Vision Care Market Size, Share, Trends and Forecast by Type, Distribution Channel, and Region, 2026-2034

Global Vision Care Market Size, Share, Trends & Forecast (2026-2034)

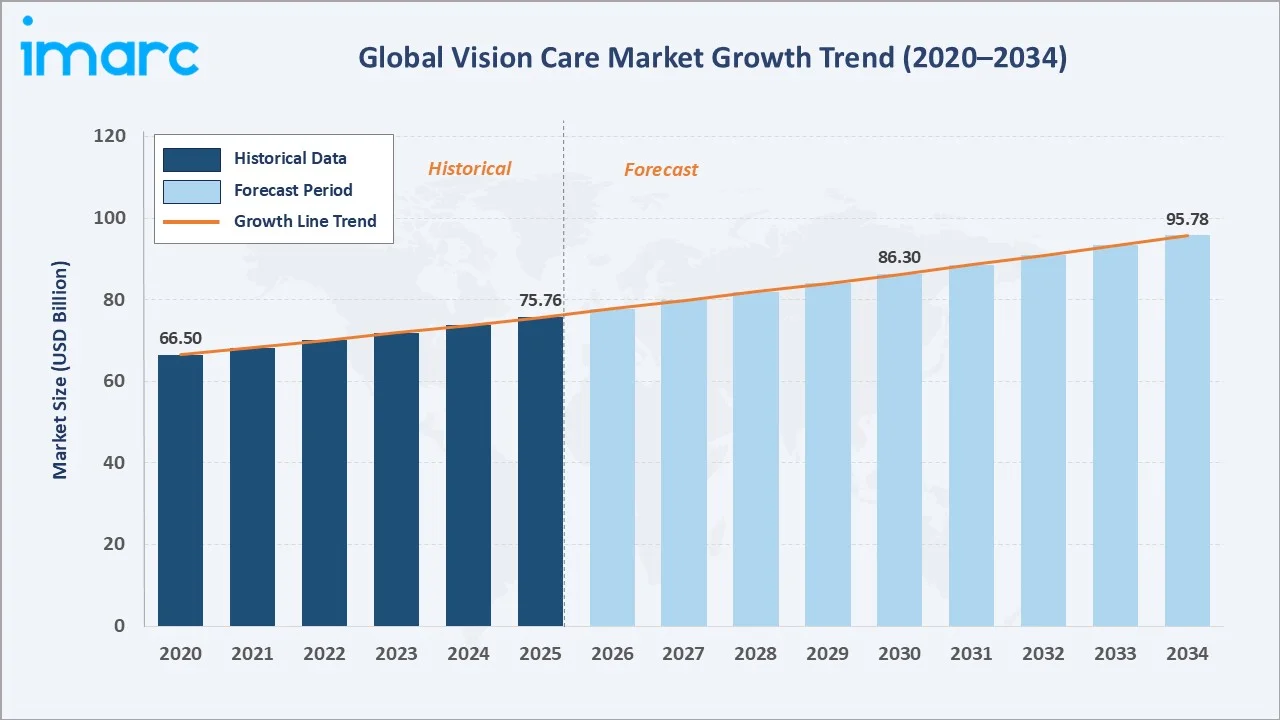

The global vision care market size reached USD 75.76 Billion in 2025 and is projected to reach USD 95.78 Billion by 2034, exhibiting a CAGR of 2.64% during 2026-2034. Rising prevalence of refractive errors, aging populations, digital eye strain, and expanding access to corrective eye care globally drive sustained market growth.

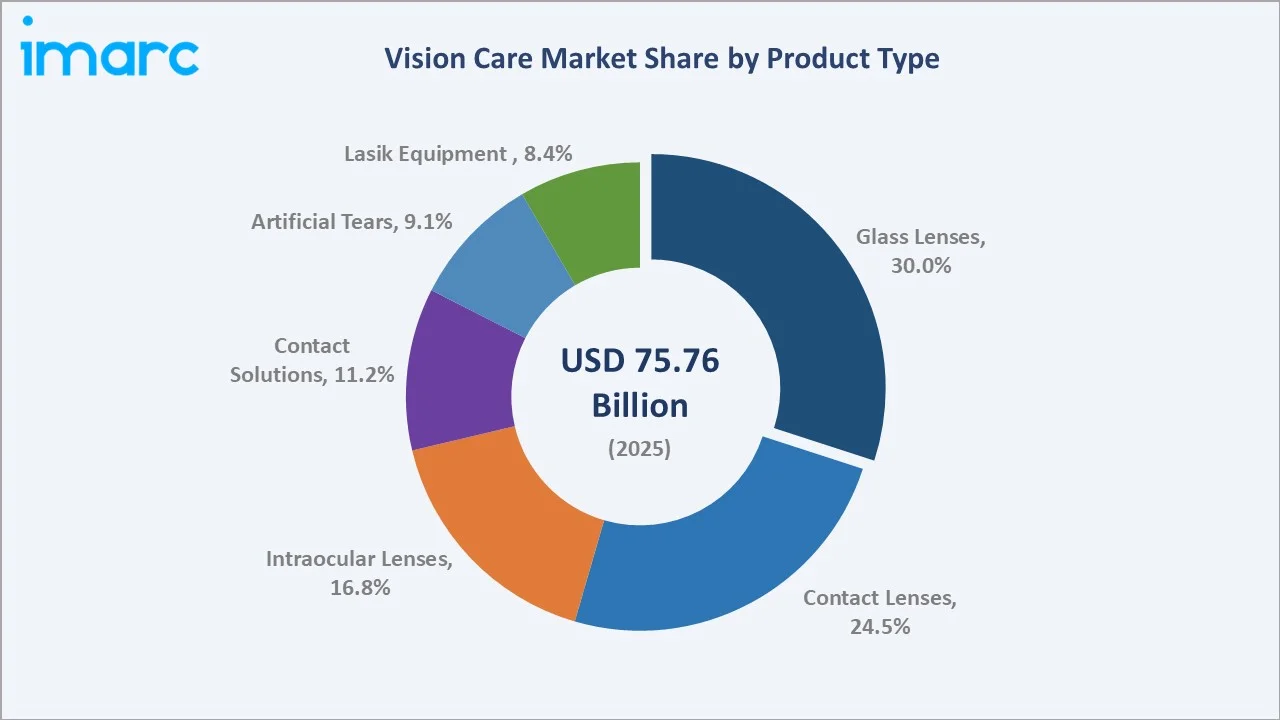

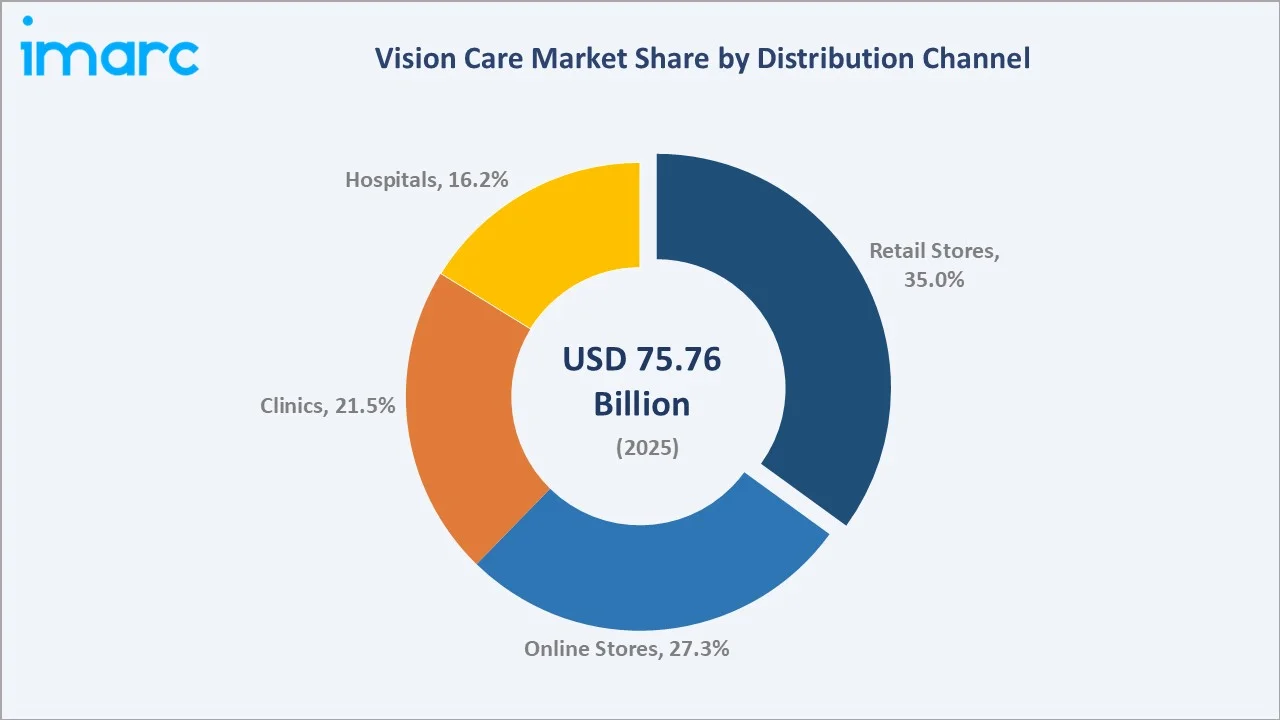

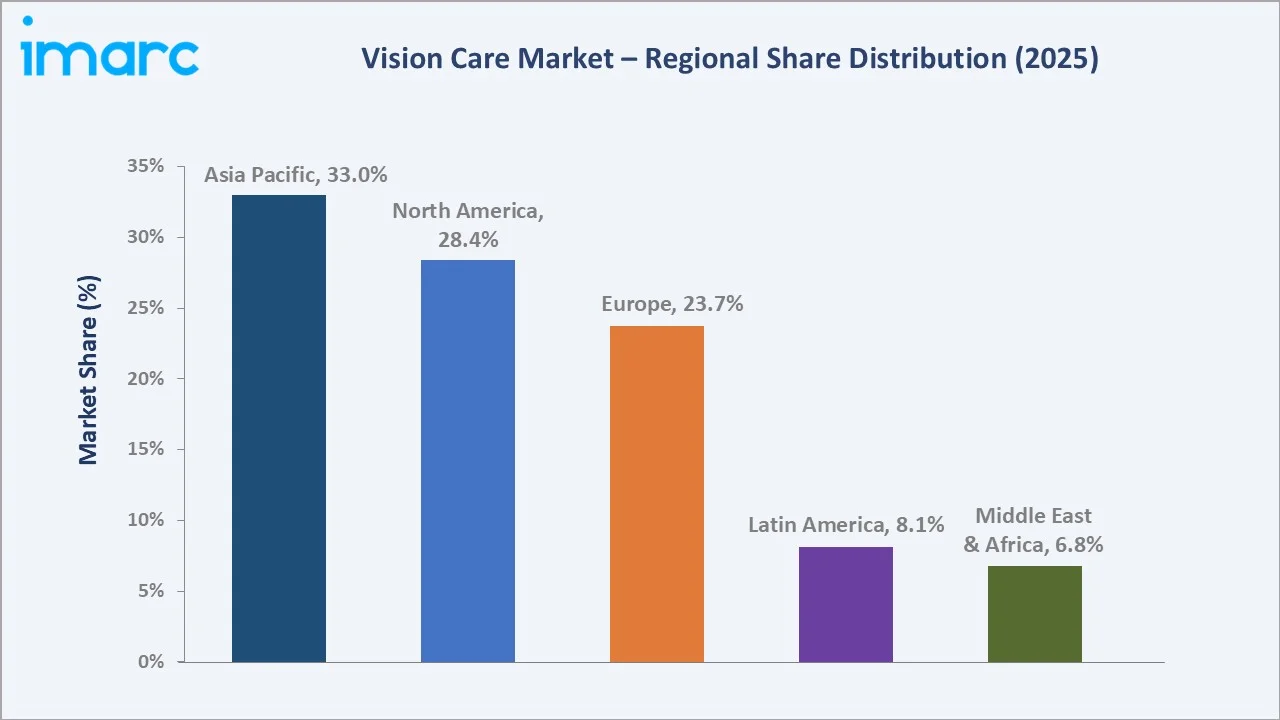

Glass Lenses dominate the product type mix at 30.0% in 2025, while Retail Stores lead distribution at 35.0%. Asia Pacific commands a dominant 33.0% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 75.76 Billion |

|

Forecast Market Size (2034) |

USD 95.78 Billion |

|

CAGR (2026-2034) |

2.64% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (33.0% share, 2025) |

|

Second Largest Region |

North America (28.4% share, 2025) |

|

Leading Product Type |

Glass Lenses (30.0%, 2025) |

|

Leading Distribution Channel |

Retail Stores (35.0%, 2025) |

The global vision care market trajectory from 2020 through 2034, with historical expansion to USD 75.76 Billion in 2025, reflects consistent demand for corrective eyewear and ophthalmic solutions. The forecast to USD 95.78 Billion captures premium contact lens adoption, intraocular lens procedure growth, and dry eye treatment expansion.

To get more information on this market, Request Sample

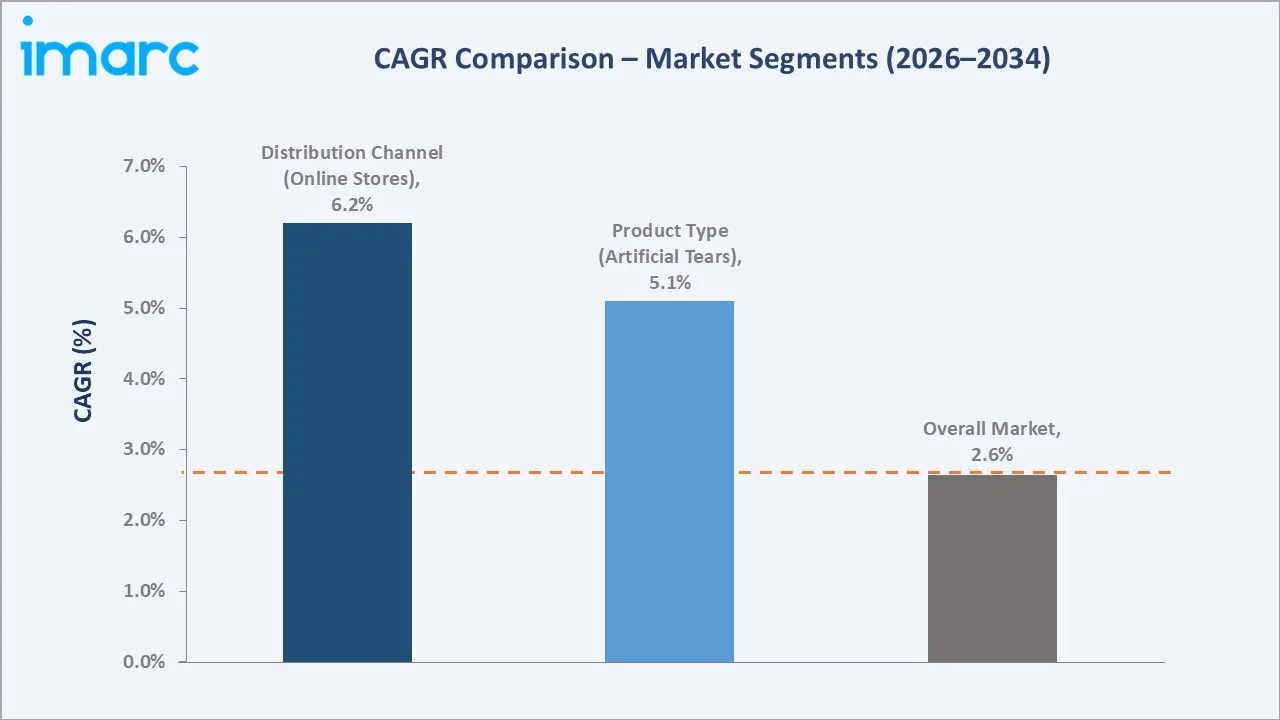

The CAGR trajectories across key product type and distribution channel sub-segments, with Artificial Tears at ~5.1% CAGR and Online Stores at ~6.2% CAGR, represent the fastest-growing categories within the global vision care industry analysis through 2034.

Executive Summary

The global vision care market is on a sustained growth trajectory from USD 75.76 Billion in 2025 to USD 95.78 Billion by 2034. Vision care encompasses corrective lenses, contact solutions, intraocular implants, artificial tears, and refractive surgery equipment serving a rapidly expanding visually impaired and aging global population.

Glass Lenses lead product type at 30.0% in 2025, driven by widespread prescription eyewear globally. Contact Lenses at 24.5% reflect specialty lens adoption. Retail Stores dominate distribution at 35.0%, while Online Stores at 27.3% reflect accelerating digital commerce penetration in optical retail channels across all major markets.

Asia Pacific dominates at 33.0% in 2025, reflecting the world's largest concentrations of myopia-affected populations in China, Japan, South Korea, and India. North America at 28.4% reflects premium product adoption, high surgical volume, and elevated per-capita ophthalmic expenditure across the United States and Canada.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Glass Lenses – 30.0% share (2025) |

|

Leading Distribution Channel |

Retail Stores – 35.0% share (2025) |

|

Leading Region |

Asia Pacific – 33.0% share (2025) |

|

Second Largest Region |

North America – 28.4% share (2025) |

|

Top Companies |

Alcon Inc., Bausch Health Companies Inc., CooperVision, EssilorLuxottica, HOYA Corporation, Johnson & Johnson |

Key Analytical Observations Expanding on the Above Data:

- Glass Lenses: Glass Lenses' 30.0% share reflects the enduring dominance of prescription spectacle lenses as the most accessible vision correction modality globally, supported by established optical retail networks and high optometrist prescription rates worldwide.

- Retail Stores: Retail Stores' 35.0% share reflects the critical role of brick-and-mortar optical chains in dispensing prescription eyewear with fitting and adjustment services that online channels cannot fully replicate, sustaining higher average transaction values consistently.

- Asia Pacific: Asia Pacific's 33.0% dominance reflects the world's highest Myopia prevalence rates concentrated in East and Southeast Asia, supported by rapidly expanding private optical retail chains, growing middle-class income, and increasing cataract surgery volume.

- Online Stores: Online Stores' 27.3% share captures the accelerating shift toward direct-to-consumer optical sales, subscription contact lens platforms, and value-driven eyewear brands leveraging digital channels to undercut traditional retail price points globally.

Global Vision Care Market Overview

Vision care encompasses the full spectrum of products and services addressing vision correction, protection, and enhancement. The ecosystem spans prescription optical lenses, contact lenses and solutions, intraocular implants for cataract and refractive surgery, artificial tears for dry eye management, and laser vision correction platforms globally.

The global vision care ecosystem benefits from growing awareness of preventive eye health, expanding ophthalmic healthcare infrastructure in emerging economies, technological innovation in premium intraocular and specialty contact lenses, and rising incidence of dry eye disease linked to digital device usage and environmental factors across global populations.

Market Dynamics

To evaluate market opportunities, Request Sample

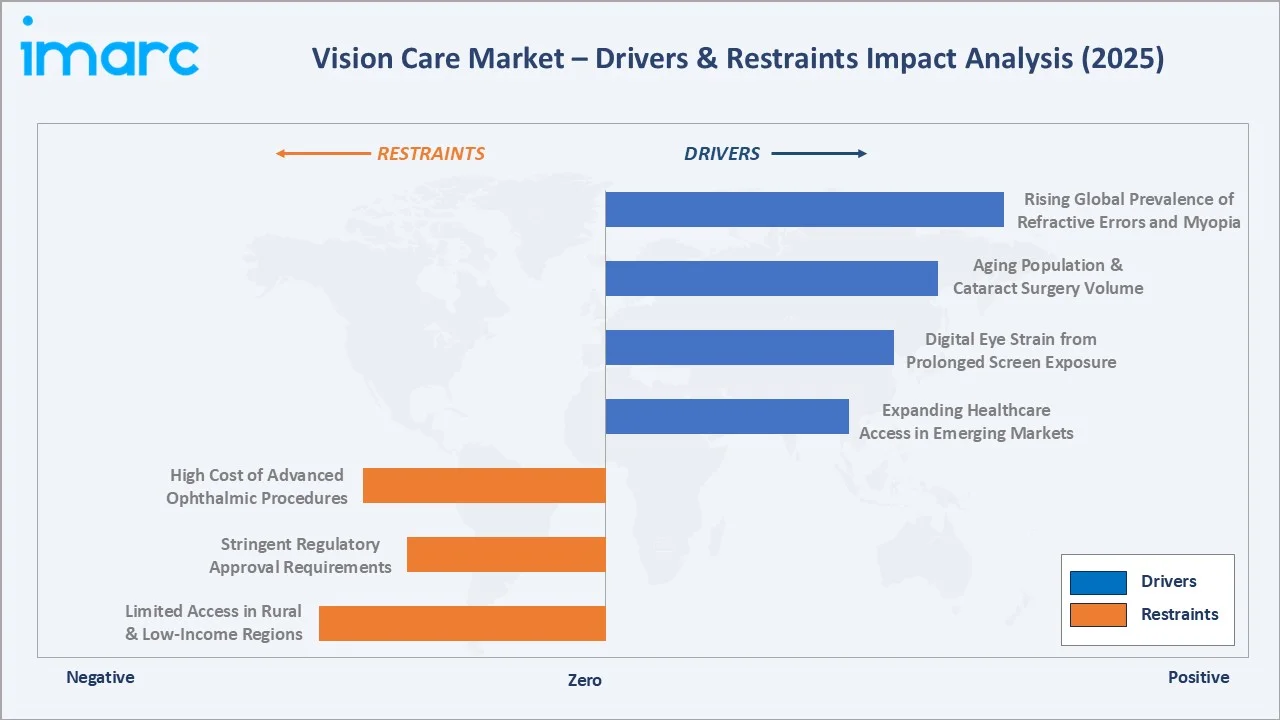

Market Drivers

- Rising Global Prevalence of Refractive Errors and Myopia: Myopia prevalence is accelerating globally, with an estimated 2.5 billion people affected by 2025. Increasing screen time, reduced outdoor activity, and urbanisation are primary structural drivers, sustaining demand for corrective eyewear, specialty myopia-control lenses, and refractive surgery procedures across all age groups globally.

- Aging Population and Increasing Cataract Surgery Volume: Populations aged 65 and above are the fastest-growing demographic globally, directly increasing cataract surgery volumes and intraocular lens demand. Premium IOL adoption is rising as patients increasingly select presbyopia-correcting and extended depth-of-focus lenses for superior post-surgical visual outcomes and spectacle independence.

- Digital Eye Strain from Prolonged Screen Exposure: Average screen time exceeding seven hours per day globally is driving a rapid increase in digital eye strain, dry eye disease, and demand for blue-light filtering lenses and preservative-free artificial tear formulations, creating sustained incremental revenue across optical lens, contact lens, and OTC ophthalmic solution categories.

- Expanding Healthcare Access in Emerging Markets: Expanding health infrastructure in Asia Pacific, Latin America, and the Middle East is bringing corrective eye care to previously underserved populations. Government vision screening programs, increasing optometrist density, and optical retail chain expansion are primary mechanisms unlocking this substantial unmet demand globally.

Market Restraints

- High Cost of Advanced Ophthalmic Procedures and Devices: Premium IOLs, LASIK procedures, and advanced contact lens categories carry significant out-of-pocket costs often excluded from standard health insurance plans, limiting adoption rates in middle-income markets and among cost-sensitive demographic segments representing large addressable but currently underserved global populations.

- Stringent Regulatory Approval Requirements: Medical devices, contact lenses, and prescription ophthalmic pharmaceuticals require regulatory approval from bodies including the FDA, EMA, and national health ministries, imposing significant development timelines and compliance burdens that delay market entry and constrain smaller competitors in global markets.

- Limited Access to Eye Care in Rural and Low-Income Regions: Despite growing global demand, significant rural and low-income populations remain without adequate access to licensed optometrists, optical dispensaries, or affordable corrective products, limiting market penetration in sub-Saharan Africa, rural Asia, and parts of Latin America where vision care infrastructure remains substantially underdeveloped.

Market Opportunities

- Premium and Specialty Contact Lens Innovation for Myopia Control: Orthokeratology, myopia-control spectacle lenses, and low-dose atropine formulations represent a rapidly emerging premium segment targeting the global pediatric myopia epidemic, commanding significant price premiums and recurring revenue through ongoing prescription management and regular lens replacement cycles across major markets.

- Expanding Optical Retail and Surgical Markets in Emerging Economies: Emerging economies in Southeast Asia, India, and Latin America represent high-growth opportunities as expanding middle classes invest in branded eyewear, premium contact lenses, and refractive surgery, supported by increasing urban optometry infrastructure and growing consumer awareness of advanced vision correction options globally.

Market Challenges

- Counterfeit and Low-Quality Optical Products in Emerging Markets: The proliferation of counterfeit spectacle lenses, unbranded contact lenses, and imitation ophthalmic solutions through informal online channels in emerging markets poses risks to consumer safety and undermines pricing power for legitimate manufacturers competing on quality and clinical validation standards globally.

- Intensifying Competition from Digital-First Optical Retail Channels: The rapid growth of direct-to-consumer online optical retail, subscription contact lens platforms, and prescription eyewear e-commerce intensifies pricing competition, compresses margins in traditional optical retail, and accelerates consolidation pressure on independent opticians lacking adequate digital commerce capabilities.

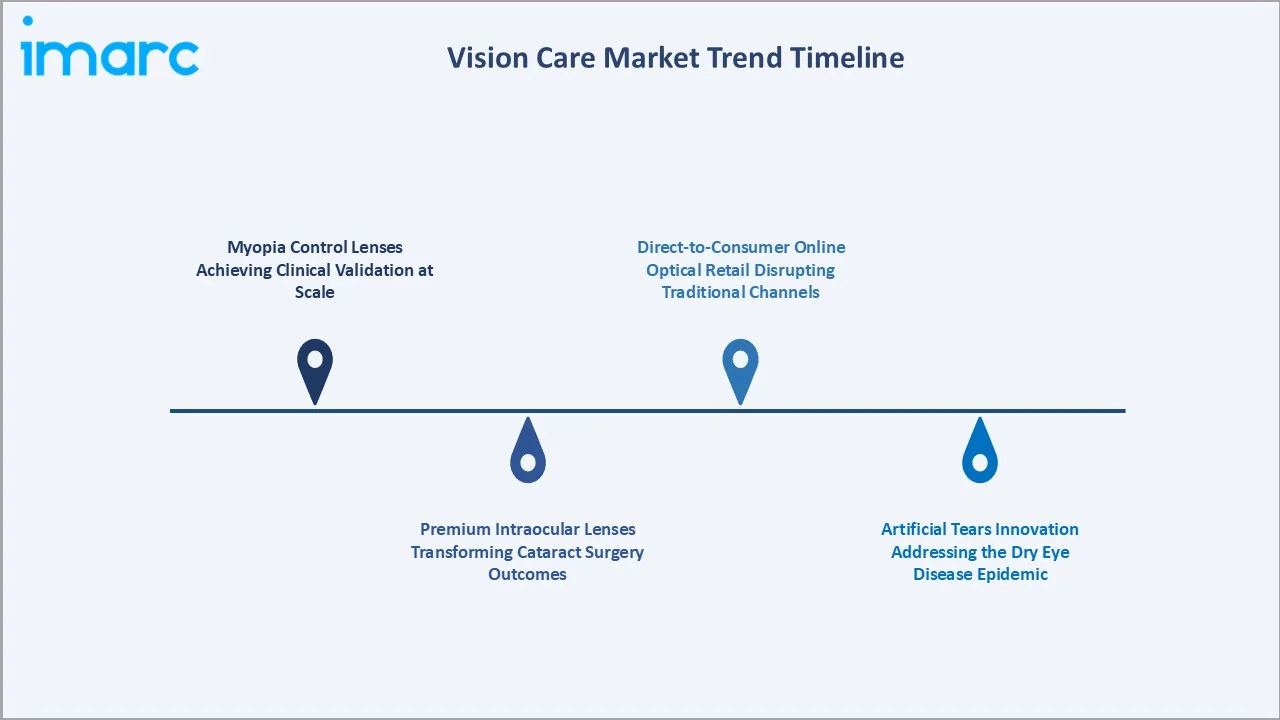

Emerging Market Trends

1. Myopia Control Lenses Achieving Clinical Validation at Scale

Spectacle lenses incorporating myopia-control technology, including defocus-incorporated multiple segments and peripheral defocus designs, have achieved regulatory approval and clinical deployment across major Asian and European markets by 2025, establishing myopia management as a defined clinical category within the global vision care industry.

2. Premium Intraocular Lenses Transforming Cataract Surgery Outcomes

Extended depth-of-focus and trifocal IOL adoption is accelerating as aging populations increasingly opt for premium surgical outcomes, enabling spectacle independence post-cataract surgery. Leading manufacturers, including Alcon, Johnson & Johnson Vision Care, and ZEISS Vision, are driving premium IOL portfolio expansion globally across major surgical markets.

3. Direct-to-Consumer Online Optical Retail Disrupting Traditional Channels

Online optical platforms offering prescription eyewear, subscription contact lens delivery, and virtual try-on technologies are capturing significant market share from traditional optical retailers globally, accelerating adoption of digital dispensing tools and remote optometry consultation platforms across all major vision care markets.

4. Artificial Tears Innovation Addressing the Dry Eye Disease Epidemic

Dry eye disease, affecting an estimated 344 million people globally, is driving significant pharmaceutical and OTC innovation in preservative-free artificial tear formulations, lipid-based tear supplements, and prescription dry eye therapies, creating one of the fastest-growing segments within the global vision care market through 2034.

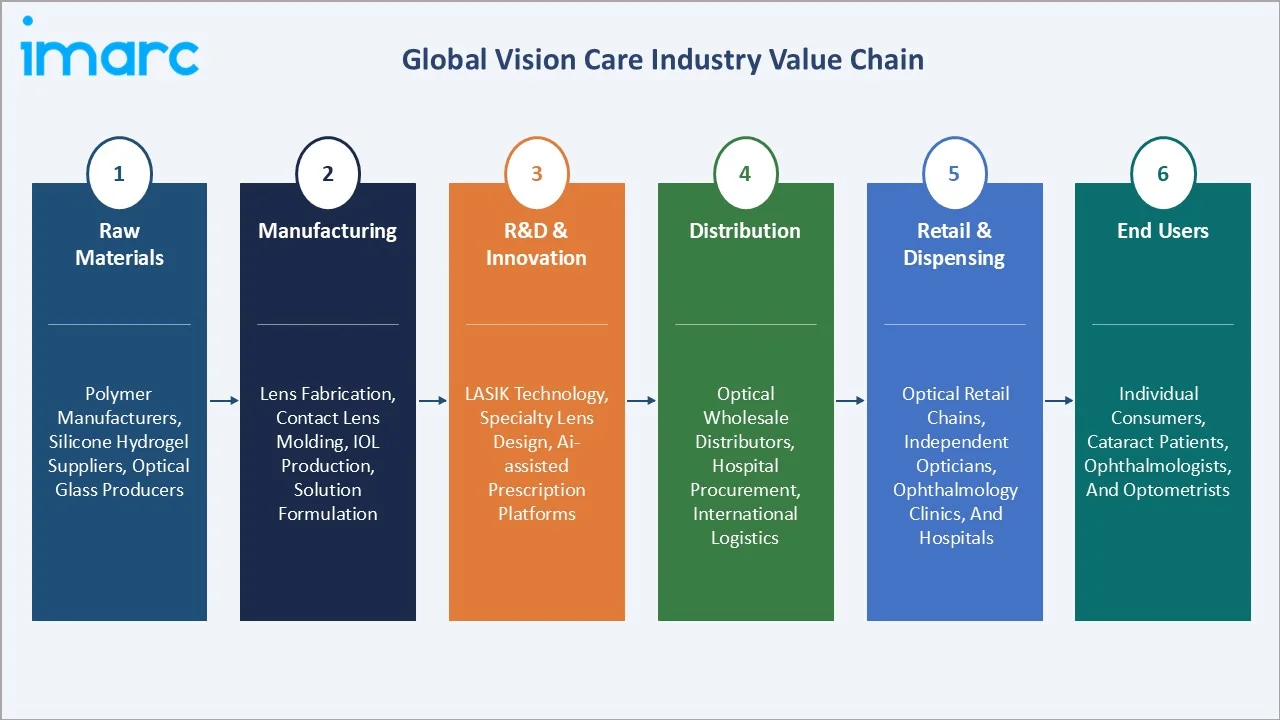

Industry Value Chain Analysis

The global vision care value chain spans six stages from raw material production through end-user delivery. R&D and product innovation capture the highest value-add margins, while commodity optical lens manufacturing faces increasing cost pressure from lower-cost manufacturers competing on standardised product quality across global markets.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Polymer manufacturers, silicone hydrogel suppliers, optical glass producers |

|

Manufacturing |

Lens fabrication, contact lens molding, IOL production, solution formulation |

|

R&D & Innovation |

LASIK technology, specialty lens design, and AI-assisted prescription platforms |

|

Distribution |

Optical wholesale distributors, hospital procurement, and international logistics |

|

Retail & Dispensing |

Optical retail chains, independent opticians, ophthalmology clinics, and hospitals |

|

End Users |

Individual consumers, cataract patients, ophthalmologists, and optometrists |

Technology Landscape in the Global Vision Care Industry

Advanced Silicone Hydrogel Contact Lens Materials

Silicone hydrogel materials now dominate premium contact lens manufacturing, delivering superior oxygen permeability, extended wear capability, and improved comfort over conventional hydrogel materials. Continuous R&D investment by CooperVision, Alcon, and Johnson & Johnson Vision Care is yielding next-generation surface treatment technologies globally.

AI-Assisted Ophthalmic Diagnostics and Prescription Technology

Artificial intelligence platforms for diabetic retinopathy screening, glaucoma detection, and automated refraction are achieving regulatory clearance and commercial deployment globally. AI-assisted optometry platforms are extending diagnostic access in resource-limited settings and enabling large-scale population screening programs across Asia and Africa.

Femtosecond Laser and Premium IOL Technology in Refractive Surgery

Femtosecond laser-assisted cataract surgery platforms from ZEISS Vision, Alcon, and Johnson & Johnson enable unprecedented surgical precision in lens fragmentation and capsulotomy, optimising outcomes for premium IOL placement. LASIK equipment advances are delivering improved visual acuity outcomes and expanding the eligible patient population globally.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Glass Lenses |

30.0% |

2025 |

|

Distribution Channel |

Retail Stores |

35.0% |

2025 |

|

Region |

Asia Pacific |

33.0% |

2025 |

By Product Type

Glass Lenses command a 30.0% majority share in 2025, driven by the widespread use of prescription spectacle lenses as the primary vision correction modality globally. Progressive and anti-reflective coated lenses dominate premium segments, while volume growth is sustained by high replacement frequency across all income levels and geographies.

To access detailed market analysis, Request Sample

Contact Lenses at 24.5% reflect growing adoption of daily disposable, specialty toric, and multifocal designs. Intraocular Lenses at 16.8% are driven by rising cataract surgery volumes. Contact Solutions at 11.2% and Artificial Tears at 9.1% serve essential maintenance and therapeutic roles, while Lasik Equipment at 8.4% reflects sustained refractive surgery demand.

By Distribution Channel

Retail Stores dominate distribution at 35.0% in 2025, anchored by large optical chains, franchise opticians, and mass merchandise optical departments providing fitting, adjustment, and eye examination services, sustaining higher average transaction values for premium prescription eyewear and contact lens categories across all major markets.

Online Stores at 27.3% are the fastest-growing channel, reflecting subscription contact lens platforms and digital eyewear brands gaining consumer trust. Clinics at 21.5% capture ophthalmology and optometry practice dispensing, while Hospitals at 16.2% primarily serve surgical IOL supply and therapeutic ophthalmic solution procurement needs.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

33.0% |

High myopia prevalence, growing middle class, expanding optical retail |

|

North America |

28.4% |

Premium product adoption, high IOL surgical volumes, and insurance coverage |

|

Europe |

23.7% |

Aging population, premium eyewear culture, established optical networks |

|

Latin America |

8.1% |

Growing optometry access, rising income, and urban optical expansion |

|

Middle East & Africa |

6.8% |

Rising eye care awareness, growing private hospitals, and youth demographics |

Asia Pacific's 33.0% market dominance in 2025 is driven by the extraordinary concentration of myopia-affected populations across China, Japan, South Korea, Taiwan, and Singapore, where myopia prevalence among young adults approaches 80-90%, creating the world's greatest captive demand for corrective lenses, specialty contact lenses, and refractive surgery.

North America's 28.4% share reflects the dominance of premium optical products, high cataract and LASIK surgical volumes, comprehensive vision insurance coverage, and the presence of major vision care manufacturers, including Alcon and Johnson & Johnson Vision Care, headquartered and commercially concentrated in the United States.

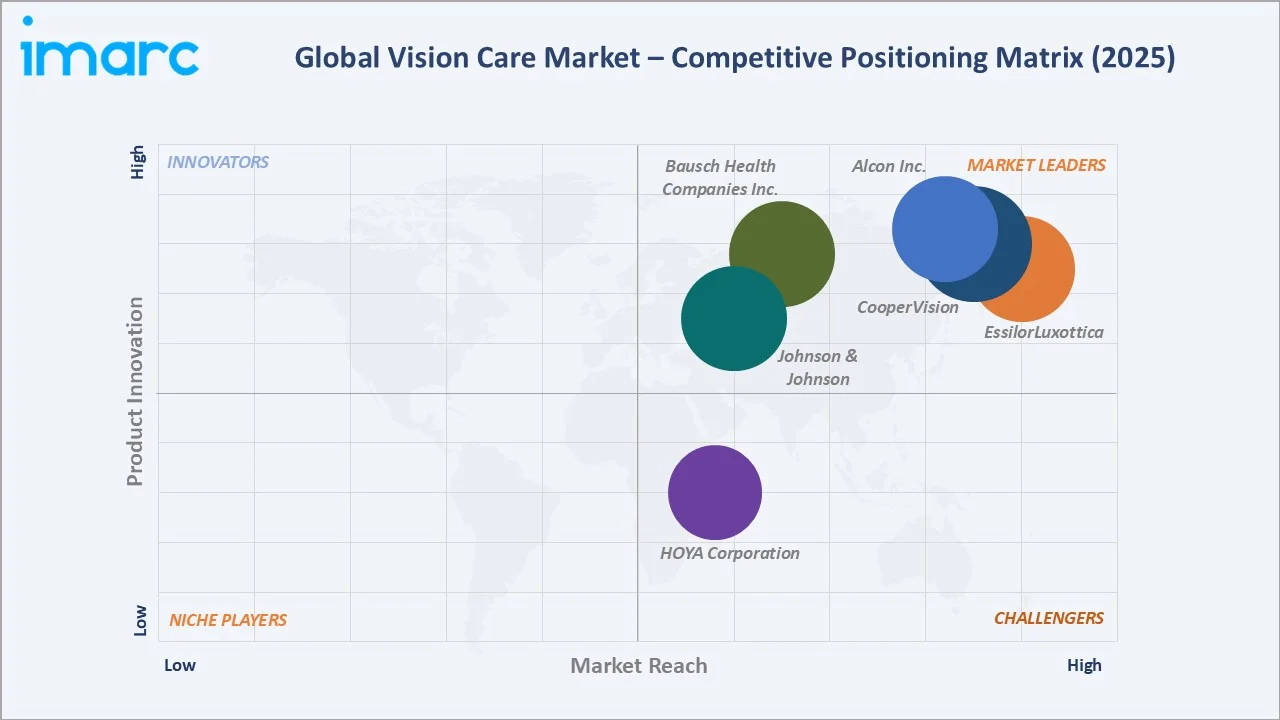

Competitive Landscape

The global vision care market is moderately concentrated, with a handful of multinational corporations commanding significant market shares across multiple product categories, while mid-tier specialists maintain strong segment-level positions.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Alcon Inc. |

Intraocular Lenses (IOLs), Eye Drops, UNITY Cataract System, UNITY Vitreoretinal Cataract System, Hydrus Microstent, Contact Lenses |

Leader |

Premium contact lenses, IOLs, and surgical equipment; global ophthalmology leadership |

|

Bausch Health Companies Inc. |

Contact lenses, lens care products, eye care products, ophthalmic pharmaceuticals, over-the-counter products, and ophthalmic surgical devices and instruments |

Leader |

Operates via Bausch + Lomb Corporation; Contact lens and ophthalmic pharmaceutical diversification; OTC eye health expansion |

|

CooperVision |

Biofinity, Avaira, clariti, MyDay, MiSight, and Proclear |

Leader |

Specialty contact lenses; myopia control leadership with regulatory approvals globally |

|

EssilorLuxottica |

Varilux, Crizal, Transitions, Ray-Ban |

Leader |

Integrated ophthalmic lens and premium eyewear brand dominance across all channels |

|

HOYA Corporation |

Eyeglass Lenses, Contact Lenses, Intraocular Lenses |

Challenger |

Precision ophthalmic lenses; progressive lens innovation; IoT healthcare integration |

|

Johnson & Johnson |

ACUVUE OASYS, ACUVUE MOIST, TECNIS IOL |

Leader |

Premium daily disposable market leadership; TECNIS IOL surgical platform expansion |

Key players include Alcon Inc., Bausch Health Companies Inc., CooperVision, EssilorLuxottica, HOYA Corporation, and Johnson & Johnson, among others.

Key Company Profiles

Alcon Inc.

Alcon is the world's leading eye care company, operating across surgical and vision care segments with a comprehensive portfolio spanning contact lenses, intraocular lenses, ophthalmic pharmaceuticals, and advanced refractive surgery systems.

- Product Portfolio: Intraocular Lenses (IOLs), Eye Drops, UNITY Cataract System, UNITY Vitreoretinal Cataract System, Hydrus Microstent, Contact Lenses

- Recent Developments: In February 2025, Alcon launched a new over-the-counter eye drop in the US called SYSTANE PRO Preservative-Free (PF), expanding its dry eye care portfolio. The new formulation combines hyaluronate, nano-sized lipids, and HP-Guar technology to provide extended relief from burning and irritation caused by dry eyes.

- Strategic Focus: Alcon's strategy centres on premium segment leadership across surgical ophthalmology and consumer vision care, leveraging its dual-segment scale to cross-sell through shared ophthalmic professional relationships while expanding accessible IOL markets globally.

EssilorLuxottica

EssilorLuxottica is the global leader in ophthalmic lenses and eyewear, formed through the 2018 merger of Essilor and Luxottica. The company combines world-leading ophthalmic lens manufacturing with iconic eyewear brands and an extensive global retail and optical laboratory network.

- Product Portfolio: Varilux, Crizal, Transitions, Ray-Ban Vision

- Recent Developments: In April 2026, EssilorLuxottica acquired Italian technology company Faro, strengthening its capabilities in high-precision eyewear manufacturing. Faro specializes in computer numerical control (CNC) machinery used for milling and diamond cutting in the eyewear and jewelry industries. The acquisition is expected to enhance EssilorLuxottica’s vertically integrated production model by adding advanced engineering and manufacturing expertise to its operations.

- Strategic Focus: EssilorLuxottica's strategy focuses on vertical integration across lens manufacturing, brand ownership, and retail distribution, capturing higher margins at every stage of the vision care value chain globally through end-to-end control of key commercial touchpoints.

Johnson & Johnson

Johnson & Johnson Vision Care is the global leader in premium contact lenses, marketing the world's best-selling contact lens brand ACUVUE. Operating as a division of Johnson & Johnson MedTech, the company combines contact lens leadership with a growing surgical ophthalmology portfolio centred on the TECNIS IOL platform globally.

- Product Portfolio: ACUVUE OASYS, ACUVUE MOIST, TECNIS IOL

- Recent Developments: In March 2026, Johnson & Johnson Vision received U.S. FDA approval for its TECNIS PureSee intraocular lens (IOL), a new extended depth of focus (EDOF) lens designed for cataract surgery patients. TECNIS PureSee is the first FDA-approved EDOF intraocular lens in the U.S. that does not carry a warning related to loss of contrast sensitivity.

- Strategic Focus: Johnson & Johnson Vision Care's strategy leverages ACUVUE's dominant brand equity in the premium daily disposable segment to sustain pricing power while expanding into myopia management, surgical ophthalmology, and digital eye health to diversify revenue streams.

Market Concentration Analysis

The global vision care market exhibits moderate-to-high concentration in key product categories. Ophthalmic lens manufacturing is dominated by EssilorLuxottica globally, while the premium contact lens segment is led by Johnson & Johnson Vision Care, Alcon, and CooperVision. IOL and refractive surgery equipment categories are similarly concentrated.

Strategic consolidation is ongoing as leading players pursue vertical integration across manufacturing, distribution, and retail, while mid-tier companies differentiate through specialty product innovation in myopia control, premium IOL, and digital eye health categories to avoid direct commodity competition with established market share leaders.

Investment & Growth Opportunities

Fastest-Growing Segments

Artificial Tears at ~5.1% CAGR through 2034 represent the highest-growth product type segment, driven by escalating dry eye disease prevalence linked to digital screen exposure, aging demographics, and pharmaceutical innovation in preservative-free and lipid-based tear formulations achieving premium price points across global markets.

Emerging Segments

Online Stores at ~6.2% CAGR through 2034 represent the fastest-growing distribution channel, capturing accelerating direct-to-consumer optical sales, subscription contact lens platforms, and digital eyewear brands leveraging AI-assisted virtual try-on and remote optometry to convert traditional retail customers to online purchasing globally.

Investment Trends

Private equity and strategic investment in vision care is concentrated in digital optometry platforms, myopia control technology companies, and AI-assisted diagnostic tools. Government-backed population myopia management programs across East Asian markets are creating additional non-dilutive capital flows supporting sector innovation.

Future Market Outlook (2026-2034)

The global vision care market is forecast to expand from USD 75.76 Billion in 2025 to USD 95.78 Billion by 2034 at a CAGR of 2.64%, adding USD 20.02 Billion in incremental annual market value over the forecast period. Steady growth reflects the essential, non-discretionary nature of vision correction for a rapidly expanding global population.

Three structural forces will most significantly shape the global vision care landscape through 2034. Myopia management products will achieve mainstream clinical adoption, premium IOL penetration will rise significantly with aging populations, and digital channels will fundamentally reshape optical retail economics and distribution structures globally.

Research Methodology

Primary Research

Primary research encompassed structured interviews with global vision care industry stakeholders, including senior executives at leading lens and equipment manufacturers, ophthalmologists and optometrists, optical retail chain operators, health insurance executives, and venture capital investors specialising in ophthalmic technology.

Secondary Research

Key secondary sources include the World Health Organisation World Report on Vision, International Agency for the Prevention of Blindness data, Brien Holden Vision Institute myopia prevalence studies, national health ministry ophthalmic expenditure reports, company annual reports, regulatory device approval databases, and ophthalmic trade publications.

Forecasting Models

Market size estimations were derived using combined top-down and bottom-up forecasting models incorporating global healthcare expenditure trends, surgical procedure volume growth rates, lens replacement frequency assumptions, myopia prevalence trajectories, and pricing trend analysis across major market segments and geographies worldwide.

Vision Care Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Glass Lenses, Contact Lenses, Intraocular Lenses, Contact Solutions, LASIK Equipment, Artificial Tears |

| Distributions Channels Covered | Retail Stores, Online Stores, Clinics, Hospitals |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Companies Covered | Alcon Inc., Bausch Health Companies Inc., CooperVision, EssilorLuxottica, HOYA Corporation, Johnson & Johnson, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the vision care market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global vision care market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the vision care industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Vision Care Market Report

The global vision care market size reached USD 75.76 Billion in 2025 and is projected to reach USD 95.78 Billion by 2034, exhibiting a CAGR of 2.64% during 2026-2034.

Glass Lenses lead the product type segment with a 30.0% share in 2025, driven by the widespread use of prescription spectacle lenses as the most accessible primary vision correction modality across all global markets and demographic groups.

Online Stores exhibit the highest projected CAGR of ~6.2% through 2034, driven by subscription contact lens delivery platforms, direct-to-consumer prescription eyewear brands, and digital-first optical retailers disrupting traditional brick-and-mortar channels.

Asia Pacific dominates with a 33.0% share in 2025, reflecting the world's highest myopia prevalence concentrated in East and Southeast Asia, a large growing middle class investing in quality vision correction, and rapidly expanding ophthalmic healthcare infrastructure.

Key players include Alcon Inc., Bausch Health Companies Inc., CooperVision, EssilorLuxottica, HOYA Corporation, Johnson & Johnson, and others.

The global vision care market is projected to reach USD 95.78 Billion by 2034, growing from USD 75.76 Billion in 2025 at a steady CAGR of 2.64% over the 2026-2034 forecast period, driven by aging demographics, myopia prevalence, and premium product adoption.

Key growth drivers include the rising global prevalence of refractive errors and myopia, aging population driving cataract surgery and IOL demand, digital eye strain increasing artificial tear and blue-light lens demand, and expanding healthcare access across emerging economies in Asia Pacific, Latin America, and the Middle East.

The global vision care market grew from USD 66.50 Billion in 2020 to USD 75.76 Billion in 2025, reflecting a consistent historical growth trajectory driven by steady demand for corrective eyewear, rising cataract procedure volumes, and growing adoption of specialty contact lenses and dry eye treatment products across global markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)