AdTech Market Size, Share, Trends and Forecast by Solution, Advertising Type, Platform, Enterprise Size, Industry Vertical, and Region, 2026-2034

AdTech Market Size and Trends:

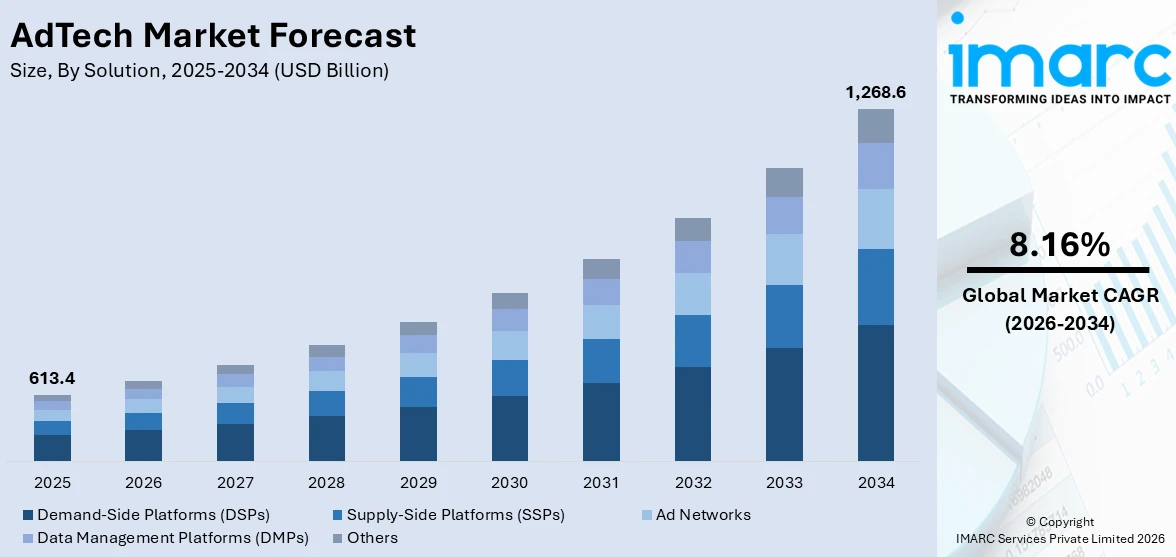

The global AdTech market size was valued at USD 613.4 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 1,268.6 Billion by 2034, exhibiting a CAGR of 8.16% from 2026-2034. North America currently dominates the AdTech market share by holding over 35.6% in 2025. The growth of the North American region is driven by advanced digital infrastructure, high internet penetration, strong user engagement, innovative solutions, and a robust regulatory environment, positioning it as a leader in AdTech market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 613.4 Billion |

| Market Forecast in 2034 | USD 1,268.6 Billion |

| Market Growth Rate (2026-2034) | 8.16% |

Businesses worldwide are adopting digital platforms to expand their reach, creating a higher demand for sophisticated advertising solutions. AdTech enables these businesses to target specific audiences effectively, maximizing engagement and return on investment (ROI) in a highly competitive environment. Additionally, artificial intelligence (AI) and machine learning (ML) technologies are improving advertising by enabling personalized campaigns, predictive analytics, and real-time bidding. These advancements allow advertisers to analyze vast amounts of data and deliver highly relevant content to audiences, improving campaign effectiveness. Moreover, the widespread adoption of smartphones and the growing popularity of social media platforms are offering a favorable AdTech market outlook. AdTech solutions enable advertisers to target users on their preferred devices and platforms, leveraging mobile-friendly and interactive ad formats.

To get more information on this market Request Sample

The United States is a crucial segment in the AdTech market growth, driven by the emergence of advanced platforms that prioritize privacy and leverage AI technologies. These solutions offer businesses enhanced tools for audience management, campaign execution, and monetization while addressing industry challenges such as data security and compliance. By integrating precision targeting with privacy-focused approaches, these platforms meet regulatory standards and build user trust. In 2024, Carter launched across North America as a privacy-first, AI-powered platform for the AdTech and Retail Media Network space. Designed for seamless integration and security, it empowers businesses with advanced audience management, campaign execution, and monetization tools. Carter's customizable, data-driven approach addresses key industry challenges while prioritizing privacy and precision.

AdTech Market Trends:

Technological Advancements in Advertising Solutions

The continuous improvement in technology is bolstering the advertising technology market growth. Advancements in digital solutions, analytics tools, and automation have empowered advertisers to enhance the efficiency and effectiveness of their campaigns. The integration of innovative technologies, such as artificial intelligence (AI) and machine learning (ML) has enabled advertisers to gain deeper insights into user behavior and preferences. This, consequently, enables more focused and individualized advertising approaches, resulting in higher engagement and conversion rates. An industrial report states that AI-driven campaigns can improve ad targeting by up to 50%, leading to higher engagement and conversion rates. Ongoing Advancements in AI, ML, and real-time bidding drive innovation in AdTech, enabling personalized ad experiences, programmatic advertising, and strategic collaborations for improved data capabilities and streamlined advertising solutions. With these innovations, advertisers are progressively using advanced tools to enhance their ad positioning, creative materials, and overall campaign effectiveness.

Rising Importance of Data-driven Decision Making

The proliferation of data in the digital landscape has become a driving force behind the increasing AdTech market demand. Advertisers are now relying on data-driven insights to make informed decisions regarding their advertising strategies. According to an industrial report, 60-70% of marketers are indeed using data-driven insights to improve their campaigns. The collection and analysis of vast amounts of user data enables advertisers to understand their target audience better, identify trends, and tailor their campaigns accordingly. However, regulatory frameworks like the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA) reshape data-driven advertising, requiring AdTech companies to prioritize compliance, ethical data use, and adaptation to evolving privacy concerns in the industry. By harnessing the power of data, advertisers can optimize ad targeting, personalize content, and allocate resources more efficiently. The emphasis on data-driven decision-making not only enhances the effectiveness of advertising efforts but also provides advertisers with a competitive edge in a dynamic and evolving market.

Increasing Demand for Programmatic Advertising

The rising demand for programmatic advertising is a significant factor influencing the AdTech market outlook. Programmatic advertising involves the automated buying and selling of ad inventory using algorithms and real-time bidding. This approach enhances the precision of ad targeting and delivery, making campaigns more efficient and cost-effective. Advertisers can leverage programmatic platforms to reach specific audiences with tailored messages at the right moment, optimizing the overall impact of their advertising efforts. IAB reports that 80% of all display ads in the U.S. are now purchased programmatically, underscoring its growing importance. For example, in 2023, programmatic ad spending in Europe was expected to reach around EUR 30 billion (approximately USD 32 billion), with further growth anticipated, as per reports. The efficiency and scalability offered by programmatic advertising have led to its widespread adoption, making it a pivotal factor supporting the AdTech market trends. AdTech serves diverse industries, from small businesses to e-commerce giants, necessitating tailored approaches to address unique end-user needs while adapting to emerging service substitutes like blockchain and innovative content distribution.

AdTech Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global AdTech market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on solution, advertising type, platform, enterprise size, and industry vertical.

Analysis by Solution:

- Demand-Side Platforms (DSPs)

- Supply-Side Platforms (SSPs)

- Ad Networks

- Data Management Platforms (DMPs)

- Others

Demand-side platforms (DSPs) lead the market due to their efficiency, scalability, and ability to provide advertisers with a unified platform for managing ad campaigns across multiple channels. DSPs streamline the ad buying process by enabling real-time bidding (RTB), allowing advertisers to bid for ad impressions in milliseconds and target audiences with precision. This capability ensures optimized ad placements based on demographics, user behavior, and other advanced data points. The platforms' integration with robust analytics tools allows advertisers to track campaign performance, adjust strategies dynamically, and maximize return on investment. DSPs also support diverse ad formats, including display, video, mobile, and connected TV, ensuring advertisers can reach audiences on their preferred devices. Their scalability makes them particularly attractive for both large enterprises and small businesses aiming to enhance market presence. With advancements in artificial intelligence and machine learning, DSPs continue to evolve, offering predictive insights and enhancing the effectiveness of targeted campaigns, reinforcing their market leadership.

Analysis by Advertising Type:

- Programmatic Advertising

- Search Advertising

- Display Advertising

- Mobile Advertising

- Email Marketing

- Native Advertising

- Others

Search advertising holds the biggest AdTech market share due to its precision, cost-effectiveness, and ability to deliver measurable results. It enables businesses to target users based on intent, as individuals actively searching for specific products or services are more likely to convert into clients. The widespread use of search engines as primary information sources is making them a critical channel for advertisers seeking to capture high-intent audiences. Pay-per-click (PPC) models allow advertisers to control budgets while gaining visibility through AdTech bidding, ensuring campaigns are tailored to business objectives. Search advertising also benefits from integration with analytics tools, enabling detailed performance tracking, optimization, and data-driven decision-making. The rise of voice search and local search trends is further enhancing its relevance, enabling businesses to target niche markets effectively. With advancements in AI, personalized and predictive search advertising is becoming more sophisticated, ensuring relevance for users and maximizing returns for advertisers, solidifying its market dominance.

Analysis by Platform:

- Mobile

- Web

- Others

Mobile represents the largest segment with 55.4% of the market share in 2025. The mobile platform encompasses a wide array of devices such as smartphones and tablets. Advertising on mobile platforms involves reaching users through mobile applications, mobile websites, and other mobile-specific channels. Mobile advertising capitalizes on the on-the-go nature of users, delivering targeted and contextually relevant ads to individuals using their mobile devices. This is achieved through various formats like in-app ads, mobile web banners, interstitials, and video ads tailored specifically for the smaller screens of mobile devices. Additionally, mobile advertising benefits from sophisticated data analytics, enabling brands to segment audiences based on location, interests, and behavior. The integration of social media platforms and mobile apps further enhances ad reach, creating highly engaging campaigns. As mobile usage continues to grow globally, mobile advertising remains a crucial tool for brands seeking direct user engagement.

Analysis by Enterprise Size:

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

Large enterprises lead the market with 66.7% of market share in 2025. Large enterprises represent the largest segment due to their extensive resources, widespread operations, and substantial advertising budgets, which enable them to implement sophisticated and multi-channel advertising strategies. These organizations prioritize brand presence, leveraging a mix of digital, programmatic, and traditional platforms to reach a broad and diverse audience across various demographics. Their ability to invest in advanced technologies, such as AI, ML, and data analytics, allows for highly personalized and data-driven campaigns, ensuring optimal engagement and measurable outcomes. Large enterprises also benefit from their access to vast user datasets, enabling real-time insights and precise targeting that smaller competitors often cannot achieve. They often experiment with emerging formats, such as AR video ads, and interactive content, to create memorable individual experiences. Their scale and influence also make them key adopters of regulatory-compliant advertising practices, ensuring trust and sustainability.

Analysis by Industry Vertical:

Access the comprehensive market breakdown Request Sample

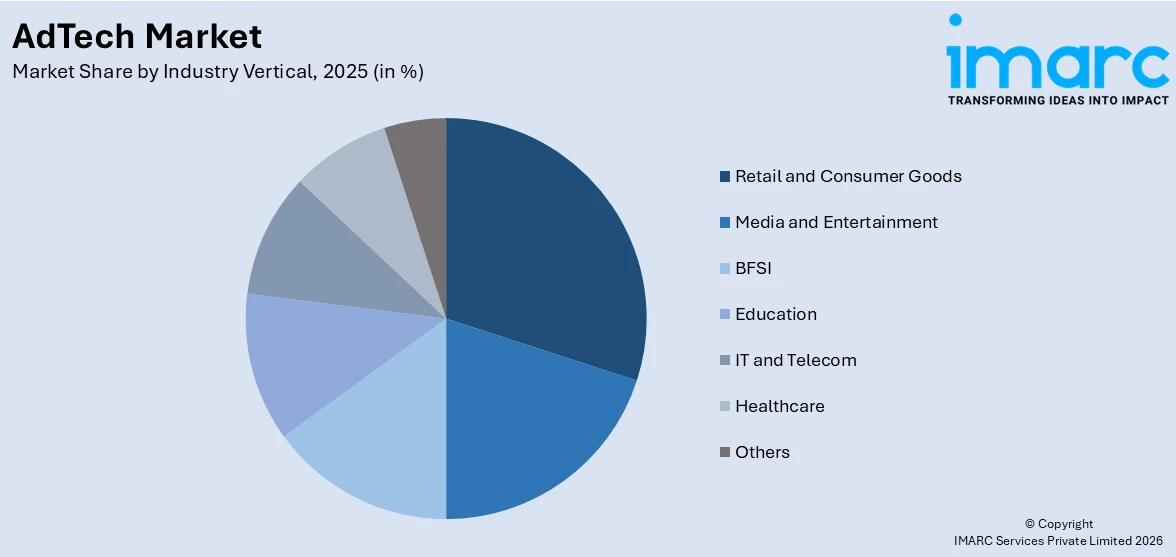

- Media and Entertainment

- BFSI

- Education

- Retail and Consumer Goods

- IT and Telecom

- Healthcare

- Others

In 2025, retail and consumer goods hold the biggest market share, accounting 28.7%. Retail and consumer goods lead the market due to their strong focus on client engagement and the need for highly targeted marketing strategies. These sectors rely heavily on data-driven insights to understand user behavior, preferences, and purchasing patterns, enabling them to design personalized campaigns that drive sales and enhance brand loyalty. With the widespread adoption of e-commerce and omnichannel retailing, businesses in this space use programmatic advertising, dynamic retargeting, and AI-driven tools to reach audiences across multiple touchpoints, ranging from websites and apps to social media platforms. The ability to track individual journeys in real-time allows retailers to optimize campaigns, improve conversion rates, and measure return on investment effectively. Furthermore, the integration of innovative technologies like AR and interactive ads is transforming client experiences, making advertising more engaging.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, the North America held the largest portion of the market, accounting 35.6%. North America leads the market because of its sophisticated technological framework, elevated digital literacy, and robust user involvement across multiple platforms. The area hosts prominent companies and pioneering startups that continuously impact the sector by utilizing advanced technologies like AI, ML, and programmatic advertising. The extensive adoption of smartphones, fast internet access, and social media sites is generating a fertile ground for marketing campaigns aimed at particular audiences. Moreover, the regulatory landscape of the region promotes the creation of privacy-centered solutions, enhancing trust between users and advertisers. Businesses in North America also gain from having access to extensive user data, which allows for more precise analytics and immediate insights. This vibrant ecosystem enables brands to develop tailored, effective campaigns, keeping North America leading in the AdTech sector. In 2024, Netflix revealed plans to introduce its own advertising technology platform, targeting a worldwide launch by late 2025. This shift enables Netflix to manage its advertising operations, deliver targeted ads to its 270 million users, and launch creative "episodic" advertising campaigns. The platform will launch in Canada prior to its expansion into the US and additional markets.

Key Regional Takeaways:

United States AdTech Market Analysis

In North America, the market share for the United States was 76.80% of the total. The U.S. AdTech market is booming as more people become dependent on digital advertising, data-driven marketing, and better targeting capabilities. According to an industrial report, the United States spent a record USD 225 billion on digital advertising in 2023, growing by 7.3% compared to 2022. The majority of the money spent falls under programmatic advertising, search engine marketing, and social media. In January 2023, an industrial report showed that about 246 million people in the U.S. used social media, making up 72.5% of the population. Companies such as Google, Meta, and Amazon dominate the landscape, thanks to their extensive data resources and ad solutions. The AI and machine learning being incorporated in the AdTech enhances the targeting effectiveness. Moreover, CCPA and GDPR push companies toward innovating in the direction of managing data and its security. Cross-platform advertisement has been a hot topic of concern for the United States too; here ad-tech companies have their eye on ensuring no breaks between platforms.

Europe AdTech Market Analysis

A survey conducted by IAB Europe disclosed a boost in the year 2023, with its total market valuation standing at an amount of about EUR 96.9 billion (USD 107.16 billion)-a 11.1% annual growth. IAB Europe shows that programmatic advertising has formed almost 60 percent of digital advertisement spending in the year 2023. This increasing shift towards programme trading is through higher automation in reaching the final clients. The market also benefits from strong multinational companies, such as The Trade Desk and Criteo, and the emergence of new local startups in ad targeting, analytics, and data privacy solutions. With more than 80% of Europeans online in 2023, as reported by Eurostat, the digital ad spend is increasing, with brands increasing their use of digital platforms to reach and engage with their audiences. Continued growth of mobile and video advertising further fortifies the region's digital ad market.

Asia Pacific AdTech Market Analysis

Asia Pacific is also recording robust growth in the digital advertising market. These have been largely propelled by growing internet penetration, increased smartphone adoption, and growing disposable incomes in the region. As per Digital Marketing for Asia, in 2023, it was estimated that digital ad spends in Asia Pacific stood at about USD 175.5 billion, or over 40% of global digital ad spending. China leads the chart with an expected USD 105.4 billion digital ad revenue mainly generated through mobile and social media advertisement. India's digital ad market has been growing quite rapidly, primarily driven by smartphone and internet penetration, and is expected to reach USD 10 billion in 2025. An industrial report says over 60 percent of the spend in digital advertisements in the Asia Pacific region goes into mobile in 2023. This speaks of a region increasingly turning digital for advertisements in Asia Pacific.

Latin America AdTech Market Analysis

The Latin America AdTech market is growing rapidly, with Brazil and Mexico being the largest contributors. According to industrial reports, Brazil accounts for around 50% of the digital retail media ad expenditure in 2023. Social media and video ads are particularly popular, driven by the fact that nearly 70% of the region's population engages with digital platforms. The rapid smartphone penetration is also supportive of the growth, with over 400 million Latin American users predicted to use a smartphone by 2024, as per reports. The rising digital engagement further adds fuel to e-commerce growth. This speaks to the growth potential in AdTech within Latin America as businesses look for means to access a more digitally connected individuals.

Middle East and Africa AdTech Market Analysis

The MEA AdTech market is witnessing rapid growth due to increasing digital engagement and mobile internet penetration across the region. As per an industrial report, approximately 39% of the population in the MENA region used mobile internet in 2023, and this opens opportunities for mobile-first advertising solutions. The Vision 2030 initiative of Saudi Arabia will also advance digital transformation, as well as the growth in e-commerce. This will directly increase the demand for targeted advertising technologies. As a consequence, while digital advertising spend is expected to rise by a significant margin within the region, the adoption of advanced advertising technologies is still being driven by the UAE, Saudi Arabia, and South Africa. These nations are now shaping the pace for digital transformation, leading to the introduction of innovative means of advertising, and providing ample opportunities for the AdTech industry to further strengthen its hold on the region.

Competitive Landscape:

The key players in the market are focusing on continuous innovation and strategic adaptations to evolving industry trends. These companies leverage advanced technologies, such as AI and ML, to enhance targeting precision and optimize ad performance. They prioritize user experience by developing interactive and personalized ad formats, fostering engagement. Investments in programmatic advertising and data analytics empower advertisers with tools for real-time bidding and insightful campaign measurement. As digital ecosystems expand globally, these players actively explore new channels and mediums, including the rising influence of connected TV and immersive experiences. In 2024, Cubera introduced Edge, a new Demand-Side Platform (DSP) designed to help businesses effectively reach the Indian audience with tailored advertising solutions. Edge supports diverse ad formats, offering flexibility, collaboration tools, and advanced analytics to enhance digital advertising. This launch marks the cornerstone of Cubera's broader AdTech ecosystem, focused on innovation and empowerment.

The report provides a comprehensive analysis of the competitive landscape in the AdTech market with detailed profiles of all major companies, including:

- Adobe Inc.

- Amazon.com Inc.

- Criteo

- Google LLC (Alphabet Inc.)

- Meta Platforms Inc.

- Microsoft Corporation

- Oracle Corporation

- The Trade Desk Inc.

Latest News and Developments:

- January 2025: Amazon Ads introduced the Amazon Retail Ad Service using AWS technology. This service allows retailers to serve contextually relevant ads, enriching shopping experiences. Beta participants include iHerb, Tilly's, and Oriental Trading Company. With Amazon Ads, advertisers can manage campaigns smoothly, reach a wider audience, and get data insights through its console and APIs.

- November 2024: Criteo highlighted its retail media ambitions at an investor event on Nov. 18, aiming to capture a USD 50 billion market by 2027. The firm’s shift from retargeting to retail media targets opportunities outside Amazon and China, projected to grow from USD 42 billion in 2022.

- October 2024: Adobe released GenStudio for Performance Marketing, which combines the generative AI tools of Firefly with partnerships of Google, Meta, and TikTok. It enables marketing and creative teams to execute campaigns at scale, relying on pre-approved assets and real-time performance insights to create personalized, compliant, and scalable content at scale across channels.

- July 2023: Meta Platforms Inc. unveiled Threads, a novel social media application.

- July 2023: Google introduced Bard, a competitor to Microsoft-backed ChatGPT, making it available in 180 countries as part of its broader integration of artificial intelligence (AI) throughout its platform.

AdTech Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Solutions Covered | Demand-Side Platforms (DSPs), Supply-Side Platforms (SSPs), Ad Networks, Data Management Platforms (DMPs), Others |

| Advertising Types Covered | Programmatic Advertising, Search Advertising, Display Advertising, Mobile Advertising, Email Marketing, Native Advertising, Others |

| Platforms Covered | Mobile, Web, Others |

| Enterprise Sizes Covered | Small and Medium-sized Enterprises (SMEs), Large Enterprises |

| Industry Verticals Covered | Media and Entertainment, BFSI, Education, Retail and Consumer Goods, IT and Telecom, Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Adobe Inc., Amazon.com Inc., Criteo, Google LLC (Alphabet Inc.), Meta Platforms Inc., Microsoft Corporation, Oracle Corporation, The Trade Desk Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the AdTech market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global AdTech market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the AdTech industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the AdTech Market Report

The AdTech market was valued at USD 613.4 Billion in 2025.

IMARC estimates the AdTech market to exhibit a CAGR of 8.16% during 2026-2034, expecting to reach USD 1,268.6 Billion by 2034.

The AdTech market is driven by trends such as technological advancements in advertising solutions, the rising importance of data-driven decision-making, and the increasing demand for programmatic advertising.

Large enterprises accounted for the largest market share based on enterprise type, holding 66.7%. This segment led to its extensive resources, broad operational reach, and significant advertising budgets, allowing for the implementation of advanced, multi-channel advertising strategies.

North America currently dominates the AdTech market, accounting for a share exceeding 35.6% in 2025. This dominance is fueled by the rising demand for targeted advertising, increased digital media consumption, advancements in AI and data analytics, and a growing focus on consumer behavior insights in North America.

Some of the major players in the AdTech market include Adobe Inc., Amazon.com Inc., Criteo, Google LLC (Alphabet Inc.), Meta Platforms Inc., Microsoft Corporation, Oracle Corporation, The Trade Desk Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade