Rare Earth Magnet Market Size, Share, Trends and Forecast by Magnet Type, Application, and Region, 2026-2034

Global Rare Earth Magnet Market Size, Share, Trends & Forecast (2026-2034)

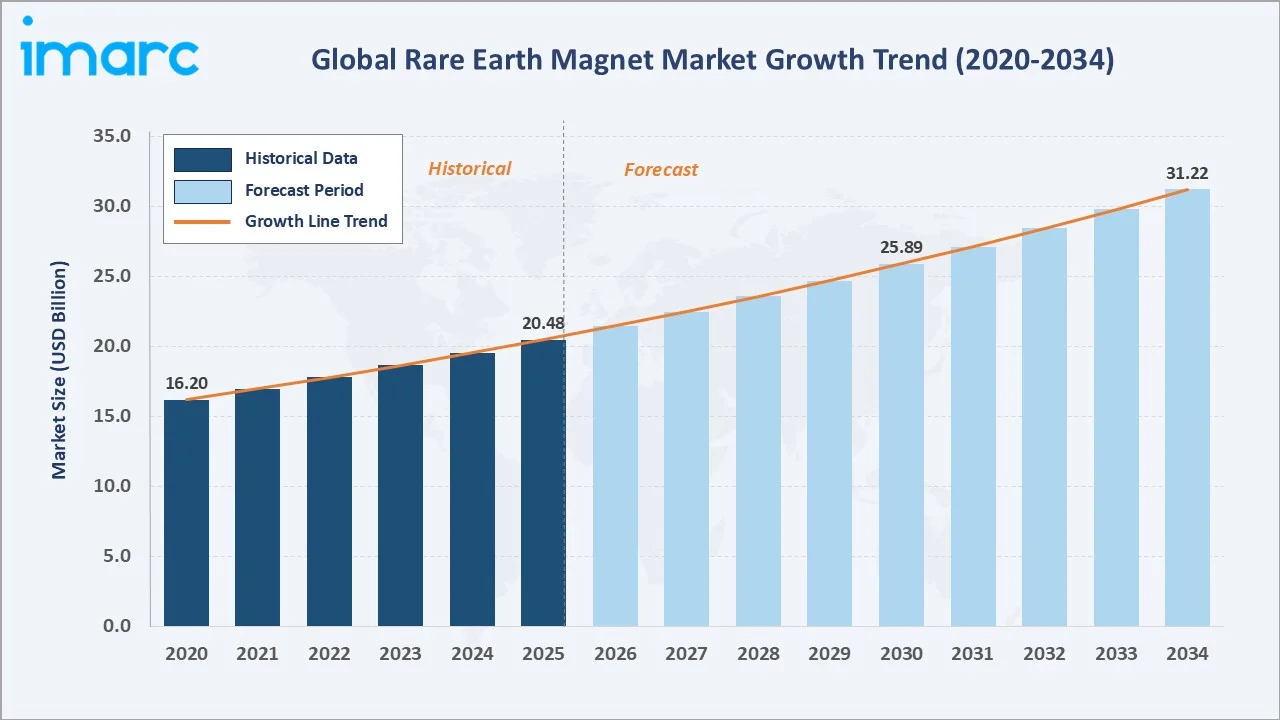

The global rare earth magnet market size reached USD 20.48 Billion in 2025 and is projected to reach USD 31.22 Billion by 2034, exhibiting a CAGR of 4.80% during 2026-2034. Accelerating global electrification with EV adoption rising sharply, rapid expansion of offshore and onshore wind energy, and growing demand for industrial automation and robotics are the primary forces driving rare earth magnet market growth.

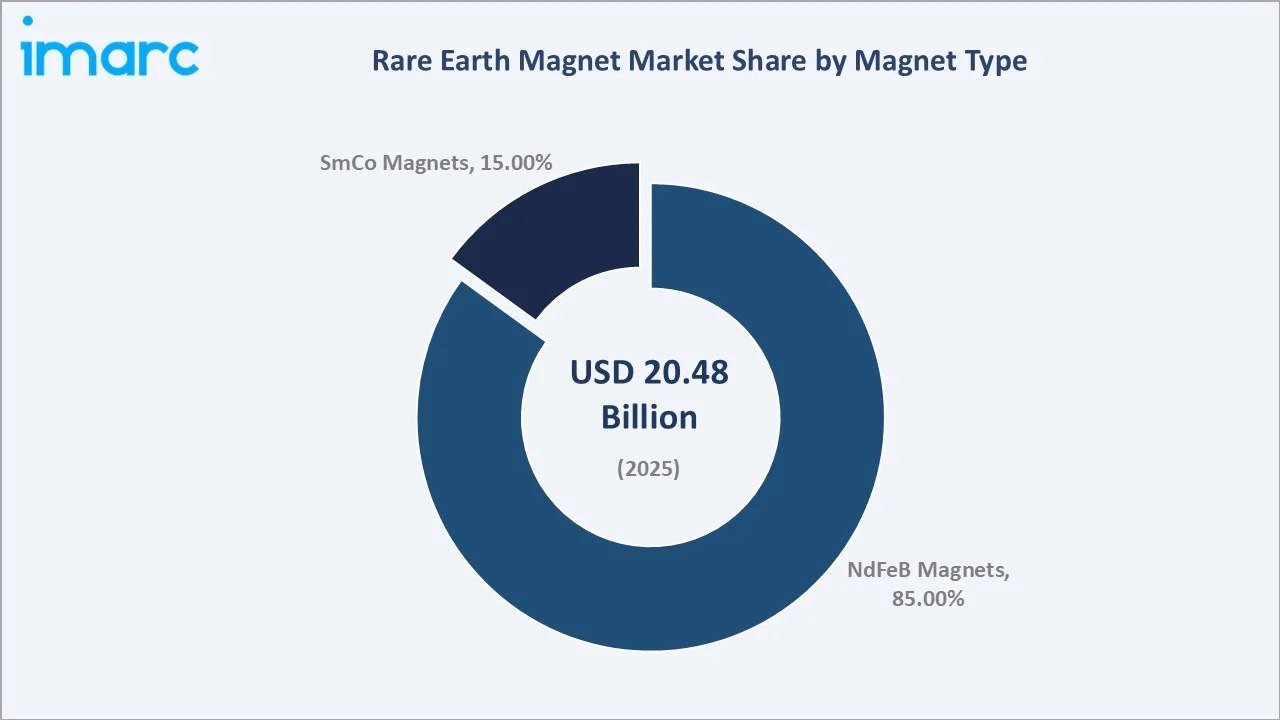

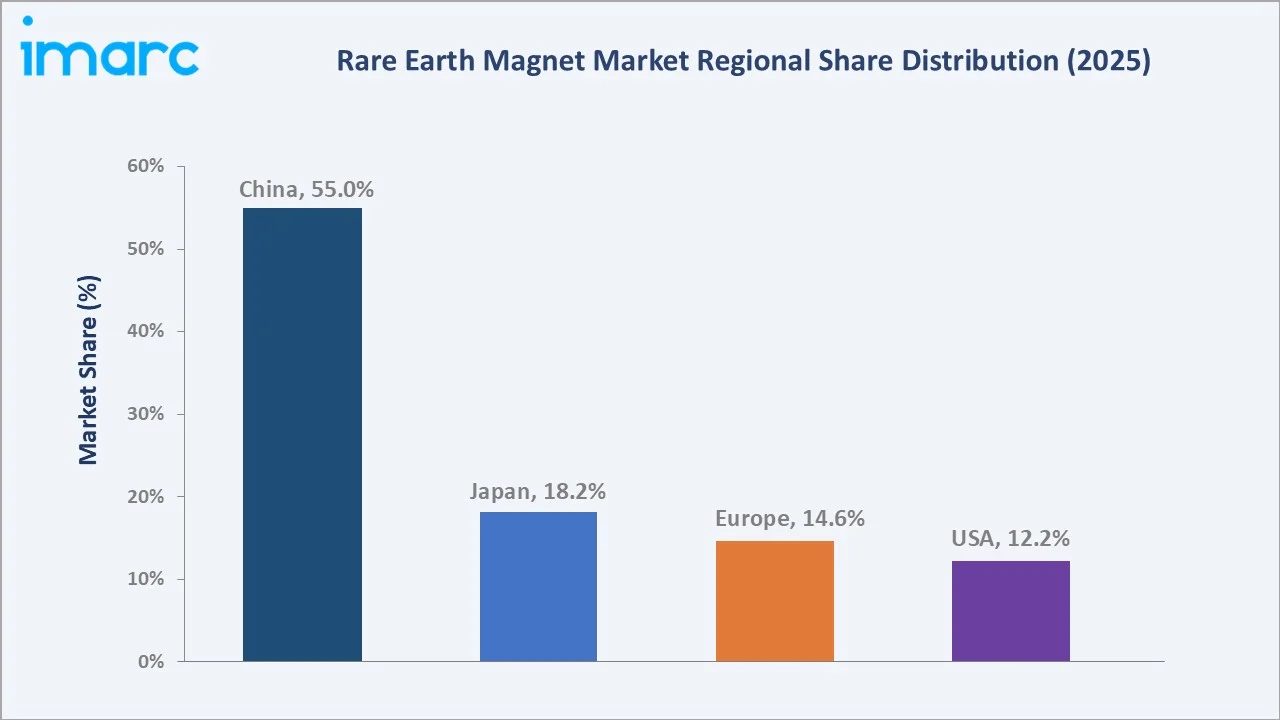

NdFeB magnets dominate the magnet type at 85.0% in 2025, while China commands a dominant 55.0% regional share in 2025, reflecting its vertically integrated rare earth supply chain.

Market Snapshot

|

Metric |

Value |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Market Size (2025) |

USD 20.48 Billion |

|

Forecast Market Size (2034) |

USD 31.22 Billion |

|

CAGR (2026-2034) |

4.80% |

|

Largest Region |

China (55.0% share, 2025) |

|

Leading Magnet Type |

NdFeB Magnets (85.0%, 2025) |

|

Leading Application |

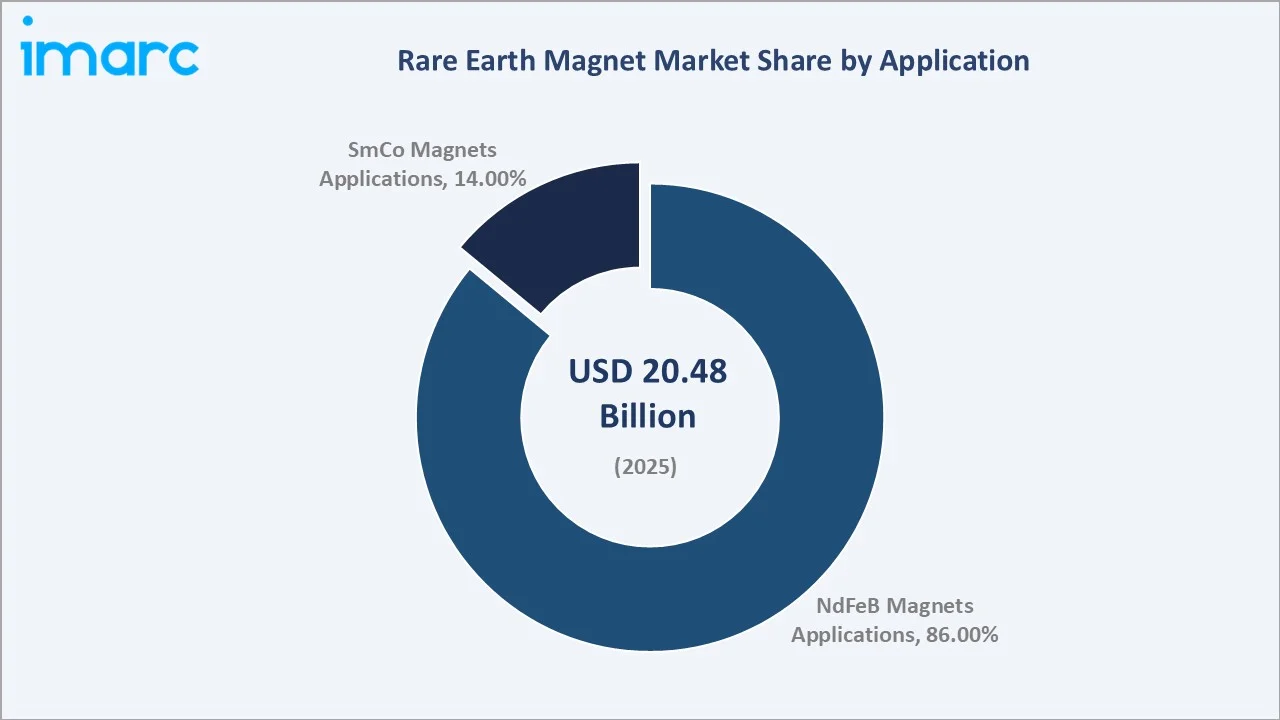

NdFeB Magnets Application (86%, 2025) |

|

Key Companies |

Arnold Magnetic Technologies, ADAMS Magnetic Products Co., Bunting Magnetics Co., Hangzhou Permanent Magnet Group Co. Ltd., Ningbo Ninggang Permanent Magnetic Materials Co., Ltd., Ningbo Ketian Magnet Co. Ltd., Thomas & Skinner Inc. |

The global rare earth magnet market growth trajectory from 2020 through 2034, with the historical expansion to USD 20.48 Billion in 2025, reflects consistent electrification-driven demand, while the forecast to USD 31.22 Billion captures accelerating EV motor, wind turbine generator, and industrial robotics-led magnet consumption across all major economies.

To get more information on this market, Request Sample

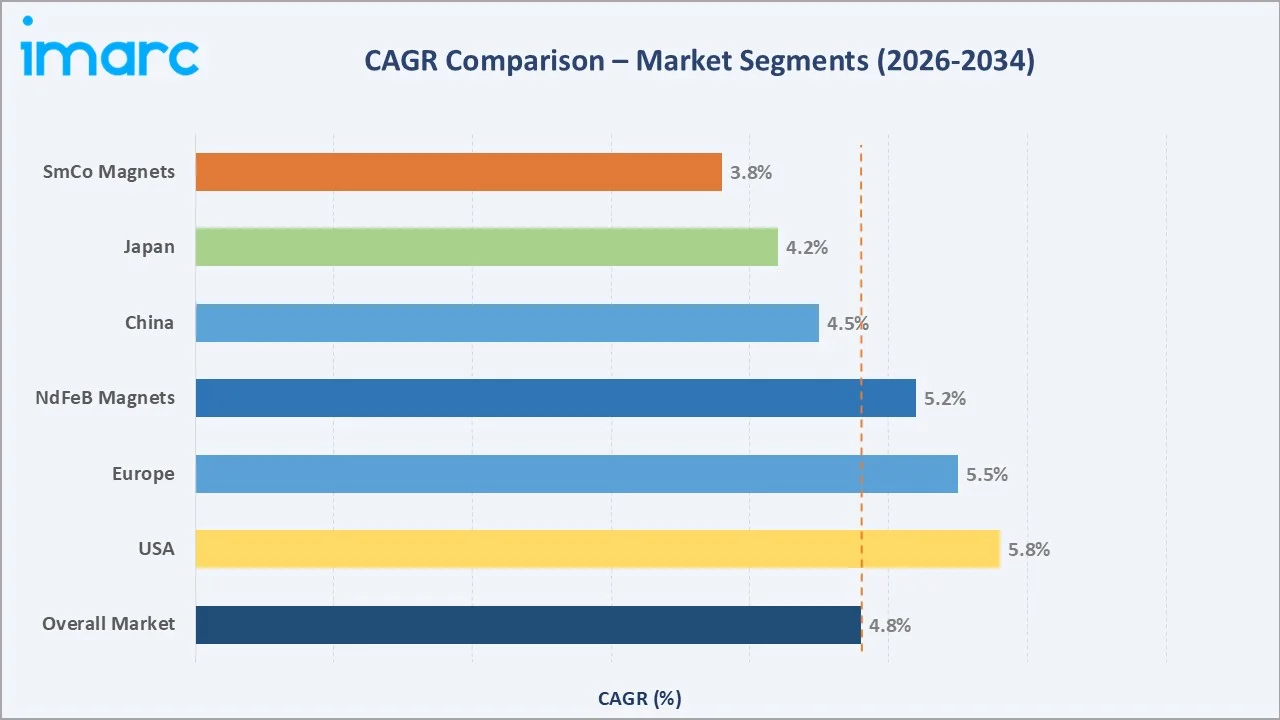

The CAGR trajectories across key magnet type, application, and regional sub-segments, with Europe and the USA growing at approximately 5.5–5.8% CAGR and NdFeB magnets at approximately 5.2% CAGR, represent the fastest-growing categories within the global rare earth magnet industry analysis through 2034.

Executive Summary

The global rare earth magnet market is on a sustained growth trajectory from USD 20.48 Billion in 2025 to USD 31.22 Billion by 2034. Rare earth magnets, essential enabling components in electric vehicle traction motors, wind turbine generators, industrial robots, consumer electronics, defense systems, and precision medical equipment, benefit from the non-discretionary nature of their demand across the global energy and mobility transition.

NdFeB magnets dominate the magnet type at 85.0% in 2025, owing to their unmatched magnetic energy product and broad applicability across EV motors, electronics, power generators, and wind applications. SmCo magnets (15.0%) command premium pricing in high-temperature and mission-critical defense, aerospace, and medical device applications where no viable substitute exists.

China's 55.0% dominance in 2025 reflects the country's vertically integrated rare earth supply chain, from mining through sintered magnet production, at cost structures that remain difficult for other regions to replicate.

Japan (18.2%), Europe (14.6%), and the USA (12.2%) follow, driven by high-performance specialty magnet demand, EV drivetrain localization initiatives, and strategic supply chain diversification investments in response to China's April 2025 export controls on NdFeB and SmCo magnet materials.

Key Market Insights

|

Insight |

Data |

|

Largest Magnet Type |

NdFeB Magnets – 85.0% share (2025) |

|

Leading Application |

NdFeB Magnets – 86% share (2025) |

|

Leading Region |

China – 55.0% revenue share (2025) |

|

Second Region |

Japan – 18.2% revenue share (2025) |

|

Top Companies |

Arnold Magnetic Technologies, ADAMS Magnetic Products Co., Bunting Magnetics Co., Hangzhou Permanent Magnet Group Co. Ltd., Ningbo Ninggang Permanent Magnetic Materials Co., Ltd., Ningbo Ketian Magnet Co. Ltd., Thomas & Skinner Inc. |

Key Analytical Observations Expanding On The Above Data:

- NdFeB Magnets at 85.0% in 2025 dominate because of their superior energy product (up to 52 MGOe), enabling compact motor designs critical for EV range optimization, drone efficiency, and miniaturized electronics. Growing global EV penetration, driven by regulatory mandates across the EU, China, and USA, reinforces NdFeB magnet market leadership through the forecast period.

- SmCo Magnets at 15.0% in 2025 server application segments where material substitution is technically impossible. Operating temperatures up to 350°C, exceptional corrosion resistance without coatings, and superior radiation stability make SmCo magnets irreplaceable in aerospace propulsion, satellite components, and downhole instrumentation.

- China's 55.0% regional dominance reflects multiple structural advantages: the country processes approximately 85–90% of global rare earth elements through refining and separation stages. China's domestic EV market, the world's largest, creates captive NdFeB magnet demand reinforcing its integrated supply chain.

- Japan at 18.2% has leveraged decades of precision NdFeB manufacturing expertise, including pioneering grain-boundary diffusion processing that maximizes coercivity while reducing dysprosium content. Japanese manufacturers serve high-value automotive, precision electronics, and industrial markets.

Global Rare Earth Magnet Market Overview

Rare earth magnets are a class of permanent magnets manufactured from alloys of rare earth elements, primarily neodymium-iron-boron (NdFeB) and samarium-cobalt (SmCo). These magnets generate exceptionally strong magnetic fields relative to their volume, enabling product miniaturization, improved motor efficiency, and superior performance-to-weight ratios compared to ferrite or alnico alternatives. NdFeB magnets offer the highest energy product of any permanent magnet material commercially available in 2025, while SmCo magnets provide superior thermal stability and corrosion resistance at premium cost.

The global ecosystem integrates rare earth mining companies, separation and refining facilities, rare earth oxide and metal manufacturers, alloy producers, sintered and bonded magnet fabricators, surface treatment providers, specialty distributors, and diverse end-use industries spanning electric vehicles, wind power, consumer electronics, industrial automation, defense, aerospace, and medical devices. Magnet recycling from end-of-life products is emerging as a strategically important supply chain layer, particularly as rare earth supply constraints intensify.

Market Dynamics

To evaluate market opportunities, Request Sample

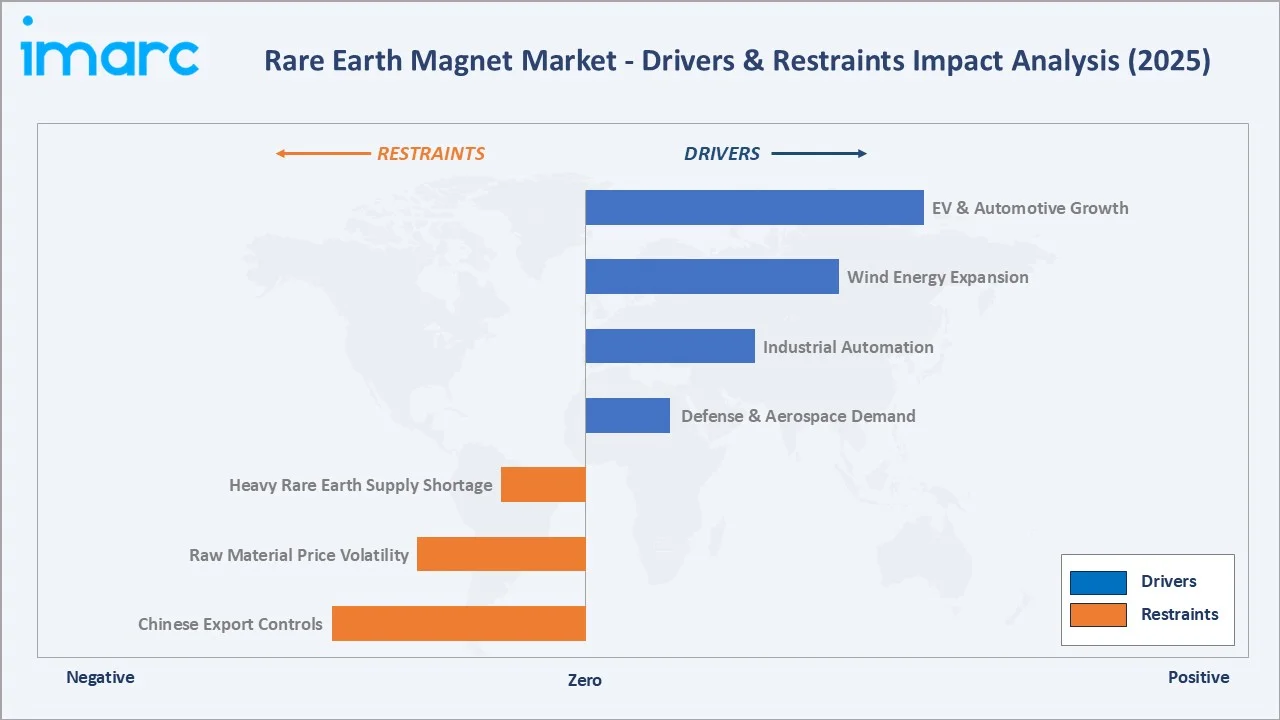

Market Drivers

- Electric Vehicle and Automotive Industry Growth: Global EV sales surpassed 17 million units in 2024, each battery EV requiring 1–3 kg of sintered NdFeB magnet in traction motors. Regulatory mandates across the EU, China, and North America accelerating ICE vehicle phase-outs ensure sustained multi-decade NdFeB magnet demand expansion.

- Wind Energy Infrastructure Expansion: Global Wind Energy Council forecasts require 15,000 tons of rare earth magnets annually for wind applications by 2027. Direct-drive offshore turbines require up to 232 kg of NdPr oxide per MW, creating substantial high-volume procurement cycles.

- Industrial Automation and Robotics: Rising adoption of collaborative robots, CNC systems, and humanoid robots, which use NdFeB actuators extensively, is creating a new high-growth demand category projected by IDTechEx to become a leading NdFeB consumption driver by 2040.

Market Restraints

- Chinese Export Controls and Geopolitical Risk: China's April 2025 export controls on NdFeB and SmCo magnet materials caused immediate supply disruptions across defense, automotive, and electronics OEM sectors globally, exposing critical single-source dependency vulnerabilities.

- Raw Material Price Volatility: Prices of rare earth elements neodymium, dysprosium, and terbium are subject to significant volatility driven by Chinese mining quota policy, export regulations, and speculative inventory cycles, creating input cost unpredictability for magnet manufacturers.

Market Opportunities

- Supply Chain Diversification Investment: The US DoD's USD 400 million commitment to MP Materials in 2025, EU Critical Raw Materials Act provisions, and Japan's rare earth stockpiling programs are catalyzing new magnet manufacturing capacity outside China, creating greenfield investment opportunities.

- Magnet Recycling and Circular Economy: Growing end-of-life EV and wind turbine volumes are creating a scalable rare earth magnet recycling market. By 2040, an estimated 240,000 tonnes shortage in rare earth magnets is projected, driving commercial recycling urgency and investment.

Market Challenges

- Heavy Rare Earth Availability: Dysprosium and terbium, used to enhance NdFeB coercivity for high-temperature applications, are predominantly sourced from China's ionic clay deposits. Limited alternative supply sources constrain magnet grade performance for automotive applications.

- Skilled Workforce and Technology Transfer Barriers: Establishing competitive sintered NdFeB magnet production outside China requires decades of accumulated process knowledge and specialized workforce development that cannot be rapidly replicated through capital investment alone.

Emerging Market Trends

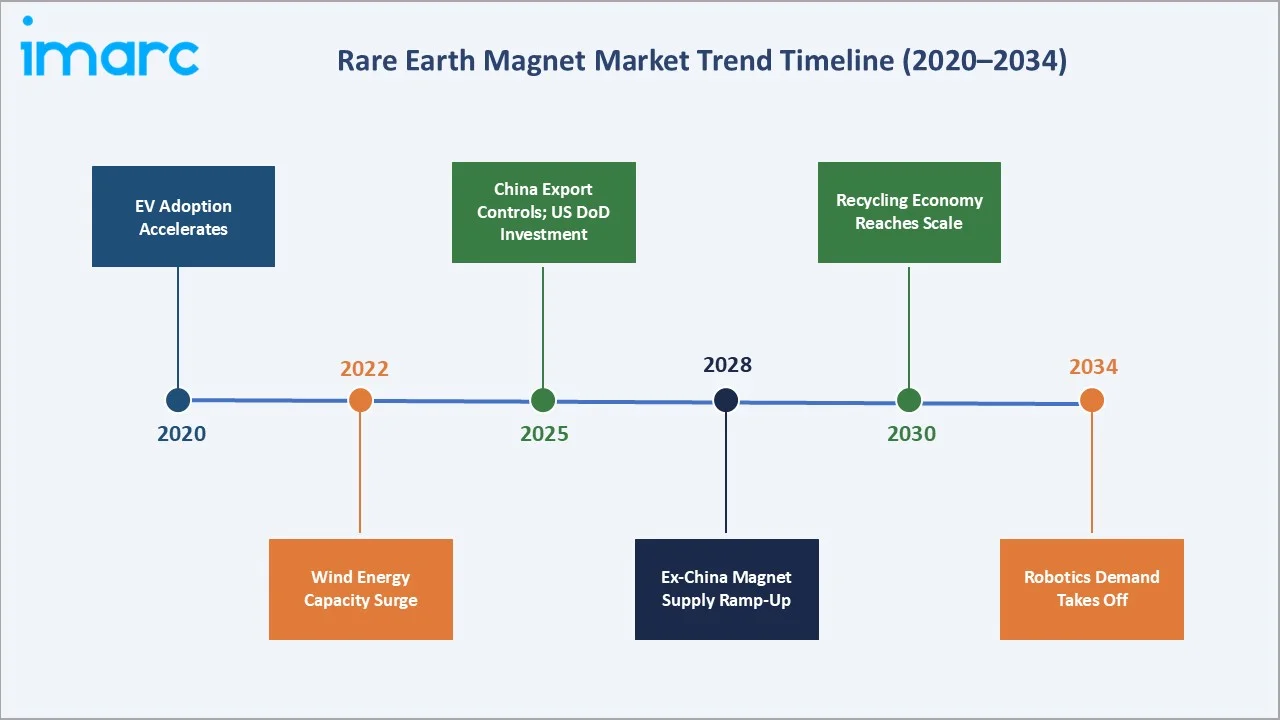

1. Surging Electric Vehicle Adoption Driving NdFeB Magnet Demand

The rapid global proliferation of battery electric vehicles and plug-in hybrid EVs is the single most consequential demand driver for the rare earth magnet market outlook through 2034. NdFeB magnets power permanent magnet synchronous motors (PMSM), the dominant EV drivetrain architecture, due to superior torque density and energy efficiency. Each EV traction motor requires 1–3 kg of sintered NdFeB, with premium performance models requiring higher quantities.

2. Wind Energy Expansion Fueling High-Volume Magnet Procurement

Rare earth magnet market trends are deeply interlinked with global wind energy capacity additions. Direct-drive permanent magnet synchronous generators, increasingly specified for offshore wind, require up to 650 kg of permanent magnet per MW in low-speed designs. The Global Wind Energy Council predicted 15,000 tons of rare earth magnet requirements for wind applications by 2027. As global annual wind installations expand, magnet manufacturers face sustained procurement pressure, creating long-term supply agreements and capacity expansion cycles that underpin rare earth magnet market volume growth.

3. Geopolitical Realignment and Supply Chain Diversification

China's implementation of export controls on NdFeB and SmCo magnet materials from April 2025 triggered immediate supply chain disruptions and geopolitical repositioning. China's rare earth magnet exports to the USA experienced dramatic volatility, with shipments surging 660% in June 2025 following trade negotiations, while still trailing prior year levels. This instability has accelerated government and private sector investment in alternative supply chains across North America, Europe, Japan, and Australia.

4. Rare Earth Magnet Recycling and Sustainability Practices

Growing environmental concerns and strategic supply security imperatives are converging to accelerate rare earth magnet recycling. The US Department of Energy has committed research funding to domestic recycling programs. As EV and wind turbine end-of-life volumes grow through the 2030s, recycled rare earth content will become a meaningful supply component.

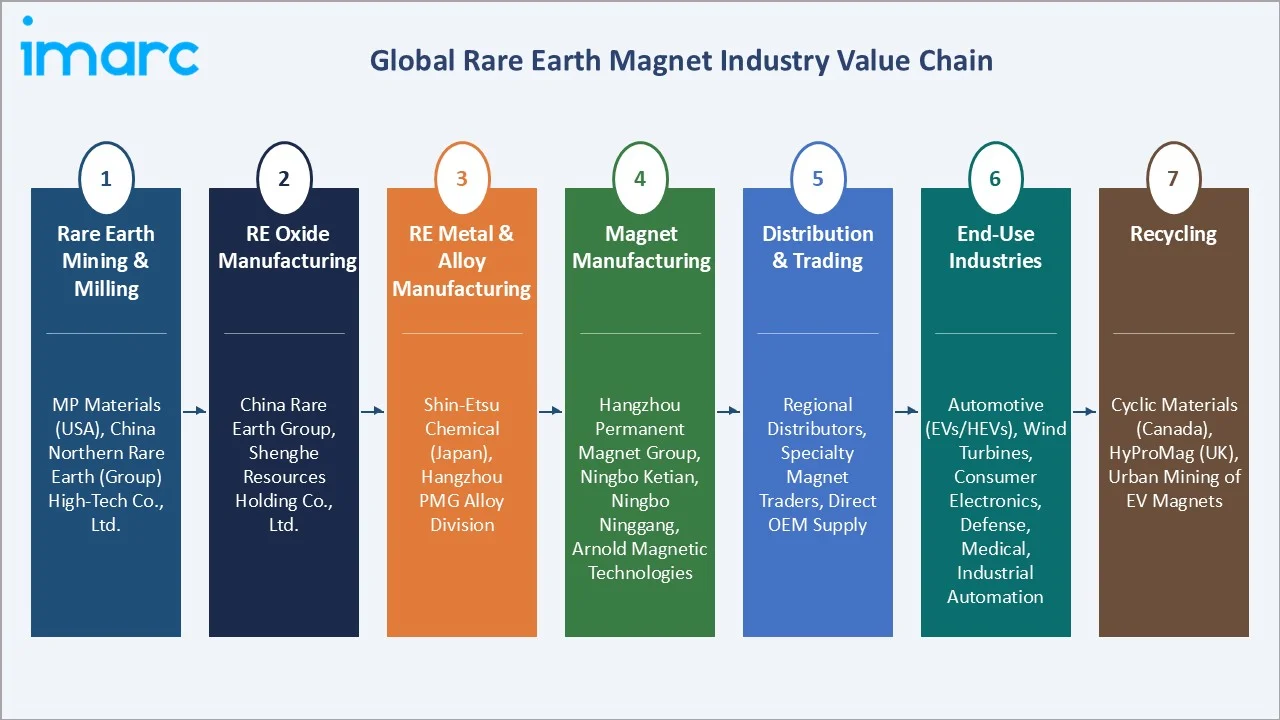

Industry Value Chain Analysis

The rare earth magnet value chain spans seven stages from upstream mining through end-use installation and recycling. Magnet manufacturing and precision processing capture the highest value-add margins, while upstream mining and separation are strategically critical due to geographic concentration in China and the geopolitical risk exposure this creates for downstream manufacturers globally.

|

Stage |

Key Players / Examples |

|

Rare Earth Mining & Milling |

MP Materials (USA), China Northern Rare Earth (Group) High-Tech Co., Ltd. |

|

RE Oxide Manufacturing |

China Rare Earth Group, Shenghe Resources Holding Co., Ltd. |

|

RE Metal & Alloy Mfg |

Shin-Etsu Chemical (Japan), Hangzhou PMG alloy division |

|

Magnet Manufacturing |

Hangzhou Permanent Magnet Group, Ningbo Ketian, Ningbo Ninggang, Arnold Magnetic Technologies |

|

Distribution & Trading |

Regional distributors, specialty magnet traders; direct OEM supply for EV and wind sectors |

|

End-Use Industries |

Automotive (EVs/HEVs), Wind Turbines, Consumer Electronics, Defense, Medical, Industrial Automation |

|

Recycling |

Urban mining of EV end-of-life magnets; Cyclic Materials (Canada), HyProMag (UK) |

Integrated magnet manufacturers with captive rare earth alloy sourcing arrangements achieve meaningful input cost advantages over those relying on spot market procurement. China's vertically integrated producers maintain cost structures 30–50% below equivalent Western manufacturing, a structural advantage that has proven durable despite recent geopolitical disruptions.

However, the US DoD's price floor commitment to MP Materials signals a policy determination to sustain domestic production through pricing support, altering the competitive economics for non-Chinese supply chains over the forecast period.

Technology Landscape in the Rare Earth Magnet Industry

Sintering Technology: Powder Metallurgy to Vacuum Sintering

The dominant NdFeB magnet manufacturing process is powder metallurgy sintering, where neodymium-iron-boron alloy is strip-cast, hydrogen decrepitated, jet-milled to micrometer-scale powder, pressed under magnetic field alignment, and vacuum sintered at approximately 1,050–1,100°C. Modern high-pressure hydrogen decrepitation processes improve powder consistency and reduce oxygen contamination, directly improving final magnet magnetic properties.

Heavy Rare Earth Reduction: Grain-Boundary Diffusion Processing

Conventional NdFeB magnets for automotive applications require dysprosium (Dy) or terbium (Tb) additions of 3–8 wt% to achieve coercivity levels required for EV motor operating temperatures above 120°C. Grain-boundary diffusion (GBD) processing, pioneered by Japanese manufacturers Shin-Etsu Chemical and TDK, achieves equivalent coercivity enhancement with 30–50% less heavy rare earth element content by concentrating Dy or Tb at grain boundaries rather than bulk substitution.

Recycling Technology: Hydrogen Processing and Hydrometallurgy

Hydrogen decrepitation (HD) recycling routes break end-of-life NdFeB magnets into powder through hydrogen absorption and desorption cycles, enabling reprocessing without full hydrometallurgical dissolution. Hydrometallurgical routes using acid leaching followed by solvent extraction can recover individual rare earth elements from magnet scrap for re-synthesis, offering greater flexibility for mixed-grade feed streams from consumer electronics end-of-life processing.

Digital Design and Magnetic Simulation Tools

Advanced finite element analysis (FEA) software for magnetic circuit simulation, including JMAG, Opera, and ANSYS Maxwell, enables magnet manufacturers to optimize geometry, grade selection, and assembly configuration for specific motor or actuator designs. Virtual prototyping reduces physical sample iterations, shortening development cycles and enabling more rapid customization for EV OEM specification requirements.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Magnet Type |

NdFeB Magnets |

85% |

2025 |

|

Application |

NdFeB Magnets |

86% |

2025 |

|

Region |

Asia Pacific |

55% |

2025 |

By Magnet Type

NdFeB Magnets command an 85.0% majority share in 2025 owing to their fundamental superiority in energy product, enabling compact motor designs that are indispensable for EV traction, wind turbine generation, consumer electronics, and industrial automation. The cost-performance profile makes NdFeB magnets the default specification for the vast majority of electric motor applications globally, driving consistent volume demand across market cycles tied to electrification megatrends.

To access detailed market analysis, Request Sample

SmCo Magnets at 15.0% in 2025 command irreplaceable demand in high-temperature and mission-critical segments where material substitution is either technically impossible or cost-prohibitive. Their higher samarium and cobalt content generate a substantial per-kilogram price premium over NdFeB, translating to revenue significance disproportionate to volume share.

By Application

NdFeB Magnets application accounts for 86% of the global rare earth magnet market by application in 2025. NdFeB magnet applications span automobiles, electronics, power generators, medical industry, and wind power. Growing global EV penetration rates and wind capacity additions ensure NdFeB application demand sustains multi-year structural growth through the forecast period.

SmCo Magnets application at 14% of the market in 2025 serves the most demanding high-reliability sectors where performance under extreme conditions is non-negotiable. Defense applications including gyroscopes, radar traveling wave tube amplifiers, and missile guidance systems; aerospace propulsion actuators; satellite attitude control mechanisms; and high-field scientific instruments all rely on SmCo magnets. Increasing global defense budgets across NATO members and Asia-Pacific nations sustain SmCo demand independent of commercial market cycles.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

China |

55.0% |

World's largest RE mining, separation and magnet production base; dominant EV market and wind turbine manufacturing; vertically integrated supply chain advantage |

|

Japan |

18.2% |

Technology leader in high-performance NdFeB and SmCo magnet grades; precision automotive electronics and industrial equipment OEM demand |

|

Europe |

14.6% |

Growing offshore wind installations; EV drivetrain localization; EU Critical Raw Materials Act driving domestic supply chain investment |

|

USA |

12.2% |

Defense and aerospace SmCo demand; EV transition; USD 400M DoD investment in domestic rare earth magnet supply chain resilience in 2025 |

China's 55.0% market dominance in 2025 is driven by the most structurally exceptional combination of rare earth mining reserves, advanced separation infrastructure, and cost-efficient large-scale NdFeB sintered magnet manufacturing in any global market. China processes approximately 85–90% of global rare earth elements through refining and separation stages, giving domestic magnet manufacturers a structural input cost advantage. China's domestic EV market, the world's largest, creates captive demand for high-volume NdFeB magnet procurement, reinforcing China's integrated rare earth magnet ecosystem dominance.

Japan, with 18.2% in 2025, leverages decades of precision NdFeB and SmCo magnet technology expertise. Japanese manufacturers pioneered the commercialization of NdFeB magnets in the 1980s and continue to lead in grain-boundary diffusion processing that maximizes coercivity while minimizing dysprosium content.

Competitive Landscape

The global rare earth magnet market is moderately concentrated at the production stage, with Chinese manufacturers controlling the majority of sintered NdFeB volume production, while Western and Japanese players maintain competitive advantages in high-performance specialty magnet grades for defense, aerospace, and precision medical applications.

|

Company Name |

Key Products |

Global Strategic Focus |

|

Arnold Magnetic Technologies |

NdFeB & SmCo magnets |

USA-based global leader; advanced materials for aerospace, defense, EV, medical applications |

|

ADAMS Magnetic Products Co. |

NdFeB, SmCo, ceramic, alnico magnets |

North American distributor-manufacturer; broad portfolio; industrial, electronics sectors |

|

Bunting Magnetics Co. |

NdFeB magnets |

USA manufacturer; industrial separation, recycling, food processing, printing sectors |

|

Eclipse Magnetics Ltd. (Spear & Jackson) |

NdFeB and SmCo magnets |

UK-based; magnetic filtration, separation, and workholding specialist; food processing, machining, oil & gas sectors |

|

Ningbo Ninggang Permanent Magnetic Materials Co., Ltd. |

SmCo Magnets, Sintered NdFeB |

China-based; specialty NdFeB; automotive and electronics OEM supply chains |

|

Ningbo Ketian Magnet Co. Ltd. |

Sintered and bonded NdFeB magnets |

China; cost-efficient NdFeB; EVs, consumer electronics, industrial motors |

|

Thomas & Skinner Inc. |

Neodymium Iron Boron Magnets, Samarium Cobalt Magnets |

USA manufacturer; specialty custom magnets; industrial and defense markets |

Key players include Arnold Magnetic Technologies, ADAMS Magnetic Products Co., Bunting Magnetics Co., Eclipse Magnetics Ltd. (Spear & Jackson), Ningbo Ninggang Permanent Magnetic Materials Co., Ltd., Ningbo Ketian Magnet Co. Ltd., Thomas & Skinner Inc., and others.

Key Company Profiles

Arnold Magnetic Technologies

Arnold Magnetic Technologies, a subsidiary of Compass Diversified, is a leading manufacturer of high-performance magnets and magnetic assemblies, serving aerospace, defense, medical, and industrial markets. The company specializes in precision NdFeB and SmCo sintered magnets, bonded magnet assemblies, and custom engineered magnetic solutions requiring tight dimensional and magnetic property tolerances.

- Product Portfolio: Offers NdFeB sintered magnets, SmCo magnets, bonded magnets, and precision magnetic assemblies for aerospace, defense, and medical applications.

- Recent Developments: In March 2026, Arnold Magnetic Technologies entered into a strategic agreement with USA Rare Earth to strengthen the domestic supply chain for high-performance rare earth magnets. The partnership enables both companies to distribute each other’s products, improving access to critical materials and supporting more resilient, U.S.-based manufacturing capabilities for industries such as aerospace, automotive, energy, and defense.

- Strategic Focus: Arnold's strategy differentiates on technical quality, precision manufacturing, and defense qualification capabilities, targeting premium aerospace, defense, and medical device market segments where performance and supply chain reliability command substantial pricing premiums over commodity Asian-produced magnets.

Bunting Magnetics Co.

Bunting Magnetics Co. is a USA-based manufacturer and distributor of magnets, magnetic assemblies, and magnetic separation equipment serving industrial, recycling, food processing, and printing sectors. The company offers both NdFeB permanent magnets and complete magnetic separation system integration.

- Product Portfolio: Offers NdFeB magnets, magnetic assemblies, magnetic separators, metal detectors, and conveyors for industrial, food processing, and recycling applications.

- Recent Developments: In October 2021, Bunting Magnetics acquired UK-based MagDev Ltd., a manufacturer of magnets and magnetic assemblies, to strengthen its global capabilities in magnetic technologies. The acquisition expands Bunting’s product portfolio and technical expertise, enabling the company to offer a broader range of customized magnetic solutions and enhance its engineering capabilities across industries such as automotive, aerospace, and electronics.

- Strategic Focus: Bunting differentiates on breadth of magnetic application solutions and responsive North American customer service, targeting industrial processing and recycling sectors where application-specific magnetic separation engineering depth and rapid delivery provide competitive differentiation.

Ningbo Ketian Magnet Co. Ltd.

Ningbo Ketian Magnet Co. Ltd., affiliated with Ningbo Jintian Copper (Group) Co., Ltd., is a China-based sintered and bonded NdFeB magnet manufacturer supplying automotive electronics, consumer electronics, and industrial motor OEMs. The company focuses on cost-efficient production of standard and performance NdFeB grades for price-sensitive mass-market applications.

- Product Portfolio: Offers sintered NdFeB magnets across multiple performance grades, GBD NdFeB magnets, and precision machined assemblies for automotive sensors, electronics, and industrial motor applications.

- Recent Developments: In June 2021, Ningbo Jintian Copper Group invested approximately 600 million yuan to develop a high-performance rare earth permanent magnet materials and devices project, aimed at expanding production capacity and meeting rising demand from high-end downstream industries.

- Strategic Focus: Ningbo Ketian focuses on cost-competitive NdFeB production for automotive and electronics OEM supply, leveraging China-based rare earth alloy access and scaled production to compete on delivered cost in volume magnet procurement programs.

Market Concentration Analysis

The global rare earth magnet market is highly concentrated at the production stage, with Chinese manufacturers controlling an estimated 85–90% of sintered NdFeB volume production globally. At the revenue level, the market is moderately concentrated, with Chinese producers holding disproportionate volume share but Western and Japanese manufacturers capturing higher per-unit revenue through premium specialty grades. No single company holds more than approximately 8–10% of total global market revenue.

China's dominance is structurally self-reinforcing: upstream rare earth mineral processing concentration gives Chinese magnet manufacturers preferential access to NdPr, Dy, and Tb at below-market transfer prices within vertically integrated conglomerates. Consolidation through government-directed mergers among Chinese rare earth groups (CNGR, China Northern, Shenghe, China Southern RE) has created fewer but larger, more disciplined competitors at the upstream stage. Outside China, no single magnet manufacturer holds significant global volume market share, though Japanese producers command premium positions in high-coercivity and specialty grades. Global consolidation through M&A is occurring primarily through large industrial conglomerates acquiring specialty magnet producers as strategic additions.

Investment & Growth Opportunities

Fastest-Growing Segments

Europe and the USA are the fastest-growing regions at approximately 5.5–5.8% CAGR through 2034, driven by EV supply chain localization, defense procurement growth, and offshore wind expansion. NdFeB magnets for the automotive sector represent the highest-volume growth opportunity, with EV traction motor magnet procurement scaling in alignment with global EV production ramp-ups. SmCo magnets for defense and aerospace applications are the highest-value growth segment, with increasing defense budgets globally expanding procurement.

Emerging Markets

India represents the fastest-emerging market for rare earth magnet demand in the forecast period, driven by its own EV manufacturing ambitions under the Production Linked Incentive scheme, domestic wind energy capacity additions, and growing electronics manufacturing sector. South America, particularly Brazil, is gaining attention for its untapped rare earth reserves in Minas Gerais and Goiás states. Serra Verde's rare earth project in Brazil is targeting magnet-grade NdPr materials for commercial production by late 2025, representing a meaningful new non-Chinese supply source.

Venture & Investment Trends

Private equity and strategic corporate interest in rare earth magnet supply chain assets outside China has surged since China's 2025 export controls. Government-backed investment vehicles including the US Defense Production Act, EU Strategic Technologies for Europe Platform, and Japan's JOGMEC are actively funding rare earth processing and magnet production projects. Magnet recycling represents the highest-growth investment sub-sector, as EV and wind turbine end-of-life volumes create economically scalable feedstock for recycled NdFeB production. Apple's USD 500 million rare earth recycling partnership and GM's investments in domestic NdFeB supply signal that OEM strategic investment in upstream magnet supply is accelerating.

Future Market Outlook (2026-2034)

The global rare earth magnet market is forecast to expand from USD 20.48 Billion in 2025 to USD 31.22 Billion by 2034 at a CAGR of 4.80%, adding USD 10.74 Billion in incremental annual market value over the forecast period. This consistent, sustained growth reflects the market's structural linkage to irreversible global electrification and decarbonization megatrends. EV penetration rates are forecast to exceed 50% of new vehicle sales in China and the EU by 2030, generating NdFeB magnet demand volumes that far exceed current non-Chinese production capacity.

Three strategic forces will most significantly reshape the rare earth magnet industry landscape through 2034. First, the establishment of viable ex-China sintered NdFeB magnet production capacity in North America, Europe, and Australia will partially redistribute global supply concentration, reducing Chinese market dominance from approximately 85% to a projected 70–75% of global volume production by 2034. Second, magnet recycling at scale will introduce secondary NdFeB material into supply chains, moderating raw material price cycles and improving supply resilience. Third, robotics and humanoid robot applications are forecast by IDTechEx to become among the highest-growth NdFeB demand categories by the early 2030s, representing a significant incremental demand source not yet fully reflected in market consensus forecasts.

Research Methodology

Primary Research

Primary research encompassed structured interviews with rare earth magnet industry stakeholders, including senior technical and commercial managers at magnet manufacturers, EV drivetrain engineers, wind turbine OEM procurement specialists, defense and aerospace buyers, rare earth industry analysts, and supply chain consultants. Primary data validated market sizing, magnet type and application segment shares, regional demand estimates, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Key secondary sources include International Energy Agency World Energy Investment Reports, Global Wind Energy Council Global Wind Reports, IDTechEx rare earth magnet market research, US Geological Survey Mineral Commodity Summaries, EU Critical Raw Materials Act impact assessments, China Rare Earth Industry Association production data, scientific journals on rare earth magnet materials, trade publications including Rare Earth Industry and Metal Bulletin, and corporate disclosures from major rare earth producers and magnet manufacturers.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating global EV sales trajectories, wind energy capacity addition forecasts, industrial automation investment data, and historical market evolution patterns. Scenario analysis encompassing base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty and geopolitical supply chain risk. Segmental forecasts for magnet type, application, and regional shares were developed from primary research validation against secondary data sources.

Rare Earth Magnet Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Magnet Types Covered | Neodymium-Iron-Boron (NdFeB) Magnets, Samarium-Cobalt (SmCo) Magnets |

| Applications Covered | NdFeB Magnets, SmCo Magnets |

| Regions Covered | China, Japan, Europe, USA |

| Companies Covered | Arnold Magnetic Technologies, ADAMS Magnetic Products Co., Bunting Magnetics Co., Eclipse Magnetics Ltd. (Spear & Jackson), Ningbo Ninggang Permanent Magnetic Materials Co., Ltd., Ningbo Ketian Magnet Co. Ltd., Thomas & Skinner Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Rare Earth Magnet Market Report

The global Rare Earth Magnet market was valued at USD 20.48 Billion in 2025, reflecting consistent demand from global electrification, renewable energy, and industrial automation investment.

The Rare Earth Magnet market is projected to exhibit a CAGR of 4.80% during 2026-2034, reaching a value of USD 31.22 Billion by 2034, driven by accelerating EV adoption, wind energy expansion, and defense procurement.

Accelerating global EV adoption requiring NdFeB traction motors, rapid offshore wind energy capacity additions requiring direct drive generators and growing industrial automation and robotics deployments are the primary growth drivers, supported by strategic government investment in domestic rare earth supply chains.

China currently dominates the Rare Earth Magnet market, accounting for a share of 55.0%. China's vertically integrated rare earth supply chain, dominant EV production, and large-scale sintered NdFeB magnet manufacturing infrastructure underpin this commanding regional position.

Some of the major players in the Rare Earth Magnet market include Arnold Magnetic Technologies, ADAMS Magnetic Products Co., Bunting Magnetics Co., Eclipse Magnetics Ltd. (Spear & Jackson), Ningbo Ninggang Permanent Magnetic Materials Co., Ltd., Ningbo Ketian Magnet Co. Ltd., Thomas & Skinner Inc., and others.

NdFeB Magnets lead with an 85.0% magnet type share in 2025, valued for their superior energy product, enabling compact motor designs critical for EV drivetrains, wind turbine generators, consumer electronics, and industrial automation applications globally.

NdFeB Magnets application accounts for 86% of the global market in 2025. Key sub-applications include automobile (EV traction motors), electronics (hard disk drives, speakers), wind power (direct-drive generators), and medical industry (MRI systems). SmCo Magnets application (14%) leads defense, aerospace, and high-temperature industrial segments.

China's April 2025 export controls on NdFeB and SmCo magnet materials caused immediate supply disruptions, triggering a 660% export surge to the USA in June 2025 following trade negotiations. The controls have accelerated strategic investment in ex-China rare earth magnet supply chains across the USA, Europe, Japan, and Australia.

NdFeB magnets offer the highest energy product of any commercially available magnet, making them optimal for compact, high-efficiency motors and electronics applications. SmCo magnets provide superior thermal stability (up to 350°C), exceptional corrosion resistance without coatings, and better resistance to demagnetization in high-vibration environments, making them preferred for defense, aerospace, and high-temperature industrial applications at premium cost.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)