Adhesion Promoter Market Size, Share, Trends and Forecast by Type, Form, Application, End Use Industry, and Region, 2026-2034

Adhesion Promoter Market Size and Share:

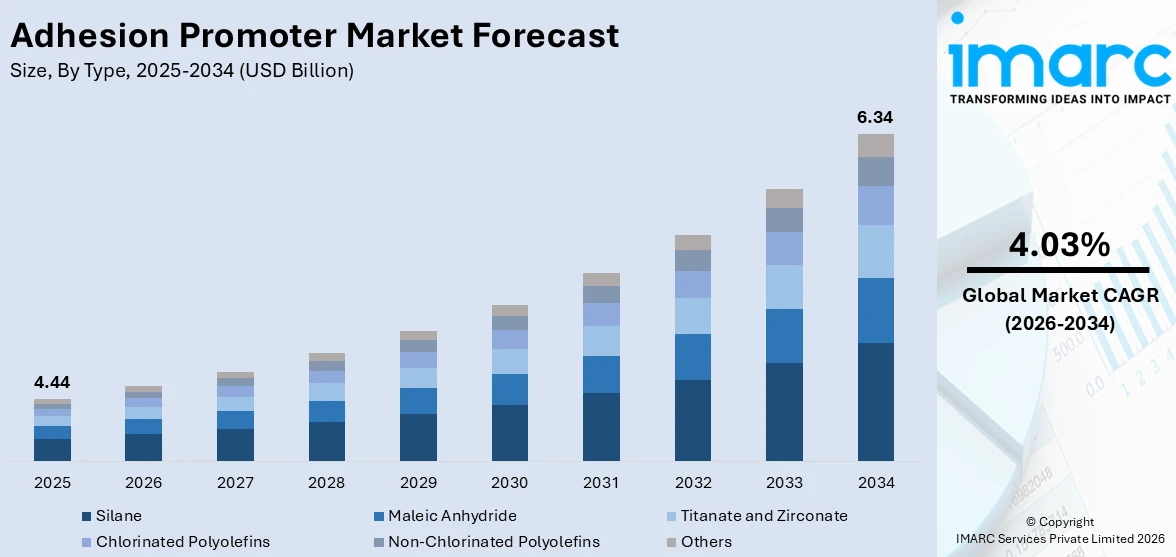

The global adhesion promoter market size was valued at USD 4.44 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 6.34 Billion by 2034, exhibiting a CAGR of 4.03% from 2026-2034. North America currently dominates the market, holding a market share of 29% in 2025. The region benefits from a well-established automotive sector, robust industrial manufacturing base, and stringent environmental regulations that drive adoption of advanced adhesion promoters across diverse applications, thereby contributing to the adhesion promoter market share.

The growing demand for adhesion promoters across end-use industries, such as automotive, construction, packaging, and electronics, is a primary factor influencing the market growth. The rising employment of advanced polymers, composites, and specialty coatings in construction activities is fueling the need for high-performance bonding solutions. Furthermore, the robust packaging industry, driven by increasing e-commerce activities and shifting user preferences toward durable and sustainable packaging, is boosting the demand for adhesion promoters. Additionally, the growing emphasis on infrastructure development across both developed and emerging economies continues to generate consistent demand for surface treatment chemicals. The trend of multi-material assemblies in manufacturing, where dissimilar substrates need reliable interfacial bonding, is also propelling the adhesion promoter market growth.

The United States is emerging as a major regional market for adhesion promoters, supported by strong demand across automotive and advanced manufacturing sectors. The country’s automotive industry is a key user, particularly in applications involving lightweight composites and multi-material vehicle assemblies that require durable bonding between metals, plastics, and engineered substrates. The rapid expansion of electric mobility is further accelerating the need for reliable adhesion solutions in battery enclosures, structural modules, and thermal management systems. Reflecting this growth trajectory, the United States electric vehicles market reached a value of USD 235.2 Billion in 2025, according to the IMARC Group. This substantial market size underscores the rising integration of advanced adhesion technologies across next-generation vehicle platforms.

To get more information on this market Request Sample

Adhesion Promoter Market Trends:

Growing Focus on Sustainable and Efficient Solutions

The rising emphasis on sustainability and eco-friendly formulations is a key factor influencing the adhesion promoter market. As industries increasingly demand environmentally responsible alternatives, companies are introducing innovative products that align with both performance and regulatory standards. For example, in 2024, Allnex launched ALNOVOL® PN 870, an advanced adhesion promoter tailored for tires and technical rubber. This revolutionary product replaced traditional adhesion systems that contain cobalt and resorcinol, both of which have raised environmental concerns. ALNOVOL® PN 870 offered exceptional adhesion, improved scorch resistance, and enhanced aging properties, addressing the industry's need for efficient, sustainable solutions. The introduction of such products highlights the automotive sector’s growing preference for safer, high-performance materials while meeting sustainability goals. As companies are investing in technologies that balance performance, safety, and environmental impact to meet rising individual expectations and industry standards, the adhesion promoter market outlook remains favorable.

Increasing Demand for Durable and High-Performance Adhesion Promoters

There is a rise in the demand for durable and high-performance adhesion promoters across various industries, which represents a vital factor propelling the market growth. With advancements in digital printing technology and a focus on improving product quality and longevity, the need for effective adhesion solutions is becoming more critical. A prime example of this trend is the 2024 launch of Boston Industrial Solutions' Natron® G2 Glass Primer. Specifically designed for UV printing on glass, tiles, and ceramics, this UV adhesion promoter offered superior resistance to moisture, weather, and industrial washing cycles. Its two-step application process ensured long-lasting durability while providing cost-effective solutions for manufacturers and printers working in demanding conditions. The product’s ability to withstand harsh environments makes it a vital component in sectors, such as construction, automotive, and consumer goods. The growing requirement for products that can endure challenging conditions is impelling the market growth as companies continue to innovate to meet these demands.

Advancements in Adhesion Promoters

The growing demand for high-performance and durable adhesion promoters in industries like construction, automotive, and coatings is positively influencing the market. One key development is Evonik’s introduction of Visiomer Hema-P 100 in 2024, a phosphate methacrylate monomer that provides superior adhesion, flame retardancy, and corrosion resistance. This advanced adhesion promoter was designed for applications in direct-to-metal (DTM) coatings, structural adhesives, and waterproofing, where long-lasting performance is essential. The product’s unique formulation offered non-migratory flame retardancy, making it ideal for use in environments requiring enhanced safety and durability. Additionally, the high monoester content of Visiomer Hema-P 100 ensured superior compatibility with various polymer systems, such as acrylic adhesives and composites. These characteristics not only improve product performance but also meet the increasing regulatory and safety demands across industries. As manufacturers focus on creating more reliable and robust solutions, products like Visiomer Hema-P 100 are pushing the boundaries of adhesion technology, strengthening the market growth.

Adhesion Promoter Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global adhesion promoter market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, form, application, and end use industry.

Analysis by Type:

- Silane

- Maleic Anhydride

- Titanate and Zirconate

- Chlorinated Polyolefins

- Non-Chlorinated Polyolefins

- Others

Silane holds a 26% share of the market due to its crucial role in enhancing the performance of various materials. As coupling agents, silane acts as intermediaries, effectively bonding organic polymers to inorganic substrates. This process enhances key properties, such as heat resistance, weatherability, and moisture resistance, making silane-based promoter indispensable across multiple industries. Its versatility ensures high demand in automotive, construction, and electronics sectors. Specifically, silane is crucial in composite materials, paints, coatings, and rubber applications, where it significantly improves mechanical strength and chemical stability. In the automotive sector, silane is used to enhance the durability of coatings, while in construction, it contributes to the strength of concrete and sealants. In electronics, silane improves the adhesion of components in demanding environments. As industries continue to prioritize performance and longevity, the demand for silane-based adhesion promoter remains strong, supporting their continued growth in the market.

Analysis by Form:

- Liquid Form

- Spray Form

Liquid form leads the market with a share of 70%. Liquid adhesion promoter is the preferred formulation type across a wide range of industrial applications owing to its superior handling and application properties. Its ease of use, excellent substrate wetting capabilities, and consistent coating uniformity make it the preferred choice across various industrial sectors. Liquid formulations allow for precise application through dipping, brushing, or roller coating methods, ensuring thorough and uniform coverage of complex surfaces and geometries. This versatility makes liquid adhesion promoter ideal for integration into manufacturing workflows, especially in continuous production lines. It is particularly beneficial in industries, such as automotive, where it is used in components like body panels and engine parts, electronics for circuit board coatings, and packaging for enhanced material bonding. Adhesion promoter market forecast indicate that this strong performance of liquid formulations will continue to reinforce their dominance across key end-use industries for its ability to deliver reliable results.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

