Watch Market Size, Share, Trends and Forecast by Type, Price Range, Distribution Channel, End User, and Region, 2026-2034

Global Watch Market Size, Share, Trends & Forecast (2026-2034)

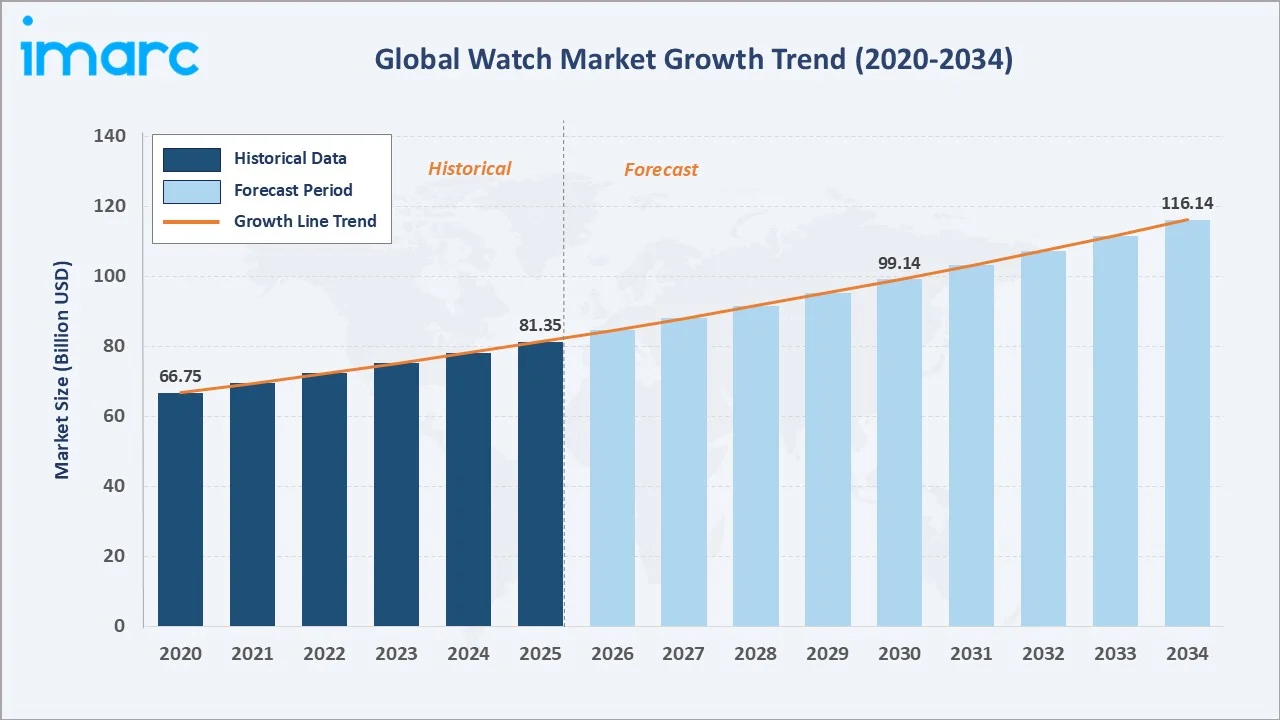

The global watch market size reached USD 81.35 Billion in 2025 and is projected to reach USD 116.14 Billion by 2034, exhibiting a CAGR of 4.04% during 2026-2034. Increasing disposable incomes, growing smartwatch adoption, and expanding e-commerce platforms are primary growth drivers.

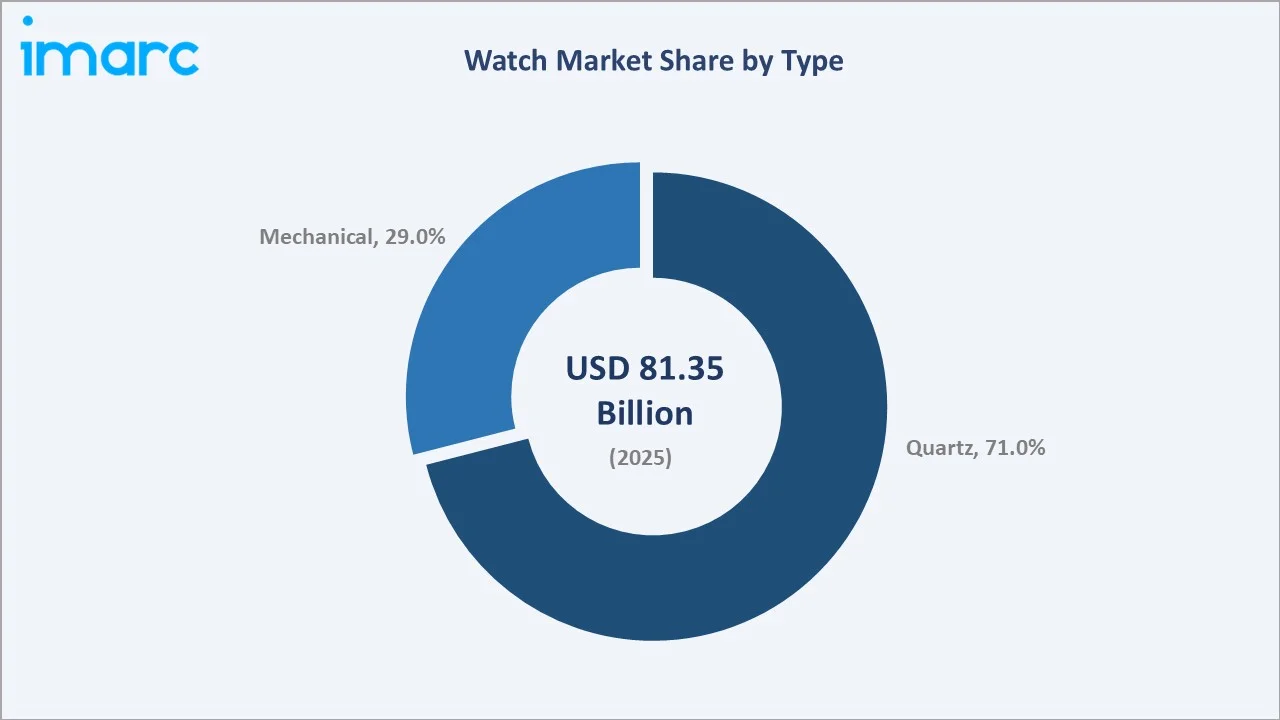

Quartz dominates at 71.0% type share; Asia-Pacific leads regionally at 33.7% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 81.35 Billion |

|

Forecast Market Size (2034) |

USD 116.14 Billion |

|

CAGR (2026-2034) |

4.04% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (33.7% share, 2025) |

|

Second Largest Region |

Europe (28.5% share, 2025) |

|

Leading Type |

Quartz (71.0%, 2025) |

|

Leading Price Range |

Low-Range (49.9%, 2025) |

The global watch market growth trajectory from 2020 through 2034, with historical expansion to USD 81.35 Billion in 2025, reflects consistent lifestyle and luxury-driven demand. The forecast to USD 116.14 Billion captures accelerating smartwatch adoption, luxury premiumisation, and Asia-Pacific middle-class expansion across emerging consumer markets.

To get more information on this market, Request Sample

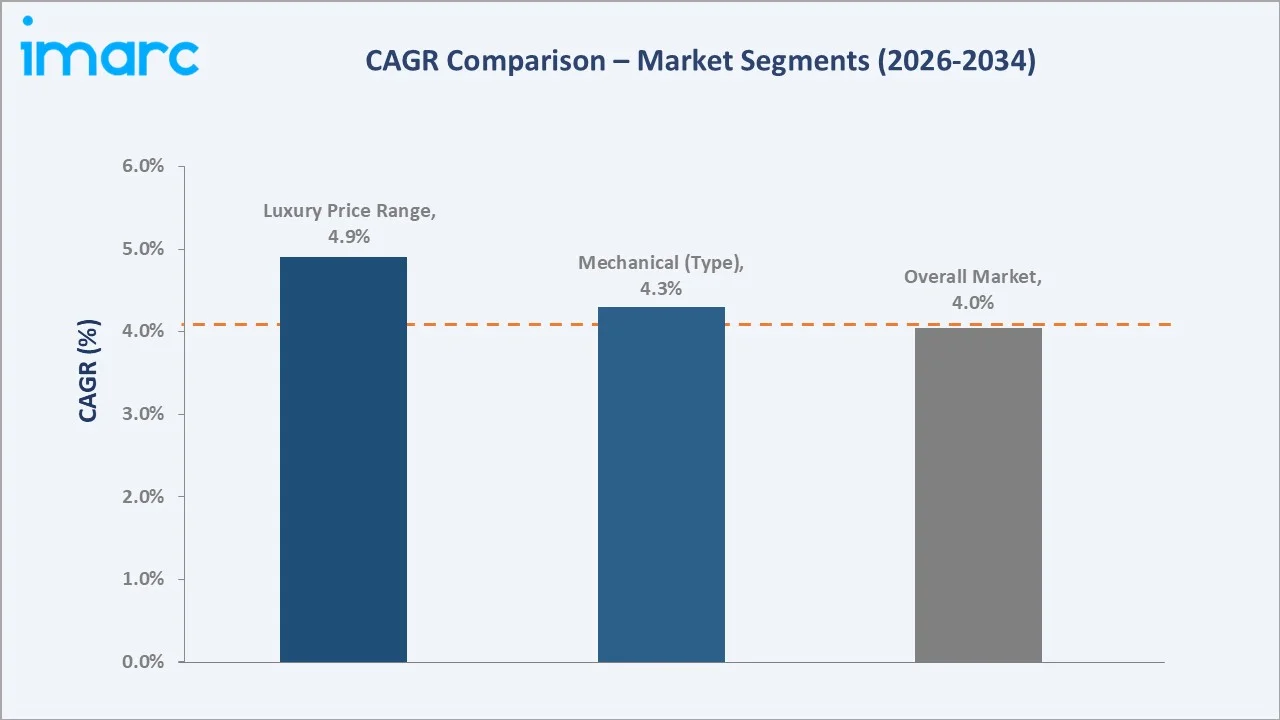

CAGR trajectories across type, price range, and regional sub-segments show Luxury price range at ~4.9% CAGR and Mechanical watches at ~4.3% CAGR as the fastest-growing categories within the global watch industry analysis through 2034.

Executive Summary

The global watch market is on a sustained growth trajectory from USD 81.35 Billion in 2025 to USD 116.14 Billion by 2034. Watches serve as timekeeping instruments, fashion accessories, status symbols, and health-monitoring platforms, generating multi-segment aspirational and non-discretionary consumer demand globally across diverse demographics.

Quartz watches dominate type at 71.0% in 2025 owing to superior accuracy, low maintenance, and broad affordability. Mechanical watches (29.0%) command premiums among collectors valuing craftsmanship and heritage, growing at approximately 4.3% CAGR as younger affluent demographics embrace horology as a cultural and investment interest.

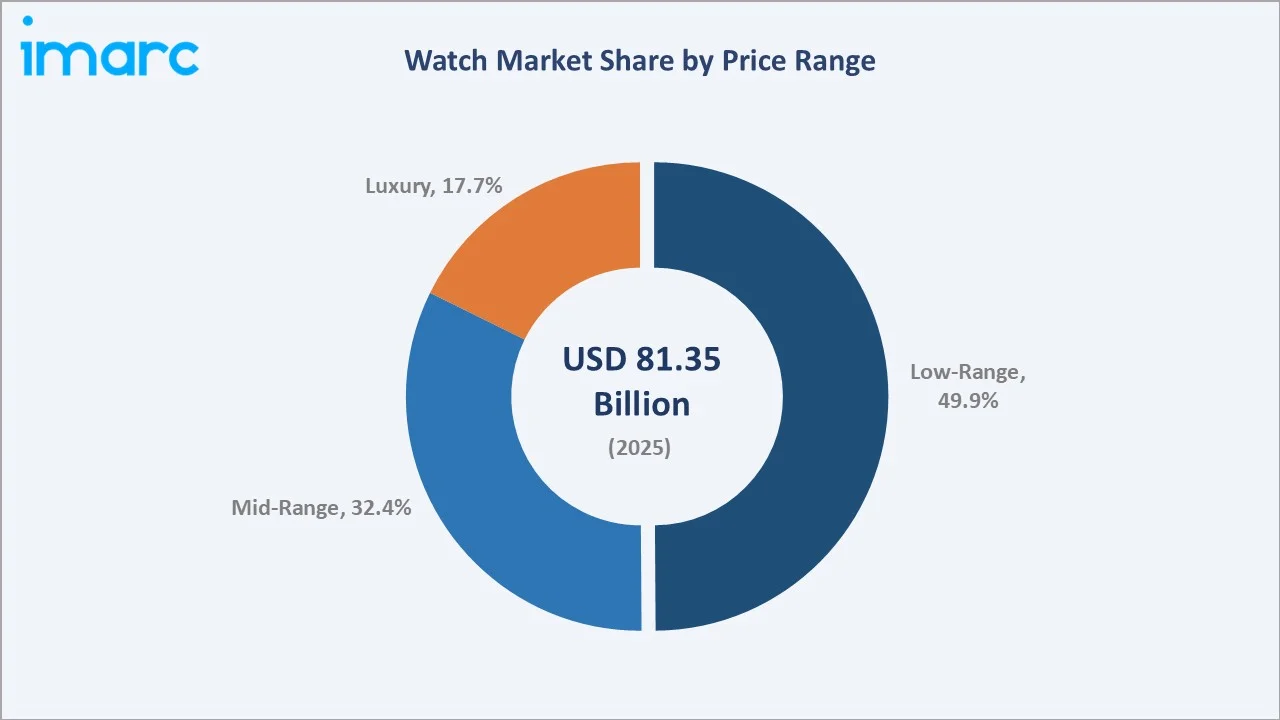

Low-Range leads at 49.9% reflecting mass-market accessibility. Mid-Range (32.4%) captures aspirational consumers. The Luxury segment (17.7%) is the fastest growing at approximately 4.9% CAGR, supported by HNWI wealth expansion, gifting culture, and the rapidly developing pre-owned certified luxury watch market worldwide.

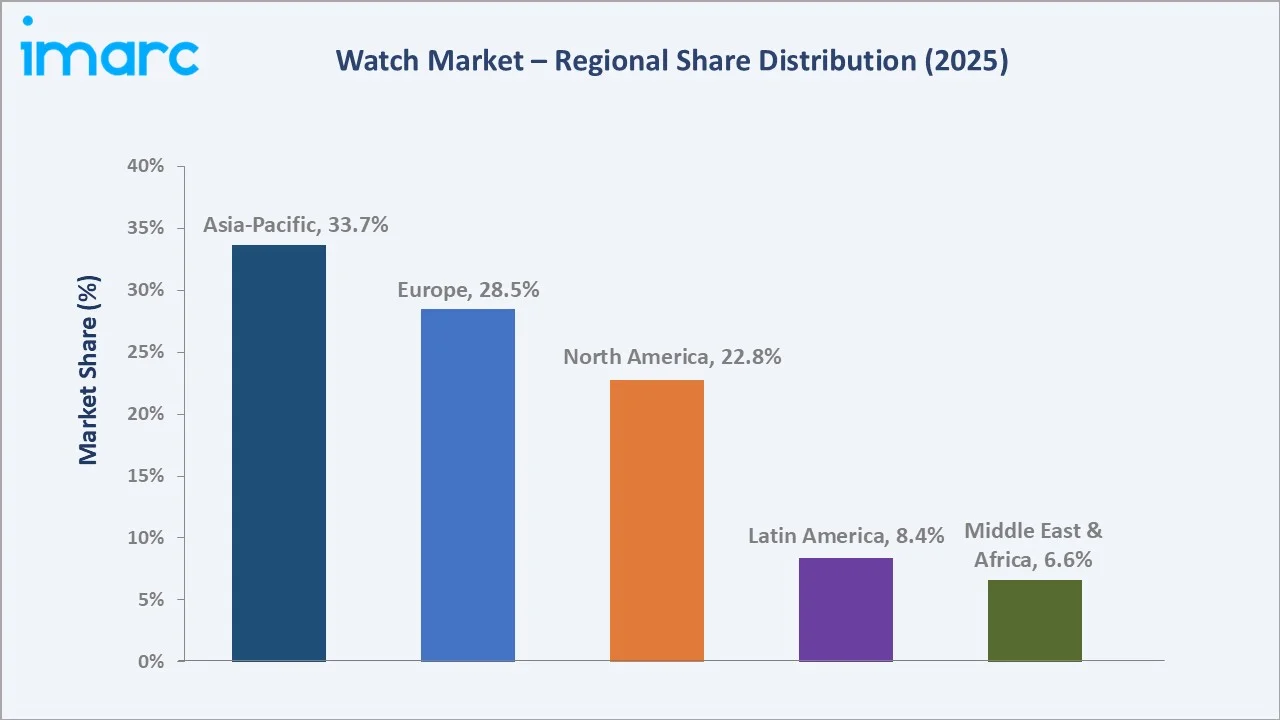

Asia-Pacific commands 33.7% in 2025 driven by China, Japan, and India. Europe (28.5%) reflects Swiss watchmaking heritage dominance. North America (22.8%) leads global smartwatch penetration and premium gifting demand, positioning the region as the primary battleground for connected and luxury watch brands.

Key Market Insights

|

Insight |

Data |

|

Leading Type |

Quartz – 71.0% share (2025) |

|

Second Type |

Mechanical – 29.0% share (2025) |

|

Leading Price Range |

Low-Range – 49.9% share (2025) |

|

Second Price Range |

Mid-Range – 32.4% share (2025) |

|

Leading Region |

Asia-Pacific – 33.7% share (2025) |

|

Second Largest Region |

Europe – 28.5% share (2025) |

|

Top Companies |

Apple Inc., Rolex, The Swatch Group Ltd, Casio Computer Co., Ltd., Samsung, Seiko Watch Corporation, Citizen Watch Co. Ltd., Titan Company |

Key Analytical Observations Expanding On The Above Data:

- Quartz at 71.0% dominates because oscillation accuracy of ±15 seconds/month at a fraction of mechanical movement cost meets mainstream consumer timekeeping needs across every price tier from entry-level to mid-range globally.

- Low-Range at 49.9% leads because fashion watches, entry-level digital models, and promotional watches drive high global unit volumes across Asia, Latin America, and Africa, where price sensitivity is the primary purchase decision driver.

- Asia-Pacific’s 33.7% share reflects China’s dominant consumer market scale, Japan’s globally exported precision watchmaking heritage, and India’s rapidly expanding organized retail penetration for fashion and mid-range watch categories.

Global Watch Market Overview

Watches are precision timekeeping instruments combining mechanical, quartz, or digital movement technologies with aesthetic case designs, dial artistry, strap materials, and embedded electronics for health monitoring, GPS navigation, and wireless connectivity capabilities.

The global ecosystem integrates raw material processors, Swiss precision movement specialists, Japanese quartz movement manufacturers, case and dial fabricators, global luxury brand houses, mass-market brand marketers, multi-channel retail networks, and diverse consumer segments spanning fashion, sport, professional, and investment-grade timepiece categories.

Market Dynamics

To access detailed market analysis, Request Sample

Market Drivers

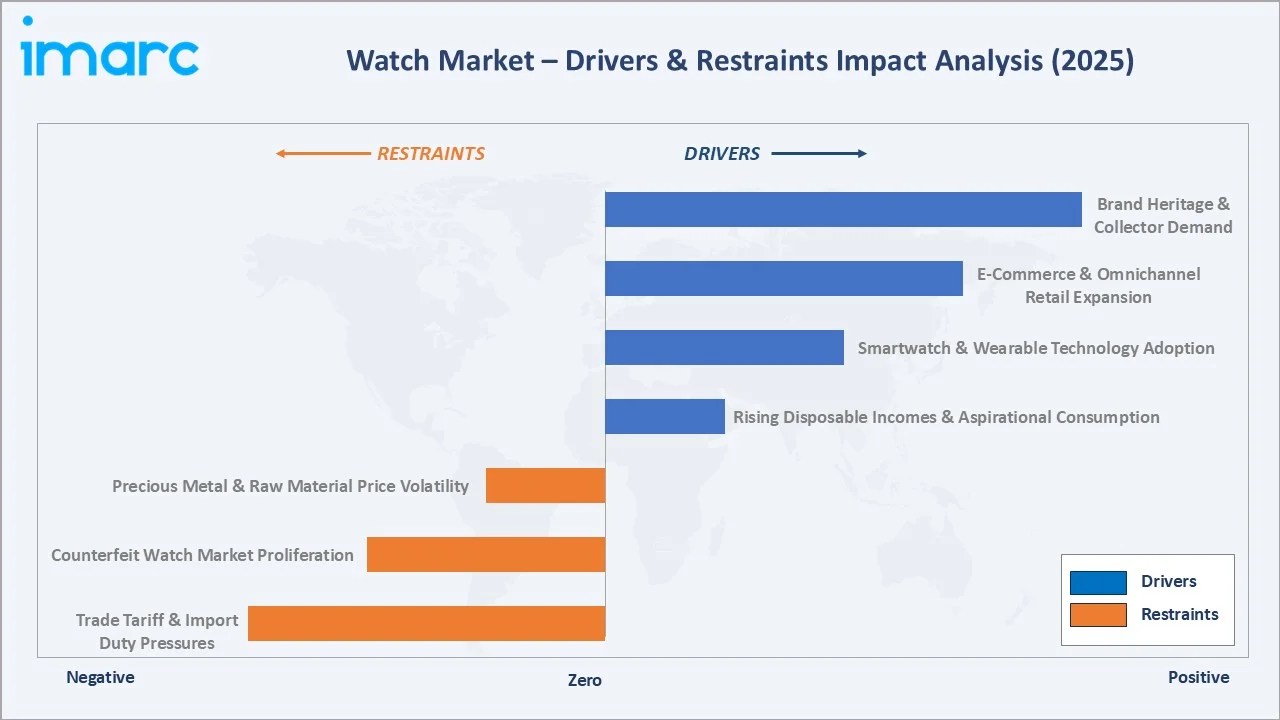

- Rising Disposable Incomes and Aspirational Consumption: Global HNWI population grew 7.8% in 2021, expanding the addressable market for mid-range and luxury watches, particularly across Asia-Pacific, Middle East, and Latin America’s fast-growing affluent consumer segments.

- Smartwatch and Wearable Technology Adoption: The global smartwatch market has been expanding rapidly, supported by strong shipment volumes and continuous innovation. In 2023 alone, more than 150 million smartwatches were shipped worldwide, highlighting growing consumer adoption and reinforcing the segment’s influence within the broader global watch market.

- E-Commerce and Omnichannel Retail Expansion: Online watch sales are growing faster than offline, with direct-to-consumer luxury platforms, pre-owned marketplaces such as Chrono24 and Watchfinder, and brand.com boutiques expanding the category’s digital-channel accessible market significantly.

Market Restraints

- Trade Tariff and Import Duty Pressures: Increasing US tariffs on Swiss watch imports and retaliatory trade measures are compressing manufacturer and authorized dealer margins, affecting Swiss export volumes into the United States, historically one of the largest Swiss watch export destination markets globally.

- Counterfeit Watch Market Proliferation: The global counterfeit watch market erodes brand equity and authorized dealer revenues; Customs and Border Protection has seized counterfeit watches valued at over USD 1.88 Billion in recent reporting periods, highlighting the scale of enforcement challenges worldwide.

Market Opportunities

- Emerging Market Middle-Class Penetration: India, Southeast Asia, and Sub-Saharan Africa represent under-penetrated markets with rapidly growing aspirational middle classes; India’s organized watch retail penetration is expected to expand significantly through 2030 as modern retail formats reach tier-2 and tier-3 cities.

- Pre-Owned and Certified Secondhand Luxury Watch Market: The global pre-owned luxury watch market is growing at approximately 10% annually, enabled by platforms such as Chrono24 and WatchBox and brand-sponsored certified pre-owned programs from leading Swiss brands expanding overall market accessibility.

Market Challenges

- Precious Metal and Raw Material Price Volatility: Fluctuations in the prices of precious metals and other key inputs are increasing production costs for premium watches, prompting brands to raise prices and potentially impacting demand in more price-sensitive segments. This cost pressure is also affecting margins and forcing manufacturers to explore material substitutions, hedging strategies, and more efficient sourcing to maintain competitiveness.

- Smartwatch Cannibalizing Traditional Entry-Level Segments: The growing popularity of smartwatches in the mid-price range is reducing demand for traditional entry-level watches, pushing conventional brands to strengthen their value proposition and differentiate beyond basic timekeeping. As consumer preferences shift toward multifunctional devices, traditional watchmakers are increasingly focusing on design, heritage, and craftsmanship to retain relevance and customer loyalty.

Emerging Market Trends

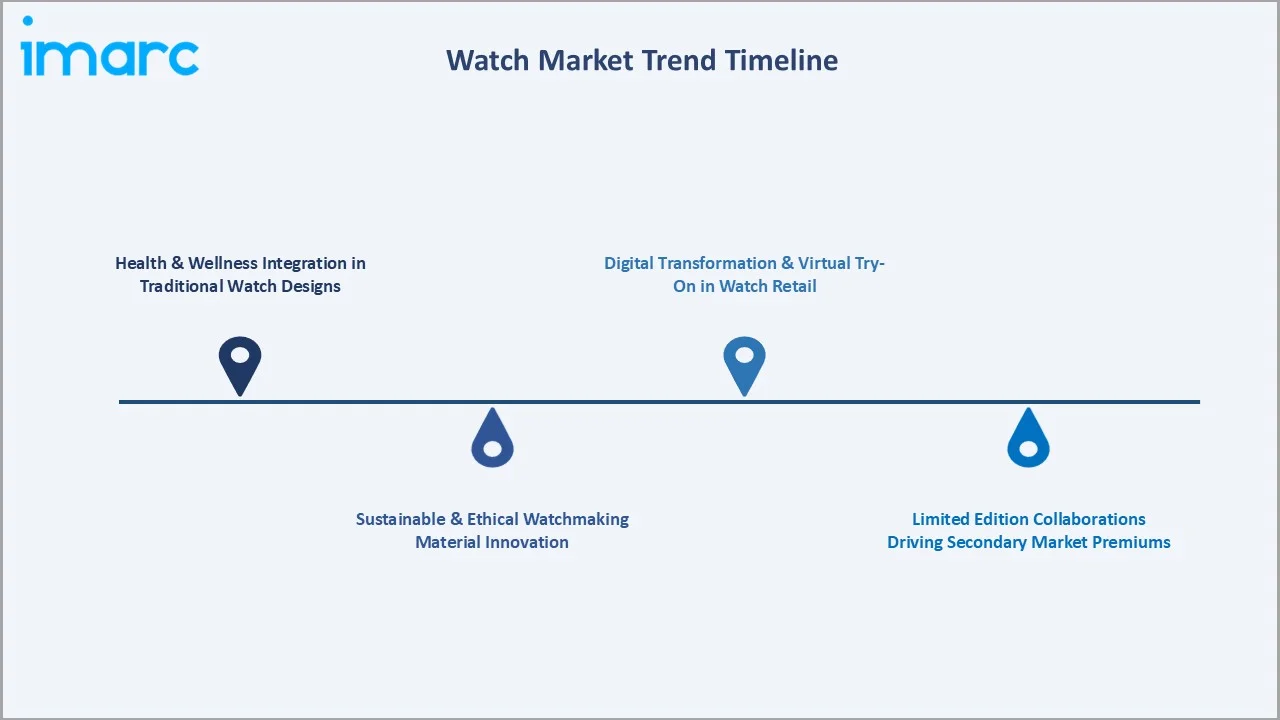

1. Health and Wellness Integration in Traditional Watch Designs

Swiss and Japanese traditional watch brands are integrating non-intrusive health monitoring features into analog designs, including light-based heart rate sensors and step counters, to compete with smartwatches while preserving the mechanical watch’s horological identity and heritage aesthetic for traditional watch consumers.

2. Sustainable and Ethical Watchmaking Material Innovation

Brands including IWC, Panerai, and Oris are adopting ocean plastic-derived straps, recycled stainless steel cases, lab-grown diamonds, and certified wooden dials, responding to Gen Z and Millennial demand for ethical luxury with transparent supply-chain provenance and independent sustainability certification credentials.

3. Limited Edition Collaborations Driving Secondary Market Premiums

Brand collaborations with luxury fashion houses, artists, and cultural institutions generate watches trading at 2–10x retail on secondary markets immediately upon release, with leading auction houses consistently recording premium results for limited-edition pieces from top Swiss and Japanese heritage watch brands.

4. Digital Transformation and Virtual Try-On in Watch Retail

Augmented reality try-on technology deployed on brand websites and applications is reducing e-commerce return rates and extending digital luxury watch sales reach, particularly benefiting markets where authorized dealer networks are sparse, underdeveloped, or where travel to physical boutiques remains impractical for consumers.

Industry Value Chain Analysis

The watch value chain spans six stages from raw material sourcing through after-sales service. Branding and marketing capture the highest margin in luxury segments, while movement manufacturing and precision assembly drive competitive advantage in technical and heritage watch categories across global markets.

|

Stage |

Description |

|

Raw Material Supply |

Steel, sapphire crystal, leather, titanium, and precious metals sourced from global commodity markets across multiple geographies. |

|

Movement Manufacturing |

Quartz and mechanical movement fabrication supplying watch brands across all price tiers and categories worldwide. |

|

Assembly & Finishing |

Watch case, dial, and movement assembly; quality control; surface finishing; and water resistance testing processes. |

|

Branding & Marketing |

Brand identity development, retail experience design, advertising, licensing, and consumer perception management activities. |

|

Retail & Distribution |

Sales through brand boutiques, authorized dealers, department stores, duty-free retail, and online platforms globally. |

|

After-Sales Service |

Warranty repair, servicing, authentication, and certified pre-owned watch program management activities. |

Vertically integrated groups maintaining proprietary movement manufacturing and in-house component supply achieve defensible competitive moats, enabling consistent quality control and greater resilience against supply disruptions, raw material cost increases, and third-party supplier quality variability across production cycles.

Technology Landscape in the Watch Industry

Movement Technology: Quartz Precision to High-Frequency Mechanical

Modern quartz movements achieve ±10 seconds/year accuracy in temperature-compensated oscillators deployed in premium solar-powered models. High-frequency mechanical movements operating at 5Hz (36,000 vibrations per hour) reduce positional error and improve chronograph precision to 1/10th second measurement capability for professional use.

Material Innovation: Ceramic, Carbon Fibre, and Sapphire Crystal

High-tech zirconia ceramics are deployed in scratch-resistant bezels and cases by leading brands, combining titanium’s lightness with ceramic’s hardness advantage. Carbon fibre composites reduce case weight by 40–60% versus stainless steel, serving the growing sports and adventure watch segment demanding extreme durability at reduced weight.

Smart Integration: Ecosystem Platforms and Health Device Convergence

Apple’s watchOS processes over 100 health metrics via its dual-core SiP processor platform with FDA-cleared atrial fibrillation detection features. Google’s Wear OS 4, deployed across Galaxy Watch series, integrates with Android health records, positioning smartwatch platforms as regulated medical device interfaces in cardiac monitoring applications.

Manufacturing Technology: CNC Precision, Laser Finishing, and Automation

Advanced CNC machining centres achieve case tolerances of ±0.01mm for complex multi-component case architectures, enabling consistent luxury finish quality at production scale. Laser surface finishing, PVD coating automation, and robotic dial printing allow premium brands to maintain artisanal aesthetic standards within industrial production volumes and quality parameters.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Quartz |

71.0% |

2025 |

|

Price Range |

Low-Range |

49.9% |

2025 |

|

Distribution Channel |

Offline Retail Stores |

63.6% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Asia-Pacific |

33.7% |

2025 |

By Type

Quartz watches command a 71.0% majority share in 2025 owing to their fundamental accuracy advantage, affordability across all price tiers, and negligible maintenance requirements versus mechanical alternatives. Battery-powered and solar-powered quartz movements satisfy mainstream consumer timekeeping needs across all global markets consistently and reliably.

To access detailed market analysis, Request Sample

Mechanical watches at 29.0% in 2025 represent the heritage-driven, collector-focused, and status-signalling segment. Hand-wound and automatic movements with visible escapements command premium pricing, with tourbillons, perpetual calendars, and minute repeaters generating the highest average selling prices across the ultra-luxury price tier.

By Price Range

Low-Range watches lead at 49.9% in 2025, encompassing fashion watches below USD 100, mass-market digital and analog models, and promotional watches driving high unit volumes across Asia and Latin America. Volume leadership reflects the broad global consumer base where functional timekeeping at accessible price points drives purchase decisions.

Mid-Range at 32.4% captures the aspirational USD 100–1,000 bracket including established mid-tier brands from Swiss and Japanese manufacturers. Luxury at 17.7% (USD 1,000+) encompasses heritage maisons and ultra-HNWI collectibles, growing fastest at approximately 4.9% CAGR as global wealth expansion supports premium discretionary spending.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

33.7% |

Largest consumer markets; rising middle-class aspirational demand; established manufacturing and distribution infrastructure. |

|

Europe |

28.5% |

Heritage watchmaking industries; luxury tourism-driven consumption; strong authorized dealer and boutique networks. |

|

North America |

22.8% |

Dominant smartwatch market; strong luxury gifting culture; high e-commerce penetration and consumer technology adoption. |

|

Latin America |

8.4% |

Growing urban middle-class demand; expanding organized retail; rising fashion and mid-range watch consumption trends. |

|

Middle East & Africa |

6.6% |

High-value gifting culture; luxury retail hub presence; expanding organized retail in major urban centres. |

Asia-Pacific’s 33.7% market dominance in 2025 is driven by China’s position as the world’s largest watch consumer market, Japan’s globally admired precision watchmaking heritage exported across premium categories, and India’s rapidly growing organized retail penetration in the mid-range and fashion watch segments.

Europe’s 28.5% share reflects Switzerland’s unrivalled position as the global centre of luxury watchmaking, housing the world’s most prestigious brands and hundreds of independent specialist manufacturers across its historic watchmaking corridors, supported by strong luxury tourism demand from international visitors globally.

Competitive Landscape

The global watch market is moderately fragmented, with Swiss luxury groups and Japanese mass-market leaders holding strong positions in their respective segments. The smartwatch category is highly concentrated, with Apple and Samsung commanding dominant global shares in the connected wearable watch segment across all major markets.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Apple Inc. |

Series 11, SE3, Ultra 3 |

Leader |

Smartwatch dominance; health OS ecosystem; premium wearable integration with iPhone and health services. |

|

Rolex |

Submariner, Datejust, Day-Date, Daytona |

Leader |

Ultra-premium positioning; supply restriction strategy; highest secondary-market resale value globally. |

|

The Swatch Group Ltd |

Omega, Longines, Tissot, Swatch |

Leader |

Widest portfolio across all price tiers |

|

Casio Computer Co., Ltd. |

G-Shock, Pro Trek |

Leader |

Mass-market durability leadership; solar technology; strong youth cultural and streetwear appeal. |

|

Samsung |

Galaxy Watch series |

Leader |

Android smartwatch leader; health monitoring; Samsung Pay; Wear OS platform ecosystem integration. |

|

Seiko Watch Corporation |

Prospex, Presage, King Seiko, Astron |

Challenger |

Japan heritage; in-house movement manufacturing; GPS solar and Spring Drive technology leadership. |

|

Citizen Watch Co. Ltd. |

Citizen, Campanola |

Challenger |

Eco-Drive light-powered technology; atomic timekeeping; sustainability-driven brand positioning. |

|

Titan Company |

Titan, Sonata, Fastrack |

Emerging |

India market leader; accessible luxury positioning; youth-centric Fastrack brand and distribution strength. |

Key players include Apple Inc., Rolex, The Swatch Group Ltd, Casio Computer Co., Ltd., Samsung, Seiko Watch Corporation, Citizen Watch Co. Ltd., Titan Company, and others.

Key Company Profiles

Apple Inc.

Apple Inc. is the world’s largest smartwatch manufacturer and the global watch market’s largest single brand by revenue, achieving an estimated 30%+ unit share of the USD 200–500 bracket through Apple Watch integration with iPhone, health monitoring capabilities, and its broader services ecosystem.

- Product Portfolio: Apple Watch Series 11, SE3, Ultra 3, and others

- Recent Developments: In September 2025, Apple introduced the Apple Watch Series 11, positioning it as its most advanced wearable yet with a strong emphasis on health and performance enhancements. The device brings new capabilities such as hypertension notifications and a sleep score feature, offering deeper insights into users’ health and wellness.

- Strategic Focus: Apple’s watch strategy leverages its installed base of over 1.5 billion active devices to drive Apple Watch as a health and connectivity platform, differentiating through FDA-cleared medical features and seamless ecosystem lock-in generating high consumer switching costs across all user segments.

Rolex

Rolex is the world’s highest-revenue individual luxury watch brand, producing approximately 1.1 million watches annually at average retail prices exceeding USD 10,000, with secondary market premiums on its most sought-after models averaging 30–150% above retail consistently across global auction platforms worldwide.

- Product Portfolio: Submariner, Datejust, Day-Date, Daytona, and others

- Recent Developments: In April 2024, Rolex unveiled a series of new models that largely focused on refined updates to its existing collections rather than entirely new product lines. The releases emphasized a blend of luxury materials, intricate detailing, and subtle design enhancements across iconic models.

- Strategic Focus: Rolex’s strategy maintains supply restriction relative to demand to sustain secondary market premiums, expands exclusive boutique distribution globally, and continuously invests in proprietary movement and material innovation to justify aspirational pricing with verifiable engineering quality credentials.

The Swatch Group Ltd

The Swatch Group is the world’s largest watch manufacturer by revenue, with a portfolio spanning sixteen brands from entry-level Swatch to ultra-luxury Breguet, and ETA movement supply capabilities serving both its own brand portfolio and third-party manufacturers requiring precision movement components globally.

- Product Portfolio: Omega, Longines, Tissot, Swatch, and others.

- Recent Developments: In November 2025, The Omega Seamaster Planet Ocean, Swatch Group Watch, was redesigned with the launch of its fourth generation, marking a major evolution of the iconic dive watch line. Introduced 20 years after the original model, the new lineup includes multiple variants with updated case structures, bracelet options, and modernized aesthetics while maintaining the collection’s core identity.

- Strategic Focus: Swatch Group’s strategy leverages its dual position as both a multi-tier brand portfolio owner and the watch industry’s critical movement supplier, balancing mass-market volume with ultra-luxury prestige across a fully vertically integrated Swiss manufacturing base with significant supply chain control.

Market Concentration Analysis

The global watch market is moderately fragmented at the overall level, with no single company holding more than 15% of total market revenue. The luxury segment is more concentrated, with dominant Swiss groups collectively commanding significant share of the USD 1,000+ price bracket globally.

Smartwatch concentration is high: Apple and Samsung account for an estimated 55–60% of global smartwatch unit shipments, creating a duopoly in connected watches that pressures traditional brands to develop credible technology narratives or cede the USD 200–500 bracket to platform-driven ecosystem competition.

Investment & Growth Opportunities

Fastest-Growing Segments

Luxury price range at approximately 4.9% CAGR through 2034 is the highest-growth segment, driven by global HNWI wealth expansion, pre-owned market development, and limited-supply premium brand strategies generating secular demand growth outpacing GDP in key markets across China, Middle East, and India.

Mechanical watch type at approximately 4.3% CAGR through 2034 benefits from growing horological appreciation among younger collectors, robust auction market liquidity globally, and the irreplaceable craftsmanship narrative that mechanical movements provide as a compelling counterpoint to digital saturation in consumer markets.

Emerging Markets

Middle East & Africa at approximately 4.8% CAGR is the fastest-growing region through 2034. GCC duty-free retail growth, Saudi Arabia’s Vision 2030 tourism expansion, and UAE’s position as a global luxury re-export hub create large-scale premium watch procurement demand from a region with a deeply embedded luxury gifting culture.

Venture & Investment Trends

Private equity interest in consolidating authorized dealer networks and multi-brand e-commerce platforms is growing. Institutional conviction in the pre-owned luxury watch market as a distinct investable asset class is driving significant platform infrastructure investment and consolidation activity across multiple global markets simultaneously.

Future Market Outlook (2026-2034)

The global watch market is forecast to expand from USD 81.35 Billion in 2025 to USD 116.14 Billion by 2034 at a CAGR of 4.04%, adding USD 34.79 Billion in incremental annual market value over the forecast period, reflecting the watch’s unique convergence of functional utility, fashion expression, and investable collectible status.

Three forces will most significantly shape the watch industry through 2034: maturation of health-monitoring smartwatches as regulated medical devices; expansion of the pre-owned certified luxury market creating a parallel demand channel alongside new watch sales; and emergence of South and Southeast Asia as the next decade’s primary growth markets for both mass-market and premium watch categories globally.

Research Methodology

Primary Research

Primary research encompassed structured interviews with watch brand executives, authorized dealers, independent watchmakers, Swiss watch export trade representatives, and luxury retail analysts. Primary data validated market sizing, type and price range segment shares, regional demand estimates, and competitive positioning assessments across key geographies.

Secondary Research

Key secondary sources include Federation of the Swiss Watch Industry FH annual export statistics, IMARC Group market databases, Statista consumer electronics panels, Morgan Stanley luxury sector research, Chrono24 secondary market transaction data, and trade publications including Europa Star, WatchPro International, and industry analysis platforms.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting models incorporating consumer expenditure data, luxury goods inflation indices, regional GDP growth projections, and wearable technology adoption curves. Scenario analysis accounting for base, optimistic, and conservative cases addresses smartwatch category disruption uncertainty through 2034.

Watch Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Quartz, Mechanical |

| Price Ranges Covered | Low-Range, Mid-Range, Luxury |

| Distribution Channels Covered | Online Retail Stores, Offline Retail Stores |

| End Users Covered | Men, Women, Unisex |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Apple Inc., Rolex, The Swatch Group Ltd, Casio Computer Co., Ltd., Samsung, Seiko Watch Corporation, Citizen Watch Co. Ltd.. Titan Company, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the watch market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global watch market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the watch industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Watch Market Report

The global watch market reached USD 81.35 Billion in 2025, reflecting consistent demand driven by rising disposable incomes, growing smartwatch adoption, luxury consumption recovery, and expanding e-commerce retail channels across all major global geographies.

The market is projected to reach USD 116.14 Billion by 2034, growing at a CAGR of 4.04% during 2026-2034, driven by Asia-Pacific consumption growth, luxury premiumisation, smartwatch health-monitoring adoption, and expansion of the pre-owned certified luxury watch market globally.

Quartz watches dominate with a 71.0% type share in 2025, valued for their superior accuracy of approximately ±15 seconds per month, broad affordability across all price tiers, and minimal maintenance requirements, serving the majority of consumer timekeeping needs worldwide across all demographics.

Low-Range watches lead with 49.9% market share in 2025, driven by high unit volumes across Asia, Latin America, and Africa where price-sensitive consumers seek reliable timepieces. Mid-Range accounts for 32.4% and Luxury 17.7%, with Luxury being the fastest-growing segment at approximately 4.9% CAGR through 2034.

Asia-Pacific commands the leading 33.7% market share in 2025, driven by China’s position as the world’s largest watch consumer market, Japan’s globally admired precision watchmaking heritage, and India’s rapidly expanding aspirational middle-class demand for fashion and mid-range timepieces through 2034.

The Luxury price segment is the fastest growing at approximately 4.9% CAGR through 2034, driven by HNWI wealth expansion globally, the growing pre-owned certified luxury watches market, limited-edition supply restriction strategies, and deepening collector culture among younger affluent demographics in key consumption markets.

Leading companies include Apple Inc., Rolex, The Swatch Group Ltd, Casio Computer Co., Ltd., Samsung, Seiko Watch Corporation, Citizen Watch Co. Ltd., Titan Company, and others.

Smartwatch adoption is reshaping the USD 200–500 price bracket significantly, with Apple Watch and Samsung Galaxy Watch capturing substantial share from traditional quartz watch brands in North America and Europe. Traditional brands are responding by integrating technology features and emphasizing craftsmanship and heritage as distinct value differentiators.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)