White Cement Market Size, Share, Trends and Forecast by Type, Application, and Region 2026-2034

Global White Cement Market Size, Share, Trends & Forecast (2026-2034)

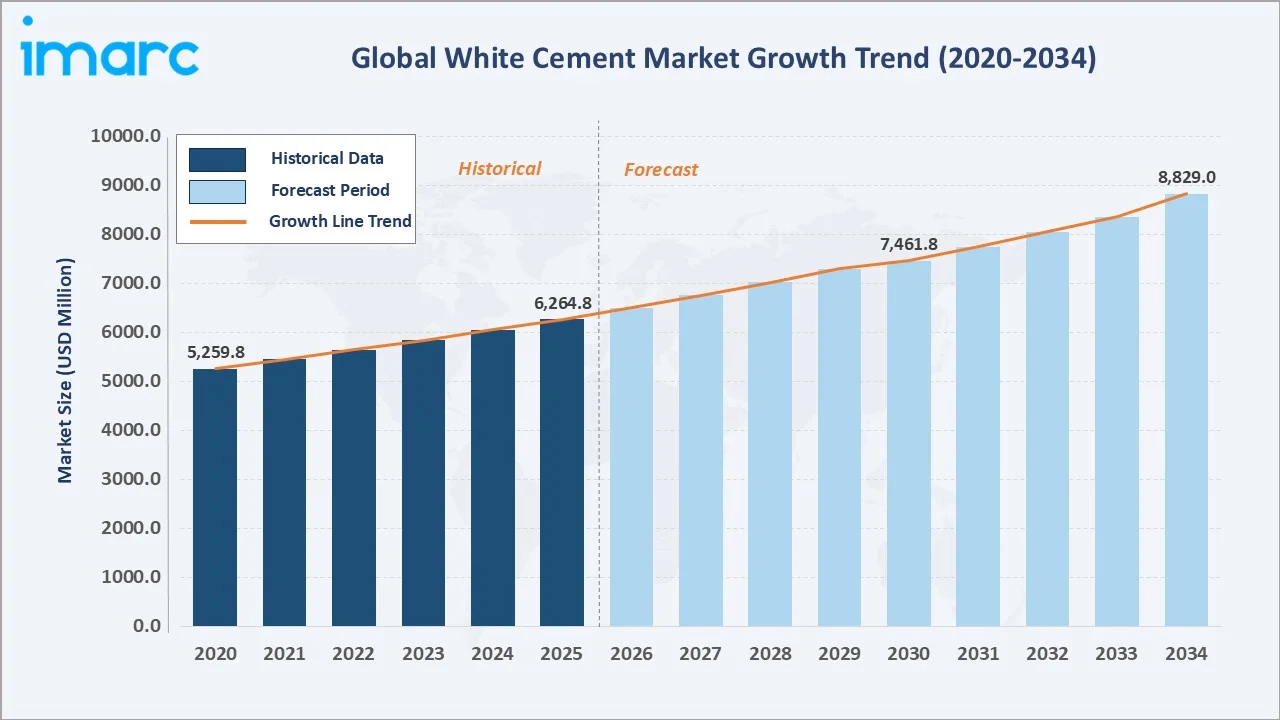

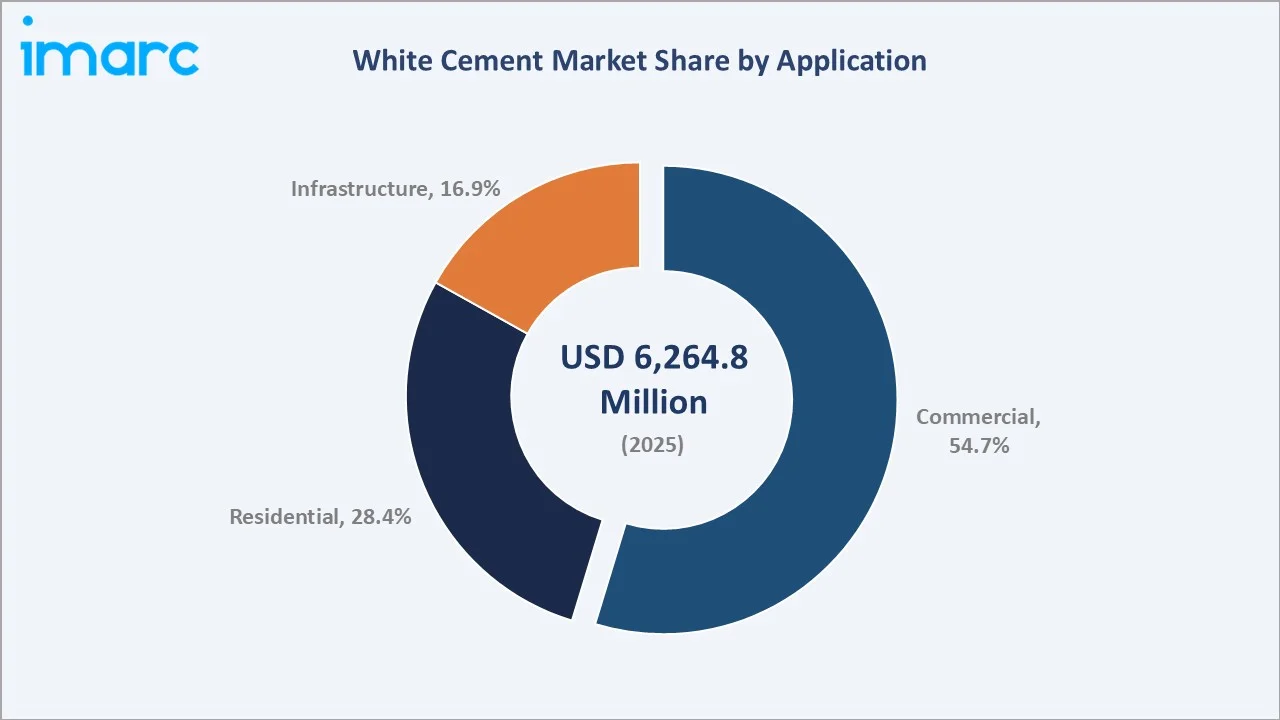

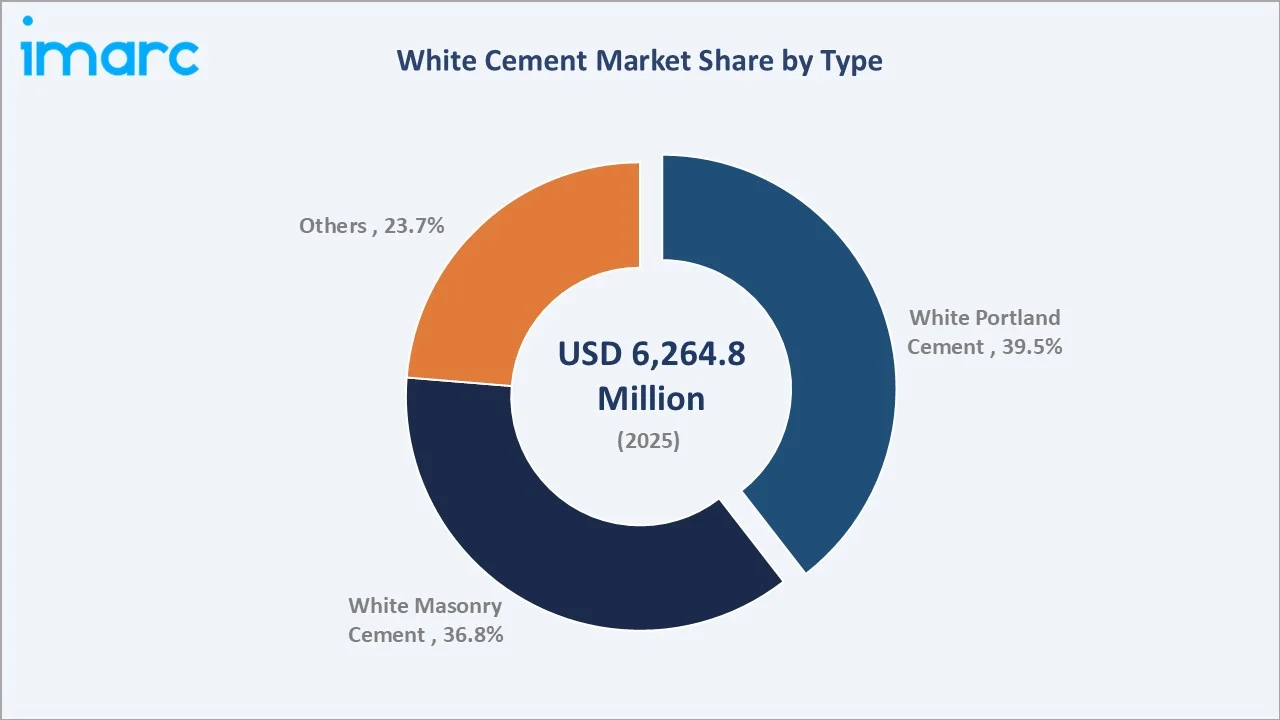

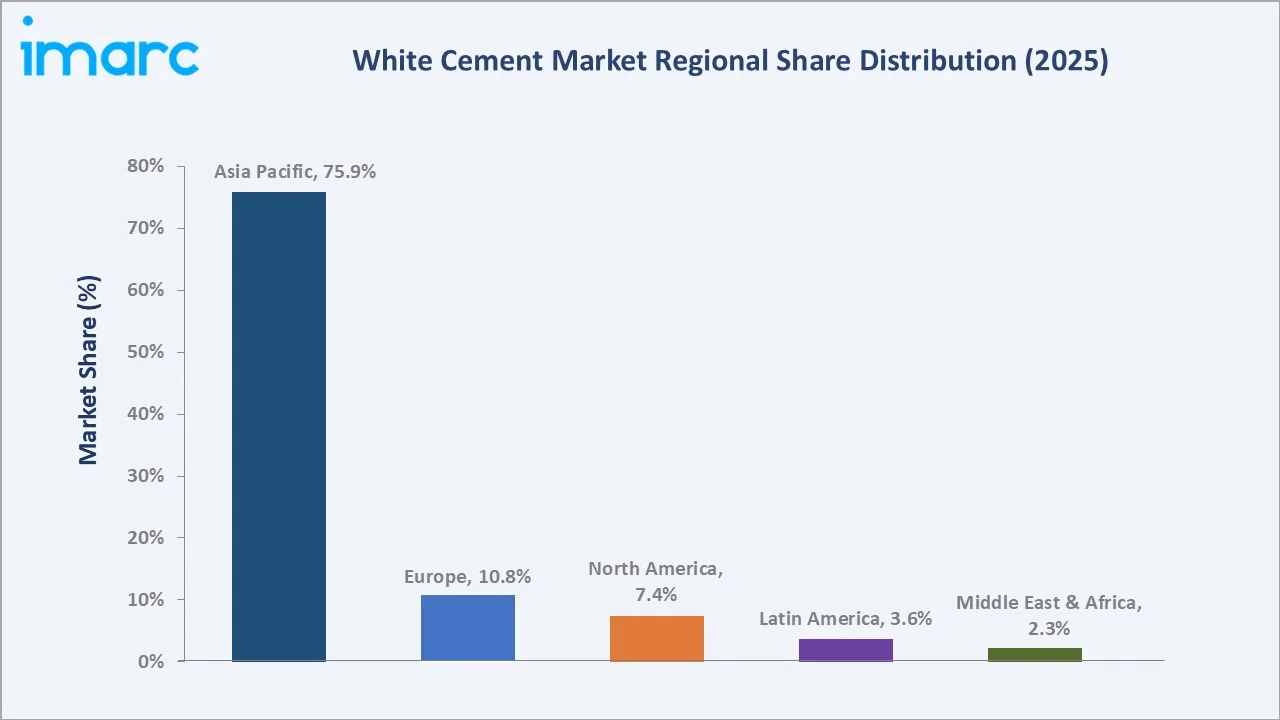

The global white cement market size was valued at USD 6,264.8 Million in 2025 and is projected to reach USD 8,829.0 Million by 2034, exhibiting a CAGR of 3.56% during the forecast period 2026-2034. Rapid urbanization, rising preference for premium decorative construction, government housing and infrastructure programs across the Asia Pacific, and growing adoption of sustainable and energy-efficient building materials are driving the white cement market growth. The Commercial application segment leads with 54.7% market share in 2025, while White Portland Cement dominates the type segment at 39.5%. Asia Pacific commands 75.9% of global revenue in 2025, the world's largest regional market for white cement.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6,264.8 Million |

|

Forecast Market Size (2034) |

USD 8,829.0 Million |

|

CAGR (2026-2034) |

3.56% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (75.9% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Application Segment |

Commercial (54.7%, 2025) |

|

Leading Type |

White Portland Cement (39.5%, 2025) |

The global white cement market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by urbanization, rising premium construction demand, and sustainability-driven adoption of reflective building materials.

To get more information on this market, Request Sample

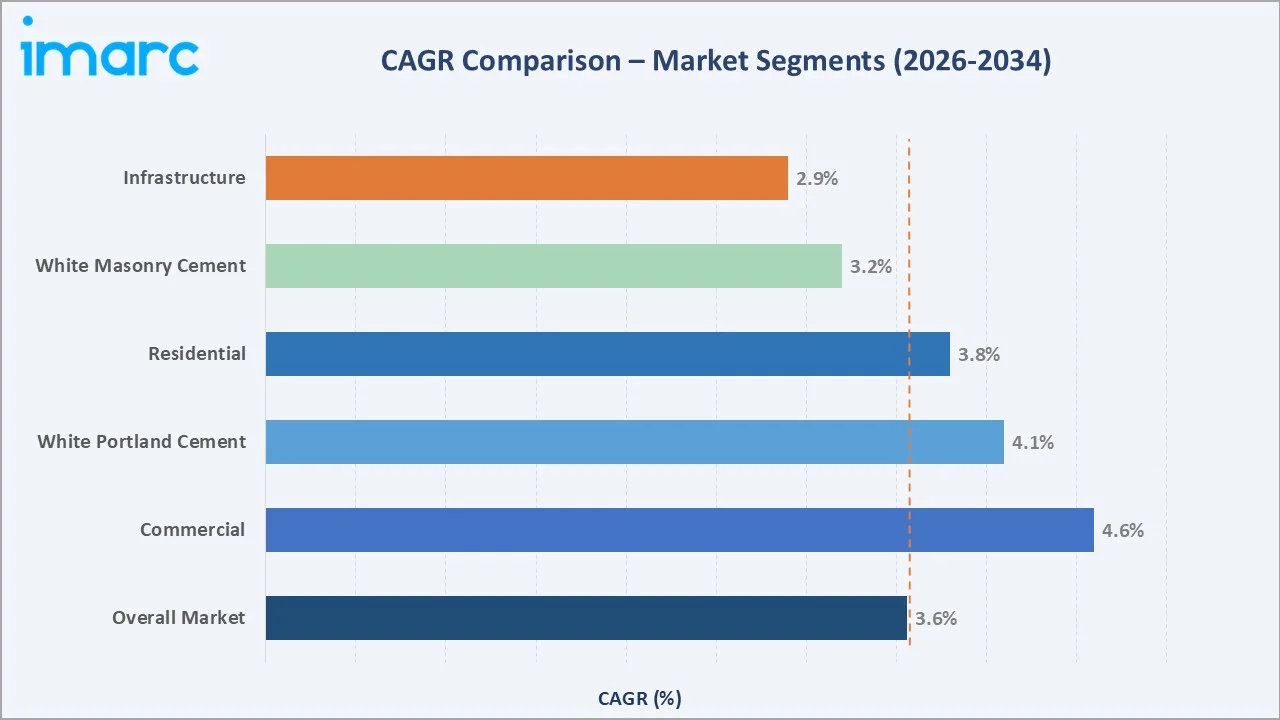

Segment-level CAGR comparisons highlighting Commercial applications and White Portland Cement as the two highest-growth sub-categories within the global white cement market analysis through 2034.

Executive Summary

The global white cement market is experiencing steady, sustained expansion driven by accelerating urbanization, rising consumer aspirations for premium construction aesthetics, and robust government investment in housing and public infrastructure. Valued at USD 6,264.8 Million in 2025, the market is forecast to reach USD 8,829.0 Million by 2034 at a CAGR of 3.56%.

The Commercial segment commands a dominant 54.7% share in 2025, driven by investments in shopping malls, corporate offices, hospitality venues, and institutional buildings where aesthetic quality directly influences occupant experience and asset value. The Residential segment contributes 28.4%, while Infrastructure accounts for 16.9%. By product type, White Portland Cement leads at 39.5% owing to its dual structural and decorative utility across construction projects of all scales, followed by White Masonry Cement at 36.8%.

Asia Pacific dominates with a 75.9% global revenue share in 2025, led by China's vast urban development programs, India's housing and infrastructure spending, and the growing premium construction markets of Indonesia, Vietnam, and Australia. Europe holds 10.8% in 2025 and North America 7.4%, with both regions characterized by strong architectural heritage restoration demand and a growing focus on energy-efficient, cool-roof building materials where white cement's light-reflective properties offer meaningful performance advantages.

Key Market Insights

|

Insight |

Data |

|

Largest Application Segment |

Commercial – 54.7% share (2025) |

|

Second Application Segment |

Residential – 28.4% share (2025) |

|

Largest Product Type |

White Portland Cement – 39.5% (2025) |

|

Leading Region |

Asia Pacific – 75.9% revenue share (2025) |

|

Second Region |

Europe – 10.8% revenue share (2025) |

|

Top Companies |

Cementir Holding N.V., Aditya Birla Group, JK Cement Ltd, CEMEX S.A.B. de C.V. |

Key Analytical Observations Supporting The Above Data:

- Commercial dominance (54.7%): Reflects accelerating investment in premium retail, office, and hospitality projects across Asia Pacific and the Middle East, where white cement's bright, pigment-compatible surface finish is architecturally specified for feature walls, lobby cladding, and exterior facades.

- White Portland Cement leadership (39.5%): Stems from its dual capability as both a structural and decorative material — offering superior compressive strength, consistent whiteness index (above 85), and compatibility with pigment-based architectural design applications.

- Asia Pacific's 75.9% dominance: Reflects sustained large-scale urban development in China, alongside major housing initiatives in India and Indonesia, collectively driving long-term structural demand for white cement.

- White cement market outlook driven by sustainability: New installations in hot climates incorporate white cement for its solar reflectance benefits, aligning with the global construction industry's net-zero building commitments.

- Market forecast momentum: Reflects structural demand from urbanization, rising disposable incomes, and expanding architectural design applications in developing markets.

Global White Cement Market Overview

White cement is a refined form of ordinary Portland cement made by removing iron oxide and manganese from raw materials such as kaolin clay, white limestone, and gypsum, giving it a high-brightness, low-chromatic finish (whiteness index >85). Produced in specialized kilns under tightly controlled conditions, it is primarily used in decorative and architectural applications, including wall putty, precast elements, terrazzo, tiles, facades, and premium interiors. Its use extends across residential, commercial, infrastructure, and heritage restoration projects where aesthetics are critical.

Market growth is supported by rising global construction spending, rapid urbanization, increasing disposable incomes, and a shift toward high-quality, visually appealing built environments, with expanding adoption beyond niche decorative uses into broader construction applications.

Market Dynamics

To evaluate market opportunities, Request Sample

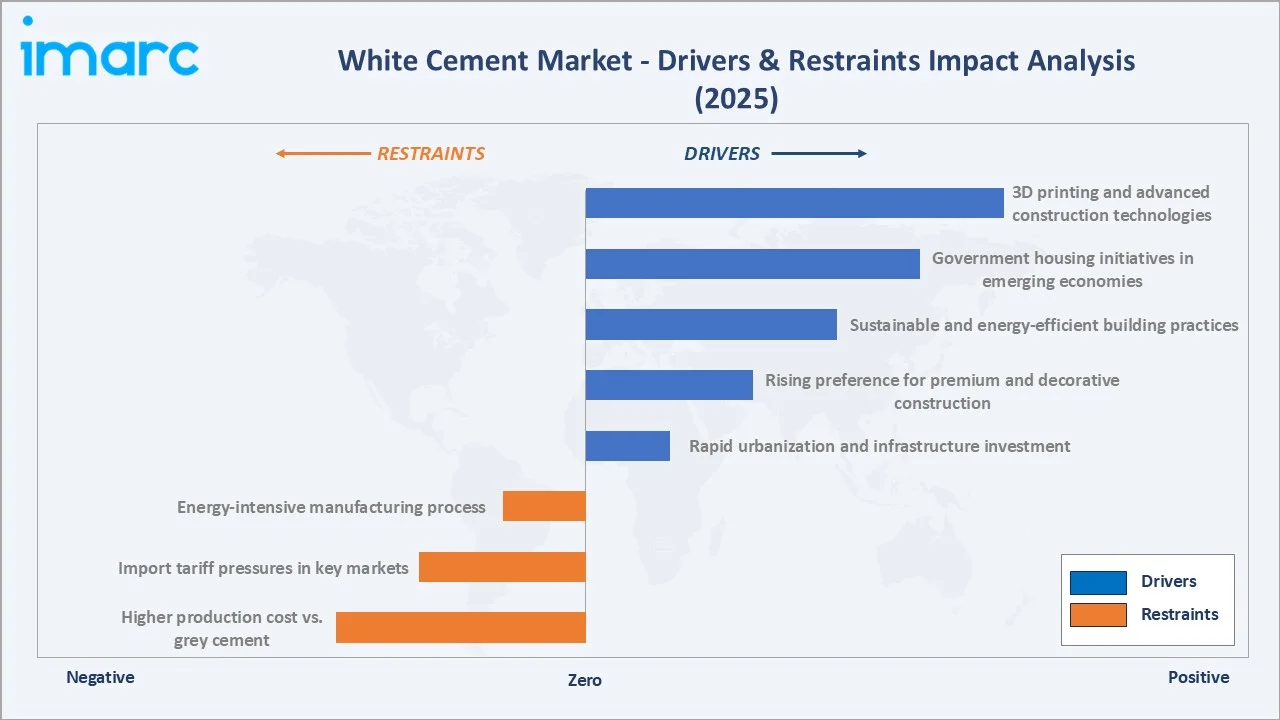

Market Drivers

- Rapid urbanization and infrastructure investment: Governments across Asia, Africa, and Latin America are allocating significant budgets toward housing, transportation, and public infrastructure. Large-scale funding programs in developed markets and a substantial infrastructure financing gap in the Asia Pacific are collectively driving sustained demand for construction materials, including white cement.

- Rising preference for premium and decorative construction: A significant share of global white cement consumption is driven by decorative architectural applications across residential and commercial segments. Increasingly, architects and developers prefer white cement for facades, precast panels, feature walls, and polished surfaces where enhanced aesthetic quality is required.

- Sustainable and energy-efficient building practices: White cement’s high solar reflectance makes it suitable for cool roofs and reflective facades, supporting energy-efficient building design. Its use is expanding in warmer climates where thermal performance and alignment with sustainability goals are key considerations.

- Government housing initiatives in emerging economies: Large-scale housing development programs across emerging economies are generating consistent demand for white cement in applications such as tiling, wall finishes, and architectural elements.

Market Restraints

- Higher production cost vs. grey cement: The production of white cement requires specialized processes, including the use of low-iron raw materials and controlled kiln conditions, resulting in a notable cost premium compared to conventional grey cement. This limits its adoption in price-sensitive construction segments.

- Import tariff pressures in key markets: Import duties and trade regulations in certain markets contribute to pricing volatility, particularly in regions that rely on imported white cement for supply.

Market Opportunities

- 3D printing and advanced construction technologies: The adoption of advanced construction methods, including 3D printing and prefabrication, is creating new demand for white cement due to its consistency, workability, and color uniformity.

- Iconic architecture and luxury developments in the Middle East: Growth in high-end real estate, tourism infrastructure, and large-scale urban projects—particularly in the Middle East and other developing regions—is driving demand for premium construction materials such as white cement.

- Photocatalytic and self-cleaning white cement formulations: The development of advanced formulations, including self-cleaning and pollution-reducing variants, is expanding the application scope of white cement in sustainable and urban construction.

Market Challenges

- Energy-intensive manufacturing process: White cement production involves higher energy consumption due to stringent processing requirements, making manufacturers more exposed to fluctuations in energy costs and environmental regulations.

- Limited raw material sourcing base: High-purity white limestone and kaolin clay — the primary raw materials for white cement — are geographically concentrated in a limited number of locations globally, creating supply chain concentration risk and potentially constraining production capacity expansion in demand-growth regions.

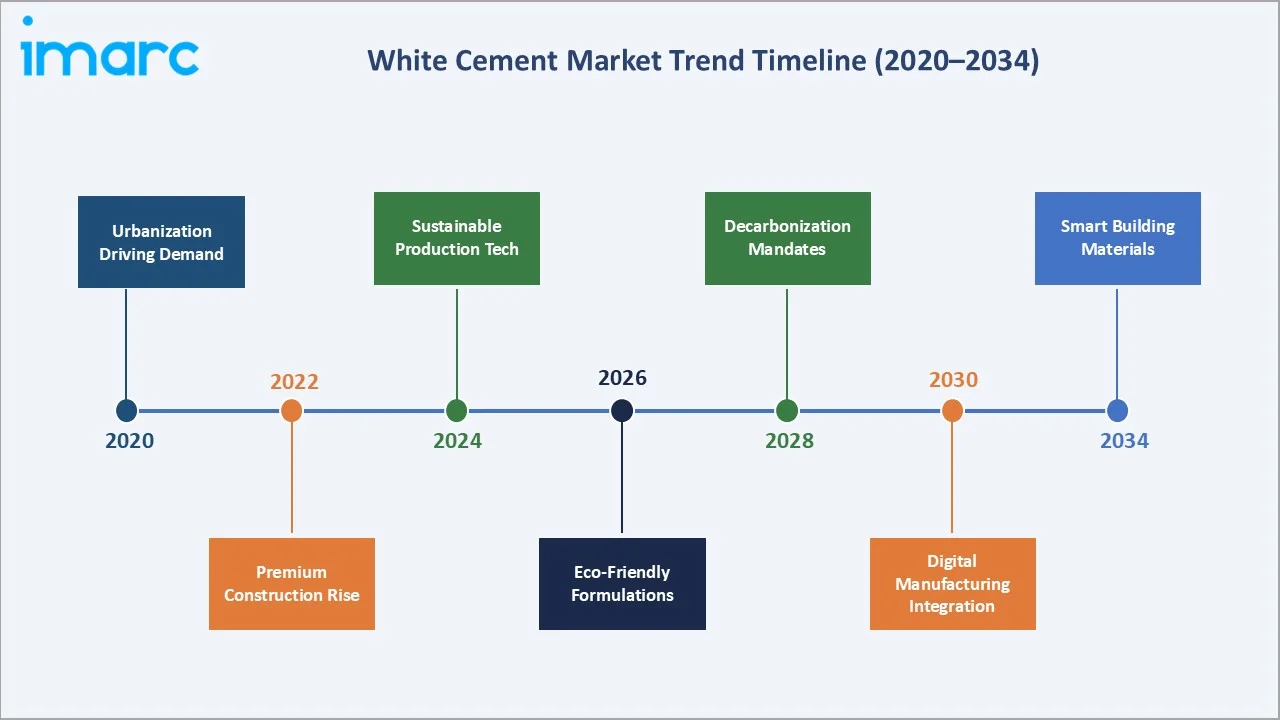

Emerging Market Trends

1. Integration of Sustainable and Low-Carbon Production Technologies

White cement manufacturers are increasingly adopting carbon reduction technologies such as energy-efficient kilns, alternative fuels, and clinker substitution materials (e.g., calcined clay and limestone blends). New product developments are focused on lowering CO₂ intensity while maintaining high whiteness levels, with some next-generation variants demonstrating measurable emission reductions versus conventional grades. This transition toward greener production is strengthening demand from ESG-aligned developers and public infrastructure projects, expanding the premium sustainable materials segment.

2. Rising Adoption in Premium Residential and High-Rise Construction

Rising demand for high-end finishes in urban residential and commercial developments is driving increased use of white cement. Its ability to deliver bright, uniform surfaces makes it a preferred material for exposed concrete, polished flooring, and architectural facades. Expansion of premium real estate and Grade-A commercial spaces across Asia, the Middle East, and developed markets continues to support higher specification rates for white cement in modern construction.

3. Decentralization of White Cement Production Networks

Manufacturers are shifting toward regionally distributed production models to improve supply reliability and reduce logistics costs and emissions. Locating plants closer to demand centers enables faster delivery, greater customization to local standards, and reduced exposure to global trade disruptions. This approach is emerging as a key competitive differentiator, particularly in high-growth regions such as Southeast Asia and the GCC.

4. Digitalization and Smart Manufacturing in White Cement Production

The integration of Industry 4.0 technologies—including AI-driven kiln optimization, real-time quality monitoring, and digital supply chain systems—is enhancing operational efficiency in white cement production. Advanced tools such as digital twins allow manufacturers to simulate and optimize production parameters, ensuring consistent product quality. This is especially critical in white cement, where minor variations in raw materials or temperature can significantly impact color uniformity.

5. White Cement in Infrastructure and Transportation Projects

White cement is increasingly being specified in infrastructure and transportation applications, including bridges, tunnels, highways, and airports. Its durability, crack resistance, and high visibility make it suitable for safety-critical structures such as road barriers and tunnel linings. This trend reflects a broader shift toward aesthetic and performance-driven infrastructure design, expanding white cement usage beyond traditional decorative applications.

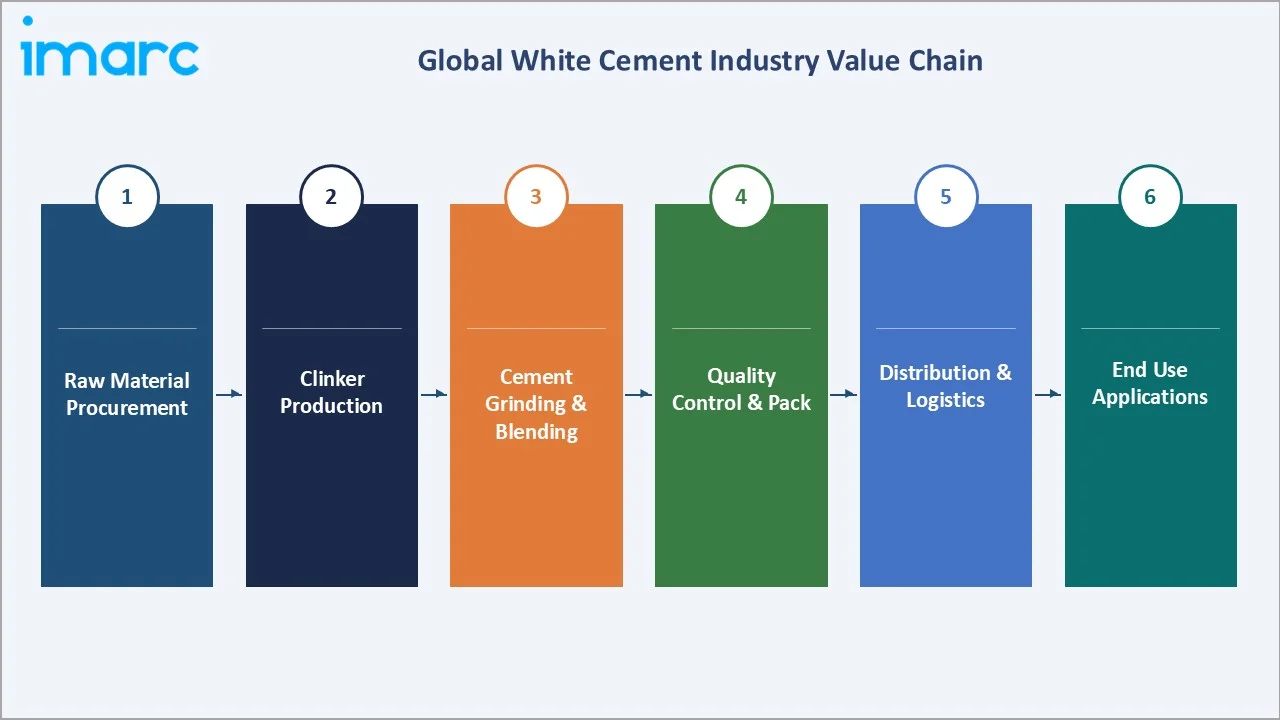

Industry Value Chain Analysis

The white cement industry value chain spans five integrated stages from raw material procurement through end-use consumption. Each stage presents distinct competitive dynamics, margin structures, and quality control requirements, reflecting the premium nature of white cement relative to standard grey cement production.

|

Stage |

Key Activities / Players |

|

Raw Material Procurement |

White limestone, kaolin clay, gypsum, and low-iron additives sourced from specialized global quarries; strict raw material quality control to ensure whiteness index compliance above 85 |

|

Clinker Production |

Dedicated white cement kilns operating at precisely controlled temperatures; bleaching and quenching processes; specialized fuel selection to minimize iron contamination and maintain color purity |

|

Cement Grinding & Blending |

Fine grinding with contamination-free mill equipment; blending with supplementary cementitious materials; quality-tested batch production with whiteness and strength certification |

|

Distribution & Logistics |

Bagged and bulk distribution via port terminals, rail, and road freight; regional distribution hubs minimizing supply chain length; cold chain management for export markets |

|

End Use |

Construction contractors, architectural precast manufacturers, tile adhesive producers, wall putty manufacturers, terrazzo and mosaic fabricators, decorative concrete producers |

Manufacturers occupy the highest strategic value position in the white cement value chain, integrating raw material processing, specialized kiln operations, quality testing, and product certification into a controlled production system that commands significant price premiums over grey cement. This structural premium position is supported by the technical barriers to white cement production — including the requirement for dedicated kiln infrastructure — which effectively limit new market entrants and support the pricing power of established producers.

Technology Landscape in the White Cement Industry

Kiln Technology and Energy Efficiency

Modern white cement production utilizes precalciner and dry-process rotary kilns optimized for high-temperature, low-iron operations. Emerging technologies such as flash calciners and oxyfuel combustion are improving energy efficiency and enabling the use of alternative fuels (biomass, waste-derived fuels, hydrogen blends) without compromising color quality.

Carbon Capture, Utilization, and Storage (CCUS)

CCUS is gaining traction as a key decarbonization pathway, targeting a significant reduction of process emissions from clinker production. Pilot projects are demonstrating high CO₂ capture potential, while new low-carbon product variants with reduced emission intensity are entering the market, aligning with evolving sustainability standards and regulatory frameworks.

Digital Quality Control and Industry 4.0 Integration

AI-driven quality control systems and real-time monitoring technologies are enhancing production precision by continuously tracking whiteness, particle size, and composition. Integration of digital supply chain platforms is further improving demand forecasting, inventory optimization, and operational efficiency across geographically distributed markets.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

Commercial |

54.7% |

2025 |

|

Type |

White Portland Cement |

39.5% |

2025 |

|

Region |

Asia Pacific |

75.9% |

2025 |

By Application

The Commercial segment commands a leading 54.7% majority share of the global white cement market in 2025, reflecting robust and sustained investment in shopping complexes, corporate office towers, hospitality properties, retail centers, and institutional buildings across both mature and emerging markets.

To access detailed market analysis, Request Sample

The Residential segment holds 28.4% in 2025, driven by growing demand for premium housing finishes in urban centers across Asia Pacific, the Middle East, and Europe. White cement is extensively used in high-rise apartments, luxury villas, and premium housing estates for interior and exterior wall finishes, marble tile installation, swimming pool construction, and decorative elements.

The Infrastructure segment at 16.9% is growing as transportation authorities and infrastructure agencies increasingly specify white cement for bridge structures, highway barriers, airport facilities, and public transit hubs where both durability and aesthetic quality are design priorities.

By Type

The White Portland Cement sub-segment commands the largest type share at 39.5% of the global white cement market in 2025. White Portland Cement boasts superior strength and durability, making it a preferred choice for construction projects requiring high-strength concrete, and its ability to retain a bright, consistent white color even when mixed with other elements has allowed architects and designers to use it extensively in decorative and structural applications. Its versatility spans precast panels, architectural concrete, facade cladding, tile adhesives, and wall putty — making it the most broadly applicable product type in the market.

White Masonry Cement holds 36.8% in 2025, widely used in masonry mortar, stucco, plaster, and decorative finishes for residential and commercial walls. Its enhanced workability and plasticity relative to Portland cement make it the preferred choice for plastering and rendering applications where smooth, uniform white surfaces are required. The Others category at 23.7% encompasses specialty formulations including White Portland Limestone Cement (PLC), White Calcium Aluminate Cement for high-temperature applications, and photocatalytic white cement variants incorporating titanium dioxide for air-purifying, self-cleaning surface properties — a growing niche in sustainable premium construction.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

75.9% |

Urban housing programs in China and India, commercial development in Southeast Asia, and premium residential demand in Australia and South Korea |

|

Europe |

10.8% |

Architectural heritage restoration, minimalist design trends, sustainable building mandates, and EU Green Deal construction standards |

|

North America |

7.4% |

Premium commercial and institutional construction, federal infrastructure investment programs, and growing domestic production capacity |

|

Latin America |

3.6% |

Urbanization-driven housing demand in Brazil and Mexico, expanding commercial real estate, and the growing construction sector in Peru and Colombia |

|

Middle East & Africa |

2.3% |

Vision 2030 iconic architecture projects, UAE smart city development, luxury tourism and hospitality construction, and new regional production capacity |

Asia Pacific accounts for 75.9% (2025) of the global white cement market, dominating due to large-scale urban development and strong residential and infrastructure demand across the region. Europe holds 10.8% (2025), supported by architectural preferences for clean aesthetics and extensive use in heritage restoration. North America represents 7.4% (2025), driven by premium commercial construction and infrastructure upgrades. Latin America captures 3.6% (2025), led by Brazil and Mexico, with urbanization and rising incomes supporting adoption in construction. The Middle East & Africa, at 2.3% (2025), is characterized by high-value projects requiring premium white cement for iconic and large-scale developments.

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Cementir Holding N.V. |

Aalborg White |

Leader |

Global white cement leader; low-carbon D-Carb innovation; Europe, Turkey, Scandinavia |

|

Aditya Birla Group |

Birla White |

Leader |

Dominant in South Asia; wall putty leadership; white cement acquisition strategy |

|

JK Cement Ltd |

JK White |

Leader |

1.72 MTPA white cement capacity in India; international expansion; wall putty |

|

CEMEX S.A.B. de C.V. |

Rugby White Cement |

Leader |

Global reach; eco-friendly white cement range launched |

|

Cementos Molins, S.A. |

DRAGÓN, Calucem |

Emerging |

Spanish cement group; majority owner of Sotacib (Tunisia); white cement operations in Spain and North Africa; Mediterranean and Latin American presence |

|

Federal White Cement |

Federal White |

Emerging |

North American specialist; serves U.S. and Canadian premium construction |

The white cement competitive landscape is moderately consolidated, with the top 10 players collectively accounting for approximately 65% of global market share in 2025. Key competitive strategies include capacity expansion, low-carbon product innovation, geographic diversification into high-growth emerging markets, and downstream integration into value-added products, including wall putty, tile adhesives, and decorative concrete formulations. The white cement market is characterized by high barriers to entry — dedicated kiln infrastructure requirements, specialized raw material sourcing, and demanding quality certification standards effectively limit new market entrants and support the pricing power of established producers.

Key Company Profiles

Cementir Holding N.V.

Cementir Holding N.V. is headquartered in the Netherlands. The company operates across Europe, Scandinavia, North America, and the Asia Pacific, supplying premium white cement products to premium construction and architectural specification markets globally.

- Product & Platform Portfolio: Aalborg White, Futurecem, D-Carb, InWhite (platform), AALBORG INBIND.

- Recent Developments: In April 2024, Cementir Group launched D-Carb reduced-CO2 white cement in Europe.

- Strategic Focus: Cementir's strategy centers on low-carbon product leadership, geographic expansion into growth markets through its Aalborg White distribution network, and premium positioning in the architectural concrete, precast panels, and wall putty segments globally.

Aditya Birla Group

Aditya Birla Group’s flagship UltraTech Cement Limited is a cement producer and a dominant player in the South Asian white cement market through its Birla White brand. The company operates integrated white cement plants and wall putty manufacturing facilities across India, serving both domestic and export markets.

- Product & Platform Portfolio: Birla White Cement, Birla White WallCare Putty, Birla White Tile Adhesive, specialty decorative cement products.

- Recent Developments: In April 2025, Aditya Birla Group’s flagship UltraTech Cement Limited acquired Wonder Cement to expand its portfolio and strengthen its market footprint in Rajasthan, one of India's key white cement production and consumption hubs

- Strategic Focus: Focuses on consolidating leadership in the Indian white cement and wall putty market through strategic acquisitions, expanding its Birla White premium brand positioning, and investing in distribution network expansion to serve Tier-2 and Tier-3 city markets in India.

JK Cement Ltd

JK Cement Ltd is a white cement producer. The company is headquartered in Kanpur, India, and serves both domestic and international markets through its JK White brand.

- Product & Platform Portfolio: JK White Cement, JK Wall Putty, JK Tile Adhesives, JK Grouts, JK White Primer.

- Recent Developments: In January 2026, JK Cement commissioned 1.0 MTPA of new grinding capacity at each of its Panna and Hamirpur plants, lifting total installed cement capacity to approximately 28.3 MTPA.

- Strategic Focus: JK Cement's white cement strategy focuses on maintaining production leadership in India through capacity expansion, deepening international distribution partnerships in the Middle East, Africa, and Southeast Asia, and growing its value-added wall putty and tile adhesive product portfolio to improve per-tonne revenue realization.

Market Concentration Analysis

The global white cement market exhibits moderate-to-high concentration among the top producers, with Cementir Holding N.V., Aditya Birla Group, JK Cement Ltd, and CEMEX S.A.B. de C.V. collectively accounting for a significant portion of global production capacity. The top 10 players capture approximately 65% of the global market share in 2025, reflecting the structural barriers to white cement production that limit new market entrants.

The white cement competitive landscape is experiencing a bifurcated dynamic. At the premium specification tier, consolidation is occurring as large-scale integrated producers with dedicated kiln infrastructure and quality certification systems command the architectural and decorative construction segments. Simultaneously, regional markets — particularly in the Middle East, North Africa, and Southeast Asia — are attracting new local production investments driven by governments seeking to reduce import dependency and develop domestic construction material industries. This regional production growth is creating new competitive pressure on established international exporters while improving market accessibility and supply security in underserved markets.

Investment & Growth Opportunities

Fastest-Growing Segments

Commercial applications lead growth, driven by premium retail, office, and hospitality construction. White Portland Cement sees steady demand from architectural concrete and precast uses, while photocatalytic and self-cleaning variants offer high-value niche growth.

Emerging Market Expansion

Southeast Asia, South Asia, and Sub-Saharan Africa are key growth regions, supported by rapid urbanization and housing demand. Supply gaps create opportunities for localized production and downstream integration.

Venture & Strategic Investment Trends

Capacity expansion and acquisitions remain key strategies, alongside investments in regional hubs. Sustainability-focused capex, including low-carbon technologies, is attracting increasing ESG-driven investment.

Future Market Outlook (2026-2034)

The global white cement market forecast projects steady value expansion from USD 6,264.8 Million in 2025 to USD 8,829.0 Million by 2034 at a CAGR of 3.56% — a sustained growth trajectory underpinned by structural demand from urbanization, premium construction premiumization, and the progressive integration of white cement into sustainable building material specifications globally.

Three structural shifts will shape the white cement market: rising adoption of low-carbon standards driving demand for sustainable formulations; rapid urbanization in Asia generating strong volume growth; and integration into advanced construction technologies such as 3D printing and modular construction, enabling premium pricing opportunities.

By 2034, the market is expected to consolidate around a few global players with integrated operations and strong downstream portfolios. Companies combining low-carbon production, product innovation, and regional presence will capture the highest value.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted with white cement industry stakeholders, including production directors at leading cement manufacturers, construction company procurement managers, architectural specification consultants, and institutional investors in building materials. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include government construction spending data (U.S. BLS, India MoHUA, Indonesia PUPR), Saudi Vision 2030 project documentation, industry association reports from the Global Cement and Concrete Association (GCCA), trade publications including International Cement Review, company annual reports, regulatory publications, and specialist building materials market intelligence databases.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, construction spending data, cement consumption per capita benchmarks, and historical white cement market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty, raw material price volatility, and energy cost variability.

White Cement Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD, Million Tons |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | White Portland Cement, White Masonry Cement, Others |

| Applications Covered | Residential, Commercial, Infrastructure |

| Regions Covered | Asia-Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, United States, Canada, Brazil, Mexico |

| Companies Covered | Cementir Holding N.V., Aditya Birla Group, JK Cement Ltd, CEMEX S.A.B. de C.V., Cementos Molins, S.A., Federal White Cement, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the white cement market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global white cement market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the white cement industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the White Cement Market Report

The global white cement market was valued at USD 6,264.8 Million in 2025, driven by urbanization, premium construction demand, and growing adoption of sustainable building materials.

The market is projected to reach USD 8,829.0 Million by 2034, growing at a CAGR of 3.56% during 2026-2034, driven by expanding infrastructure investment, premium residential construction, and sustainable building material adoption.

The Commercial application segment leads with a 54.7% share in 2025, driven by investment in shopping malls, office complexes, hospitality properties, and institutional buildings where white cement's aesthetic finish quality is architecturally specified.

White Portland Cement leads with a 39.5% share in 2025, driven by its dual capability as a structural and decorative material with superior compressive strength, consistent whiteness, and broad compatibility with architectural and decorative concrete applications.

Asia Pacific leads with a 75.9% share in 2025, driven by China's urban development programs, India's housing initiative, and the growing premium construction markets of Southeast Asia and Australia.

Key drivers include rapid urbanization and infrastructure investment in emerging economies, rising demand for decorative and premium-quality construction materials, growing adoption of sustainable and energy-efficient building practices (white cement's solar reflectance benefits), and technological advancements in low-carbon white cement manufacturing.

Key trends include integration of CCUS and low-carbon production technologies, rising adoption in premium residential and high-rise construction, decentralization of production networks toward demand centers, digitalization and Industry 4.0 in manufacturing operations, and expanding use in transportation and public infrastructure projects.

Leading companies include Cementir Holding N.V., Aditya Birla Group, JK Cement Ltd, CEMEX S.A.B. de C.V., Cementos Molins, S.A., and Federal White Cement.

Asia Pacific is the fastest-growing region, supported by India's urban housing programs, Indonesia's government construction targets, and Vietnam's expanding commercial real estate sector, all creating structural volume demand growth that exceeds other major regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)