Wood Pellet Market Size, Share, Trends, and Forecast by Feedstock Type, Application, and Region, 2026-2034

Global Wood Pellet Market Size, Share, Trends & Forecast (2026-2034)

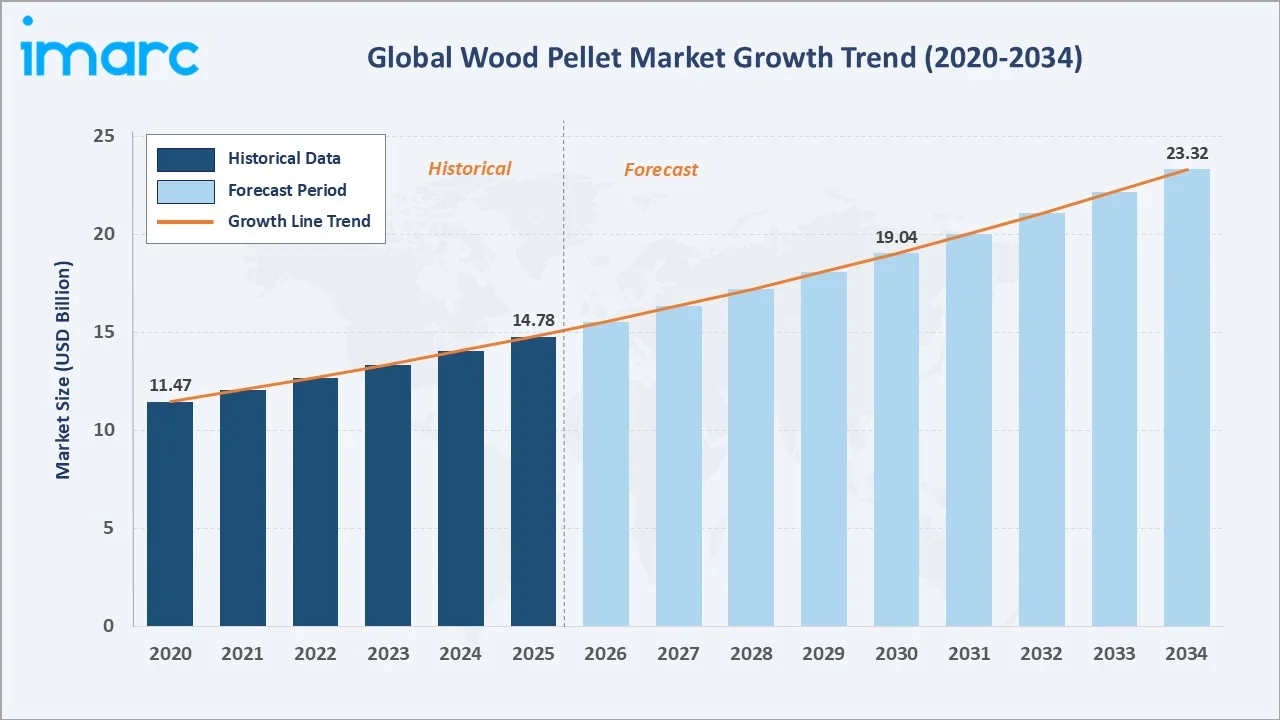

The global wood pellet market size reached USD 14.78 Billion in 2025 and is projected to reach USD 23.32 Billion by 2034, exhibiting a CAGR of 5.20% during 2026-2034. Rising demand for renewable energy, supportive government policies, and expanding biomass co-firing in power generation are the primary growth drivers.

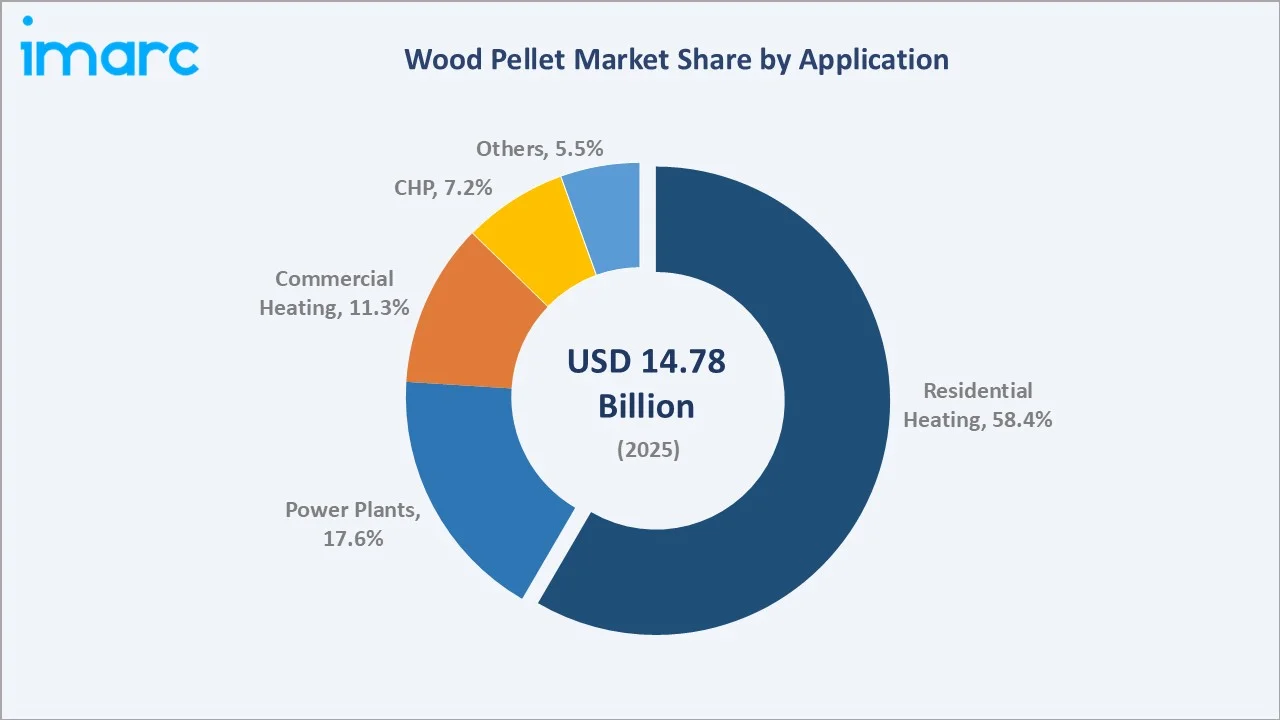

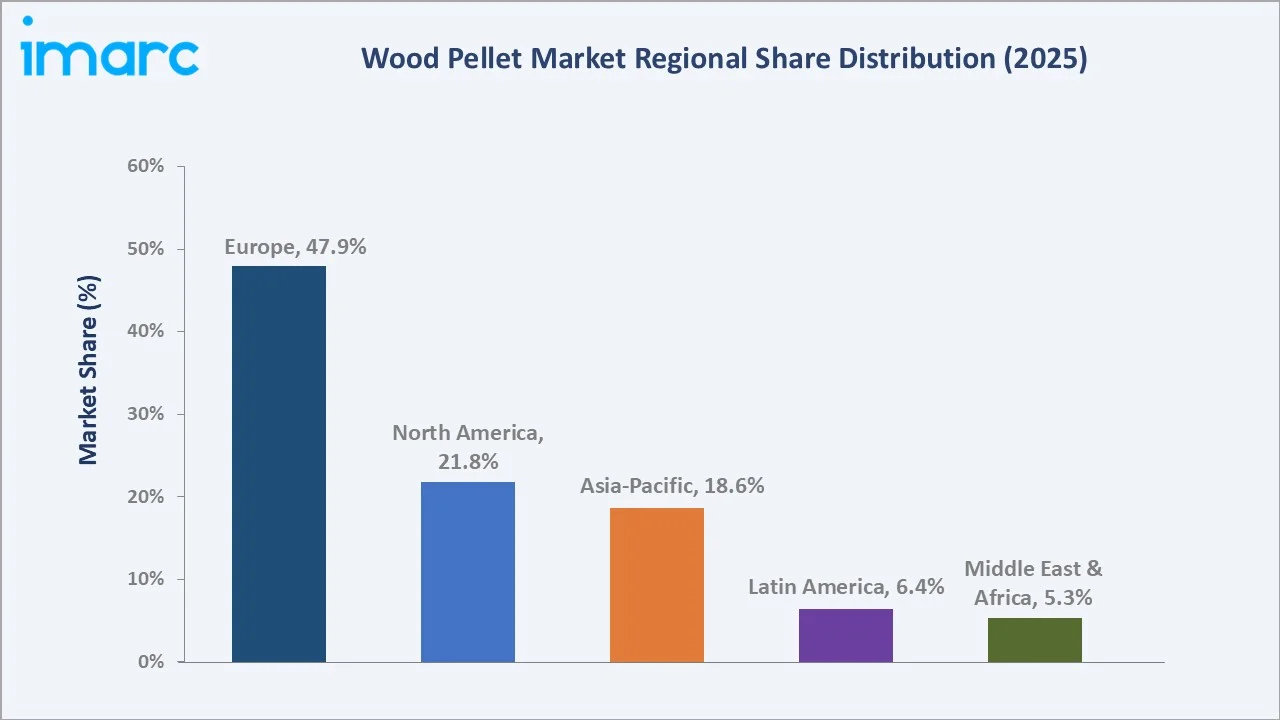

Residential Heating dominates application at 58.4% in 2025, while Forest Wood and Waste lead feedstock type at 33.6%. Europe commands the largest regional share at 47.9% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 14.78 Billion |

|

Forecast Market Size (2034) |

USD 23.32 Billion |

|

CAGR (2026-2034) |

5.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (47.9% share, 2025) |

|

Second Largest Region |

North America (21.8% share, 2025) |

|

Leading Feedstock Type |

Forest Wood and Waste (33.6%, 2025) |

|

Leading Application |

Residential Heating (58.4%, 2025) |

The global wood pellet market growth trajectory from 2020 through 2034, with the historical expansion to USD 14.78 Billion in 2025, reflects rising demand for renewable biomass energy. The forecast to USD 23.32 Billion captures accelerating energy transition investment, expanding residential and industrial heating adoption, and growing Asian utility co-firing demand.

