Africa Mobile Money Market Size, Share, Trends and Forecast by Technology, Business Model, Transaction Type, and Country 2026-2034

Africa Mobile Money Market Size, Share, Trends & Forecast (2026-2034)

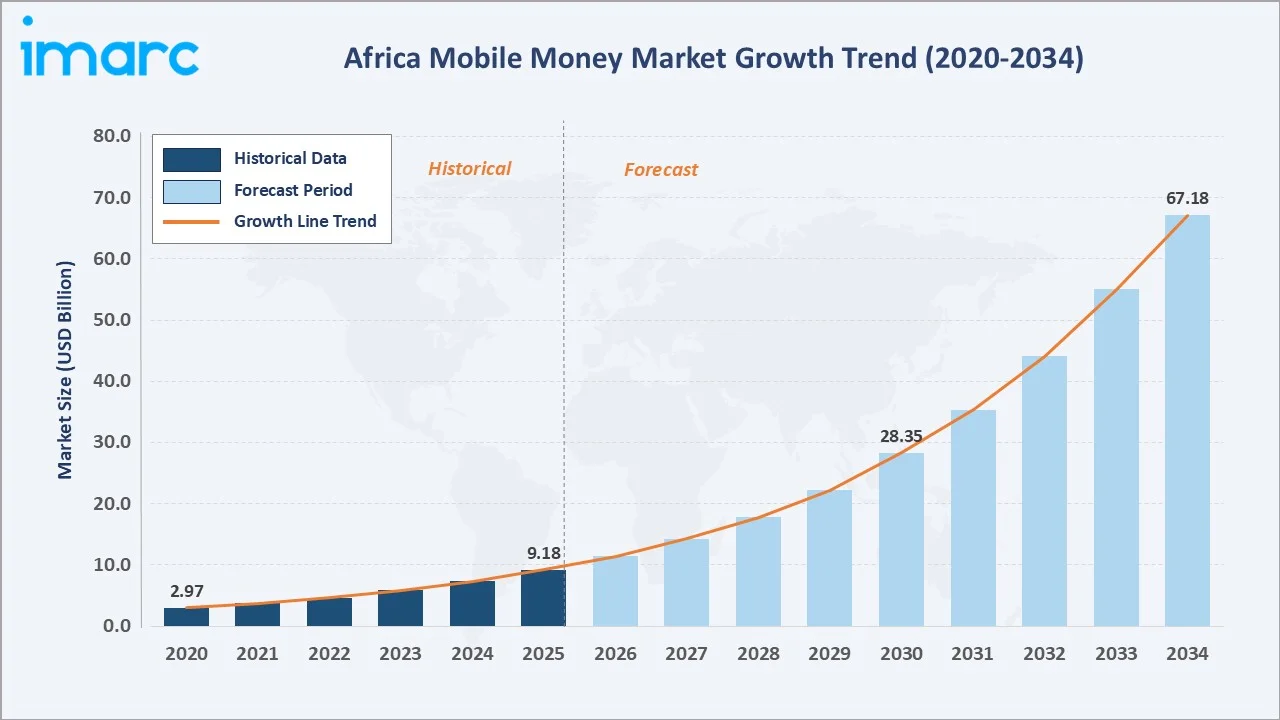

Africa mobile money market reached USD 9.18 Billion in 2025 and is projected to reach USD 67.18 Billion by 2034, growing at a CAGR of 25.30% during 2026-2034. Surging financial inclusion initiatives, rapid smartphone adoption, expanding agent networks, and increasing government digitization programs are the primary catalysts propelling Africa's mobile money market growth across Sub-Saharan and East African economies.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.18 Billion |

|

Forecast Market Size (2034) |

USD 67.18 Billion |

|

CAGR (2026-2034) |

25.30% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Country |

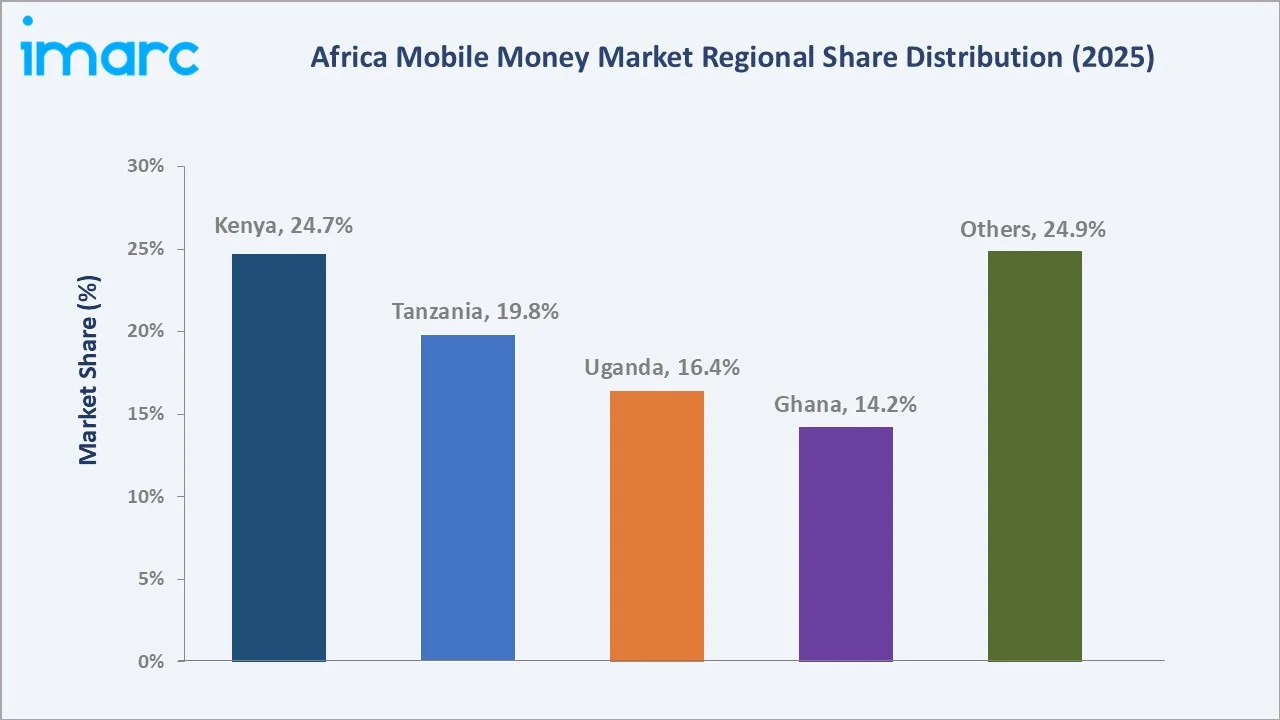

Kenya (24.7% share, 2025) |

|

Fastest Growing Country |

Ghana |

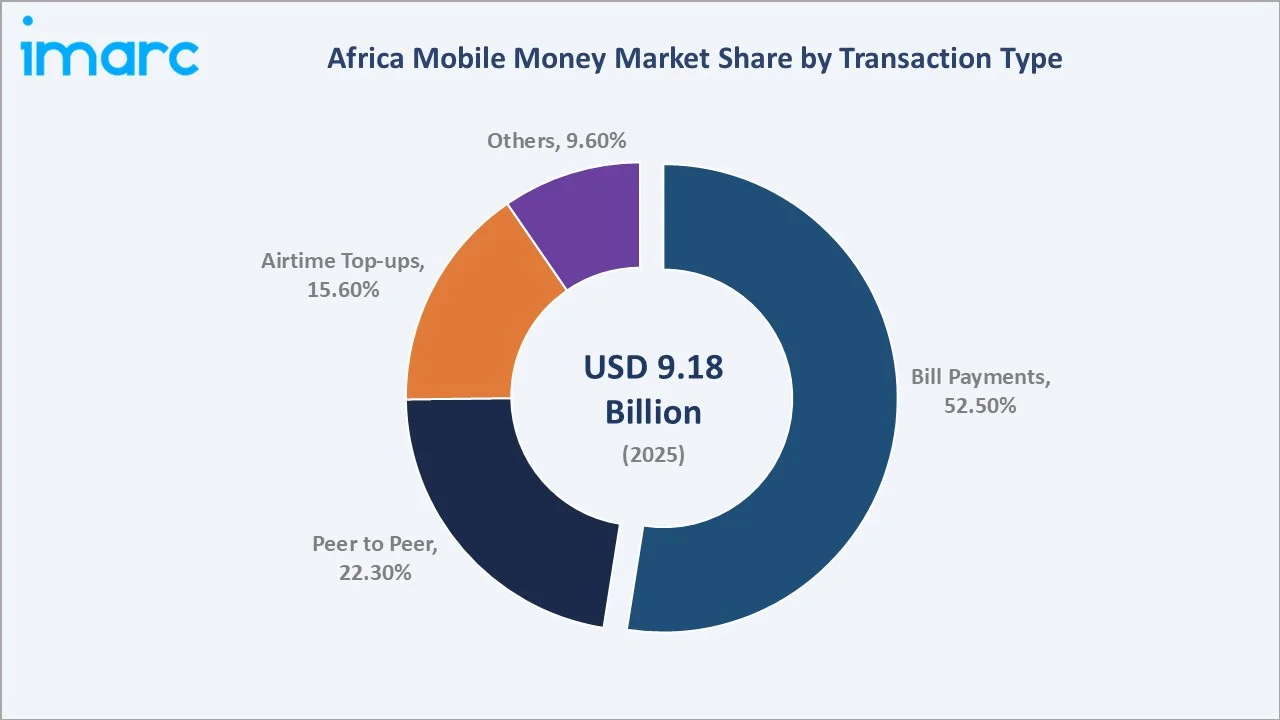

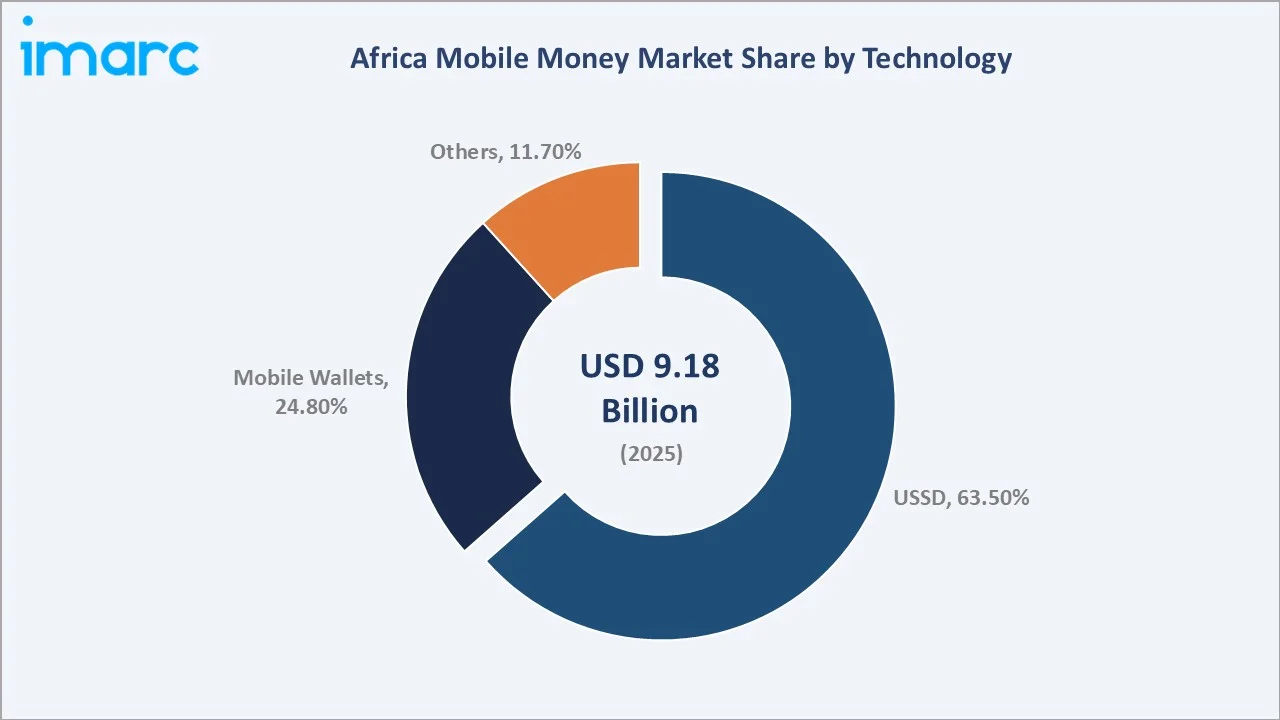

Kenya dominates, holding a 24.7% country share in 2025, while USSD technology leads transaction volume at 63.5% of total transactions. Bill payments represent the largest transaction type at 52.5%. Africa's mobile money ecosystem benefits from its large unbanked population, dense agent infrastructure, and accelerating policy support from regional central banks and telecom regulators.

To get more information on this market, Request Sample

With transaction demand spanning peer-to-peer transfers, bill payments, airtime top-ups, and emerging merchant payments, the Africa mobile money market outlook remains robust through the forecast period. According to the GSMA’s 2024 State of the Industry Report on Mobile Money, mobile money services in West Africa experienced growth of doubling over the past decade, underscoring the continent's central role in digital financial services.

Executive Summary

Africa mobile money market is experiencing an era of exceptional expansion, reaching USD 9.18 Billion in 2025 and projected to surpass USD 67.18 Billion by 2034, reflecting a CAGR of 25.30%. This trajectory is underpinned by surging financial inclusion mandates, the proliferation of agent banking networks, and the accelerating digitization of government-to-person (G2P) payments across Sub-Saharan Africa.

Kenya leads with a 24.7% country share in 2025, anchored by Safaricom mobile money platform M-Pesa's unrivaled ecosystem penetration, with over 34 million active users. Tanzania (19.8%) and Uganda (16.4%) follow, buoyed by multi-operator competition, regulatory interoperability mandates, and robust rural agent networks. Ghana (14.2%) has emerged as a regulatory benchmark, achieving a 95.06 points on the GSMA Mobile Money Regulatory Index in 2024.

USSD technology dominates at 63.5% due to its universal compatibility with basic handsets, critical in markets where 2G/3G infrastructure remains the primary connectivity layer. Mobile wallets at 24.8% represent the fastest-growing technology segment, driven by declining smartphone prices and expanding 4G/5G coverage. Bill payments lead transaction types at 52.5%, reflecting the growing digitization of utility, government, and household service payments across the continent.

Key Market Insights

|

Insight |

Data |

|

Largest Transaction Type |

Bill Payments – 52.5% share (2025) |

|

Dominant Technology |

USSD – 63.5% share (2025) |

|

Leading Country |

Kenya – 24.7% revenue share (2025) |

|

Fastest Growing Country |

Ghana (regulatory leadership + interoperability) |

|

Top Companies |

MTN Group Management Services (Pty) Ltd, Safaricom/Vodacom, Airtel Africa, Orange |

|

Market Opportunity |

Cross-border AfCFTA payments and AI-powered credit scoring platforms projected for above-average growth through 2034 |

Key Analytical Observations Supporting The Above Data:

- Bill Payments dominate transaction type at 52.5% (2025), driven by the rapid digitization of utility, tax, and government service payments. Mobile money is the leading payment method in Ghana, with more active users than traditional bank accounts, and is widely used for P2P transfers, merchant transactions, and bill payments.

- USSD technology commands 63.5% of transaction volume in 2025, according to the latest research. Africa’s smartphone market expanded by 3% year-on-year in Q3 2024, reaching 18.4 million units, demonstrating resilience despite a challenging economic environment.

- Kenya accounts for 24.7% of regional mobile money value in 2025, anchored by M-Pesa's deep ecosystem integration covering savings, loans, insurance, and merchant payments for over 34 million active users.

- Mobile wallets at 24.8% are the fastest-growing technology segment, as GSMA’s October 2025 initiative, involving Airtel, MTN, Orange, and Vodacom, introduced minimum specifications for affordable 4G smartphones to accelerate app-based wallet adoption.

Africa Mobile Money Market Overview

Africa's mobile money market encompasses a broad spectrum of digital financial services delivered through mobile telecommunications infrastructure, including peer-to-peer transfers, bill payments, airtime top-ups, merchant payments, savings, micro-credit, and cross-border remittances. The market ecosystem spans telecom operators, fintech platforms, agent banking networks, regulatory bodies, and an expanding base of third-party service integrators.

Macroeconomic factors, including high unbanked population density, expanding mobile network coverage, and supportive central bank policies in Kenya, Ghana, and Tanzania, are primary growth catalysts. Africa hosts approximately 755 registered mobile money agents per 100,000 adults in active markets, underscoring the agent network as the foundational distribution infrastructure of this market.

Market Dynamics

To evaluate market opportunities, Request Sample

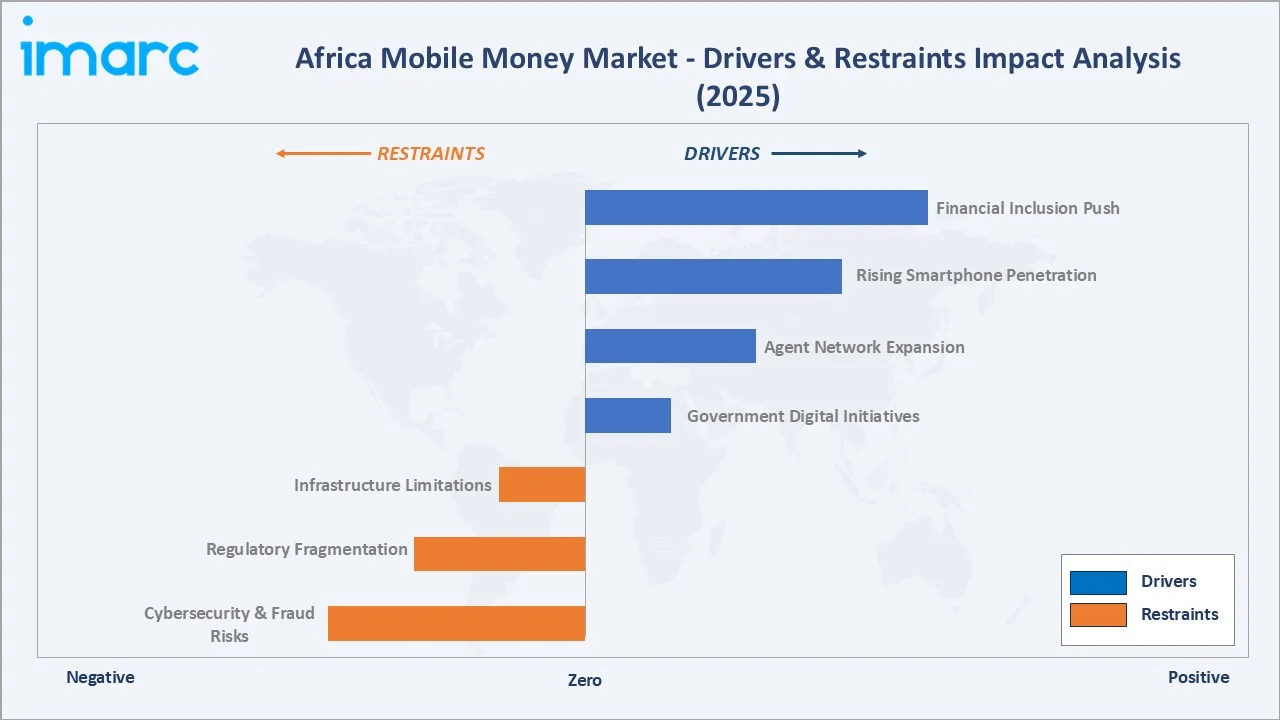

Market Drivers

- Financial Inclusion Push Across Sub-Saharan Africa: Approximately 45% of Sub-Saharan African adults remain unbanked, per World Bank data, representing a vast addressable market for mobile money services.

- Rising Smartphone Penetration and 4G Expansion: In 2025, the average cost of 1GB of data in South Africa was USD 1.29 (R20.50), with 27 African countries offering lower prices for the same data volume, enabling greater app-based wallet adoption.

- Agent Network Expansion and Rural Reach: Airtel Africa reported that its total customer base reached 179.4 million, with 81.8 million users subscribed to data services across the continent. It is reinforcing last-mile cash-in/cash-out access in underserved rural communities.

- Government Digital Transformation Initiatives: Nearly 100% of all government-to-person (G2P) and government-to-government (G2G) payments are conducted digitally. Similar initiatives in Uganda and Zambia, where Airtel Money facilitates social welfare fund disbursements, are creating high-frequency, high-trust use cases that anchor platform stickiness.

These drivers reinforce a self-sustaining adoption cycle: agent network density increases cash-in/cash-out accessibility, which lowers the friction of initial registration; growing registered user bases attract merchant and government partners; expanded service ecosystems increase platform utility and retention across all user segments.

Market Restraints

- Infrastructure Limitations in Remote Areas: Despite strong agent network growth, physical infrastructure constraints, including inconsistent mobile network coverage in rural areas and limited electricity access for agent device charging, continue to limit last-mile transaction reliability, particularly in low-density agricultural regions.

- Regulatory Fragmentation Across 54 Countries: The absence of a unified pan-African regulatory framework creates compliance complexity for operators seeking to offer cross-border services. Differing KYC requirements, capital holding rules, and interoperability mandates across national central banks elevate the operational cost of multi-market expansion.

- Cybersecurity and Fraud Risks: Mobile money fraud, including SIM swap attacks, agent fraud, and phishing schemes, remains a critical challenge. Operators are investing heavily in AI-driven fraud detection systems, but fraud incidents continue to erode user trust in undereducated consumer segments.

Market Opportunities

- Cross-Border AfCFTA Payment Facilitation: The African Continental Free Trade Area (AfCFTA) is creating structural demand for seamless digital cross-border payment solutions supporting SME trade.

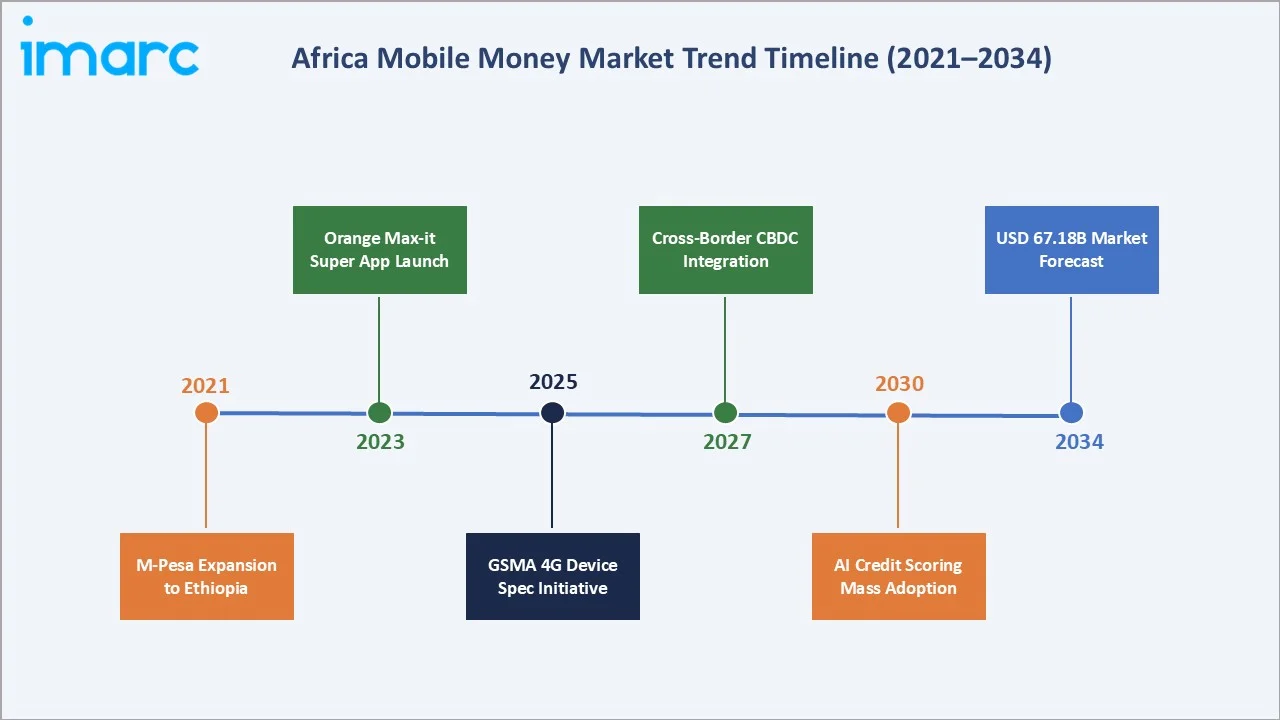

- AI-Powered Credit Scoring and Micro-Lending: In July 2025, Orange Money Group partnered with fintech firm JUMO to expand credit services across Africa by introducing AI-driven microcredit solutions aimed at improving financial inclusion among unbanked populations.

- Super-App Integration and E-Commerce Convergence: In November 2023, Orange launched its “Max it” super-app to provide a unified digital platform in Africa and the Middle East, integrating telecom services, mobile money, and e-commerce to simplify users’ daily activities.

Market Challenges

- Interoperability Barriers Between Operators: Wallet-to-wallet transfers across different mobile money operators, allowing an M-Pesa user to send directly to an MTN MoMo user, face technical, commercial, and competitive barriers that limit the network effects the ecosystem could generate from full interoperability.

- Digital and Financial Literacy Gaps: Low digital literacy in rural and older demographic segments creates friction in new user onboarding, limiting organic platform growth in communities where mobile money could have the highest financial inclusion impact.

Emerging Market Trends

1. Super-App Transformation of Mobile Money Platforms

The MTN MoMo app transforms mobile money into a comprehensive digital financial platform in Uganda, enabling users to manage payments, access credit, and use a wide range of financial services in one place. It reflects a structural shift toward platform-based financial ecosystems that increase user engagement frequency and average revenue per user.

2. Shift from USSD to App-Based Mobile Wallets

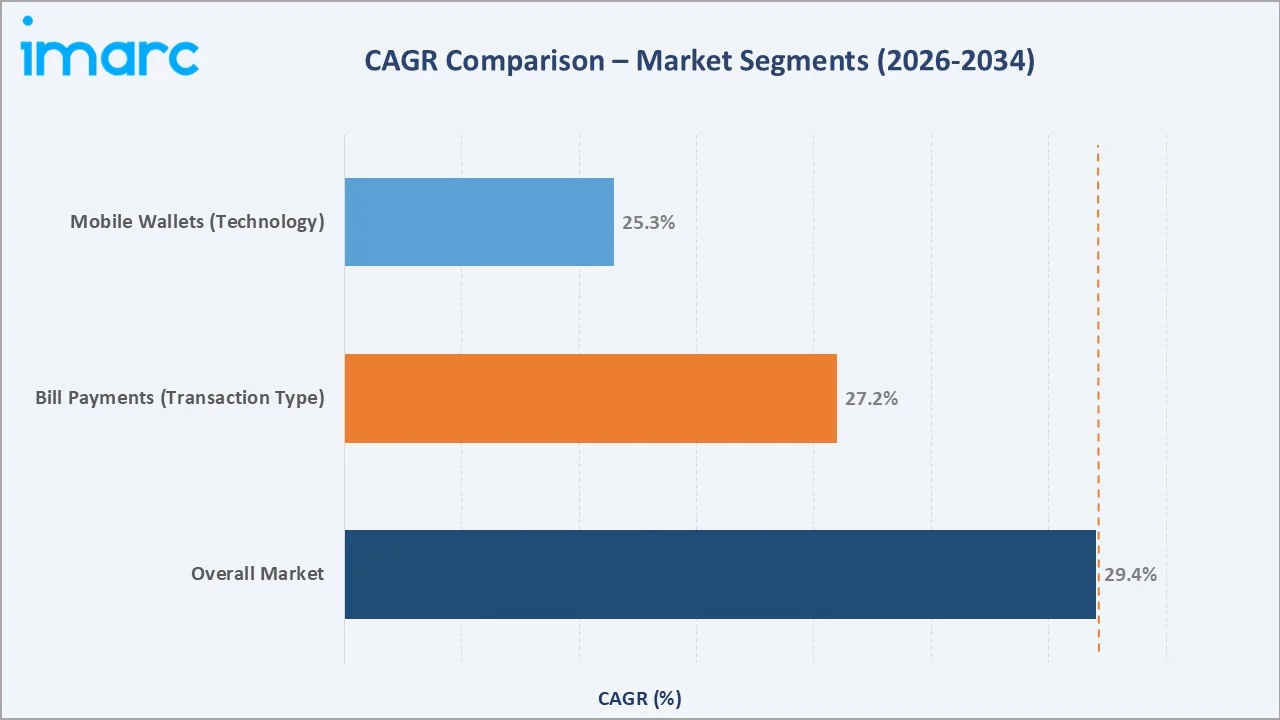

The declining cost of 4G smartphones is steadily shifting transaction volume from USSD toward app-based interfaces. While USSD remains dominant at 63.5% in 2025, Mobile Wallets are growing at an estimated CAGR of 29.4%, as enhanced smartphone interfaces unlock richer product features, including QR-based merchant payments, investment products, and biometric authentication.

3. Cross-Border Payment Integration Under AfCFTA

Mastercard and MTN partnered to enable millions of consumers across Africa to make secure global e-commerce payments using a virtual payment solution linked to MTN MoMo wallets. Onafriq (formerly MFS Africa) is building a "network of networks" connecting disparate mobile money systems across the continent to facilitate interoperable cross-border settlements.

4. AI and Machine Learning Integration in Financial Services

Optasia, listed on the JSE in November 2025, processes over 30 million loan transactions daily using AI-powered microcredit delivered through MTN and Vodacom infrastructure. MTN MoMo's fintech platform led to a 15% growth in transaction volumes to over 23 billion and pushed total transaction value beyond USD 500 billion.

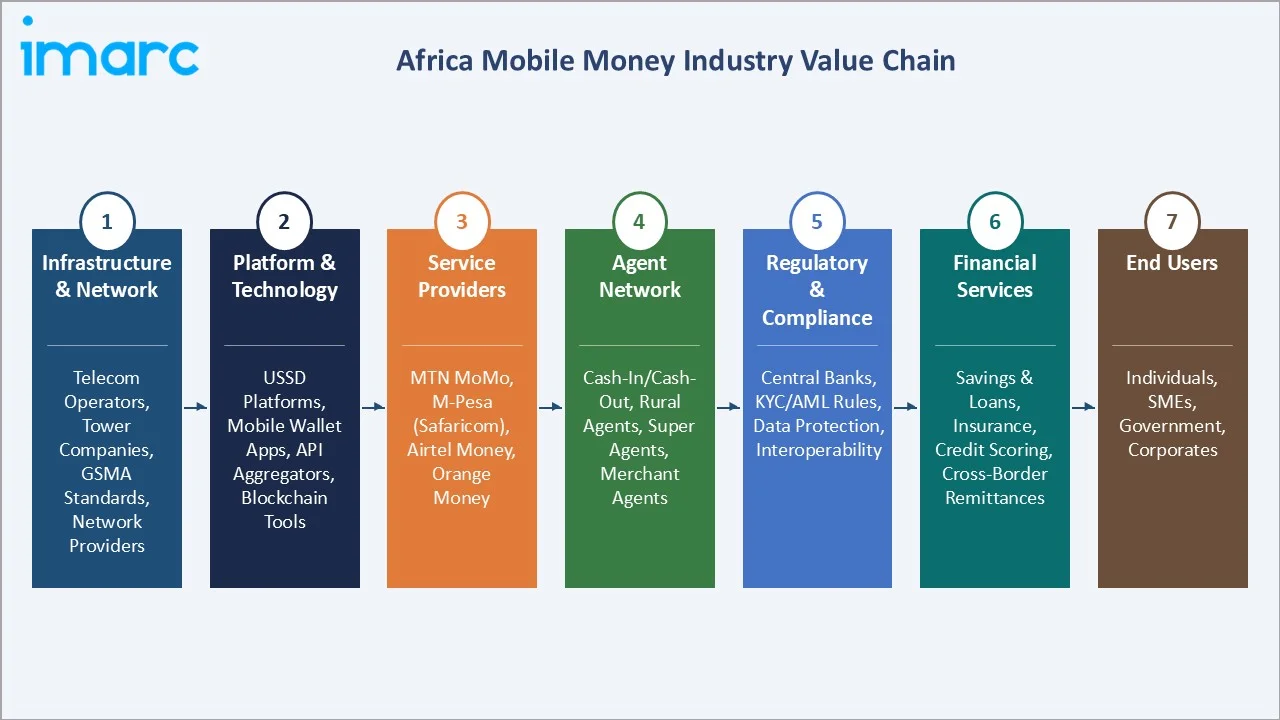

Industry Value Chain Analysis

The Africa mobile money value chain spans telecommunications infrastructure through end-user financial service delivery, with each stage populated by specialized operators whose performance directly influences service accessibility, transaction reliability, and financial inclusion outcomes.

|

Stage |

Key Participants / Examples |

|

Infrastructure & Network |

Telecom operators (MTN, Airtel, Safaricom), tower companies, and GSMA standards |

|

Platform & Technology |

USSD platforms, mobile wallet apps, API aggregators, blockchain tools |

|

Service Providers |

MTN MoMo, M-Pesa (Safaricom/Vodacom), Airtel Money, Orange Money, Mixx by Yas |

|

Agent Network |

Cash-in/cash-out agents, rural agents, super-agents, merchant agents |

|

Regulatory & Compliance |

Central banks, KYC/AML frameworks, data protection authorities, interoperability mandates |

|

Financial Services |

Savings accounts, micro-loans, insurance, credit scoring, cross-border remittances |

|

End Users |

Individuals, SMEs, government agencies, corporate entities |

Technology Landscape in Africa Mobile Money Industry

USSD Technology and Feature Phone Accessibility

USSD (Unstructured Supplementary Service Data) remains the dominant technology layer in Africa's mobile money ecosystem, commanding a 63.5% share of total transaction volume in 2025. Operating over 2G and 3G networks without requiring internet connectivity, USSD provides universal accessibility for the continent's large feature-phone user base across rural and peri-urban markets.

Mobile Wallet Applications and Smartphone-Based Platforms

Mobile wallet applications represent the fastest-growing technology segment at an estimated CAGR of 29.4%, driven by the declining cost of 4G-enabled smartphones and increasing 4G/5G network coverage across urban and suburban corridors. Smartphone-based wallets enable richer financial product delivery, including QR-based merchant payments, biometric authentication, push notifications, and integrated AI-driven credit scoring.

AI and Machine Learning in Credit Scoring and Fraud Detection

Artificial intelligence and machine learning are fundamentally reshaping the credit and risk management capabilities of Africa's mobile money platforms. With the majority of mobile money users lacking formal credit histories, AI-driven alternative data models — analyzing transaction frequency, airtime top-up patterns, and behavioral metadata — are enabling platforms to extend microcredit to previously unscored populations at scale.

Interoperability APIs and Cross-Border Payment Infrastructure

API-based interoperability frameworks are the critical technical enabler for expanding mobile money utility beyond single-operator ecosystems. Bilateral and multilateral interoperability agreements, facilitated by API gateways and clearing house infrastructure, allow users to transact across different mobile money platforms, bank accounts, and international remittance corridors, directly expanding the addressable use case set and total transaction volumes.

Blockchain and Distributed Ledger Technology in Settlements

Blockchain and distributed ledger technology (DLT) are gaining traction as settlement and transparency infrastructure within Africa's mobile money ecosystem, particularly for cross-border remittances and government disbursement programs where auditability, immutability, and real-time settlement finality are required. While USSD and API-based systems continue to dominate transaction processing, DLT is emerging as a complementary layer for settlement reconciliation and compliance.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

USSD |

63.5% |

2025 |

|

Business Model |

🔒 |

🔒 |

2025 |

|

Transaction Type |

Bill Payments |

52.5% |

2025 |

|

Country |

Kenya |

24.7% |

2025 |

By Transaction Type

Bill Payments dominate the transaction type segment with a 52.5% share in 2025 (approximately USD 4.82 Billion), reflecting the rapid digitization of utility, government, and household service payments across East and West Africa.

To access detailed market analysis, Request Sample

Peer-to-peer transfers account for 22.3%, representing the original core use case of mobile money and remaining significant for domestic remittances, family support payments, and informal economy transactions. Airtime top-ups at 15.6% continue to serve as a primary gateway transaction for new users, driving platform adoption before migration to higher-value services.

By Technology

USSD technology leads with a 63.5% share in 2025, reflecting its universal accessibility across 2G and 3G feature phones, the primary handset category across rural and low-income user segments in Sub-Saharan Africa.

Mobile Wallets hold 24.8% of the market in 2025, growing at an estimated CAGR of 29.4%, well above the overall market rate, as smartphone penetration expands and app-based interfaces enable richer financial services, including AI-powered credit scoring, investment products, and QR-based merchant payments.

Regional Market Insights

Kenya's market leadership (24.7%, 2025) reflects M-Pesa's foundational role as the world's first successful mobile money ecosystem, processing transactions equivalent to over 50% of Kenya's GDP. In May 2023, Safaricom and KCB Bank Kenya (KCB) launched Fuliza ya Biashara, where business owners can access a minimum overdraft of KSh 1,000 and draw multiple overdrafts of up to KSh 400,000, depending on their assigned limit.

|

Country |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Brands/Companies |

|

Kenya |

24.7% |

M-Pesa ecosystem depth; GDP-level transaction volumes; SME credit expansion |

CBK mobile money licensing; interoperability mandate |

M-Pesa (Safaricom), Airtel Money |

|

Tanzania |

19.8% |

Multi-operator competition; rural agent density; Vodacom & Yas presence |

TCRA interoperability rules; NPS Act |

Mixx by Yas, M-Pesa (Vodacom), Airtel Money |

|

Uganda |

16.4% |

Mobile money = 100+% of GDP in transactions; government welfare disbursements |

Bank of Uganda e-money guidelines; OTT tax revision |

MTN MoMo, Airtel Money |

|

Ghana |

14.2% |

GSMA #1 regulatory ranking (2024); Ghana.Gov integration; 80% G2P digital |

BoG mobile money interoperability; MMIP platform |

MTN MoMo, Airtel Money, Telecel Cash |

|

Others |

24.9% |

West Africa WAEMU growth; diaspora remittances; emerging francophone markets |

BCEAO regional framework; AfCFTA trade finance |

Orange Money, Wave, MTN MoMo |

Competitive Landscape

Africa mobile money market exhibits a moderately concentrated structure at the pan-African operator tier, with global telecom groups commanding significant shares of active mobile money accounts while regional fintech specialists and emerging super-app platforms compete aggressively in specific countries and demographic segments.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

MTN Group Management Services (Pty) Ltd, |

MTN MoMo |

Market Leader |

10+ African markets; 69.5 M monthly active users; USD 500B in transactions (2025) |

|

Safaricom/Vodacom |

M-Pesa |

Market Leader |

Pioneer platform; 34M+ Kenya users; deep ecosystem (savings, credit, merchant) |

|

Airtel Africa |

Airtel Money |

Strong Challenger |

14 countries; 40+M users; QR merchant payments; government integration |

|

Orange |

Orange Money |

Strong Challenger |

Francophone Africa leadership; Max it super-app; AI credit scoring (2024) |

Key Company Profiles

MTN Group Management Services (Pty) Ltd,

MTN Group, headquartered in Johannesburg, South Africa, operates the continent's largest mobile money platform, MTN MoMo, across 10+ African markets with 69.5 million monthly active users, processing USD 500 billion in transactions in 2025. MTN's collaboration with the Gates Foundation has supported agent network digitization for improved rural liquidity management.

- Product Portfolio: MTN MoMo wallet, MoMo Pay (QR merchant payments), MoMo Agent banking, MoMo Credit, MoMo Insurance.

- Recent Developments: Mastercard-MTN strategic partnership (February 2024) to introduce cross-border mobile payment solutions; integration of PayShap into MoMo in South Africa (April 2024).

- Strategic Focus: Advanced financial services expansion; AI fraud detection investment; cross-border AfCFTA payment facilitation.

Safaricom / Vodacom

M-Pesa, launched by Safaricom in Kenya in 2007 and now operated across multiple markets under the Vodacom umbrella, is the pioneering mobile money platform and benchmark for the global industry. With over 30 million active users in Kenya alone.

- Product Portfolio: M-Pesa mobile wallet, Fuliza overdraft facility, M-Shwari savings, KCB M-Pesa credit, M-Pesa Global for cross-border remittances.

- Recent Developments: Launched Fuliza Ya Biashara (business overdraft) in 2023 for SMEs; M-Pesa Ethiopia launch via Safaricom Ethiopia.

- Strategic Focus: Super-app ecosystem deepening; international remittance corridor expansion; merchant payment digitization.

Airtel Africa

Airtel Africa, headquartered in London with operations across 14 African nations, serves approximately 50 million mobile money users. The company has strategically focused on government integration and QR-based merchant payments to deepen platform engagement.

- Product Portfolio: Airtel Money wallet, Airtel Money Pay (QR payments), Airtel Money Mastercard virtual cards, agent banking network.

- Recent Developments: Mastercard partnership announced for a cross-border remittance service across all 14 African markets (August 2023); government welfare fund integration in Uganda and Zambia; GSMA 4G device specification initiative participation (2025).

- Strategic Focus: Merchant ecosystem digitization; government payment integration; 4G device accessibility partnerships.

Orange

Orange, headquartered in Paris, France, operates Orange Money across Francophone Africa and the Middle East, with a strong presence in Côte d'Ivoire, Senegal, Mali, and Cameroon. The November 2023 launch of the Max-it super-app represents Orange's strategic pivot toward comprehensive digital ecosystem services.

- Product Portfolio: Orange Money wallet, Orange Money Mastercard, Orange Bank Africa, Max-it super-app (payments, e-commerce, telecoms).

- Recent Developments: Max it super-app launch across five African/Middle Eastern markets (November 2023); AI-driven micro-loan products for unbanked users.

- Strategic Focus: Super-app ecosystem; AI-powered credit; francophone Africa leadership consolidation.

Market Concentration Analysis

Africa mobile money market exhibits high concentration at the platform operator tier, with the top four providers, MTN Group Management Services (Pty) Ltd, Safaricom/Vodacom, Airtel Africa, and Orange, collectively commanding the overwhelming majority of active mobile money users and transaction value across sub-Saharan Africa in 2025. Together, these four operators process well over USD 800 billion in combined annual transaction value, underscoring the depth of platform entrenchment.

Despite this top-tier concentration, the market retains significant fragmentation at the country and sub-segment level, particularly in West and Central Africa, where multiple overlapping operator footprints, independent fintech entrants, and bank-led mobile wallet solutions compete vigorously for the large unbanked population.

Investment & Growth Opportunities

Fastest Growing Segments

Advanced financial services layered on mobile money rails represent the three highest-growth investment vectors within the Africa mobile money market through 2034. Together, these sub-categories are growing materially faster than the overall market, driven by structural demand from Africa's 57% unbanked adult population, the rapid expansion of smartphone adoption, and government-led financial inclusion mandates across key markets, including Nigeria, Kenya, Tanzania, and Ghana.

Emerging Sub-Market Expansion

East Africa, anchored by Kenya's M-Pesa ecosystem, remains the most mature and deeply integrated mobile money sub-market, with mobile money transactions representing nearly 60% of Kenya's GDP. West Africa, led by Ghana and Nigeria, represents the highest-growth frontier given the scale of the addressable unbanked population, rapidly rising 4G penetration, and the entry of fintech challengers accelerating competitive fee compression and product innovation.

Venture and Institutional Investment Themes

- Key investment themes include AI-native credit scoring and digital lending infrastructure, cross-border payment interoperability platforms aligned with the African Continental Free Trade Area (AfCFTA) agenda, super-app ecosystem development integrating mobile money with e-commerce and insurance, and QR-based merchant payment digitization targeting Africa's large informal retail sector.

- Institutional investors and development finance institutions are targeting mobile money infrastructure plays, agent network digitization, and fintech-telco partnership vehicles that extend formal financial services to underbanked populations across Sub-Saharan Africa.

- Corporate venture and strategic investment activity is intensifying around the fintech spin-off cycle: MTN Group's structural separation of MoMo into standalone entities across Ghana, Nigeria, and Uganda creates new institutional entry points for equity participation in Africa's largest mobile money platform at the market level.

Future Market Outlook (2026-2034)

The Africa mobile money market is positioned for sustained, broad-based growth through 2034. From a base of USD 9.18 Billion in 2025, the market is projected to reach USD 67.18 Billion by 2034, representing total incremental value creation of approximately USD 58 Billion over the forecast decade.

This growth will be driven by deepening smartphone penetration, accelerated by affordable 4G device initiatives, expanding super-app ecosystems layering financial services on established mobile money platforms, and the structural opportunity created by AfCFTA's integration of 54 African markets.

Three structural themes will define the long-term trajectory: the technology transition from USSD to app-based wallets, unlocking richer product categories; the formalization of cross-border payment infrastructure, enabling SME trade finance under AfCFTA; and the AI-driven layering of credit, insurance, and investment products onto existing mobile money rails.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 150 industry participants in 2024–2025, including mobile money platform operators (MTN MoMo, M-Pesa, Airtel Money, Orange Money, and Tigo-Pesa), fintech startups, central bank and telecom regulatory officials, agent network managers, microfinance institution executives, and government financial inclusion program representatives across Kenya, Tanzania, Uganda, Ghana, Nigeria, and Côte d’Ivoire.

Secondary Research

Secondary research encompassed a systematic review of GSMA Mobile Money Annual Reports (2022–2025), Central Bank of Kenya (CBK) digital payments statistics, Bank of Ghana and Bank of Tanzania monetary policy and payment system publications, AfCFTA Secretariat trade finance documentation, and World Bank Global Financial Inclusion Database (Global Findex 2021–2024).

Forecasting Models

Market size estimates and growth projections were derived using a combination of top-down and bottom-up forecasting methodologies, incorporating smartphone penetration rates, mobile broadband infrastructure expansion plans, agent network density projections, financial inclusion policy targets, GDP growth forecasts, and historical transaction volume and revenue trends validated against operator-reported data.

Africa Mobile Money Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | USSD, Mobile Wallets, Others |

| Business Models Covered | Mobile Led Model, Bank Led Model |

| Transaction Types Covered | Peer to Peer, Bill Payments, Airtime Top-ups, Others |

| Countries Covered | Tanzania, Kenya, Uganda, Ghana, Others |

| Companies Covered | MTN Group Management Services (Pty) Ltd, Safaricom/Vodacom, Airtel Africa, Orange, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Africa mobile money market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Africa mobile money market.

- The study maps the leading, as well as the fastest-growing, markets. It further enables stakeholders to identify the key country-level markets within the region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Africa mobile money industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Africa Mobile Money Market Report

The Africa mobile money market reached USD 9.18 Billion in 2025. It is projected to reach USD 67.18 Billion by 2034, growing at a CAGR of 25.30% during the 2026-2034 forecast period.

The Africa mobile money market is expected to grow at a CAGR of 25.30% during the forecast period from 2026 to 2034, supported by rising smartphone adoption, accelerated by affordable 4G device programs and investment products layered onto existing mobile money rails.

Kenya leads with a 24.7% revenue share in 2025, anchored by M-Pesa’s unrivalled ecosystem penetration with over 34 million active users and transaction volumes exceeding 50% of Kenya’s GDP.

Bill payments are the largest transaction type segment with a 52.5% share in 2025, reflecting the growing digitalization of utility, government service, household, and subscription payments across the continent.

USSD technology dominates with a 63.5% share in 2025, owing to its universal compatibility with basic feature phones across markets where 2G and 3G infrastructure remains the primary connectivity layer.

Key players include MTN Group Management Services (Pty) Ltd, Safaricom/Vodacom, Airtel Africa, and Orange, among others.

Key growth drivers include surging financial inclusion mandates from African central banks and the IMF, rapid smartphone and 4G network penetration driven by affordable device initiatives, the expansion of dense agent banking networks enabling last-mile financial access, and accelerating government-to-person (G2P) payment digitalization.

Key challenges include regulatory fragmentation across 54 African jurisdictions, creating compliance complexity and limiting cross-border interoperability, elevated cybersecurity and fraud risks as transaction volumes scale, and persistent operator interoperability barriers that impede seamless transfers across platforms.

Significant investment opportunities exist in cross-border payment infrastructure platforms enabling AfCFTA trade finance corridors, super-app ecosystem development integrating e-commerce, savings, credit, and insurance onto existing mobile money rails.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade