Water Treatment Chemicals Market Size, Share, Trends and Forecast by Type, End-User, and Region, 2026-2034

Global Water Treatment Chemicals Market Size, Share, Trends & Forecast (2026-2034)

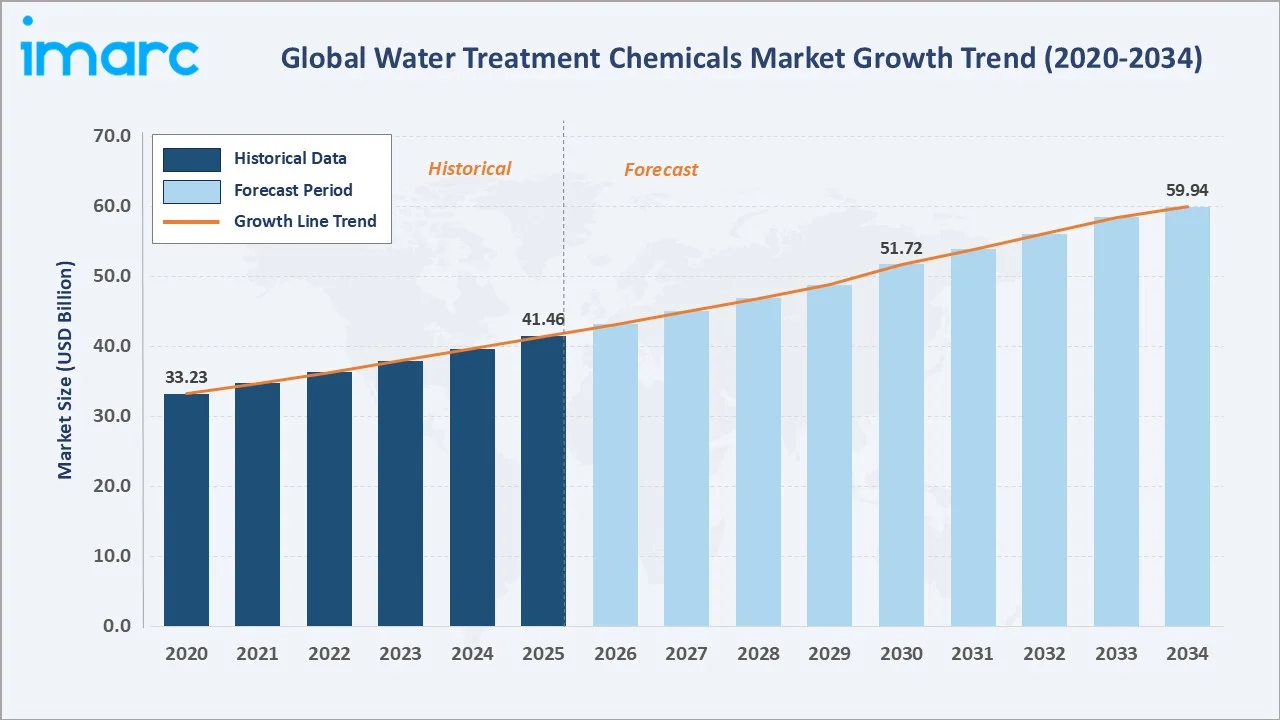

The global water treatment chemicals market size reached USD 41.46 Billion in 2025 and is projected to reach USD 59.94 Billion by 2034, exhibiting a CAGR of 4.53% during 2026-2034. Rising water scarcity, rapid urbanization, and increasingly stringent environmental regulations on wastewater discharge are the primary forces driving market growth.

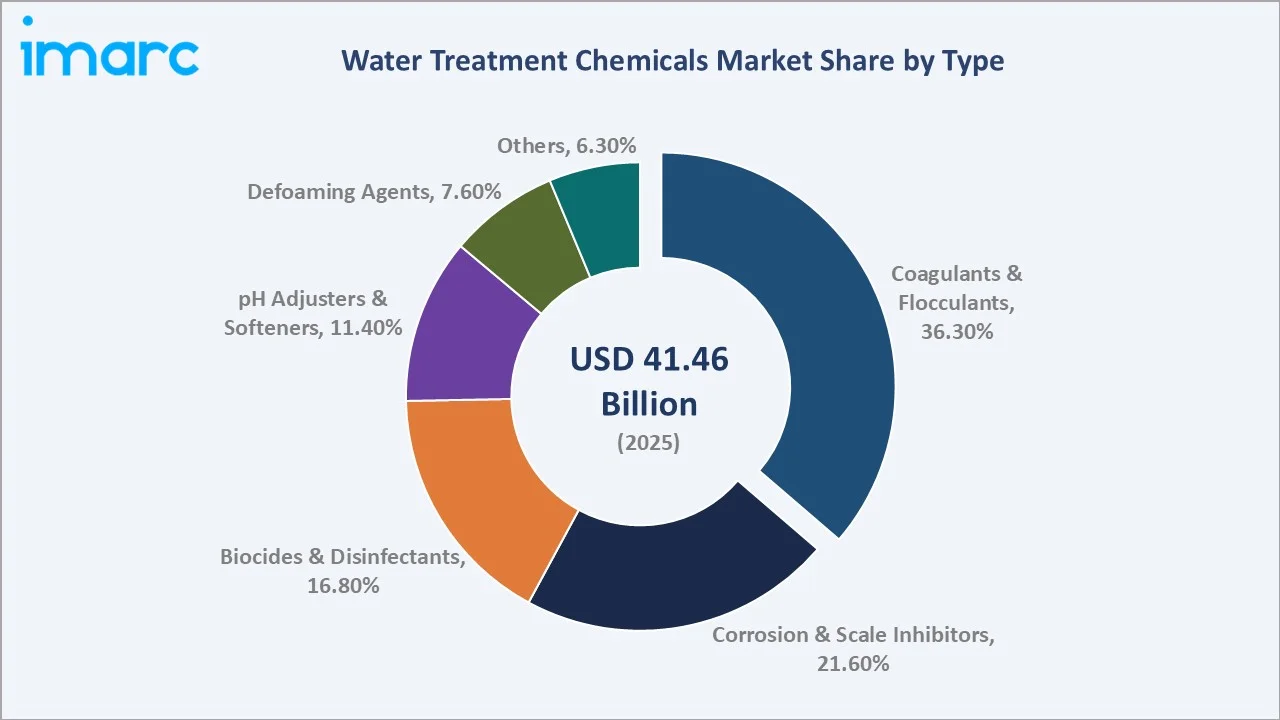

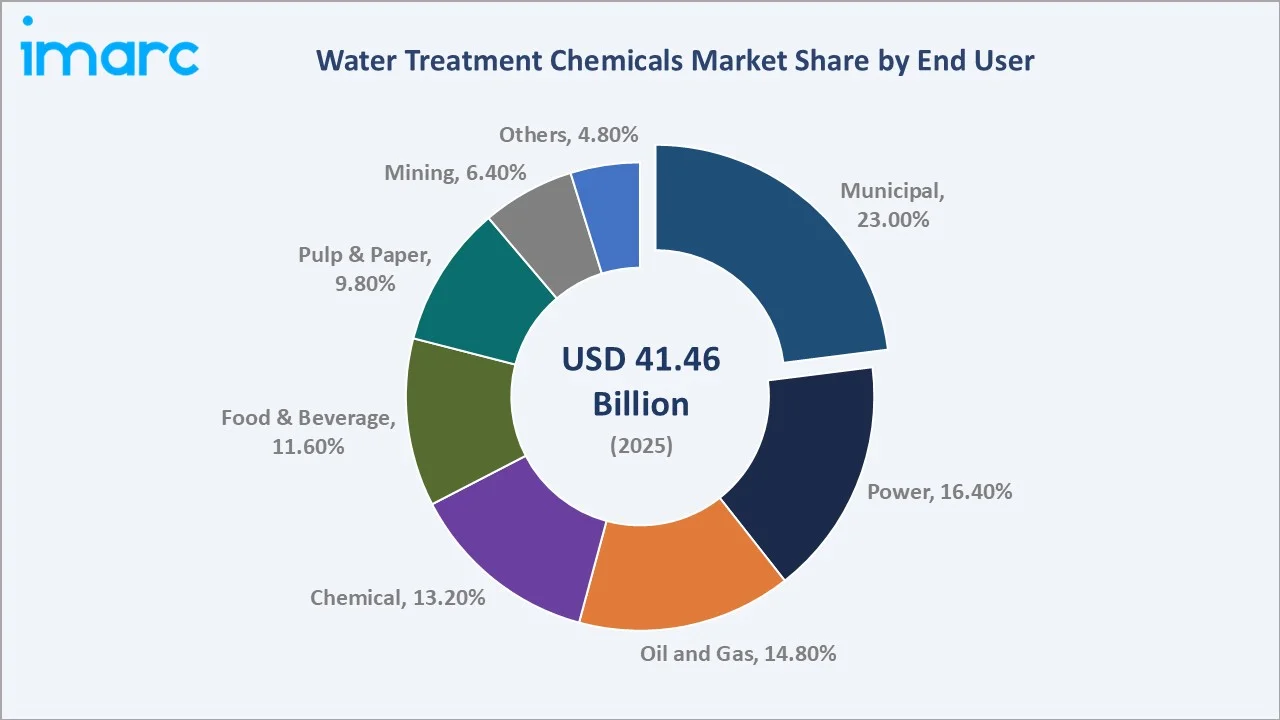

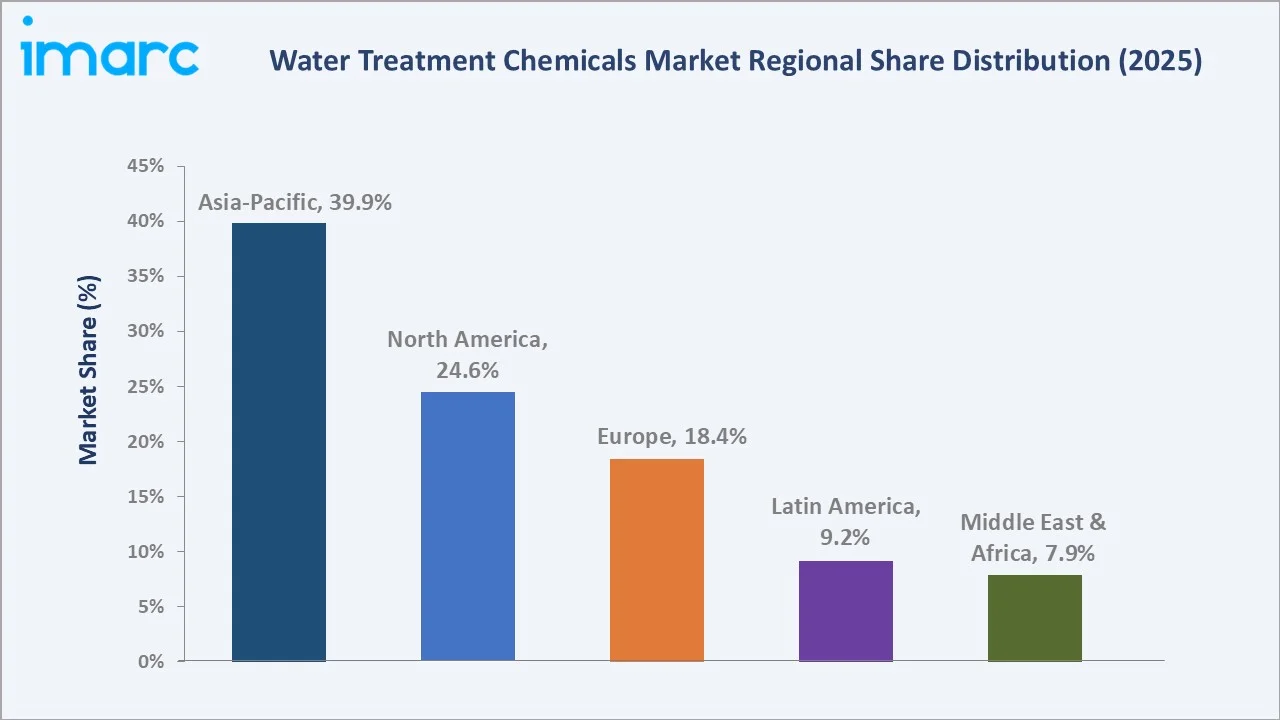

Coagulants and Flocculants dominate the type mix at 36.3% in 2025, while the Municipal segment leads end-user demand at 23.0%. Asia-Pacific commands a 39.9% regional share in 2025, reflecting Asia's vast industrial base and population-driven water treatment needs.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 41.46 Billion |

|

Forecast Market Size (2034) |

USD 59.94 Billion |

|

CAGR (2026-2034) |

4.53% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (39.9% share, 2025) |

|

Leading Type |

Coagulants and Flocculants (36.3%, 2025) |

|

Leading End-User |

Municipal (23.0%, 2025) |

The global water treatment chemicals market growth trajectory from 2020 through 2034, with historical expansion to USD 41.46 Billion in 2025, reflects consistent infrastructure-driven demand, while the forecast to USD 59.94 Billion captures accelerating wastewater reuse investment, industrial growth, and Asia-Pacific urbanization-led demand.

To get more information on this market, Request Sample

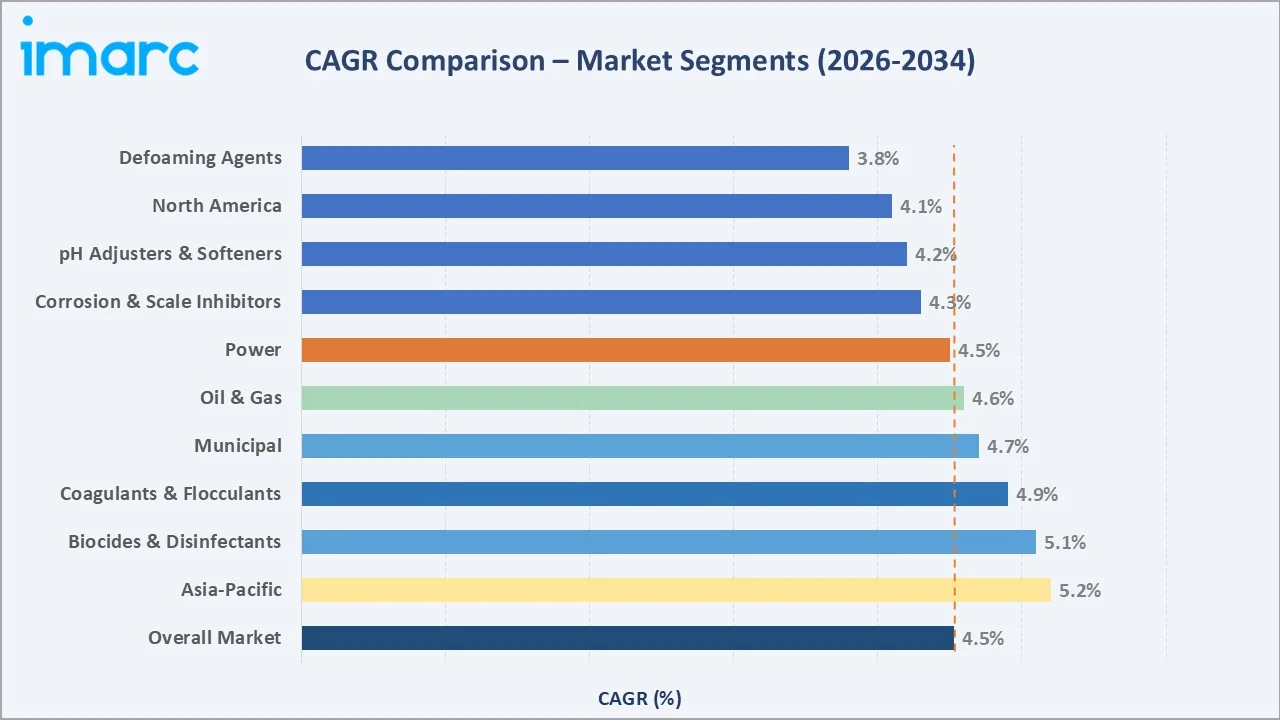

The CAGR trajectories across key type, end-user, and regional sub-segments, with Biocides and Disinfectants at ~5.1% CAGR and Asia-Pacific at ~5.2% CAGR, are the fastest-growing categories within the global water treatment chemicals industry analysis through 2034.

Executive Summary

The global water treatment chemicals market is on a sustained growth trajectory from USD 41.46 Billion in 2025 to USD 59.94 Billion by 2034. Water treatment chemicals are essential additives deployed across municipal, industrial, and commercial water systems to remove contaminants, inhibit corrosion, and ensure regulatory compliance.

Coagulants and Flocculants dominate type at 36.3% in 2025, owing to their indispensable role in primary water clarification across municipal treatment plants and industrial effluent processing globally. Corrosion and Scale Inhibitors (21.6%) command significant share in power generation and oil and gas industries where pipeline integrity and heat exchanger efficiency are critical operational requirements.

Asia-Pacific dominates at 39.9% in 2025, driven by China and India's massive municipal water expansion programs and growing industrial base. North America (24.6%) and Europe (18.4%) follow, driven by infrastructure upgrades and tightening environmental discharge standards.

In September 2025, Kemira expanded its portfolio into industrial water treatment services through the acquisition of Water Engineering, Inc., a U.S.-based specialist in this field. The deal strengthens Kemira’s Water Solutions business by adding service capabilities alongside its existing chemical offerings.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Coagulants and Flocculants – 36.3% share (2025) |

|

Second Type |

Corrosion and Scale Inhibitors – 21.6% share (2025) |

|

Leading End-User |

Municipal – 23.0% revenue share (2025) |

|

Second End-User |

Power – 16.4% revenue share (2025) |

|

Top Companies |

BASF SE, Ecolab Inc., Veolia, Kemira Oyj, Dow Inc., Solenis LLC, SNF Floerger, Kurita Water Industries Ltd., Nouryon |

Key Analytical Observations Expanding On The Above Data:

- Coagulants and Flocculants, with 36.3% in 2025, dominate because they represent the foundational water clarification chemistry across virtually every potable water and industrial effluent treatment process globally, making them the largest volume water treatment chemical category by a significant margin.

- Corrosion and Scale Inhibitors, with 21.6% in 2025, command the second-largest share because power generation, oil and gas, and chemical processing industries rely on these chemistries to protect critical infrastructure, with corrosion-related losses in US industries alone estimated at tens of billions annually.

- Asia-Pacific's 39.9% dominance in 2025 reflects multiple structural forces acting simultaneously, including China's ongoing urbanization requiring massive wastewater treatment investment and India's national clean water access mission (Jal Jeevan Mission) targeting universal rural household water connections.

- North America, with 24.6% in 2025, benefits from aging water infrastructure replacement investment, increasingly stringent EPA effluent discharge regulations, and the extensive industrial base across power generation, oil and gas, and food and beverage sectors requiring sophisticated water treatment programs.

Global Water Treatment Chemicals Market Overview

Water treatment chemicals are specialized chemical formulations applied to raw water, process water, cooling water, and wastewater streams to remove suspended solids, dissolved impurities, biological contaminants, and corrosive agents. Product categories span coagulants, flocculants, biocides, corrosion inhibitors, scale inhibitors, pH adjusters, and defoaming agents.

The global ecosystem integrates raw chemical feedstock producers, specialty chemical manufacturers, formulators and blenders, distribution networks, water treatment service companies, engineering firms, and diverse end-use industries spanning municipal utilities, power generation, oil and gas, chemicals, food and beverage, pulp and paper, and mining.

Market Dynamics

To evaluate market opportunities, Request Sample

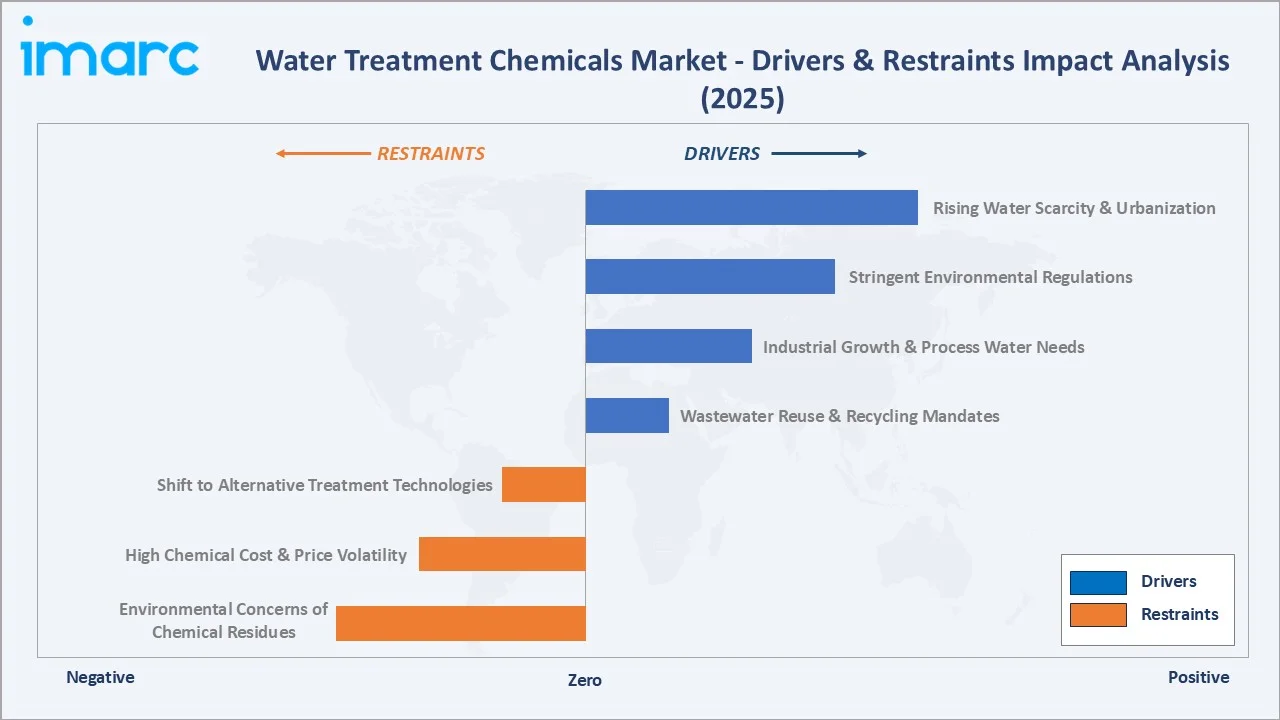

Market Drivers

- Rising Water Scarcity and Urbanization: Rapid global urbanization is intensifying pressure on existing water supply infrastructure, compelling municipalities and industrial operators to invest in advanced water treatment programs. The UN estimates that by 2030, global water demand will exceed supply by 40%, directly driving chemical treatment adoption.

- Stringent Environmental Regulations: Governments worldwide are tightening discharge standards for industrial wastewater, mandating advanced treatment programs that increase the volume and complexity of water treatment chemical dosing. EPA, EU Water Framework Directive, and equivalent Asian regulations are key compliance drivers.

- Industrial Growth and Process Water Demand: Expanding power generation, oil and gas, chemical, and food processing industries worldwide require large volumes of treated process and cooling water, sustaining robust demand for corrosion inhibitors, biocides, and scale inhibitors across industrial sectors.

Market Restraints

- Raw Material Price Volatility: Water treatment chemicals are derived from petrochemical and mineral feedstocks subject to commodity price cycles, creating margin pressure for formulators and cost uncertainty for end-users, potentially slowing adoption of premium chemical programs.

- Environmental Concerns Over Chemical Residues: Increasing regulatory scrutiny over chemical residues in treated water effluents, particularly chlorine-based biocides and certain polymer flocculants, is creating compliance complexity and encouraging exploration of alternative non-chemical treatment technologies.

Market Opportunities

- Wastewater Reuse and Circular Water Economy: Growing freshwater scarcity is accelerating industrial and municipal investment in wastewater recycling and reuse programs, each requiring sophisticated multi-chemical treatment trains to meet reuse quality standards, representing a significant demand expansion opportunity.

- Emerging Market Municipal Infrastructure: Billions of dollars in municipal water treatment infrastructure investment across India, Southeast Asia, Africa, and Latin America is creating large-scale, sustained demand for commodity water treatment chemicals supplying newly commissioned treatment plants.

Market Challenges

- Shift to Alternative Treatment Technologies: Growing adoption of membrane filtration (ultrafiltration, nanofiltration, reverse osmosis), UV disinfection, and advanced oxidation processes in municipal and industrial settings creates competitive pressure on chemical treatment volumes in certain application segments.

- Regulatory Complexity and Product Registration: Water treatment chemical suppliers face increasing complexity in product registration, toxicology documentation, and biocide regulatory approval across multiple jurisdictions (EPA, ECHA, APVMA), adding cost and time-to-market burden for new formulation launches.

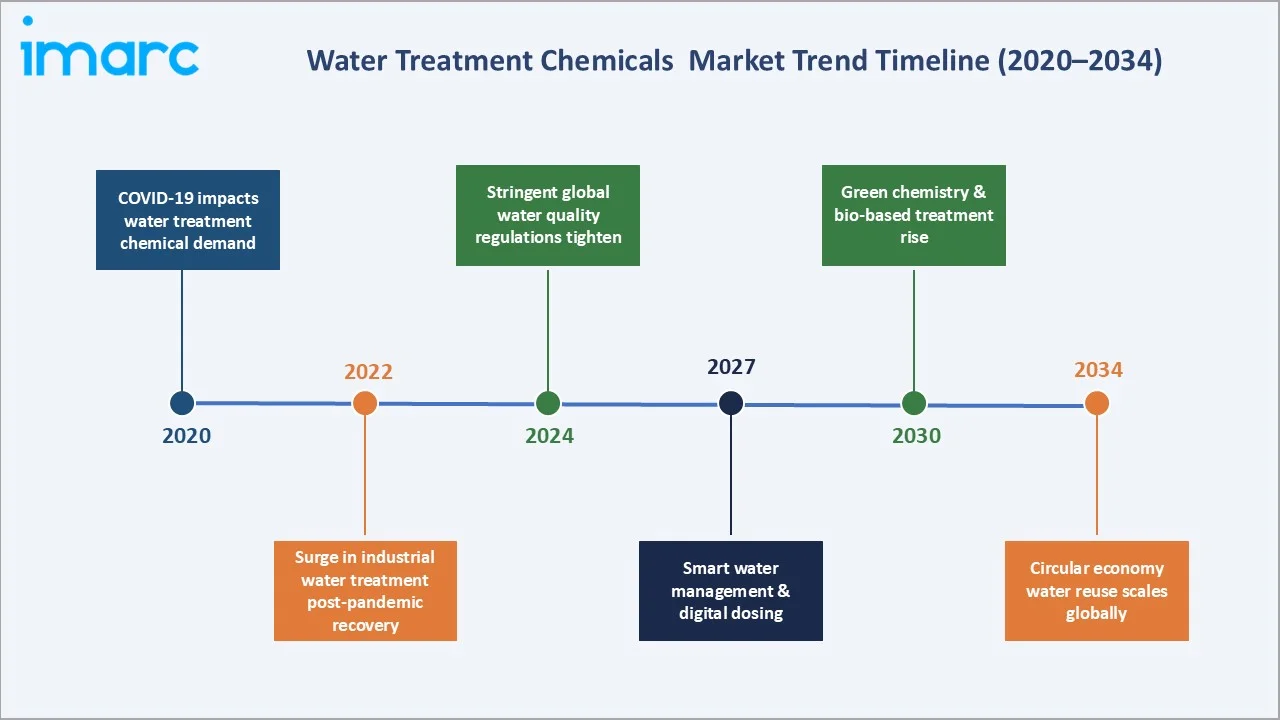

Emerging Market Trends

1. Green and Sustainable Chemistry Replacing Conventional Formulations

Bio-based coagulants derived from plant tannins, chitosan, and moringa seed extracts are gaining commercial traction as environmentally preferred alternatives to synthetic aluminum and iron-based coagulants, particularly in food and beverage and potable water treatment applications where residual chemical concerns are paramount.

2. Digital Water Management and Real-Time Chemical Dosing Optimization

IoT-enabled chemical dosing systems integrated with online water quality sensors are enabling utilities and industrial operators to optimize treatment chemical consumption in real time, reducing chemical usage by 15-25% while maintaining discharge compliance, creating demand for precision chemical programs over bulk commodity chemical supply.

3. PFAS Treatment Driving Specialized Chemical Demand

The global regulatory campaign against PFAS (per- and polyfluoroalkyl substances) contamination in water supplies is creating specialized demand for advanced oxidation chemical treatment systems and granular activated carbon regeneration chemicals as utilities address PFAS removal requirements in drinking water supplies.

4. Decentralized Water Treatment and Modular Plant Adoption

Growing adoption of modular and containerized water treatment plants in mining, oil and gas field operations, and remote industrial sites is creating demand for pre-packaged, field-deployable chemical treatment programs optimized for small-volume, high-performance applications with minimal operator intervention.

Industry Value Chain Analysis

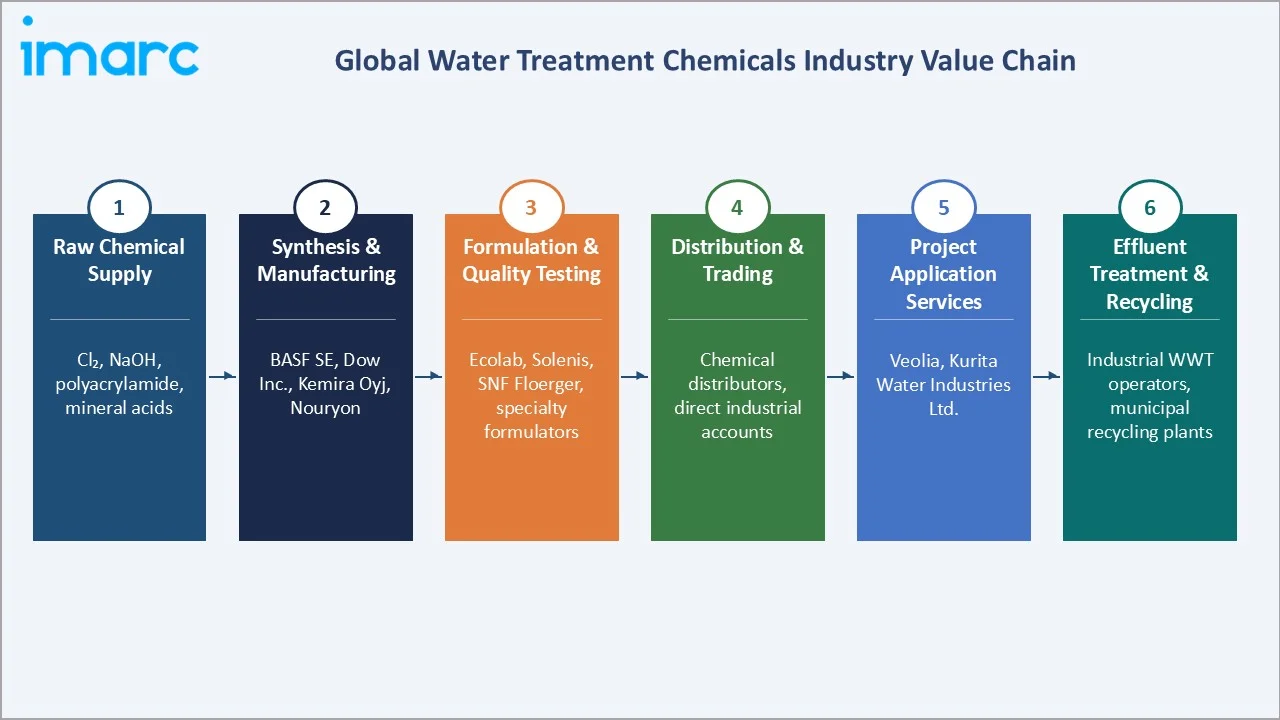

The water treatment chemicals value chain spans six stages from raw chemical feedstock through end-use application. Formulation and application services capture the highest value-add margins, while distribution and large-volume industrial supply generate significant working capital requirements that favor well-capitalized specialty chemical companies.

|

Stage |

Key Players / Examples |

|

Raw Chemical Supply |

Cl2, NaOH, polyacrylamide, mineral acids |

|

Synthesis & Manufacturing |

BASF SE, Dow Inc., Kemira Oyj, Nouryon |

|

Formulation & Quality Testing |

Ecolab, Solenis, SNF Floerger, specialty formulators |

|

Distribution & Trading |

Chemical distributors, direct industrial accounts |

|

Project Application Services |

Veolia, Kurita Water Industries Ltd. |

|

Effluent Treatment & Recycling |

Industrial WWT operators, municipal recycling plants |

Integrated chemical manufacturers with captive production of key active ingredients and proprietary formulation technology, such as BASF SE and Dow Inc., achieve lower material cost bases than pure formulators. This vertical integration is a meaningful competitive advantage in commodity market segments where price competition is intense.

Technology Landscape in the Water Treatment Chemicals Industry

Coagulation and Flocculation Chemistry Advances

High-performance polyaluminum chloride (PAC) formulations with optimized basicity ratios are progressively replacing conventional alum (aluminum sulfate) in municipal water treatment due to superior performance across a wider pH range, reduced sludge volume, and improved turbidity removal efficiency. Cationic polyacrylamide flocculants with tailored molecular weight distributions deliver enhanced settling rates in industrial clarification applications.

Biocide Technology: Oxidizing and Non-Oxidizing Systems

Advanced oxidizing biocide programs combining chlorine dioxide, bromine-based biocides, and monochloramine are replacing simple chlorination in complex cooling water and process water systems to address biofilm control challenges. Non-oxidizing biocides including isothiazolinones, glutaraldehyde, and quaternary ammonium compounds provide targeted microbiological control in systems incompatible with oxidizing chemistry.

Digital Dosing and Smart Treatment Technology

Real-time online water quality analyzers integrated with automated chemical dosing systems are enabling precision chemical addition based on actual influent water quality, replacing fixed-dose programs with demand-responsive dosing that reduces chemical consumption by up to 25% while improving treatment consistency and regulatory compliance documentation.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Coagulants and Flocculants | 36.3% | 2025 |

| End-User | Municipal | 23.0% | 2025 |

| Region | Asia-Pacific | 39.9% | 2025 |

By Type

Coagulants and flocculants command a 36.3% majority share in 2025 owing to their fundamental role as the first treatment step in virtually every water clarification process, from municipal drinking water production to industrial effluent clarification. Their high-volume application across millions of treatment facilities globally makes them the largest tonnage and revenue category within water treatment chemicals.

To access detailed market analysis, Request Sample

Corrosion and Scale Inhibitors at 21.6% in 2025 represent the highest value-per-tonne sub-segment, as these precision-formulated specialty chemicals protect billions of dollars in industrial heat exchanger, pipeline, and cooling tower infrastructure from corrosion and scale deposition. Biocides and Disinfectants (16.8%) are essential across all water systems where microbiological control is a regulatory or operational requirement.

By End-User

The municipal segment dominates end-user demand at 23.0% in 2025, reflecting the scale of global public water supply and wastewater treatment infrastructure, which collectively processes billions of cubic meters of water annually across thousands of treatment facilities. Municipal utilities are the largest single volume consumer of commodity coagulants, flocculants, and disinfection chemicals globally.

The Power segment at 16.4% in 2025 requires sophisticated multi-chemical cooling water and boiler water treatment programs to maintain heat exchanger efficiency, prevent microbiological fouling, and comply with once-through and recirculating cooling water discharge regulations. Oil and Gas (14.8%) relies on specialized injection water treatment, produced water management, and process water conditioning chemical programs.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

39.9% |

China & India municipal expansion; industrial growth; Jal Jeevan Mission |

|

North America |

24.6% |

EPA regulatory tightening; aging infrastructure; industrial sector demand |

|

Europe |

18.4% |

EU Water Framework Directive compliance; industrial efficiency programs |

|

Latin America |

9.2% |

Brazil industrial growth; Mexico manufacturing; infrastructure investment |

|

Middle East & Africa |

7.9% |

GCC desalination; water scarcity-driven treatment; African urbanization |

Asia-Pacific's 39.9% market dominance in 2025 is driven by an exceptional combination of population scale, urbanization pace, industrial expansion, and government-mandated water quality improvement programs. China's municipal water treatment investment and India's Jal Jeevan Mission targeting universal piped water supply to rural households represent the largest single government-driven demand catalysts in the global water treatment chemicals market.

North America, with 24.6% in 2025, is experiencing sustained demand from aging water infrastructure replacement, increasingly stringent EPA PFAS and nutrient discharge regulations mandating advanced chemical treatment programs, and robust industrial water treatment demand from the power generation, oil and gas, and food and beverage sectors operating in the region.

Competitive Landscape

The global water treatment chemicals market is moderately fragmented, with global specialty chemical leaders holding strong multi-regional positions while regional specialists compete effectively in their home markets. The market is served by large diversified chemical companies (BASF, Dow), dedicated water treatment specialists (Ecolab, Veolia), and focused product specialists (SNF Group in flocculants, Kemira in coagulants).

|

Company Name |

Key Products |

Position |

Global Strategic Focus |

|

BASF SE |

Coagulants, biocides, corrosion inhibitors |

Leader |

Global diversified chemical leader |

|

Dow Inc. |

Scale inhibitors, biocides, membrane treatment chemicals |

Leader |

Global; water treatment for industrial & municipal sectors |

|

Ecolab Inc. |

Cooling water, boiler water, wastewater treatment programs |

Leader |

US & global; industrial water treatment services leader |

|

Kemira Oyj |

Coagulants, flocculants, retention aids |

Leader |

Europe & global; pulp/paper & municipal focus |

|

Veolia Water Technologies & Solutions |

Full water treatment chemical programs |

Leader |

Global; integrated treatment services & chemicals |

|

Solenis LLC |

Flocculants (Magnafloc), coagulants, biocides, and hygiene chemicals |

Leader |

Global presence; industrial water & process |

|

SNF Floerger |

Polyacrylamide flocculants, coagulants |

Leader |

Global polyacrylamide leader; municipal & industrial |

|

Kurita Water Industries Ltd. |

Cooling water, boiler treatment, membrane chemicals |

Leader |

Asia-Pacific focus; Japan water treatment leader |

|

Nouryon |

Chelating agents, biocides |

Challenger |

Europe & global; specialty chemical programs |

The competitive positioning of key global water treatment chemicals market participants across global market presence and strategic investment dimensions in 2025. The key players include BASF SE, Dow Inc., Ecolab Inc., Kemira Oyj, Veolia Water Technologies & Solutions, Solenis LLC, SNF Floerger, Kurita Water Industries Ltd., Nouryon, and others.

Key Company Profiles

BASF SE

BASF SE is one of the world's largest chemical companies, headquartered in Ludwigshafen, Germany. Its water treatment chemicals portfolio spans coagulants, biocides, corrosion inhibitors, and scale inhibitors serving municipal and industrial customers across the globe.

- Product Portfolio: Offers polyaluminum chloride, specialty biocides, and corrosion inhibitor programs for industrial water systems.

- Recent Developments: In March 2026, BASF Corporation and Oxidium Technologies LLC announced an agreement to acquire BASF’s Aseptrol technology portfolio. The Aseptrol chlorine dioxide product line is used for water purification, disinfection, and dental line cleaning.

- Strategic Focus: BASF's strategy leverages its global chemical production network and R&D capabilities to develop next-generation green chemistry coagulants and biocides that meet emerging environmental regulations while delivering superior performance.

Ecolab Inc.

Ecolab Inc. is a global leader in water treatment services and specialty chemicals, headquartered in Saint Paul, Minnesota. The company provides integrated cooling water, boiler water, wastewater treatment, and membrane chemical programs to industrial customers across 170+ countries.

- Product Portfolio: Offers comprehensive cooling water treatment, boiler water conditioning, membrane antiscalants, and process water chemical programs for industrial applications.

- Recent Developments: In October 2025, Ecolab introduced a first-of-its-kind direct-to-chip cooling monitoring program in Southeast Asia, launching it in Singapore. The program is designed to improve energy and water efficiency while supporting the growing demand for AI-driven data infrastructure. By integrating monitoring with cooling operations, it enables data centers to enhance performance, reliability, and sustainability across their systems.

- Strategic Focus: Ecolab differentiates through integrated digital water management services bundled with chemical supply, creating long-term customer relationships and differentiated value beyond commodity chemical price competition.

Kemira Oyj

Kemira Oyj is a global chemicals company headquartered in Helsinki, Finland, specializing in water treatment and pulp and paper process chemistry. Kemira is among the world's largest producers of coagulants and flocculants for municipal water treatment globally.

- Product Portfolio: Provides aluminum and iron-based coagulants, polyacrylamide flocculants, retention aids, and specialty chemicals for municipal and industrial water treatment.

- Recent Developments: In September 2024, Kemira is expanding its coagulant production capacity in Norway to address rising demand in the Nordic region. The investment will strengthen supply capabilities and improve delivery reliability for customers across countries such as Norway, Sweden, and Finland. This expansion supports Kemira’s strategy to enhance its water treatment chemical offerings while ensuring consistent product availability and operational efficiency in the region.

- Strategic Focus: Kemira focuses on sustainable chemistry leadership, developing lower-carbon coagulant and flocculant formulations that meet municipal procurement sustainability criteria while maintaining competitive total treatment cost.

SNF Floerger

SNF Floerger is the world's largest producer of water-soluble polyacrylamide polymers, headquartered in Andrézieux-Bouthéon, France. The company dominates the flocculant segment of the global water treatment chemicals market.

- Product Portfolio: Offers a comprehensive range of cationic, anionic, and non-ionic polyacrylamide flocculants for municipal wastewater, industrial water treatment, and mining applications.

- Strategic Focus: SNF maintains global polyacrylamide market leadership through the broadest product grade portfolio, most extensive global manufacturing network, and continuous investment in production technology to maintain cost leadership.

Market Concentration Analysis

The global water treatment chemicals market is moderately fragmented at the global level, with no single company holding more than 8-10% of total global market revenue. Large diversified chemical companies compete alongside specialized water treatment companies and regional product specialists. Market concentration is higher in specific product sub-segments, where SNF Group holds a dominant position in polyacrylamide flocculants and Kemira commands significant share in European coagulant supply.

Consolidation through M&A is ongoing, with large specialty chemical companies acquiring regional water treatment specialists to expand geographic reach and product portfolio breadth. Ecolab's acquisition strategy and BASF's portfolio expansion have created larger, more diversified competitive platforms that compete across multiple chemical categories and geographies simultaneously.

Investment & Growth Opportunities

Fastest-Growing Segments

Biocides and Disinfectants at ~5.1% CAGR through 2034 is the highest-growth type segment, driven by increasingly stringent microbiological standards in municipal drinking water, industrial cooling water, and food processing water applications. Asia-Pacific at ~5.2% CAGR is the fastest-growing regional market through 2034.

Emerging Markets

Latin America and Middle East & Africa represent the fastest-growing emerging market opportunities, driven by large-scale municipal water infrastructure investment, industrial development, and acute water scarcity creating urgent need for water treatment and reuse programs. India's Jal Jeevan Mission and GCC desalination expansion are major investment catalysts.

Venture & Investment Trends

Private equity interest in specialty water treatment chemical companies is growing, reflecting the sector's recurring revenue characteristics, regulatory tailwinds, and infrastructure-linked demand stability. Green chemistry investment targeting bio-based coagulants, enzyme-based biocides, and biodegradable scale inhibitors is attracting significant venture and corporate R&D investment as ESG procurement requirements expand.

Future Market Outlook (2026-2034)

The global water treatment chemicals market is forecast to expand from USD 41.46 Billion in 2025 to USD 59.94 Billion by 2034 at a CAGR of 4.53%. This consistent, sustained growth reflects the market's infrastructure-linked, non-discretionary demand characteristics.

Three structural forces will most significantly shape the water treatment chemicals industry landscape through 2034: accelerating wastewater reuse programs driven by freshwater scarcity across arid regions, PFAS and emerging contaminant regulations mandating advanced chemical treatment programs, and Asia-Pacific industrial expansion generating large-scale new demand for process and cooling water treatment chemistry.

Research Methodology

Primary Research

Primary research encompassed structured interviews with water treatment chemicals industry stakeholders, including senior commercial managers at chemical companies, municipal water utility procurement directors, industrial water treatment engineers, and chemical distribution executives. Primary data validated market sizing, type and end-user segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include UN Environment Programme water quality reports, IEA World Energy Investment Report, WHO Global Water Quality Assessment, US EPA regulatory guidance documents, EU Water Framework Directive implementation reports, World Bank water infrastructure investment data, industry publications including Water Technology, Water & Wastes Digest, and Global Water Intelligence, and chemical industry trade association publications.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, industrial production indices, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Water Treatment Chemicals Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Coagulants and Flocculants, Corrosion and Scale Inhibitors, Biocides and Disinfectants, Ph Adjusters and Softeners, Defoaming Agents, Others |

| End-Users Covered | Municipal, Power, Oil and Gas, Mining, Chemical, Food and Beverage, Pulp and Paper, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BASF SE, Dow Inc., Ecolab Inc., Kemira Oyj, Veolia Water Technologies & Solutions, Solenis LLC, SNF Floerger, Kurita Water Industries Ltd., Nouryon, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the water treatment chemicals market from 2020-2034.

- The water treatment chemicals market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the water treatment chemicals industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Water Treatment Chemicals Market Report

The global water treatment chemicals market reached USD 41.46 Billion in 2025, reflecting consistent demand from global infrastructure investment, industrial expansion, and strengthening water quality regulations.

The market is projected to reach USD 59.94 Billion by 2034, growing at a CAGR of 4.53% during 2026-2034, driven by Asia-Pacific urbanization, wastewater reuse investment, and industrial sector expansion.

Coagulants and Flocculants lead with a 36.3% type share in 2025, valued for their essential role in primary water clarification across municipal and industrial treatment facilities globally.

Municipal leads at 23.0% in 2025, representing the largest volume consumer of commodity water treatment chemicals across thousands of drinking water and wastewater treatment facilities globally.

Asia-Pacific commands a 39.9% market share in 2025, driven by China's industrial scale, India's Jal Jeevan Mission, and broad-based Southeast Asian industrialization generating extensive water treatment chemical demand.

Biocides and Disinfectants is the fastest-growing type at ~5.1% CAGR through 2034, driven by tightening microbiological standards across municipal, industrial cooling water, and food processing water treatment applications.

Leading companies include BASF SE, Dow Inc., Ecolab Inc., Kemira Oyj, Veolia Water Technologies & Solutions, Solenis LLC, SNF Floerger, Kurita Water Industries Ltd., Nouryon, and others.

Key applications include municipal drinking water clarification, industrial cooling water treatment, boiler water conditioning, wastewater treatment and effluent polishing, desalination pretreatment, and process water purification across power, oil and gas, food, and chemical industries.

PFAS contamination regulations are creating specialized demand for advanced oxidation treatment chemicals, activated carbon programs, and PFAS-specific coagulant formulations as utilities worldwide upgrade treatment capabilities to meet emerging PFAS maximum contaminant levels.

Coagulants (typically aluminum or iron salts) destabilize colloidal particles through charge neutralization. Flocculants (typically polyacrylamide polymers) bridge and agglomerate the destabilized particles into settleable flocs. Both are typically used in sequence in water clarification treatment trains.

Asia-Pacific dominates through a combination of China's massive industrial base and wastewater volumes, India's government-mandated water access programs, and Southeast Asian industrial expansion collectively representing the world's largest and fastest-growing regional demand center for water treatment chemicals.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)