To get more information on this market, Request Sample

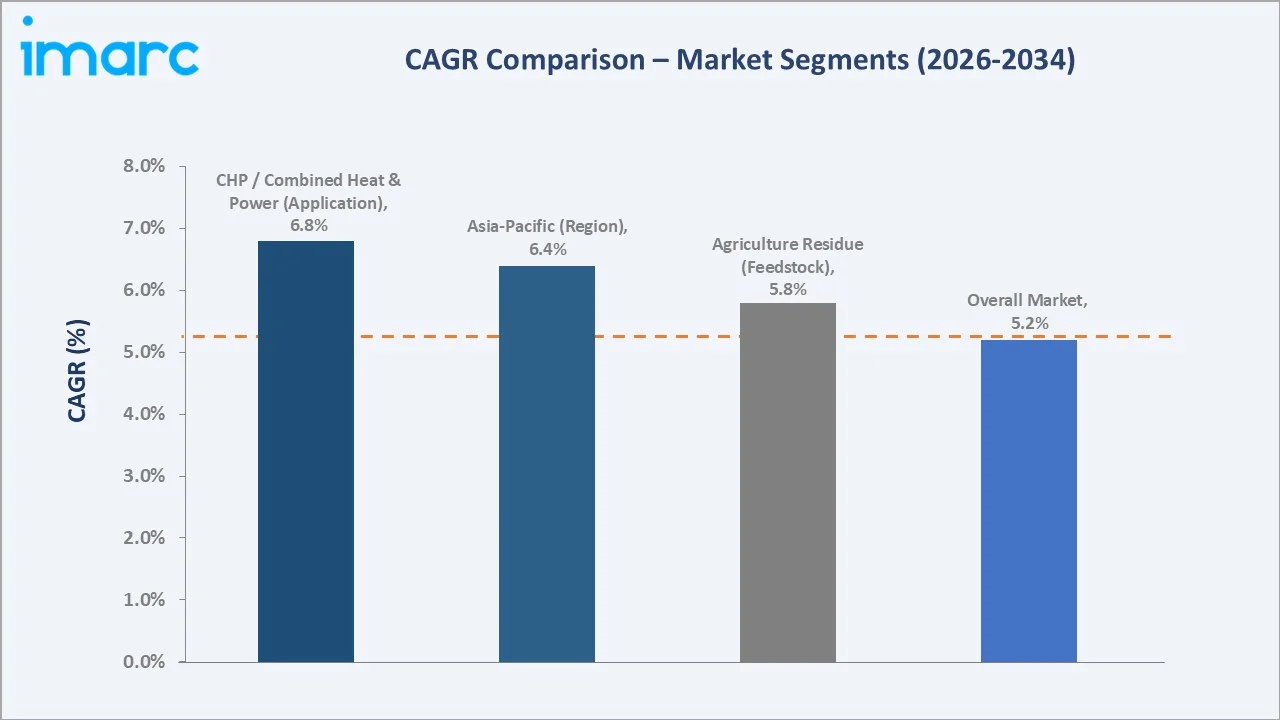

The CAGR trajectories across key feedstock type, application, and regional sub-segments, with CHP at ~6.8% CAGR and Asia-Pacific at ~6.4% CAGR, represent the fastest-growing categories within the global wood pellet industry through 2034.

Executive Summary

The global wood pellet market is on a sustained growth trajectory from USD 14.78 Billion in 2025 to USD 23.32 Billion by 2034. Wood pellets, compressed biomass fuel derived from forestry residues, agricultural waste, and wood processing byproducts, serve as a renewable substitute for coal and fossil fuels in heating and power generation.

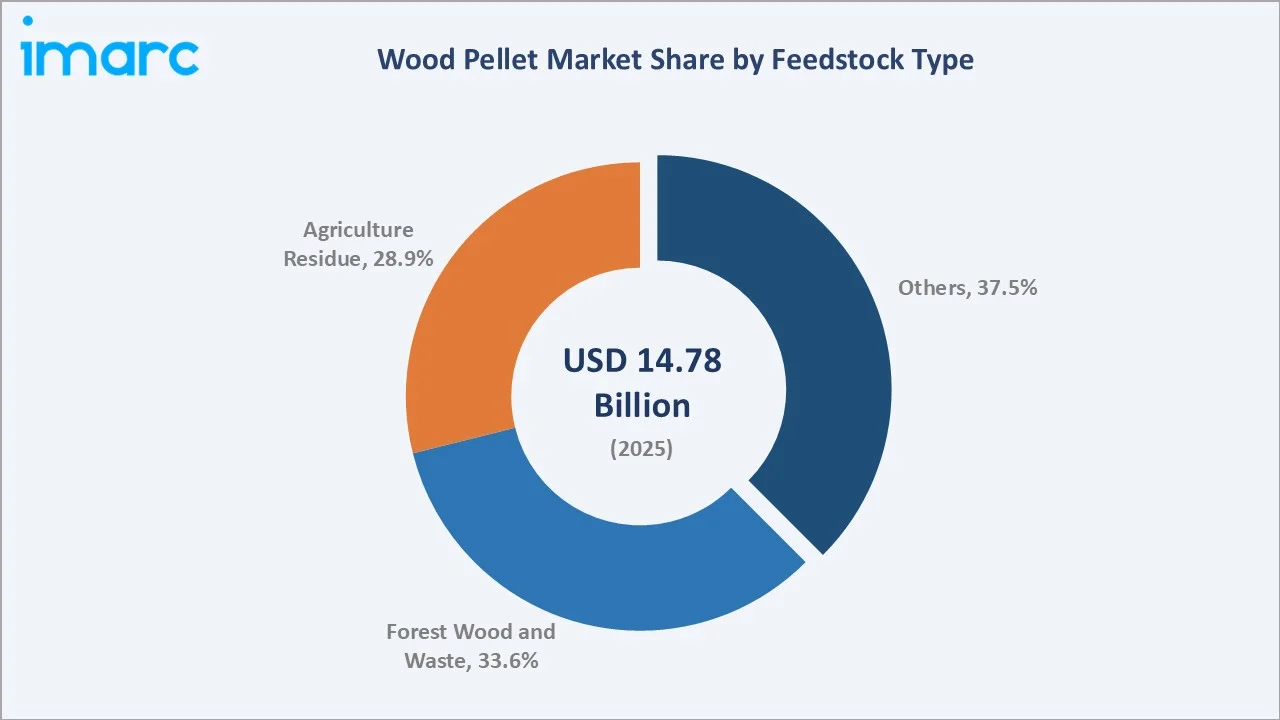

Forest Wood and Waste dominate feedstock type at 33.6% in 2025, owing to its widespread availability as sawmill byproducts, logging residues, and wood chips. Agriculture Residue (28.9%) reflects growing adoption of crop residues such as rice husks and straw as cost-effective pellet inputs, particularly in Asia and developing markets.

Residential Heating leads application at 58.4% in 2025, reflecting strong penetration in European households and North American markets as a carbon-neutral substitute for gas and oil systems. Europe (47.9%) dominates regionally, underpinned by EU Renewable Energy Directive mandates and carbon pricing mechanisms across member states.

Key Market Insights

|

Insight |

Data |

|

Largest Feedstock Type |

Forest Wood and Waste – 33.6% share (2025) |

|

Leading Application |

Residential Heating – 58.4% share (2025) |

|

Leading Region |

Europe – 47.9% share (2025) |

|

Second Largest Region |

North America – 21.8% share (2025) |

|

Top Companies |

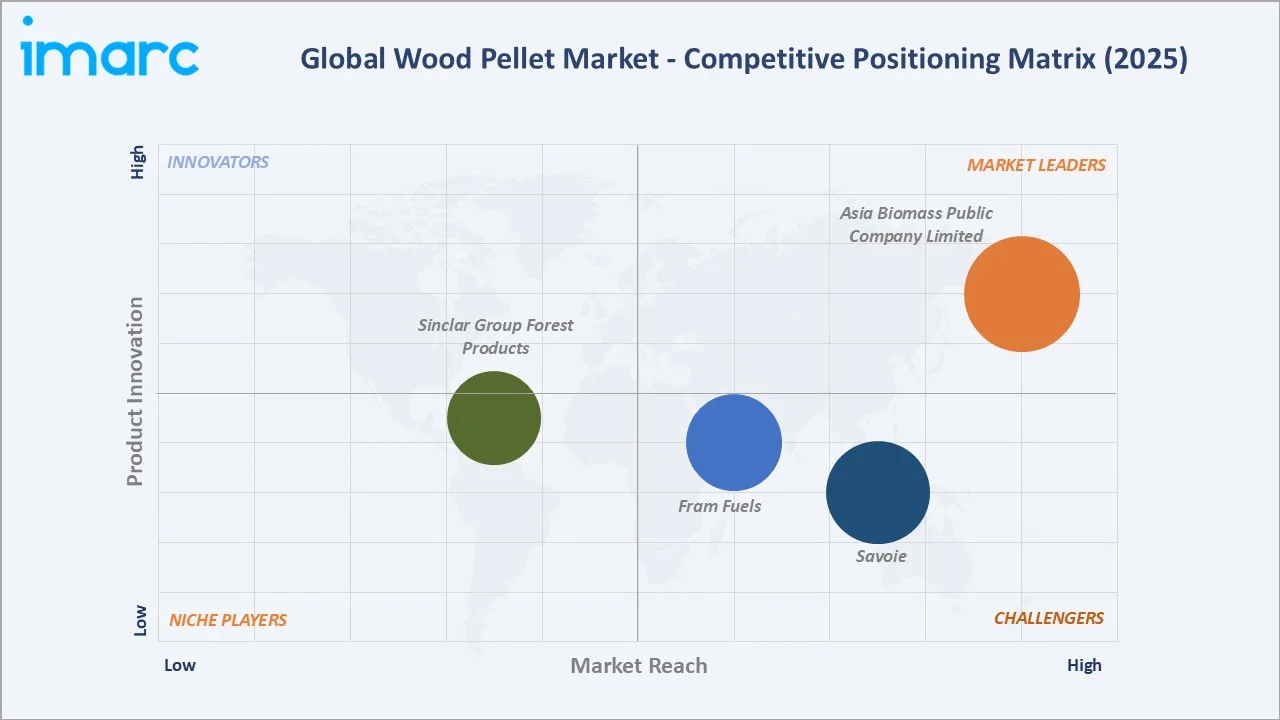

Asia Biomass Public Company Limited, Fram Fuels, Savoie, Sinclar Group Forest Products |

Key Analytical Observations Expanding on the Above Data:

- Forest Wood and Waste, with 33.6% in 2025, dominates because sawmill residues and forestry leftovers are low-cost, abundant inputs with established supply chain infrastructure across North America and Scandinavia, enabling consistent, large-scale production at competitive pricing.

- Residential Heating, with 58.4% in 2025, leads because pellet stoves and boilers are widely adopted across European households as cost-effective, carbon-neutral substitutes for gas and oil heating, supported by government subsidy programs across Germany, Italy, Austria, and France.

- Europe's 47.9% dominance reflects EU Renewable Energy Directive mandates, carbon pricing under the EU ETS, and deep infrastructure networks for pellet distribution and combustion technology, creating the most policy-supportive environment for biomass energy globally.

- North America, with 21.8% in 2025, benefits from a large production base serving export demand to Europe alongside growing domestic co-firing adoption in utility-scale power plants under clean energy policies.

Global Wood Pellet Market Overview

Wood pellets are cylindrical, compressed biomass fuel products manufactured by drying and pelletizing wood residues, forestry waste, agricultural residues, and energy crops under high pressure. Typically, 6–8 mm in diameter with a length of 10–30 mm, they offer high energy density, low moisture content (~8–10%), and standardized combustion properties meeting ENplus A1/A2 or ISO 17225 standards.

The global ecosystem integrates forestry and agriculture residue suppliers, pellet production facilities, logistics and port terminal operators, biomass trading intermediaries, and end-use consumers spanning residential heating, commercial HVAC, industrial heat processes, combined heat and power (CHP) plants, and utility-scale co-firing power stations.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

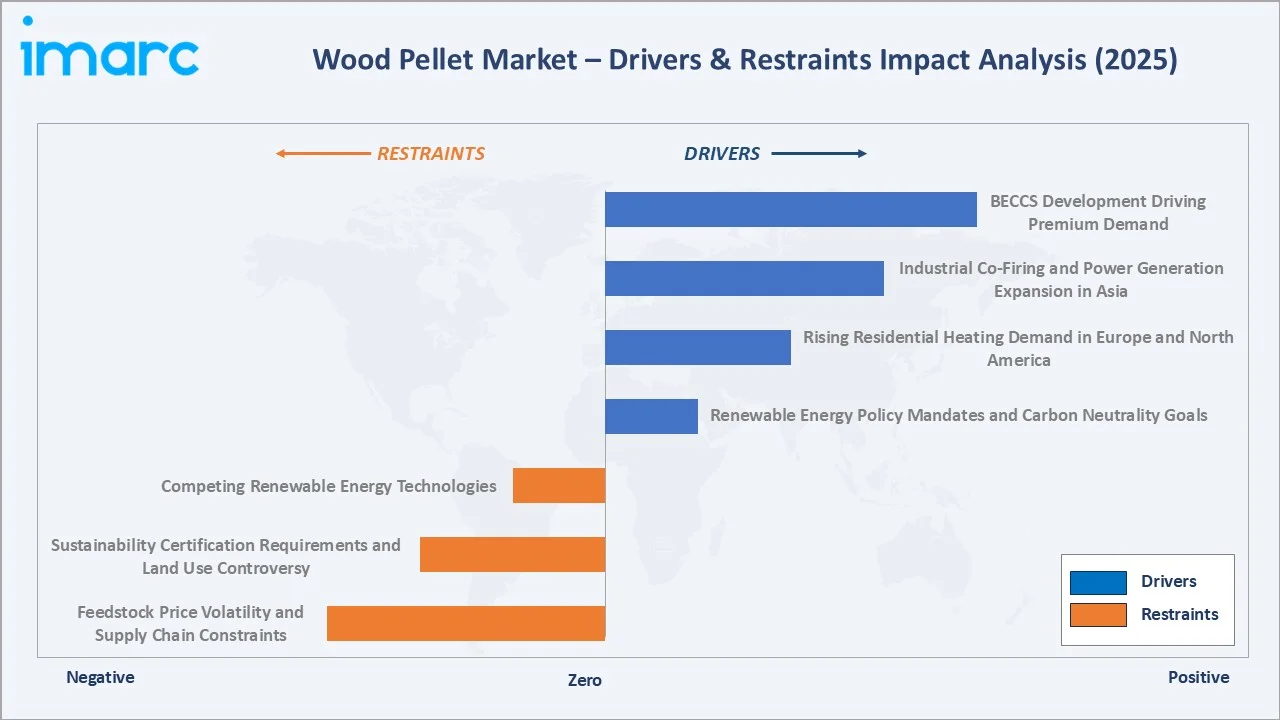

- Renewable Energy Policy Mandates and Carbon Neutrality Goals: The EU Renewable Energy Directive (RED III) mandates a 42.5% renewable energy share by 2030, directly driving biomass co-firing adoption and wood pellet demand across European utilities and industrial heat consumers.

- Rising Residential Heating Demand in Europe and North America: Over 12 million residential pellet heating installations exist across Europe, with Germany, Italy, Austria, and France leading adoption due to high fossil fuel heating costs and government subsidy programs supporting biomass boiler transitions.

- Industrial Co-Firing and Power Generation Expansion in Asia: South Korea's Renewable Portfolio Standard (RPS) mandates 25% renewable electricity by 2034, with wood pellet co-firing in coal plants as a primary compliance pathway, generating 10+ million metric ton annual import demand.

- BECCS Development Driving Premium Biomass Demand: Bioenergy with Carbon Capture and Storage (BECCS) projects position sustainably certified wood pellets as a negative emissions technology, creating premium demand from energy companies targeting net-negative carbon footprints through 2034.

Market Restraints

- Feedstock Price Volatility and Supply Chain Constraints: Wood residue availability is subject to competition from pulp and paper, engineered wood products, and direct bioenergy applications, with softwood lumber market cycles and forest management policy shifts tightening supply and pushing production costs higher.

- Sustainability Certification Requirements and Land Use Controversy: ENplus and Sustainable Biomass Program (SBP) certification requirements add compliance costs for producers, while ongoing EU sustainability criteria debates around forest carbon debt and indirect land use change create policy uncertainty for the market.

- Competing Renewable Energy Technologies: Falling solar PV and wind power costs increasingly compete with biomass power generation on a levelized cost basis, potentially reducing utility-scale wood pellet demand over the long term in markets without dedicated biomass incentive frameworks.

Market Opportunities

- Torrefied and Premium-Grade Pellet Development: Torrefied wood pellets, offering higher energy density and hydrophobic storage properties, are gaining traction for co-firing in pulverized coal plants without mill modifications, opening new utility customer segments with premium pricing potential.

- Asia-Pacific Demand Expansion via Renewable Portfolio Standards: Japan's Feed-in-Premium (FiP) scheme and South Korea's RPS are generating substantial long-term offtake contracts with North American and Southeast Asian producers, supporting new plant investment across the supply chain.

Market Challenges

- Logistical Complexity of International Pellet Trade: Long-distance pellet trade from North American production hubs to European and Asian end-users requires specialized port terminals, bulk vessels, and moisture-controlled storage, adding substantial logistical cost and supply chain risk.

- Skilled Workforce and Technical Expertise Shortage: The wood pellet industry faces a growing deficit of qualified engineers, pellet technologists, and certified quality auditors, constraining production capacity expansion and certification compliance across emerging producer markets in Southeast Asia and Latin America.

Emerging Market Trends

1. BECCS Integration Elevating Premium Biomass Demand

Bioenergy with Carbon Capture and Storage (BECCS) is emerging as a critical negative emissions technology within national climate strategies. Projects targeting annual CO2 removal represent the most advanced deployment, creating premium demand for sustainably certified, high-quality industrial wood pellets for BECCS-compatible power generation.

2. ENplus Certification Standardizing Global Quality Benchmarks

ENplus A1 certification is becoming a de facto requirement for residential and commercial heating pellet sales across Europe and increasingly in Asia. Producers investing in certified quality management systems gain access to premium pricing tiers, reducing commodity price pressure and improving margin stability over the forecast period.

3. Agricultural Residue Pellets Gaining Share in Emerging Markets

In India, Vietnam, and Thailand, agricultural residue pellets from rice husks, sugarcane bagasse, and crop straw are emerging as cost-competitive alternatives to forestry-based pellets, leveraging abundant waste streams to supply domestic industrial heating and export markets across the Asia-Pacific region.

4. Pellet Production Automation Reducing Operational Costs

Advanced pelletizing press technology, automated dryer systems with heat recovery, and AI-driven process optimization are reducing specific energy consumption in pellet manufacturing by 15–20%, enabling producers to improve margins and compete more effectively against fossil fuel alternatives.

Industry Value Chain Analysis

The wood pellet value chain spans six stages from raw biomass sourcing through end-use combustion. Pellet production and quality certification capture the highest value-add margins, while logistics and port terminal operations represent significant capital requirements that favor well-capitalized mid-to-large manufacturers.

|

Stage |

Key Activities / Description |

|

Raw Material Supply |

Forestry residues, sawmill byproducts, agricultural crop residues, and energy crops sourced via long-term supply agreements or spot procurement from regional suppliers |

|

Drying & Preparation |

Green biomass dried to below 12% moisture content using rotary drum or belt dryer systems with heat recovery integration to reduce primary energy input |

|

Pelletizing & Finishing |

Ring die pelletizing press compresses dried material into 6–8 mm pellets; cooling, screening, and dust removal produce market-ready product meeting density and durability standards |

|

Quality & Certification |

Independent third-party audits verify compliance with ENplus A1/A2, SBP, FSC, or PEFC certification schemes required for premium residential and utility-scale market access |

|

Logistics & Distribution |

Bulk shipping via specialized port terminals, containerized export for smaller consignments, and bagged retail distribution through national and regional distribution networks |

|

End-Use Consumption |

Residential pellet stoves and boilers, commercial district heating systems, utility-scale coal co-firing, dedicated biomass power plants, combined heat and power facilities |

Integrated producers with captive biomass supply agreements and in-house certification capabilities achieve lower feedstock cost bases and greater supply security than processors dependent on spot market residue procurement, providing a meaningful cost and reliability competitive advantage.

Technology Landscape in the Wood Pellet Industry

Pelletizing Press Technology: Flat Die to Ring Die Systems

Ring die pelletizing presses dominate industrial-scale production, capable of producing 2–10 tonnes per hour of standardized EN 17225-2 compliant pellets with bulk densities of 600–700 kg/m³. Modern high-pressure ring die systems achieve production efficiencies of 85–90% and specific energy consumption of 60–80 kWh per tonne, improving competitive economics at scale.

Drying Technology: Rotary Drum and Belt Dryer Systems

Green wood residues at 40–60% moisture content require energy-intensive drying to below 12% prior to pelletizing. Heat recovery systems integrating dryer exhaust heat with steam from biomass combustion reduce primary energy inputs by 30–40%, materially improving carbon efficiency and operating cost of pellet production facilities.

ENplus Digital Traceability and Chain of Custody Systems

Digital mass balance and chain of custody software platforms enable certification bodies and regulators to trace pellet flows from forest origin through to end-use combustion, satisfying EU RED III sustainability reporting requirements and enabling carbon credit verification for BECCS applications globally.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Feedstock Type |

Forest Wood and Waste |

33.6% |

2025 |

|

Application |

Residential Heating |

58.4% |

2025 |

|

Region |

Europe |

47.9% |

2025 |

By Feedstock Type

Forest Wood and Waste commands a 33.6% majority share in 2025 owing to the fundamental cost-competitiveness of sawmill residues, wood chips, and forestry leftovers as pellet inputs. The established supply chain infrastructure in North American and European forestry regions supports consistent raw material availability for large-scale production facilities.

To access detailed market analysis, Request Sample

Agriculture Residue at 28.9% in 2025, growing rapidly, reflects expanding use of crop residues including rice husks, sugarcane bagasse, and wheat straw, particularly in Asian and developing markets where forestry residues are limited. Others (37.5%) encompass energy crops, urban wood waste, and industrial process byproducts diversifying feedstock inputs.

By Application

Residential Heating dominates the application segment at 58.4% in 2025, representing the largest and most established end-use market. The combination of European government subsidy programs for biomass boiler installations and rising fossil fuel heating costs underpins sustained demand, particularly in Germany, Italy, Austria, France, and the UK.

Power Plants (17.6%) in 2025 reflect utility-scale co-firing and dedicated biomass power generation driven by renewable portfolio standard compliance. Commercial Heating (11.3%) serves district heating systems, hotels, and institutional buildings.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

47.9% |

EU RED III mandates; carbon pricing; established pellet heating and power generation infrastructure |

|

North America |

21.8% |

Large production base; export demand; domestic co-firing adoption under clean energy incentives |

|

Asia-Pacific |

18.6% |

South Korea and Japan RPS; Vietnam production expansion; India industrial biomass demand |

|

Latin America |

6.4% |

Agricultural residue pellet production growth; emerging biomass energy demand in major economies |

|

Middle East & Africa |

5.3% |

Emerging biomass energy interest; industrial fuel switching; forestry-based pellet exports |

Europe's 47.9% market dominance in 2025 is driven by the most policy-supportive environment globally for biomass energy. Germany, Italy, Austria, France, and the UK collectively account for the majority of European pellet consumption, spanning residential heating, commercial district heating, and utility-scale power generation co-firing.

North America, with 21.8% in 2025, is experiencing production-led growth, with the United States exporting 10 million metric tons of wood pellets in 2024, predominantly to European utilities. Canada's British Columbia and Quebec provinces host major production facilities supplying both domestic and export markets globally.

Competitive Landscape

The global wood pellet market is moderately fragmented, with large integrated producers holding dominant positions in export-oriented trade while numerous regional producers serve domestic residential and commercial heating markets.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Asia Biomass Public Company Limited |

Wood pellets |

Leader |

Southeast Asia; agricultural residue pellets; Thailand and ASEAN market supply |

|

Fram Fuels |

Premium residential and commercial wood pellets |

Challenger |

European and Asian markets; premium certified product differentiation strategy |

|

Savoie |

Wood pellet |

Challenger |

Premium residential heating |

|

Sinclar Group Forest Products |

Premium Wood Pellet |

Emerging |

British Columbia; export-oriented production targeting Asian and European utility markets |

Key players include Asia Biomass Public Company Limited, Fram Fuels, Savoie, Sinclar Group Forest Products, and others.

Key Company Profiles

Fram Fuels

Fram Renewable Fuels, LLC is a US-based wood pellet producer headquartered in Georgia, established in 2005 as one of the first large-scale pellet manufacturers in the US Southeast. The company operates multiple pellet mills across Georgia, supplying both industrial export and residential heating markets.

- Product Portfolio: Premium residential and commercial wood pellets

- Strategic Focus: Fram's strategy focuses on leveraging its US Southeast production cost advantage and established European industrial customer relationships to grow long-term offtake contract volumes, while diversifying into residential ENplus-certified pellets to capture margin uplift from the premium domestic heating market.

Sinclar Group Forest Products

Sinclar Group Forest Products is a family-owned, vertically integrated forest products company headquartered in Prince George, British Columbia, operating lumber mills and the Premium Pellet manufacturing facility in Vanderhoof, BC.

- Product Portfolio: Premium Wood Pellet

- Strategic Focus: Sinclar's pellet strategy leverages its integrated forest management and lumber operations to secure a consistent, low-cost white wood waste fibre stream for Premium Pellet, targeting the bulk overseas export market, primarily Japan and South Korea, where SBP-certified British Columbia softwood pellets command stable long-term utility supply contracts.

Market Concentration Analysis

The global wood pellet market is moderately fragmented at the global level, reflecting significant regional concentration among national producers and export-oriented large-scale manufacturers. No single company holds more than 8–10% of total global market revenue, given the breadth of regional production across North America, Europe, and Asia-Pacific.

Consolidation at the production level is occurring primarily through large energy companies acquiring pellet producers to secure biomass supply. The acquisition of Pinnacle Renewable Energy is the most significant recent consolidation, creating the world's largest vertically integrated biomass energy and pellet supply organization with operations across multiple continents.

Investment & Growth Opportunities

Fastest-Growing Segments

CHP applications at ~6.8% CAGR through 2034 represent the highest-growth end-use segment, driven by European energy efficiency directives mandating higher CHP penetration in industrial and municipal heat supply. Asia-Pacific at ~6.4% CAGR is the fastest-growing region, with South Korea, Japan, and Vietnam generating the most significant incremental demand volumes.

Emerging Markets

Southeast Asia, particularly Vietnam and Indonesia, represents the most compelling emerging market opportunity for wood pellet production, combining large agricultural residue feedstock availability, low production costs, and growing proximity to Japanese and Korean export markets. Vietnam exported 2.6 million tons of wood pellets in 2024, reflecting rapid capacity expansion.

Venture & Investment Trends

Long-term offtake contracts with creditworthy European and Asian utility counterparties are enabling project finance investment in new pellet production facilities, with typical 10–15-year contracts providing sufficient revenue certainty for debt financing. BECCS project development is attracting carbon credit monetization interest from financial investors and ESG-focused energy companies.

Future Market Outlook (2026-2034)

The global wood pellet market is forecast to expand from USD 14.78 Billion in 2025 to USD 23.32 Billion by 2034 at a CAGR of 5.20%, adding USD 8.54 Billion in incremental annual market value over the forecast period. This sustained growth reflects biomass energy's role as a dispatchable, carbon-neutral renewable energy source in heating and power generation.

Three structural forces will most significantly shape the wood pellet market through 2034. EU RED III compliance requirements will maintain strong European import demand. Asian RPS and FiP schemes in South Korea and Japan will generate growing Pacific Basin demand. BECCS project development will create premium pricing for certified, high-quality industrial pellets meeting negative emissions verification requirements across major economies.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews with wood pellet industry stakeholders, including senior commercial managers at pellet producers, utility biomass procurement teams, ENplus and SBP certification managers, and residential heating system distributors across Europe, North America, and Asia-Pacific regions.

Secondary Research

Key secondary sources include the Wood Pellet Association of Canada, Bioenergy Europe Pellet Report, IEA Bioenergy Task 40 reports, European Biomass Association (AEBIOM) statistics, FAO forestry residue data, US EIA bioenergy reports, and trade publications including Biomass Magazine and Argus Biomass Markets.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating energy policy trajectories, renewable energy capacity addition forecasts, feedstock availability assessments, and historical market evolution patterns, with scenario analysis for base, optimistic, and conservative outcomes.

Wood Pellet Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Feedstock Types Covered | Forest Wood and Waste, Agriculture Residue, Others |

| Applications Covered | Power Plants, Residential Heating, Commercial Heating, Combined Heat and Power (CHP), Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Asia Biomass Public Company Limited, Fram Fuels, Savoie, Sinclar Group Forest Products, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the wood pellet market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global wood pellet market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the wood pellet industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Wood Pellets Market Report

The global wood pellet market reached USD 14.78 Billion in 2025, reflecting consistent demand driven by European renewable energy mandates, residential heating adoption, and expanding Asian utility co-firing demand across the forecast period.

The market is projected to reach USD 23.32 Billion by 2034, growing at a CAGR of 5.20% during 2026-2034, driven by EU RED III compliance, Asian RPS demand, and expanding BECCS applications in major energy-producing economies.

Forest Wood and Waste lead with a 33.6% feedstock share in 2025, valued for its cost-effectiveness and widespread availability as sawmill residues and forestry byproducts in North America, Scandinavia, and other major timber-producing regions.

Residential Heating leads at 58.4% in 2025, representing widespread European household adoption of pellet stoves and boilers as cost-effective, carbon-neutral substitutes for gas and oil heating systems, supported by government subsidy programs.

Europe commands a dominant 47.9% market share in 2025, driven by EU renewable energy mandates, carbon pricing, and established biomass heating and power generation infrastructure across member states creating consistent long-term demand.

Leading companies include Asia Biomass Public Company Limited, Fram Fuels, Savoie, Sinclar Group Forest Products, and others.

Combined Heat and Power (CHP) are the fastest-growing application at ~6.8% CAGR through 2034, driven by European energy efficiency directives and industrial decarbonization programs mandating higher combined heat and power penetration in industrial and municipal facilities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade