Wearable Injectors Market Size, Share, Trends and Forecast by Type, Technology, Application, End Use, and Region, 2026-2034

Global Wearable Injectors Market Size, Share, Trends & Forecast (2026-2034)

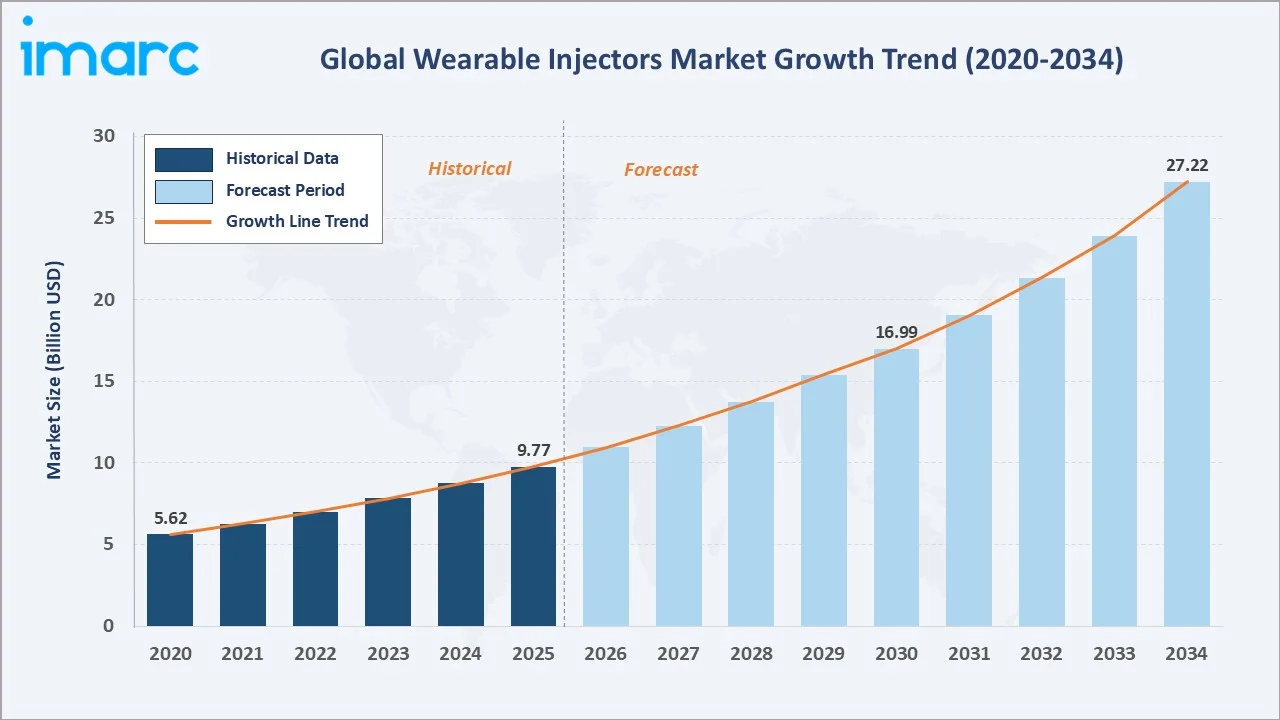

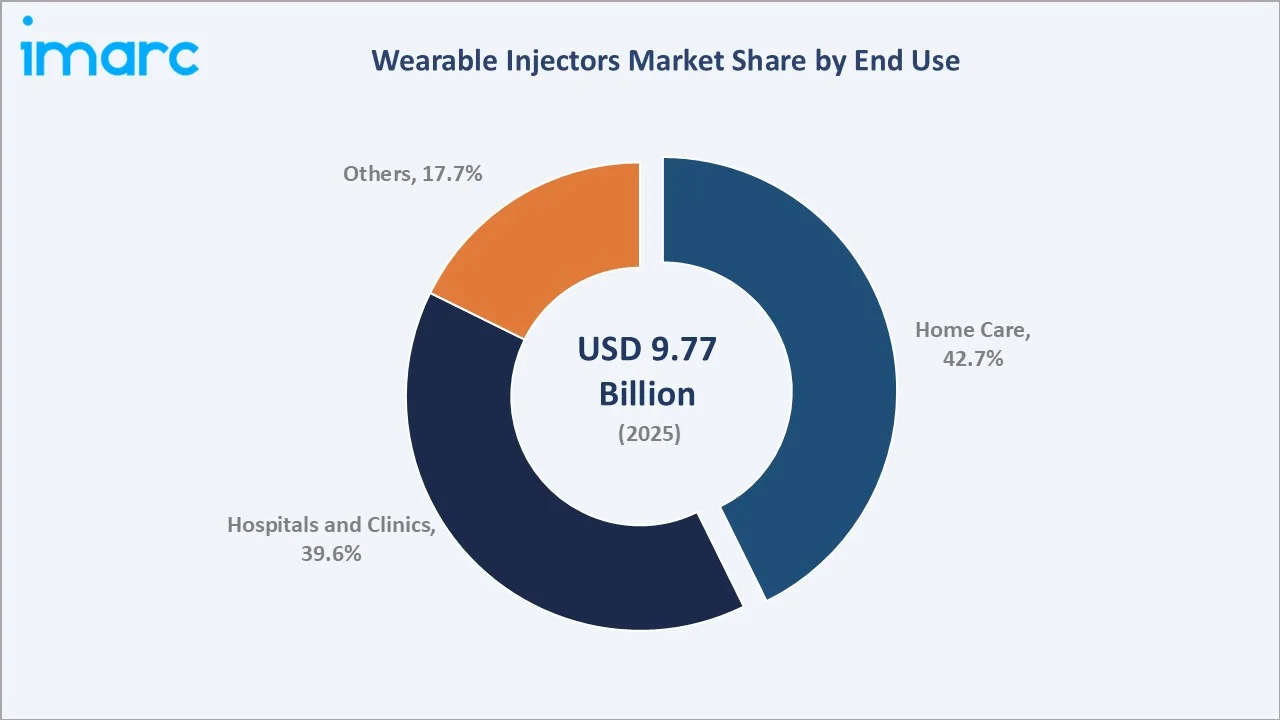

The global wearable injectors market size was valued at USD 9.77 Billion in 2025 and is projected to reach USD 27.22 Billion by 2025, exhibiting a CAGR of 11.69% during the forecast period 2026-2034. Rising prevalence of chronic diseases, accelerating shift of biologic therapy delivery from hospital to home, and growing subcutaneous reformulation of large-volume monoclonal antibodies are driving the wearable injectors market growth. On-body wearable injectors lead the type segment at 63.4% in 2025, while Home Care dominates end use at 42.7%. North America accounts for 34.2% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.77 Billion |

|

Forecast Market Size (2034) |

USD 27.22 Billion |

|

CAGR (2026-2034) |

11.69% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (34.2% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (highest CAGR) |

|

Leading Type |

On-body (63.4%, 2025) |

|

Leading End Use |

Home Care (42.7%, 2025) |

The global wearable injectors market growth trajectory from 2020 through 2034 contrasts a steady historical expansion against a sharper forecast curve, driven by biologic pipeline scale-up, chronic disease burden, and the systemic shift of parenteral drug delivery into home-care settings.

