Agricultural Biologicals Market Size, Share, Trends and Forecast by Type, Source, Mode of Application, Application, and Region, 2026-2034

Agricultural Biologicals Market Size, Share, Trends & Forecast (2026-2034)

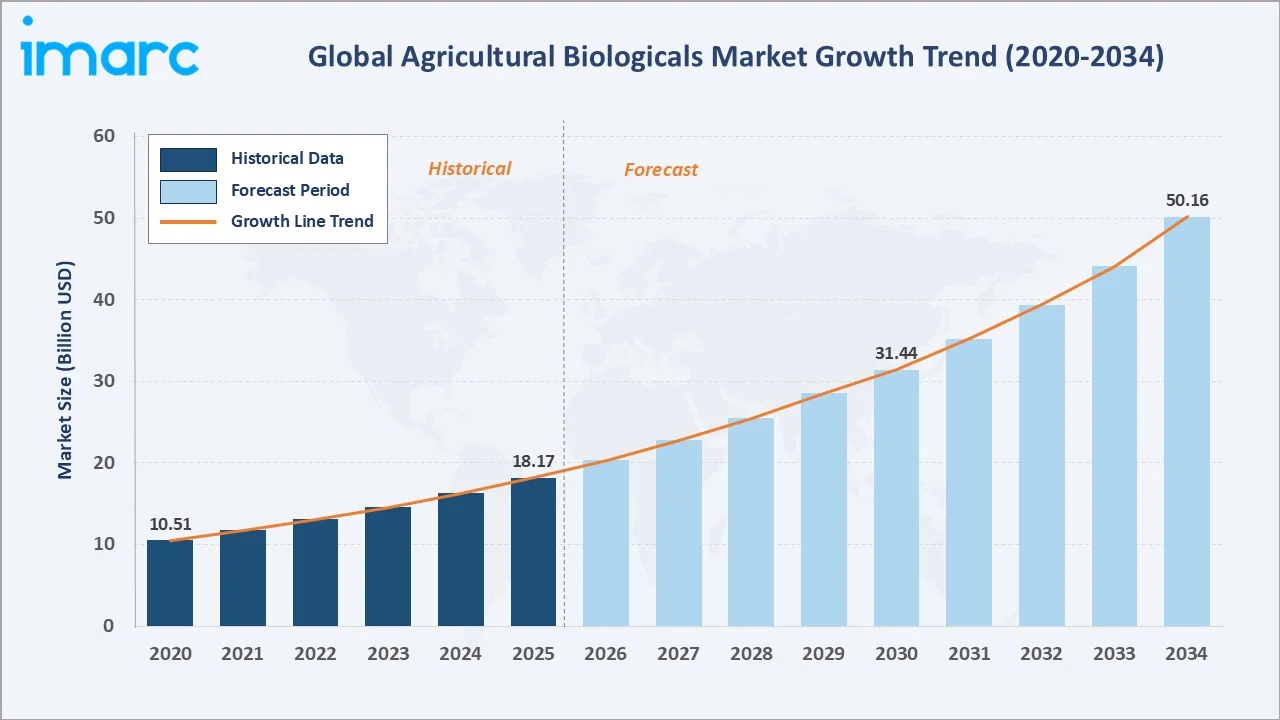

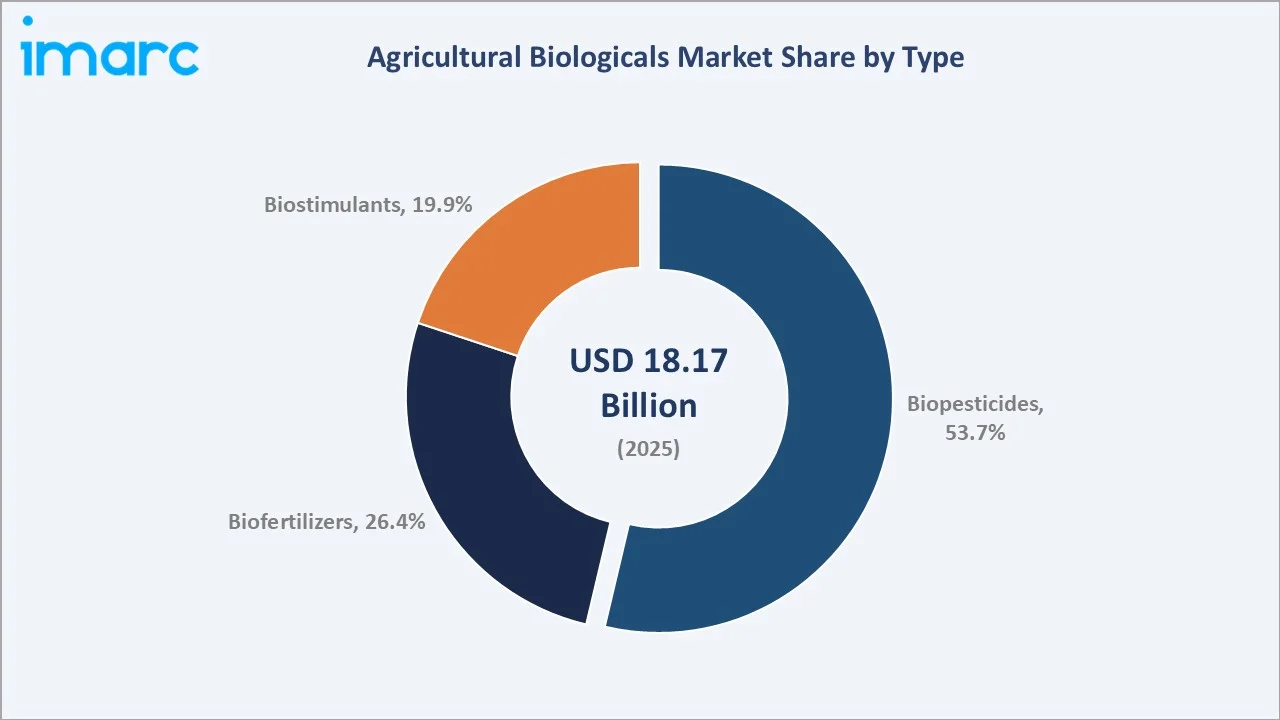

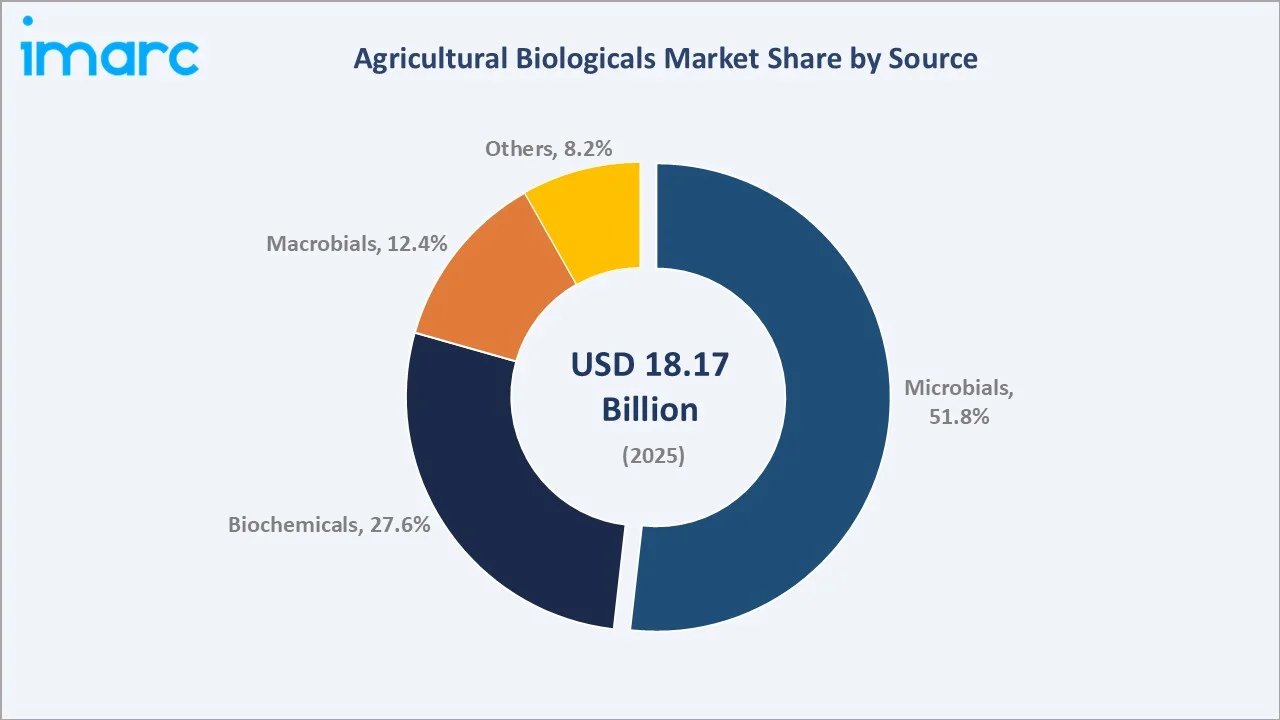

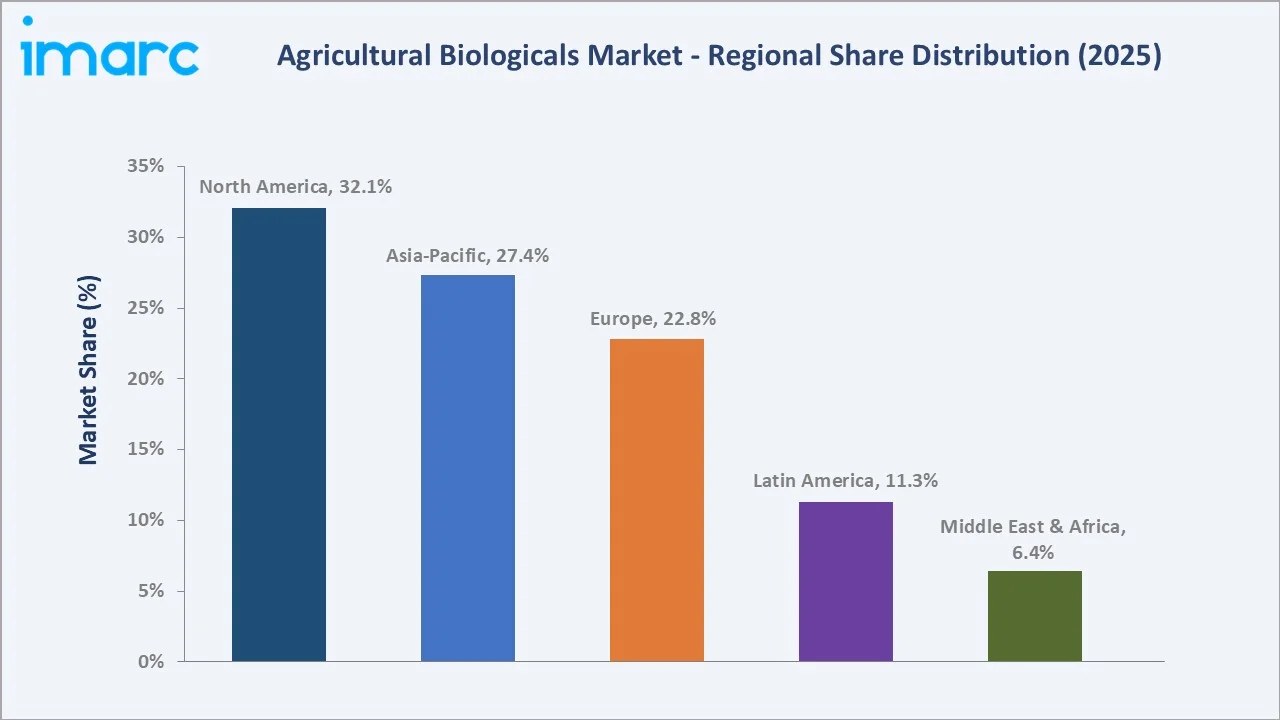

The global agricultural biologicals market reached USD 18.17 Billion in 2025 and is projected to reach USD 50.16 Billion by 2034, growing at a CAGR of 11.58% during 2026-2034. The market is driven by rising demand for sustainable farming, organic food, and eco-friendly crop protection solutions. Growing concerns over chemical pesticide use, soil health, and regulatory support for bio-based inputs are further boosting market growth. The Indian Council for Agricultural Research (ICAR) estimated that demand for foodgrain would increase to 345 million tonnes by 2030. This growing demand is driving the agricultural biologicals market by encouraging farmers to adopt biofertilizers, biopesticides, and biostimulants that improve crop yield, soil health, and sustainable productivity. Biopesticides dominate at 53.7%. Microbials lead source at 51.8%. North America commands 32.1% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 18.17 Billion |

|

Forecast Market Size (2034) |

USD 50.16 Billion |

|

CAGR (2026-2034) |

11.58% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Biopesticides (53.7%, 2025) |

|

Dominant Source |

Microbials (51.8%, 2025) |

|

Leading Region |

North America (32.1%, 2025) |

The market expanded from USD 10.51 Billion in 2020 to USD 18.17 Billion in 2025, anchored at USD 31.44 Billion in 2030, and forecast to reach USD 50.16 Billion by 2034. COVID-19 accelerated organic food demand and supply chain resilience investment, driving above-trend agricultural biological product adoption.

To get more information on this market, Request Sample

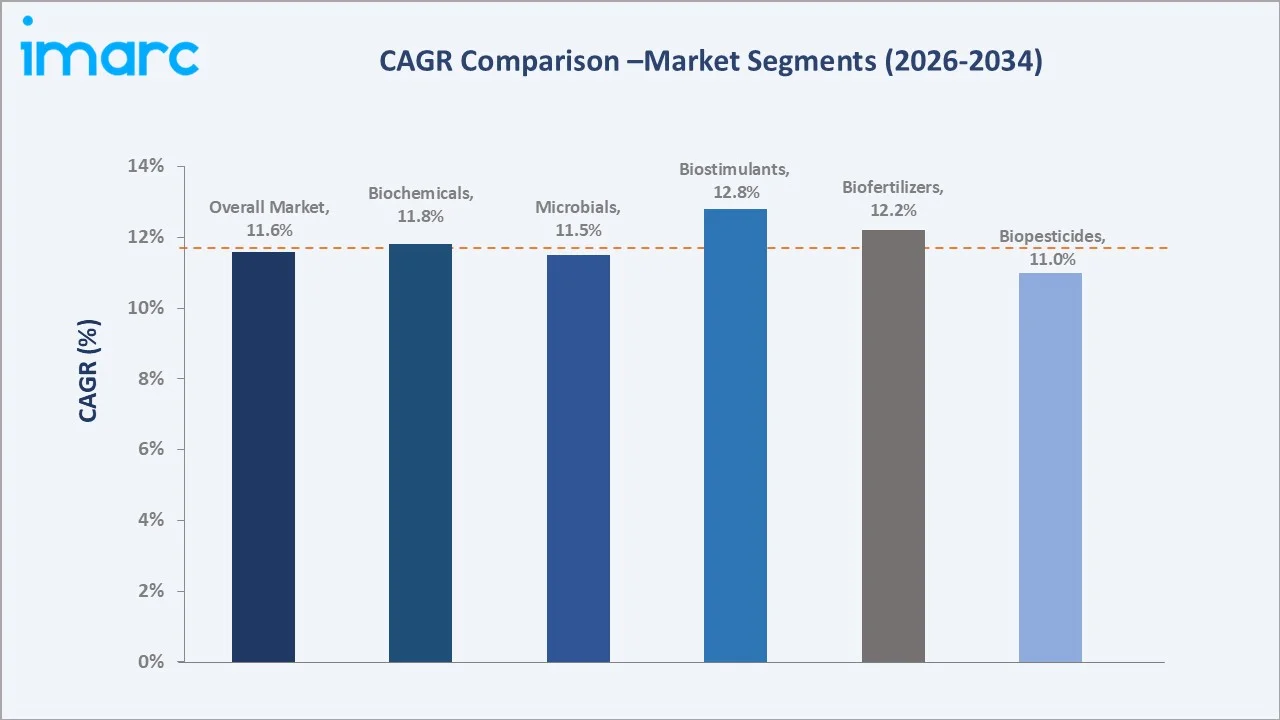

Biostimulants grow fastest at ~12.8% CAGR through the regulations supporting the adoption. Biochemicals grow at ~11.8% CAGR through semiochemical pheromone mating disruption, RNAi biopesticide platform commercialization, and botanical extract biopesticide adoption in premium specialty crop markets.

Executive Summary

The global agricultural biologicals market reached USD 18.17 Billion in 2025, representing the world's fastest-growing segment of the global crop inputs market. Agricultural biologicals, defined as crop production inputs derived from natural materials (microorganisms, biochemicals, beneficial insects, and plant-derived compounds) that improve crop production through pest and disease management (biopesticides), nutrient provision (biofertilizers), or plant growth and stress tolerance enhancement (biostimulants), are experiencing the most transformative commercial decade in their history. The market is projected to reach USD 50.16 Billion by 2034.

Biopesticides at 53.7% lead through commercial maturity. Microbials lead the source at 51.8%. North America, at 32.1%, leads through the US mature biopesticide registration infrastructure and Canada-US large-scale row crop biologicals adoption.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Biopesticides - 53.7% share (2025) |

|

Dominant Source |

Microbials - 51.8% market share (2025) |

|

Leading Region |

North America - 32.1% market share (2025) |

|

Market Opportunity |

Regulatory pesticide phase-outs; carbon sequestration biofertilizer programs; RNAi biopesticide platform; microbiome-as-a-service; integrated biocontrol |

Key Analytical Observations Supporting the Above Data:

- Biopesticides at 53.7%: The biopesticides are dominant due to rising demand for residue-free crops and eco-friendly pest control solutions. Increasing restrictions on chemical pesticides and growing adoption of integrated pest management further support its market leadership.

- Microbials at 51.8%: The microbials dominate because microbial products such as bacteria, fungi, and viruses help improve soil fertility, nutrient uptake, and natural pest control. Their effectiveness in sustainable farming and compatibility with organic agriculture further support strong adoption.

- North America at 32.1%: North America dominates due to strong adoption of sustainable farming practices, advanced agricultural technologies, and high awareness of bio-based crop protection solutions. Supportive regulations for organic farming and the strong presence of key biological product manufacturers further strengthen the region’s leading position.

Agricultural Biologicals Market Overview

The global agricultural biologicals market encompasses the discovery, development, manufacture, registration, and commercialization of all crop inputs derived from or inspired by biological systems, encompassing microbial organisms (bacteria, fungi, viruses), biochemicals (plant extracts, semiochemicals, enzymes), and macrobials (beneficial insects, nematodes) applied to crops for pest and disease control (biopesticides), nutrient provision (biofertilizers), or plant growth and stress tolerance enhancement (biostimulants).

The agricultural biologicals ecosystem integrates strain and molecule discovery scientists, fermentation and production specialists, formulation technology companies, regulatory submission specialists, major agri-input distributors, and commercial growers whose adoption decisions ultimately determine biological product commercial success. Macroeconomic factors include rising global food demand, increasing focus on sustainable agriculture, and growing consumer preference for organic food products.

Market Dynamics

To evaluate market opportunities, Request Sample

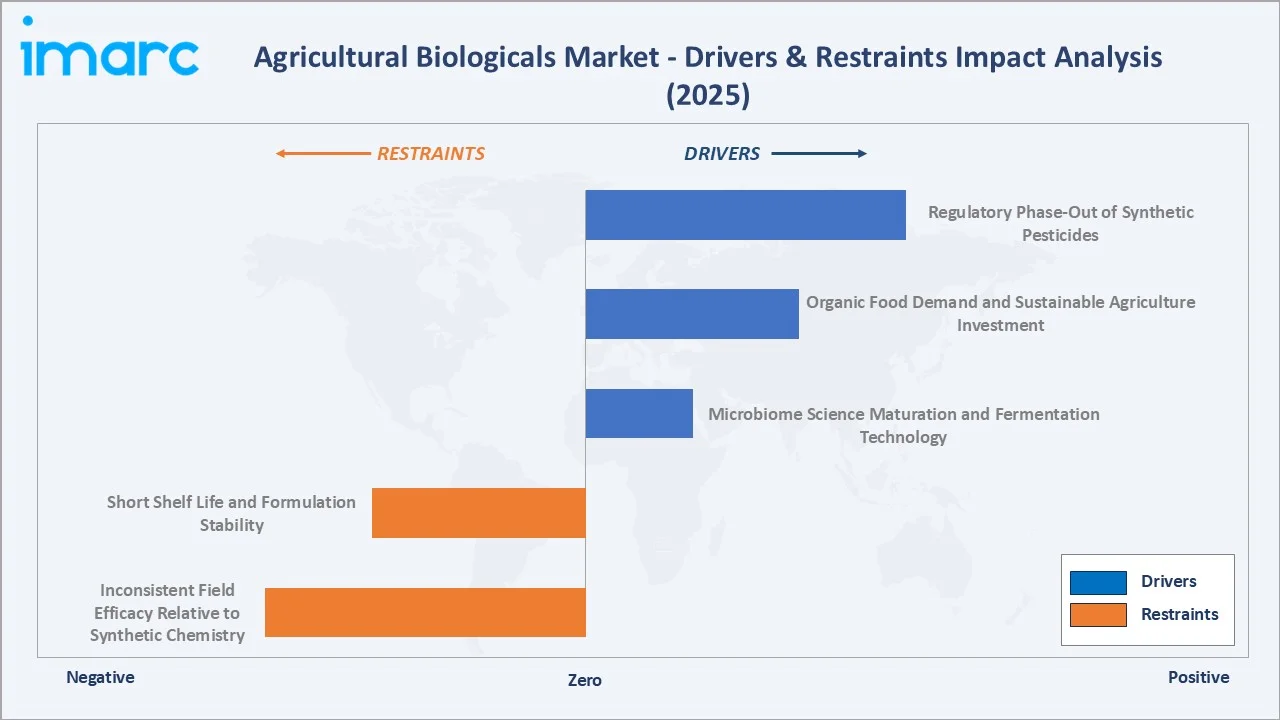

Market Drivers

- Regulatory Phase-Out of Synthetic Pesticides: Regulatory phase-out of synthetic pesticides encourages farmers to shift toward safer and more eco-friendly crop protection products. Stricter rules on chemical residues, soil contamination, and environmental safety are increasing the demand for biopesticides and microbial solutions. Biological products also help growers meet organic and residue-free food standards. As regulatory pressure rises, companies are expanding bio-based product portfolios to replace conventional chemical inputs.

- Organic Food Demand and Sustainable Agriculture Investment: India produced nearly 3.6 million metric tonnes of certified organic products in FY24, including oil seeds, fiber, sugarcane, cereals &millets, cotton, pulses, aromatic &medicinal plants, tea, coffee, fruits, spices, dry fruits, vegetables, processed foods, etc. This rising organic food demand and sustainable agriculture investment are increasing the need for eco-friendly crop protection and nutrition solutions. Consumers are increasingly preferring residue-free and organically grown food, encouraging farmers to use biopesticides, biofertilizers, and biostimulants. Investments in sustainable farming practices are also supporting wider adoption of biological inputs. This shift helps improve soil health, crop productivity, and environmental safety.

- Microbiome Science Maturation and Fermentation Technology: Microbiome science maturation and fermentation technology are improving the development of effective microbial-based products. Better understanding of plant–soil–microbe interactions helps companies create targeted biofertilizers, biopesticides, and biostimulants. Advanced fermentation processes enable large-scale, consistent, and cost-efficient production of beneficial microorganisms. This is increasing product reliability, farmer confidence, and wider adoption of biological inputs.

Market Restraints

- Short Shelf Life and Formulation Stability: Short shelf life and formulation stability create storage and transportation challenges for microbial-based products. Many biological formulations are sensitive to temperature, humidity, and environmental conditions, which can reduce product effectiveness over time. Inconsistent field performance due to stability issues also affects farmer confidence and adoption. These challenges increase the need for advanced formulation technologies and cold-chain logistics to maintain product quality.

- Inconsistent Field Efficacy Relative to Synthetic Chemistry: Inconsistent field efficacy compared to synthetic chemicals is hampering the market because biological products are highly influenced by environmental conditions such as temperature, soil quality, and moisture levels. Their performance can vary across different crops and regions, making results less predictable for farmers. In contrast, synthetic agrochemicals often provide faster and more consistent outcomes. This variability reduces farmer confidence and slows the large-scale adoption of agricultural biologicals.

Market Opportunities

- RNAi Biopesticide Platform Commercialization: RNAi biopesticide platform commercialization enabling highly targeted pest and disease control with lower environmental impact. RNAi-based products can silence specific genes in pests, reducing crop damage while minimizing harm to beneficial organisms. This technology supports residue-free and sustainable crop protection, aligning with organic and eco-friendly farming trends. As commercialization advances, RNAi platforms can expand the next generation of biological crop protection solutions.

- Microbiome-as-a-Service Creating Precision Biological Input Prescription Platforms for Individual Farm Soil Health Management: Microbiome-as-a-Service creates opportunities in the agricultural biologicals market by using soil testing, microbial profiling, and data analytics to recommend farm-specific biological inputs. These platforms help farmers select the right biofertilizers, biostimulants, and microbial treatments based on individual soil health conditions. This improves product effectiveness, crop productivity, and farmer confidence in biological solutions. As precision agriculture grows, customized microbiome-based prescriptions can support wider adoption of agricultural biologicals.

Market Challenges

- Storage and Transportation Challenges for Microbial Products: Storage and transportation challenges for microbial products are creating difficulties because these products are highly sensitive to temperature, humidity, and handling conditions. Improper storage or long transportation periods can reduce microbial viability and product effectiveness. Maintaining cold-chain logistics and controlled environments increases operational costs for manufacturers and distributors. These challenges can limit product availability, especially in remote agricultural regions, and affect farmer confidence in biological solutions.

- Need for Advanced Fermentation and Formulation Technologies: The need for advanced fermentation and formulation technologies is challenging because producing stable and effective microbial products requires specialized manufacturing processes. Developing formulations that maintain microbial viability, shelf life, and field performance can be technically complex and costly. Small and medium-sized companies often face difficulties in scaling production while ensuring product consistency and quality. These technological barriers can slow commercialization and limit the widespread adoption of agricultural biologicals.

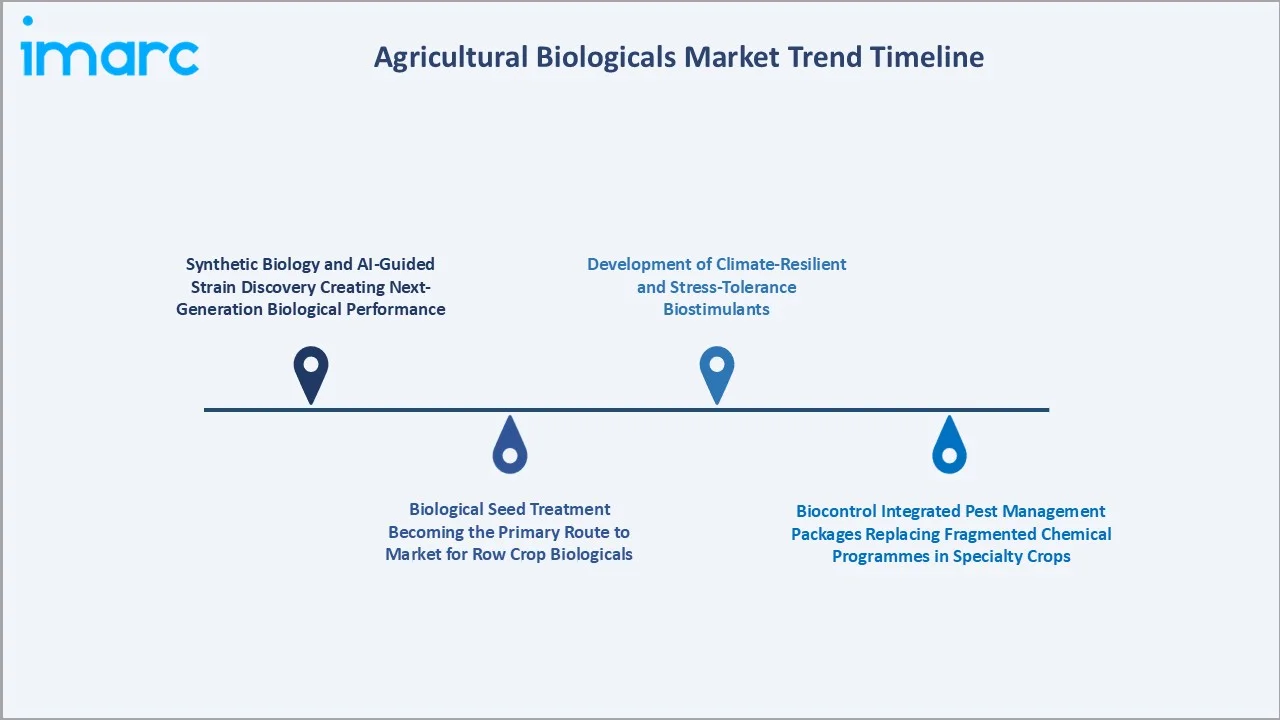

Emerging Market Trends

1. Synthetic Biology and AI-Guided Strain Discovery Creating Next-Generation Biological Performance

Synthetic biology and AI-guided strain discovery enable the development of highly effective and targeted microbial solutions. AI and data analytics help identify beneficial microbial strains faster, while synthetic biology enhances their performance, stability, and adaptability. In March 2025, Verinomics launched two new platforms to accelerate innovation in specialty crops. Its Genesis platform enables transgene-free gene editing for vegetatively propagated crops, while Genova supports faster genomics-led breeding for both seed-based and vegetatively propagated crops, helping bring improved crop varieties to market more quickly. Such platforms help identify, enhance, and commercialize desirable traits more efficiently, supporting next-generation agricultural biological solutions with better crop resilience, productivity, and adaptability.

2. Biological Seed Treatment Becoming the Primary Route to Market for Row Crop Biologicals

Biological seed treatment allows microbes and biostimulants to be applied directly at the planting stage. This improves early root development, nutrient uptake, and crop protection while fitting easily into existing farmer practices. Seed treatment also reduces application complexity and supports large-scale adoption across crops such as corn, soybean, and wheat. As a result, companies are using seed-based delivery to expand biological product penetration in mainstream agriculture.

3. Biocontrol Integrated Pest Management Packages Replacing Fragmented Chemical Programmes in Specialty Crops

Biocontrol integrated pest management (IPM) packages offering comprehensive and sustainable alternatives to fragmented chemical pest control programs. These solutions combine biopesticides, beneficial insects, microbial products, and monitoring systems to manage pests more effectively in specialty crops such as fruits and vegetables. They help reduce chemical residues, improve crop quality, and support compliance with export and organic farming standards. As growers seek safer and long-term pest management strategies, the adoption of integrated biocontrol programs is increasing.

4. Development of Climate-Resilient and Stress-Tolerance Biostimulants

The development of climate-resilient and stress-tolerant biostimulants is emerging due to increasing climate variability and extreme weather conditions. These biostimulants help crops withstand drought, heat, salinity, and nutrient stress while improving plant growth and productivity. Farmers are increasingly adopting such solutions to maintain stable yields under challenging environmental conditions. This trend is encouraging innovation in sustainable crop enhancement technologies and strengthening demand for advanced biological inputs.

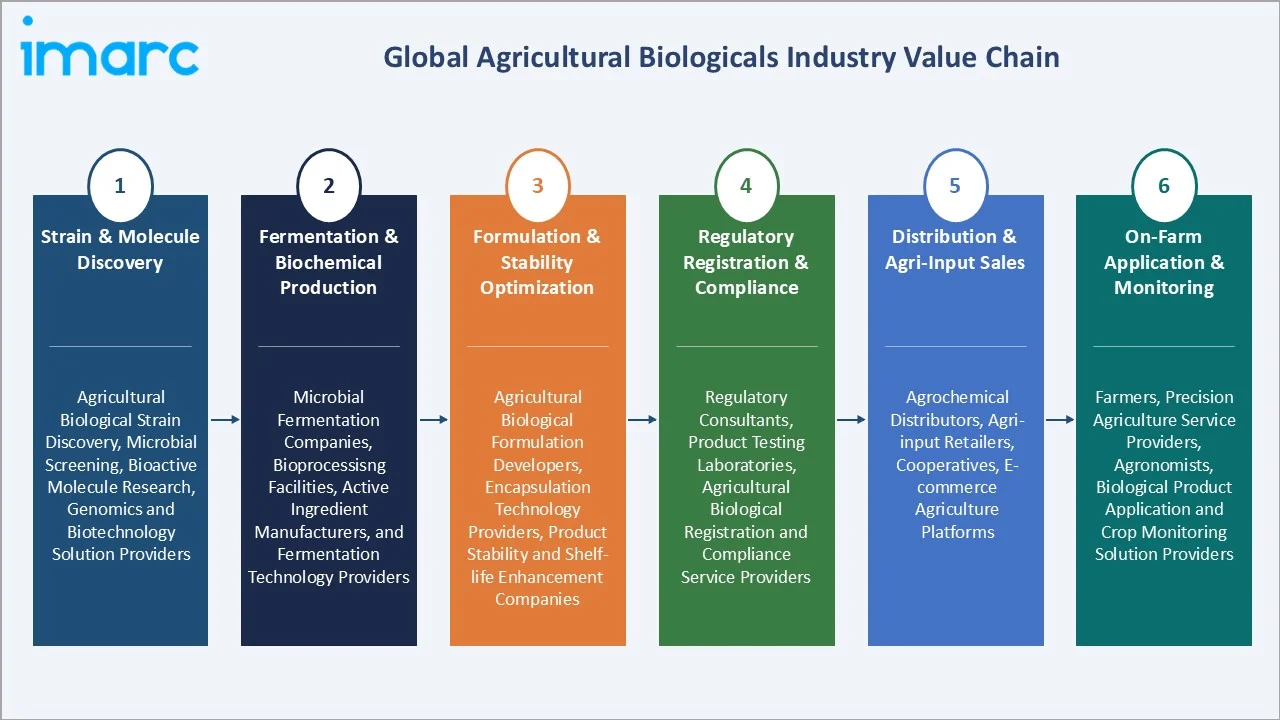

Industry Value Chain Analysis

The agricultural biologicals value chain integrates strain and molecule discovery, fermentation and biochemical production, formulation and stability optimization, regulatory registration and compliance, distribution and agri-input sales, and on-farm application and performance monitoring.

|

Stage |

Key Participants |

|

Strain & Molecule Discovery |

Agricultural biological strain discovery, microbial screening, bioactive molecule research, genomics and biotechnology solution providers |

|

Fermentation & Biochemical Production |

Microbial fermentation companies, bioprocessing facilities, active ingredient manufacturers, and fermentation technology providers |

|

Formulation & Stability Optimization |

Agricultural biological formulation developers, encapsulation technology providers, product stability and shelf-life enhancement companies |

|

Regulatory Registration & Compliance |

Regulatory consultants, product testing laboratories, agricultural biological registration and compliance service providers |

|

Distribution & Agri-Input Sales |

Agrochemical distributors, agri-input retailers, cooperatives, e-commerce agriculture platforms |

|

On-Farm Application & Monitoring |

Farmers, precision agriculture service providers, agronomists, biological product application and crop monitoring solution providers |

The formulation stage is the agricultural biologicals value chain's most commercially under-invested and technically challenging phase relative to its commercial importance. The acquired companies' biological product portfolios are being valued not just for biological product technology but for the distribution channel access and customer relationships that conventional agrochemical companies' distribution networks can accelerate compared to independent biological company distribution development timelines.

Technology Landscape in the Agricultural Biologicals Industry

Microbial Fermentation Technology for Biologically Active Ingredient Production

Microbial fermentation technology enables the large-scale production of beneficial microorganisms used in biofertilizers, biopesticides, and biostimulants. Advanced fermentation systems improve microbial growth, purity, consistency, and cost-efficiency during manufacturing. These technologies also help enhance product stability and commercial scalability for agricultural applications. As demand for sustainable crop inputs increases, companies are investing in advanced fermentation infrastructure to improve biological product performance and supply reliability.

RNAi Platform Technology for Next-Generation Biopesticide Development

RNAi platform technology enabling highly targeted and gene-specific pest control solutions. RNAi-based biopesticides work by silencing essential genes in pests, reducing crop damage while minimizing impact on beneficial organisms and the environment. In May 2026, Renaissance Bioscience developed a new yeast-based virus-like particle (VLP) system that could significantly broaden the capabilities of its RNAi platform. The technology is designed to support the production of stable and cost-efficient biopesticides for controlling a wider range of pests. These technologies support residue-free and sustainable agriculture practices compared to conventional chemical pesticides. As research and commercialization advance, RNAi platforms are driving innovation in next-generation biological crop protection products.

Precision Microbiome Technology and AI-Guided Biological Product Development

Precision microbiome technology and AI-guided biological product development enable the identification of beneficial microbes and optimized biological formulations for specific crops and soil conditions. AI and data analytics help analyze complex soil–microbe interactions, accelerating strain discovery and product customization. These technologies improve the effectiveness, consistency, and precision of biofertilizers, biopesticides, and biostimulants. As a result, companies are developing next-generation biological solutions tailored to sustainable and precision agriculture practices.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Biopesticides |

53.7% |

2025 |

|

Source |

Microbials |

51.8% |

2025 |

|

Mode of Application |

Foliar Spray |

58.5% |

2025 |

|

Application |

Cereals and Grains |

44.6% |

2025 |

|

Region |

North America |

32.1% |

2025 |

By Type

Biopesticides lead at 53.7% (2025). The biopesticide segment encompasses microbial insecticides, microbial fungicides, biochemical biopesticides, and macrobial biological control. Biopesticides' ~11.0% CAGR reflects sustained regulatory-driven replacement demand as chemical pesticide withdrawals create mandatory biological adoption above voluntary preference-driven switching.

To access detailed market analysis, Request Sample

Biofertilizers at 26.4% anchor on expanding toward nitrogen fixation in non-legume cereals, phosphate biofertilizers in potassium-depleted Asian soils, and carbon credit-incentivized synthetic fertilizer displacement globally. Biostimulants at 19.9% grow fastest at ~12.8% CAGR through seaweed biostimulant adoption in European and North American specialty crop markets.

By Source

Microbials lead at 51.8% (2025). Bacillus (multiple species) and Trichoderma collectively represent the microbial biopesticide segment's commercial foundation, with Bradyrhizobium and other nitrogen-fixing bacteria anchoring microbial biofertilizers, and plant growth-promoting rhizobacteria (PGPR), including Azospirillum, Pseudomonas fluorescens, and Bacillus velezensis, defining microbial biostimulants.

Biochemicals at 27.6% encompass semiochemicals, plant-derived biochemicals, and humic and fulvic acids. Macrobials at 12.4% represent commercial beneficial insects, entomopathogenic nematodes, and predatory beetles distributed primarily in European and North American greenhouse and specialty crop markets.

Regional Market Insights

|

Region |

Share (2025) |

Key Agricultural Biologicals Market Drivers & Characteristics |

|

North America |

32.1% |

Driven by strong adoption of sustainable farming practices, advanced agri-biotech infrastructure, and increasing demand for residue-free crop protection solutions. |

|

Asia Pacific |

27.4% |

Driven by rising food demand, expanding organic farming activities, and increasing awareness regarding sustainable agriculture. |

|

Europe |

22.8% |

Supported by stringent environmental regulations, restrictions on synthetic agrochemicals, and a strong focus on sustainable crop production. |

|

Latin America |

11.3% |

Driven by the large-scale cultivation of export-oriented crops and the rising adoption of integrated pest management practices. |

|

Middle East and Africa |

6.4% |

Growing steadily due to increasing interest in sustainable agriculture, improving awareness of biological crop inputs, and the need to enhance crop productivity under challenging climatic conditions. |

North America's market leadership is reinforced by the US-registered biological pesticide active ingredients, creating the most commercially accessible biopesticide regulatory infrastructure. Asia-Pacific's 27.4% reflects India's leading biofertilizer volume consumption and China's government-mandated chemical reduction, creating one of the largest structural biological demand transitions. Europe's 22.8% reflects the EU regulations creating the most commercially significant regulatory-driven biological product demand signal.

Latin America's 11.3% is disproportionately commercially significant. Middle East and Africa, at 6.4%, is growing above global CAGR through Middle East food security, greenhouse biological IPM adoption and Sub-Saharan Africa biofertilizer government expansion, creating first-generation commercial biological product markets in previously unserved geographies.

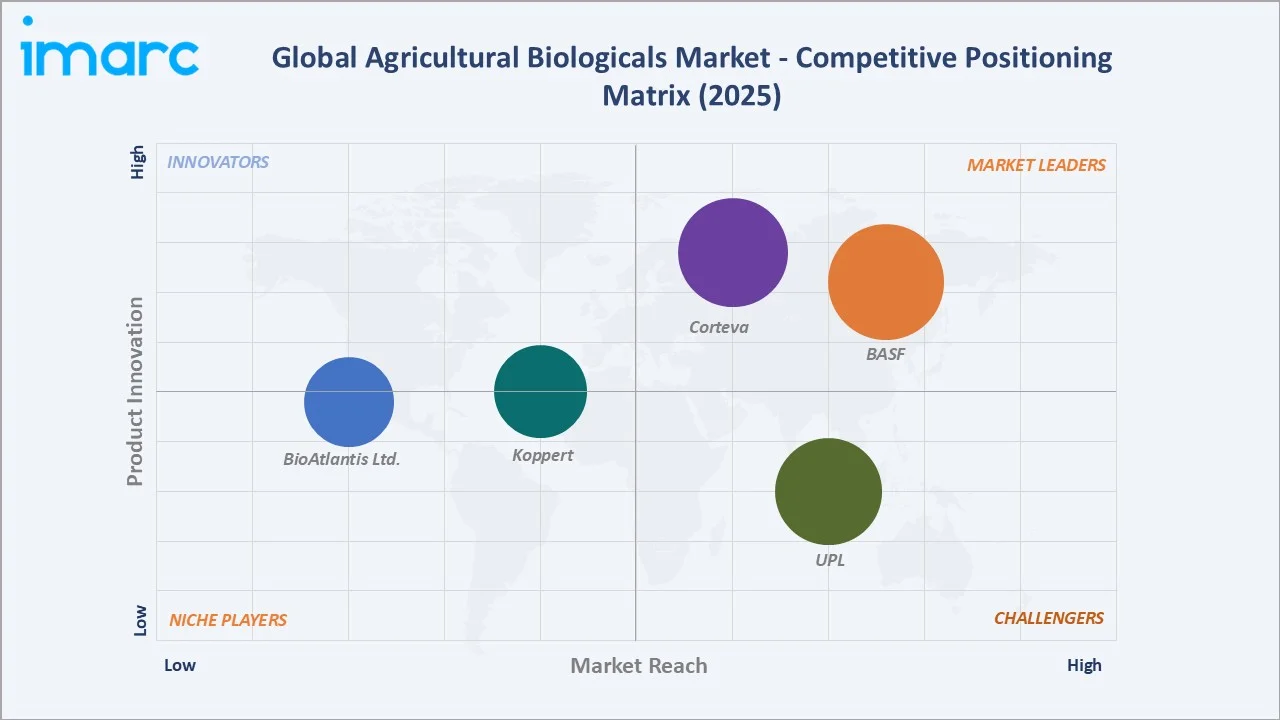

Competitive Landscape

The global agricultural biologicals market competitive landscape is structured across three distinct commercial tiers: integrated major agrichemical companies, pure-play biological specialists, and emerging biological technology companies.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

BASF |

Poncho Votivo, Votivo Prime, Nodulator Duo SCG, Vault IP Plus, Integral Pro |

Market Leader |

BASF is a leading global player in agricultural biologicals, providing a diverse portfolio of microbial-based products designed to complement conventional crop protection. |

|

Corteva |

Bexfond Biological Fungicide, Golden Pest Spray Oil, Bio-Forge Premier, Fortified Stimulate Yield Enhancer Plus, MycoUp, X-Cyte |

Market Leader |

Corteva is positioning itself as a leader in the agricultural biologicals market by integrating natural-based solutions such as biocontrols and biostimulants, with traditional chemical crop protection to improve yield, sustainability, and stress resilience. |

|

UPL |

Foltron, Biozyme TF, Gainexa FC, Calibra |

Strong Challenger |

UPL is a major global player in agricultural biologicals. Their role focuses on enhancing crop protection, improving soil health, and facilitating chemical residue management through products like seaweed extracts, biocontrol agents, and biostimulants. |

|

Koppert |

Addit, Anso-Mite, Anso-Mite Plus, Aphidalia, Aphidend, Aphilin, Aphipar, Aphipar-M |

Established Player |

Koppert specializes in sustainable crop protection and natural pollination. They develop beneficial microorganisms, macro-organisms, and natural solutions to replace or complement chemical pesticides, enhancing plant resilience, soil health, and residue-free food production. |

|

BioAtlantis Ltd. |

SuperFifty Prime, BlackFort, MicroGrow, AtlantiCal |

Established Player |

BioAtlantis Ltd. is a leading biotechnology company specializing in the development and manufacture of natural, seaweed-derived bioactive compounds for agriculture, with a core focus on plant biostimulants and stress mitigation technology. |

The competitive landscape is being reshaped by digital agriculture integration. The digital farming platforms are creating data-driven biological product recommendation capabilities that associate biological product application decisions with field performance data across millions of acres. Companies that integrate biological product decision support within digital farming platforms will command adoption advantages over competitors relying solely on agronomist recommendations and grower trial-and-error for biological product adoption.

Key Company Profiles

BASF

BASF is a leading global chemical and agricultural solutions company with a strong presence in the agricultural biologicals market through its sustainable crop protection and plant health portfolio. The company offers a range of biological products, including biopesticides, inoculants, and biostimulants, designed to improve crop productivity, soil health, and environmental sustainability.

- Key Products: Poncho Votivo, Votivo Prime, Nodulator Duo SCG, Vault IP Plus, Integral Pro.

- Recent Developments: In May 2026, BASF Agricultural Solutions opened its new BioHub fermentation facility at its Ludwigshafen site to produce biological and biotechnology-based crop protection products. The plant manufactures biological fungicides and seed treatments, strengthening BASF’s portfolio of sustainable and integrated crop protection solutions.

- Strategic Focus: Expanding biological crop protection, seed treatment, and plant health solutions that support sustainable, residue-free, and high-yield farming.

Corteva

Corteva is a leading global agriculture company with a growing presence in the agricultural biologicals market through its focus on sustainable crop protection and biological innovation. The company offers biological solutions, including biostimulants, microbial products, and natural crop protection technologies aimed at improving crop yield, resilience, and soil health.

- Key Products: Bexfond Biological Fungicide, Golden Pest Spray Oil, Bio-Forge Premier, Fortified Stimulate Yield Enhancer Plus, MycoUp, X-Cyte.

- Recent Developments: In November 2025, Corteva introduced Goltrevo, its first bioinsecticide, designed to help farmers reduce crop losses caused by damaging pests such as the corn leafhopper.

- Strategic Focus: Expanding biological seed treatments, biostimulants, and sustainable crop protection solutions to improve crop resilience, productivity, and soil health.

Market Concentration Analysis

The global agricultural biologicals market is moderately fragmented. Market concentration is increasing through M&A. The biopesticide category is most concentrated, biofertilizers are most fragmented, and biostimulants are emerging from fragmentation. Regional market concentration varies significantly, with North America highly consolidated, Europe more fragmented, with strong regional specialists, Latin America highly fragmented in biofertilizers but consolidated in biopesticides, and Asia-Pacific most fragmented.

Investment & Growth Opportunities

Highest Growth Segments

Biostimulants (~12.8% CAGR), biochemicals/RNAi platform (~11.8% CAGR), precision microbiome biological services (~25% CAGR from small base), biological seed treatments (~15% CAGR in row crops), carbon-credit-linked biofertilizers (~20% CAGR in North American and European carbon markets), and African smallholder biofertilizer programs (~18% CAGR from near-zero base) represent the highest-growth agricultural biologicals investment vectors through 2034.

Emerging Investment Opportunities

The EU pesticide phase-out, creating an estimated USD 3-4 Billion European biological product replacement market by 2030, represents the most commercially certain near-term agricultural biologicals investment opportunity, with biological product companies with EU-registered biopesticides targeting the specific pest-crop combinations affected by withdrawn active substances positioned for above-market European revenue growth through mandatory grower adoption without competition from withdrawn conventional alternatives.

Investment Themes

- RNAi biopesticide platform investment capturing the next-generation biological crop protection market with new mode of action advantages: RNAi biopesticides entering commercial launch create first-mover advantage in a biological insecticide category with fundamental performance advantages, species specificity eliminating non-target effects, new mode of action circumventing all existing insecticide resistance mechanisms, and biodegradable environmental fate profile.

- Precision microbiome service platform development, creating subscription biological input prescription business above commodity product sales: Soil microbiome assessment service at USD 200-500 per sample, creating a recurring annual service revenue model that positions biological input companies as agronomic data and service businesses above commodity product suppliers.

Future Market Outlook (2026-2034)

The global agricultural biologicals market is projected to grow from USD 18.17 Billion in 2025 to USD 50.16 Billion by 2034, delivering an 11.58% CAGR over the forecast period. The market's anchor value of USD 31.44 Billion in 2030 represents an agricultural biologicals industry at its most transformative commercial inflection. Biostimulants will have achieved mainstream row crop adoption in Europe and North America following EU regulation-registered product availability at commercial scale, RNAi biopesticides will have commercial products for multiple major pest targets beyond the pioneer fall armyworm product, and the carbon credit market will have created measurable financial incentives above agronomic benefit for biological nitrogen fixation and biopesticide adoption in carbon programme enrolled farms.

Three structural forces define the agricultural biologicals market growth through 2034 with exceptional confidence. Regulatory pesticide withdrawal is mathematically certain and commercially irreversible. Microbiome science maturation is creating a commercial biological product pipeline of unprecedented breadth. Consumer food system demand transformation, sustaining above-market biological product adoption, even in regulatory environments that move more slowly than the EU and US.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including Senior Vice Presidents; R&D Directors; Commercial Directors; regulatory specialists; agricultural biologicals investors; and regional market specialists.

Secondary Research

Secondary research encompassed Biopesticide Active Ingredients List; Pesticide Active Substances Database; European Biostimulants Industry Council market data; Biological Products Committee industry statistics; company annual reports; Pesticides Biological Pesticides review; Organic Monitor World Organic Trade Statistics; Agri-Food Tech Investment Report. Over 65 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a product category bottom-up model: (i) biopesticide component; (ii) biofertilizer component; (iii) biostimulant component.

Agricultural Biologicals Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Biopesticides, Biofertilizers, Biostimulants |

| Sources Covered | Microbials, Macrobials, Biochemicals, Others |

| Modes of Applications Covered | Foliar Spray, Soil Treatment, Seed Treatment, Post-harvest |

| Applications Covered | Cereals and Grains, Oilseed and Pulses, Fruits and Vegetables, Turf and Ornamentals, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BASF, Corteva, UPL, Koppert, BioAtlantis Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the agricultural biologicals market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global agricultural biologicals market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the agricultural biologicals industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Agricultural Biologicals Market Report

The global agricultural biologicals market reached USD 18.17 Billion in 2025. The market is driven by rising demand for sustainable and residue-free farming practices, along with increasing concerns over the environmental impact of synthetic agrochemicals. Growing adoption of organic farming, supportive government regulations, and advancements in microbial and biological crop protection technologies are further accelerating market growth.

The market grows at 11.58% CAGR during 2026-2034, reaching USD 50.16 Billion by 2034. Biostimulants grow fastest at ~12.8% CAGR through EU regulation harmonized registration, creating the world's first legal biostimulant framework. Biochemicals grow at ~11.8% CAGR through RNAi biopesticide commercial launch and semiochemical pheromone mating disruption expansion. The overall market growth is sustained by organic food market growth and microbiome science maturation, creating next-generation biological product performance.

Biopesticides lead at 53.7% through commercial development, creating the world's most diverse biological pest management portfolio from insecticides through Trichoderma fungicides to biochemical pheromone mating disruption systems.

Microbials lead at 51.8% through Bacillus and Trichoderma commercial deployment in biopesticides, Bradyrhizobium and PGPR in biofertilizers, and PGPR biostimulants.

North America leads at 32.1% through the US-registered biologically active substances and California specialty crop biological adoption, driven by strict pesticide residue regulations.

Leading companies include BASF, Corteva, UPL, Koppert, and BioAtlantis Ltd., among others.

The market is projected to reach approximately USD 31.44 Billion by 2030, with RNAi biopesticides achieving commercial products for multiple pest targets beyond fall armyworm, EU regulation-registered biostimulants achieving commercial scale across all major EU member state markets, the carbon credit market creating measurable financial incentives for biological nitrogen fixation adoption in enrolled North American and European farm acres, and biostimulant mainstream adoption.

RNA interference (RNAi) biopesticides are double-stranded RNA (dsRNA) molecules designed to silence specific gene expression in target pest organisms, causing mortality or reduced fitness through molecular mechanisms rather than conventional toxicological chemistry. RNAi biopesticides' commercial significance derives from three fundamental advantages: species specificity, a new mode of action, and biodegradable environmental fate.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)