Europe Online Grocery Market Size, Share, Trends and Forecast by Product Type, Business Model, Platform, Purchase Type, and Country, 2026-2034

Europe Online Grocery Market Size, Share, Trends & Forecast (2026-2034)

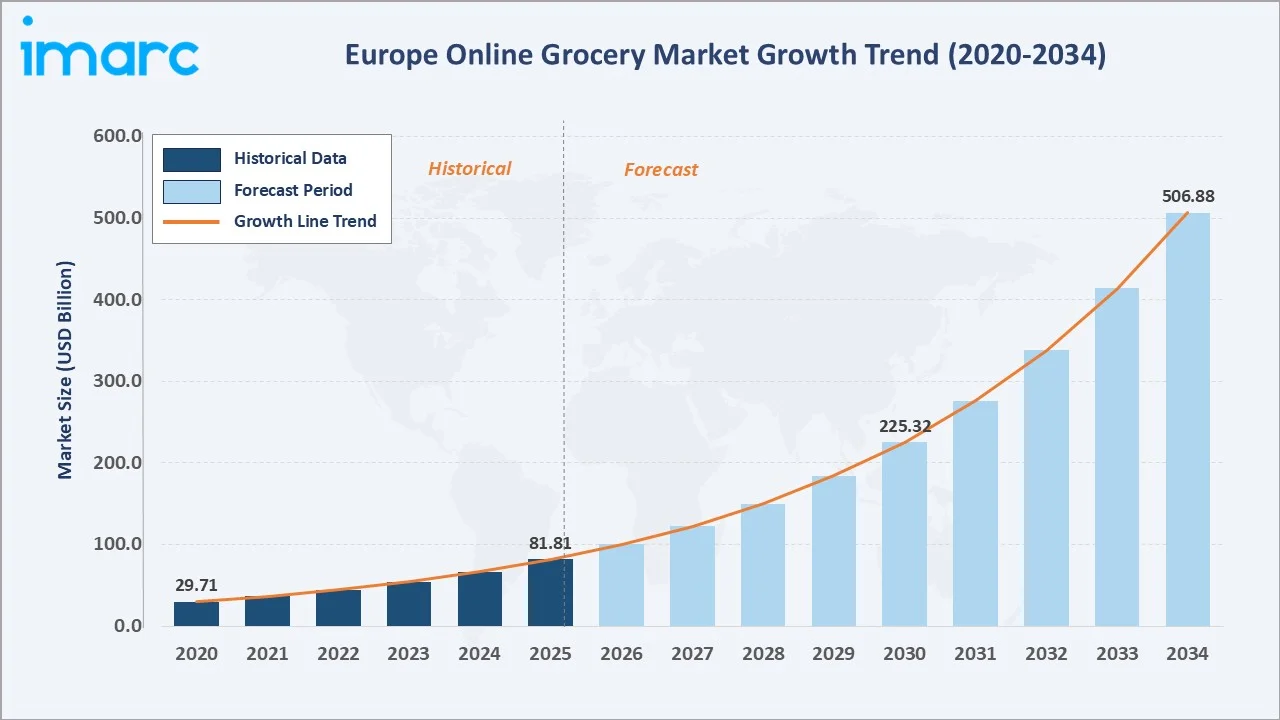

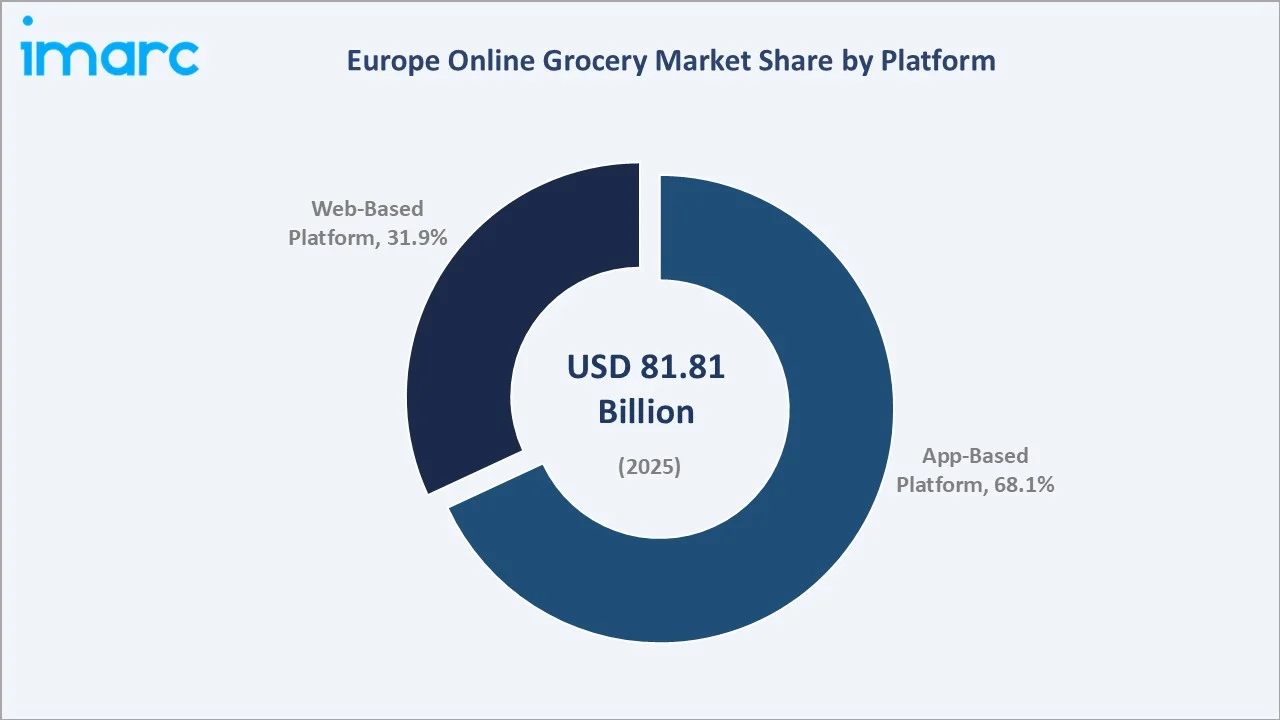

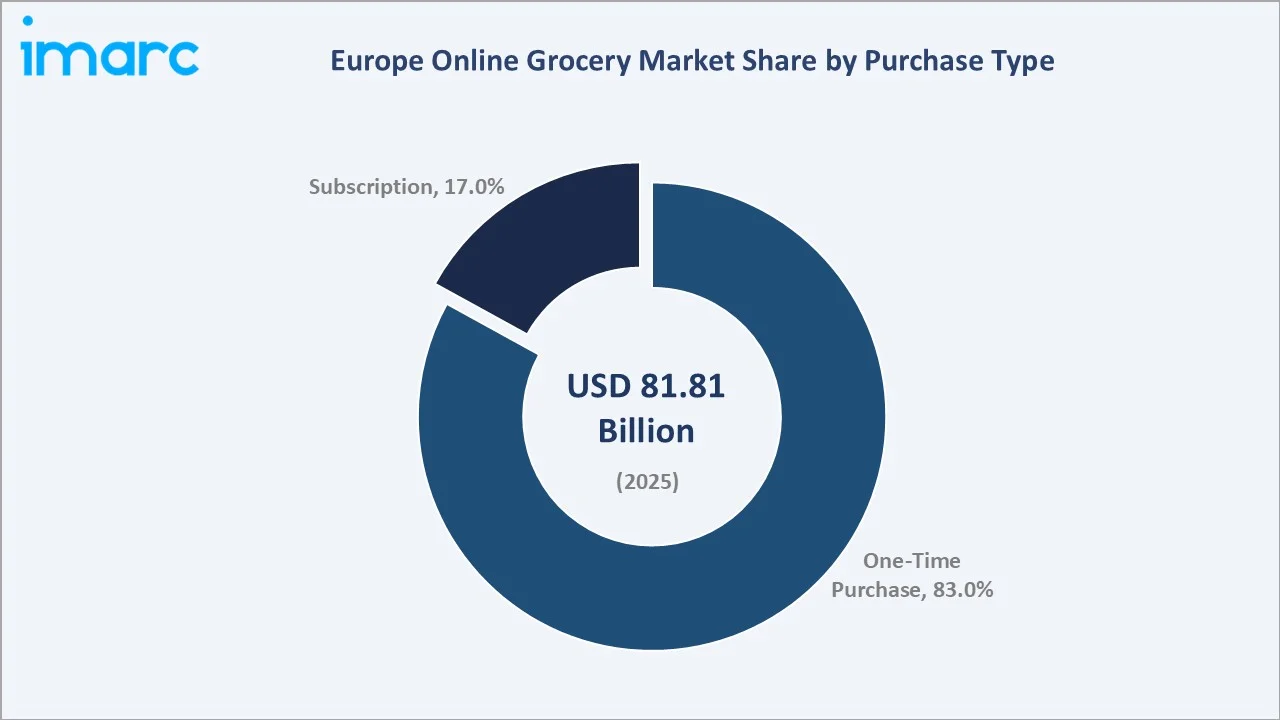

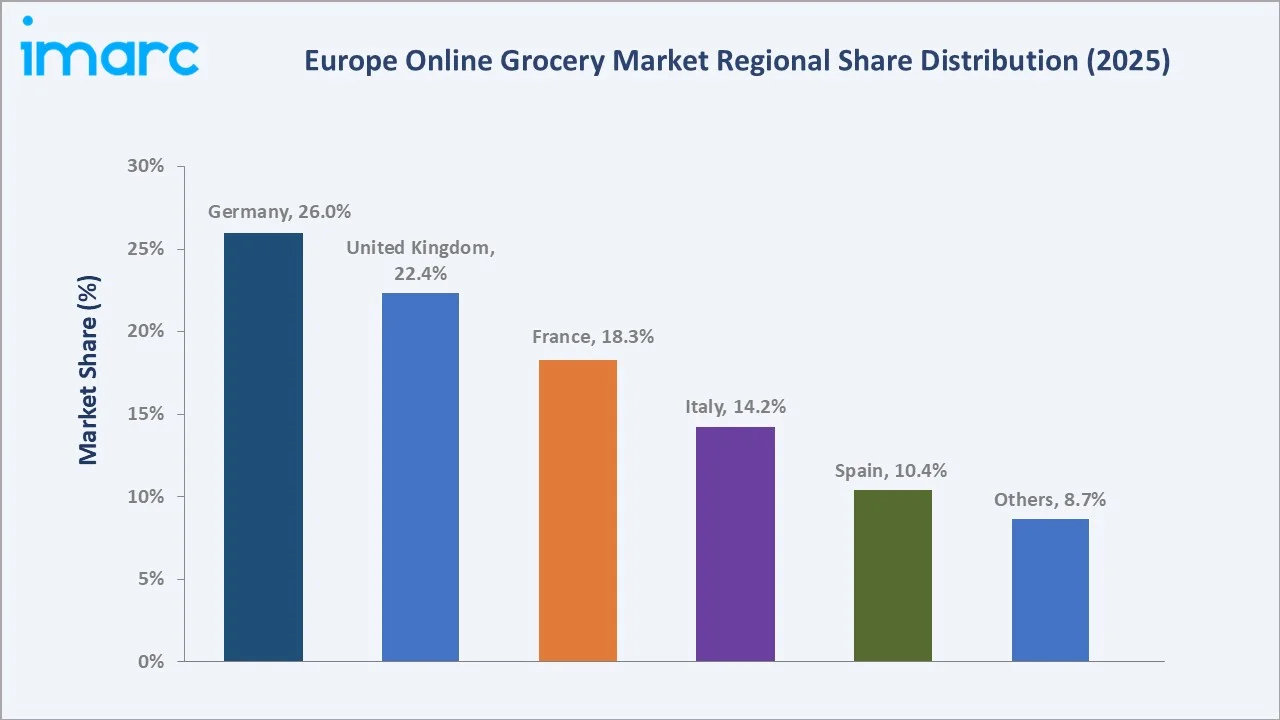

The Europe online grocery market was valued at USD 81.81 Billion in 2025 and is projected to reach USD 506.88 Billion by 2034, expanding at a remarkable CAGR of 22.46% during the forecast period (2026-2034). Growth is driven by the COVID-19-induced permanent shift to digital grocery shopping, explosive smartphone and app adoption, the q-commerce revolution delivering groceries in under 10 minutes and rising urbanization across European cities. Europe's level of urbanization is expected to increase to approximately 83.7% in 2050. App-based platforms dominate at 68.08% share, while one-time purchases lead at 83.0%. Germany commands the largest country share at 26.0%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 81.81 Billion |

|

Forecast Market Size (2034) |

USD 506.88 Billion |

|

CAGR (2026-2034) |

22.46% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

Germany (26.0%, 2025) |

|

Fastest Growing Country |

Italy (CAGR ~23.2%, 2026-2034) |

To get more information on this market, Request Sample

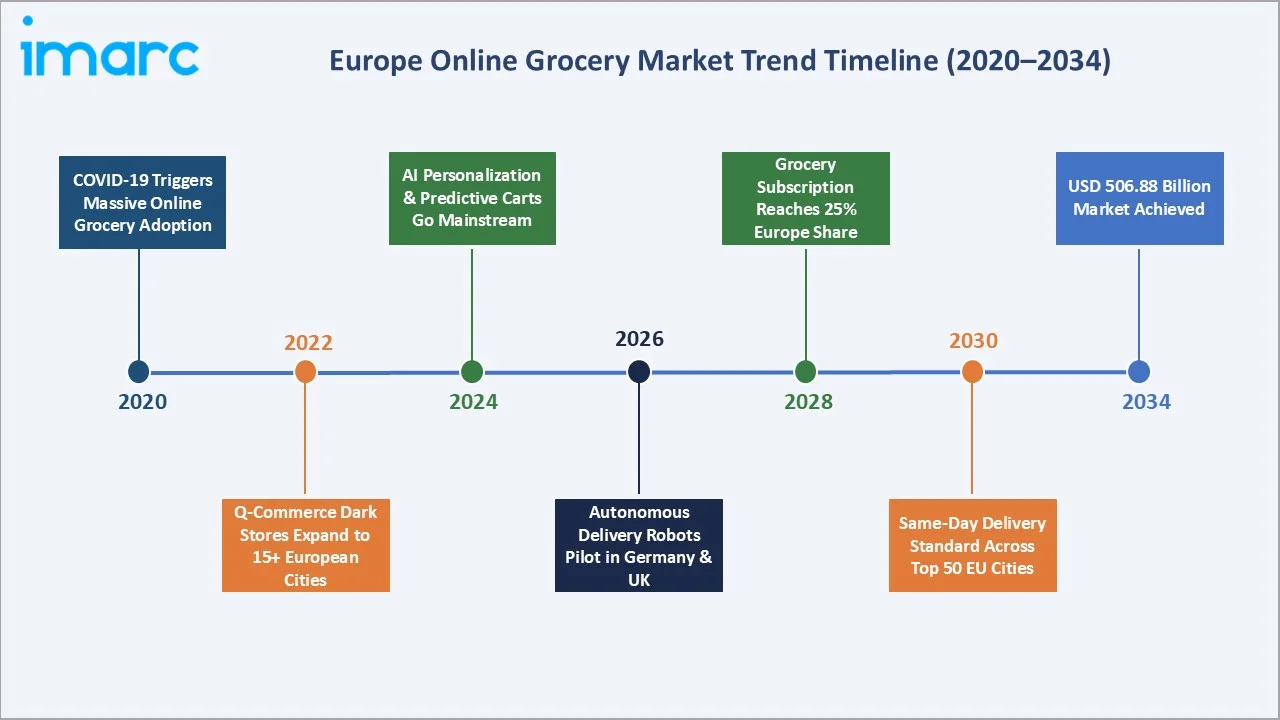

The Europe online grocery market growth market expanded from USD 29.71 Billion in 2020 to USD 81.81 Billion in 2025, reflecting the COVID-19-era digital adoption acceleration. Anchored at USD 225.32 Billion in 2030, the forecast to USD 506.88 Billion by 2034, underlining the transformational shift from in-store to digital-first grocery shopping across Europe’s 450 million consumers.

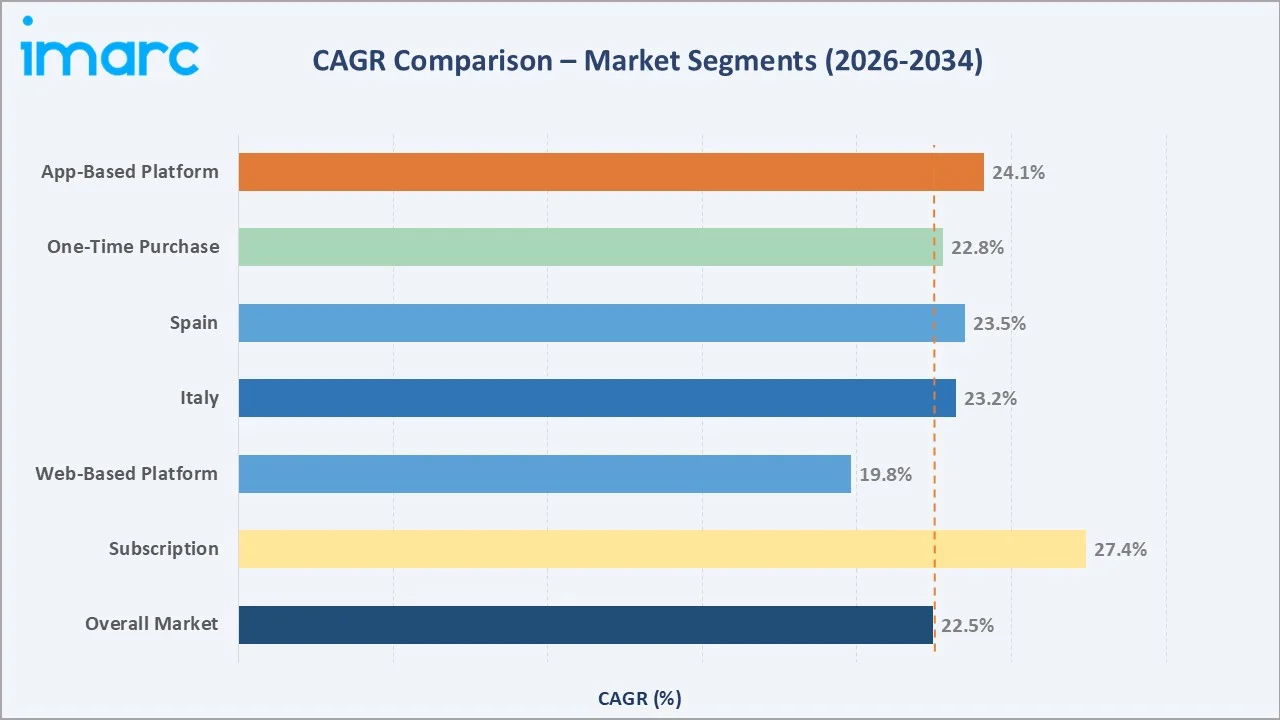

The CAGR across key segments with subscription models at ~27.4% CAGR are growing fastest, reflecting the increasing adoption of grocery loyalty programs and recurring delivery services by European retailers. App-based platforms at ~24.1% CAGR outpace web-based at ~19.8%, as mobile-first shopping habits deepen among Europe’s 300+ million smartphone users under 45 years old.

Executive Summary

The Europe online grocery market has demonstrated extraordinary compound growth from USD 29.71 Billion in 2020 to USD 81.81 Billion in 2025, driven by a generational behavioral shift that began with COVID-19’s forced digital grocery adoption and has evolved into a permanent consumer preference anchored by convenience, speed, and increasingly personalized digital shopping experiences.

App-based platforms at 68.08% market share (2025) reflect the smartphone’s dominance as Europe’s primary digital commerce interface. By 2030, Europe is projected to have 527 million unique mobile subscribers, accounting for an 89% penetration rate across the region, with grocery apps competing for home screen real estate through loyalty rewards, personalized promotions, and 1-tap reordering features that make app-based grocery shopping more habitual than conscious.

Germany’s 26.0% country market dominance reflects Europe’s largest grocery retail market by absolute value. The UK’s 22.4% share represents the most mature European online grocery market, competing intensely for digital grocery wallet share in a market where online grocery penetration leads Europe. France, at 18.3%, is uniquely defined by the Drive click-and-collect model that accounts for 15%+ of total French grocery sales, demonstrating Europe’s geographic variation in preferred online grocery fulfillment formats.

Key Market Insights

|

Insight |

Data |

|

Dominant Platform |

App-Based – 68.08% revenue share (2025) |

|

Dominant Purchase Type |

One-Time – 83.0% revenue share (2025) |

|

Leading Country |

Germany – 26.0% revenue share (2025) |

|

Fastest Growing Country |

Italy (CAGR ~23.2%, 2026-2034) |

Key Analytical Observations Supporting the Above Data:

- App-Based dominates at 68.08% (2025): In April 2020, Pyaterochka emerged as Europe’s most downloaded grocery app with nearly 681,000 installs, followed by Sbermarket, which recorded over 436,000 installs during the same period. The shift from desktop to mobile ordering reflects broader European retail trends.

- One-Time purchases at 83.0% in 2025: Subscription grocery models, where consumers pay for unlimited free deliveries and exclusive member pricing, are growing, as platforms prioritize customer lifetime value over transactional revenue.

- Germany leads at 26.0% (2025): Germany’s online grocery market growth reflects the successful digital transformation of Rewe and Edeka, Germany’s two largest supermarket chains, combined with the emergence of Berlin as the capital of European q-commerce.

Europe Online Grocery Market Overview

The Europe online grocery market encompasses digital platforms, mobile applications, websites, and third-party marketplaces that enable consumers to order food and grocery products for home delivery or click-and-collect pickup. The ecosystem integrates grocery retailers, pure-play online grocers, quick-commerce platforms, and food delivery aggregators that have expanded from restaurant food into grocery and convenience products.

Applications span weekly family household shopping via traditional delivery slots, impulse and top-up shopping via q-commerce apps, subscription meal-kit deliveries, and corporate catering through B2B online grocery channels. Macroeconomic influences include European smartphone penetration, 5G network rollout accelerating app performance, European logistics infrastructure investment, food inflation driving price-conscious consumers to comparison-shop online, and demographic trends showing under-35s spending more on online grocery than the European average.

Market Dynamics

To evaluate market opportunities, Request Sample

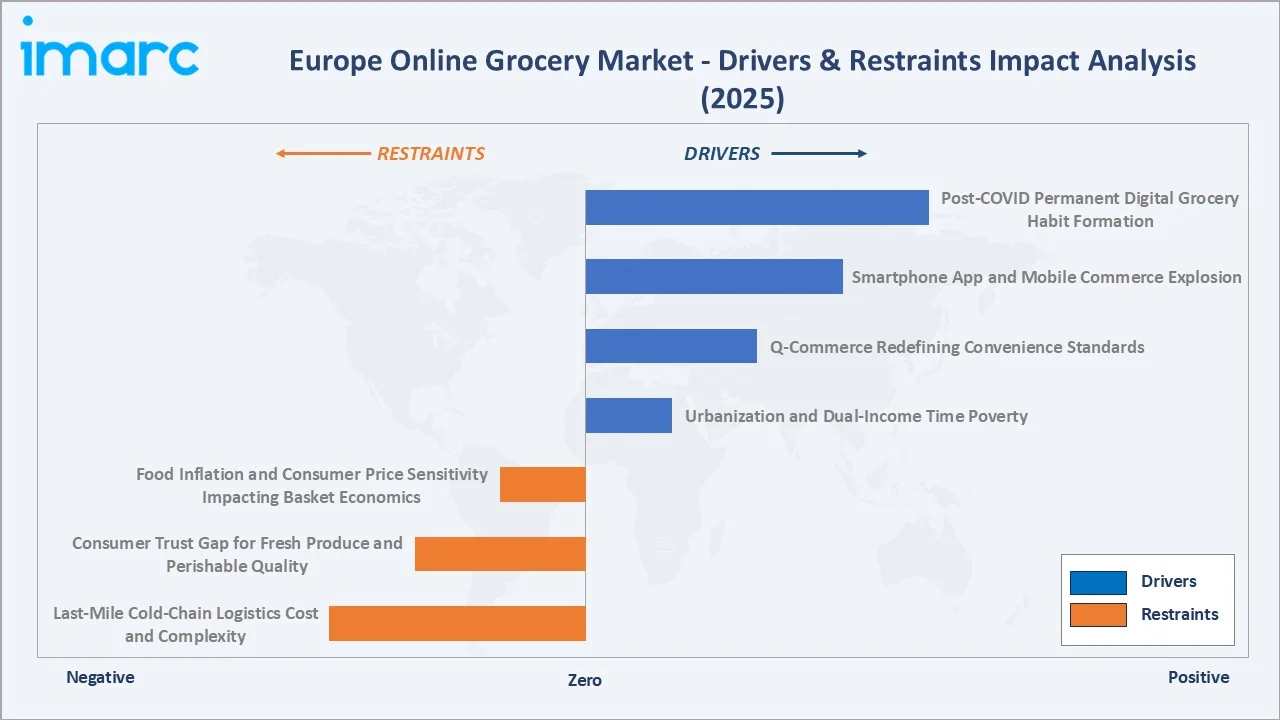

Market Drivers

- Post-COVID Permanent Digital Grocery Habit Formation: A PwC study indicated that 22% of German consumers use the internet as their main grocery shopping channel. Around 52% increased their online grocery purchases during the COVID-19 pandemic, and over 82% plan to continue buying groceries online going forward.

- Smartphone App and Mobile Commerce Explosion: By 2030, Europe is projected to have 527 million unique mobile subscribers, accounting for an 89% penetration rate across the region, with grocery apps competing as essential home screen staples alongside banking and messaging.

- Q-Commerce Redefining Convenience Standards: 10–15-minute grocery delivery, virtually non-existent in Europe before 2020, reshaped consumer expectations of delivery speed.

- Urbanization and Dual-Income Time Poverty: Urban population in the European Union reported at 75.95 % in 2024, concentrating consumers in dense urban environments where online grocery delivery is operationally efficient and highly time-competitive versus in-store shopping.

Market Restraints

- Last-Mile Cold-Chain Logistics Cost and Complexity: Temperature-controlled grocery delivery, mandatory for dairy, fresh produce, frozen foods, and pharmaceutical-adjacent products such as baby formula, requires 3–5× higher capital investment per delivery unit than ambient parcel logistics.

- Consumer Trust Gap for Fresh Produce and Perishable Quality: Despite improving trends, European consumers still expressed concern about receiving suboptimal fresh produce quality when ordering online, particularly for avocados, berries, tomatoes, and artisan bread that require sensory assessment at point of purchase.

Market Opportunities

- AI-Powered Personalization and Predictive Commerce: Machine learning systems trained on individual household purchase histories, dietary preferences, and seasonal behavior patterns can predict with accuracy what a consumer will want to order in the following week.

- B2B and Corporate Catering Online Grocery Channel: European B2B grocery e-commerce, serving office catering, restaurant ingredient supply, hotel breakfast procurement, and corporate canteen management, represents a European market opportunity that most consumer online grocery platforms have barely penetrated.

Market Challenges

- Q-Commerce Unit Economics and Path to Profitability: Ultra-fast grocery delivery’s 10–15 minute promise requires dark stores every 2–3km in dense urban areas, creating extraordinarily high fixed cost structures. Each dark store costs a high setup investment (fit-out, refrigeration, technology, and opening inventory).

- Food Inflation and Consumer Price Sensitivity Impacting Basket Economics: Food prices in the EU rose by 2.8% in 2025 compared with 2024. This price sensitivity is compressing average basket sizes and increasing customer churn rates at platforms unable to compete on price transparency against discounters’ in-store prices, particularly in Germany where Aldi and Lidl’s store-only value positioning constrains online grocery average transaction values.

Emerging Market Trends

1. Autonomous and Robot-Assisted Grocery Fulfilment

Automated Micro-Fulfilment Centers (AMFCs) are processing grocery orders at 5–8× the speed of manual picking at 30-40% lower operating cost. Ocado’s Luton CFC became the fastest-ramping fulfillment center, reaching approximately 40,000 orders per week within its first four weeks of operation. At full capacity, the facility is expected to handle up to 65,000 orders weekly.

2. Subscription-First Grocery Models Building Customer Lifetime Value

European grocery subscription models, unlimited free deliveries, exclusive member pricing, early access to promotions, and personalized loyalty rewards are becoming primary customer retention strategies for all major platforms.

3. Sustainability and Zero-Waste Online Grocery

European consumer demand for sustainable online grocery options, zero-plastic packaging, verified organic provenance, reduced food waste algorithms, and carbon-neutral delivery is creating a new premium market segment.

4. Voice Commerce and Smart Home Grocery Integration

Amazon Alexa, Google Assistant, and Samsung SmartThings integrations with European grocery platforms are enabling voice-commanded grocery reordering, “Alexa, add milk to my Tesco order”, with European smart speaker users estimated to be active grocery reorders via voice.

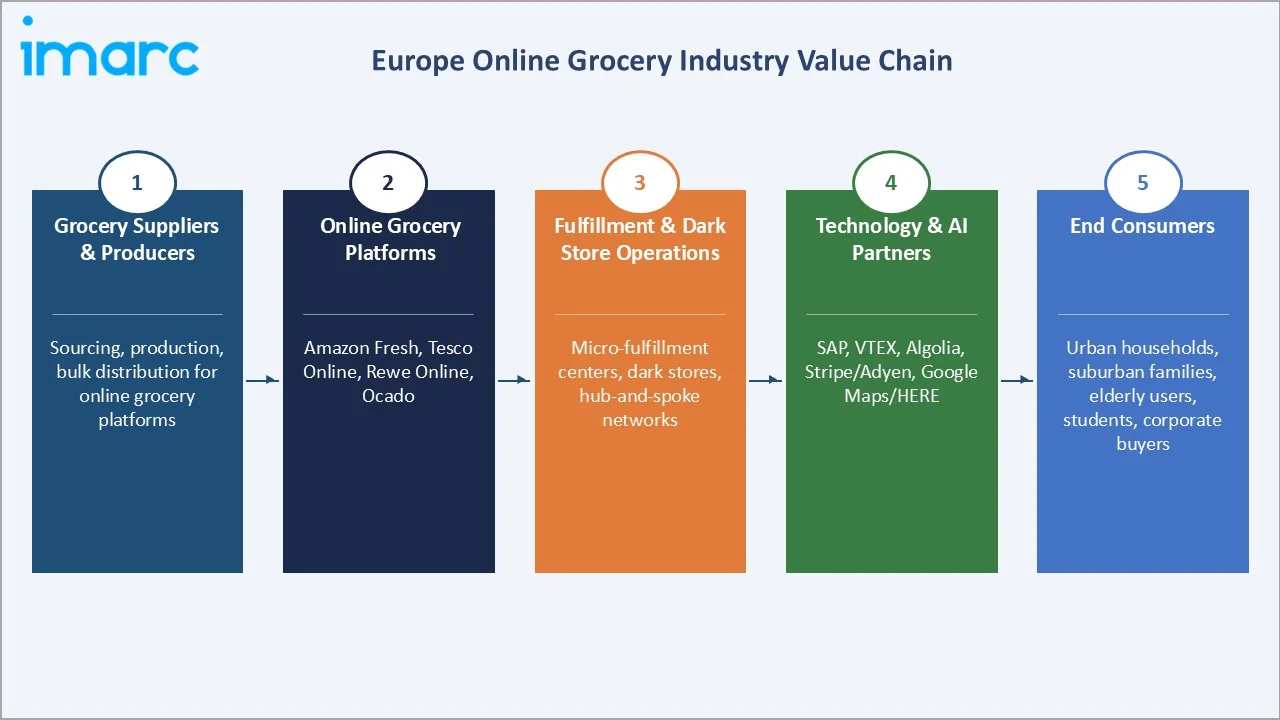

Industry Value Chain Analysis

The Europe online grocery value chain spans food production and supplier relationships through digital platform ordering, automated fulfilment, temperature-controlled last-mile delivery, and post-purchase customer service across the continent’s 750+ million consumers.

|

Stage |

Key Participants |

|

Grocery Suppliers & Producers |

Sourcing, production, and bulk distribution for online grocery platforms |

|

Online Grocery Platforms |

Amazon Fresh, Tesco Online, Rewe Online, Ocado – digital ordering, catalogue management, and customer interface |

|

Fulfilment & Dark Store Operations |

Automated micro-fulfilment centers, dark stores, hub-and-spoke distribution networks, and temperature-controlled warehousing |

|

Technology & AI Partners |

SAP (ERP), VTEX, Algolia (search), Stripe/Adyen (payments), Google Maps/HERE (routing) |

|

End Consumers |

Urban households (primary), suburban families, elderly tech adopters, time-poor dual-income consumers, students via subscription services, corporate catering buyers through B2B channels |

The online grocery platform layer captures the highest margin per GMV unit, while fulfilment and delivery networks represent the highest cost-per-order. The technology and AI partner layer is the fastest-growing value chain segment, with grocery tech software companies achieving 30–40% annual revenue growth from their platform licensing businesses.

Technology Landscape in the Europe Online Grocery Industry

Automated Micro-Fulfilment and Robotics

First-generation grocery fulfilment, manual pickers walking 12–15km daily in traditional distribution centers, is being replaced by robotic AutoStore grid systems (HAPET bots) and Ocado-style 3D grid warehouses where robots retrieve ambient, chilled, and frozen items simultaneously.

5G and Real-Time Delivery Optimization

5G network rollout in European cities is enabling real-time communication between delivery riders, dark store dispatchers, and consumers at millisecond latency, allowing dynamic route optimization that adjusts delivery paths live based on traffic conditions, order clustering opportunities, and rider capacity.

Contactless, BNPL, and Embedded Payment Technology

European online grocery checkout has become a primary fintech innovation battleground. 78% of 16 to 24-year-olds regularly use mobile payments, reducing checkout abandonment. Buy Now Pay Later (BNPL) integration in grocery apps allows high baskets to be spread across 3 installments, increasing average basket size by 22–28% for budget-conscious consumers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Types |

Vegetables and Fruits |

32.0% |

2025 |

|

Business Models |

Hybrid Marketplace |

53.0% |

2025 |

|

Platform |

App-Based |

68.08% |

2025 |

|

Purchase Types |

One-Time |

83.0% |

2025 |

|

Country |

Germany |

26.0% |

2025 |

By Platform

To access detailed market analysis, Request Sample

App-based platforms lead at 68.08% market share (2025). This dominance reflects the smartphone’s primacy in European daily life, Europeans spend an average 4.8 hours daily on their smartphones, with grocery apps accessible at any moment compared to web-based platforms requiring active computer access. Grocery apps’ push notification capabilities, stored payment methods, and one-tap reorder functionality create frictionless repeat purchase journeys that web browsers cannot match.

Web-based platforms at 31.92% remain important for desktop-first consumers, particularly in the 55+ age cohort that represents European online grocery spending, and for large weekly shops where users prefer the larger screen for browsing full product catalogues, comparing nutritional information, and managing recurring order lists. Web platforms also serve B2B corporate ordering, where procurement managers place large, complex orders on desktop systems.

By Purchase Type

One-time purchases dominate at 83.0% (2025). This dominance reflects the current stage of European online grocery development; the majority of consumers still approach online grocery as a transactional channel for specific shopping occasions rather than a subscription service for habitual grocery management. One-time purchase behavior is particularly prevalent for q-commerce apps and for consumers supplementing their in-store primary shop with specific online items unavailable locally.

Subscription at 17.0% is the fastest-growing segment at ~27.4% CAGR, more than double the overall market rate. The economics are compelling for both platforms and consumers: subscribers generate 4–6× the annual GMV of non-subscribers, while consumers with unlimited free delivery subscriptions order 3.5× more frequently than pay-per-delivery customers. Amazon Prime’s grocery delivery benefit, Ocado Smart Pass, Rohlik’s Premium subscription, and Picnic’s planned subscription service represent Europe’s leading grocery subscription programs.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

Germany |

26.0% |

Highest e-commerce adoption in Europe; Rewe and Edeka online grocery expansion |

|

United Kingdom |

22.4% |

Most mature European online grocery market; Ocado’s world-class robotic fulfilment |

|

France |

18.3% |

Drive-through click-and-collect model; Monoprix’s Paris premium delivery; Intermarche’s rural drive network expansion |

|

Italy |

14.2% |

Fastest-growing European online grocery market from low base; Esselunga Online Italy market leader; Amazon Fresh Milan and Rome |

|

Spain |

10.4% |

Mercadona Online Spain’s most trusted grocery brand, is launching national delivery; growing immigrant population adopting app-based grocery for cultural food products |

|

Others |

8.7% |

Netherlands’ Picnic ultra-efficient electric van delivery model; Poland’s Allegro grocery and Biedronka online growth; Sweden’s Matsmart and MatHem growth; Belgium’s Colruyt and Proxy Delhaize online |

Germany’s 26.0% dominance underscores the country’s dual position as Europe’s largest grocery market and its most innovation-dense online grocery ecosystem. Berlin has emerged as the capital of European q-commerce, hosting the headquarters of Gorillas, Flink, and Knuspr, and this concentration of VC-backed q-commerce investment has fundamentally shifted German consumer expectations for delivery speed.

The UK’s 22.4% share represents Europe’s most mature online grocery market by penetration rate. Ocado’s unique position as Europe’s only pure-play online grocery retailer with proprietary robotic fulfilment technology has given the UK a global-first operational model studied by grocery retailers worldwide, highlighting the innovation and growth potential of the Online Grocery Market in UK. The UK’s post-pandemic hybrid work patterns have permanently elevated mid-week online grocery ordering as employees work from home on days when supermarket visits would have previously been impossible.

Competitive Landscape

The Europe online grocery market is moderately concentrated, with Amazon Fresh, Tesco Online, and Carrefour collectively representing approximately 35-40% of European online grocery GMV.

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

Amazon.com, Inc. |

Amazon Prime |

Dominant Market Leader |

Europe’s largest online marketplace as a fulfilment infrastructure for grocery; Amazon Fresh operates France, Italy, Spain with 2-hour delivery |

|

Tesco.com |

Tesco Groceries |

Market Leader |

UK’s #1 online grocery platform, Tesco Whoosh same day home delivery |

|

Carrefour Group |

Carrefour Drive |

Market Leader |

France’s one of the largest grocery retailers with 15%+ online share via Drive click-and-collect; Carrefour’s data alliance with Google Cloud for AI-powered personalized promotions |

|

Rewe Group |

rewe.de |

Strong Challenger |

Germany’s one of the online grocers with around 6K+ stores across the country; systematic slot-based home delivery in German cities |

|

Flink SE |

Flink Grocery App |

Specialist |

Berlin-headquartered q-commerce pure-play |

|

Ocado Retail Limited |

Ocado.com |

Technology Leader |

UK’s pure-play online grocer and world’s most advanced grocery technology platform |

The top five platforms account for approximately 50–55% of the total market value. The remaining 45–50% is distributed across national supermarket chains’ online operations, q-commerce specialists, dedicated online grocers, and food delivery aggregators with grocery add-on services.

Key Company Profiles

Amazon.com, Inc.

Amazon is Europe’s dominant online grocery infrastructure company, leveraging its Prime membership ecosystem, AWS logistics technology, and fulfillment network to operate Amazon Fresh grocery delivery in the UK, Germany, France, Italy, and Spain.

- Portfolio: Amazon Prime, Amazon Fresh.

- Recent Developments: In May 2025, Amazon planned to launch Same-Day Delivery in 20 new locations across Europe, including places like Augsburg, Metz, and Bergamo, in the 12 months.

- Strategic Focus: Prime membership as grocery customer acquisition engine, every European Prime renewal included grocery delivery as primary retention benefit; AWS grocery AI as B2B platform licensing opportunity for third-party retailers; drone delivery Prime Air European certification pursuit for 2025–2026 commercial launch.

Tesco.com

Tesco is Europe’s leading supermarket-owned online grocery operator and the UK’s online grocer.

- Portfolio: Tesco Groceries

- Recent Developments: In September 2024, Tesco launched a new e-commerce initiative, Transcend Retail Solutions, to rival Ocado and assist global supermarket chains in growing their online operations.

- Strategic Focus: Clubcard data platform as unassailable competitive moat for personalized online grocery; CFCs automation expansion reducing fulfilment cost to sub-EUR 2 per order; Tesco Now q-commerce competing directly for impulse UK grocery; Tesco Delivery Saver subscription as customer lifetime value maximization – subscribers spend 4.5× more annually than non-subscribers.

Flink SE

Flink is Europe’s leading independent q-commerce grocery specialist, operating dark stores across Germany and Netherlands with its 10-minute grocery delivery promise.

- Portfolio: Flink grocery app for 10-minute delivery of 2,500–3,500 ambient, chilled, and frozen SKUs.

- Recent Developments: In March 2026, Flink secured $100 million in fresh funding from Prosus Ventures and Btomorrow Ventures, valuing the Berlin-based grocery delivery startup at $900 million. The round reflects renewed investor confidence in the sector following a post-COVID slowdown, bringing the company’s total funding to approximately $1.4 billion.

- Strategic Focus: Subscription penetration (target: 25% orders from subscribers) and further picking automation; REWE strategic partnership deepening through co-branded product development; European expansion into Belgium, Poland, and Switzerland as near-term geographic targets for 2025–2027.

Market Concentration Analysis

The Europe online grocery market exhibits moderate concentration at the platform tier, with Amazon Fresh, Tesco Online, and Carrefour collectively accounting for approximately 35-40% of total European online grocery GMV. The top five platforms represent approximately 50–55% of total market value. This moderate concentration level is unusual for a digital commerce category where platform economics typically drive winner-take-all dynamics, but European online grocery’s geographic fragmentation by national retail preferences prevents any single platform from achieving pan-European dominance.

Market fragmentation below the top tier is pronounced. National supermarket chains’ online operations capture 25–35% of their respective national online grocery markets with limited cross-border presence. Q-commerce specialists have each established city-level market positions in 2–6 European countries but lack the pan-European scale of Amazon or Tesco. This geographic fragmentation makes Europe’s online grocery market an aggregation of 20+ distinct national markets rather than a single homogeneous European market, requiring multinational operators to adapt platform design, product assortment, and fulfilment models to each country’s specific consumer preferences and infrastructure constraints.

Investment & Growth Opportunities

Fastest Growing Segments

Subscription-based grocery (~27.4% CAGR), app-based platform channel (~24.1% CAGR), q-commerce dark store expansion (~35%+ CAGR), and B2B online grocery (~30–35% CAGR) represent the four highest-return investment vectors through 2034. Italy’s online grocery market, growing at ~25.8% from a 3.2% penetration base, represents the highest absolute incremental market opportunity among the five major European markets, with an estimated USD 35–45 billion in incremental annual GMV achievable by 2034 as penetration converges toward the European average.

Emerging Market Opportunities

CEE (Central and Eastern European) online grocery markets, Poland, Czech Republic, Hungary, Romania, Bulgaria, represent the highest-growth European online grocery frontier, with online grocery penetration below 2% in most CEE countries and in total grocery market value.

Venture and Institutional Investment Themes

European online grocery attracted venture and growth equity investments, with dark store automation, grocery subscription platforms, and sustainable delivery infrastructure as primary investment themes.

- Key investment themes: Dark store automation CAPEX, grocery subscription LTV models, AI demand forecasting SaaS, electric last-mile fleet deployment, B2B catering grocery platforms, and voice-and-smart-home grocery reordering infrastructure.

- Strategic M&A pipeline: Amazon, Tesco, and Carrefour are evaluating acquisitions of national online grocery champions in Italy, Spain, and CEE markets to accelerate penetration versus organic platform build timelines.

Future Market Outlook (2026-2034)

The Europe online grocery market is entering its most transformational phase in its 25-year history. From USD 81.81 Billion in 2025, the market will reach USD 506.88 Billion by 2034, at a 22.46% CAGR. This extraordinary growth is powered by three irreversible structural forces: online grocery penetration convergence in mature digital retail categories as platform quality, delivery speed, and price competitiveness reach parity with physical supermarkets; the subscription economy’s transformation of occasional online grocery buyers into habitual daily digital shoppers whose annual online grocery spend is 4–6× that of non-subscribers; and the demographic replacement of grocery’s remaining digital laggards, with digitally native under-35 consumers who will conduct 40–60% of their lifetime grocery spending online as their natural default behavior.

Research Methodology

Primary Research

Primary research included structured interviews with 150+ industry stakeholders in 2025, comprising online grocery platform commercial directors, dark store operations managers, last-mile logistics executives, FMCG e-grocery trade marketing leads, consumer behavior researchers, and EU digital commerce regulatory experts. Geographic coverage spanned Germany, UK, France, Italy, Spain, Netherlands, and Poland. Primary insights validated platform market shares, consumer adoption behavioral drivers, and technology investment timelines.

Secondary Research

Secondary research encompassed Statista digital commerce data, Kantar retail FMCG panel data, Eurostat consumer expenditure surveys, Pitchbook venture investment data, EuroCommerce e-grocery policy reports, company annual reports and earnings call transcripts, EU DMA and DSA regulatory documents, and food e-commerce academic research. Over 280 secondary sources were reviewed and synthesized.

Forecasting Models

Market size forecasts were developed using a bottom-up country-platform aggregation validated against top-down. Key inputs include European internet penetration forecasts, online grocery penetration S-curve adoption models by country, smartphone commerce conversion rates, q-commerce unit economics evolution projections, and subscription uptake diffusion models.

Europe Online Grocery Market Report Segmentation:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Covered | Vegetables and Fruits, Dairy Products, Staples and Cooking Essentials, Snacks, Meat and Seafood, Others |

| Business Model Covered | Pure Marketplace, Hybrid Marketplace, Others |

| Platform Covered | Web-Based, App-Based |

| Purchase Covered | One-Time, Subscription |

| Country Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | Amazon.com, Inc., Tesco.com, Carrefour Group, Rewe Group, Flink SE, Ocado Retail Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Europe Online Grocery Market Report

The Europe online grocery market was valued at USD 81.81 billion in 2025 and is projected to reach USD 506.88 billion by 2034.

The Europe online grocery market is forecast to grow at a CAGR of 22.46% during 2026-2034, driven by smartphone adoption, q-commerce expansion, subscription models, and post-COVID behavioral permanence.

App-based platforms dominate with 68.08% revenue share (2025), driven by smartphone primacy in European commerce, push notification reordering, 1-tap checkout, and superior conversion versus web-based platforms.

One-time purchases lead at 83.0% market share (2025), though subscription is growing fastest at ~27.4% CAGR as Amazon Prime, Ocado, and Flink Premium drive subscription grocery model adoption.

Germany leads with 26.0% market share (2025), driven by Europe’s highest Amazon Prime household penetration, Berlin q-commerce innovation hub, and Rewe’s systematic digital grocery expansion across 55+ cities.

Key market players include Amazon.com, Inc., Tesco.com, Carrefour Group, Rewe Group, Flink SE, and Ocado Retail Limited.

Key drivers include post-COVID permanent digital grocery habit formation, smartphone app explosion, q-commerce 10-minute delivery normalization, urbanization, dual-income time poverty, and AI personalization improving conversion.

Key trends include autonomous dark store fulfilment, subscription-first models, social commerce grocery, sustainability-led delivery, voice and smart home integration, and B2B corporate catering channel development.

Key challenges include cold-chain last-mile logistics cost, consumer fresh produce quality trust gaps, high customer acquisition costs, q-commerce unit economics, DMA regulatory pressure on dominant platforms, and food inflation impact on basket size.

Italy’s 3.2% online grocery penetration creates massive headroom. Amazon Fresh, Rohlik (Sezamo), and Glovo are driving rapid adoption with same-day delivery from multiple competing platforms now live in Milan and Rome.

Top opportunities include dark store automation CAPEX, grocery subscription platforms, AI demand forecasting SaaS, EV delivery fleets, B2B catering grocery, CEE market penetration, and voice/smart-home grocery integration technology.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)