To get more information on this market, Request Sample

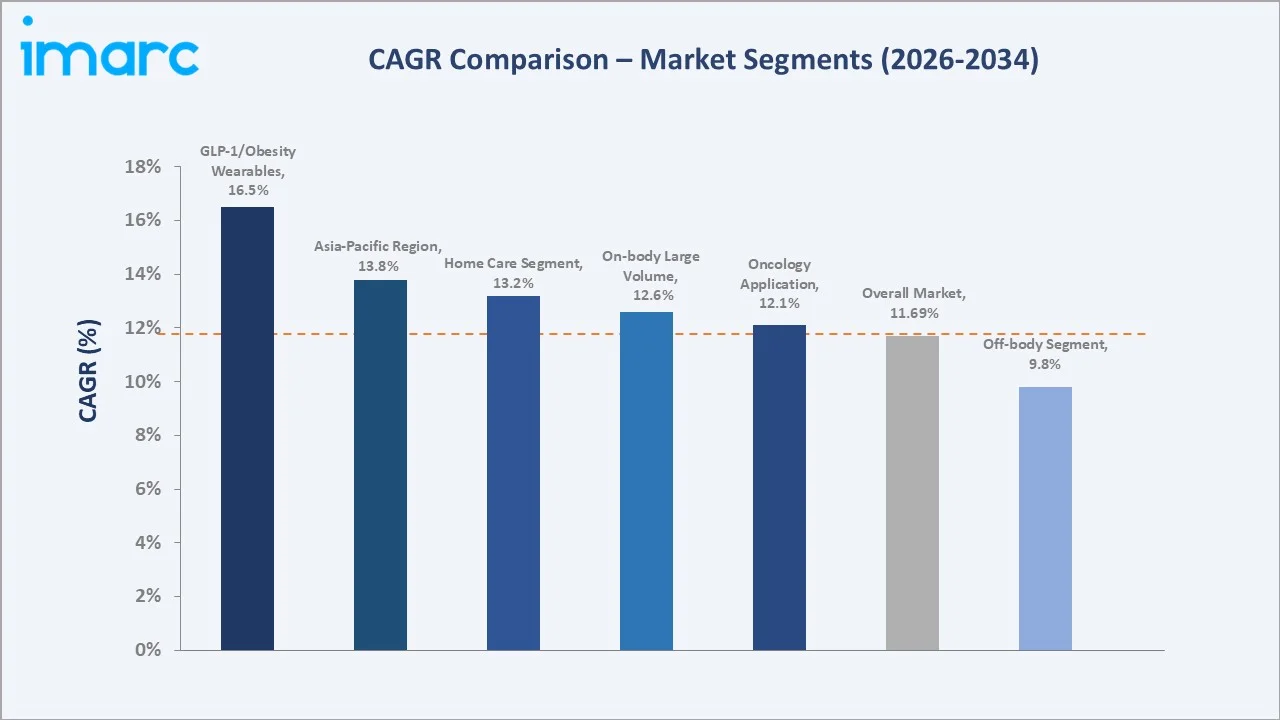

Segment-level CAGR comparisons highlighting GLP-1 wearables and Asia-Pacific as the two fastest-growing pockets within the global wearable injectors industry analysis through 2034.

Executive Summary

The global wearable injectors market is undergoing a structural shift as the life sciences sector pivots toward patient-centric self-administration of biologic therapies. Valued at USD 9.77 Billion in 2025, the market is forecast to reach USD 27.22 Billion by 2034 at a CAGR of 11.69%. Rising biologic drug approvals, expanding subcutaneous reformulation pipelines, and healthcare-system pressure to reduce hospital infusion-chair utilisation are the central structural drivers.

On-body wearable injectors command 63.4% share in 2025, supported by higher patient compliance, larger fluid volume capacity of 10-30 mL, and tighter integration with connected-care platforms. Home Care leads end use at 42.7% in 2025, ahead of Hospitals and Clinics at 39.6%, as payers accelerate the shift of high-cost infusions from hospital to home. Off-body formats hold 36.6%, serving established insulin and specific oncology niches.

North America dominates with 34.2% global revenue share in 2025, led by the United States and its scale-up of GLP-1 and oncology biologic therapies. Asia-Pacific at 27.8% is the fastest-growing region, propelled by diabetes prevalence, local manufacturing expansion, and regulatory modernisation in China, Japan, and India. Europe holds 22.6%, supported by biosimilar adoption and national home-health reimbursement frameworks.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

On-body - 63.4% share (2025) |

|

Leading End Use |

Home Care - 42.7% share (2025) |

|

Leading Region |

North America - 34.2% revenue share (2025) |

|

Second Region |

Asia-Pacific - 27.8% revenue share (2025) |

|

Top Companies |

Becton, Dickinson and Company, Insulet Corporation, West Pharmaceutical Services, Inc., Ypsomed, ENABLE INJECTIONS |

Key Analytical Observations Supporting the Above Data:

- On-body's 63.4% dominance in 2025 reflects the industry-wide shift toward large-volume subcutaneous biologic delivery, particularly for oncology and autoimmune therapies where dose volumes regularly exceed 5 mL.

- Home Care at 42.7% in 2025 is the fastest-expanding end-use pocket, supported by US Medicare home-infusion coverage expansion and the payer push to shift subcutaneous oncology and immunology drugs out of hospitals.

- North America's 34.2% global dominance in 2025 reflects the United States' dual role as the world's largest biologics market AND the most aggressive adopter of home-administered therapy.

Global Wearable Injectors Market Overview

Wearable injectors are body-worn or body-adjacent drug-delivery devices engineered for the subcutaneous administration of large-volume (1-50 mL), high-viscosity biologic therapies over a programmed window of 5 to 45 minutes. The device category bridges the gap between conventional autoinjectors, limited to around 2 mL, and infusion pumps tethered to hospital chairs.

Applications span oncology biologics, chronic autoimmune disorders, cardiovascular therapies (PCSK9 inhibitors), infectious diseases, and insulin delivery. Ecosystem stakeholders include device designers, contract manufacturers, drug-device combination partners (biopharma), payers, specialty pharmacies, home-health agencies, and digital-health platforms.

Macroeconomic enablers include an ageing global population, with over 1 billion people aged 60 and above in 2025 per WHO data, rising chronic-disease prevalence, and the sustained 9-10% annual growth of the global biologics market, generating deep structural demand for large-volume subcutaneous delivery devices.

Market Dynamics

To evaluate market opportunities, Request Sample

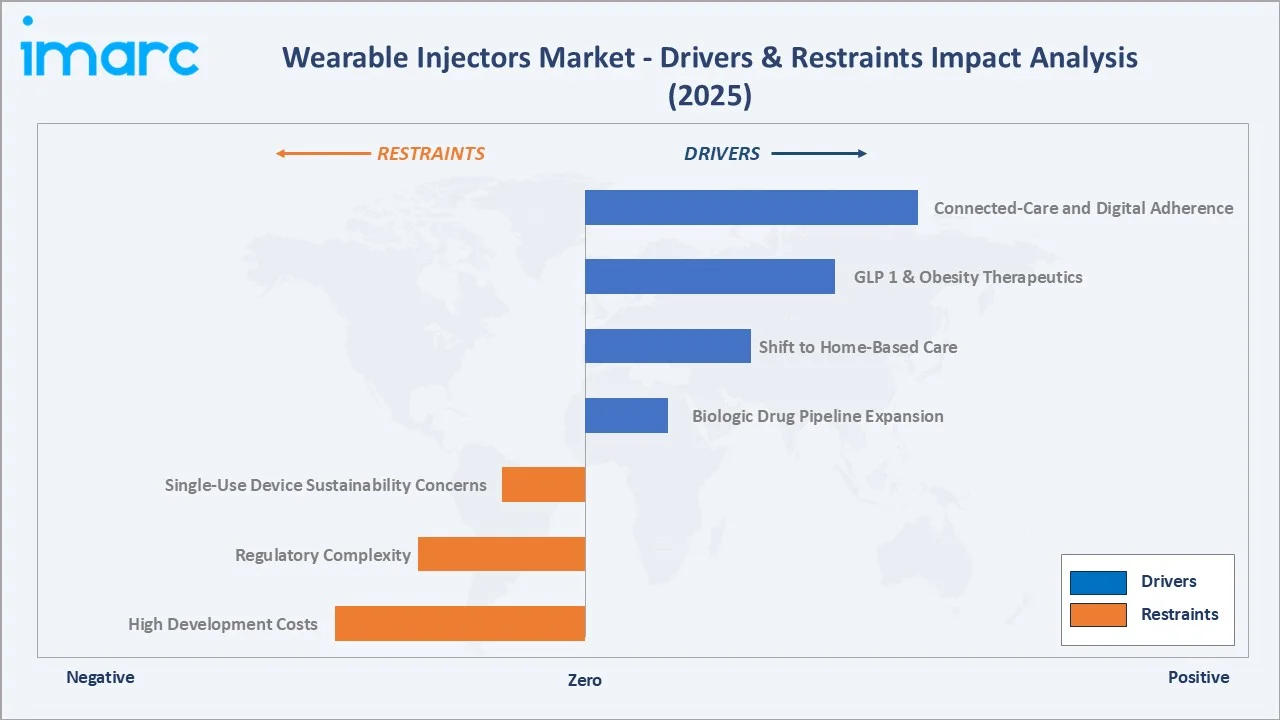

Market Drivers

- Biologic Drug Pipeline Expansion: The global biologics pipeline exceeds 8,000 active candidates in 2025, with more than 400 in late-stage subcutaneous reformulation. Halozyme's ENHANZE platform alone underpins over 10 launched subcutaneous conversions, directly expanding the addressable device market.

- Shift to Home-Based Care: US hospital-infusion costs range from USD 1,500 to USD 3,500 per chair-hour, creating a structural payer incentive to shift therapy to home. CMS Medicare home-infusion benefit expansion from 2021 has accelerated this transition across oncology and autoimmune indications.

- Rising Chronic Disease Burden: WHO estimates global diabetes prevalence reached 830 million in 2022, while cancer incidence is projected to climb to 35 million annual cases by 2050. These volumes translate directly into device unit demand, especially for insulin and oncology wearable formats.

- Connected-Care and Digital Adherence: Next-generation wearable injectors integrate Bluetooth telemetry, injection-confirmation logging, and patient-app dashboards, enabling biopharma to tie reimbursement to real-world adherence evidence.

Market Restraints

- High Development and Combination-Product Costs: A fully validated drug-device combination programme routinely runs USD 50-150 million over 4-6 years, creating a cost barrier for emerging biotech sponsors and constraining overall device-platform diversity.

- Regulatory Complexity of Combination Products: FDA 21 CFR Part 4 and EU MDR dual-track requirements compress launch timelines and increase post-market surveillance burdens. Human-factors validation adds 12-18 months to typical combination-product approval pathways.

- Single-Use Device Sustainability Concerns: Wearable injectors generate non-trivial plastic and electronic waste per dose. Growing ESG scrutiny from European payers is pushing for reusable, recyclable, and primary-container-agnostic designs.

Market Opportunities

- GLP-1 and Obesity Therapeutics: The GLP-1 receptor agonist class, led by semaglutide and tirzepatide, is projected to exceed USD 130 Billion in 2030 sales. Wearable injector formats targeting weekly or monthly dosing represent one of the largest single-indication opportunities in the device category.

- Biosimilar and Generic-Biologic Device Partnerships: As 25+ biologics lose exclusivity through 2030, wearable injector platforms are becoming a differentiation lever for biosimilar sponsors competing on convenience rather than price alone.

- Emerging-Market Scale-Up: China, India, and Brazil together represent over 3 billion patients with limited home-care infrastructure today. Government-led home-health programmes and local-manufacturing incentives are unlocking wearable injector demand across Asia-Pacific and Latin America.

Market Challenges

- Drug-Device Interface Compatibility: High-viscosity biologics above 20 cP require device-specific engineering of needle gauge, drive force, and reservoir material. Any change in formulation triggers expensive device re-validation.

- Reimbursement Fragmentation: Wearable injectors straddle durable medical equipment, specialty pharmacy, and medical-benefit reimbursement frameworks. Misclassification can delay patient access by 3-6 months across the US commercial and Medicare channels.

Emerging Market Trends

1. Large-Volume On-Body Platforms for Oncology and Immunology

Device programmes supporting 10-50 mL subcutaneous delivery are scaling rapidly. Enable Injections' enFuse, West Pharmaceutical's SmartDose 10, and BD Libertas are enabling the subcutaneous conversion of biologics previously restricted to IV infusion, unlocking a multi-billion USD reformulation opportunity.

2. Pre-filled, Fully Disposable Wearables

The market is shifting from reusable battery-driven pumps to fully disposable, pre-filled, single-use wearable cartridges. This model simplifies cold-chain logistics, eliminates patient training complexity, and reduces infection risk, which is critical for immunocompromised oncology patients.

3. Connected Digital Health and Adherence Analytics

BLE-enabled wearables now pair with biopharma-sponsored patient-support apps to capture injection timestamp, dose completeness, and adverse-event signals. Over 40% of new wearable injectors launched between 2023 and 2025 include connectivity, up from under 10% in 2019.

4. GLP-1 and Obesity-Class Dedicated Wearables

With global GLP-1 demand outstripping pen-injector supply in 2024, biopharma sponsors are actively evaluating wearable injector formats for weekly, bi-weekly, and monthly dosing. This single therapeutic class could reshape the device demand curve through 2030.

5. Sustainability-Driven Device Redesign

European procurement frameworks are increasingly scoring devices on lifecycle carbon footprint. Ypsomed's YpsoMate On-Body and Gerresheimer's Gx SensAir programmes are piloting reusable electronic modules with disposable drug-contact cartridges to cut per-dose plastic waste by 60-70%.

Industry Value Chain Analysis

The wearable injectors value chain spans six integrated stages, from primary container supply through end-user home delivery. Each stage demands distinct engineering depth, regulatory competence, and commercial scale.

|

Stage |

Description |

|

Raw Materials & Primary Containers |

Supplies drug-contact glass vials, polymer cartridges, and elastomer closures engineered for biologic stability. |

|

Device Components |

Provides motors, springs, microcontrollers, sensors, and battery systems that power the injection mechanism. |

|

Device Design & Manufacturing |

Engineers and assemble the complete wearable injector platform under ISO 13485 quality-system controls. |

|

Drug-Device Integration (Biopharma) |

Combines the biologic therapy with the wearable platform into a regulated drug-device combination product. |

|

Distribution & Specialty Pharmacy |

Manages cold-chain logistics, prescription fulfilment, and patient onboarding for high-cost biologic therapies. |

|

End Users |

Self-administer subcutaneous biologic therapies across home-care, hospital, and outpatient clinical settings. |

Device manufacturers occupy the strategic midpoint, but biopharma sponsors hold the highest share of end-value as drug-device combination pricing is anchored by the therapy, not the hardware.

Technology Landscape in the Wearable Injectors Industry

Drive Mechanisms

Spring-based systems lead at 35.8% share in 2025 due to low cost and mechanical simplicity. Motor-driven and rotary-pump platforms deliver more precise flow-rate control, which is essential for viscous biologics above 20 cP. Expanding battery chemistry enables very thin form factors ideal for body-worn applications.

Connectivity and Smart Features

Bluetooth Low Energy telemetry, NFC pairing, and integrated accelerometers are now standard on premium wearable platforms. Over 40% of devices launched in 2024 capture injection events and sync with cloud-based adherence dashboards used by biopharma patient-support programmes.

Materials and Primary Container Innovation

Polymer cartridge systems such as SiO2 Materials' Plus+ Technology and Schott toppac are displacing glass for high-viscosity and light-sensitive biologics, reducing breakage risk during home-care handling by an estimated 70-85%.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | On-body | 63.4% | 2025 |

| Technology | Spring-based | 35.8% | 2025 |

| Application | Oncology | 29.5% | 2025 |

| End Use | Home Care | 42.7% | 2025 |

| Region | North America | 34.2% | 2025 |

By Type

On-body wearable injectors command a 63.4% majority share in 2025, reflecting their ability to deliver high-volume biologic doses up to 30 mL directly onto the patient's skin, typically over 5-45 minutes. The on-body architecture has become the preferred format for oncology, autoimmune, and long-acting biologic therapies.

To access detailed market analysis, Request Sample

Off-body wearable injectors hold 36.6% share in 2025. These devices, typically worn on a belt or placed adjacent to the patient, dominate specific niches, including insulin pumps and certain legacy oncology platforms. Off-body systems benefit from longer-life reusable electronics and larger reservoir capacity, though they trade off patient convenience relative to on-body formats.

By End Use

Home Care leads the end-use segment at 42.7% share in 2025, driven by payer-led migration of high-cost biologic infusions out of hospital chairs and into patient homes. US Medicare's home-infusion benefit expansion, alongside European national home-health reimbursement frameworks, is structurally accelerating this segment's share.

Hospitals and Clinics at 39.6% share in 2025 remain the primary channel for device first-dose administration, oncology induction cycles, and therapies requiring clinical observation. The segment is expected to hold a substantial share through the forecast period, though its relative weight will gradually decline as home-care expands. Others (17.7%) encompass ambulatory surgical centres, long-term care facilities, and specialty infusion clinics.

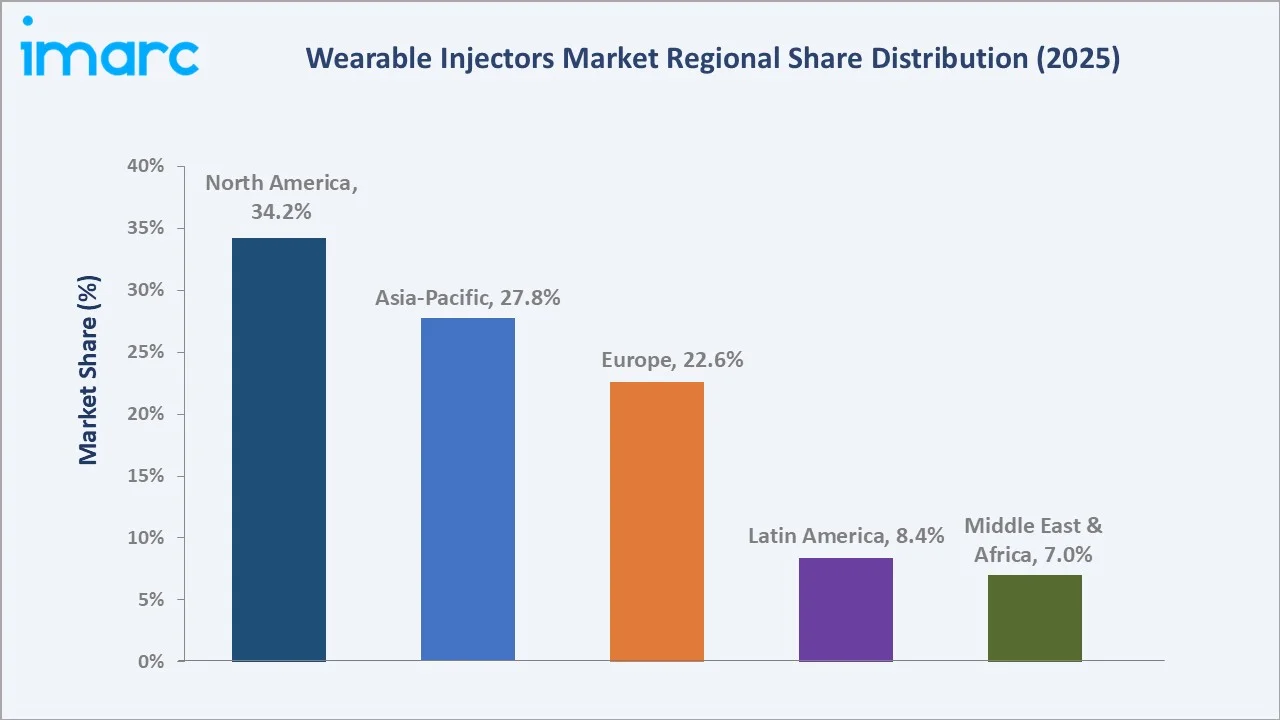

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

34.2% |

US biologics pipeline, Medicare home-infusion, GLP-1 demand |

|

Asia-Pacific |

27.8% |

Diabetes prevalence, local manufacturing scale, NMPA modernisation |

|

Europe |

22.6% |

Biosimilar adoption, EU MDR framework, national home-health schemes |

|

Latin America |

8.4% |

Brazil public-health scale-up, Mexico biosimilar access |

|

Middle East & Africa |

7.0% |

GCC premium-care investment, South Africa oncology expansion |

North America commands a 34.2% global revenue share in 2025, the largest regional position in the global wearable injectors market. The United States is the single most important national market, hosting the world's deepest biologic R&D base, over 900 active biologic INDs, and a commercial payer infrastructure that has aggressively supported home-infusion reimbursement expansion since 2021.

Asia-Pacific at 27.8% in 2025 is the fastest-growing region. China's diabetes patient pool exceeds 140 million, while Japan's ageing demographics and South Korea's biosimilar manufacturing base provide structural demand. India is emerging as both a consumption and a low-cost manufacturing hub for insulin and GLP-1 device platforms. Europe holds 22.6%, led by Germany, the United Kingdom, and France, while Latin America (8.4%) and the Middle East & Africa (7.0%) are smaller but expanding pockets anchored by Brazil, GCC states, and South Africa.

Competitive Landscape

|

Company Name |

Key Brand / Offerings |

Market Position |

Core Strength |

|

Becton, Dickinson and Company |

BD Libertas |

Leader |

Large-volume on-body platform, biopharma partnerships |

|

Insulet Corporation |

Omnipod Go |

Leader |

On-body insulin delivery, subscription distribution |

|

West Pharmaceutical Services, Inc. |

SmartDose |

Leader |

Large-volume on-body, pre-filled cartridge integration |

|

Ypsomed |

YpsoDose |

Leader |

Swiss engineering, biopharma co-development |

|

ENABLE INJECTIONS |

enFuse |

Challenger |

Large-volume vial-to-body, oncology focus |

|

Debiotech SA |

Debiotech on-body injectors |

Emerging |

Precision micro-pump technology, insulin |

|

Sonceboz |

LVI-V, LVI-P |

Emerging |

Mechatronics specialist based in the Canton of Bern |

The wearable injectors competitive landscape is led by a small group of device-platform specialists commanding deep biopharma partnerships, alongside diabetes-focused on-body pure-plays and primary-container companies expanding into full device assembly.

Key Company Profiles

Becton Dickinson and Company (BD)

BD is a global medical-technology company and one of the most strategically positioned suppliers in the wearable injectors market, leveraging decades of drug-delivery expertise and deep biopharma combination-product relationships.

- Product & Platform Portfolio: BD Libertas wearable injector (2-10 mL on-body), BD Evolve autoinjectors, BD Neopak glass prefilled syringes, BD Effivax combination platforms.

- Recent Developments: In July 2025, BD (Becton, Dickinson and Company) announced the first pharma-sponsored combination product clinical trial using the BD Libertas Wearable Injector for subcutaneous delivery of complex biologics.

- Strategic Focus: BD's strategy centres on drug-device combination partnerships with top-10 biopharma sponsors, vertical integration from primary container to finished combination product, and expansion into GLP-1 wearable formats.

Insulet Corporation

Insulet is the global leader in on-body insulin delivery, with its Omnipod platform serving over 400,000 patients across the United States, Europe, and select Asia-Pacific markets in 2025.

- Product & Platform Portfolio: Omnipod 5 Automated Insulin Delivery System, Omnipod DASH, Omnipod GO basal-only system.

- Recent Developments: In June 2024, Insulet Corporation announced that Omnipod 5, compatible with both Dexcom G6 and Abbott FreeStyle Libre 2 Plus continuous glucose monitor (CGM) sensors, is now fully available in the U.K. and the Netherlands for individuals aged two years and older with type 1 diabetes.

- Strategic Focus: Continued Type 2 diabetes expansion, global geographic roll-out beyond North America, and extension of the pay-as-you-go pharmacy-channel distribution model.

Ypsomed AG

Ypsomed is a Swiss drug-delivery specialist with deep expertise in self-injection systems and a rapidly scaling on-body wearable injector portfolio for biopharma combination-product partners.

- Product & Platform Portfolio: YpsoDose pre-filled large-volume patch injector, YpsoMate On-Body, and a broader pen and autoinjector portfolio.

- Recent Developments: In September 2024, Ypsomed celebrated the opening of a new production hall at its German site in Schwerin. The expansion will enable the company to increase its production capacity to meet the growing global demand for high-quality medical technology products.

- Strategic Focus: Capacity expansion, biopharma co-development for GLP-1 and oncology programmes, and sustainability-driven re-design of device platforms.

Market Concentration Analysis

The global wearable injectors market exhibits moderate concentration, with the top five players collectively accounting for an estimated 55-62% of global device-platform revenue in 2025. Becton, Dickinson and Company, Insulet Corporation, West Pharmaceutical Services, Inc., Ypsomed, and ENABLE INJECTIONS represent the strategic core.

At the premium biopharma combination-product tier, consolidation is intensifying as combination-product development costs exceed USD 100 Million per programme and regulatory complexity continues to rise, structurally excluding sub-scale entrants. Parallel fragmentation is visible in insulin-specific on-body segments, where regional specialists and emerging Chinese suppliers are scaling alternative platforms.

Investment & Growth Opportunities

Fastest-Growing Segments

Large-volume on-body formats supporting 10-50 mL subcutaneous biologic delivery are the fastest-growing device sub-segment through 2034. GLP-1 obesity therapeutics represent the single largest addressable indication opportunity, potentially generating USD 4-6 Billion in annual wearable injector pull-through by 2030.

Emerging Market Expansion

China, India, and Brazil are emerging as both demand and manufacturing hubs. Chinese NMPA modernisation, India's PLI scheme for medical devices, and Brazil's SUS-linked biosimilar adoption collectively represent a multi-billion USD addressable expansion through the forecast period.

Venture & Private Investment Trends

Private-market investment in wearable injector start-ups surged in 2023-2024, with notable rounds for Enable Injections, Sonceboz-backed programmes, and multiple diabetes-specific on-body specialists. Strategic biopharma investment is also accelerating, reflecting the device's rising share of end-product economics.

Future Market Outlook (2026-2034)

The global wearable injectors market forecast projects sustained value expansion from USD 9.77 Billion in 2025 to USD 27.22 Billion by 2034 at a CAGR of 11.69%, nearly tripling in value across the forecast window. This trajectory is underpinned by the subcutaneous reformulation pipeline, GLP-1 demand surge, and the structural shift of biologic therapy into home care.

Three discontinuities are likely to reshape the market through 2034: convergence of device platforms with digital-therapeutic apps, widespread adoption of reusable-plus-disposable hybrid device architectures for sustainability compliance, and consolidation of biopharma-device combination partnerships into a smaller set of preferred platform suppliers.

By 2034, wearable injectors are forecast to transition from a specialty drug-delivery niche into the default format for home-administered biologic therapy. The competitive landscape will be shaped by three platform archetypes: large-volume on-body for oncology and immunology, high-frequency insulin and GLP-1 wearables, and connected-device ecosystems integrated with biopharma patient-support programmes.

Research Methodology

Primary Research

Primary research included over 50 structured interviews conducted in 2024-2025 with wearable-injector device engineering leads, biopharma combination-product programme managers, specialty-pharmacy distribution executives, home-health payers, and clinical-trial investigators across oncology and immunology.

Secondary Research

Secondary sources include WHO chronic disease prevalence data, US FDA combination product approvals, EU EMA biosimilar registrations, CMS home-infusion benefit data, IQVIA biologic pipeline analytics, industry association publications, company annual reports, and peer-reviewed drug-delivery literature.

Forecasting Models

Market sizing and projections were derived using combined top-down and bottom-up models, incorporating biologic pipeline conversion rates, chronic-disease patient pools, device unit pricing, and region-specific reimbursement scenarios. Base, optimistic, and conservative cases were modelled to stress-test the outlook.

Wearable Injectors Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | On-body, Off-body |

| Technologies Covered | Spring-based, Motor-driven, Rotary Pump, Expanding Battery, Others |

| Applications Covered | Oncology, Infectious Diseases, Cardiovascular Diseases, Autoimmune Diseases, Others |

| End Uses Covered | Hospitals and Clinics, Home Care, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Becton, Dickinson and Company, Insulet Corporation, West Pharmaceutical Services, Inc., Ypsomed, ENABLE INJECTIONS, Debiotech SA, Sonceboz, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the wearable injectors market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global wearable injectors market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the wearable injectors industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Wearable Injectors Market Report

The global wearable injectors market was valued at USD 9.77 Billion in 2025, driven by rising biologic drug volumes, home-care migration, and chronic disease prevalence.

The market is projected to reach USD 27.22 Billion by 2034, growing at a CAGR of 11.69% during 2026-2034, supported by GLP-1, oncology, and subcutaneous biologic expansion.

On-body wearable injectors lead with a 63.4% share in 2025, driven by large-volume biologic delivery capability and higher patient compliance in home-care settings.

Home Care leads with 42.7% share in 2025, accelerated by payer-led migration of high-cost biologic infusions out of hospitals and into patient homes in the US and Europe.

North America leads with 34.2% share in 2025, led by the United States biologics pipeline, Medicare home-infusion reimbursement, and surging GLP-1 therapy demand.

Key drivers include biologic pipeline expansion, GLP-1 demand, home-infusion reimbursement, chronic disease burden, and connected-care digital adherence platforms.

Oncology is among the fastest-growing applications, anchored by subcutaneous reformulations of monoclonal antibodies such as daratumumab, pertuzumab-trastuzumab, and rituximab.

Leading companies include Becton, Dickinson and Company, Insulet Corporation, West Pharmaceutical Services, Inc., Ypsomed, ENABLE INJECTIONS, Debiotech SA, and Sonceboz.

GLP-1 obesity and diabetes therapies represent a multi-billion USD wearable injector opportunity through 2030, enabling weekly and monthly dosing without pen-injector burden.

Bluetooth-enabled wearables capture injection events and sync with biopharma patient-support apps, allowing reimbursement tied to real-world adherence and outcome evidence.

Key challenges include high combination-product development costs, regulatory complexity under FDA 21 CFR Part 4 and EU MDR, and fragmented reimbursement classification pathways.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)