Water Flosser Market Size, Share, Trends and Forecast by Product, Application, Distribution Channel, and Region, 2026-2034

Water Flosser Market Size, Share, Trends & Forecast (2026-2034)

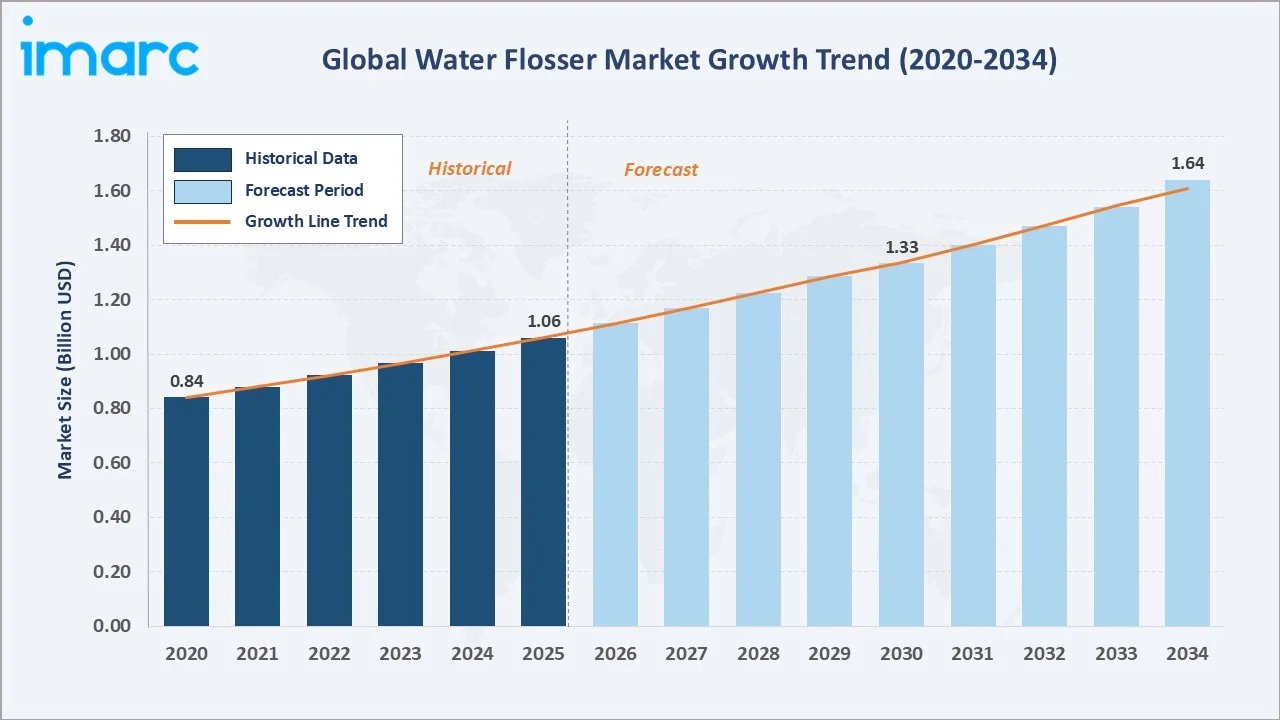

The global water flosser market reached USD 1.06 Billion in 2025 and is projected to reach USD 1.64 Billion by 2034, growing at a CAGR of 4.74% during 2026-2034. Rising global awareness of periodontal disease and gum health, increasing dentist recommendation of water flossers as adjuncts to mechanical brushing, growing e-commerce penetration enabling wider consumer access to oral care devices, and the superior plaque removal efficacy of water flossers relative to traditional string floss are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.06 Billion |

|

Forecast Market Size (2034) |

USD 1.64 Billion |

|

CAGR (2026-2034) |

4.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

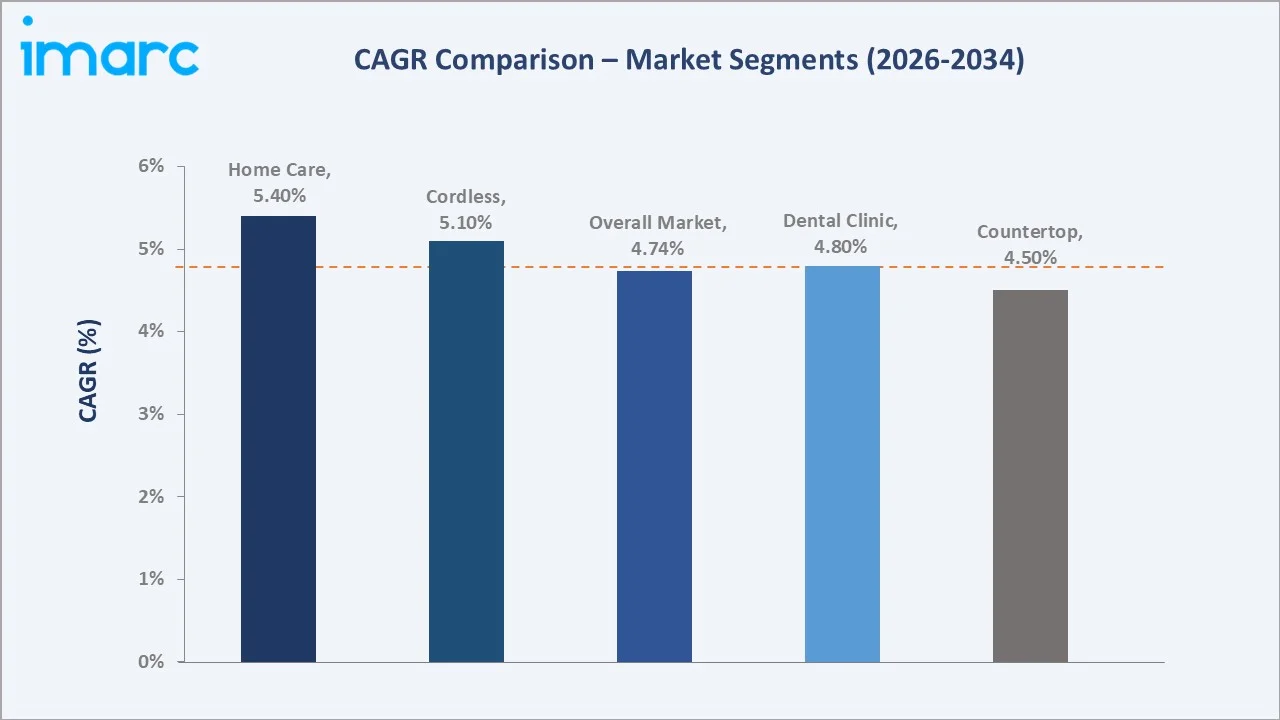

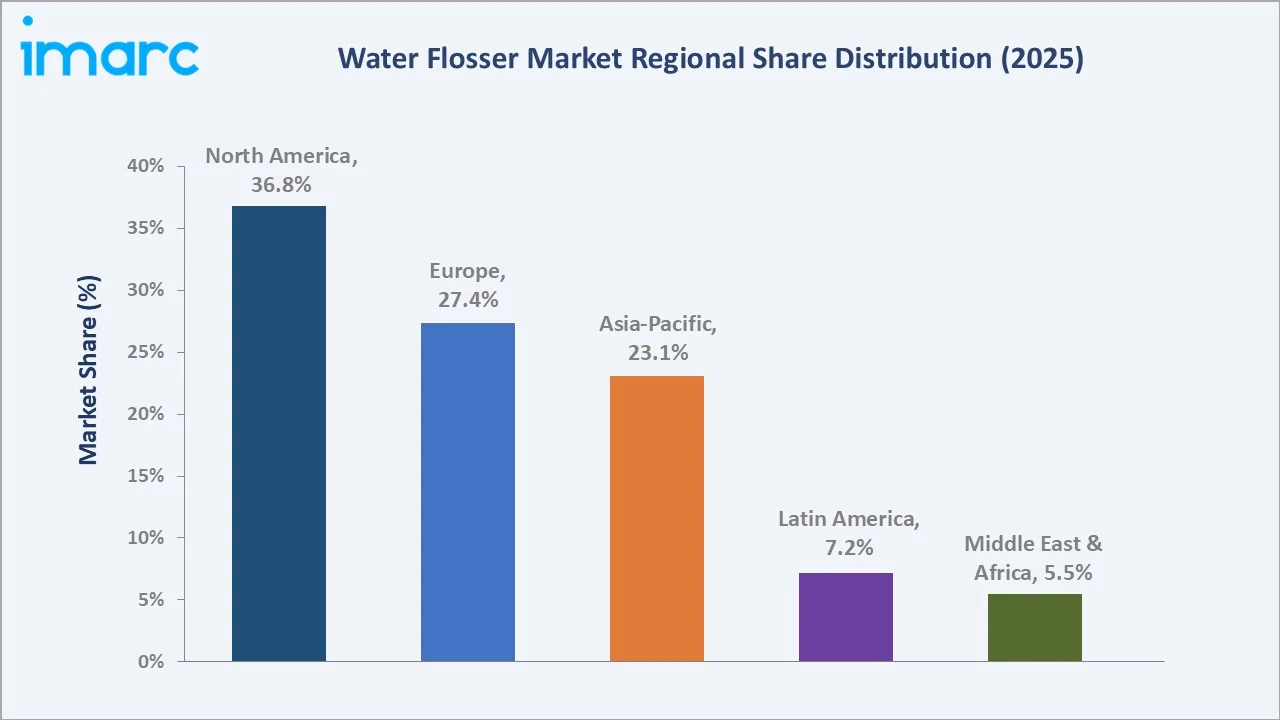

North America leads regionally with a 36.8% market share in 2025, underpinned by high consumer awareness of advanced oral hygiene and a large installed base of dental clinics actively recommending adjunctive flossing devices. Cordless models dominate the product segment at 52.8%, while dental clinics represent the largest application at 47.6%, reflecting the critical role of professional recommendation and clinical use in driving adoption across all consumer segments.

To get more information on this market, Request Sample

The global water flosser market is underpinned by three structural forces: the growing body of clinical evidence documenting water flossers' superiority over string floss for subgingival cleaning and gingival health improvement, the progressive shift of consumer oral care from reactive (dental treatment) to preventive, and the expanding accessibility of premium oral care devices through e-commerce platforms.

Executive Summary

The global water flosser market is experiencing consistent growth, driven by increasing preventive oral healthcare adoption globally and expanding professional endorsement. The market was valued at USD 1.06 Billion in 2025 and is forecast to reach USD 1.64 Billion by 2034 at a CAGR of 4.74%. This trajectory is supported by a robust clinical evidence base, strong dentist and periodontist recommendation behavior, and the growing consumer trend toward comprehensive at-home oral hygiene routines that extend beyond conventional toothbrushing.

Cordless water flossers command 52.8% of product market share in 2025, having displaced countertop models as the consumer preference through portability advantages, rechargeable battery convenience, and competitive pricing enabled by improvements in battery energy density and water reservoir miniaturization.

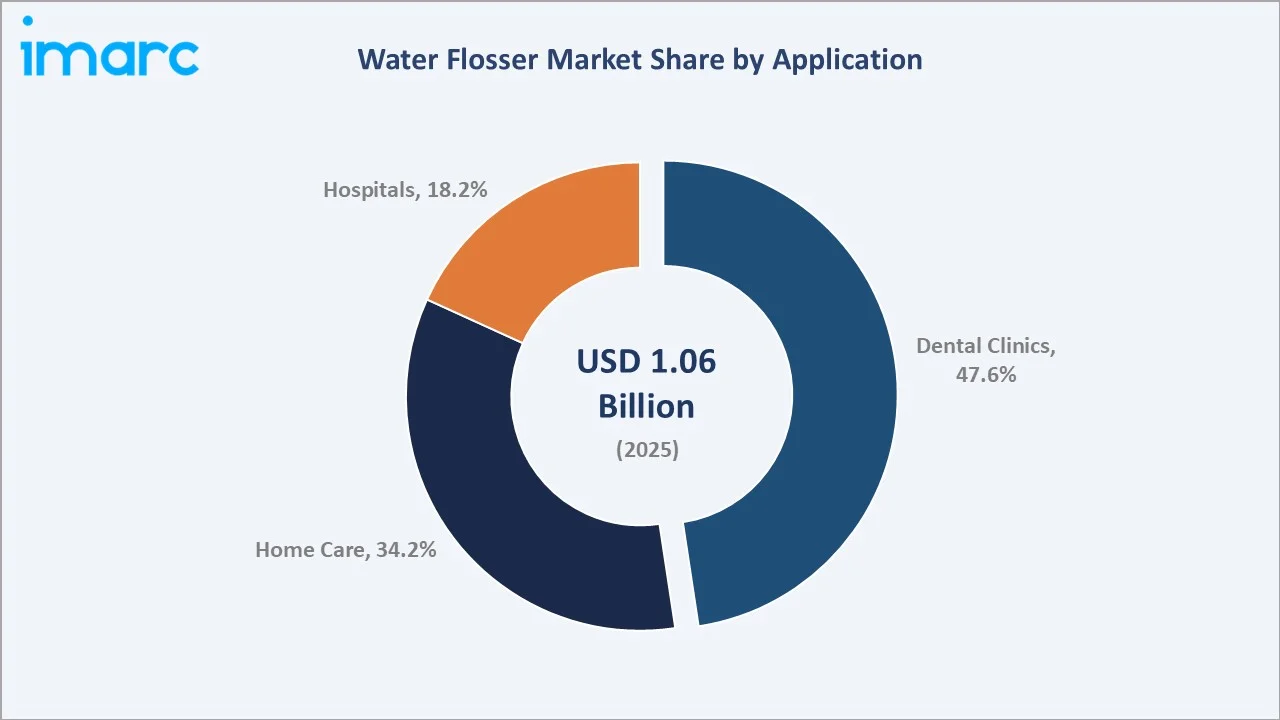

Dental clinics dominate application at 47.6%, reflecting both professional use for patient irrigation during procedures and the practice recommendation pathway that drives home care adoption. Home care at 34.2% is the fastest-growing application as clinical recommendation converts to direct-to-consumer device purchase.

Key Market Insights

|

Insight |

Data |

|

Largest Product |

Cordless – 52.8% share (2025) |

|

Fastest Growing Product |

Cordless – ~5.1% CAGR (2026-2034) |

|

Largest Application |

Dental Clinics – 47.6% share (2025) |

|

Fastest Growing Application |

Home Care – ~5.4% CAGR (2026-2034) |

|

Leading Region |

North America – 36.8% share (2025) |

|

Top Companies |

Church & Dwight Co., Inc., Koninklijke Philips N.V., Procter & Gamble, Aquapick |

Key Analytical Observations Supporting The Above Data:

- Cordless account for 52.8% of global product market share in 2025, having achieved market leadership over countertop models through a combination of technological improvement and consumer preference shift. Improvements in lithium-ion battery capacity have extended cordless flosser operational time to 30–45 days per charge for typical daily use, while advances in miniaturized pump technology have enabled cordless models to achieve water pressure ranges of 30–100 PSI.

- Dental clinics represent 47.6% of global water flosser application demand in 2025. This dominance reflects two distinct demand streams: clinical use for intraoral irrigation during prophylaxis, periodontal treatment, and implant maintenance procedures, and the professional recommendation pipeline where dentists and hygienists directly recommend and often sell water flosser devices to patients during check-up appointments.

- North America's 36.8% market leadership (2025) reflects the United States' position as the world's largest and most mature oral care device market, with high consumer expenditure on preventive dental products, a large periodontal patient population requiring irrigation adjuncts, and a well-developed dental professional recommendation ecosystem that actively endorses water flossers as adjuncts to mechanical brushing.

- Home Care’s 34.2% share (2025) is expected to be the fastest-growing application at ~5.4% CAGR reflects the convergence of dental professional awareness campaigns, social media oral care content driving consumer education, and e-commerce price accessibility that has brought cordless water flossers into the USD 25–80 mass-consumer price bracket.

Water Flosser Market Overview

Water flossers are personal oral hygiene devices that deliver a pulsating or rotating stream of pressurized water to remove food debris, plaque biofilm, and bacteria from between teeth and below the gumline. Unlike traditional string floss, which mechanically disrupts plaque through friction against tooth surfaces, water flossers use hydrodynamic shear and pulsation frequency to penetrate subgingival pockets and flush debris from orthodontic brackets, dental implants, bridges, and other restoration sites inaccessible to conventional floss.

The global market is segmented by product form factor (cordless, countertop, and others), application (dental clinics, home care, and hospitals), and distribution channel (online retail, specialty dental stores, pharmacy chains, and professional dental supply). The market encompasses devices ranging from entry-level cordless units at USD 20–40 to premium countertop clinical irrigators at USD 100–200, with clinical professional models for dental chair attachment reaching USD 300–800.

Market Dynamics

To evaluate market opportunities, Request Sample

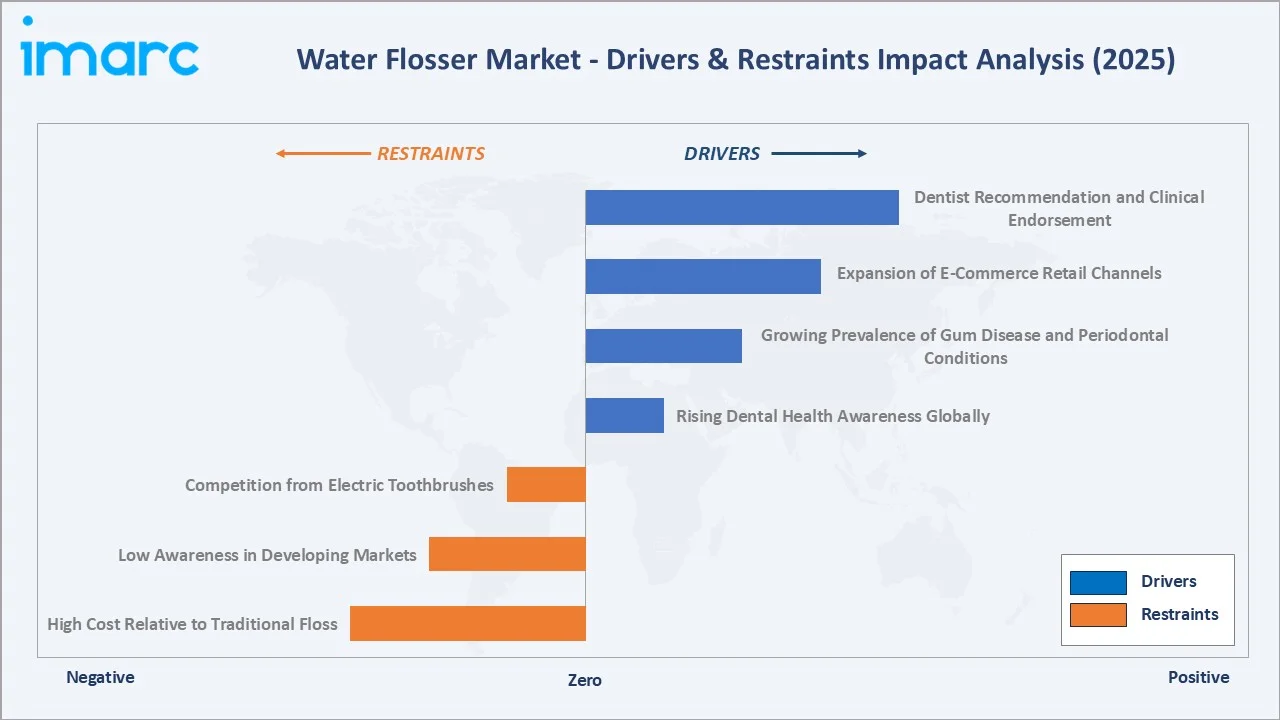

Market Drivers

- Rising Dental Health Awareness Globally: Global dental hygiene awareness campaigns from the American Dental Association (ADA), British Dental Association (BDA), FDI World Dental Federation, and national health ministries are increasingly recommending water flossers as evidence-based adjuncts to tooth brushing for interdental cleaning.

- Growing Prevalence of Gum Disease and Periodontal Conditions: The WHO estimates that approximately 1 billion people suffer from severe periodontal disease globally, with 45–50% of adults in developed markets and a rising proportion in emerging markets affected by some form of gum disease. Periodontal patients under active maintenance care are routinely prescribed water flossers for daily home irrigation between professional cleanings.

- Expansion of E-Commerce Retail Channels: E-commerce has been the most significant distribution channel shift in the water flosser market over 2020–2025, with online sales accounting for an estimated 45–55% of consumer water flosser purchases globally by 2025. Amazon, Tmall, JD.com, and regional e-commerce platforms have enabled water flosser brands to reach consumers in markets previously underserved by specialist dental product retail, dramatically expanding addressable market geography particularly across Asia-Pacific.

- Dentist Recommendation and Clinical Endorsement: Clinical research demonstrating water flossers' superiority over string floss for patients with orthodontic appliances (reducing gingival bleeding by 93% versus traditional floss per clinical studies) and implant maintenance has driven broad dental professional endorsement. Water Pik Inc.'s ADA Seal of Acceptance across its product range and Philips Sonicare's clinical study program have established professional credibility that translates directly into patient recommendation and in-office sale programs.

Market Restraints

- High Cost Relative to Traditional Floss: At USD 25–150 for device purchase plus replacement tips at USD 8–15 per set, water flossers represent a 50–200x price premium per year relative to traditional waxed dental floss at USD 3–8 annually. While the clinical cost-benefit argument for water flossers is strong, this price differential is a significant adoption barrier for cost-sensitive consumers in both developed and emerging markets.

- Low Awareness in Developing Markets: Despite growing e-commerce penetration, consumer awareness of water flossers remains low across large emerging market populations in South and Southeast Asia, Sub-Saharan Africa, and Latin America outside Brazil, where traditional toothbrushing is the dominant oral hygiene practice and interdental cleaning awareness is limited.

- Competition from Electric Toothbrushes: Electric toothbrush penetration is growing rapidly in the same health-conscious consumer demographic that represents the water flosser's primary target market, with premium electric toothbrush brands investing heavily in consumer education that emphasizes brushing technology over interdental cleaning.

Market Opportunities

- Smart and Connected Water Flosser Products: Integration of Bluetooth connectivity, pressure and technique feedback sensors, brushing session tracking via companion smartphone apps, and AI-driven personalized flossing program recommendations represents a high-growth opportunity in the premium water flosser segment.

- Orthodontic and Implant Patient Targeting: The global orthodontic market is experiencing record growth, with adult clear aligner adoption expanding the orthodontic patient population beyond traditional adolescent demographics. Adults wearing clear aligners and fixed braces represent a high-propensity water flosser purchase segment, as professional recommendation during orthodontic treatment consultation is standard practice.

Market Challenges

- Consumer Compliance and Habit Formation: Water flosser adoption does not guarantee sustained daily use, limiting the clinical benefits that would otherwise drive positive word-of-mouth recommendation and repeat brand loyalty. The bathroom device storage space required, water cleanup after use, and the additional time required compared to quick traditional string flossing create habit formation barriers that require ongoing consumer engagement to overcome.

- Regulatory Complexity Across Markets: Water flossers sold for clinical use are subject to medical device regulation in the EU clearance requirements, and equivalent regulatory frameworks in Japan, Australia, and China. Navigating multi-market regulatory compliance for clinical-grade products adds time and cost to product launch programs that constrains smaller manufacturers' ability to address professional clinical markets.

Emerging Market Trends

1. Cordless Innovation and Battery Technology Driving Market Leadership

The cordless segment's rise has been enabled by successive battery and pump technology improvements that have progressively closed the performance gap with countertop models. The introduction of IPX7 waterproof certification for bathroom-safe usage, USB-C charging standardization enabling universal charging cables, and Type-C fast-charge capability providing full charge in 1.5–2 hours have transformed the cordless flosser consumer experience.

2. Social Media and Dental Influencer Marketing Reshaping Consumer Discovery

The dental health content creator ecosystem has become the dominant consumer discovery channel for water flossers, displacing traditional TV advertising for the Gen Z and millennial demographic. 'Before and after' gum health content, water flosser comparison reviews, and dental professional product endorsement videos on social media have driven substantial purchase intent for water flosser products across markets where professional dental recommendation frequency is lower than North America and Europe.

3. Asia-Pacific Market Acceleration Through E-Commerce and Rising Oral Awareness

China's water flosser market has undergone rapid expansion driven by Alibaba's Tmall platform and short-video commerce on Douyin, with domestic brands competing aggressively on price to capture the large Chinese middle-class consumer base. South Korea is a strong growth market, while India represents an emerging growth opportunity as dental awareness programs and expanding dental clinic infrastructure drive initial water flosser adoption in urban centers.

4. Professional-Grade Clinical Irrigation Expanding Hospital Application

Hospital oral care protocols are progressively incorporating powered irrigation for patients with complex dental restoration histories, post-surgical recovery requirements, and chronic periodontal disease management programs. Oral Breeze's QuickFloss products are specifically marketed to clinical professionals for bedside irrigation in post-operative dental surgery recovery, oncology patient oral mucositis management, and critical care oral hygiene programs that reduce ventilator-associated pneumonia risk.

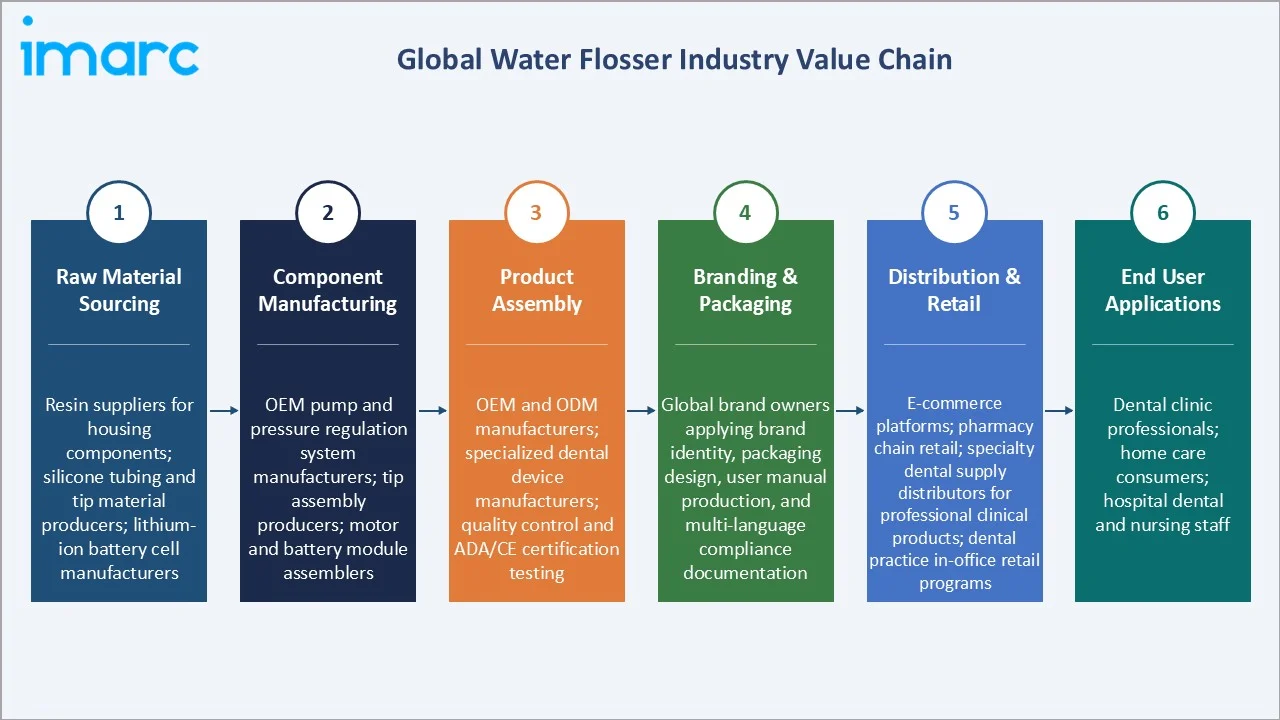

Industry Value Chain Analysis

The water flosser value chain spans raw material and component sourcing through end-user application, with distinct stages for consumer retail products versus professional clinical grade devices.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Resin suppliers for housing components; silicone tubing and tip material producers; lithium-ion battery cell manufacturers |

|

Component Manufacturing |

OEM pump and pressure regulation system manufacturers; tip assembly producers; motor and battery module assemblers |

|

Product Assembly |

OEM and ODM manufacturers; specialized dental device manufacturers; quality control and ADA/CE certification testing |

|

Branding & Packaging |

Global brand owners applying brand identity, packaging design, user manual production, and multi-language compliance documentation |

|

Distribution & Retail |

E-commerce platforms; pharmacy chain retail; specialty dental supply distributors for professional clinical products; dental practice in-office retail programs |

|

End User Applications |

Dental clinic professionals; home care consumers; hospital dental and nursing staff |

Technology Landscape in the Water Flosser Industry

Pump and Pressure Regulation Technology

The pump and pressure system is the core technical differentiator between water flosser product tiers. Entry-level cordless devices use miniaturized diaphragm or gear pumps generating 30–70 PSI with fixed pressure settings. Premium cordless and countertop models use piston pump systems enabling consumers to calibrate irrigation intensity for sensitive gums, implant maintenance, and post-surgical care.

Tip Technology and Specialization

Interchangeable tip assemblies are a key innovation and recurring revenue driver in the water flosser market. Standard jet tips provide directed single-stream irrigation for general interdental cleaning; orthodontic tips with tapered tip for bracket-by-bracket cleaning reduce gingival bleeding in brace-wearing patients versus string floss; periodontal tips with rubber cannula for 1–3 mm subgingival delivery enable professional-standard pocket irrigation at home; tongue cleaning tips with soft rubber surface supplement irrigation-based oral malodor control; and implant care tips with soft rubber tip minimize peri-implant tissue trauma during cleaning.

Connectivity and Smart Features

The premium water flosser segment is progressively integrating digital health technology: Bluetooth Low Energy (BLE) connectivity enables session data transmission to companion smartphone apps tracking flossing frequency, duration, and pressure selection; pressure sensors provide real-time feedback to prevent users from applying excessive pressure that may damage gum tissue; and voice assistant integration for flossing reminders is emerging in IoT-connected bathroom device ecosystems from Philips and Procter & Gamble.

Sustainable Design and Material Innovation

Consumer and regulatory sustainability pressure is driving water flosser product design evolution: replacement tip programs using recycled materials are being piloted by oral care device brands; USB-C universal charging standardization reduces adapter waste; and modular device architectures enabling motor and pump module replacement rather than full device disposal are being developed.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Cordless |

52.8% |

2025 |

|

Application |

Dental Clinics |

47.6% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

North America |

36.8% |

2025 |

By Product

The product segment is analyzed across cordless (52.8%), countertop (33.4%), and others (13.8%). Cordless models have achieved market leadership through portability, rechargeable convenience, and competitive pricing, while Countertop models retain preference in clinical settings and among heavy-use consumers requiring higher reservoir capacity and pressure range.

To access detailed market analysis, Request Sample

Countertop models maintain clinical preference for their larger water reservoirs, connection to antimicrobial solution addition for peri-implant and periodontal applications, and higher maximum pressure output for deep periodontal pocket irrigation.

By Application

The application segment is led by dental clinics (47.6%), followed by home care (34.2%), and hospitals (18.2%). Dental Clinics lead due to both professional clinical use and the critical role of dentist recommendation in converting consumers to home care water flosser adoption.

Home care is one of the fastest-growing applications, expanding as dental recommendation converts to device purchase and as social media oral health content drives independent consumer adoption without dental professional trigger. Hospitals at 18.2% serves critical care oral hygiene programs and post-operative dental surgery recovery protocols, creating institutional purchasing relationships with hospital procurement departments.

Regional Market Insights

North America leads the global water flosser market at 36.8% in 2025, reflecting the United States' status as the world's most developed oral health device market, with high consumer expenditure on preventive dental products and widespread dental insurance coverage encouraging preventive care visits where water flossers are recommended.

Europe at 27.4% represents a mature market with high oral care awareness and professional recommendation infrastructure, while Asia-Pacific at 23.1% is the fastest-growing region driven by China, South Korea, and emerging Southeast Asian markets.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

36.8% |

US dental professional recommendation ecosystem; large periodontal patient population; high consumer willingness to pay for premium oral care; expanding clear aligner orthodontic patient base requiring irrigation |

|

Europe |

27.4% |

Germany, UK, France dental awareness and specialist oral care retail; GDPR-compliant smart flosser data features; growing periodontal prevention focus in NHS and statutory dental systems |

|

Asia-Pacific |

23.1% |

China e-commerce and social commerce driving rapid adoption; South Korea high oral care device penetration; Japan mature dental hygiene market; India and Southeast Asia emerging urban middle-class oral care awareness growth |

|

Latin America |

7.2% |

Brazil dental care market expansion; rising middle class oral health spending in Colombia, Mexico, and Chile; growing private dental clinic networks recommending adjunctive oral hygiene devices; e-commerce accessibility to previously underserved markets |

|

Middle East & Africa |

5.5% |

GCC dental tourism and premium healthcare expansion; UAE and Saudi Arabia high-income consumer oral care spending; South Africa premium oral care retail growth; growing dental clinic infrastructure across MENA region |

Competitive Landscape

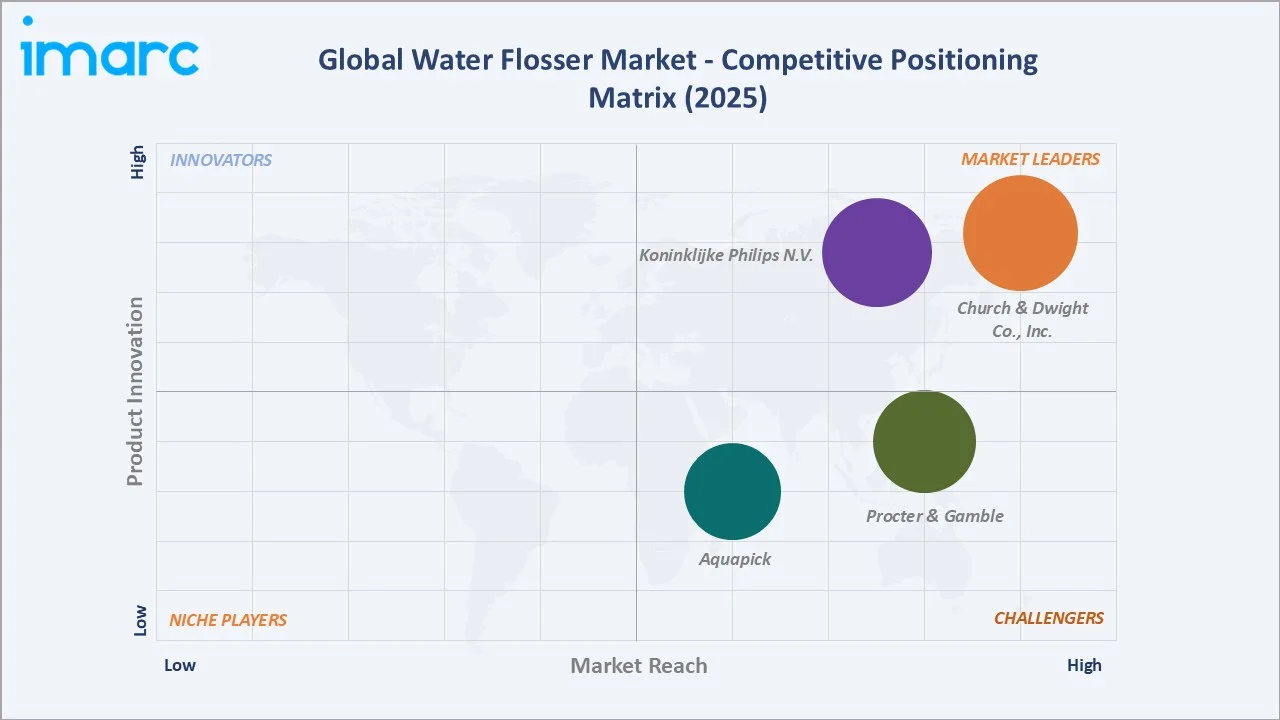

The global water flosser market exhibits moderate concentration in the professional and premium consumer segments, with key market players collectively holding an estimated 55–65% of the professional clinical and North American/European premium consumer market.

|

Company Name |

Brands/Products |

Market Position |

Core Strength |

|

Church & Dwight Co., Inc. |

Cordless Advanced 2.0 Water Flosser, ION Professional Cordless Water Flosser, Cordless Gem 5100 Water Flosser, Promax, Aquarius, Evolution, Ultra, Sidekick, among others |

Market Leader |

One of the broadest clinical evidence base; US professional recommendation leadership; countertop and cordless premium range; dental professional in-office sales program |

|

Koninklijke Philips N.V. |

Sonicare Power Flosser series, Cordless Power Flosser |

Market Leader |

Philips Sonicare Power Flosser range; connected oral care ecosystem integration; global pharmacy distribution; European brand trust; clinical study program supporting professional recommendation |

|

Procter & Gamble |

Oral-B Water Flosser Advanced |

Strong Challenger |

Oral-B brand integration with electric toothbrush ecosystem; global distribution reach; consumer marketing investment; professional dental network relationships |

|

Aquapick |

AQ-230, AQ-205, AQ-206, AQ-207, AQ-208, AQ-240, AQ-350, AQ-300, and AQ-320 |

Strong Challenger |

Korean innovation leader in cordless premium segment; strong Asia-Pacific distribution; clinical-grade tip technology at consumer price points; UV sanitization features |

Market leaders compete through clinical evidence investment, professional recommendation programs, and broad retail distribution. Chinese OEM manufacturers and regional brands compete in the e-commerce value segment on price and feature breadth, driving accessible consumer adoption that ultimately benefits the overall market by expanding the water flosser consumer base.

Key Company Profiles

Church & Dwight Co., Inc.

Church & Dwight Co. Inc.’s subsidiary Water Pik, Inc. is the global water flosser market's category pioneer and largest professional-endorsed brand.

- Product Portfolio: Waterpik Aquarius Professional Water Flosser (countertop flagship, 10 pressure settings, 90-second reservoir); Waterpik Cordless Advanced 2.0 (IPX7, 360-degree tip rotation); Waterpik Sonic-Fusion 2.0 (combined sonic toothbrush and water flosser); Waterpik Kids Water Flosser; professional clinical models including the Waterpik Professional Water Flosser (dental chair attachment).

- Recent Developments: In March 2026, Water Pik, Inc. introduced the PROMAX Water Flosser, featuring SMARTADVANCE technology that gradually increases water pressure to provide a deeper and more comfortable clean. The device offers 10 intensity settings, five specialized tips, a quadrant timer, and is clinically shown to significantly reduce gum bleeding within six weeks.

- Strategic Focus: Sustained clinical evidence investment to maintain professional recommendation leadership; connected oral care ecosystem development; cordless portfolio expansion to capture the growing portability segment; orthodontic and implant patient specialty marketing through dental professional channel partnerships.

Koninklijke Philips N.V.

Koninklijke Philips N.V. is a global health technology leader whose Personal Health division includes the Philips Sonicare oral care range, encompassing electric toothbrushes, power flossers, and tongue care devices.

- Product Portfolio: Philips Sonicare Power Flosser Quad Stream (four-stream nozzle tip, 3 pressure modes); Philips Sonicare Power Flosser 3000 and 5000 series; Philips One by Sonicare entry-level cordless range; Philips Sonicare DiamondClean Smart toothbrush with app integration (synergistic oral care ecosystem).

- Strategic Focus: Sonicare ecosystem cross-sell (electric toothbrush owners converting to power flosser for complete routine); European pharmacy and specialist oral care retail distribution strengthening; Bluetooth health data integration; Asia-Pacific expansion with Mandarin and Korean language app support.

Market Concentration Analysis

The global water flosser market exhibits a bifurcated concentration structure: the professional clinical and premium consumer segment is moderately concentrated, with top players collectively holding the majority of professional recommendation-driven revenue; the value consumer segment accessed primarily through e-commerce is highly fragmented, with dozens of Chinese OEM manufacturers and regional brands competing on price and feature specification in the USD 20–50 price tier.

Investment & Growth Opportunities

Fastest Growing Segments

Smart and connected cordless water flossers (~7%+ CAGR in premium segment), Home Care application expansion driven by social media discovery (~5.4% CAGR), specialty orthodontic and implant tip subscription programs (~6% CAGR), and Asia-Pacific e-commerce channel growth (~6.5% CAGR in regional market) represent the highest-growth investment vectors through 2034.

Emerging Market Expansion

India represents the most significant emerging market opportunity for water flosser adoption over the 2025–2034 period, with a large and growing urban middle class, rapidly expanding private dental clinic network, and government oral health initiatives driving awareness. India's dental device import market is growing at 8–10% annually, with water flosser penetration still below 2% of dental-aware urban consumers.

Venture and Institutional Investment Trends

- Direct-to-consumer oral care brands with subscription models are attracting venture capital investment as they demonstrate recurring revenue models that differentiate from one-time device purchase economics, with replacement tip subscription programs commanding USD 50–120 in annual recurring revenue per subscriber and reducing churn risk relative to open-market competitive re-purchase.

- Smart oral health platforms are attracting digital health funds targeting the preventive oral care segment, where demonstrated clinical behavior improvement translates directly to insurer and dental network cost reduction.

Future Market Outlook (2026-2034)

The global water flosser market is positioned for steady, sustained growth through 2034. From a base of USD 1.06 Billion in 2025, the market is projected to reach USD 1.64 Billion by 2034 at a CAGR of 4.74%, representing total incremental value creation of USD 580 Million.

This growth is underpinned by rising global periodontal disease prevalence, the growing adult orthodontic and implant patient population, and progressive consumer adoption of comprehensive at-home oral care routines that extend beyond traditional brushing.

The Home care application will grow from 34.2% to approximately 40–42% of total market as social media-driven consumer discovery and direct-to-consumer brand programs expand adoption beyond the dental clinic recommendation pathway. Asia-Pacific will close its gap with Europe, approaching 27–28% of global market by 2034 as China, India, and Southeast Asia markets scale.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 70 industry participants in 2024–2025, including oral care device manufacturers, dental supply distributors, dental professionals (dentists, periodontists, dental hygienists), retail pharmacy oral care buyers, and e-commerce platform category managers across North America, Europe, Asia-Pacific, and Latin America.

Secondary Research

Secondary research encompassed American Dental Association and FDI World Dental Federation oral hygiene recommendation publications, clinical research studies on water flosser efficacy in peer-reviewed journals (Journal of Clinical Periodontology, Journal of Dental Hygiene), oral care device market publications from industry associations including the American Academy of Periodontology, e-commerce sales data from Amazon and Tmall category analytics, and financial disclosures from key players covering oral care product segment performance.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating global periodontal disease prevalence data (WHO, CDC), dental clinic and dental professional count growth by region, e-commerce oral care device category growth rates, consumer willingness-to-pay studies for oral hygiene devices, and product price tier mix evolution models.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Cordless, Countertop, Others |

| Applications Covered | Hospitals, Dental Clinics, Home Care |

| Distribution Channels Covered | Online, Offline |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Church & Dwight Co. Inc., Koninklijke Philips N.V., Procter & Gamble, Aquapick, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Water Flosser Market Report

The global water flosser market reached USD 1.06 Billion in 2025 and is projected to reach USD 1.64 Billion by 2034.

The market is expected to grow at a CAGR of 4.74% during 2026-2034, driven by rising global periodontal disease awareness, dentist recommendation programs, growing adult orthodontic and implant patient populations, and expanding e-commerce accessibility of oral care devices.

North America leads with a 36.8% market share in 2025, driven by the United States' mature dental professional recommendation ecosystem, the large periodontal patient population, Water Pik's domestic market leadership, and high consumer expenditure on preventive oral care products.

Cordless water flossers dominate with a 52.8% share in 2025, having achieved market leadership over countertop models through portability advantages, rechargeable battery improvements, and competitive pricing enabled by advances in miniaturized pump and battery technology.

Dental clinics hold the largest application share at 47.6%, reflecting both professional clinical use for patient procedures and the critical recommendation pathway through which dental professionals drive 65–70% of consumer home care water flosser purchases.

Some of the key players include Church & Dwight Co., Inc., Koninklijke Philips N.V., Procter & Gamble, and Aquapick.

Key drivers include rising global awareness of periodontal disease and gum health, clinical evidence demonstrating water flossers' superiority for orthodontic and implant patients, e-commerce expansion enabling global consumer access, and social media oral health content driving consumer discovery beyond the dental recommendation channel.

Key challenges include the high cost premium versus traditional string floss creating adoption barriers, low consumer awareness in developing markets where dental professional recommendation networks are less developed, and competition from electric toothbrushes for consumer oral care device budget.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)