Wellness Tourism Market Size, Share, Trends and Forecast by Travelers Type, Service Type, Location, and Region 2026-2034

Wellness Tourism Market Size, Share, Trends & Forecast (2026-2034)

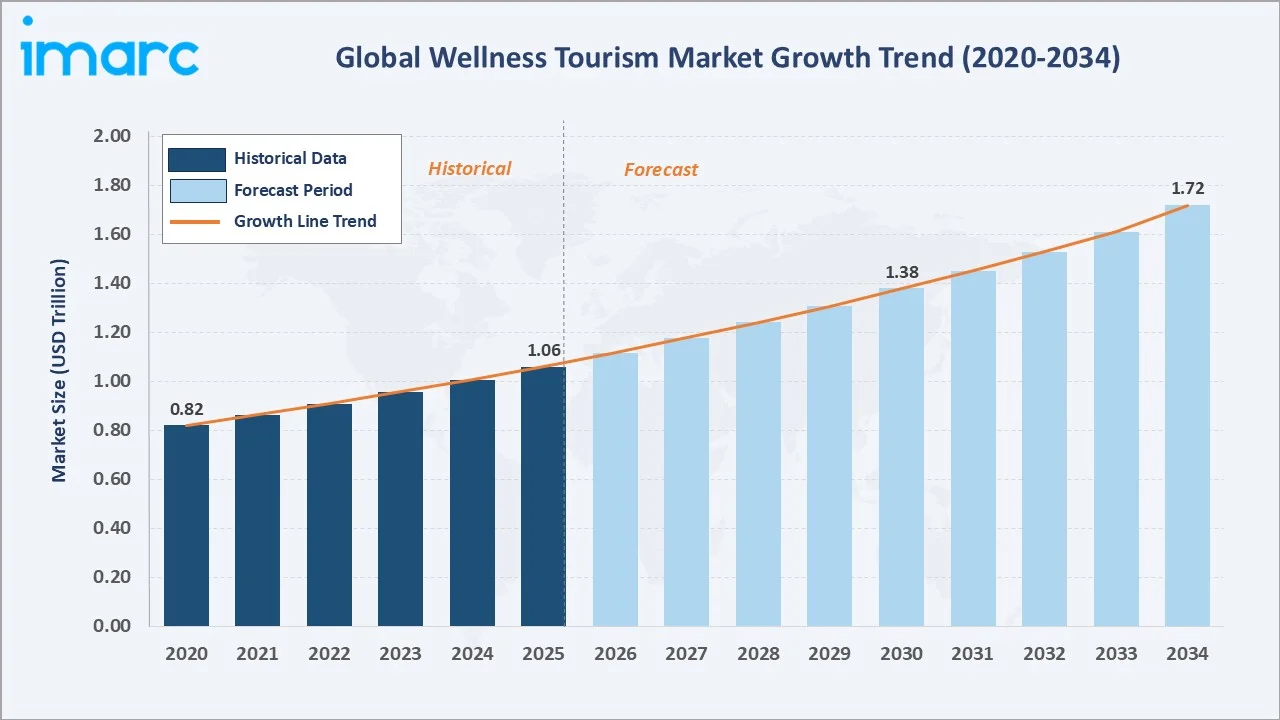

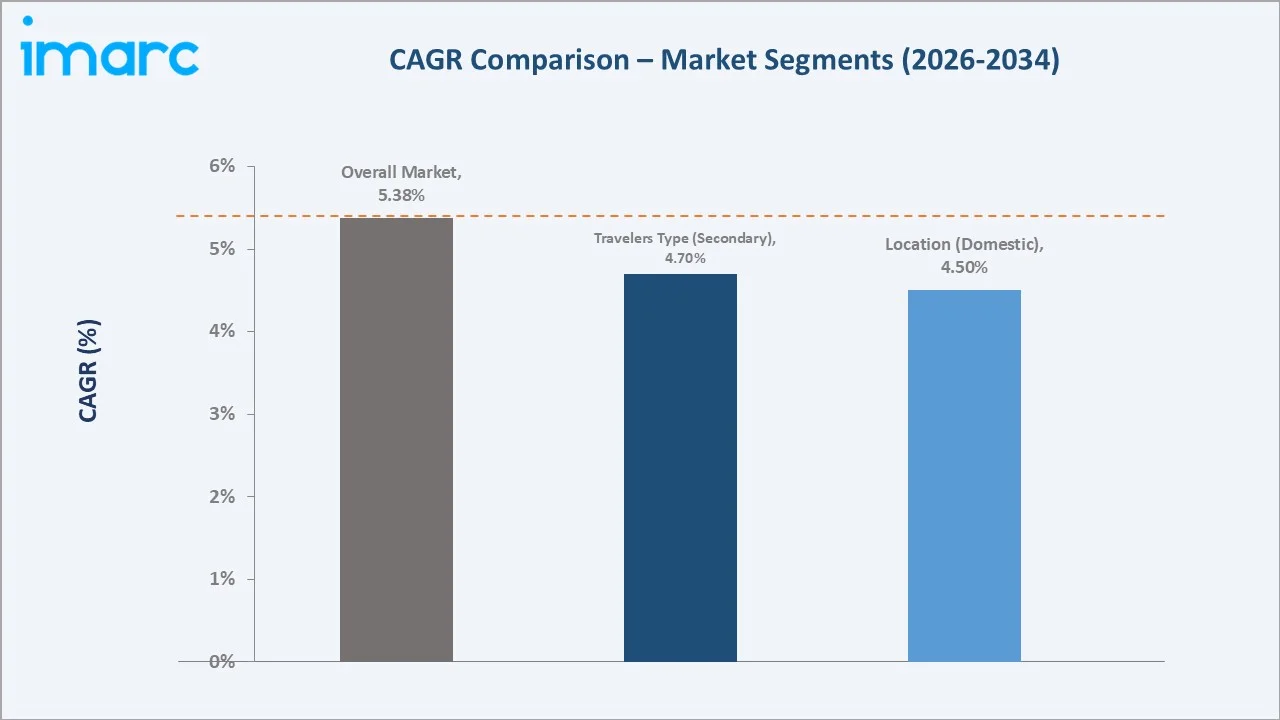

The wellness tourism market was valued at USD 1.06 Trillion in 2025 and is projected to reach USD 1.72 Trillion by 2034, exhibiting a CAGR of 5.38% during 2026-2034. Growing consumer preference for preventive healthcare, stress management, fitness retreats, mindfulness programs, and holistic well-being experiences is driving sustained expansion of the wellness tourism market alongside conventional leisure travel.

Secondary leads the travelers type segment at 67.4%, domestic dominates the location segment at 63.5%, and North America commands 35.8% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.06 Trillion |

|

Forecast Market Size (2034) |

USD 1.72 Trillion |

|

CAGR (2026-2034) |

5.38% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (35.8%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (23.1%, 2025) |

|

Leading Travelers Type |

Secondary (67.4%, 2025) |

|

Leading Location |

Domestic (63.5%, 2025) |

The wellness tourism market expanded from USD 0.82 Trillion in 2020 to USD 1.06 Trillion in 2025, driven by rising health consciousness and growing integration of wellness services into mainstream hospitality. Anchored at USD 1.38 Trillion in 2030, the forecast to USD 1.72 Trillion by 2034 is supported by structural demand growth across both domestic and international wellness travel segments.

To get more information on this market, Request Sample

CAGR trajectories across travelers type and location sub-segments show international and primary expanding faster than the overall 5.38% market CAGR, driven by growing disposable incomes, improved air connectivity, and expanding premium wellness resort development across Asia-Pacific and the Middle East.

Executive Summary

The wellness tourism market is on a robust growth trajectory, expanding from USD 0.82 Trillion in 2020 to a projected USD 1.72 Trillion by 2034. The market has evolved from a niche premium offering to a mainstream travel category as consumers increasingly integrate health, mental well-being, and preventive care into their travel decisions. Investments in purpose-built wellness retreats, medical tourism infrastructure, and digital health platforms are collectively reinforcing this transition across both developed and emerging markets.

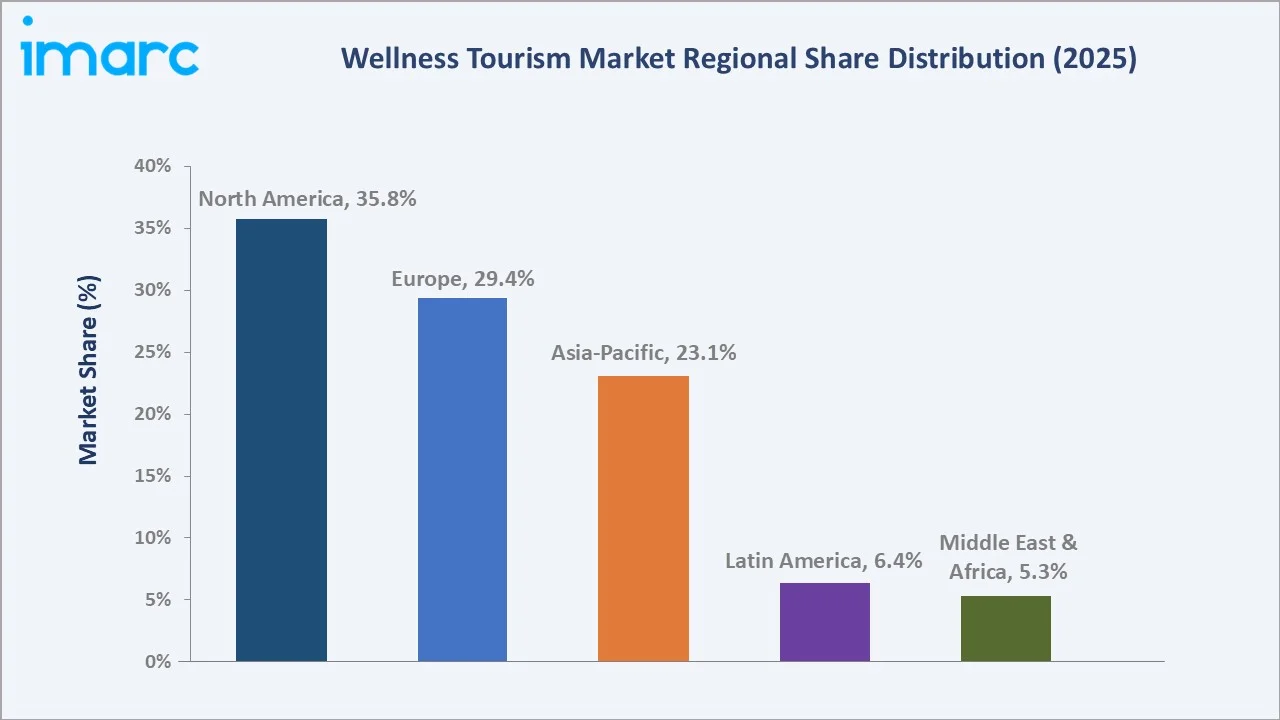

Based on travelers type segment, secondary dominates at 67.4% in 2025, reflecting the mainstream integration of wellness activities into standard leisure and business trips. As per IMARC Group, the global business travel market size reached USD 1.2 Trillion in 2025. Domestic prevails over the location segment with 63.5% share, fueled by growing preference for short-distance wellness retreats and increasing consumer interest in preventive healthcare. North America leads at 35.8% regional share, driven by advanced wellness infrastructure, high health-focused travel spending, and strong demand for holistic tourism experiences.

Key Market Insights

|

Insight |

Data |

|

Leading Travelers Type |

Secondary – 67.4% share (2025) |

|

Second Travelers Type |

Primary – 32.6% share (2025) |

|

Leading Location |

Domestic – 63.5% share (2025) |

|

Second Location |

International – 36.5% share (2025) |

|

Leading Region |

North America – 35.8% share (2025) |

|

Fastest Growing Region |

Asia-Pacific – 23.1% share (2025) |

|

Top Companies |

InterContinental Hotels Group, Jardine Matheson, Aman Group S.a.r.l., Marriott International, Inc., Hyatt Hotels Corporation |

Key Analytical Observations Expanding On The Data Above:

- Secondary at 67.4% represents individuals who incorporate wellness activities, such as spa treatments, yoga, and mindfulness sessions, within broader leisure or business trips, reflecting the mainstreaming of wellness across standard hospitality offerings.

- Primary at 32.6% travel specifically for wellness purposes and are growing at a faster pace than the overall market, driven by rising demand for dedicated wellness retreats, medical health tourism, and immersive therapeutic programs. According to the Indian Ministry of Tourism, in 2025, around 507,244 international visitors visited the country primarily for medical care.

- Domestic leadership at 63.5% is supported by rising preference for short-distance wellness trips, easier travel accessibility, and growing consumer spending on health-focused leisure experiences within home countries.

- International at 36.5% share is the fastest-growing segment, driven by growing cross-border demand for exclusive wellness retreats and destination health programs across Asia-Pacific and the Middle East.

- North America at 35.8% leads the regional landscape, supported by high consumer health expenditure, a well-established wellness resort network, and strong corporate wellness travel demand across the United States and Canada.

Wellness Tourism Market Overview

Wellness tourism encompasses travel undertaken primarily or partly to maintain, enhance, or restore personal well-being. It spans a diverse spectrum of activities including spa and thermal therapy, yoga and meditation retreats, medical and preventive health travel, fitness and adventure wellness, nutrition and detox programs, and mental health escapes. The market sits at the intersection of healthcare, hospitality, and travel, benefiting from structural tailwinds across all three sectors.

The global ecosystem integrates wellness service providers, specialized hospitality operators, technology platforms enabling discovery and booking, travel intermediaries, and a growing network of wellness-certified accommodation providers. Government tourism boards across Thailand, India, Germany, and the United Arab Emirates are actively promoting wellness tourism as a high-value, high-growth segment within their broader national tourism strategies.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

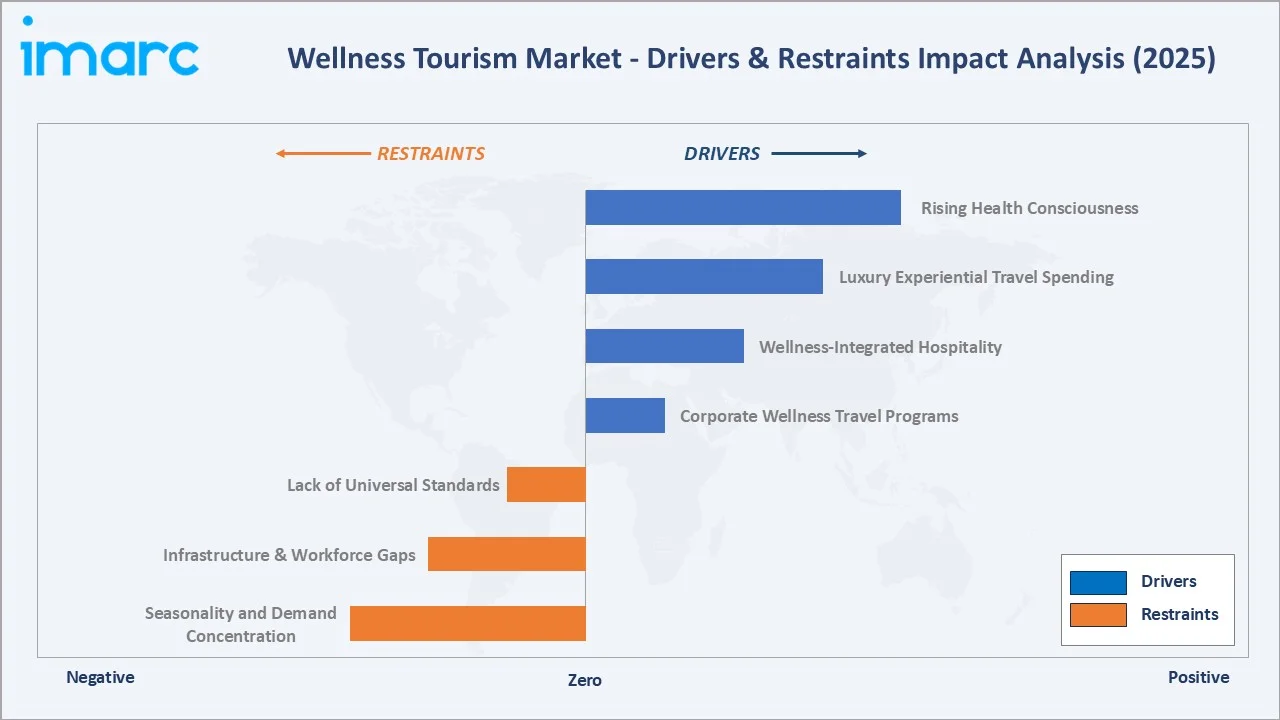

- Rising Health Consciousness and Preventive Healthcare Demand: A fundamental shift in consumer mindsets, from reactive to preventive healthcare, is one of the most powerful demand drivers. The World Health Organization estimated that in 2024, depression and anxiety disorders cost the global economy USD 1 Trillion per year in lost productivity, accelerating demand for mental wellness and stress-recovery travel experiences.

- Growth in Luxury and Experiential Travel Spending: Rising disposable incomes among high-net-worth individuals and expanding affluent middle-class populations, particularly in Asia-Pacific and the Middle East, are fueling demand for premium wellness travel experiences. Consumers are increasingly prioritizing transformative health experiences over material purchases, creating strong demand for luxury wellness retreats and personalized health programs.

- Expansion of Wellness-Integrated Hospitality: Major global hospitality operators are aggressively integrating wellness into core product offerings, developing dedicated spa facilities, wellness floors, and holistic health programs. This mainstream integration substantially expands the addressable market beyond traditional high-end retreat guests to include mid-market leisure and corporate traveler segments.

- Corporate Wellness Travel Programs: Employers across North America, Europe, and Asia-Pacific are investing in corporate wellness travel, including executive health retreats and employee well-being programs, as a strategic tool to reduce burnout, improve productivity, and enhance talent retention, adding a resilient institutional demand layer to the wellness tourism market.

Market Restraints

- Lack of Universal Standards and Certification Frameworks: The sector lacks universally recognized quality standards and certification frameworks, creating challenges for consumers in evaluating the credibility and efficacy of wellness offerings. This absence of standardization can erode consumer confidence and impede the scaling of wellness tourism into mainstream travel segments.

- Infrastructure and Workforce Gaps in Emerging Markets: While emerging economies in Asia-Pacific, Latin America, and Africa present significant growth potential, inadequate wellness infrastructure, limited availability of trained wellness practitioners, and underdeveloped medical tourism support ecosystems constrain the pace of market development in these regions.

- Seasonality and Demand Concentration: Wellness tourism demand remains concentrated in specific seasons and geographic clusters, creating operational challenges around yield management, workforce utilization, and facility capacity planning, particularly for smaller, specialized wellness retreats with limited revenue diversification.

Market Opportunities

- Greenfield Wellness Resort Development: Rapid expansion of wellness tourism infrastructure in Southeast Asia, the Middle East, and sub-Saharan Africa presents significant investment opportunities for global hospitality operators seeking new high-growth markets with favorable consumer and policy tailwinds.

- Digital Health Integration: Growing demand for AI-driven wellness profiling, wearable health monitoring, and telemedicine-supported travel packages creates new product differentiation opportunities for wellness resort operators, enabling measurable health outcome delivery that reinforces premium positioning and repeat visitation.

Market Challenges

- Quality Consistency Across a Fragmented Supply Chain: Maintaining consistent wellness service quality and health outcome delivery across a geographically diverse and highly fragmented global wellness tourism supply chain represents a significant ongoing operational challenge for market operators at all scale levels.

- Evolving Sustainability Expectations: Growing consumer expectation for environmental stewardship, community engagement, and responsible tourism practices among premium wellness travelers is requiring resort operators to make substantial investments in sustainable infrastructure and operations, raising development costs and complexity.

Emerging Market Trends

1. Personalized and Precision Wellness Travel

The convergence of genomics, advanced diagnostics, and data analytics is enabling highly personalized wellness travel programs tailored to individual biometric profiles, health history, and wellness goals. Leading wellness destinations are partnering with health technology firms to offer personalized nutrition, fitness, and recovery programs, fundamentally elevating the perceived value and measurable outcomes of wellness tourism experiences.

2. Sustainability-First Wellness Destinations

Environmental consciousness is reshaping the wellness tourism product landscape, with sustainability and ecological authenticity emerging as key differentiation drivers. Wellness resorts across Asia-Pacific and Europe are investing in carbon-neutral operations, zero-waste hospitality, regenerative agriculture-linked wellness programs, and eco-architecture to align with the values of environmentally conscious high-net-worth travelers.

3. Digital Wellness Integration and Remote Health Connectivity

The proliferation of digital health technologies is creating new hybrid wellness experiences that bridge physical travel and digital health management. Smartphone ownership in the United States rose significantly over the past decade, with around 91% of Americans owning a smartphone in 2025, compared to 35% in 2011, underpinning the infrastructure for app-based wellness planning, real-time biometric monitoring during retreats, and post-trip virtual wellness coaching, thus extending the wellness tourism value chain well beyond the duration of the physical journey.

4. Medical and Preventive Health Tourism

The integration of evidence-based medical services, including executive health screenings, preventive oncology checks, regenerative medicine, and longevity programs, into wellness travel offerings is creating a fast-growing sub-segment. Destinations, such as Switzerland, Thailand, and South Korea, are positioning themselves as global hubs for premium medical wellness tourism, attracting high-value traveler segments seeking comprehensive health evaluation and optimization.

5. Rise of Immersive Cultural and Spiritual Wellness

Authentic, culturally immersive wellness experiences, which are rooted in traditional healing systems, such as Ayurveda in India, Traditional Chinese Medicine, and Japanese Shinrin-yoku, are gaining significant traction among experience-seeking travelers. This trend is creating competitive moats for heritage wellness destinations and supporting premium pricing for authenticity-led offerings in Asia-Pacific and Latin America.

Industry Value Chain Analysis

The wellness tourism value chain spans six interconnected stages, from wellness service design through to post-trip consumer engagement. Wellness program development and on-site guest experience delivery capture the highest value-add, while distribution platforms and tour operator relationships generate downstream competitive advantages across this experience-led category.

|

Stage |

Key Players / Examples |

|

Wellness Service Design |

Holistic health practitioners, wellness program developers, preventive medicine specialists, and destination wellness resort concept designers |

|

Infrastructure & Facilities |

Hospitality developers, resort operators, spa equipment suppliers, wellness resort architects, and thermal and hydrotherapy facility specialists |

|

Distribution & Booking |

Online travel agencies, wellness-focused travel agents, digital booking platforms, and tour operators offering wellness travel packages |

|

Marketing & Promotion |

Tourism boards, hospitality marketing teams, wellness influencers, digital marketing agencies, and corporate wellness travel program managers |

|

Consumer Experience |

On-site wellness coaches, nutritionists, physiotherapists, medical professionals, spa therapists, and fitness instructors delivering guest wellness programs |

|

Post-Trip Engagement |

Digital health platforms, wellness app providers, telemedicine services, and loyalty program teams maintaining guest wellness continuity post-departure |

Vertically integrated players managing both wellness program design and resort delivery infrastructure achieve stronger guest experience consistency and greater pricing power than operators dependent on fragmented third-party wellness service providers.

Technology Landscape in the Wellness Tourism Industry

AI-Driven Personalization and Health Profiling

AI platforms are enabling wellness resorts to deliver deeply personalized programs based on biometric data, health history, and wellness goal profiling. AI algorithms are deployed to customize nutrition plans, fitness regimens, sleep optimization protocols, and therapeutic treatment sequences for individual guests, substantially elevating the perceived and measurable value of wellness travel experiences.

Wearable Health Technology Integration

The integration of wearable devices, including fitness trackers, continuous glucose monitors, and sleep quality sensors, into wellness travel programs is enabling real-time health monitoring and data-driven program adjustments during and after retreat stays. Premium wellness destinations are incorporating wearable health data into program design, creating evidence-based narratives around measurable health improvement outcomes.

Digital Booking and Discovery Platforms

Dedicated wellness travel booking platforms and integrated wellness modules within mainstream online travel agencies are streamlining the discovery, comparison, and booking of wellness travel experiences globally. These platforms are enabling wellness operators to reach new international customer segments beyond their traditional geographic markets while improving yield management and inventory optimization.

Telemedicine and Virtual Wellness Services

The integration of telemedicine capabilities, including pre-travel health consultations, on-retreat virtual specialist access, and post-trip follow-up care, is extending the health service continuum of wellness tourism. This integration supports the development of comprehensive medical wellness travel packages that appeal to health-conscious, high-net-worth traveler segments.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Travelers Type | Secondary | 67.4% | 2025 |

| Service Type | 🔒 | 🔒 | 2025 |

| Location | Domestic | 63.5% | 2025 |

| Region | North America | 35.8% | 2025 |

By Travelers Type

Secondary commands a 67.4% majority share in 2025, driven by the mainstream integration of wellness activities, including spa treatments, yoga sessions, fitness facilities, and healthy dining options, into standard leisure and business travel itineraries across the broader hospitality sector. These travelers represent individuals for whom wellness is an important but not exclusive component of their travel experience.

To access detailed market analysis, Request Sample

Primary at 32.6% in 2025represent individuals who travel specifically for wellness purposes and are growing at a faster pace than the overall market. This segment commands higher per-trip spend and stronger destination loyalty, representing the core demand driver for purpose-built wellness retreat operators and destination health program providers globally.

By Location

Domestic accounts for 63.5% of the location segment in 2025, reflecting the strong and consistent demand for accessible wellness experiences within travelers' home markets. The expansion of day spas, urban wellness centers, and short-break retreat offerings in proximity to major population centers continues to support robust domestic wellness tourism volume across all regions.

LOM1International at 36.5% is the faster-growing location segment. Expansion is driven by increasing cross-border travel for premium wellness retreats, destination health programs, and culturally authentic wellness experiences unavailable domestically. Thailand, India, Switzerland, and Bali are among the most sought-after international wellness destinations globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

35.8% |

High health consciousness, well-established wellness resort infrastructure, and strong corporate wellness travel demand |

|

Europe |

29.4% |

Thermal spa traditions, government-supported wellness tourism frameworks, and a mature luxury retreat ecosystem |

|

Asia-Pacific |

23.1% |

Rich wellness heritage, rapidly expanding wellness infrastructure, and rising health awareness among growing middle-class populations |

|

Latin America |

6.4% |

Emerging eco-wellness destinations, biodiversity-based wellness offerings, and growing medical tourism infrastructure |

|

Middle East and Africa |

5.3% |

Luxury wellness resort development, government tourism diversification strategies, and rising health tourism investment |

North America at 35.8% in 2025leads the global market, driven by robust consumer health expenditure, a large concentration of dedicated wellness resorts across the United States, and strong institutional demand from corporate wellness travel programs. Well-developed wellness-certified hospitality infrastructure and high consumer health consciousness are further supporting sustained market leadership.

Asia-Pacific at 23.1% is the most dynamic regional growth market through 2034. Strong government tourism investment, rich traditional wellness heritage spanning Ayurveda, Traditional Chinese Medicine, and Thai therapeutic traditions, and rapidly rising domestic health awareness among the region's expanding middle class are collectively driving accelerating wellness tourism growth across Thailand, India, Japan, and Indonesia.

Competitive Landscape

The wellness tourism market is moderately fragmented, with global hospitality groups competing alongside regional wellness retreat operators and destination-focused service providers. Brand positioning, integrated wellness offerings, and resort infrastructure remain key competitive differentiators.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

InterContinental Hotels Group |

Six Senses Hotels Resorts Spas |

Leader |

Premium immersive wellness; sustainability focus; global retreat expansion |

|

Jardine Matheson |

Mandarin Oriental Hotel Group |

Leader |

Luxury urban and resort spa operations; holistic guest wellness experience |

|

Aman Group S.a.r.l. |

Aman Spa |

Leader |

Ultra-luxury destination wellness; exclusive retreat programming and positioning |

|

Marriott International, Inc. |

Ritz-Carlton Spa |

Challenger |

Broad-portfolio wellness integration; global distribution network and scale |

|

Hyatt Hotels Corporation |

Miraval Resorts and Spas |

Challenger |

Dedicated wellness retreat operations; mindfulness and well-being programming |

Key players include InterContinental Hotels Group, Jardine Matheson, Aman Group S.a.r.l., Marriott International, Inc., and Hyatt Hotels Corporation, among others.

Key Company Profiles

InterContinental Hotels Group

InterContinental Hotels Group is one of the world's leading hospitality companies. IHG's acquisition of Six Senses Hotels Resorts Spas in 2019 added one of the most acclaimed luxury wellness resort brands globally to its portfolio. Six Senses Hotels Resorts Spas delivers immersive, sustainability-led wellness programming, including sleep optimization, biohacking, detox retreats, and longevity programs, from properties in remote, high-beauty natural settings across Asia, Europe, and the Middle East.

- Product Portfolio: Six Senses Hotels Resorts Spas, IHG Hotels & Resorts loyalty ecosystem, wellness-integrated room and dining concepts

- Recent Developments: IHG continues to expand the Six Senses portfolio as a strategic growth driver, announced additional Six Senses properties across new markets, and is integrating wellness programming across broader IHG brand tiers to capture mid-market wellness demand.

- Strategic Focus: Premium wellness resort expansion; sustainability leadership; integration of wellness across broader IHG brand portfolio.

Jardine Matheson

Jardine Matheson is one of Asia's most established conglomerates. Jardine Matheson completed the full acquisition of Mandarin Oriental in January 2026, taking the brand fully private to accelerate its global expansion strategy.

- Product Portfolio: Mandarin Oriental Hotel Group spa and wellness facilities across all properties, holistic wellness dining and fitness programming, branded residences with integrated wellness amenities.

- Recent Developments: In February 2025, Mandarin Oriental Hotel Group, a subsidiary of Jardine Matheson, revealed plans to manage a new luxury hotel in Suzhou, China, expected to debut in 2026. Comprehensive spa and wellness amenities will showcase Mandarin Oriental’s renowned signature spa treatments, offering a wide array of wellness, beauty, and massage services.

- Strategic Focus: Luxury hotel and spa excellence; holistic wellness positioning; accelerated global expansion under full private ownership.

Marriott International, Inc.

Marriott International, Inc. is among the largest hotel companies. Within the wellness tourism segment, Marriott's primary offering centers on Ritz-Carlton Spa, delivering luxury spa and wellness experiences across its premium resort portfolio. Marriott is progressively integrating wellness programming, including sleep health, nutritional wellness, and mindfulness, across its broader brand portfolio.

- Product Portfolio: Ritz-Carlton Spa; spa and wellness facilities across JW Marriott and Westin brands

- Recent Developments: Marriott has expanded wellness-focused programming across its resort collection and continues to develop wellness floor concepts across flagship urban and resort properties.

- Strategic Focus: Broad-portfolio wellness integration; global distribution scale; wellness-linked loyalty programming across several hotel brands.

Market Concentration Analysis

The wellness tourism market exhibits a moderately fragmented competitive structure globally, with a small number of premium hospitality groups occupying leadership positions in the luxury wellness travel segment while a vast and diverse ecosystem of independent wellness resorts, boutique retreat operators, day spa networks, and wellness-integrated hotels serves the broader mid-market and emerging segments.

Barriers to entry include high capital investment requirements, the need for integrated wellness infrastructure, established hospitality partnerships, and the ability to deliver consistent, personalized wellness experiences across multiple destinations, favoring well-established operators with strong brand recognition and service networks.

Consolidation activity is expected to accelerate over the forecast period, as large hospitality groups seek to acquire differentiated wellness brands to bolster premium positioning. Technology-driven aggregators and wellness travel platforms are also emerging as consolidating forces in the fragmented discovery and booking layer of the value chain.

Investment & Growth Opportunities

Fastest-Growing Segments

International at 36.5% expands faster than the overall 5.38% market CAGR through 2034, driven by growing cross-border demand for exclusive wellness retreats and destination health programs across Asia-Pacific and the Middle East. Primary at 32.6% represents the fastest-growing travelers type category, commanding higher per-trip spend and stronger destination loyalty.

Emerging Markets

Asia-Pacific at 23.1% is among the highest-growth regions, with Thailand, India, and Bali driving international wellness tourism arrivals. Latin America and the Middle East and Africa represent significant untapped growth opportunities as rising disposable incomes, improved wellness infrastructure, and government-led tourism strategies accelerate market development across Mexico, Brazil, the United Arab Emirates, and Saudi Arabia.

Venture & Investment Trends

Investment is concentrated in AI-driven wellness travel personalization platforms, premium wellness resort development in Asia-Pacific and the Middle East, digital health technology integration for wellness travel, and corporate wellness travel program management platforms. Capital is also expanding into sustainable wellness resort development and evidence-based longevity program operators as investor appetite for high-margin, differentiated wellness travel assets continues to grow.

Future Market Outlook (2026-2034)

The wellness tourism market is forecast to expand from USD 1.06 Trillion in 2025 to USD 1.72 Trillion by 2034 at a CAGR of 5.38%, adding significant incremental market value over the forecast period as wellness travel transitions from a premium niche to a mainstream global travel category.

Four forces will shape the market through 2034: AI-driven personalization unlocking precision wellness programming at scale; sustainability-first resort development meeting the environmental expectations of premium travelers; corporate wellness travel institutionalizing well-being investment; and the democratization of wellness travel through mid-market product development and technology-driven cost reduction in wellness service delivery.

By 2034, wellness is expected to be a standard, non-negotiable amenity across the premium and upper-upscale hospitality segments globally. Purpose-built destination wellness resorts will represent the highest-growth niche, with international wellness tourism outpacing domestic growth, supported by improving global air connectivity, rising cross-border health tourism flows, and continued development of world-class wellness infrastructure across Asia-Pacific and the Middle East.

Research Methodology

Primary Research

Primary research included in-depth interviews with senior executives at leading wellness resort operators, hospitality group strategy directors, corporate wellness travel managers, health and wellness practitioners, and institutional tourism investors, validating market sizing, segment share estimates, regional demand dynamics, and competitive positioning assessments across the wellness tourism market.

Secondary Research

Secondary sources encompassed Global Wellness Institute reports, World Health Organization global health statistics, World Tourism Organization travel data, government tourism board publications, company annual reports and investor presentations from listed hospitality operators, industry trade publications, and peer-reviewed academic journals covering health tourism and preventive healthcare trends.

Forecasting Models

Market forecasts used top-down and bottom-up modeling approaches combining wellness travel trip volume projections, average spend per trip by segment, wellness resort capacity expansion pipelines, and segment-level CAGR differentials. Scenario analysis addressed macroeconomic variability, exchange rate impacts on international tourism flows, and regulatory changes affecting medical wellness tourism across key markets.

Wellness Tourism Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Trillion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Travelers Types Covered | Primary, Secondary |

| Service Types Covered | Transport, Lodging, Food and Beverage, Shopping, Activities and Excursion, Others |

| Locations Covered | Domestic, International |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | InterContinental Hotels Group, Jardine Matheson, Aman Group S.a.r.l., Marriott International, Inc., Hyatt Hotels Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the wellness tourism market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global wellness tourism market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the wellness tourism industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Wellness Tourism Market Report

The wellness tourism market was valued at USD 1.06 Trillion in 2025, driven by rising health consciousness and the deepening integration of wellness into mainstream hospitality offerings globally.

The market is projected to grow at a CAGR of 5.38% from 2026 to 2034, reaching USD 1.72 Trillion, supported by structural demand growth across both domestic and international wellness travel segments.

Secondary leads at 67.4% in 2025, representing individuals who incorporate wellness activities within broader leisure or business trips.

Domestic accounts for 63.5% of the location segment in 2025, driven by strong consumer preference for accessible local wellness experiences.

North America commands 35.8% in 2025, led by the United States, fueled by mature wellness resort infrastructure and high consumer health expenditure. Asia-Pacific at 23.1% is the fastest-growing region through 2034.

Leading players include InterContinental Hotels Group, Jardine Matheson, Aman Group S.a.r.l., Marriott International, Inc., and Hyatt Hotels Corporation.

Key drivers include rising global health consciousness, growing preventive healthcare demand, expansion of luxury experiential travel spending, corporate wellness travel growth, and mainstream integration of wellness into premium hospitality offerings worldwide.

Primary restraints include the high cost of premium wellness travel limiting accessibility, absence of universal wellness tourism quality standards, infrastructure and workforce gaps in emerging markets, and seasonal demand concentration challenges for wellness operators.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade