Aerogel Market Size, Share, Trends and Forecast by Type, Form, Processing, Application, and Region, 2026-2034

Global Aerogel Market Size, Share, Trends & Forecast (2026-2034)

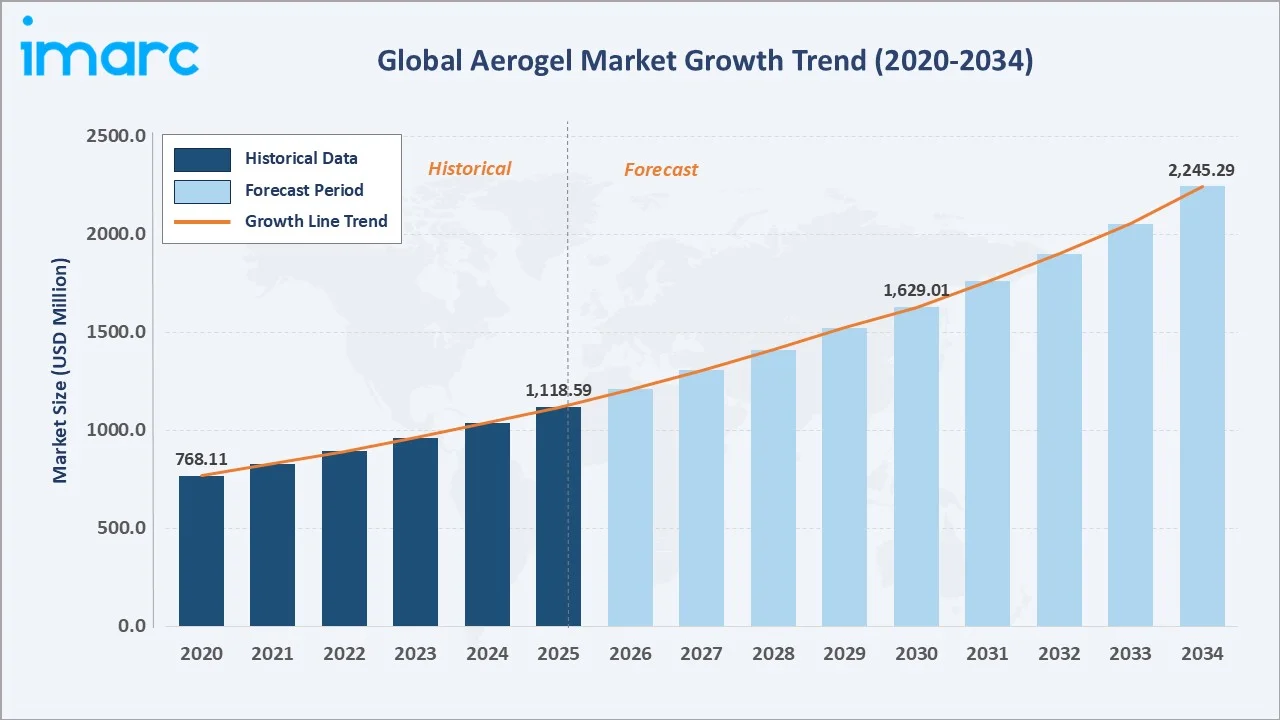

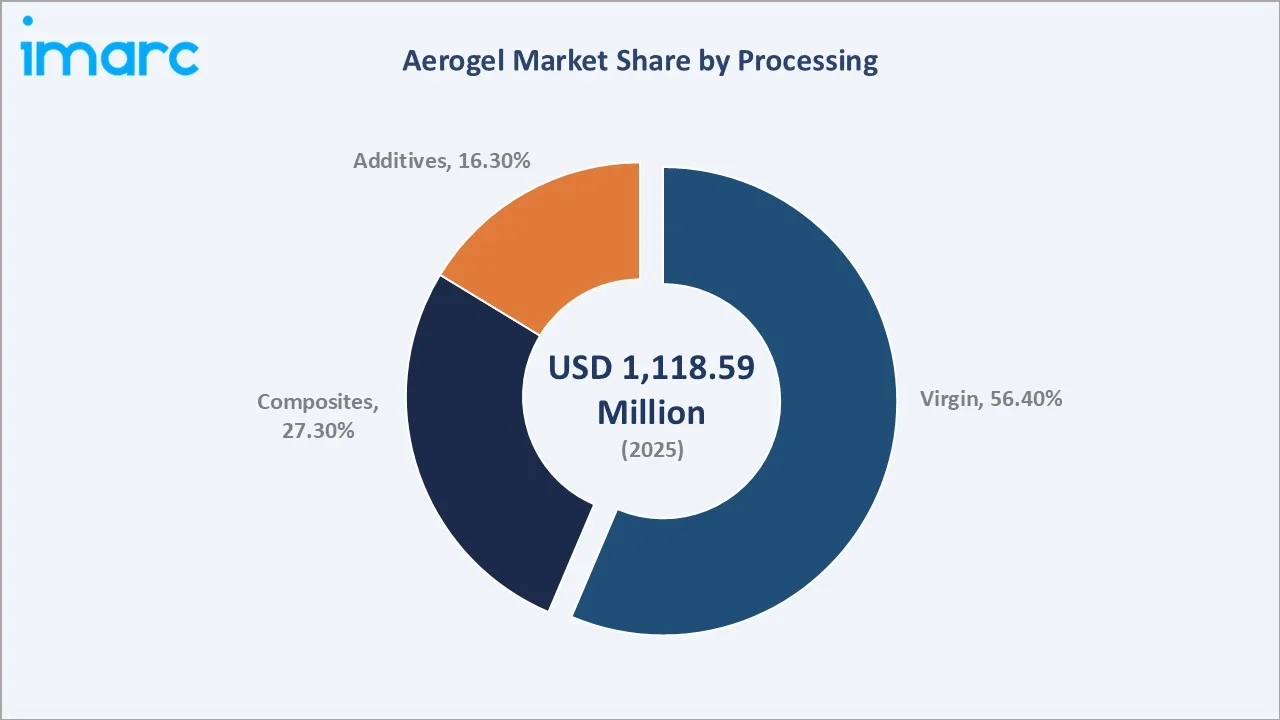

The global aerogel market size was valued at USD 1,118.6 Million in 2025 and is projected to reach USD 2,245.29 Million by 2034, exhibiting a CAGR of 7.81% during the forecast period 2026-2034. Rising global demand for high-performance thermal insulation materials, expanding oil and gas pipeline infrastructure, accelerating electric vehicle adoption - with EV-related aerogel demand growing nearly 20-fold between 2021 and 2024 - and increasingly stringent energy efficiency regulations across construction and industrial sectors are collectively propelling aerogel market growth. Blanket leads the form segment at 65.0% in 2025, while Virgin processing dominates at 56.4%. North America accounts for 44.2% of global revenue in 2025, the largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,118.6 Million |

|

Forecast Market Size (2034) |

USD 2,245.29 Million |

|

CAGR (2026-2034) |

7.81% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (44.2% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~10.25%) |

|

Leading Form |

Blanket (65.0%, 2025) |

|

Leading Processing |

Virgin (56.4%, 2025) |

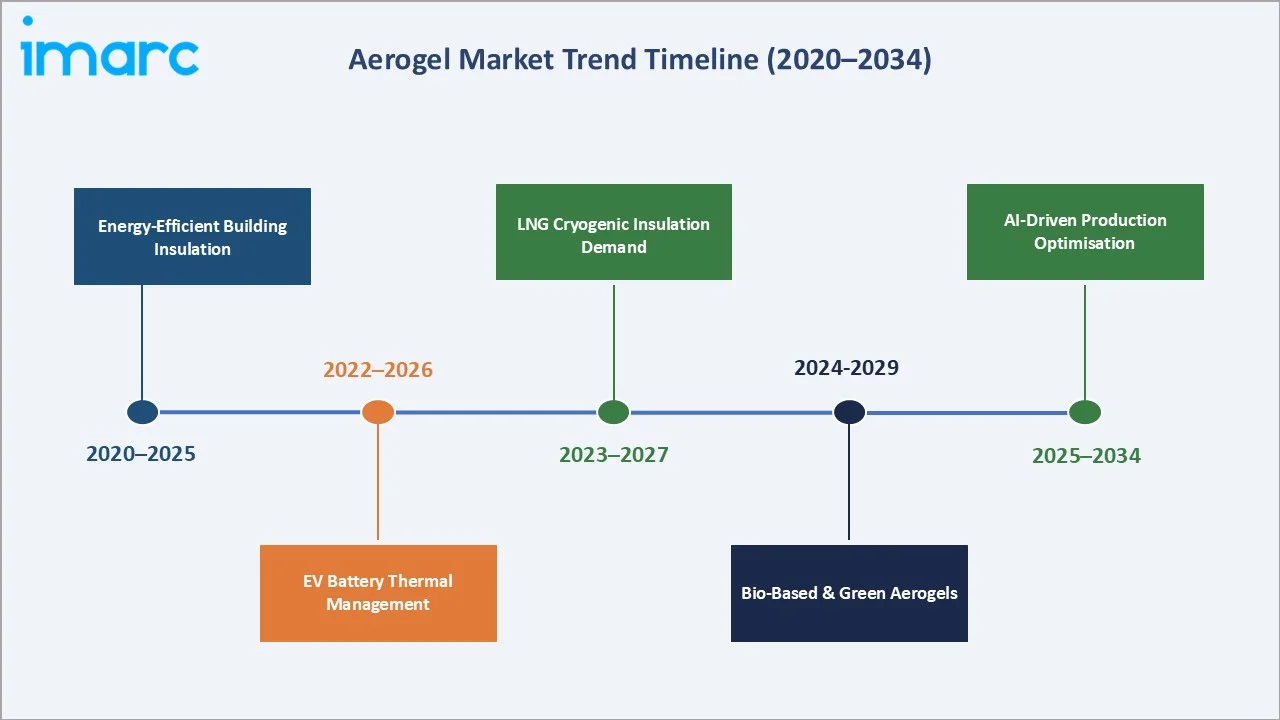

The global aerogel market growth trajectory from 2020 through 2034, contrasting consistent historical expansion against a sustained forecast curve powered by construction energy mandates, LNG infrastructure growth, and EV battery thermal management integration.

To get more information on this market, Request Sample

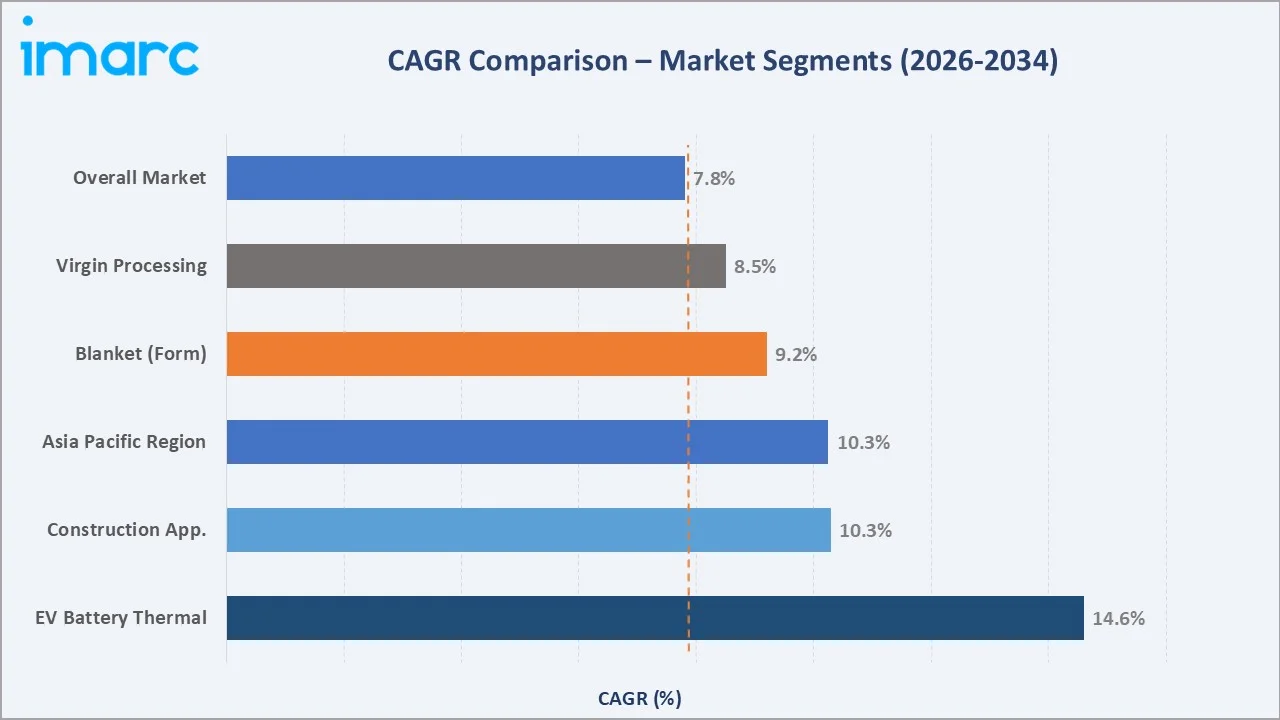

Segment-level CAGR comparisons highlighting EV battery thermal management and Asia Pacific as the two fastest-growing categories within the global aerogel industry analysis through 2034.

Executive Summary

The global aerogel market is undergoing meaningful structural expansion, driven by the convergence of energy efficiency mandates, industrial insulation upgrades, and next-generation mobility applications. Valued at USD 1,118.6 Million in 2025, the market is forecast to reach USD 2,245.29 Million by 2034 at a CAGR of 7.81%. Aerogels' exceptional thermal performance - with conductivity as low as 0.012 W/m·K - and lightweight properties are driving adoption across oil and gas, construction, and automotive sectors globally.

Blanket aerogels command 65.0% of form-factor revenue in 2025, reflecting their unmatched versatility for pipeline insulation, building retrofits, and industrial thermal management. Virgin aerogels hold 56.4% of processing-type revenue, favoured for their purity and consistent thermal performance in demanding applications. The market for aerogels in EV battery thermal protection is a high-growth niche, with over 110 distinct aerogel products now engineered specifically for electric vehicle applications globally.

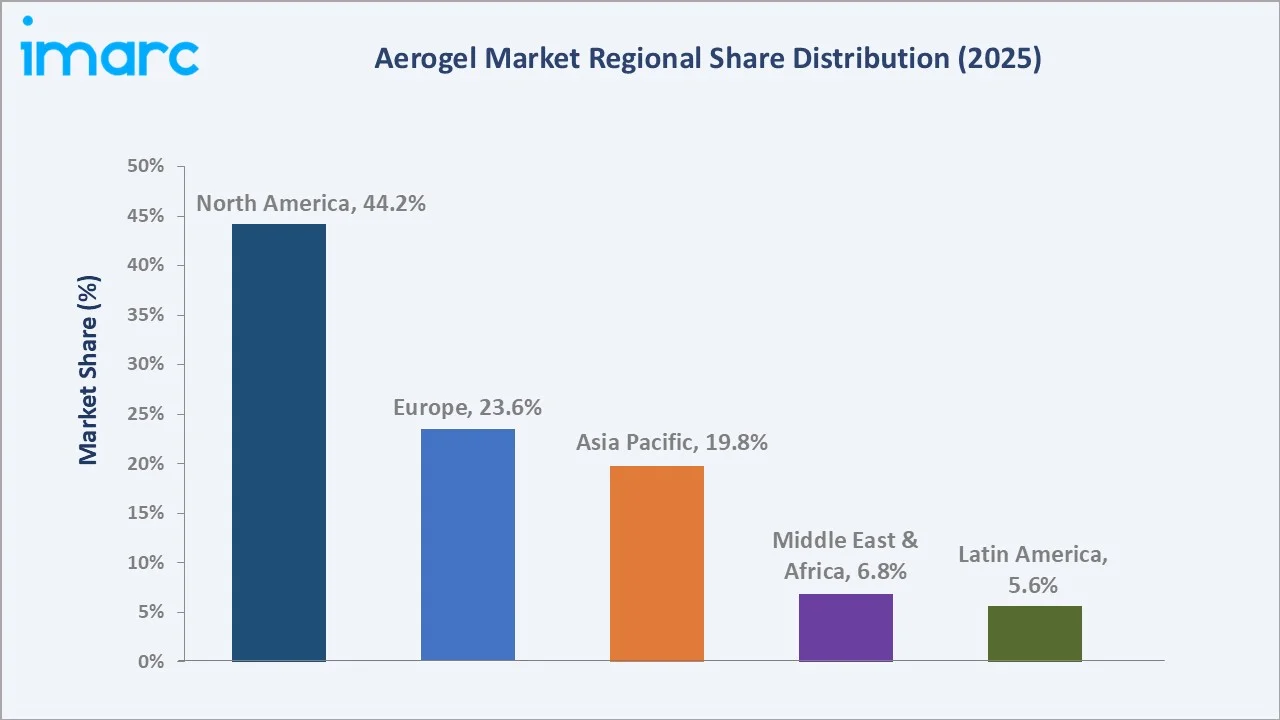

In 2025, North America leads with a 44.2% global aerogel share, supported by oil and gas activity, energy efficiency programs, and building retrofits. Europe holds 23.6%, driven by the Renovation Wave and industrial decarbonization, while Asia Pacific, at 19.8%, is the fastest-growing region due to LNG expansion, China’s EV ramp-up, and stricter energy codes. The market is led by Aspen Aerogels and Cabot Corporation, alongside regional specialists in Europe and Asia.

Key Market Insights

|

Insight |

Data |

|

Largest Form Segment |

Blanket - 65.0% share (2025) |

|

Leading Processing Type |

Virgin - 56.4% share (2025) |

|

Leading Region |

North America - 44.2% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific - CAGR ~10.25% (2026-2034) |

|

Top Companies |

Aspen Aerogels, Cabot Corporation, BASF, Armacell, Dow |

|

Key Growth Driver |

Energy Efficiency Regulations & EV Adoption |

|

Market Opportunity |

LNG Cryogenic Insulation & Green Building Retrofits |

Key Analytical Observations Supporting the Above Data:

- Blanket's 65.0% dominance in 2025 reflects the material format's unmatched combination of flexibility, ease of installation, and high thermal performance across pipeline insulation and building applications globally.

- Virgin aerogels lead at 56.4% due to their superior purity levels and homogeneous pore structures derived from supercritical drying, making them the preferred specification for oil and gas and aerospace end-uses where performance consistency is critical.

- North America's 44.2% dominance is underpinned by robust oil and gas capital expenditure, active LNG terminal expansion along the Gulf Coast, and federal policy support for advanced insulation in building and transportation sectors.

- Asia Pacific's ~10.25% CAGR reflects China's dual role as the world's largest EV market and an aggressive adopter of energy-efficient building materials, alongside rapid LNG infrastructure build-out across the region.

- EV battery thermal management is emerging as the highest-growth application niche, with aerogel demand from this segment growing nearly 20-fold between 2021 and 2024, with a further 4x growth projected through 2030.

Global Aerogel Market Overview

Aerogels are ultra-porous solid materials with air filling 80-99% of their structure, yielding the lowest thermal conductivity of any solid material known - typically 0.012 to 0.020 W/m·K. Originally developed from silica, they are now commercially produced from polymer and carbon precursors as well. Modern aerogels are manufactured via sol-gel synthesis followed by supercritical or ambient-pressure drying, yielding materials with extremely low density (as low as 1 mg/cm³) and very high surface area (500-1,000 m²/g).

Aerogel applications span oil and gas infrastructure, building insulation, LNG storage, EV battery thermal barriers, aerospace systems, and specialty coatings. Growth is supported by net-zero-driven energy efficiency mandates, LNG infrastructure expansion in the Asia Pacific and the Middle East, and rapid EV adoption.

Market Dynamics

To evaluate market opportunities, Request Sample

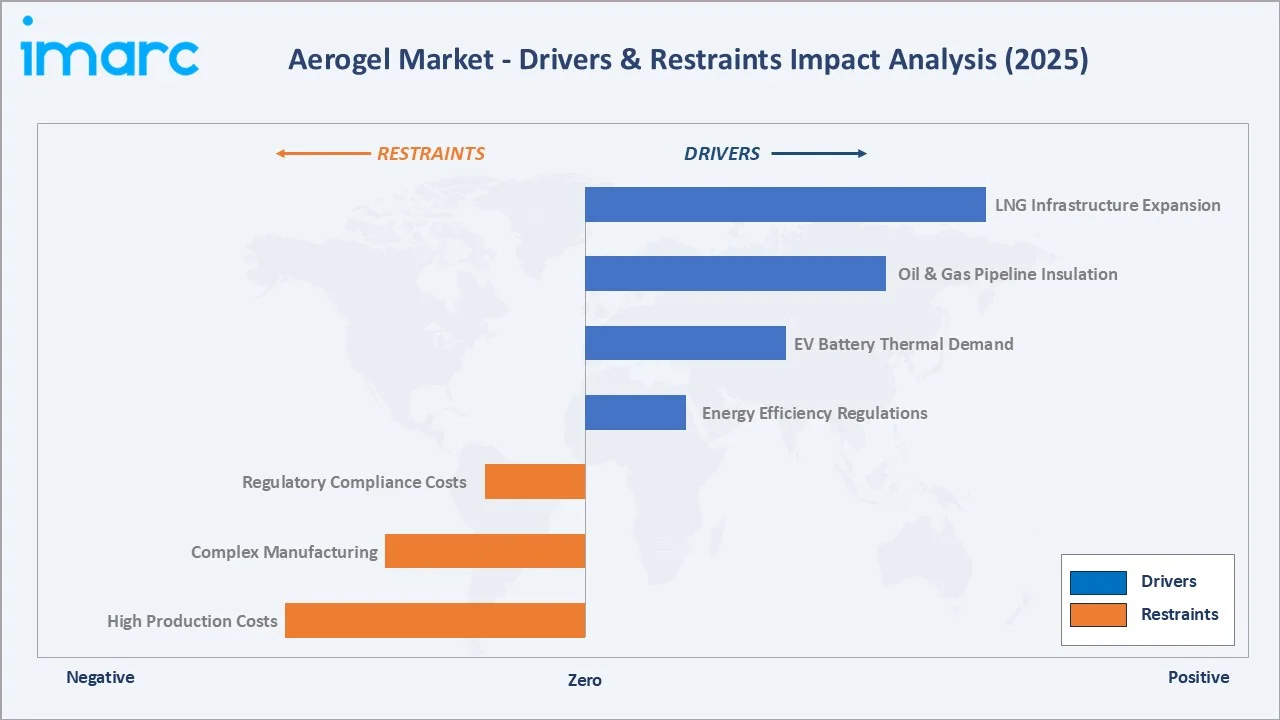

Market Drivers

- Surging EV Battery Thermal Management Demand: Aerogels are increasingly standard in lithium-ion battery packs to prevent thermal runaway. A 5mm aerogel blanket can delay thermal runaway by up to 14 minutes, exceeding automotive safety thresholds. Over 110 distinct aerogel products are engineered for EV applications, with demand growing 20x between 2021 and 2024.

- Oil & Gas Pipeline Insulation Requirements: Oil and gas represented 57% of global aerogel demand in 2024. Aerogel blankets reduce heat loss in subsea pipelines, prevent hydrate formation, and minimize corrosion-under-insulation on offshore platforms, delivering measurable operational cost savings.

Market Restraints

- High Production Costs: Aerogel manufacturing involves complex supercritical drying processes, premium silica precursors, and specialized equipment, resulting in production costs 3-10x higher than conventional insulation materials, limiting adoption in cost-sensitive construction segments.

- Mechanical Fragility of Pure Aerogels: Standard aerogels are brittle and susceptible to mechanical damage during handling and installation, requiring fibre reinforcement in blanket formats and limiting their application in mechanically demanding environments.

Market Opportunities

- Bio-Based and Sustainable Aerogel Development: Research programs are advancing cellulose nanofiber, alginate, and agricultural waste-derived aerogels that offer comparable thermal performance with lower carbon footprints. Commercial scale-up of bio-based formulations will open new procurement pathways for sustainability-focused buyers.

- Aerospace and Defence Applications: Aerogel monoliths and composites are being evaluated for thermal protection systems in satellite launches, cryogenic fuel tanks, and high-altitude aircraft, representing a structurally new, high-margin application segment.

Market Challenges

- Supply Chain Concentration: Silica aerogel production depends on narrow-specification precursors from a limited supplier base. Rapid demand expansion across construction, EV, and LNG sectors creates simultaneous demand surges that can trigger supply bottlenecks and price volatility.

- Price Competition from Conventional Insulation: Mineral wool, expanded polystyrene, and polyurethane foam remain substantially cheaper per unit area. Aerogel adoption depends on a total-cost-of-ownership value proposition that is not always apparent to end-user procurement teams unfamiliar with performance specifications.

Emerging Market Trends

1. Rising Demand for Energy-Efficient Building Insulation

Global net-zero building targets and tightening energy codes are positioning aerogels as a go-to premium insulation solution. Thin-profile aerogel blankets and plasters enable passive house compliance and deep retrofits without sacrificing usable floor area, a critical advantage in space-constrained urban markets. Europe's Renovation Wave strategy alone is expected to drive sustained aerogel procurement for building applications through 2030.

2. Accelerating Integration in EV Battery Thermal Barriers

Electric vehicle manufacturers are rapidly standardising aerogel-based thermal barriers in lithium-ion battery packs. With EV production share in Europe projected to nearly triple to 39% by 2030, and leading manufacturers awarding multi-year supply contracts, aerogel producers are investing aggressively in EV-grade product lines and production capacity expansion to secure this structurally durable growth driver.

3. Emergence of Bio-Based and Green Aerogel Formulations

Research groups globally are developing aerogels from cellulose nanofibers, chitosan, alginate, and agricultural byproducts. Empa researchers successfully demonstrated 3D-printable cellulose-based aerogels in 2024, combining biodegradability with ultra-light insulation performance. These formulations are expected to access sustainability-driven procurement channels in Europe and North America within the forecast period.

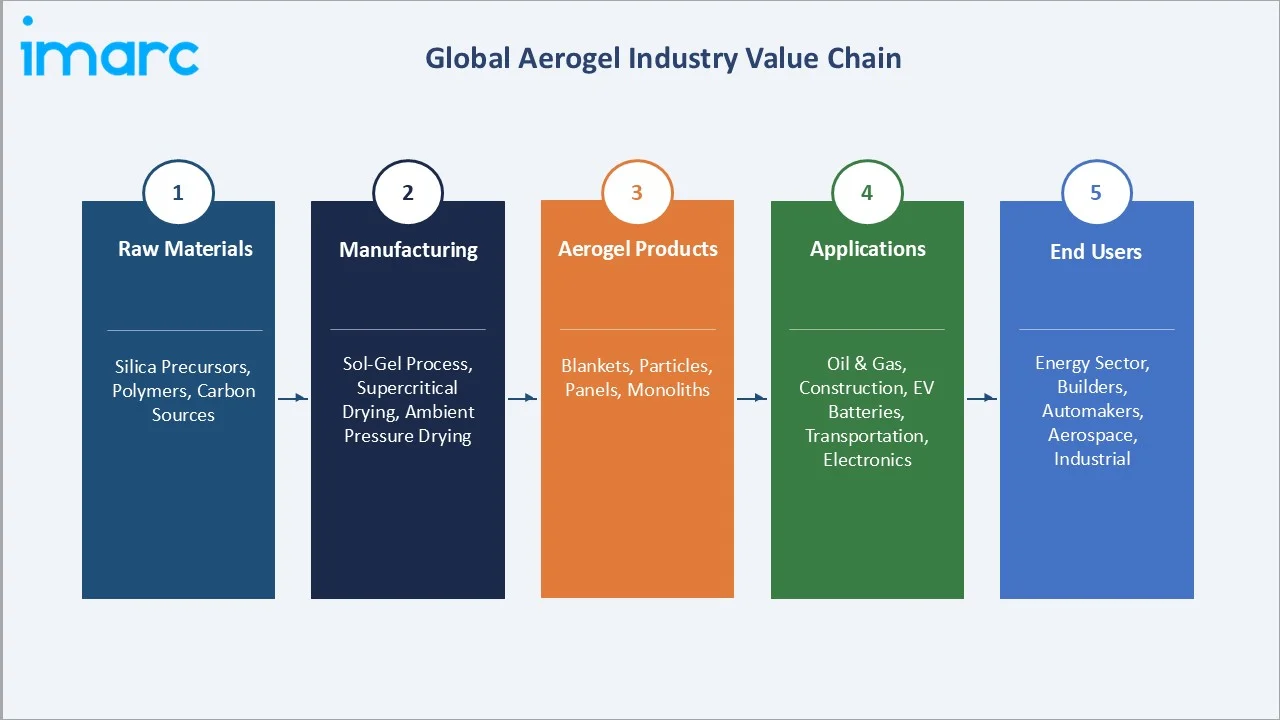

Industry Value Chain Analysis

The aerogel value chain spans five integrated stages from raw material supply through end-user application. Each stage presents distinct margin profiles, technology investment requirements, and competitive dynamics.

|

Stage |

Key Players / Examples |

|

Raw Materials & Precursors |

Silica precursor suppliers, TEOS producers, polymer resin manufacturers, carbon fibre suppliers, specialty chemical companies |

|

Aerogel Manufacturing |

Aspen Aerogels, Cabot Corporation, BASF SE, Armacell, Nano Technology Co., Guangdong Alison Hi-Tech, JIOS Aerogel |

|

Product Formulation & Processing |

Blanket compositors, panel fabricators, particle processors, additive formulators, coating specialists |

|

Distribution Channels |

Industrial distributors, direct OEM supply, construction material wholesalers, specialty insulation contractors, and online industrial platforms |

|

End-Use Industries |

Oil & gas operators, construction companies, EV and automotive OEMs, aerospace & defence contractors, industrial process plants |

Aerogel manufacturers occupy the highest strategic value position in this chain, holding proprietary process knowledge in sol-gel chemistry and drying technology. However, vertical integration by large industrial groups and backward integration by end-user majors seeking supply security are creating structural shifts in the competitive balance of the value chain.

Technology Landscape in the Aerogel Industry

Manufacturing Technology: Supercritical vs. Ambient-Pressure Drying

Supercritical drying dominates aerogel production, accounting for ~74% of capacity in 2024, as it preserves nanoporous structure and maximizes surface area, with advanced systems reducing cycle times by up to 4 hours and improving consistency. Ambient-pressure drying is emerging as a cost-efficient alternative, lowering capital costs by 20–30% with some trade-off in pore uniformity.

Material Innovation: Silica, Polymer, and Carbon Aerogels

Silica aerogels account for approximately 63-65% of global market volume in 2025, favoured for ultra-low thermal conductivity, non-combustibility, and broad application compatibility. Polymer aerogels - particularly polyimide and polyurethane variants - offer superior flexibility and mechanical resilience, gaining traction in EV battery and aerospace applications. Carbon aerogels, including graphene-oxide formulations, now combine insulation with load-bearing capability for high-temperature industrial furnace applications above 1,000°C. New silica aerogels, achieving 95% porosity at 75 kg/m³ density, enable multiple service cycles without thermal performance degradation.

EV Battery Integration Technology

Aerogel thermal barriers for lithium-ion batteries are engineered to meet thermal runaway standards requiring at least a 5-minute delay in fire propagation; a 5 mm aerogel blanket achieved a 14-minute delay in 2024 testing, significantly exceeding this threshold, with integration via bonded sheets, aerogel-infused separators, and particle-filled composite spacers for module-level protection.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Silica |

64.8% |

2025 |

|

Form |

Blanket |

65.0% |

2025 |

|

Processing |

Virgin |

🔒 |

2025 |

|

Application |

Oil and Gas |

61.0% |

2025 |

|

Region |

North America |

44.2% |

2025 |

By Form

To access detailed market analysis, Request Sample

Blanket commands a 65.0% majority share in 2025, reflecting its dominance as the most versatile and widely deployed aerogel product format. Blanket aerogels - flexible sheets with aerogel particles embedded in fibrous mats - can be managed, cut, and installed across complex geometries, including pipes, tanks, and irregular surfaces. Their lightweight nature reduces structural load in offshore and aerospace applications. Blanket aerogels captured 65.4% of global market revenue in 2024, and this leadership position is expected to be maintained through 2034. Integration with reinforced fibre composites has improved durability, fire ratings, and service life, broadening addressable applications.

By Processing

Virgin processing dominates at 56.4% in 2025, representing aerogels produced directly from primary precursor materials via supercritical drying. These materials deliver the highest purity, most consistent thermal performance, and the widest range of application suitability. Supercritical drying accounted for approximately 74% of processing technology share in 2024, underscoring strong end-user preference for this route in demanding industrial, oil and gas, and aerospace applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

44.2% |

Oil & gas pipeline insulation, LNG Gulf Coast expansion, federal energy efficiency incentives, building retrofit programs |

|

Europe |

23.6% |

EU Renovation Wave, EPBD mandates, EV production ramp-up, Germany/Italy/UK deep retrofit programs |

|

Asia Pacific |

19.8% |

China LNG infrastructure, EV production scale-up, India industrial growth, ASEAN building codes tightening |

|

Middle East & Africa |

6.8% |

GCC industrial expansion, Saudi Vision 2030, extreme-climate insulation demand, LNG export infrastructure |

|

Latin America |

5.6% |

Brazil's deepwater pre-salt offshore, Argentina's Vaca Muerta shale, and growing construction efficiency awareness. |

North America commands a 44.2% global revenue share in 2025, the most dominant regional position in the aerogel market. The United States is the primary demand driver, combining strong oil and gas capital expenditure, active LNG terminal expansion along the Gulf Coast, and a well-established building energy retrofit ecosystem. Federal-level investment programs, including USD 50 million DOE awards to localize battery-grade thermal management materials, affirm policy-driven aerogel market support. Strict ASHRAE 90.1 building energy standards and state-level retrofit incentives further underpin robust domestic demand across commercial, industrial, and residential end-uses. Asia Pacific holds 19.8% of the global market in 2025 and is positioned as the fastest-growing regional market at approximately 10.25% CAGR through 2030. China drives regional aerogel demand with the world’s largest EV production, major LNG infrastructure investment, and government-backed energy efficiency programs.

Competitive Landscape

|

Company Name |

Key Product/Brand |

Market Position |

Core Strength |

|

Aspen Aerogels, Inc. |

Pyrogel / Cryogel |

Leader |

EV thermal barriers, oil & gas blankets, OTA supply agreements |

|

Cabot Corporation |

Enova Aerogel |

Leader |

Aerogel particles/additives, coatings & composites integration |

|

BASF SE |

Slentex |

Challenger |

Polymer aerogel composites, construction & HVAC applications |

|

Armacell International |

ArmaGel |

Challenger |

Industrial insulation, LNG applications, APAC expansion |

|

Nano Technology Co., Ltd. |

NT Aerogel Blanket |

Challenger |

Silica aerogel scale-up, energy buildings & transportation |

|

Aerogel Technologies, LLC |

Airloy / Airglass |

Challenger |

Polymer aerogel mechanical strength, aerospace & defense |

|

JIOS Aerogel Corporation |

JIOS AeroVa |

Emerging |

Cryogenic aerogel systems, LNG & cold-chain applications |

|

Guangdong Alison Hi-Tech |

Alison Aerogel |

Emerging |

Cost-competitive silica aerogel, APAC construction markets |

The global aerogel market shows moderate-to-high concentration, led by Aspen Aerogels and Cabot Corporation, alongside a growing base of regional and innovation-focused players. Competition is driven by manufacturing efficiency, product range, and long-term supply agreements with EV OEMs and EPC contractors, while Chinese producers are rapidly scaling with integrated supply chains and cost advantages to compete in construction and industrial segments.

Key Company Profiles

Aspen Aerogels, Inc.

Aspen Aerogels is the global leader in aerogel technology and one of the world's largest aerogel blanket manufacturers, with a focused portfolio spanning oil and gas, construction, and electric vehicle battery thermal management.

- Product Portfolio: Pyrogel (high-temperature industrial insulation), Cryogel (cryogenic pipeline insulation), PyroThin (EV battery thermal barrier), Spaceloft (building insulation).

- Recent Developments: In February 2026, Aspen Aerogels announced its European expansion strategy following its Volvo Cars program award, projecting a USD 220 million revenue opportunity in 2027 from awarded and quoted European EV programs, potentially growing to over USD 450 million in 2028, positioning Europe as a central pillar of the company's long-term growth platform.

- Strategic Focus: Aspen Aerogels is investing in European EV supply partnerships, BESS aerogel applications, and fixed cost reduction, targeting adjusted EBITDA breakeven at USD 175 million revenue by 2027.

Cabot Corporation

Cabot Corporation is a global specialty chemicals and performance materials company with a well-established aerogel business focused on particles and additives used in coatings, building materials, and industrial applications.

- Product Portfolio: Enova aerogel particles and pellets, used as thermal and acoustic performance additives in plasters, coatings, composite insulation panels, and specialty polymers.

- Recent Developments: In September 2024, Cabot received a USD 50 million Department of Energy award in 2024 to localize battery-grade conductive additive materials with direct aerogel thermal management application synergies, reinforcing its role in the US advanced materials policy ecosystem.

- Strategic Focus: Cabot Corporation is expanding aerogel particle distribution in construction coatings and industrial composites, using its global network to grow beyond core OEM customers.

Armacell International S.A.

Armacell is a global leader in flexible insulation foams and advanced aerogel insulation systems, serving industrial, LNG cryogenic, and construction markets with a growing Asia Pacific manufacturing presence.

- Product Portfolio: ArmaGel, a versatile family of aerogel insulation products, delivers outstanding performance across various parameters, including superior thermal insulation, non-combustibility, fire protection and space-efficiency.

- Recent Developments: In April 2024, Armacell opened a new aerogel insulation manufacturing plant in India and launched its next-generation aerogel product line, targeting rising demand for high-performance thermal insulation across Asia Pacific industrial and construction markets.

- Strategic Focus: Armacell is focusing on LNG cryogenic insulation, premium building insulation, and expanding Asia Pacific manufacturing to cut logistics costs and improve supply responsiveness.

Market Concentration Analysis

The global aerogel market is moderately concentrated, with Aspen Aerogels and Cabot Corporation together accounting for about 35% of global revenue in 2025, while the top five players hold roughly 55–65%, reflecting high capital intensity, complex supercritical drying processes, and strong IP barriers.

The market is structurally bifurcated, with consolidation in high-performance industrial and EV applications driven by long-term supply agreements and quality requirements, while construction and coatings segments are becoming increasingly fragmented as regional producers in Asia scale cost-efficient ambient-pressure technologies.

Fragmentation risk is most pronounced in the Asia Pacific construction, where aggressive pricing by Chinese producers is intensifying competition, prompting Western leaders to defend premium positioning through performance differentiation, certifications, and long-term technical partnerships.

Investment & Growth Opportunities

Fastest-Growing Segments

EV battery thermal management is the fastest-growing aerogel application, with ~14.6% CAGR through 2034; demand surged nearly 20x between 2021 and 2024 and is expected to grow another 4x by 2030, driven by accelerating EV adoption in Europe and the Asia Pacific. Meanwhile, construction energy retrofits represent the largest volume opportunity, supported by long-term policy programs such as Europe’s Renovation Wave and North American retrofit tax incentives.

Emerging Market Expansion

India and Southeast Asia are high-potential underserved markets, driven by manufacturing growth, LNG infrastructure, and stricter energy codes. The Middle East, particularly Saudi Arabia, the UAE, and Qatar, offers strong demand from oil, gas, and LNG projects backed by Vision 2030 investments. Meanwhile, bio-based aerogels are an emerging segment, expected to scale commercially and tap sustainability-driven demand in Europe and North America.

Venture & Private Investment Trends

Private and corporate investment in aerogel capacity and innovation is accelerating, highlighted by Armacell’s India plant expansion in 2024, Aspen Aerogels’ targeted USD 70 million net cash strategy for 2026, and aggressive capacity additions by Chinese producers backed by state industrial policy. At the same time, global research funding is advancing bio-based aerogels and AI-driven manufacturing, supported by programs such as the National Science Foundation, Horizon Europe, and China’s national science initiatives.

Future Market Outlook (2026-2034)

The global aerogel market forecast projects steady value expansion from USD 1,118.6 Million in 2025 to USD 2,245.29 Million by 2034 at a CAGR of 7.81%, a doubling of market value underpinned by sustained end-user demand across oil and gas, construction, and EV sectors, combined with progressive cost reduction through manufacturing innovation.

Three forces will reshape the aerogel market through 2034: EV battery thermal management will become a mass-market application as OEMs standardise aerogel barriers from 2026–2028; advances in ambient-pressure drying and AI-driven optimisation will cut production costs by ~25%, improving competitiveness in construction and industrial insulation; and bio-based aerogels will unlock sustainability-driven demand in Europe and North America.

By 2034, aerogels are expected to transition from a niche specialty material to a mainstream insulation solution across construction, transport, and energy, with competition defined by global EV-integrated leaders, cost-competitive regional players, and innovation-focused bio-based and high-performance specialists.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with aerogel industry stakeholders, including product and R&D directors at aerogel manufacturers, procurement managers at oil and gas operators and EV manufacturers, construction materials specifiers, LNG facility project engineers, and institutional investors in advanced materials companies. Primary insights validated market sizing estimates, segment share allocations, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include IEA Global EV Outlook 2024, company annual reports (Aspen Aerogels, Cabot Corporation, Armacell), U.S. Department of Energy advanced materials program documentation, EU Renovation Wave implementation reports, NSF aerogel insulation research publications, and trade publications including Insulation Outlook, AZoBuild, and Chemical Week.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, construction activity indices, EV production volume forecasts, energy efficiency regulatory timelines, and historical aerogel market evolution patterns. Scenario analysis incorporating base, optimistic, and conservative growth cases was performed to account for macroeconomic uncertainty and technology adoption timing variability.

Aerogel Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Silica, Polymer, Carbon, Others |

| Forms Covered | Blanket, Particle, Panel, Monolith |

| Processing Covered | Virgin, Composites, Additives |

| Applications Covered | Oil and Gas, Construction, Transportation, Electronics, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Aspen Aerogels, Inc., Cabot Corporation, BASF SE, Armacell International, Nano Technology Co., Ltd., Aerogel Technologies, LLC, JIOS Aerogel Corporation, Guangdong Alison Hi-Tech |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the aerogel market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global aerogel market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the aerogel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Aerogel Market Report

The global aerogel market was valued at USD 1,118.6 Million in 2025, driven by sustained demand from oil and gas, construction, and emerging EV battery thermal management applications globally.

The market is projected to reach USD 2,245.29 Million by 2034, growing at a CAGR of 7.81% during 2026-2034, driven by energy efficiency mandates, EV adoption, and LNG infrastructure expansion.

Blanket aerogels lead with 65.0% revenue share in 2025, driven by their versatility for pipeline insulation, building envelope retrofits, and EV battery integration across diverse industries globally.

Virgin aerogels dominate at 56.4% share in 2025, favoured for their superior purity, homogeneous nanopore structure, and consistent thermal performance in oil and gas and aerospace applications.

North America leads with a 44.2% revenue share in 2025, backed by its oil and gas sector, LNG terminal expansion, building retrofit programs, and federal energy efficiency investment incentives.

Key drivers include tightening building energy codes (EU Renovation Wave, ASHRAE 90.1), EV battery thermal barrier demand (20x growth 2021-2024), oil and gas pipeline insulation, and LNG cryogenic system requirements.

Asia Pacific is the fastest-growing region at approximately 10.25% CAGR through 2030, driven by China's LNG investment, EV production expansion, and India's growing industrial insulation demand.

Leading companies include Aspen Aerogels, Cabot Corporation, BASF SE, Armacell International, Nano Technology Co. Ltd., Aerogel Technologies LLC, JIOS Aerogel Corporation, and Guangdong Alison Hi-Tech.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)