Wireless Gigabit Market Size, Share, Trends and Forecast by Product, Technology, End Use Industry, and Region, 2026-2034

Wireless Gigabit Market Size and Share:

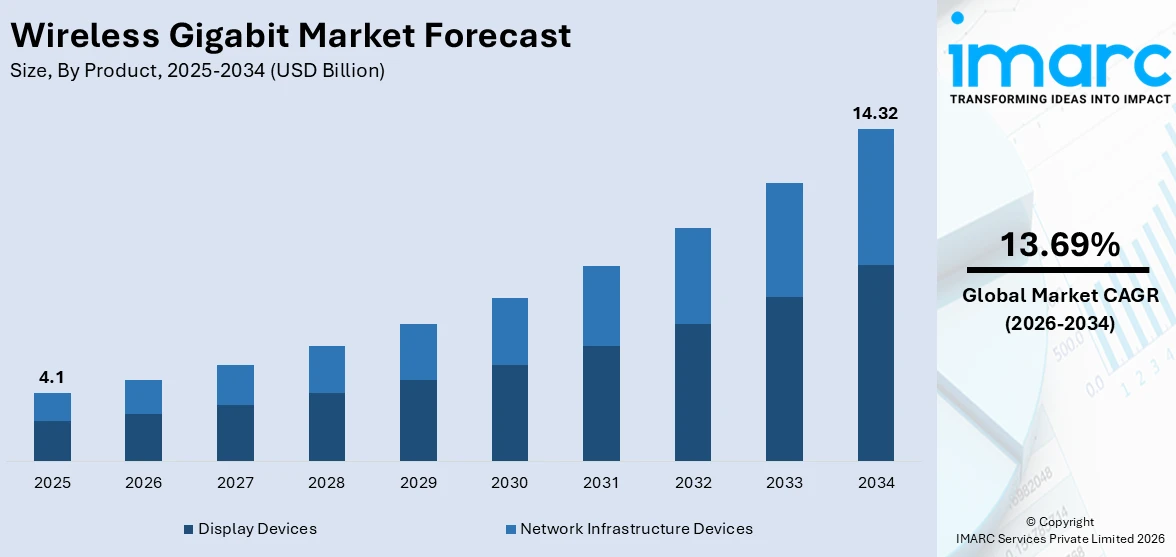

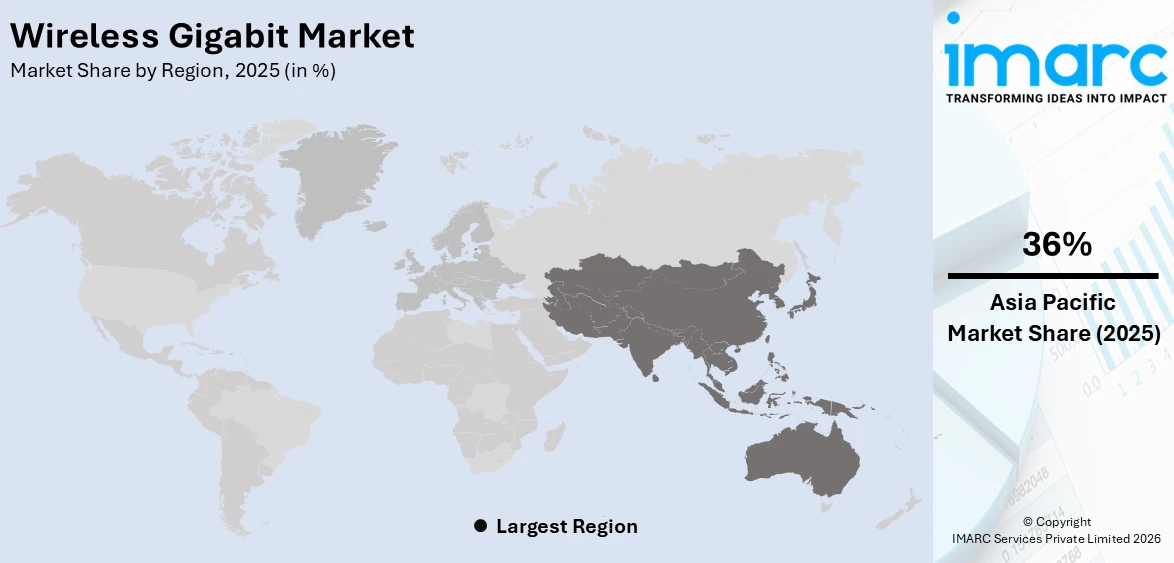

The global wireless gigabit market size was valued at USD 4.1 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 14.32 Billion by 2034, exhibiting a CAGR of 13.69% from 2026-2034. Asia-Pacific currently dominates the market, holding a market share of 36% in 2025. The region benefits from extensive manufacturing capabilities in semiconductor and electronics components, rapid expansion of 5G infrastructure across major economies, and increasing integration of multi-gigabit wireless solutions in consumer devices and industrial automation systems, all contributing to the wireless gigabit market share.

The growing demand for ultra-high-speed wireless connectivity across diverse sectors is driving the global wireless gigabit market. The proliferation of bandwidth-intensive applications, including virtual reality, augmented reality, 8K video streaming, and cloud gaming, necessitates wireless solutions capable of delivering multi-gigabit data rates with minimal latency. Additionally, the increasing adoption of wireless docking stations in enterprise environments is eliminating the need for cumbersome cable connections, enhancing workplace flexibility and productivity. The ongoing transition toward smart infrastructure, encompassing smart cities, connected healthcare facilities, and automated manufacturing plants, further amplifies the need for reliable short-range wireless communication at gigabit speeds. Furthermore, the expansion of the Internet of Things ecosystem, with billions of connected devices generating massive data volumes, is accelerating the deployment of advanced wireless protocols. The evolution of IEEE 802.11ad and 802.11ay standards is also enabling broader commercial adoption of wireless gigabit market growth solutions worldwide.

The United States has emerged as a major region in the wireless gigabit market owing to many factors. The country's advanced technological infrastructure, coupled with substantial investments in 5G and millimeter-wave deployment, creates a favorable environment for wireless gigabit adoption across both consumer and enterprise segments. The presence of leading semiconductor firms and chip designers accelerates innovation in 60 GHz system-on-chip and integrated circuit solutions tailored for wireless display, docking, and fixed wireless access applications. The growing emphasis on hybrid work models and flexible office configurations is boosting demand for wireless docking and display solutions in corporate environments. For instance, in July 2025, the U.S. federal government signed the One Big Beautiful Bill Act into law, restoring the FCC’s general auction authority and directing the auction of at least 800 MHz of spectrum including 100 MHz in the Upper C-band within two years, strengthening the regulatory framework for high-frequency wireless technologies.

To get more information on this market Request Sample

Wireless Gigabit Market Trends:

Expanding Spectrum Availability for WiGig

The expansion of unlicensed spectrum bands is catalyzing the adoption of wireless gigabit solutions globally. Regulatory bodies worldwide are recognizing the critical importance of allocating additional high-frequency spectrum to support the growing demand for multi-gigabit wireless connectivity. The availability of wider channels in the 60 GHz band enables devices to achieve data transfer rates that rival wired connections, making wireless gigabit technology increasingly viable for applications ranging from wireless display and docking to fixed wireless access. Governments and regulatory agencies are streamlining licensing procedures and opening new frequency bands to encourage commercial deployment of millimeter-wave technologies. For instance, in March 2025, the U.S. Federal Communications Commission expanded unlicensed very low power device operation to the entire 6 GHz band, effective May 2025, providing additional spectrum for high-throughput and low-latency operations. This regulatory momentum is creating a more supportive ecosystem for the development and commercialization of next-generation wireless gigabit devices and infrastructure across various industries.

Convergence of WiGig with 5G Networks

The integration of wireless gigabit technology with 5G cellular networks is creating hybrid connectivity solutions that combine the strengths of both platforms. While 5G networks deliver wide-area coverage and mobility, wireless gigabit technology operating in the 60 GHz band provides complementary short-range, ultra-high-speed connectivity ideal for indoor environments and dense deployment scenarios. This convergence enables seamless handoff between network types, optimizing user experience for bandwidth-intensive applications such as immersive media streaming, autonomous systems, and edge computing workloads. The wireless gigabit market outlook is favorable as telecom operators and enterprise networks integrate millimeter-wave links for small cell backhaul and last-mile delivery. For instance, in 2025, KDDI Corporation and Kyocera Corporation developed compact 28 GHz millimeter-wave repeaters in the Shinjuku area of Tokyo that increased 5G street-level coverage from 33% to 99%. This synergy between technologies is enabling more robust and versatile networking architectures that address the diverse connectivity requirements of modern digital environments.

Advancing Beamforming and SoC Integration

Advancements in beamforming algorithms and system-on-chip design are significantly enhancing the performance and affordability of wireless gigabit devices. Modern beamforming techniques utilize phased array antennas to dynamically steer signal beams toward target devices, overcoming the inherent propagation challenges of millimeter-wave frequencies and extending effective communication range. Simultaneously, the integration of 60 GHz radio, baseband processing, and power management onto a single silicon die reduces board space requirements, lowers power consumption, and cuts manufacturing costs. These technological improvements are making wireless gigabit connectivity accessible to a broader range of consumer electronics and networking equipment. The continued wireless gigabit market forecast is bolstered by these innovations. For instance, in June 2025, NTT Corporation achieved a world-record 280 Gbps data rate using a wideband 300 GHz amplifier, demonstrating a viable technology path for expanding ultra-high-frequency wireless communications beyond current capabilities. Such breakthroughs are paving the way for next-generation wireless standards that will further expand throughput and reliability across commercial applications.

Wireless Gigabit Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global wireless gigabit market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product, technology, and end use industry.

Analysis by Product:

- Display Devices

- Smartphones

- Laptops and Tablets

- Others

- Network Infrastructure Devices

- Routers and Access Points

- Adapters

- Backhaul Stations

- Docking Stations

Display Devices holds 56% of the market share. Display devices encompass a wide range of consumer electronics, including smartphones, laptops, tablets, monitors, and augmented reality and virtual reality headsets, that leverage wireless gigabit technology for cable-free content delivery and docking functionality. The demand for wireless display solutions is driven by the growing consumer preference for clutter-free setups, the proliferation of high-definition and ultra-high-definition content formats, and the rapid expansion of immersive media applications. The ability of 60 GHz wireless links to deliver low-latency, high-bandwidth video transmission makes display devices an ideal platform for wireless gigabit integration. Moreover, the rising adoption of wireless docking stations in enterprise environments, where employees require flexible connectivity to external monitors and peripherals, is further reinforcing this segment’s dominance. For instance, in June 2025, Peraso Inc. secured its first production order for 60 GHz wireless video systems designed for educational environments, providing high-performance, low-latency video transmission independent of existing school Wi-Fi infrastructure.

Analysis by Technology:

- System on Chip (SoC)

- Integrated Circuit Chip (IC Chip)

System on Chip (SoC) leads the market with a share of 54%. System-on-chip solutions integrate multiple functional components, including the 60 GHz radio frequency front-end, baseband processor, and power management circuitry, onto a single silicon substrate. This level of integration delivers substantial advantages in terms of reduced board space, lower power consumption, and streamlined device design, making SoC implementations highly attractive for compact consumer devices such as smartphones, laptops, and virtual reality headsets. The ongoing miniaturization enabled by advanced semiconductor fabrication processes at sub-three nanometer nodes continues to reduce the incremental cost of incorporating wireless gigabit capabilities into mainstream devices. For instance, in March 2025, Qualcomm Technologies launched the Dragonwing FWA Gen 4 Elite, a 5G Advanced-capable fixed wireless access platform powered by the Qualcomm X85 5G Modem-RF system, delivering downlink speeds up to 12.5 Gbps. The efficiency and compactness of SoC designs also accelerate qualification and certification timelines for device manufacturers.

Analysis by End Use Industry:

Access the comprehensive market breakdown Request Sample

- BFSI

- Healthcare

- IT and Telecom

- Retail

- Consumer Electronics

- Media and Entertainment

- Others

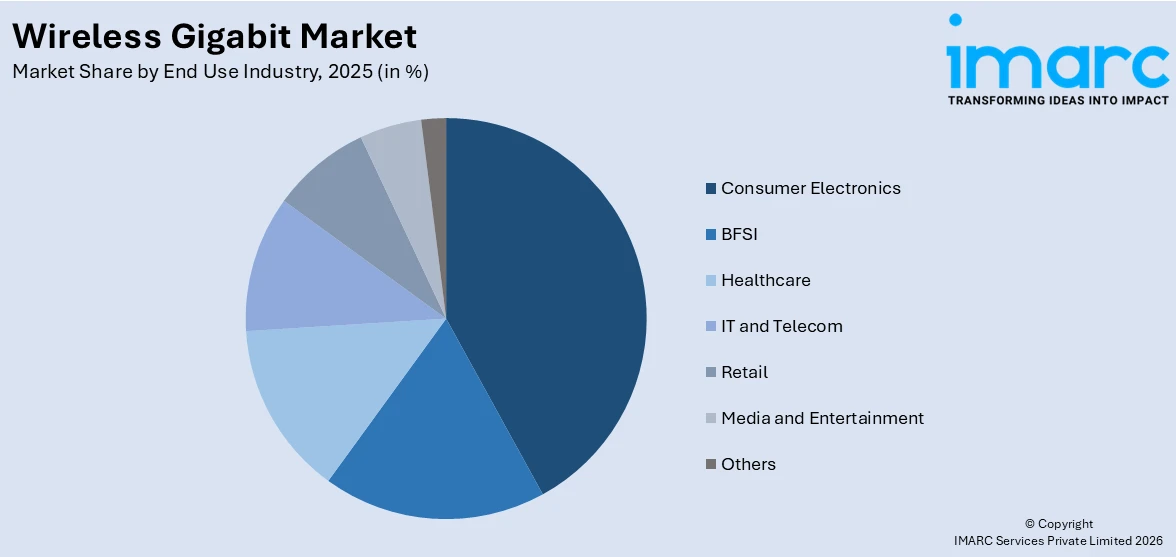

Consumer Electronics dominates the market, with a share of 42%. The consumer electronics segment encompasses a broad array of devices, including smartphones, tablets, laptops, gaming consoles, and wearable technology, that increasingly integrate wireless gigabit capabilities to meet consumer expectations for seamless, high-speed connectivity. The growing demand for immersive experiences, particularly in gaming, virtual reality, and augmented reality, requires data transfer rates that traditional wireless standards cannot reliably deliver, positioning wireless gigabit technology as a critical enabler for next-generation consumer products. Additionally, the increasing consumer appetite for wireless peripherals, cable-free entertainment systems, and smart home devices is expanding the addressable market for wireless gigabit solutions. For instance, in October 2024, Vodafone, Qualcomm, and Ericsson completed 5G millimeter-wave trials in the United Kingdom using Ericsson Radio System products and devices powered by the Snapdragon X65 5G Modem-RF System, demonstrating the commercial viability of ultra-fast wireless technology in consumer applications.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia-Pacific, accounting for 36% of the share, enjoys the leading position in the market. The region’s dominance is underpinned by its vast consumer electronics manufacturing base, rapid adoption of advanced wireless technologies, and significant government investments in digital infrastructure across major economies such as China, Japan, South Korea, and India. The proliferation of smart devices, combined with strong domestic demand for high-speed wireless connectivity in both consumer and enterprise applications, creates a substantial addressable market for wireless gigabit solutions. Furthermore, the region’s leading semiconductor foundries and component manufacturers facilitate shorter supply chains and faster time-to-market for wireless gigabit chipsets and modules. For instance, China had deployed approximately 4.65 million 5G base stations by the end of September 2025, reflecting the scale of telecommunications infrastructure expansion that supports the integration of millimeter-wave and wireless gigabit technologies across the region.

Key Regional Takeaways:

North America Wireless Gigabit Market Analysis

North America represents a key market for wireless gigabit technology, driven by the region’s advanced digital infrastructure, strong presence of leading semiconductor and networking companies, and supportive regulatory environment for high-frequency spectrum utilization. The United States and Canada lead in the implementation of millimeter-wave solutions for enterprise wireless docking, fixed wireless access, and delivery of immersive media. This has an advantageous ecosystem of chipset designers, device manufacturers, and network operators that collaborate effectively to launch products of wireless gigabit to the market in the area. The wireless docking and display solutions are gaining rapid adoption by enterprises, with organizations moving to flexible and hybrid work designs that require monitors, peripherals, and collaboration devices to be connected without the use of cables. Wireless gigabit application is also being used in high-speed data transfer in secure surroundings in the healthcare and financial services industries. For instance, in November 2025, the US Federal Communications Commission voted unanimously to adopt a Notice of Proposed Rulemaking for auctioning up to 180 MHz of Upper C-Band spectrum, signaling a continued commitment to expanding available frequency resources for next-generation wireless services. The expanding 5G small cell backhaul market further creates opportunities for wireless gigabit technology in dense urban environments.

United States Wireless Gigabit Market Analysis

The United States serves as a prominent contributor to the wireless gigabit market within North America, supported by substantial technology investments, a thriving semiconductor industry, and a progressive regulatory approach to spectrum management. Wireless gigabit solutions to modernize offices are gaining popularity among the corporate community in the country, and wireless docking stations and display systems are becoming popular in the flexible workspace structure. New application fields include the defense and aerospace sectors, which are utilizing 60 GHz wireless technology in high-capacity and secure tactical communications because of narrow beamwidth and reduced risk of interception. Learning institutions are also adopting wireless gigabit technology in delivering quality video streaming in classrooms to deal with the increasing challenges of Wi-Fi network overloads. The growth of augmented reality and virtual reality systems in the gaming, entertainment, and professional training is creating a further need for ultra-low-latency wireless connections. For instance, in April 2025, Nokia won a strategic 5G radio access network deal with T-Mobile US to extend nationwide millimeter-wave coverage, underscoring the growing synergy between 5G infrastructure and wireless gigabit technologies. The wireless gigabit market trends point toward increasing enterprise and defense adoption across the country.

Europe Wireless Gigabit Market Analysis

Europe presents a growing opportunity for the wireless gigabit market, driven by the region’s commitment to achieving comprehensive gigabit connectivity and advancing 5G deployment across member states. The European Union’s Digital Decade strategy and Gigabit Infrastructure Act are fostering an environment conducive to investment in advanced wireless technologies, including millimeter-wave solutions for indoor connectivity and enterprise networking. Germany’s leadership in Industry 4.0 and smart manufacturing is creating demand for high-speed, low-latency wireless links in factory environments, while the United Kingdom and France are prioritizing 5G infrastructure buildout that complements wireless gigabit deployments. The region’s emphasis on data privacy and cybersecurity is also driving demand for wireless solutions that offer inherent security advantages through directional transmission characteristics. For instance, the European Commission selected 56 projects for EUR 389 million in investment under the Connecting Europe Facility Digital Programme for cable, 5G, and quantum communications infrastructure. The automotive sector in Europe is additionally exploring in-cabin wireless gigabit connections for infotainment systems, representing a promising growth avenue for the technology.

Asia-Pacific Wireless Gigabit Market Analysis

Asia-Pacific continues to lead the global wireless gigabit market, supported by the region’s dominant position in consumer electronics manufacturing, semiconductor fabrication, and telecommunications infrastructure development. China, Japan, South Korea, and India collectively drive substantial demand for wireless gigabit chipsets and modules across smartphones, laptops, gaming devices, and networking equipment. The region’s aggressive 5G rollout programs create a complementary infrastructure that enhances the value proposition of wireless gigabit technology for both consumer and enterprise applications. Government-backed digital transformation initiatives, including smart city development and industrial automation programs, further stimulate demand for high-speed wireless connectivity solutions. For instance, the global 5G services market size reached USD 184.6 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 4,426.4 Billion by 2033, exhibiting a growth rate (CAGR) of 42.34% during 2025-2033, reflecting the massive scale of wireless infrastructure expansion across the region.

Latin America Wireless Gigabit Market Analysis

Latin America is emerging as a developing market for wireless gigabit technology, supported by expanding telecommunications infrastructure and growing demand for high-speed broadband alternatives in both urban and underserved areas. The rollout of 5G networks in key economies such as Brazil and Mexico is establishing the foundational infrastructure that can support the integration of millimeter-wave and wireless gigabit solutions for fixed wireless access and enterprise connectivity. The region’s increasing smartphone penetration and digitalization of commercial sectors are generating demand for faster wireless data transfer capabilities. For instance, Brazil surpassed 50 million 5G accesses by the third quarter of 2025, demonstrating the accelerating pace of next-generation wireless adoption in the region.

Middle East and Africa Wireless Gigabit Market Analysis

The Middle East and Africa region presents emerging opportunities for the wireless gigabit market, driven by ambitious smart city initiatives, growing investments in telecommunications infrastructure, and increasing demand for high-speed wireless connectivity. Countries across the Gulf Cooperation Council are implementing large-scale digital transformation programs that necessitate advanced wireless technologies for smart infrastructure, surveillance systems, and enterprise networking. The defense and security sector in the region is also exploring millimeter-wave wireless solutions for secure, high-capacity communications in field operations. For instance, in 2025, defense and aerospace organizations increasingly adopted 60 GHz fixed wireless access systems for mission-critical communications, leveraging the technology’s narrow beamwidth and low probability of detection for secure field deployments.

Competitive Landscape:

The global wireless gigabit market features an actively competitive landscape, with established semiconductor companies and specialized wireless technology firms driving innovation in chipset design, module development, and system integration. Leading players are leveraging deep radio frequency portfolios, advanced fabrication capabilities, and strategic partnerships with device manufacturers to secure design wins across consumer electronics, enterprise networking, and telecommunications infrastructure. The competitive dynamics are characterized by continuous investment in research and development aimed at improving beamforming algorithms, reducing power consumption, and achieving greater levels of integration through system-on-chip architectures. Companies are also expanding their product portfolios to address emerging application areas, including fixed wireless access, tactical communications, and automotive infotainment connectivity, while simultaneously pursuing cost reduction strategies to enable penetration into mid-tier device segments and emerging markets.

The report provides a comprehensive analysis of the competitive landscape in the wireless gigabit market with detailed profiles of all major companies, including:

- Broadcom Inc

- Cisco Systems Inc.

- Intel Corporation

- Marvell Technology Inc.

- MediaTek Inc.

- Millitronic

- NXP Semiconductors N.V.

- Panasonic Corporation

- Peraso Technologies Inc.

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- Sivers Semiconductors AB

Latest News and Developments:

- In February 2026, the GFiber Multi-Gig Wi-Fi 7 Router introduced the company’s most advanced wireless technology to date and comes included at no additional charge with its Home 3 Gig and Edge 8 Gig plans, enabling seamless multi-gig performance throughout the residence without the need for extensive cabling.

- In July 2025, Tachyon Networks selected Peraso’s PRM2141X module for its latest outdoor 60 GHz fixed wireless solution, the TNA-303L-65. The system delivers up to 1 Gbps throughput with a range exceeding 3 kilometers and supports up to 48 client terminals per sector. The solution addresses the growing need for fiber-class wireless broadband in both urban and rural deployments.

Wireless Gigabit Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Technologies Covered | System on Chip (SoC) and Integrated Circuit Chip (IC Chip) |

| End Use Industries Covered | BFSI, Healthcare, IT and Telecom, Retail, Media and Entertainment, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Broadcom Inc, Cisco Systems Inc., Intel Corporation, Marvell Technology Inc., MediaTek Inc., Millitronic, NXP Semiconductors N.V., Panasonic Corporation, Peraso Technologies Inc., Qualcomm Technologies Inc., Samsung Electronics Co. Ltd., Sivers Semiconductors AB, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the wireless gigabit market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global wireless gigabit market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter’s Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the wireless gigabit industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Wireless Gigabit Market Report

The wireless gigabit market was valued at USD 4.1 Billion in 2025.

The wireless gigabit market is projected to exhibit a CAGR of 13.69% during 2026-2034, reaching a value of USD 14.32 Billion by 2034.

The wireless gigabit market is driven by the growing demand for ultra-high-speed wireless connectivity, proliferation of bandwidth-intensive applications such as virtual reality and augmented reality, increasing adoption of wireless docking in enterprises, expansion of 5G millimeter-wave infrastructure, and advancing system-on-chip integration that reduces costs and enhances device compatibility.

Asia-Pacific currently dominates the wireless gigabit market, accounting for a share of 36%. The region benefits from extensive consumer electronics manufacturing capabilities, rapid 5G deployment across major economies, significant government investments in digital infrastructure, and a thriving semiconductor ecosystem that accelerates the commercialization of wireless gigabit technologies.

Some of the major players in the wireless gigabit market include Broadcom Inc, Cisco Systems Inc., Intel Corporation, Marvell Technology Inc., MediaTek Inc., Millitronic, NXP Semiconductors N.V., Panasonic Corporation, Peraso Technologies Inc., Qualcomm Technologies Inc., Samsung Electronics Co. Ltd. and Sivers Semiconductors AB, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)