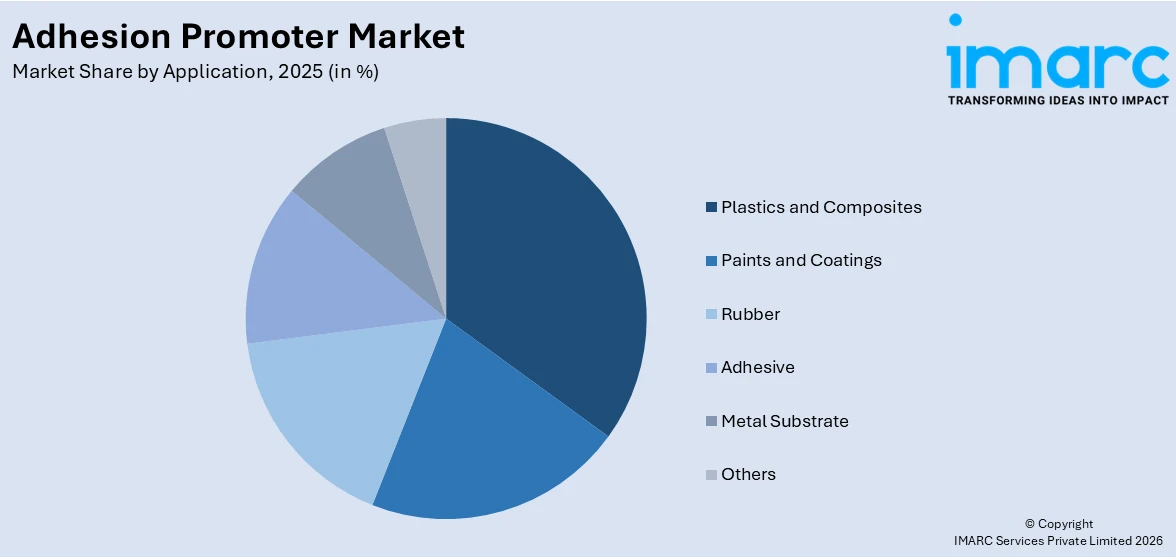

- Plastics and Composites

- Paints and Coatings

- Rubber

- Adhesive

- Metal Substrate

- Others

Plastics and composites dominate the market, accounting for 33% of the total share. This segment represents the largest application area due to the expanding adoption of fiber-reinforced plastics, thermoplastic composites, and multi-material assemblies across the automotive, aerospace, and construction sectors. Adhesion promoters play a critical role in strengthening interfacial bonding between organic polymer matrices and inorganic reinforcements, including glass fibers, carbon fibers, and mineral fillers, thereby enhancing structural integrity and long-term performance. The rising emphasis on lightweight vehicle design and energy-efficient infrastructure is further driving the demand for high-performance composite materials. Reflecting this momentum, in 2025, Boston Industrial Solutions introduced the Natron MD3 UV Adhesion Promoter, specifically formulated to improve UV ink adhesion on challenging substrates, such as aluminum composite panels and powder-coated metals, delivering enhanced durability and resistance to chipping and peeling in demanding industrial applications. These developments collectively highlight evolving adhesion promoter market trends, underscoring the growing importance of advanced bonding solutions in high-performance plastics and composite applications.

Analysis by End Use Industry:

- Automotive and Transportation

- Electrical and Electronics

- Packaging

- Consumer Goods

- Construction

- Others

Automotive and transportation represent the leading segment, with a market share of 28%. The sector’s dominance is driven by the growing adoption of multi-material vehicle architectures, advanced coating technologies, and lightweight composite components aimed at improving fuel efficiency and structural performance. Adhesion promoters are essential in facilitating durable bonding between dissimilar substrates such as metals, plastics, and glass used in body panels, bumpers, interior trims, and under-the-hood systems. The accelerating shift toward EVs is further catalyzing the demand for high-performance adhesion solutions in battery module assembly and thermal management applications. Reflecting this technological progression, in 2025, 3M introduced the 3M™ VHB™ Tape Max Series, engineered with advanced acrylic chemistry to deliver superior bonding strength as an alternative to mechanical fasteners, thereby enhancing efficiency, reliability, and long-term durability in demanding transportation environments.

Regional Analysis:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 29% of the share, enjoys the leading position in the market. The region’s dominance is supported by a highly developed automotive manufacturing base, strong industrial infrastructure, and stringent environmental regulations that encourage the adoption of advanced surface treatment and bonding chemicals. Increasing investments in electric mobility and localized supply chains are further reinforcing the demand for high-performance adhesion promoters across vehicle assembly and component manufacturing. Reflecting this momentum, in 2024, Honda Motor Co. announced plans to invest nearly USD 11 Billion in Canada to establish a comprehensive EV value chain, including a battery production facility in Alliston, Ontario, with a targeted capacity of 240,000 EVs annually by 2028. Such large-scale investments are expected to stimulate sustained demand for advanced adhesion technologies throughout the regional automotive and materials ecosystem.

Key Regional Takeaways:

United States Adhesion Promoter Market Analysis

The United States represents the largest contributor to the adhesion promoter market, driven by its well-established automotive industry, expansive construction activities, and stringent regulatory framework supporting sustainable and low-emission chemical technologies. Automotive manufacturers are increasingly implementing multi-material vehicle architectures that depend on advanced adhesion promoters to ensure strong and durable bonding between metals, plastics, and composite materials in both structural and exterior applications. The rapid expansion of EV production is further catalyzing the demand for specialized adhesion solutions in battery pack assembly, thermal management systems, and lightweight structural components. According to estimates by the International Council on Clean Transportation, more than 1.2 million light-duty electric vehicles were sold in the United States during the first three quarters of 2025, underscoring the scale of electrification and its impact on material innovation requirements. Additionally, sustained investments in semiconductor manufacturing and advanced electronics production continue to strengthen the need for high-performance adhesion promoters across diverse industrial applications.

Europe Adhesion Promoter Market Analysis

Europe constitutes a prominent market for adhesion promoters, supported by its robust automotive manufacturing base, advanced construction landscape, and well-established aerospace and industrial sectors. Regulatory directives introduced by the European Union are accelerating the transition toward low-VOC and environmentally sustainable adhesion technologies, encouraging manufacturers to adopt high-performance solutions that enhance durability while minimizing ecological impact. The region’s strong automotive output further reinforces demand. For instance, Germany’s passenger car production reached 347,100 units in July, reflecting a 9% year-on-year increase, while EV production surged to 864,000 units in the first half of 2025, accounting for 40% of total output. This expansion in electric mobility, coupled with the growing investments in renewable energy infrastructure and energy-efficient buildings, is driving the need for advanced bonding solutions capable of joining metals, composites, and engineered plastics across diverse high-performance applications.

Asia-Pacific Adhesion Promoter Market Analysis

The Asia-Pacific region is experiencing significant growth in the adhesion promoter market, supported by rising automotive production, expanding infrastructure projects, and rapid industrialization across emerging economies. Increasing investments in construction, manufacturing, and advanced materials are strengthening the demand for high-performance bonding solutions in adhesives, coatings, and plastics applications. Reflecting this upward trajectory, in 2025, Wacker Chemie AG and SICO Performance Material inaugurated a 2,300-square-meter application development center in Jining, China, dedicated to advancing organofunctional silanes and adhesion promoter technologies. The facility was designed to accelerate product innovation and support the growing need for hybrid polymers and advanced adhesion systems. Such strategic expansions reinforce the region’s role as a key hub for technological advancement and market growth.

Latin America Adhesion Promoter Market Analysis

Latin America is emerging as a promising market for adhesion promoters, supported by expanding automotive production in Brazil and Mexico, growing construction activities, and increasing industrial modernization across the region. The rising demand for durable and sustainable packaging solutions is driving adoption of adhesion promoters in the packaging sector. For instance, in 2025, the automotive production in Brazil totaled 184,500 units (including cars, light commercial vehicles, trucks, and buses), as reported by sector association Anfavea, compared to 219,100 units in November, creating significant demand for adhesion-enhanced coatings and composite materials. The region's focus on infrastructure development and urbanization continues to generate opportunities for adhesion promoter applications in construction sealants and protective coatings.

Middle East and Africa Adhesion Promoter Market Analysis

The Middle East and Africa region presents growing opportunities for adhesion promoter manufacturers, driven by expanding construction activities, increasing infrastructure investments, and the development of local manufacturing capabilities. The region's ambitious infrastructure projects, particularly in the Gulf Cooperation Council countries, are generating demand for adhesion promoters used in construction sealants, coatings, and concrete applications. For example, in 2024, Saudi Arabia announced a USD 1.28 Billion investment in housing projects for 2025, planning the construction of 16,000 new homes, apartments, and villas across the Kingdom, supporting demand for advanced surface treatment chemicals.

Competitive Landscape:

The global adhesion promoter market is characterized by a moderately consolidated competitive landscape, with leading chemical companies utilizing their technological expertise, broad product portfolios, and extensive distribution networks to secure dominant positions. To stay ahead of market demands, key players focus on product innovation and strategic partnerships, alongside expanding their production capacities. In response to growing environmental concerns, there is a shift towards sustainable formulations. As a result, companies are increasingly investing in research and development (R&D) to create eco-friendly solutions, such as water-based, bio-based, and low-VOC adhesion promoter technologies. These innovations not only align with regulatory requirements but also address the evolving needs of industries such as automotive, packaging, and construction, where high-performance and environmentally conscious products are becoming essential. This focus on sustainability is expected to drive future growth and strengthen the market's competitiveness.

The report provides a comprehensive analysis of the competitive landscape in the Adhesion Promoter market with detailed profiles of all major companies, including:

- 3M Company

- Akzo Nobel N.V.

- Arkema S.A.

- Borica Co. Ltd.

- Eastman Chemical Company

- Ems-Chemie Holding AG

- Evonik Industries AG

- Momentive Performance Materials Inc.

- Nagase America LLC (Nagase & Co. Ltd.)

- Nippon Paper Industries Co. Ltd.

- The Dow Chemical Company

- Toyobo Co. Ltd.

Latest News and Developments:

- In February 2026, Borchers, a Milliken brand, is showcasing advanced coating additives at Paint India in Mumbai, aimed at enhancing performance and durability in modern coatings formulations. The portfolio includes catalysts, dispersants, and adhesion promoters designed to support industry trends like waterborne systems and sustainability. Highlighted products include Borchi® OXY-Coat 1101 for waterborne alkyd coatings, next-gen dispersants for pigment dispersion, and Borchi® Gen AOD, an adhesion promoter for non-ferrous substrates.

- In June 2025, Boston Industrial Solutions introduced the world's first acrylic adhesion promoter, Natron® LX5, designed to enhance latex ink adhesion to acrylic and metal surfaces. This innovative primer improved ink flexibility, durability, and weather resistance, addressing long-standing challenges in eco-friendly ink applications. It offered a ready-to-use solution, ensuring strong bonds and preventing issues like chipping or peeling, particularly in the signage industry.

- In March 2025, TRAMACO launched TRAPYLEN® 189 S, a new adhesion promoter for printing inks, particularly in screen printing. The product, based on chlorinated polypropylene, features an ECHA-compliant stabilizer and provided excellent adhesion, high gloss, and weather resistance. It also served as an adhesion promoter for plastic coatings and solvent-based adhesives, with versatile applications in various industries.

Adhesion Promoter Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Silane, Maleic Anhydride, Titanate and Zirconate, Chlorinated Polyolefins, Non-Chlorinated Polyolefins, Others |

| Forms Covered | Liquid Form, Spray Form |

| Applications Covered | Plastics and Composites, Paints and Coatings, Rubber, Adhesive, Metal Substrate, Others |

| End Use Industries Covered | Automotive and Transportation, Electrical and Electronics, Packaging, Consumer Goods, Construction, Others |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | 3M Company, Akzo Nobel N.V., Arkema S.A., Borica Co. Ltd., Eastman Chemical Company, Ems-Chemie Holding AG, Evonik Industries AG, Momentive Performance Materials Inc., Nagase America LLC (Nagase & Co. Ltd.), Nippon Paper Industries Co. Ltd., The Dow Chemical Company, Toyobo Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the adhesion promoter market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global adhesion promoter market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the adhesion promoter industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Adhesion Promoter Market Report Report

The adhesion promoter market was valued at USD 4.44 Billion in 2025.

The adhesion promoter market is projected to exhibit a CAGR of 4.03% during 2026-2034, reaching a value of USD 6.34 Billion by 2034.

The adhesion promoter market is primarily driven by the growing focus on sustainable and efficient solutions, increasing demand for durable high-performance formulations, and continuous technological advancements in product development. Manufacturers are prioritizing eco-friendly chemistries that comply with regulatory standards while maintaining superior bonding strength. Simultaneously, industries require long-lasting adhesion under harsh operating conditions, encouraging innovation in advanced, multifunctional promoter systems.

North America currently dominates the adhesion promoter market, accounting for a share of 29%. The region benefits from a robust automotive manufacturing base, stringent environmental regulations promoting advanced surface treatment solutions, and significant investments in electric vehicle production and infrastructure development.

Some of the major players in the adhesion promoter market include 3M Company, Akzo Nobel N.V., Arkema S.A., Borica Co. Ltd., Eastman Chemical Company, Ems-Chemie Holding AG, Evonik Industries AG, Momentive Performance Materials Inc., Nagase America LLC (Nagase & Co. Ltd.), Nippon Paper Industries Co. Ltd., The Dow Chemical Company, Toyobo Co. Ltd., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade