Water-based Adhesive Market Report by Resin Type (Acrylic Polymer Emulsion (PAE), Polyvinyl Acetate (PVA) Emulsion, Vinyl Acetate Ethylene (VAE) Emulsion, Styrene Butadiene (SB) Latex, Polyurethane Dispersion (PUD), and Others), Application (Tapes and Labels, Paper and Packaging, Building and Construction, Woodworking, Automotive and Transportation, and Others), and Region 2026-2034

Water-based Adhesive Market Overview:

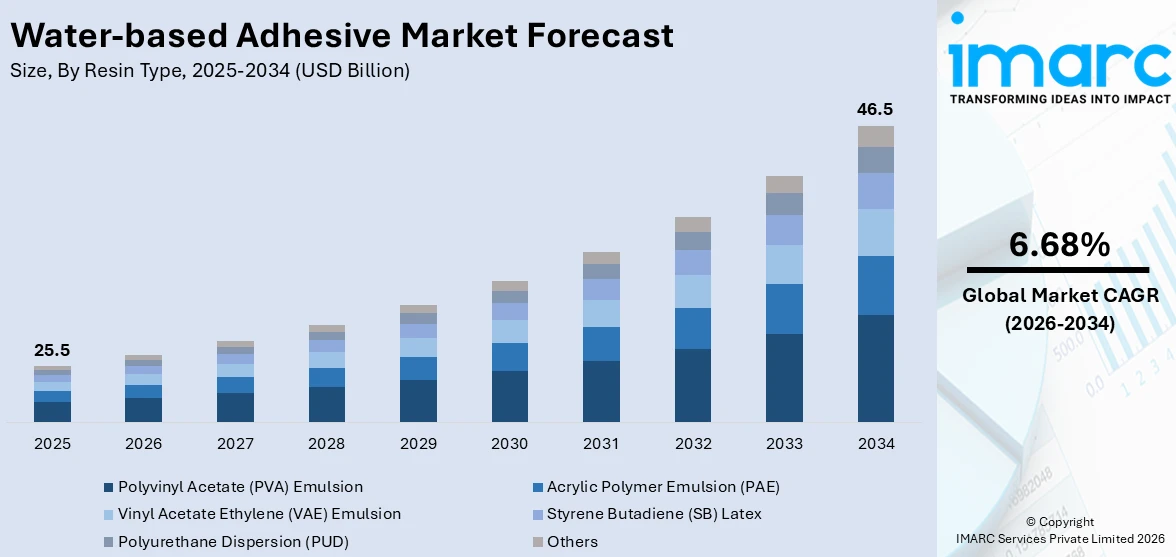

The global water-based adhesive market size reached USD 25.5 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 46.5 Billion by 2034, exhibiting a growth rate (CAGR) of 6.68% during 2026-2034. The market is driven by the rising demand for flexible packaging, rapid urbanization, and thriving textile industry that require water-based adhesives to emphasize on sustainability while improving performance and efficiency of textile manufacturing processes.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 25.5 Billion |

|

Market Forecast in 2034

|

USD 46.5 Billion |

| Market Growth Rate 2026-2034 | 6.68% |

Water-based Adhesive Market Analysis:

- Major Market Drivers: The growing demand for flexible packaging and rapid urbanization is positively influencing the market.

- Key Market Trends: The rising awareness among the masses about sustainable products and ongoing technological advancements are propelling the market growth.

- Geographical Trends: Asia Pacific holds the largest segment because of its rapid urbanization and industrialization.

- Competitive Landscape: Some of the major market players in the water-based adhesive industry include 3M Company, Arkema, Bond Tech Industries Inc., DuPont de Nemours, Inc., Evonik Industries AG, H.B. Fuller Company, Henkel AG and Co. KgaA, MAPEI S.p.A., Pidilite Industries Ltd., Sika AG, Weilburger Coatings GmbH, among many others.

- Challenges and Opportunities: While the market face challenges like performance limitations, it also encounters opportunities in the development of advanced water-based adhesive.

To get more information on this market Request Sample

Water-based Adhesive Market Trends:

Rising demand for flexible packaging

As per the IMARC Group’s report, the global flexible packaging market reached US$ 136.0 Billion in 2023. Flexible packaging is preferred for its lightweight nature and ability to reduce material consumption compared to traditional rigid packaging. Water-based adhesives align well with sustainability goals as they are compatible with a wide range of flexible packaging materials, such as films, foils, and paper and have lower environmental impact and volatile organic compound (VOC) emissions. Moreover, flexible packaging materials often come into direct contact with food and pharmaceuticals, necessitating strict compliance with regulatory standards for safety and hygiene. Such applications require non-toxic adhesive type like water-based adhesives that are compatible with food contact applications to meet the strict regulatory requirements.

Rapid urbanization

According to the content updated in 2023 on the website of the World Bank, around 50% of the population resides in urban areas. Urbanization resulted in the need for houses, businesses, and other structures, such as roads, bridges, and buildings. Construction or water based adhesives are used for sticking materials like woods, floorings, insulators, and wall coverings. Due to their low VOC emission, and their compliance to strict environmental standards, they are ideal for use in the urban areas where emissions are high. Furthermore, urbanization is leading to high vehicles adoption and demand for automotive products. Water-based adhesives are widely employed in automotive interiors for bonding fabric materials, carpeting and trim components. Low emissions and performance profiles satisfy the specific requirements of the automotive industry.

Thriving textile industry

Water-based adhesives are used in the textile industry for laminating fabrics, attaching linings, bonding trims, and assembling textile products including apparels, footwear, and furniture. They offer good bonding ability without affecting the elasticity and softness of textile substrates. In line with this, water-based adhesives are developed to respond to the requirements of the textile industry like flexibility, wash fastness, heat setting, and affinity to natural and synthetic textile materials including cotton, wool polyester, and nylon. Further development of the adhesive technology enhances these performance features. In addition, these adhesives are preferred in textile applications as they can be easily applied by using techniques, such as spraying, roller coating, or screen printing. It has good wet tack and adhesion, which enable smooth running of production processes in the textile industry. The IMARC Group’s report shows that the global textile market is expected to reach US$ 1,445.4 Billion by 2032.

Water-based Adhesive Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on resin type and application.

Breakup by Resin Type:

- Acrylic Polymer Emulsion (PAE)

- Polyvinyl Acetate (PVA) Emulsion

- Vinyl Acetate Ethylene (VAE) Emulsion

- Styrene Butadiene (SB) Latex

- Polyurethane Dispersion (PUD)

- Others

Polyvinyl acetate (PVA) emulsion accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the resin type. This includes acrylic polymer emulsion (PAE), polyvinyl acetate (PVA) emulsion, vinyl acetate ethylene (VAE) emulsion, styrene butadiene (SB) latex, polyurethane dispersion (PUD), and others. According to the report, polyvinyl acetate (PVA) emulsion represents the largest segment.

PVA emulsion adhesives are favored for their high ability to bond with porous materials, such as wood, paper, cardboard, and textiles, making them ideal for applications in woodworking, packaging, bookbinding, and textiles. They provide flexible adhesive strength and ease of use that make them ideal for home use and in the industries. Furthermore, PVA emulsions are classified as non-toxic, low odor suitable to meet the existing and future stringent regulatory standards and individual demands for safe, environment-friendly products. In addition, they can set and harden to a fine sleek surface that forms a coherent structure without shrinkage or brittleness, which is strengthening the water-based adhesive market growth.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Tapes and Labels

- Paper and Packaging

- Building and Construction

- Woodworking

- Automotive and Transportation

- Others

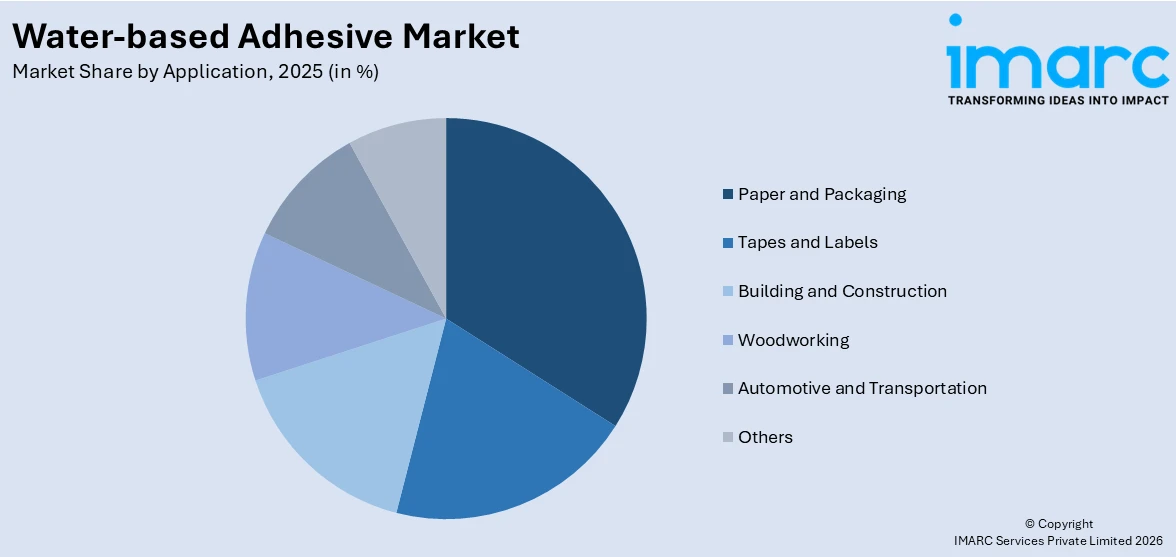

Paper and packaging hold the largest share of the industry

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes tapes and labels, paper and packaging, building and construction, woodworking, automotive and transportation, and others. According to the report, paper and packaging accounts for the largest market share.

Paper and packaging offer environmental advantages over solvent-based alternatives. Additionally, water-based adhesives are very useful and effective in bonding various kinds of paper and cardboard that improve production processes in companies dealing with packaging solutions. The fact that they can offer high-quality and long-lasting connections at a lower cost also guarantees their leadership in this field. Moreover, innovations in adhesive technology are continually improving their performance characteristics, such as faster curing times and enhanced adhesion properties, making them indispensable in the production of boxes, cartons, and labels.

Breakup by Region:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific leads the market, accounting for the largest water-based adhesive market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific represents the largest regional market for water-based adhesive.

As per the website of the National Bureau of Statistics of China, in 2023, the urbanization rate of permanent residents reached 66.16 percent. Rapid urbanization in China is driving the demand for packaging materials as consumption habits are changing and e-commerce platforms are expanding. Water-based adhesives play a crucial role in the production of sustainable packaging solutions, such as corrugated boxes, cartons, and labels, which are essential in urban logistics and retail sectors. Moreover, the availability of raw materials, lower production costs, and expanding manufacturing capabilities in the region contribute to its dominance in the global market. As industries in Asia Pacific are continuously expanding and modernizing, the water-based adhesives demand is expected to remain robust.

Key Regional Takeaways:

United States Water-based Adhesive Market Analysis

United States water-based adhesive market is experiencing consistent growth with increasing demand in packaging, woodworking, and construction industries. Growing use of environmentally friendly adhesives, as a result of stringent VOC regulations and awareness about the environment, is one of the driving forces in the market. The packaging sector, particularly food and beverage, plays an important role in fueling market growth as manufacturers move toward environmentally friendly bonding products. In addition, technological advances in adhesive technology have promoted performance, expanding their usage in automotive interior and textile applications. Industry leaders are now concentrating on creating high-strength, quick-curing adhesives to address the requirements of the industrial sector. Growth in e-commerce has also triggered demand for corrugated packaging, enhancing adhesive consumption. With continued innovations and favorable regulatory environments, the U.S. market will continue on its positive growth path.

Europe Water-based Adhesive Market Analysis

The European water-based adhesive market is growing as a result of environmental regulations and a high drive toward sustainability. Germany, France, and the UK are among the leaders in embracing low-emission adhesive technology, especially in packaging, construction, and automotive applications. The established manufacturing base of the region combined with an increasing focus on recyclable and biodegradable components has boosted the trend toward water-based systems. Also, growth in demand for on-line trading and advanced labeling solutions is driving the market. Advances in adhesive chemistry to enhance bonding strength and durability are also increasing their application base.

Asia Pacific Water-based Adhesive Market Analysis

Asia Pacific leads the world in water-based adhesive consumption, boosted by accelerated industrialization, urbanization, and high usage within packaging, building, and footwear industries. China and India are the growth drivers, with their growing manufacturing platforms and growing infrastructure development. The surging e-commerce sector has further raised the need for environmentally friendly packaging adhesives. Government policies supporting green products have also started to influence manufacturers to invest in water-based technologies.

Latin America Water-based Adhesive Market Analysis

Latin American water-based adhesive market is expanding gradually due to packaging, furniture, and construction applications. Brazil and Mexico dominate regional consumption, fueled by their growing industrial bases. Rising awareness of green adhesives and a slow transition toward eco-friendly packaging solutions are stimulating adoption.

Middle East and Africa Water-based Adhesive Market Analysis

In Africa and the Middle East, the market for water-based adhesives is making a strong entry, led mainly by construction work and the need for packaging. The UAE and South Africa are experiencing increasing adoption for rising infrastructure projects and industrial growth. Also, the growing trend towards low-VOC, environmentally friendly adhesives favor the market growth.

Competitive Landscape:

- The market research report has also provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the major market players in the water-based adhesive industry include 3M Company, Arkema, Bond Tech Industries Inc., DuPont de Nemours, Inc., Evonik Industries AG, H.B. Fuller Company, Henkel AG and Co. KgaA, MAPEI S.p.A., Pidilite Industries Ltd., Sika AG, and Weilburger Coatings GmbH.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

- Key players are continuously improving adhesive formulations to enhance performance characteristics, such as bonding strength, flexibility, and environmental sustainability. They are introducing new adhesive products tailored as per specific applications and industries, including packaging, construction, automotive, and healthcare. Moreover, many companies are developing adhesives with reduced volatile organic compounds (VOCs) emissions, low toxicity, and improved biodegradability to comply with stringent environmental regulations. They are integrating advanced technologies to improve adhesive application processes, enhance curing speeds, and optimize bonding performance. Key players are also collaborating with suppliers, other industries, and research institutions to drive innovations, address industry challenges, and expand market reach. For instance, in 2023, Arkema acquired Arc Building Products in Ireland, specialized in construction adhesives and sealants. This acquisition will strengthen its position in Ireland’s market with a broader range of solutions and a local manufacturing footprint.

Latest News and Developments:

- In January 2025, Mitsui Chemicals ICT Materia, Inc. developed a new surface protective tape using a water-based acrylic adhesive for fiber laser cutting, launched in September 2024. Mass production will start in April 2025 under the Mitsui Masking Tape™ lineup. The innovation reduces VOC and CO₂ emissions while maintaining easy peelability and low-noise unwinding, marking a sustainable alternative to solvent-based adhesives in metal processing.

- In November 2024, Henkel and Celanese partnered to produce water-based adhesives using captured CO₂ emissions. Leveraging Celanese’s carbon capture and utilization (CCU) technology at its Clear Lake, Texas site, industrial CO₂ is converted into methanol, a key component for adhesive polymers. These CCU-based adhesives enhance sustainability for packaging, labeling, and consumer goods industries, offering renewable content options and supporting manufacturers in meeting environmental goals.

- In June 2024, Zelu Chemie GmbH introduced a 2-component water-based contact adhesive for upholstered furniture, offering high initial adhesion strength even on complex geometries. The single-sided application reduces adhesive weight by up to 30%, cutting costs and saving production space. Designed for solvent-free production, it enhances occupational safety and environmental performance. The adhesive integrates easily into existing processes, providing a reliable, flexible, and durable bonding solution for diverse furniture substrates.

Water-based Adhesive Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Resin Types Covered | Acrylic Polymer Emulsion (PAE), Polyvinyl Acetate (PVA) Emulsion, Vinyl Acetate Ethylene (VAE) Emulsion, Styrene Butadiene (SB) Latex, Polyurethane Dispersion (PUD), Others |

| Applications Covered | Tapes and Labels, Paper and Packaging, Building and Construction, Woodworking, Automotive and Transportation, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | 3M Company, Arkema, Bond Tech Industries Inc., DuPont de Nemours, Inc., Evonik Industries AG, H.B. Fuller Company, Henkel AG and Co. KgaA, MAPEI S.p.A., Pidilite Industries Ltd., Sika AG, Weilburger Coatings GmbH, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the water-based adhesive market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global water-based adhesive market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the water-based adhesive industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Water-based Adhesive Market Report

The water-based adhesive market was valued at USD 25.5 Billion in 2025.

The water-based adhesive market is projected to exhibit a CAGR of 6.68% during 2026-2034, reaching a value of USD 46.5 Billion by 2034.

The water-based adhesive market is driven by rising demand for eco-friendly, low-VOC solutions, stricter environmental regulations, and the shift toward sustainable packaging. Growth in construction, automotive, woodworking, and e-commerce packaging sectors, along with advancements in adhesive formulations offering improved strength and versatility, further fuel market expansion globally.

Polyvinyl acetate (PVA) emulsion currently dominates the water-based adhesive market driven by its cost-effectiveness, strong adhesion, and versatility across applications like paper, packaging, woodworking, and textiles. Its low toxicity, quick setting time, and compatibility with eco-friendly formulations make it a preferred choice, especially amid rising demand for sustainable and low-VOC adhesives globally.

Paper and currently dominates the water-based adhesive market owing to surging e-commerce, rising demand for sustainable packaging, and strict environmental regulations. Water-based adhesives provide strong bonding, recyclability, and low VOC emissions, making them ideal for cartons, labels, and corrugated boxes in food, beverage, and consumer goods packaging industries.

Asia Pacific dominates the water-based adhesive market due to rapid industrialization, urbanization, and strong growth in packaging, construction, and footwear sectors. Countries like China and India drive demand with expanding manufacturing bases, booming e-commerce, and infrastructure projects. Additionally, government initiatives promoting eco-friendly products support widespread adoption of water-based adhesives.

Some of the major players in the water-based adhesive market include 3M Company, Arkema, Bond Tech Industries Inc., DuPont de Nemours, Inc., Evonik Industries AG, H.B. Fuller Company, Henkel AG and Co. KgaA, MAPEI S.p.A., Pidilite Industries Ltd., Sika AG, Weilburger Coatings GmbH, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)