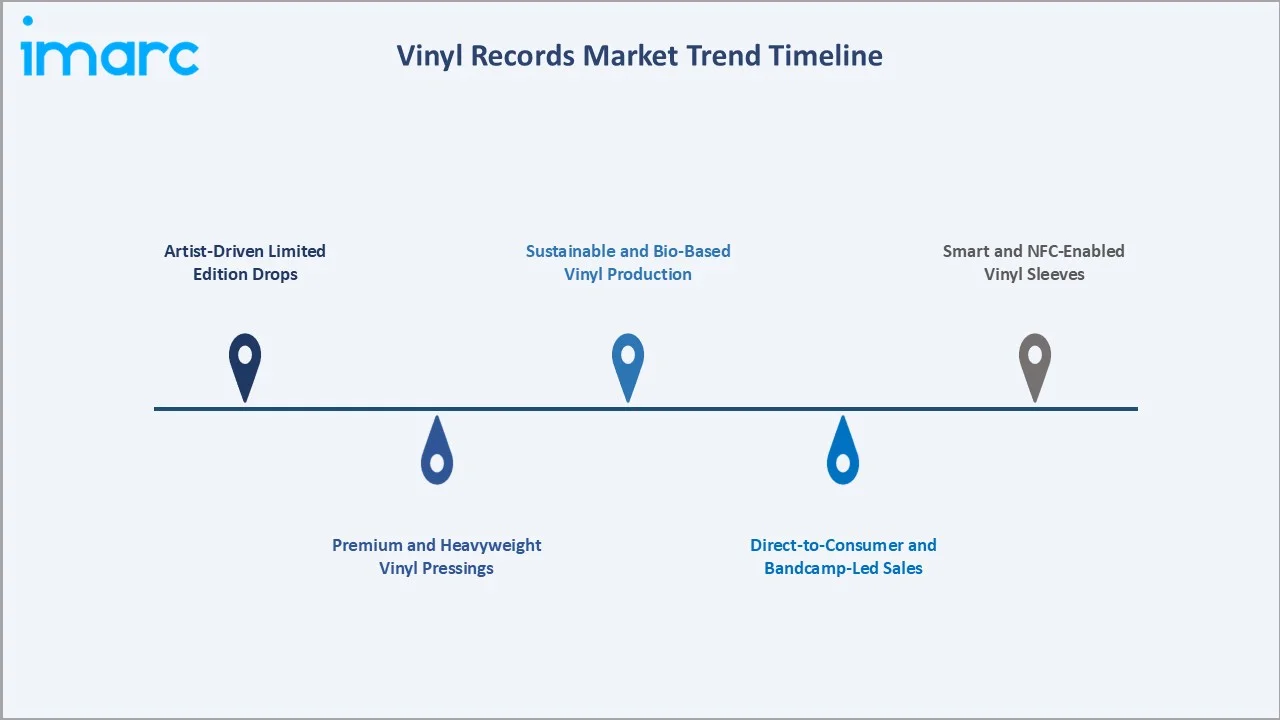

Emerging Market Trends

1. Artist-Driven Limited Edition Drops

Major and indie artists are increasingly using exclusive vinyl variants as a primary engagement tool with their fanbase. Taylor Swift's 2023 vinyl sales accounted for 7% of the total sales alone, while K-pop acts such as BTS and BLACKPINK routinely sell out limited Korean pressings within minutes. This trend is fundamentally reshaping how labels plan their release calendars and inventory commitments.

2. Premium and Heavyweight Vinyl Pressings

Audiophile-grade pressings on 180-gram and 200-gram heavyweight vinyl are gaining strong traction. Half-speed mastered and direct-to-disc editions are commanding prices of USD 40-80 per unit. The premium pressings sub-segment is growing at roughly 1.5x the broader market and now represents an estimated 18% of total category revenue in 2025.

3. Sustainable and Bio-Based Vinyl Production

Pressing plants are piloting PVC-free, recycled, and bio-resin alternatives. Green Vinyl Records and Evolution Music have demonstrated bio-vinyl prototypes with comparable acoustic fidelity. The sustainable vinyl sub-segment is forecast to scale the CAGR through 2034 as the EU and California advance plastics-related regulation.

4. Direct-to-Consumer and Bandcamp-Led Sales

Artist-owned stores and platforms such as Bandcamp and Shopify are unlocking direct vinyl sales bypassing traditional retail. Bandcamp paid out over USD 150+ Million to artists in 2024, with vinyl emerging as the most profitable physical format. This DTC channel offers margins 2-3x higher than wholesale models.

5. Smart and NFC-Enabled Vinyl Sleeves

Emerging pressings feature NFC tags, QR codes, and AR-enabled sleeves linking the physical object to digital extras such as exclusive videos, lyric content, and concert footage. This convergence of analog and digital is redefining what a vinyl release can deliver, with major labels expected to scale smart sleeves through 2027.

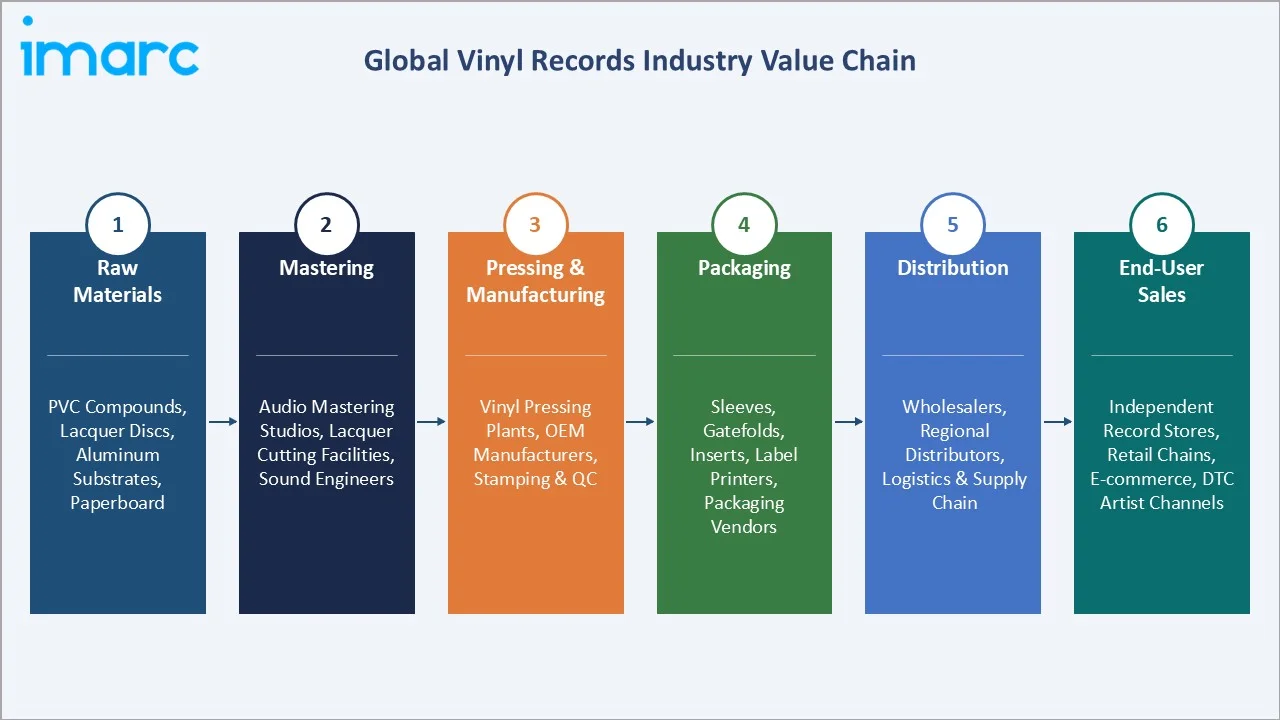

Industry Value Chain Analysis

The global vinyl records industry value chain spans six integrated stages from raw PVC and lacquer sourcing through end-consumer purchase. Each stage carries distinct competitive dynamics, capital requirements, and strategic opportunity relevant to the overall vinyl record market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Suppliers of PVC compounds, lacquer discs, aluminum substrates, and paperboard used for sleeves and packaging |

|

Mastering |

Audio mastering studios, lacquer cutting facilities, and sound engineers responsible for preparing recordings for vinyl production |

|

Pressing & Manufacturing |

Vinyl pressing plants and OEM manufacturers handling stamping, pressing, and quality control of records |

|

Packaging |

Printing and packaging vendors producing sleeves, gatefolds, inserts, and labels for finished products |

|

Distribution |

Wholesalers, regional distributors, and logistics providers managing inventory movement and supply chain coordination |

|

End-User Sales |

Independent record stores, large retail chains, e-commerce platforms, and direct-to-consumer artist channels |

Pressing plants hold the highest strategic value due to their fixed-capacity nature and current global supply constraint. GZ Media of the Czech Republic alone presses an estimated 70 Million units annually, making it the world's largest player. Mastering studios and packaging printers are increasingly bundling services to capture more value per release.

Technology Landscape in the Vinyl Records Industry

Pressing Technology and Automation

Modern automated pressing lines from Pheenix Alpha and Newbilt Machinery have boosted plant throughput versus legacy 1970s presses. Average press cycle times have dropped from 32 seconds to under 24 seconds per unit, helping plants address the persistent global supply backlog.

Materials Innovation and Sustainable Vinyl

Companies such as Green Vinyl Records, Evolution Music, and Deepgrooves Pressing Plant are commercializing PVC-free and bio-resin pressings. Recent prototypes have achieved comparable acoustic fidelity with lower carbon footprint. The sustainable vinyl segment is on track.

Smart Sleeve and NFC Connectivity

NFC tags, QR codes, and AR-enabled vinyl sleeves are creating bridges between physical pressing and exclusive digital content. Major labels are piloting smart sleeves with bonus video, lyric content, and concert footage, with mainstream commercialization expected by 2027.

Mastering and Audio Restoration

AI-driven audio restoration tools from iZotope and Waves are enabling cleaner reissues of decades-old recordings. Half-speed mastering and direct-to-disc cutting techniques have re-emerged as premium formats, supporting the audiophile sub-segment's 18% revenue contribution.

Market Segmentation Analysis

IMARC Group provides analysis of the key trends in each segment of the global vinyl record market, along with forecasts at the regional and global level from 2026 to 2034. The market has been analyzed based on Product and Type.

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Single Vinyl Record |

58.6% |

2025 |

|

Feature |

Colored |

44.2% |

2025 |

|

Gender |

Men |

🔒 |

2025 |

|

Age Group |

26-35 |

🔒 |

2025 |

| Application | Private | Private | 2025 |

| Distribution Channel | Independent Retailers | 🔒 | 2025 |

|

Region |

Asia Pacific |

33.9% |

2025 |

By Product

Single Vinyl Records lead the product segment with a 58.6% market share in 2025. The format's dominance is driven by short-run artist drops, viral chart hits, anniversary editions, and the rise of 7-inch collectible releases.

To access detailed market analysis, Request Sample

LP/EP Vinyl Records hold a 41.4% share in 2025, driven by full-album releases, deluxe reissues, and audiophile editions. Vinyl LPs of $1 Billion were sold in the United States alone in 2024, marking 18 consecutive years of growth. Average price points for LPs range from USD 25-45, with deluxe editions reaching USD 60-100.

By Type

Colored Vinyl commands the largest share at 44.2% in 2025. The format's appeal lies in its visual collectibility, with translucent, splattered, marble, and glow-in-the-dark variants commanding price premiums over standard black pressings. Major artists routinely release 5-8 colored variants per album to drive completist purchasing behaviour.

Gatefold Vinyl hold a 31.6% share in 2025. The format is favoured for elaborate cover art, lyric inserts, and double-LP packaging. Premium reissue programs from Mobile Fidelity Sound Lab and Analogue Productions have positioned gatefold vinyl as the preferred audiophile format, with average price points of USD 50-80.

Picture Vinyl represents 24.2% of the market. These visually striking discs feature artwork printed directly onto the playable surface and are widely used for limited tour editions, fan-club exclusives, and Record Store Day releases. Picture discs typically retail at USD 30-55 and command strong secondary-market resale value.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

33.9% |

Japan audiophile base, K-pop vinyl exclusives, Australia indie scene, China & India e-commerce expansion |

|

North America |

27.6% |

Record Store Day, Taylor Swift effect, indie store revival, Bandcamp DTC sales |

|

Europe |

21.8% |

GZ Media (Czech) pressing capacity, UK Record Store Day, Germany audiophile market |

|

Latin America |

9.1% |

Brazil & Mexico indie scenes, growing collector base, vintage record fairs |

|

Middle East & Africa |

7.6% |

UAE audiophile retailers, South Africa indie pressing, growing youth interest |

Asia Pacific commands 33.9% of the global vinyl record market in 2025. Japan anchors regional demand with one of the world's most mature audiophile cultures, contributing nearly 30% of regional revenue. South Korea's K-pop ecosystem has transformed vinyl into a cornerstone of fan engagement, with BTS, BLACKPINK, and SEVENTEEN releases routinely selling out within minutes. Australia's indie scene and growing e-commerce penetration in India and China further reinforce regional momentum.

North America holds 27.6%. The United States alone sold over $1 Billion in 2024, the 18th consecutive year of growth. Record Store Day generates over USD 80 Million in single-day sales annually. Taylor Swift's 2023 vinyl run of 7% of total sales single-handedly reshaped the US release calendar, while Bandcamp's DTC platform delivered USD 150+ Million in artist payouts in 2024.

Europe represents 21.8% of global market value. The Czech Republic's GZ Media is the world's largest pressing plant, delivering an estimated 70 Million units annually. The United Kingdom's Record Store Day, Germany's Berlin-based audiophile retailers, and the Netherlands' boutique pressing scene collectively underpin regional demand.

Latin America accounts for 9.1%. Brazil and Mexico anchor the regional market with vibrant indie scenes, growing vinyl fairs, and rising collector demand among urban millennials. Brazilian pressings of MPB classics and Mexican releases of regional Mexican music are gaining international resale traction.

Middle East & Africa holds the smallest regional share at 7.6%. The United Arab Emirates leads with audiophile-focused retailers in Dubai, while South Africa's indie pressing scene and growing youth interest in Egypt and Nigeria are establishing structured market foundations for the next decade.

Competitive Landscape

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

Sony Music Entertainment |

Legacy Recordings |

Leader |

Catalogue depth, global distribution, premium reissues |

|

Universal Music Group |

Capitol Records, Decca |

Leader |

Largest music catalogue, vinyl-first releases |

|

Warner Music Group |

Rhino Entertainment |

Leader |

Iconic reissue programs, audiophile editions |

|

GZ Media |

GZ Media |

Leader |

Largest global pressing capacity (~30M units annually) |

|

United Record Pressing |

United Record Pressing |

Challenger |

Largest US pressing plant, Nashville-based |

|

MPO International |

MPO |

Challenger |

European pressing leader, France-based |

|

Edel SE & Co. KGaA |

Optimal Media GmbH |

Challenger |

Germany-based, premium audiophile pressings |

|

Quality Record Pressings |

Quality Record Pressings |

Challenger |

Audiophile-grade pressings, Acoustic Sounds |

|

Furnace Record Pressing |

Furnace Record Pressing |

Emerging |

Boutique US pressing, indie label focus |

|

Third Man Pressing |

Third Man Pressing |

Emerging |

Jack White-owned, Nashville and Detroit plants |

The vinyl record market's competitive landscape is moderately fragmented, with major label catalogue owners, large-scale pressing plants, and boutique audiophile manufacturers competing across distinct value pools. Leading players differentiate through catalogue rights, pressing capacity, premium pressing capability, and direct-to-consumer infrastructure. Sony, Universal, and Warner together control over 65% of the global recorded music catalogue feeding into vinyl reissues.

Strategic acquisitions and partnerships are reshaping the landscape. In 2024, Universal Music Group expanded its vinyl-first release strategy across 80+ artists. GZ Media added a new pressing line in 2024, increasing capacity by 12%. Third Man Pressing opened a Detroit plant in 2023, bringing US-based audiophile pressing to a new tier. Independent pressers are also forming consortiums to compete on capacity with major plants.

Key Company Profiles

Sony Music Entertainment

Sony Music Entertainment is one of the world's largest music companies, headquartered in New York. Owned by Sony Group Corporation, the company generated over USD 10 Billion in recorded music revenues in FY 2024. Sony's Legacy Recordings division manages one of the deepest catalogues of vinyl reissues globally, spanning Bob Dylan, Miles Davis, Bruce Springsteen, and Beyoncé.

- Product Portfolio: Sony offers vinyl pressings across Legacy Recordings (catalogue reissues), Columbia Records (current artist releases), and RCA Records (pop, hip-hop, K-pop). Premium audiophile editions are released through partnerships with Mobile Fidelity Sound Lab and Analogue Productions. Sony also operates regional pressing partnerships across Japan, Europe, and the United States.

- Recent Developments: In 2026, Sony Music Entertainment announced a $25 million investment in expanding its vinyl manufacturing capacity in 2024, reinforcing its commitment to meet sustained global demand for physical music formats and reduce supply bottlenecks in vinyl production.

- Strategic Focus: Sony's strategy centers on monetizing its catalogue through premium audiophile reissues, expanding K-pop vinyl distribution, and growing direct-to-consumer artist stores while maintaining wholesale partnerships with global retailers.

Universal Music Group

Universal Music Group (UMG) is the largest music company globally, headquartered in Hilversum, Netherlands. UMG generated over EUR 11.8 Billion in recorded music revenues in FY 2024, with vinyl representing approximately 11% of physical music revenue. Its UMe (Universal Music Enterprises) division leads vinyl-first reissue strategy across 80+ heritage artists.

- Product Portfolio: UMG's vinyl portfolio spans Verve Records (jazz), Decca (classical), Interscope (pop and hip-hop), Capitol Records, Republic Records, and Island Records. Premium pressings are released through UMe's Heritage Series. Vinyl-first artist contracts now cover Taylor Swift, Olivia Rodrigo, Drake, and Billie Eilish.

- Recent Developments: In 2025, Universal Music India signed a vinyl licensing and distribution partnership with Blisstainment, enabling wider release of its catalogue on premium vinyl formats.

- Strategic Focus: UMG focuses on vertical integration across pressing, packaging, and distribution while accelerating audiophile-grade reissues and exclusive limited variants for top-tier global artists.

Warner Music Group

Warner Music Group is the third-largest major label globally, headquartered in New York. Warner generated USD 1.3 Billion in recorded music revenues in FY 2024. Its Rhino Entertainment division anchors the company's reissue and catalogue vinyl business with iconic releases from Led Zeppelin, Fleetwood Mac, and Prince.

- Product Portfolio: Warner releases vinyl across Rhino Entertainment (reissues), Atlantic Records, Warner Records, and Parlophone. The Rhino High Fidelity Series offers half-speed mastered audiophile pressings at premium price points. Warner also operates strategic partnerships with Third Man Pressing for US-based premium runs.

- Recent Developments: Warner Music India signed an exclusive global distribution agreement with Ultra Music India, taking over distribution of a catalogue of over 14,000 tracks and future releases, expanding its global reach and monetization capabilities.

- Strategic Focus: Warner's strategy targets premium audiophile reissues, regional K-pop and J-pop expansion, and selective DTC vinyl partnerships with high-margin artists in the indie and rock categories.

Market Concentration Analysis

The global vinyl record market exhibits moderate fragmentation. The top five players spanning major labels and large pressing plants - Sony Music Entertainment, Universal Music Group, Warner Music Group, GZ Media, United Record Pressing - collectively account for an estimated 40-45% of global vinyl revenue in 2025. The remaining market is distributed across MPO International, Optimal Media, Quality Record Pressings, Furnace Record Pressing, Third Man Pressing, and a long tail of regional pressers and indie label brands.

The market is bifurcated into two distinct competitive tiers. At the catalogue-and-distribution tier, the three major labels dominate revenue capture through ownership of premium reissue rights and DTC partnerships. At the pressing-and-manufacturing tier, GZ Media holds dominant capacity, while specialized boutique pressers compete on audiophile quality, custom variants, and turnaround speed.

Consolidation is accelerating at the pressing tier. Universal Music Group acquired controlling interests in two boutique plants in 2024, while major labels are increasingly forming long-term capacity agreements with leading pressers to lock in supply. This consolidation trend is expected to intensify between 2026 and 2030 as global demand outpaces capacity, creating winner-take-most dynamics in scale-dependent pressing operations.

Investment & Growth Opportunities

Fastest-Growing Segments

Single Vinyl Records remain the highest-volume product sub-segment with continued growth, supported by artist-led short-run drops. Colored Vinyl is the fastest-growing type at an estimated 7.5% CAGR through 2034, driven by visual collectibility and premium pricing. Sustainable bio-based vinyl is projected to expand at 12-15% CAGR, reflecting environmental regulation and consumer preference shifts.

Emerging Market Expansion

India, China, Brazil, and Southeast Asia represent significant untapped vinyl market opportunities. India alone saw vinyl sales grow over 60% between 2022 and 2024, albeit from a small base. Online platforms such as Amazon, Discogs, and regional e-commerce players are unlocking previously inaccessible collector demographics, with cross-border shipping further enabling international participation.

Venture and Strategic Investment Trends

Vinyl-economy startups and platforms attracted approximately USD 350 Million in investment between 2022 and 2025. Notable investments include Discogs' marketplace expansion, Vinyl Me Please's subscription service growth, and direct investment in pressing plant capacity.

Future Market Outlook (2026-2034)

The vinyl record market forecast projects steady value expansion from USD 2.07 Billion in 2025 to USD 3.64 Billion by 2034 at a CAGR of 6.48%. An intermediate milestone of USD 2.83 Billion by 2030 reflects the market's mid-period acceleration driven by Gen Z adoption, expanded pressing capacity, and growing K-pop and J-pop vinyl exports.

Technological disruptions shaping the market through 2034 include: bio-based and PVC-free vinyl pressings driven by EU and California plastics regulation; smart and NFC-enabled sleeves bridging analog and digital experiences; and AI-driven mastering and audio restoration technologies enabling new tiers of high-fidelity reissues. These shifts will redefine product premiumization and unit economics across the value chain.

Vinyl's growing role as a culturally significant lifestyle product positions the format for compounding structural advantages in the recorded music economy through 2034. The convergence of generational nostalgia, artist-led release strategies, sustainable manufacturing, and direct-to-consumer commerce collectively support a positive long-term vinyl record market outlook.

Research Methodology

Primary Research

Primary research forms the qualitative and validation backbone of this report. IMARC Group's analysts conducted structured interviews with vinyl pressing plant executives, A&R managers at major labels, indie record store owners, vinyl distribution heads, and audiophile retailers. Primary inputs were used to validate market size, segment growth projections, competitive positioning, and emerging trend identification.

Secondary Research

Secondary research drew upon authoritative sources including: Recording Industry Association of America (RIAA) annual revenue reports; British Phonographic Industry (BPI) data; IFPI Global Music Reports; Nielsen Music and Luminate sales tracking; Discogs market data; Bandcamp annual artist payout reports; and company annual reports, investor presentations, and press releases for profiled competitors.

Forecasting Models

Market forecasts were developed using bottom-up and top-down estimation approaches. Bottom-up modeling aggregated revenue data across product, type, and regional segments. Top-down validation cross-referenced global recorded music industry growth rates, consumer disposable income indices, and discretionary entertainment spending. The 6.48% CAGR was derived through triangulation across multiple data sources and scenario analysis.

Vinyl Record Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | LP/EP Vinyl Records, Single Vinyl Records |

| Features Covered | Colored, Gatefold, Picture |

| Genders Covered | Men, Women |

| Age Groups Covered | 13-17, 18-25, 26-35, 36-50, Above 50 |

| Applications Covered | Private, Commercial |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Independent Retailers, Online Stores, Others |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Sony Music Entertainment, Universal Music Group, Warner Music Group, GZ Media, United Record Pressing, MPO International, Edel SE & Co. KGaA, Quality Record Pressings, Furnace Record Pressing, Third Man Pressing, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the vinyl record market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global vinyl record market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the vinyl record industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Vinyl Record Market Report

The global vinyl record market was valued at USD 2.07 Billion in 2025 and is projected to reach USD 3.64 Billion by 2034, growing at a CAGR of 6.48% during 2026-2034.

The market is forecast to expand at a CAGR of 6.48% from 2026 to 2034, driven by collector demand, Gen Z adoption, artist-led exclusive drops, and ongoing analog format revival.

Single Vinyl Record lead with 58.6% market share in 2025, followed by LP/EP Vinyl Record at 41.4%, reflecting strong artist-driven short-run releases and viral chart hits.

Colored Vinyl leads with 44.2% share in 2025, followed by Gatefold at 31.6% and Picture discs at 24.2%, driven by visual collectibility and premium pricing dynamics.

Asia Pacific leads with 33.9% market share in 2025, anchored by Japan's audiophile base, South Korea's K-pop vinyl ecosystem, and Australia's indie scene strength.

Asia Pacific is also the fastest-growing region, expanding at an estimated 7.4% CAGR through 2034, fuelled by K-pop, J-pop, and rising e-commerce penetration.

Key drivers include vintage cultural revival, artist-led exclusive drops, premium audiophile demand, and the resurgence of independent record stores generating USD 80+ Million on Record Store Day.

Key players include Sony Music Entertainment, Universal Music Group, Warner Music Group, GZ Media, United Record Pressing, MPO International, Edel SE & Co. KGaA, Quality Record Pressings, Furnace Record Pressing, Third Man Pressing.

The vinyl record market is forecast to reach USD 2.83 Billion by 2030, representing a key intermediate milestone supported by capacity expansion and Gen Z collector growth.

Independent record stores generated over USD 80 Million in single-day sales on Record Store Day 2024 alone, with 1,500+ stores worldwide acting as anchor points for niche releases.

Roughly 50% of new vinyl buyers in 2024 were aged 18-34, signalling a generational shift driven by social-media-led discovery, TikTok trends, and aesthetic-driven music collecting.

Key opportunities include sustainable bio-based vinyl, smart NFC-enabled sleeves, K-pop and J-pop reissue programs, direct-to-consumer artist platforms, and emerging market expansion in India and Brazil.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)