Europe Beer Market Size, Share, Trends and Forecast by Product Type, Packaging, Production, Alcohol Content, Flavor, Distribution Channel, and Country, 2026-2034

Europe Beer Market Size, Share, Trends & Forecast (2026-2034)

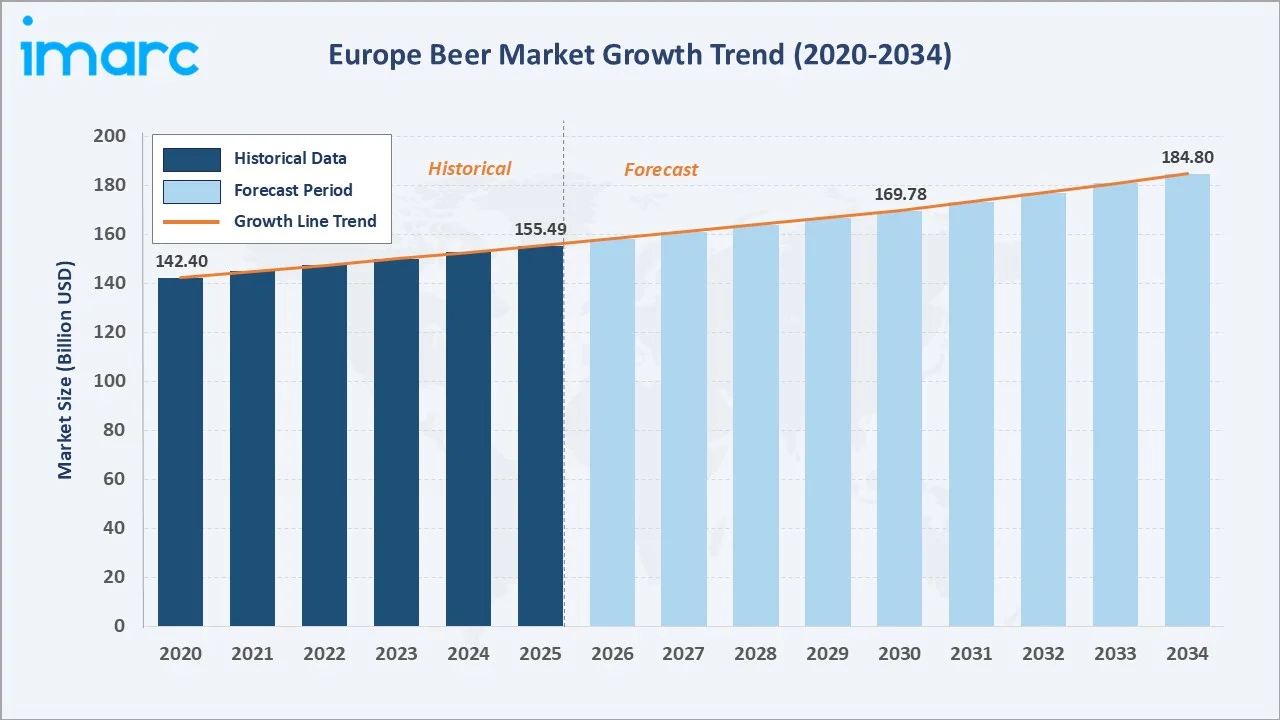

The Europe beer market size was valued at USD 155.49 Billion in 2025 and is projected to reach USD 184.80 Billion by 2034, exhibiting a CAGR of 1.77% during the forecast period 2026-2034. Growth is driven by the premiumization of craft and specialty beers, rising tourism-led on-trade consumption, and expanding low-and-no-alcohol categories across the continent.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 155.49 Billion |

|

Forecast Market Size (2034) |

USD 184.80 Billion |

|

CAGR (2026-2034) |

1.77% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (28.4% share, 2025) |

|

Fastest Growing Country |

Spain (~2.3% CAGR) |

|

Leading Product Type |

Standard Lager (42.3%, 2025) |

|

Leading Packaging |

Glass (48.3%, 2025) |

To get more information on this market, Request Sample

The following chart illustrates the Europe beer market growth trajectory from 2020 through 2034, contrasting historical expansion against a sustained forecast curve powered by premiumization, craft beer adoption, and health-driven innovation.

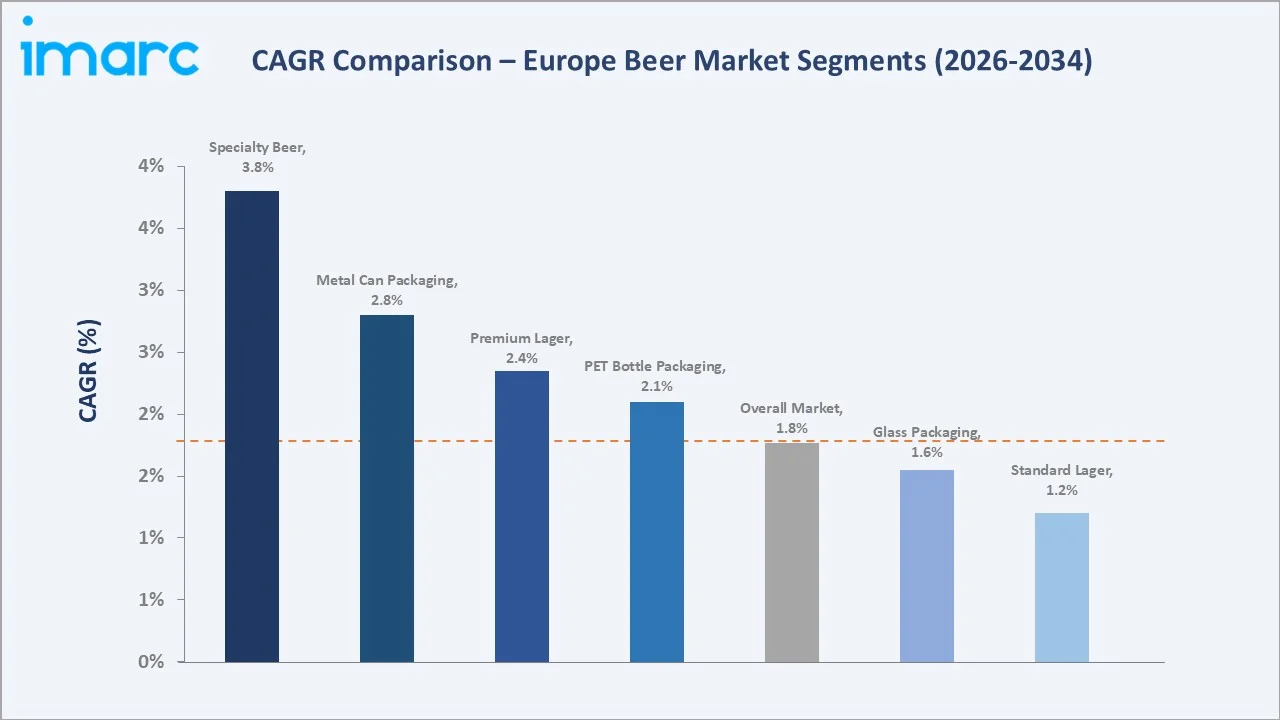

The CAGR comparison below highlights Specialty Beer and Premium Lager as the fastest-growing sub-categories within the Europe beer market forecast through 2034, while Standard Lager remains the volume anchor.

Executive Summary

The Europe beer market is undergoing a measured yet sustained transformation. It is valued at USD 155.49 Billion in 2025 and is forecast to reach USD 184.80 Billion by 2034, at a CAGR of 1.77%. While volume growth remains modest, value expansion is driven by premiumization, craft beer proliferation, and the rapid ascent of low-alcohol and alcohol-free categories.

Standard Lager commands 42.3% of product revenue in 2025, anchored by established brand loyalty and extensive supermarket distribution. Premium Lager follows at 28.6%, growing rapidly on the back of consumer willingness to trade up for quality. Specialty Beer – encompassing craft ales, stouts, and wheat beers – accounts for 18.4% and remains the fastest-growing product sub-category, attracting millennial and Gen Z consumers seeking differentiated experiences.

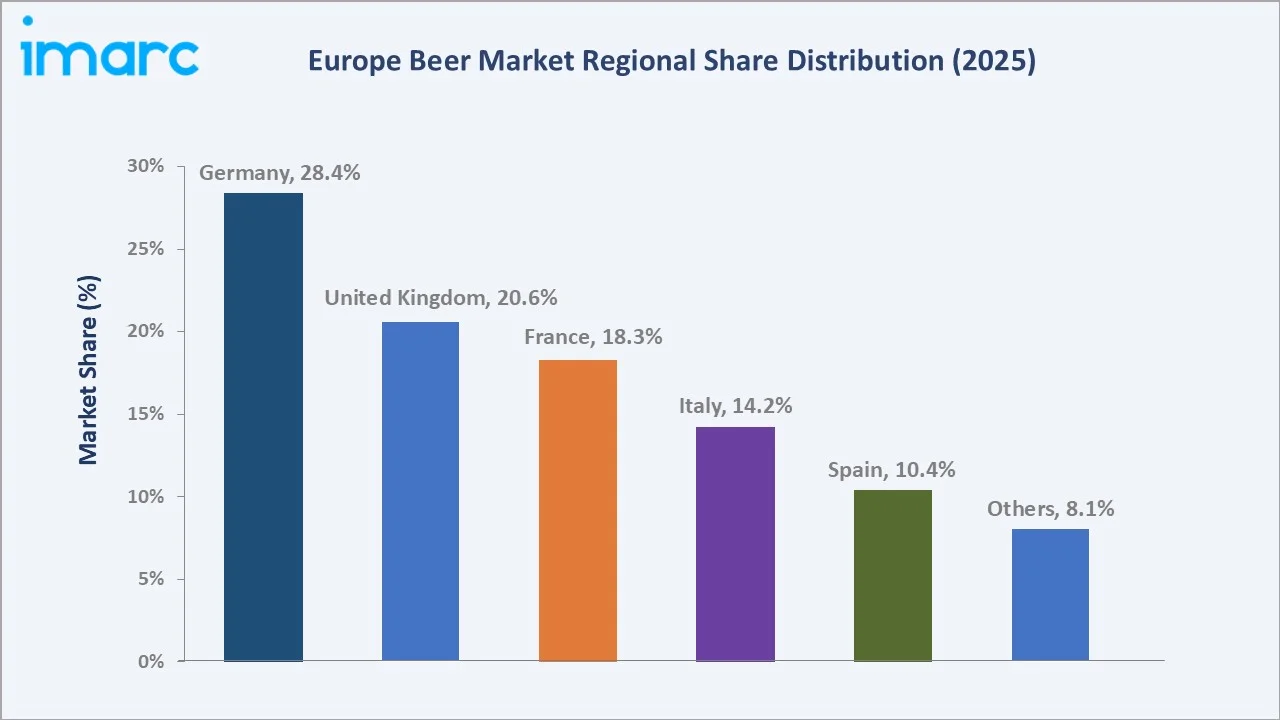

Germany anchors European beer consumption with a 28.4% country share in 2025, supported by deep-rooted brewing heritage and robust export capabilities. The United Kingdom (20.6%) and France (18.3%) follow. The beer market outlook is positive, driven by on-trade recovery, e-commerce expansion, and intensifying investment in sustainable brewing infrastructure across the continent.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Standard Lager – 42.3% share (2025) |

|

Fastest Growing Product Type |

Specialty Beer – Est. ~3.8% CAGR (2026-2034) |

|

Largest Packaging |

Glass – 48.3% share (2025) |

|

Fastest Growing Packaging |

Metal Can – Est. ~2.8% CAGR (2026-2034) |

|

Leading Country |

Germany – 28.4% revenue share (2025) |

|

Fastest Growing Country |

Spain – Est. ~2.3% CAGR (2026–2034) |

|

Top Companies |

Heineken NV, Anheuser-Busch InBev, Carlsberg Breweries A/S, ASAHI GROUP HOLDINGS, LTD., Molson Coors Beverage Company, Kirin Holdings Company, Limited., Bitburger Braugruppe GmbH, OeTTINGER Brauerei GmbH, Krombacher |

Key Analytical Observations Supporting The Above Data:

- Standard Lager's 42.3% dominance in 2025 reflects its entrenched position in European mass-market retail. Volume leadership is sustained through aggressive shelf placements in supermarkets and hypermarkets.

- Specialty Beer's emergence at 18.4% share is driven by the craft beer revolution, particularly in the United Kingdom, Germany, and Belgium. The number of active breweries in Europe surpassed 9,700 as of 2024, underscoring the structural shift toward artisanal and locally produced options.

- Glass packaging's 48.3% majority is entrenched in European culture, especially for on-trade (bar and restaurant) consumption. Returnable glass bottle schemes mandated in Germany (Pfandsystem) and expanding in France and the Netherlands reinforces this dominance.

- Metal Can packaging at 28.6% is experiencing structural growth driven by convenience, portability, and e-commerce compatibility. The premium canned craft segment is an especially high-growth niche, attracting new brand entrants.

- Germany's 28.4% market leadership reflects a brewing heritage spanning over 500 years. There were 1,459 breweries operate within Germany as of 2024, producing a diverse portfolio of styles. German beer warehouses sold around 7.8 billion litres of beer in 2025, cementing its role as Europe's primary beer exporter.

Europe Beer Market Overview

Beer is the most consumed alcoholic beverage in Europe, spanning a diverse portfolio that includes lagers, ales, stouts, porters, wheat beers, craft varieties, and low-or-no-alcohol formulations. The industry ecosystem encompasses raw material suppliers, large-scale macro-breweries, independent craft micro-breweries, packaging manufacturers, logistics networks, and multi-channel retail distribution spanning supermarkets, on-trade establishments, specialty stores, and e-commerce platforms.

Macroeconomic factors shaping the market include rising disposable incomes in Southern Europe, tourism-driven on-trade recovery post-2022, evolving excise tax regimes, stringent EU regulations on labelling and alcohol advertising, and the increasing prominence of sustainability mandates compelling brewers toward carbon-neutral production and circular packaging models.

Market Dynamics

To evaluate market opportunities, Request Sample

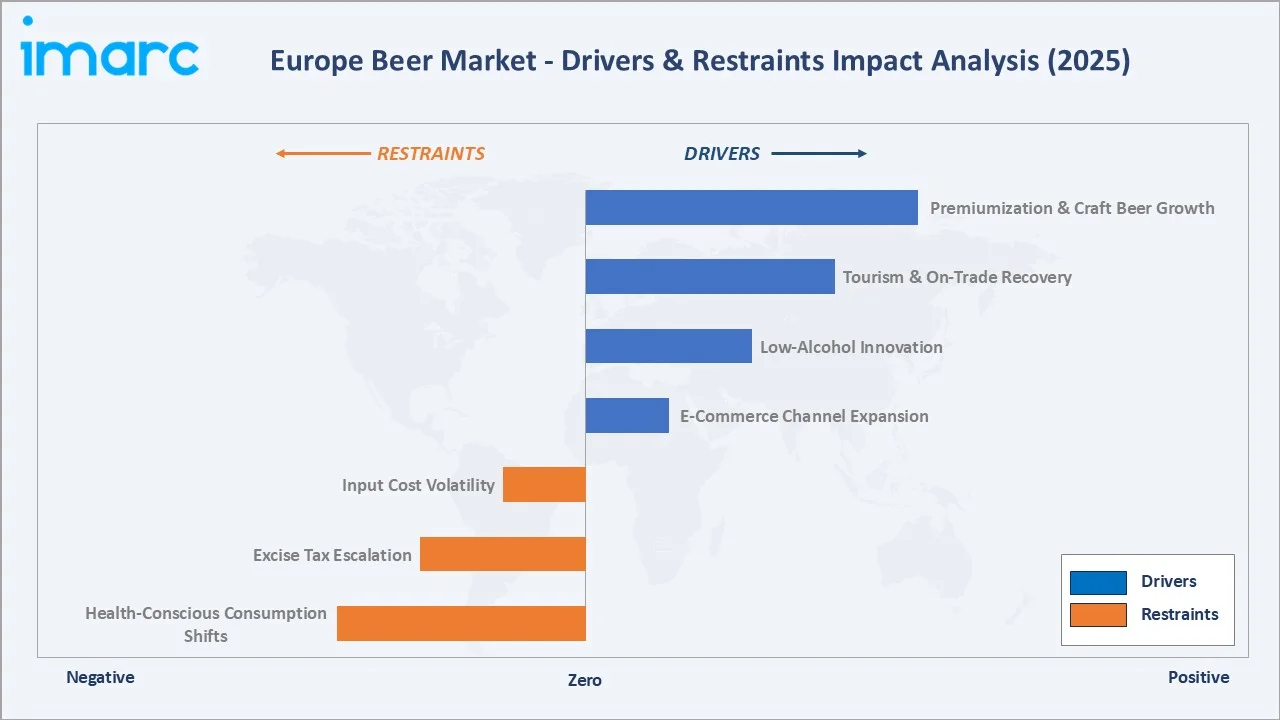

Market Drivers

- Premiumization and Craft Beer Growth: European consumers are increasingly trading up from standard lager to premium and specialty offerings. Craft beer represents a significant share of volumes in markets such as the UK and Belgium. This trend supports higher price points, boosting overall market value despite modest growth in volumes.

- Tourism and On-Trade Recovery: Europe recorded 793 million international tourists in 2025, a 4% increase from 2024, with beer accounting for a significant share of on-trade food and beverage spend in Germany, the Czech Republic, Spain, and Ireland. Tourism-linked on-trade consumption is a structural demand driver.

- Low Alcohol Innovation: Regulatory campaigns, health awareness programs, and WHO alcohol reduction targets in Europe are driving innovation in the low- alcohol beer segment.

- E-Commerce Channel Expansion: Online beer retail in Europe has expanded rapidly in recent years. Direct-to-consumer models deployed by micro-breweries, along with subscription beer services, are attracting younger consumers while bypassing traditional wholesale distribution channels.

Market Restraints

- Health-Conscious Consumption Shifts: Rising awareness of alcohol-related health risks is moderating per-capita beer consumption across Northern and Western Europe. Consumption levels in markets such as the UK have declined over time, reflecting shifting consumer preferences toward healthier lifestyles.

- Excise Tax Escalation: Governments across the EU and the UK are incrementally raising alcohol excise duties. In markets such as the UK, higher beer duties are putting pressure on margins for pub operators and retail-focused brewers.

- Input Cost Volatility: Hop and malt prices have increased in recent years due to adverse weather conditions and supply chain disruptions, squeezing brewery margins, particularly for small and mid-sized operators.

Market Opportunities

- Alcohol-Free Beer Category: The no-alcohol beer segment is experiencing strong growth, representing a significant white-space opportunity. The number of European consumers purchasing alcohol-free beer has increased notably in recent years, reflecting a shift toward healthier consumption habits.

- Sustainable Brewing & Green Packaging: EU Green Deal mandates and corporate sustainability commitments are driving investment in solar-powered breweries, water recycling systems, and fully recyclable packaging. Initiatives such as Heineken's carbon-neutral brewery targets and AB InBev's EverGreen sustainability framework highlight the growing premium positioning around sustainability credentials.

- Emerging Eastern European Markets: Poland, the Czech Republic, Romania, and Hungary represent high-growth sub-markets within the broader “Others” category. Rising middle-class incomes and expanding craft beer cultures are creating untapped revenue potential in these markets.

Market Challenges

- Regulatory Complexity Across Markets: Divergent alcohol marketing, labelling, and duty regulations across EU member states and the post-Brexit UK create compliance complexity for pan-European brands, adding to operational costs.

- Intensifying Competition from Wine & Spirits: RTD (ready-to-drink) cocktails and wine-based beverages are gaining share among younger adult consumers in Southern Europe, putting pressure on beer’s share of the overall alcoholic beverage market.

Emerging Market Trends

1. Craft Beer Revolution and Micro-Brewery Proliferation

The number of craft breweries in Europe has grown significantly in recent years. Local, small-batch brewing is reshaping consumer preferences across the UK, Germany, and Scandinavia. This trend is fostering strong local brand loyalty and providing consumers with authentic, story-driven products that command premium pricing compared to standard lager.

2. Low-and-No-Alcohol Beer Acceleration

Europe's alcohol-free beer market is projected to witness strong growth in the coming years. Major players including Heineken, Carlsberg, and AB InBev have launched dedicated no-alcohol product lines, with Heineken 0.0 widely available across European markets. Health-motivated purchasing decisions, particularly among younger and middle-aged consumers, are structurally sustaining this sub-category.

3. Premiumization of Packaging and Product Format

Premium canned craft beers, collectible glass bottle editions, and multi-pack innovations are elevating per-unit revenue. Metal can adoption for premium and craft segments is steadily increasing. Brands are investing in embossed labelling, limited-edition artwork, and smart-packaging QR codes to enhance consumer engagement.

4. Sustainable Brewing and Circular Economy Integration

Brewers are increasingly committing to science-based targets aligned with the EU Green Deal. Initiatives such as Heineken's PACT for Growth highlight efforts to significantly reduce emissions. Water conservation, renewable energy adoption, and returnable glass schemes are becoming standard practices for brewers operating in the EU. This trend is also influencing procurement decisions by major on-trade partners and supermarket chains that prioritize ESG compliance.

5. Digital Commerce and Direct-to-Consumer (DTC) Channels

Online beer sales across Europe have grown rapidly in recent years. Subscription-based craft beer clubs, brewery webshops, and marketplace integrations on platforms like Amazon Fresh and Ocado are capturing new consumer segments. The direct-to-consumer channel enables breweries to access consumer data, personalize offerings, and build recurring revenue streams independent of traditional distributor networks.

Industry Value Chain Analysis

The Europe beer industry value chain spans six integrated stages from raw material sourcing through end-consumer consumption. Each stage presents distinct competitive dynamics, margin structures, and sustainability pressures that are reshaping procurement and operational strategies across the continent.

|

Value Chain Stage |

Key Activities |

|

Raw Material Supply |

Barley, hops, yeast, water sourcing; malt production |

|

Ingredients & Additives |

Specialty hops, adjuncts, brewing enzymes, flavourings |

|

Brewing & Production |

Macro-brewery mass production; craft micro-brewery output |

|

Packaging |

Glass bottling, metal canning, PET filling, kegging |

|

Distribution & Logistics |

Wholesale distribution, cold-chain logistics, import/export |

|

Retail & End Consumption |

Supermarkets, on-trade pubs & bars, e-commerce, specialty stores |

Raw material supply chains are increasingly regionalized as brewers reduce dependency on global commodity markets. Packaging represents approximately 30–35% of total production cost, making material selection and sustainability a key strategic lever. On-trade distribution remains the highest-margin channel, accounting for approximately 40% of beer revenue across Europe despite volume concentration in off-trade retail.

Technology Landscape in the Beer Industry

Precision Fermentation and Brewing Automation

Industry 4.0 technologies are rapidly penetrating European breweries. AI-powered fermentation monitoring systems enable real-time control of key parameters such as pH, temperature, and dissolved oxygen, helping reduce batch inconsistencies. Automated brewing platforms deployed by Heineken and Carlsberg at their flagship plants optimize energy use and lower water consumption per unit of production.

Sustainable Ingredient Innovation

Novel hop cultivars engineered for drought resistance and higher alpha-acid yield are being adopted to address climate change impacts on traditional growing regions. Upcycled grain and spent brewing yeast applications are gaining commercial traction as protein and flavour adjuncts, supporting circular economy commitments and reducing raw material waste volumes.

Smart Packaging and Connectivity

QR-code-enabled beer labels offering consumers access to provenance data, brewing stories, allergen information, and direct-to-consumer purchase links are gaining adoption. Temperature-sensitive inks and smart can closure that indicate optimal serving conditions are being tested by AB InBev and Carlsberg as premium differentiation tools.

E-Commerce and Data Analytics

Leading brewers are deploying advanced consumer analytics platforms to optimize SKU portfolios, personalize digital promotions, and improve demand forecasting accuracy. AB InBev's BEES platform – a B2B e-commerce tool for on-trade operators – is being expanded across European markets, with a large and growing global network of connected retailers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Standard Lager |

42.3% |

2025 |

|

Packaging |

Glass |

48.3% |

2025 |

|

Production |

Macro-Brewery |

🔒 |

2025 |

|

Alcohol Content |

High |

🔒 |

2025 |

| Flavor | Unflavored | 🔒 | 2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 🔒 | 2025 |

|

Country |

Germany |

28.4% |

2025 |

By Product Type

To access detailed market analysis, Request Sample

Standard Lager represents 42.3% of the Europe beer market in 2025, led by established brands such as Heineken, Carlsberg, Oettinger, and Amstel. Mass-market pricing, wide supermarket availability, and strong brand recall drive this segment's dominance across Germany, the UK, and Spain.

By Packaging

Glass packaging dominates with a 48.3% share in 2025. Germany's mandatory Pfand system (deposit-return scheme) and the deep-rooted on-trade tradition of draught and bottled beer reinforce glass dominance. Glass commands premium price positioning and aligns with sustainability narratives around recyclability.

Regional Market Insights

|

Country |

Share 2025 |

Key Growth Drivers |

Regulatory Factors |

|

Germany |

28.4% |

Oktoberfest tourism, export-oriented brewing, craft expansion |

Reinheitsgebot purity law, Pfandsystem deposit system |

|

United Kingdom |

20.6% |

Canned craft beer boom, pub culture, ale heritage |

UK alcohol duty (10.1% rise, Aug 2023), Drinkaware compliance |

|

France |

18.3% |

Rising beer-versus-wine shift among youth, tourism |

Evin Law (alcohol advertising restrictions), EU labelling |

|

Italy |

14.2% |

Craft microbrewery growth, aperitivo culture expansion |

EU agricultural subsidies for barley; packaging regulations |

|

Spain |

10.4% |

Tourism-driven on-trade, hot climate beer demand |

Moderate excise taxes; regional autonomy on alcohol rules |

|

Others |

8.1% |

Emerging craft scenes in Poland, Czech Republic, Romania |

Varied EU and non-EU regulatory frameworks |

The Europe beer market is geographically concentrated, with Germany, the United Kingdom, and France collectively accounting for 67.3% of regional revenue in 2025. Each market exhibits distinct consumption patterns, regulatory environments, and competitive dynamics.

Competitive Landscape

The Europe beer market exhibits a moderately consolidated structure, with the top three players – Heineken NV, Anheuser-Busch InBev, and Carlsberg Breweries A/S – collectively commanding an estimated 55–60% of regional revenue in 2025. The remaining share is fragmented among national champions, regional brewers, and a rapidly expanding craft micro-brewery segment.

|

Company Name |

Key Brand(s) |

Market Position |

HQ Country |

|

Heineken N.V. |

Heineken, Amstel, Desperados |

Market Leader |

Netherlands |

|

Anheuser-Busch InBev |

Budweiser, Stella Artois, Beck's, Leffe, Corona |

Market Leader |

Belgium |

|

Carlsberg Breweries A/S |

Carlsberg, Tuborg, Kronenbourg 1664 |

Market Leader |

Denmark |

|

ASAHI GROUP HOLDINGS, LTD. |

Peroni (Nastro Azzurro), Grolsch, Pilsner Urquell |

Strong Challenger |

Japan (EU ops) |

|

Molson Coors Beverage Company |

Coors Light, Carling, Staropramen |

Challenger |

USA (EU ops) |

|

Kirin Holdings Company, Limited. |

Kirin Ichiban |

Niche/Regional |

Japan (EU ops) |

|

Bitburger Braugruppe GmbH |

Bitburger, Köstritzer, König Pilsener |

National Champion |

Germany |

|

OeTTINGER Brauerei GmbH |

Oettinger |

Volume Player |

Germany |

|

Krombacher |

Krombacher Pils, Krombacher Weizen |

National Champion |

Germany |

The competitive positioning matrix below plots key players across estimated market share and innovation/brand strength dimensions:

Key Company Profiles

Carlsberg Breweries A/S

Carlsberg Breweries A/S is a leading global brewing company, headquartered in Copenhagen, Denmark. Founded in 1847 by J.C. Jacobsen, the company has evolved into one of the world’s largest beer producers, with a strong presence across Europe and Asia.

- Product Portfolio: Carlsberg, Tuborg, Kronenbourg 1664, San Miguel (licensed), Brooklyn Brewery (partnership), and a growing portfolio of low/no-alcohol variants including Carlsberg 0.0.

- Recent Developments: In 2024, Carlsberg Breweries A/S has completed the acquisition of Britvic plc through its subsidiary, forming a new integrated beverage company named Carlsberg Britvic in the UK. The deal combines beer and soft drinks portfolios to create a stronger market offering with enhanced supply chain and distribution capabilities.

- Strategic Focus: Portfolio premiumization, alcohol-free category leadership, cross-category diversification via the Britvic acquisition, and digital commerce enablement.

Heineken N.V.

Heineken N.V. is one of the world’s leading brewing companies, headquartered in Amsterdam, Netherlands. Founded in 1864, the company has built a strong global presence with operations in over 190 countries and a broad portfolio of beer, cider, and non-alcoholic beverage brands.

- Product Portfolio: Heineken, Amstel, Desperados, Birra Moretti, Affligem, Lagunitas, and Heineken 0.0 (alcohol-free). The group also operates Heineken-owned pub chains across the UK and Ireland.

- Recent Developments: In 2022, Heineken N.V. introduced its lower-ABV Heineken Silver brand extension in the UK and several EU markets. The launch reflects the company’s strategy to expand its presence in the low-alcohol segment and cater to evolving consumer preferences for lighter beer options.

- Strategic Focus: Premium brand portfolio expansion, no-alcohol category leadership via Heineken 0.0, on-trade estate optimization in the UK, and digital direct-to-consumer capabilities.

Anheuser-Busch InBev

- Company Overview: AB InBev is the world's largest brewer and holds a dominant position in the European beer market through a multi-brand portfolio spanning premium, mainstream, and craft categories. Its European operations are headquartered in Leuven, Belgium.

- Product Portfolio: Stella Artois, Budweiser, Beck's, Leffe, Hoegaarden, Jupiler, and Corona

- Recent Developments: In 2026, Anheuser-Busch InBev is driving growth through premiumization and digital expansion strategies. The company is strengthening its higher-margin product portfolio, including premium and non-alcoholic offerings, it is also accelerating its “Beyond Beer” and digital initiatives, expanding into categories like ready-to-drink beverages while scaling platforms such as BEES and Zé Delivery to enhance customer engagement and operational efficiency.

- Strategic Focus: Premium brand portfolio strengthening, sustainability-led brand equity, on-trade digital tools via BEES, and direct-to-consumer craft beer expansion.

Market Concentration Analysis

The Europe beer market exhibits a moderately concentrated structure. The top three players – Heineken N.V., AB InBev, and Carlsberg Breweries A/S – together command an estimated 55–60% of regional market revenue in 2025, reflecting strong brand equity, multi-country manufacturing footprints, and extensive distribution networks.

Consolidation activity remains active at the regional level. Carlsberg's acquisition of Britvic in 2024 signals emerging cross-category consolidation beyond pure beer. The fragmented craft segment is expected to see continued M&A as major brewers seek to acquire authentic brand credentials and expand into the high-margin specialty beer category.

Investment & Growth Opportunities

- Alcohol-Free Beer Manufacturing: The low- and no-alcohol segment represents a major high-growth investment theme within the beer industry. Capital deployment in dedicated alcohol-free brewing lines, brand marketing, and retail shelf space expansion is expected to deliver strong returns in key markets such as the UK, Germany, and Spain.

- Eastern European Market Entry: Poland, Romania, the Czech Republic, and Hungary represent a sizeable combined market within Europe. Rising disposable incomes, expanding modern retail infrastructure, and growing craft beer cultures make these markets prime targets for premium brand entry and micro-brewery investment.

- Sustainable Brewing Infrastructure: EU Green Deal subsidies, carbon border taxes, and corporate ESG commitments are driving demand for renewable-energy-powered breweries, closed-loop water recycling systems, and fully recyclable packaging lines. Investors supporting sustainability-led brewery upgrades are well positioned to benefit from regulatory tailwinds and premium brand positioning.

- Digital Commerce and DTC Platforms: Beer e-commerce in Europe has grown significantly in recent years. Investment in direct-to-consumer subscription platforms, B2B digital ordering tools, and data analytics infrastructure offers strong potential for margin improvement and enhanced consumer loyalty.

- Craft and Specialty M&A: Venture capital interest in craft breweries has intensified, with increasing deal activity in the UK, Germany, and Scandinavia. Strategic acquirers such as AB InBev and Carlsberg are actively pursuing craft brand acquisitions to refresh their product portfolios and capture younger consumer segments.

Future Market Outlook (2026-2034)

The Europe beer market is forecast to grow from USD 155.49 Billion in 2025 to USD 184.80 Billion by 2034, at a CAGR of 1.77%. While overall volume growth will remain modest, value expansion driven by premiumization, specialty product proliferation, and alcohol-free innovation will sustain positive market trajectory.

By 2030, the market is projected to reach USD 169.78 Billion, Specialty beer and premium lager collectively contribute a significant share of total market value. The low- and no-alcohol sub-segment is expected to increase its share of overall beer market revenue over time, reflecting strong growth and rising consumer adoption.

Technological disruption – including AI-driven fermentation control, smart packaging, and direct-to-consumer digital channels – will accelerate competitive differentiation. Environmental regulatory pressures under the EU Green Deal will mandate material packaging shifts and energy transition investments, with glass and metal can remaining dominant but undergoing circular economy integration. Germany, the UK, and Spain are expected to be the highest-growth value markets within the European region through 2034.

Research Methodology

Primary Research

Primary data was gathered through structured interviews with senior executives across European brewery operators, packaging manufacturers, retail buyers, and distribution channel managers. Consumer surveys were conducted across 6 European markets to validate consumption trends, purchasing behaviour, and brand preference dynamics.

Secondary Research

Secondary research incorporated data from national statistical offices (Destatis, ONS, INSEE), industry associations (Brewers of Europe, British Beer & Pub Association, German Brewers Association), EU regulatory databases, trade publications (Beverage Daily, Just Drinks), and company annual reports and investor presentations.

Market Estimation & Forecasting

Market sizing employs a combination of bottom-up (aggregating country-level brewery shipment data and consumer expenditure) and top-down (applying European share estimates to global market totals) approaches. Forecast models integrate macroeconomic indicators, historical CAGR analysis, regulatory impact assessments, and expert validation to produce the 2026–2034 projection.

Europe Beer Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Standard Lager, Premium Lager, Specialty Beer, Others |

| Packagings Covered | Glass, PET Bottle, Metal Can, Others |

| Productions Covered | Macro-Brewery, Micro-Brewery, Others |

| Alcohol Contents Covered | High, Low, Alcohol-Free |

| Flavors Covered | Flavored, Unflavored |

| Distribution Channels Covered | Supermarkets and Hypermarkets, On-Trades, Specialty Stores, Convenience Stores, Others |

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Heineken N.V., Anheuser-Busch InBev, Carlsberg Breweries A/S, ASAHI GROUP HOLDINGS, LTD., Molson Coors Beverage Company, Kirin Holdings Company, Limited., Bitburger Braugruppe GmbH, OeTTINGER Brauerei GmbH, Krombacher, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe beer market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe beer market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe beer industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Beer Market Report

The Europe beer market size was valued at USD 155.49 Billion in 2025, with steady growth supported by premiumization and craft beer demand.

The market is projected to reach USD 184.80 Billion by 2034, growing at a CAGR of 1.77% during the 2026-2034 forecast period.

The Europe beer market is forecast to grow at a CAGR of 1.77% between 2026 and 2034, driven by premium and specialty beer categories.

Standard Lager leads with 42.3% market share in 2025, followed by Premium Lager at 28.6% and Specialty Beer at 18.4%.

Glass packaging dominates with 48.3% share in 2025, supported by returnable bottle schemes in Germany and on-trade consumption traditions.

Germany leads with a 28.4% country share in 2025, followed by the United Kingdom at 20.6% and France at 18.3%.

Leading companies include Heineken N.V., Anheuser-Busch InBev, Carlsberg Breweries A/S, ASAHI GROUP HOLDINGS, LTD., Molson Coors Beverage Company, Kirin Holdings Company, Limited., Bitburger Braugruppe GmbH, OeTTINGER Brauerei GmbH, Krombacher.

Key drivers include craft beer premiumization, tourism-driven on-trade recovery, low-and-no-alcohol innovation, and expanding e-commerce beer retail channels.

Specialty Beer is the fastest-growing product segment, with an estimated CAGR of ~3.8% (2026–2034), driven by craft breweries and millennial demand.

Key challenges include rising excise tax pressures, health-conscious consumption shifts, raw material cost volatility, and intensifying competition from RTD spirits.

The market is segmented by product type, packaging, production method, alcohol content, flavor, and distribution channel, analyzed across six country markets.

The report combines primary interviews with industry stakeholders, secondary data from industry associations, and bottom-up and top-down market estimation models.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade