Warehousing and Storage Market Size, Share, Trends, and Forecast by Type of Warehouses, Ownership, End-Use, and Region, 2026-2034

Global Warehousing and Storage Market Size, Share, Trends & Forecast (2026-2034)

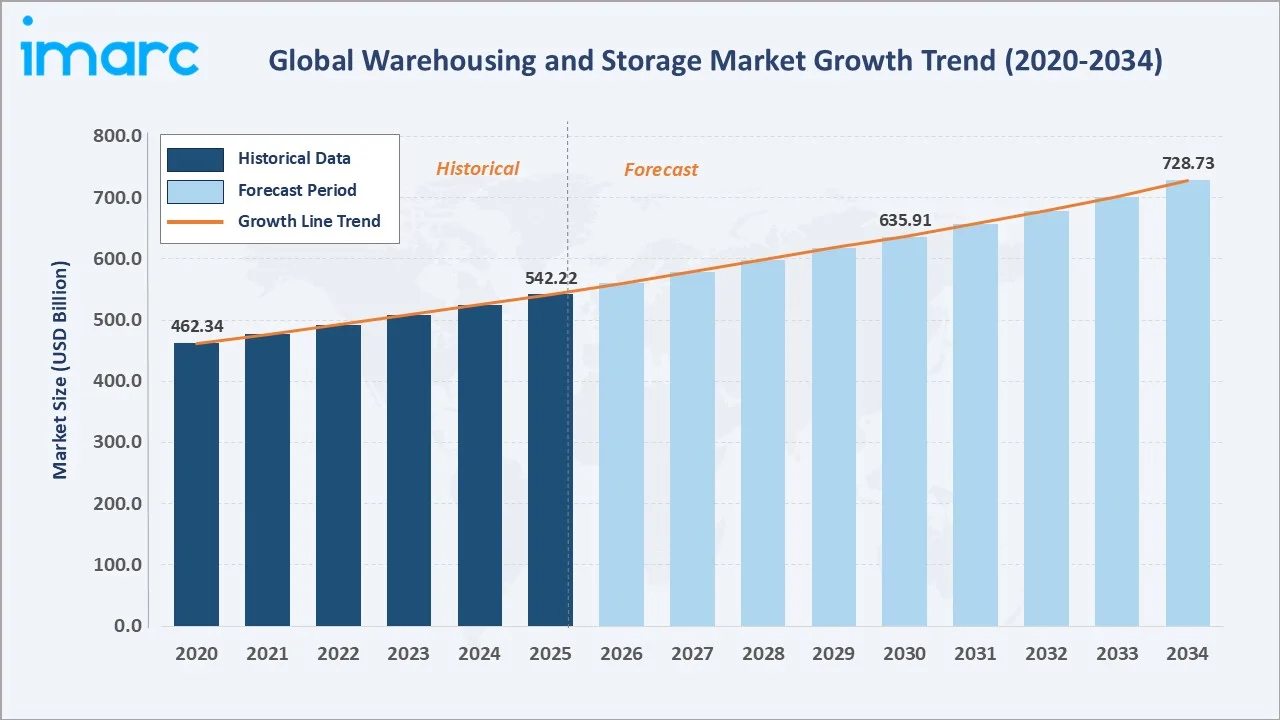

The global warehousing and storage market size was valued at USD 542.2 Billion in 2026-2034 and is projected to reach USD 728.7 Billion by 2034, exhibiting a CAGR of 3.20% during 2026-2034. Rapid e-commerce proliferation, supply chain modernization, and surging third-party logistics (3PL) adoption are the primary catalysts. Asia-Pacific commands dominant market leadership at 54.5% of global revenue in 2025, driven by manufacturing-intensive economies and port-linked logistics corridors. General Warehousing and Storage leads the type-of-warehouse segment at 69.3%, while Private Warehouses hold a 65.4% ownership share – reflecting sustained enterprise investment in captive logistics infrastructure worldwide.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 542.2 Billion |

|

Forecast Market Size (2034) |

USD 728.7 Billion |

|

CAGR (2026-2034) |

3.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (54.5% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Leading Warehouse Type |

General Warehousing & Storage (69.3%, 2025) |

|

Leading Ownership Type |

Private Warehouses (65.4%, 2025) |

The chart below illustrates the global warehousing and storage market growth trajectory from 2020 through 2034, contrasting a steady historical expansion base against a sustained forecast curve powered by e-commerce acceleration, 3PL outsourcing, and automation-driven efficiency improvements.

To get more information on this market, Request Sample

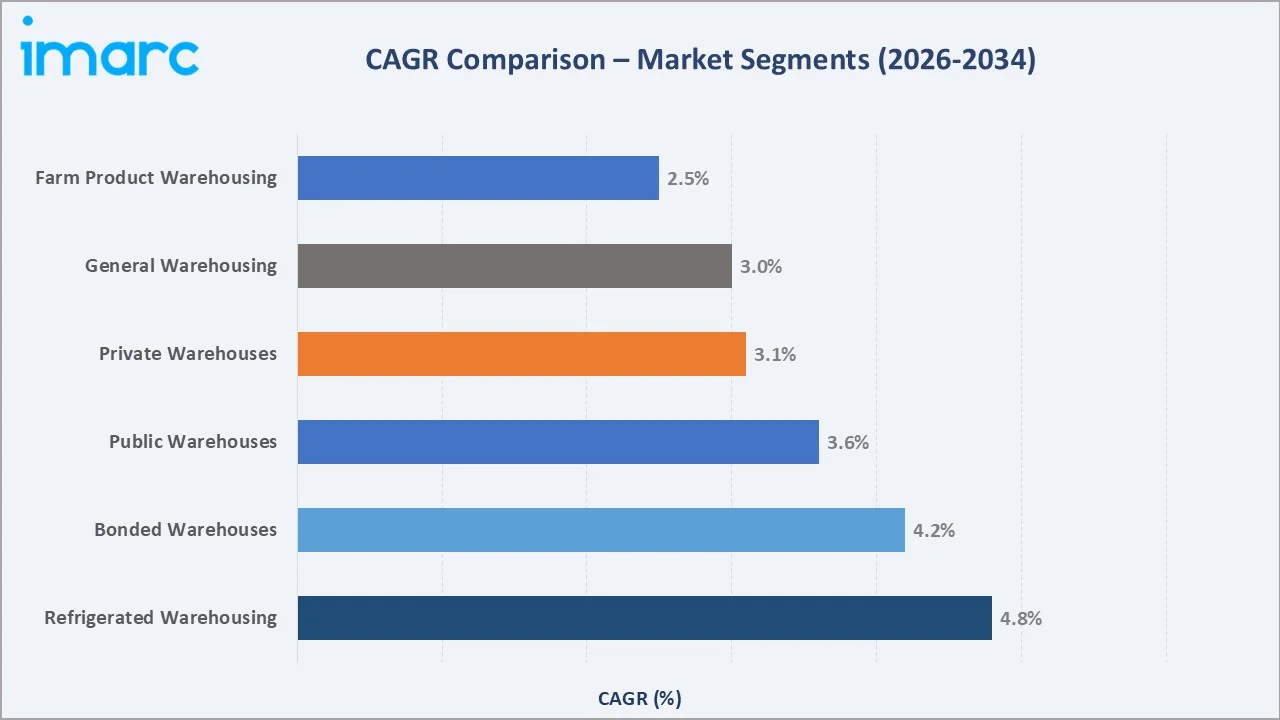

Segment-level CAGR comparisons highlight refrigerated warehousing and bonded warehouses as the fastest-growing sub-categories within the global warehousing and storage industry analysis through 2034.

Executive Summary

The global warehousing and storage market is undergoing structural transformation driven by the convergence of digital commerce, supply chain resilience mandates, and advanced logistics automation. Valued at USD 542.2 Billion in 2025, the market is forecast to reach USD 728.7 Billion by 2034, at a CAGR of 3.20%. The surge in e-commerce – which accounted for over 20% of global retail sales in 2024– continues to generate unprecedented demand for fulfillment centers, last-mile warehouses, and multi-tier distribution hubs, fundamentally reshaping facility design and locational strategy.

General Warehousing and Storage dominates the global warehousing market with a 69.3% share in 2025, driven by its versatility across manufacturing, consumer goods, retail, and IT hardware industries. Refrigerated Warehousing is emerging as the fastest-growing segment, supported by expanding cold-chain demand for pharmaceuticals and perishable foods. Private warehouses hold 65.4% ownership share, reflecting enterprise preference for dedicated facilities, while Bonded Warehouses account for 11.8%, gaining traction as global trade recovery boosts customs-deferred inventory strategies.

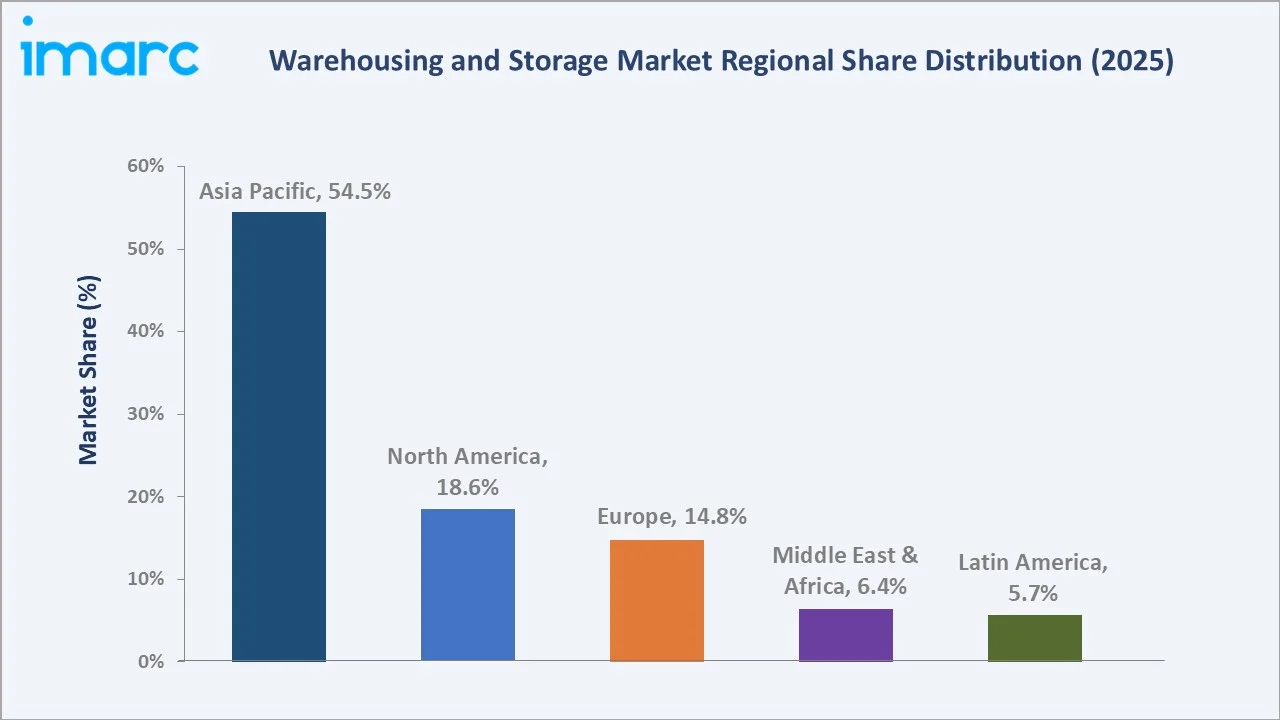

Asia-Pacific leads the global warehousing and storage market with a 54.5% revenue share in 2025, driven by strong manufacturing bases and rapid e-commerce growth across China, India, Japan, and Southeast Asia. North America (18.6%) and Europe (14.8%) remain mature, technology-focused markets emphasizing automation and sustainable warehouses, while Middle East & Africa (6.4%) and Latin America (5.7%) are expanding due to infrastructure investments and rising trade activity.

Key Market Insights

|

Insight |

Data |

|

Largest Warehouse Type |

General Warehousing & Storage – 69.3% share (2025) |

|

Fastest Growing Type |

Refrigerated Warehousing & Storage (~4.8% CAGR, 2026-2034) |

|

Leading Ownership |

Private Warehouses – 65.4% share (2025) |

|

Leading Region |

Asia-Pacific – 54.5% revenue share (2025) |

|

Second Largest Region |

North America – 18.6% revenue share (2025) |

|

Top Companies |

Prologis, GLP, Goodman Group, DHL Supply Chain, XPO Logistics, DB Schenker, Panattoni, Segro |

|

Market Opportunity |

Smart warehousing automation & cold-chain expansion in emerging markets |

Key Analytical Observations Supporting the Above Data:

- General Warehousing & Storage's 69.3% dominance in 2025 reflects its broad end-use applicability across manufacturing, retail, consumer goods, and IT hardware sectors globally.

- Refrigerated Warehousing is the fastest-growing warehouse type at ~4.8% CAGR (2026-2034), fuelled by pharmaceutical cold-chain expansion and e-grocery adoption in Asia-Pacific and North America.

- Private Warehouses lead ownership at 65.4% in 2025, as large enterprises prioritize control over dedicated, automation-upgraded logistics facilities for supply chain resilience.

- Asia-Pacific's 54.5% global dominance reflects China's role as the world's largest manufacturing base – with over USD 4.66 trillion in goods produced annually– alongside India's warehousing capacity expansion under the National Logistics Policy 2022.

- Bonded Warehouses at 11.8% are gaining momentum as cross-border e-commerce volumes grow, enabling customs-deferred inventory management and reducing import duty exposure for global traders.

Global Warehousing and Storage Market Overview

Warehousing and storage refer to facilities offering short- and long-term storage for goods, raw materials, and finished products used by manufacturers, retailers, and logistics providers. The market includes general warehouses, temperature-controlled cold storage, bonded facilities, and agricultural storage. Applications span retail fulfilment, pharmaceutical cold chains, industrial materials, agricultural commodities, and e-commerce distribution, supporting operations across nearly all industries globally.

Macroeconomic drivers include accelerating global trade volumes, urbanization creating demand for proximate urban logistics nodes, and industrial output growth in emerging economies. The global e-commerce market exceeded USD 6.3 trillion in 2024, generating structural demand for warehouse space at an unprecedented scale. Government infrastructure investment programs in India, Southeast Asia, and the Middle East are enabling rapid warehousing capacity expansions across both developed and developing corridors.

Market Dynamics

To evaluate market opportunities, Request Sample

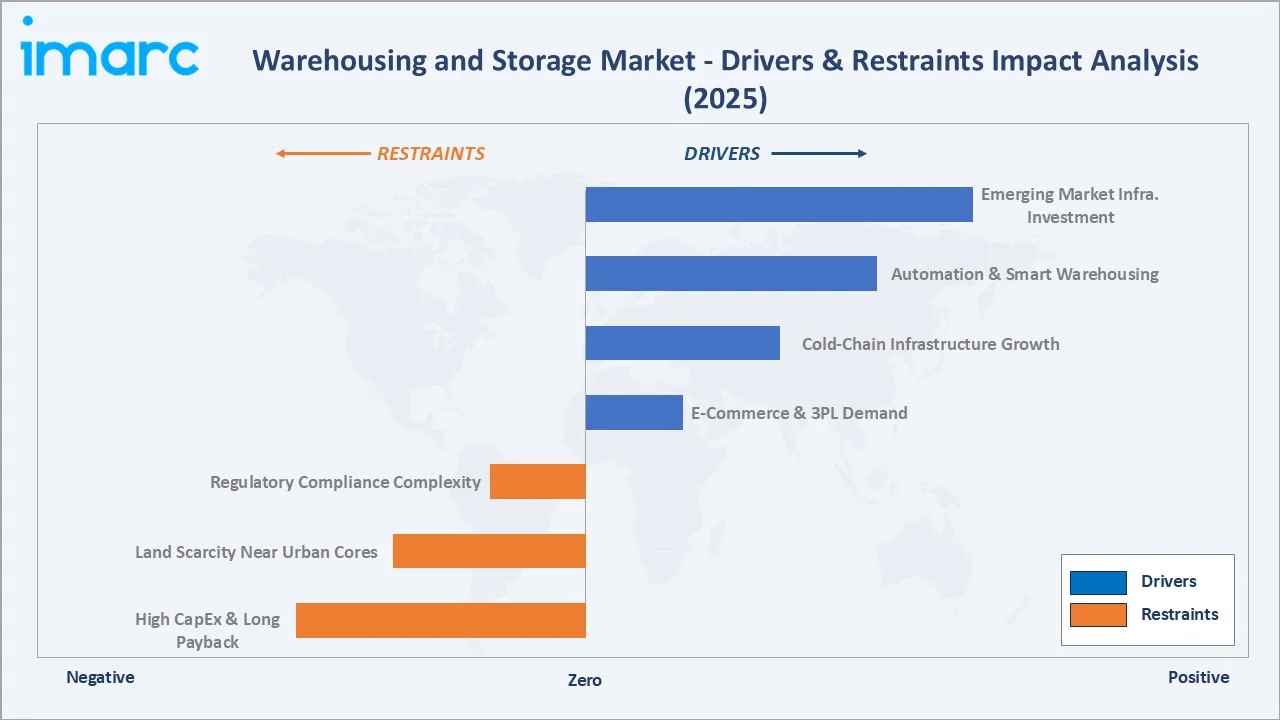

Market Drivers

- E-Commerce Expansion and Fulfillment Infrastructure Demand: Global e-commerce sales exceeded USD 6.3 trillion in 2024, accelerating demand for fulfillment infrastructure. Major players including Amazon, Alibaba, and JD.com collectively operate over 2,000 fulfillment centers globally, supporting same-day and next-day delivery. This has increased development of urban micro-fulfillment centers and large distribution hubs within 30–50 km of major cities, reshaping warehouse location strategies worldwide.

- Third-Party Logistics (3PL) Outsourcing Growth: The global 3PL market reached approximately USD 1.3 trillion in 2024, as companies increasingly outsource warehousing to providers like DHL, XPO Logistics, and DB Schenker. This trend reduces capital expenditure and supports flexible, technology-enabled managed warehousing solutions.

- Cold Storage Infrastructure Expansion: Growing pharmaceutical demand, fresh produce trade, and frozen food consumption are accelerating cold-chain logistics. The global cold chain market is projected to grow at ~7% CAGR through 2030, driving investment in refrigerated warehouses across North America, Europe, and Asia-Pacific.

- Automation and Smart Warehousing Adoption: Automation technologies including AMRs, AS/RS, and AI-based WMS improve throughput by 30–50% in advanced warehouses. Global warehouse automation spending exceeded USD 21.3 billion in 2024, supported by labor shortages and rising operational costs in developed markets.

Market Restraints

- High Capital Expenditure and Long Payback Periods: Modern warehouse construction typically ranges USD 20–70 per sq. ft., while automation investments often achieve 2–5 year payback periods, creating capital barriers for smaller operators despite long-term efficiency and productivity benefits.

- Real Estate and Land Scarcity Near Urban Cores: Prime industrial rents vary across major cities, with London exceeding USD 25 per sq. ft., Los Angeles averaging USD 14–16 per sq. ft., and Tokyo ranging USD 10–15 per sq. ft., driven by supply constraints and logistics demand, compressing operating margins for warehouse operators in key demand zones.

- Regulatory Compliance Complexity: Bonded and cold storage facilities must comply with customs certifications, FDA and HACCP food safety standards, and pharmaceutical GDP regulations, creating operational complexity for operators managing multi-region warehousing networks.

Market Opportunities

- Smart Warehousing and IoT Integration: Integration of IoT sensors, real-time inventory tracking, and AI-powered predictive analytics presents a USD 59.52 billion investment opportunity through 2030, allowing operators to offer premium managed services at 15–25% higher margins.

- Emerging Market Warehousing Capacity Expansion: India's warehousing sector surpasses 549 million sq ft, fueled by manufacturing and e-commerce in 2025, while Southeast Asia, Middle East, and Africa are expected to attract USD 50+ billion logistics infrastructure investments through 2034.

- Green and Sustainable Warehousing: Green warehouse developments can reduce financing costs by 30–50 basis points through ESG funding and green bonds. Sustainable warehouses also command 10–15% rental premiums in North America and Europe due to corporate Scope 3 emission reduction targets.

Market Challenges

- Supply Chain Disruptions and Demand Volatility: Post-pandemic inventory destocking cycles and geopolitical trade disruptions – including Red Sea shipping disruptions in 2024 – create demand volatility that complicates long-term warehouse capacity planning and lease structuring.

- Skilled Labor Shortage: Labor shortages remain a major restraint, with industry reports indicating hundreds of thousands of unfilled logistics and warehousing roles in 2024. This talent gap drives wage inflation and operational bottlenecks, accelerating automation investments across distribution and fulfillment facilities.

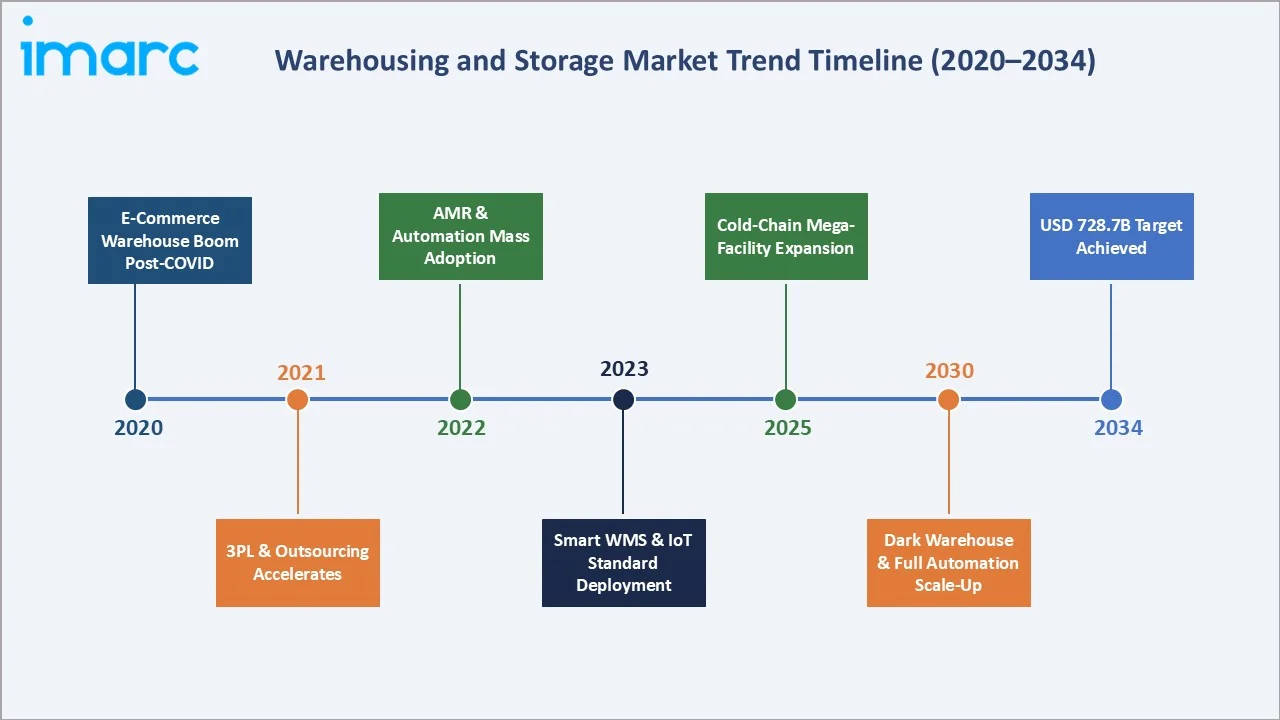

Emerging Market Trends

1. Rise of Micro-Fulfillment Centers for Last-Mile Delivery

Urban micro-fulfillment centers (MFCs) are compact 3,000–10,000 sq. ft. automated facilities, sometimes up to 25,000 sq. ft., located in urban areas to enable faster last-mile delivery. Retailers including Walmart, Target, and Ocado are deploying MFCs to enable 1–2 hour delivery windows. Interact Analysis estimates ~86 micro-fulfillment centers in 2021, projected to reach ~7,300 by 2030, driven by rising e-commerce demand.

2. Automation and Robotics Integration Scaling Rapidly

Amazon operates over 750,000 mobile robots across its global fulfillment network as of 2024 – up from 200,000 in 2020. Collaborative robots, goods-to-person picking systems, and autonomous forklifts are becoming standard in Class-A logistics facilities, compressing order pick times by 40–60%.

3. Cold-Chain Infrastructure as a Strategic Asset Class

The global cold chain industry is projected to reach $393–453B in 2025 and scale to $1.63T by 2035. Pharmaceutical cold-chain requirements – particularly for biologics and mRNA-based medicines – are driving GDP-compliant temperature-controlled facility investment globally.

4. Data-Driven Warehouse Management Systems (WMS)

Cloud-based warehouse management systems integrating AI and analytics are replacing legacy platforms. Modern WMS solutions improve inventory accuracy to 99%+ and can reduce operating and fulfillment costs by 10–30%, compared with manual warehouse processes.

5. Green and Sustainable Warehousing

Prologis – the world's largest logistics REIT with over 1.2 billion sq. ft. of industrial space – committed to net-zero carbon operations by 2040. Solar rooftops, EV charging infrastructure, LED retrofits, and BREEAM/LEED certifications are becoming standard requirements from corporate tenants globally.

Industry Value Chain Analysis

|

Stage |

Key Participants / Examples |

|

Facility Development & Construction |

Panattoni, Prologis, Goodman Group, Segro, ESR Group |

|

Technology & Automation Systems |

Geek+, Locus Robotics, Dematic, KION Group, Swisslog, Knapp |

|

Warehouse Operations & 3PL |

DHL Supply Chain, XPO Logistics, DB Schenker, Segro |

|

Inventory & Distribution Management |

SAP Extended WMS, Oracle Fusion WMS, Manhattan Associates, Blue Yonder |

|

Sales & Delivery Channels |

E-commerce platforms, retail distribution networks, direct-to-consumer channels |

|

End Users |

Manufacturing, Consumer Goods, Retail, Food & Beverage, Healthcare/Pharma, IT Hardware, Chemicals, Agriculture |

Technology Landscape in the Warehousing and Storage Industry

Automation and Robotics

AS/RS, AMRs, and autonomous forklifts are transforming throughput capacity. Facilities deploying AS/RS achieve storage density improvements of 2–3x versus conventional racking, with throughput rates exceeding 1,000 order lines per hour. The global warehouse robotics market exceeded USD 7 billion in 2024.

IoT and Real-Time Monitoring

IoT sensor networks enable real-time temperature monitoring, RFID-based asset tracking, and predictive maintenance, improving warehouse visibility, operational efficiency, and cold-chain management.

Cloud-Based Warehouse Management Systems

Cloud WMS platforms from SAP, Oracle, and Manhattan Associates provide real-time inventory visibility, labor management, and multi-site coordination. Cloud WMS reduces IT infrastructure costs by 30% faster implementation times and 40% lower IT costs compared to on-premises solutions.

Artificial Intelligence and Predictive Analytics

AI-driven demand forecasting, slotting optimization, and labor planning enable 15–20% reductions in inventory carrying costs. Companies such as Gather AI are deploying drone-based inventory scanning powered by computer vision for real-time cycle counts.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type of Warehouses |

General Warehousing and Storage |

69.3% |

2025 |

|

Ownership |

Private Warehouses |

65.4% |

2025 |

|

End-Use |

Manufacturing |

18.2% |

2025 |

|

Region |

Asia Pacific |

54.5% |

2025 |

By Type of Warehouses

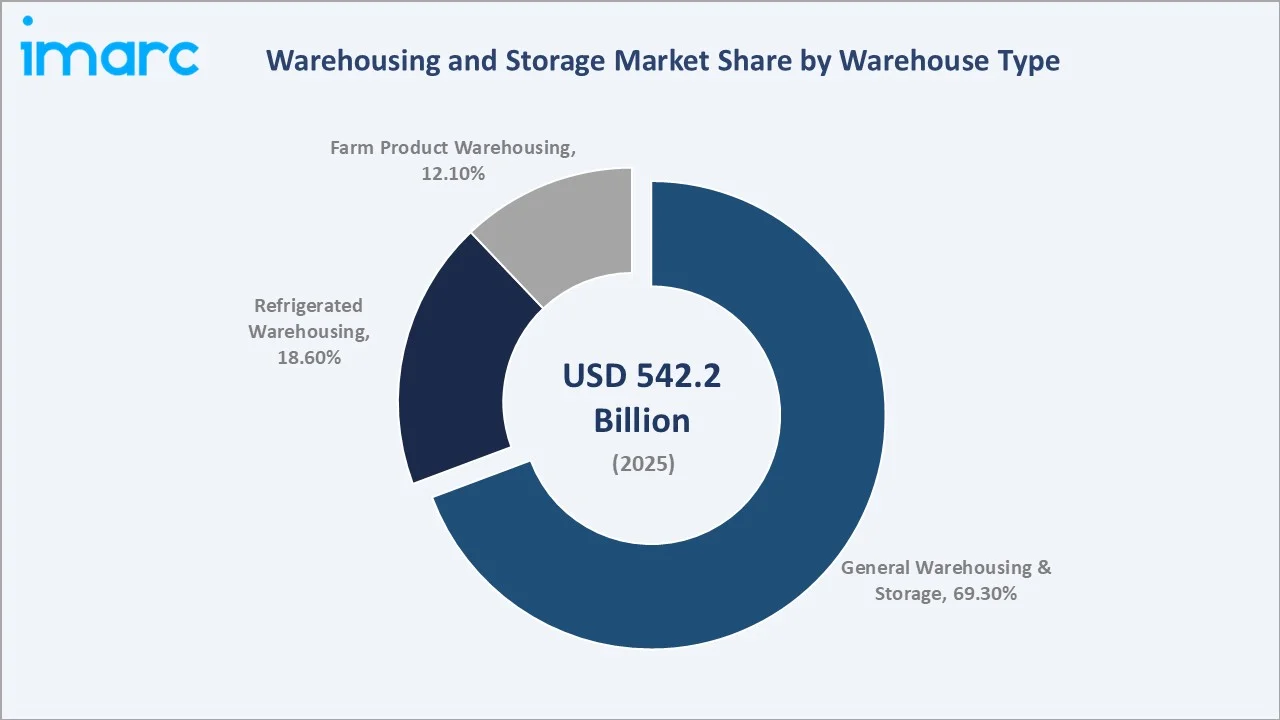

General Warehousing and Storage leads with a 69.3% market share in 2025 driven by broad applicability across manufacturing, consumer goods, retail, IT hardware, and chemicals industries. These facilities serve as the backbone of global supply chains, providing flexible, ambient-temperature storage adaptable to diverse product categories.

To access detailed market analysis, Request Sample

Refrigerated Warehousing and Storage accounts for 18.6% of market value in 2025 and is the fastest-growing segment. Pharmaceutical cold-chain expansion combined with e-grocery adoption is compelling investment in modern refrigerated facilities globally. Farm Product Warehousing and Storage represents 12.1%, serving agricultural commodity storage from grain elevators to controlled-atmosphere fruit storage.

The segmentation chart above reflects the structural dominance of general warehousing, while refrigerated warehousing emerges as the fastest-growing segment – indicative of cold-chain investment as a strategic priority globally.

By Ownership

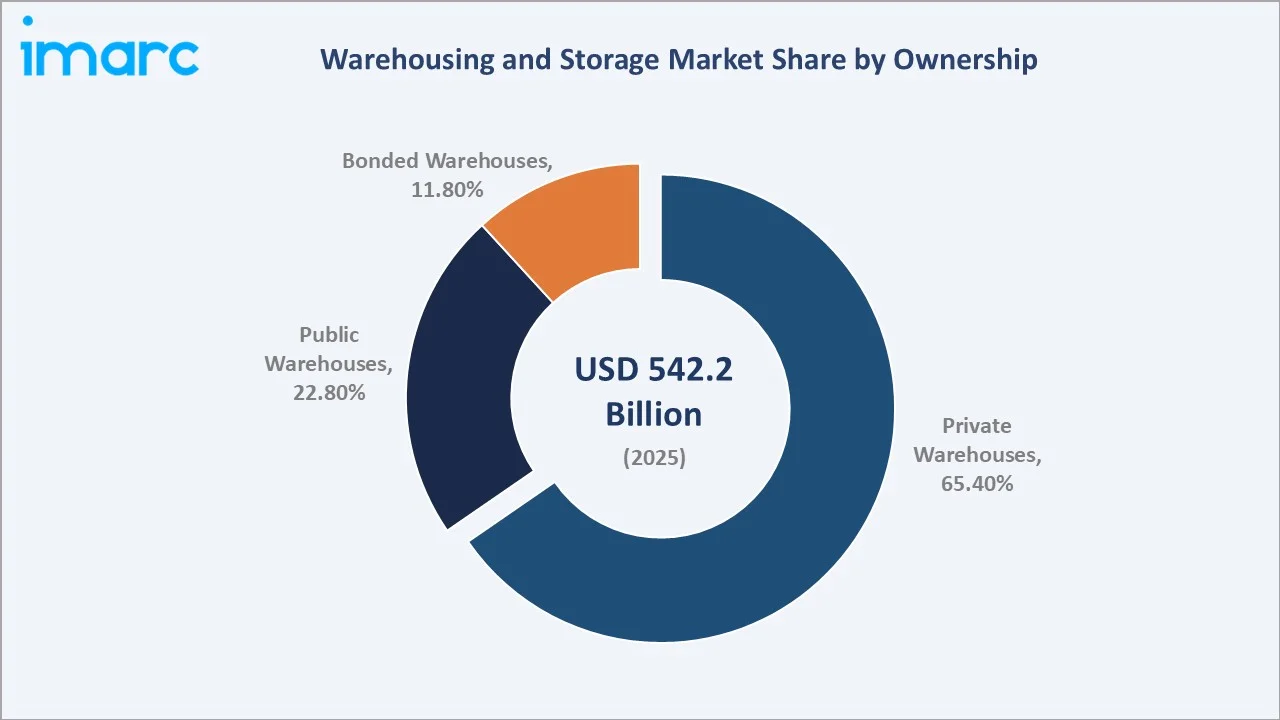

Private Warehouses dominate with a 65.4% share in 2025, reflecting enterprise preference for dedicated facilities offering full operational control and advanced automation integration. Public Warehouses account for 22.8%, providing flexible shared-use storage critical for SMEs and seasonal inventory management. Bonded Warehouses represent 11.8% and are gaining importance as cross-border e-commerce volumes increase.

The ownership segmentation underscores enterprise-driven private warehouse dominance, while growing public and bonded segments reflect the increasing importance of flexible and trade-facilitation storage solutions in the evolving global logistics environment.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers |

Regulatory Context |

Leading Companies |

|

Asia-Pacific |

54.5% |

Manufacturing hub, e-commerce surge, port logistics |

China modernization, India NLP 2022, ASEAN trade |

GLP, ESR, Goodman |

|

North America |

18.6% |

E-commerce fulfillment, 3PL growth, automation |

OSHA standards, DSCSA pharma cold-chain |

Prologis, XPO, DHL |

|

Europe |

14.8% |

Green logistics mandates, nearshoring, cross-border trade |

EU Green Deal, EU customs reform 2028 |

Segro, Prologis, DB Schenker |

|

Middle East & Africa |

6.4% |

Infrastructure development, FTZ expansion |

UAE Vision 2031, Saudi Vision 2030 |

DP World, Agility |

|

Latin America |

5.7% |

Rising e-commerce, agri-commodity storage |

Brazil Mercosur, Mexico nearshoring |

GLP, Panattoni, DHL |

Asia-Pacific holds a dominant 54.5% market share in 2025, driven by China’s large manufacturing base, expanding regional trade, and rapid e-commerce growth across emerging Asian economies. North America accounts for 18.6%, supported by advanced automation, high logistics spending, and mature distribution networks. Europe represents 14.8%, where warehouse development is increasingly shaped by sustainability regulations, energy-efficient facilities, and growing demand for green logistics infrastructure.

Competitive Landscape

|

Company |

Brand / Subsidiary |

Market Position |

Core Strength |

|

Prologis |

Prologis REIT |

Global Leader – 1.2B+ sq. ft. under management (2024) |

Largest industrial REIT operating across 19 countries, specializing in e-commerce logistics parks, last-mile fulfillment, and high-occupancy portfolios, supported by proprietary data analytics to optimize asset and customer performance. |

|

GLP (Global Logistic Properties) |

GLP / GLP Capital Partners |

Asia-Pacific & Americas Leader |

Major logistics real estate platform across China, Japan, Brazil, and the US with over 110M sq. m. assets under management, combining fund management, property development, and digital technology integration through GLP Digital Business Group.. |

|

Goodman Group |

Goodman Logistics |

Industrial REIT Leader – Europe & APAC |

Vertically integrated industrial real estate developer focused on urban infill and high-barrier markets, offering build-to-suit warehousing and ESG-compliant facilities, with strong development margins supported by in-house construction capabilities. |

|

DHL Supply Chain |

DHL / Deutsche Post |

Global 3PL Leader in Managed Warehousing |

Global 3PL leader across 220+ countries, focused on contract logistics, automation, cold chain, and omnichannel fulfillment, supported by Deutsche Post’s extensive logistics network. |

|

XPO Logistics |

XPO |

North America Challenger – Tech-Driven 3PL |

Technology-focused logistics provider offering LTL freight and contract logistics with real-time visibility, predictive analytics, and warehouse automation to enhance operational efficiency. |

|

DB Schenker |

Deutsche Bahn |

Global Challenger – Integrated Contract Logistics |

Deutsche Bahn division offering integrated warehousing and multimodal logistics, with expertise in industry-specific supply chains and sustainable logistics solutions. |

|

Panattoni |

Panattoni Europe / US |

Emerging Leader – Industrial Park Development |

Leading European industrial developer focused on logistics parks and last-mile facilities, with strengths in rapid construction, land bank access, and global tenant partnerships. |

|

Segro |

SEGRO Logistics |

European Leader – Urban & Big-Box Logistics |

UK-listed REIT specializing in urban warehouses and big-box distribution centers across key European markets, with strong focus on last-mile logistics, sustainable facilities, and long-term tenant relationships. |

Key Company Profiles

Prologis, Inc.

Prologis is the world's largest logistics real estate company, owning and operating over 1.2 billion square feet of industrial and logistics facilities across 19 countries as of 2024. The company's portfolio spans Class-A distribution centers, e-commerce fulfillment hubs, and urban logistics facilities. Prologis committed to net-zero carbon operations by 2040, deploying 650+ MW of rooftop solar across its global portfolio. Key customers include Amazon, DHL, Walmart, FedEx, and Home Depot.

GLP (Global Logistic Properties)

GLP is the leading logistics real estate developer in Asia-Pacific, with over 83 million sq. m of logistics and industrial facilities across China, Japan, Vietnam, India, and the Americas as of 2024. GLP's subsidiary ESR Group manages approximately USD 156 billion in combined assets under management. The company is investing heavily in smart warehousing and last-mile infrastructure across emerging Asian markets.

DHL Supply Chain

DHL Supply Chain, a division of Deutsche Post DHL Group, is the world's largest contract logistics and managed warehousing provider, operating over 1,400 warehouses across 55 countries. In February 2025, DHL announced a USD 2 billion investment in supply chain digitalization including AI-powered WMS deployment across its global network.

Goodman Group

Goodman Group is a global industrial REIT with a portfolio valued at over USD 78 billion in 2024, specializing in large-scale logistics and business parks across 17 countries. The group's development pipeline exceeded USD 13 billion in 2024, predominantly focused on mega-distribution centers with integrated renewable energy systems.

XPO Logistics

XPO is a leading technology-driven supply chain company providing contract logistics and transportation across North America and Europe. XPO operates approximately 206 warehouses globally and has invested heavily in robotics, AI-driven freight brokerage, and proprietary WMS platforms.

Market Concentration Analysis

The global warehousing and storage market is moderately fragmented. The top 5 operators – Prologis, GLP, Goodman Group, DHL Supply Chain, and Segro – collectively account for an estimated 12–15% of global market revenues in 2025, reflecting the industry's inherently localized character and the presence of thousands of regional and national operators.

Market consolidation is increasing due to REIT acquisitions, 3PL expansion, and high automation investment costs. However, emerging markets like India, Southeast Asia, and Africa remain fragmented, with domestic operators dominating.

Investment & Growth Opportunities

- Cold-Chain and Refrigerated Warehousing: India's cold chain logistics market is set to reach USD 30.98 billion by 2030, yet 40% food loss and pharma excursions persist. Private equity and logistics REITs are increasingly targeting cold storage assets, driving cap rate compression due to strong demand and limited supply.

- Smart Warehouse Technology Platforms: The global warehouse automation market is projected to reach USD 55 billion by 2030, with venture capital deployment into robotics startups exceeding USD 4.2 billion between 2020-2024.

- Emerging Market Infrastructure: India's Grade A warehousing stock, across the top 8 cities is projected to cross 500 million sq ft by 2030. Southeast Asia, the Middle East, and Africa offer significant greenfield development opportunities, driven by expanding logistics demand and rising infrastructure investments.

- Urban Logistics and Micro-Fulfillment: Urban last-mile logistics is emerging as a major investment opportunity, driven by rising e-commerce density and growing consumer expectations for faster, same-day delivery.

- Green and Sustainable Warehousing: Carbon-neutral warehouse development qualifies for green bonds, lowering cost of capital by 30–50 basis points. The green building premium in logistics real estate is projected to become standard pricing across North America and Europe by 2028-2030.

Future Market Outlook (2026-2034)

The global warehousing and storage market is projected to grow from USD 542.2 Billion in 2025 to USD 728.7 Billion by 2034, at a CAGR of 3.20%. Growth will be driven by structural demand from e-commerce expansion, pharmaceutical cold-chain investment, manufacturing nearshoring, and the accelerating adoption of smart warehousing technologies across all major geographies.

Fully automated dark warehouses are expected to move from pilot projects to mainstream Class-A facility standards across North America, Japan, and Northern Europe. AI-driven demand forecasting will lower inventory costs and support just-in-time regional distribution models. Meanwhile, geopolitical supply chain shifts, including nearshoring to Mexico, India, Vietnam, and Eastern Europe, will drive new warehouse demand. Additionally, the Middle East’s logistics hub expansion, led by Dubai and Abu Dhabi initiatives, is expected to support faster-than-average market growth through 2034.

Research Methodology

IMARC Group's market research methodology for this report combines primary and secondary research approaches to ensure data accuracy, analytical rigor, and forecast reliability.

Primary Research

Primary research included structured interviews with warehouse operators, logistics service providers, real estate developers, technology vendors, and end-use industry procurement managers across key geographies. Supply-side and demand-side interviews yielded insights into investment priorities, technology adoption data, and operational challenges.

Secondary Research

Secondary research encompassed analysis of trade publications (Logistics Management, DC Velocity, Supply Chain Dive), government statistical databases (US Census Bureau, Eurostat, National Bureau of Statistics of China), industry associations (IWLA, GS1, IANA), company annual reports, and real estate data from CBRE, JLL, and Cushman & Wakefield.

Forecasting Models

Market size estimates and forecasts were developed using bottom-up and top-down triangulation. Econometric forecasting models incorporating GDP growth, e-commerce penetration rates, and 3PL spending trends were applied to generate the 2026–2034 forecast range.

Warehousing and Storage Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Type of Warehouses Covered | General Warehousing and Storage, Refrigerated Warehousing and Storage, Farm Product Warehousing and Storage |

| Ownerships Covered | Private Warehouses, Public Warehouses, Bonded Warehouses |

| End-Uses Covered | Manufacturing, Consumer Goods, Retail, Food and Beverage, IT Hardware, Healthcare, Chemicals, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Prologis, GLP, Goodman Group, DHL Supply Chain, XPO Logistics, DB Schenker, Panattoni, Segro, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the warehousing and storage market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global warehousing and storage market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the warehousing and storage industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Warehousing and Storage Market Report

The global warehousing and storage market was valued at USD 542.2 Billion in 2025, driven by e-commerce expansion, 3PL growth, and cold storage demand across key global regions.

The market is projected to reach USD 728.7 Billion by 2034, growing at a CAGR of 3.20% during 2026-2034, driven by automation investment, cold-chain expansion, and emerging market infrastructure development.

Asia-Pacific dominates with a 54.5% revenue share in 2025, led by China, India, Japan, and Southeast Asia's manufacturing and e-commerce logistics corridors and rapid industrial growth.

Refrigerated Warehousing and Storage is the fastest-growing type at ~4.8% CAGR (2026-2034), driven by pharmaceutical cold-chain expansion, biologics storage requirements, and e-grocery adoption globally.

Private Warehouses lead with a 65.4% market share in 2025, reflecting enterprise preference for dedicated, automation-integrated logistics facilities providing full operational control and supply chain security.

Key drivers include e-commerce expansion, 3PL outsourcing growth, cold-chain infrastructure investment, automation adoption (AMRs, AS/RS, AI-WMS), and emerging market warehouse capacity development programs.

Automation – including AMRs, AS/RS, and AI-driven WMS platforms – improves throughput by 30–50%, reduces labor costs, and enables competitive differentiation. The global warehouse robotics market exceeded USD 7 billion in 2024.

Leading companies include Prologis, GLP, Goodman Group, DHL Supply Chain, XPO Logistics, DB Schenker, Panattoni, and Segro across real estate development and 3PL managed warehousing segments.

Asia-Pacific growth is driven by China's manufacturing scale, India's National Logistics Policy, Southeast Asian e-commerce adoption, and massive port-linked logistics corridor investments across the region.

Key trends include smart warehousing automation, micro-fulfillment center proliferation, cold-chain as a strategic asset class, cloud WMS adoption, and green/sustainable warehouse development globally.

Bonded warehouses at 11.8% share (2025) are gaining momentum from rising cross-border e-commerce, free trade zone expansion, and customs-deferred inventory management strategies by global traders.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)