Agricultural Films Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Agricultural Films Market Size, Share, Trends & Forecast (2026-2034)

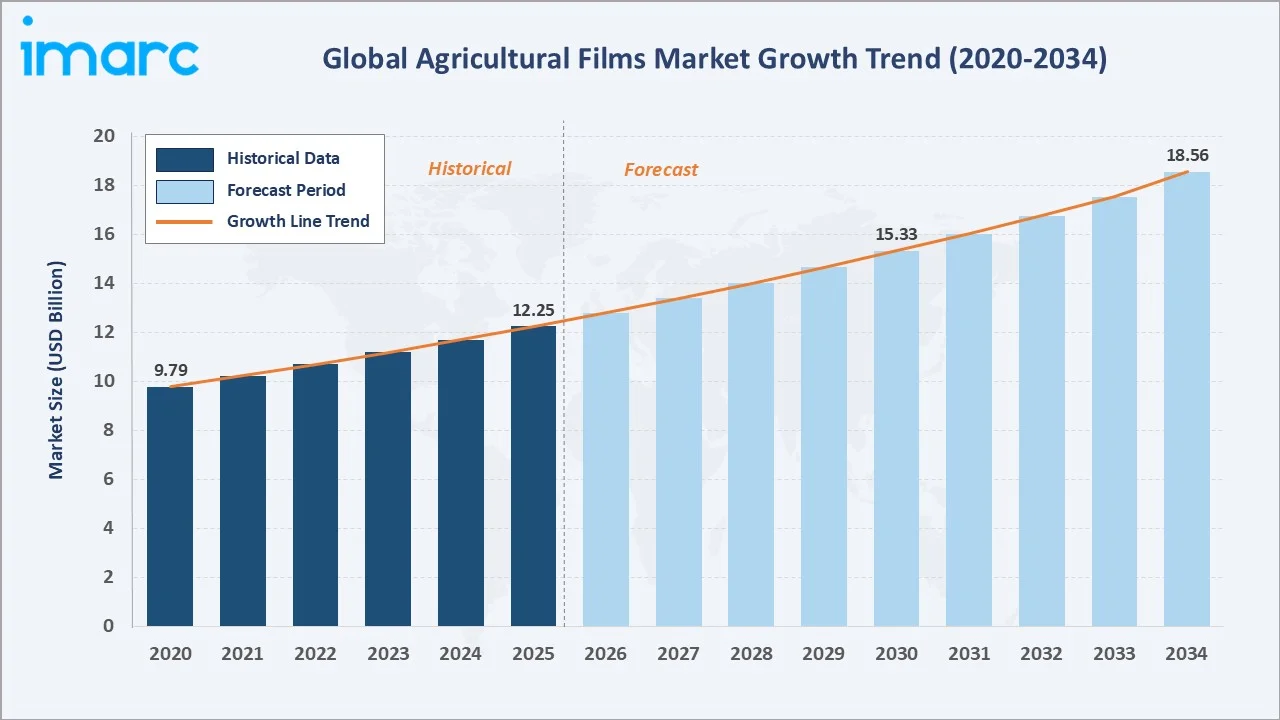

The global agricultural films market reached USD 12.25 Billion in 2025 and is projected to reach USD 18.56 Billion by 2034, growing at a CAGR of 4.59% during 2026-2034. Market growth is driven by rising global food security demands, escalating water scarcity accelerating mulch film adoption, expanding greenhouse farming, and growing policy support for biodegradable film alternatives.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 12.25 Billion |

| Forecast Market Size (2034) | USD 18.56 Billion |

| CAGR (2026-2034) | 4.59% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

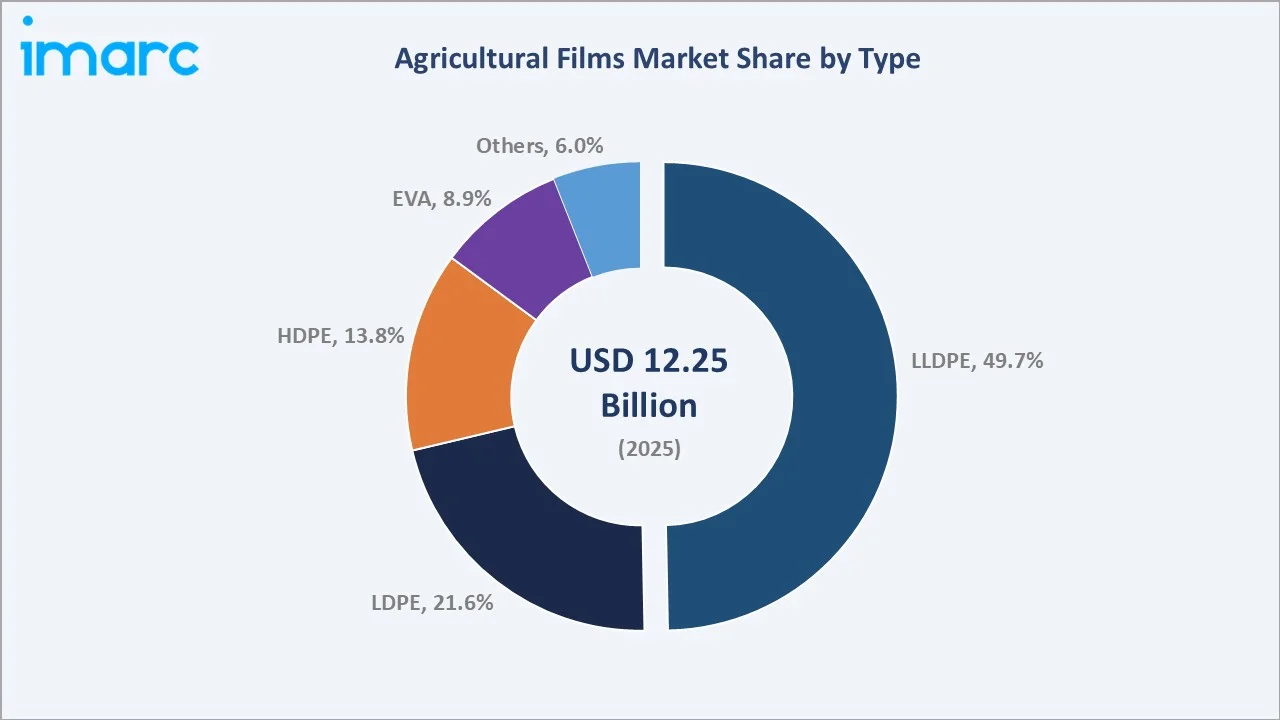

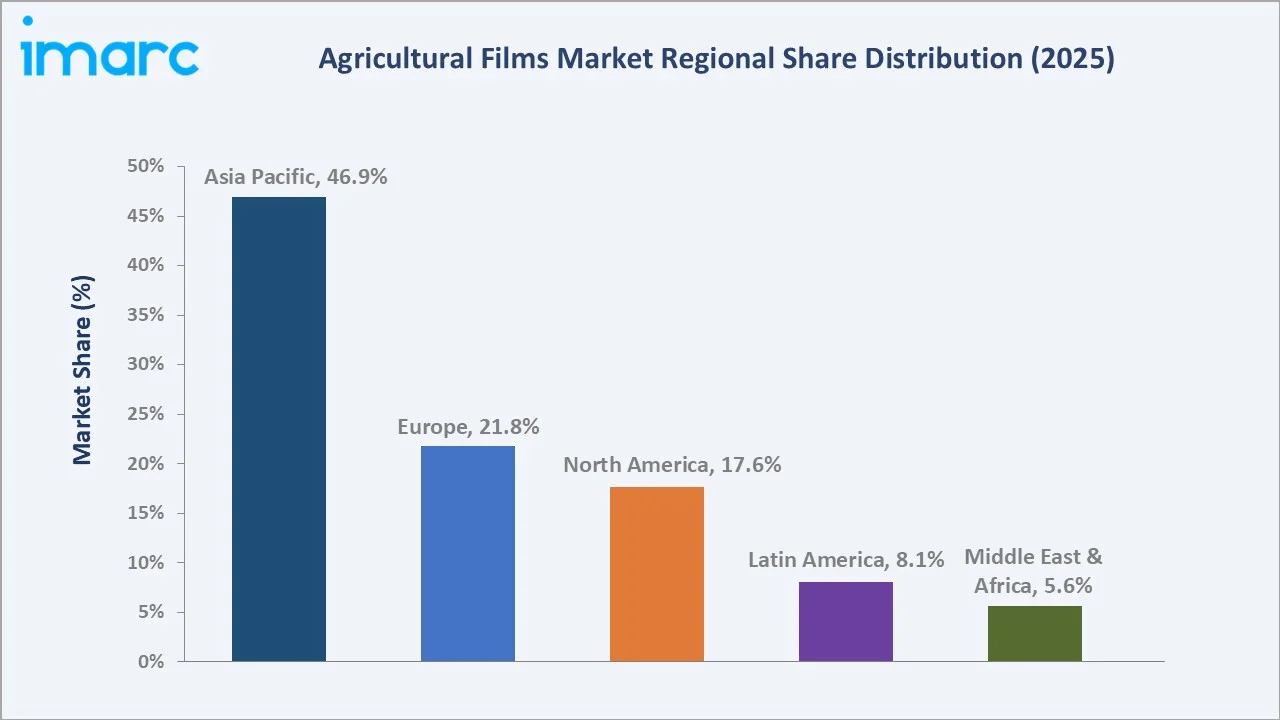

Asia Pacific's 46.9% dominance reflects China's position as the world's largest agricultural film producer and consumer, deploying over 1.2 million tons annually across vegetable mulch cultivation, greenhouse horticulture, and silage baling. Linear low-density polyethylene’s 49.7% type share reflects its optimal balance of puncture resistance, film clarity, UV stability, and processability that makes it the resin of choice for mulch, greenhouse cover, and silage wrap film applications across all geographies.

To get more information on this market, Request Sample

The market's 4.59% CAGR reflects the steady, non-discretionary demand for agricultural films driven by the structural imperative of feeding a global population projected to reach 9.8 Billion by 2050. Agricultural films are among the most cost-effective crop yield improvement technologies available to farmers; mulch films alone increase yields by 15–50% while reducing irrigation requirements by 20–50%, delivering compelling economic returns across all farm scale categories.

Executive Summary

The global agricultural films market is growing steadily, underpinned by the fundamental requirement of modern agriculture to optimize land, water, and energy productivity in the context of climate change and population growth. From USD 12.25 Billion in 2025, the market is forecast to reach USD 18.56 Billion by 2034, creating incremental value of USD 6.31 Billion at a 4.59% CAGR.

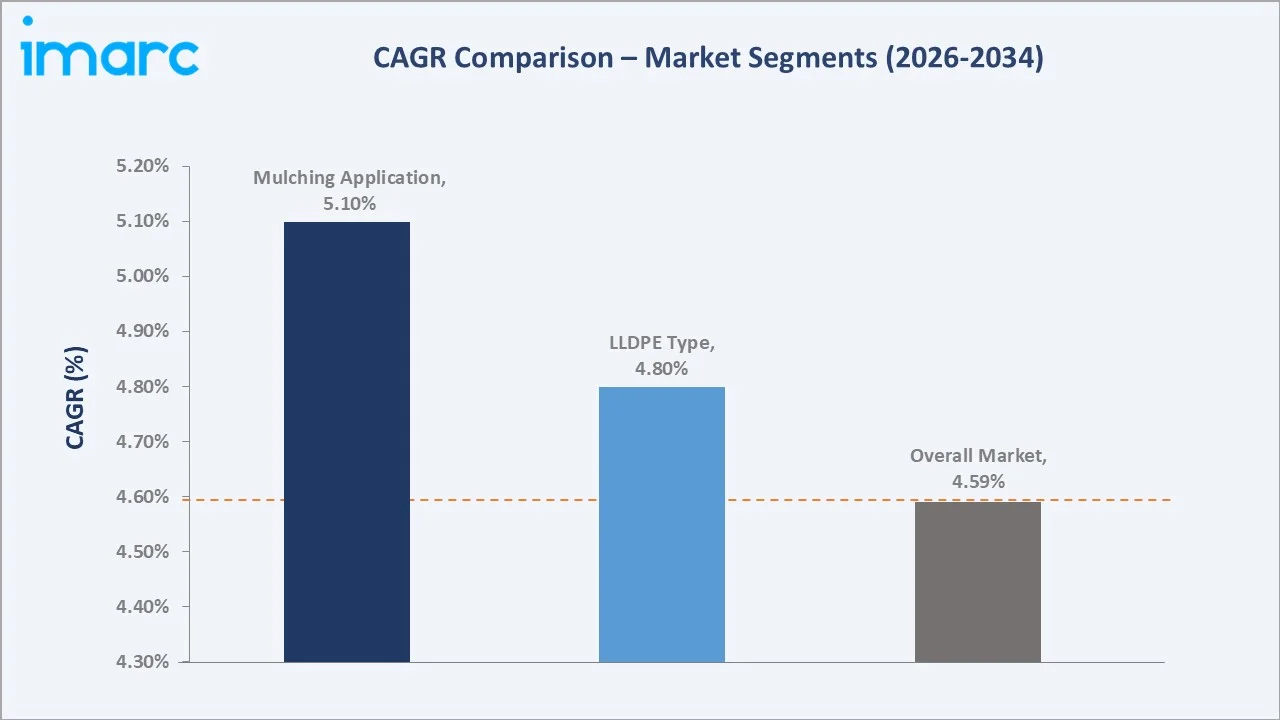

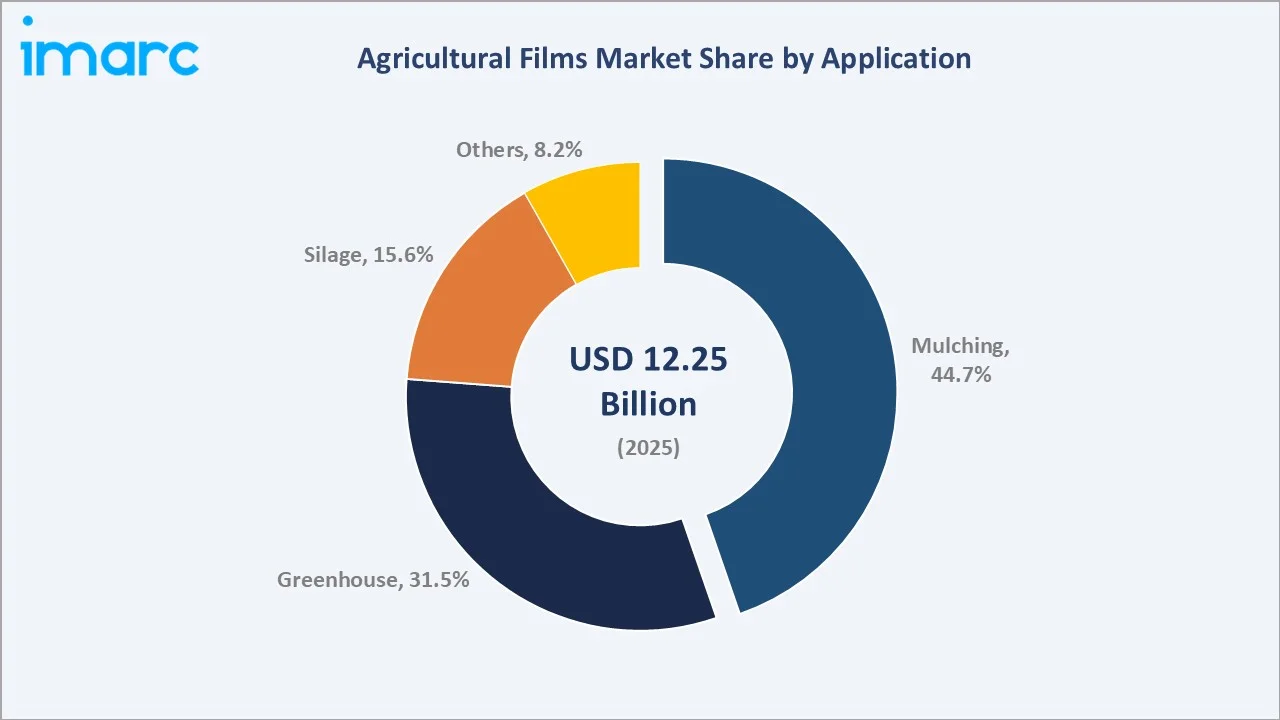

Linear low-density polyethylene leads the type segment at 49.7% in 2025, valued for its superior stretch properties, puncture resistance, and multi-layer coextrusion compatibility. Mulching films lead applications at 44.7%, driven by the global expansion of intensive vegetable cultivation, strawberry farming, and vineyard management practices that rely on plastic mulch for weed suppression, soil temperature regulation, and moisture conservation.

Key players, including Amcor plc, BASF, Armando Alvarez S.A., RKW Group, and Exxon Mobil Corporation, compete through resin technology leadership, film performance additive expertise, biodegradable film development, and global distribution networks serving agricultural input dealers and direct farmer channels.

Key Market Insights

| Insight | Data |

|---|---|

| Largest Type Segment | Linear Low-Density Polyethylene – 49.7% share (2025) |

| Fastest Growing Type | Linear Low-Density Polyethylene – ~4.80% CAGR; biodegradable grades growing at 12%+ |

| Largest Application Segment | Mulching – 44.7% share (2025) |

| Fastest Growing Application | Mulching – ~5.10% CAGR driven by intensive vegetable farming |

| Leading Region | Asia Pacific – 46.9% share (2025) |

| Top Companies | Amcor plc, BASF, Armando Alvarez S.A., RKW Group, and Exxon Mobil Corporation |

Key Analytical Observations:

- Linear low-density polyethylene commands a dominant 49.7% market share in 2025. Its preference reflects superior mechanical properties over conventional LDPE: LLDPE provides higher tear and puncture resistance at equivalent film thickness, enabling lighter-gauge films that reduce material costs per hectare without sacrificing performance.

- Mulching applications at 44.7% (2025) reflect the massive global scale of plastic mulch deployment in intensive horticulture. Globally, plastic mulch is used on an estimated ~20 million hectares of cropland. Mulch films increase soil temperature, reduce weed emergence, and decrease irrigation frequency, providing compelling ROI for farmers across all economic development levels.

- Greenhouse films at 31.5% (2025) represent a growing and premium application segment. Greenhouse films incorporate sophisticated functional coatings: diffuse coatings scatter direct sunlight to improve light distribution, anti-condensation coatings prevent water droplet formation, and thermal IR retention coatings reduce nighttime heat loss.

- Asia Pacific's commanding 46.9% share reflects the concentration of global intensive horticulture production across China, India, South Korea, Japan, and Southeast Asia. China's dominance in both film production and film consumption makes the region structurally irreplaceable in the global agricultural film supply chain.

Agricultural Films Market Overview

Agricultural films are thin plastic sheets manufactured primarily from polyethylene resins (LLDPE, LDPE, HDPE) and specialty polymers (EVA, biodegradable PLA/PBAT blends) that are deployed in farming applications to modify growing environments, protect crops, and improve resource use efficiency.

The three primary categories are mulch films (laid on soil surface to regulate temperature and moisture), greenhouse films (covering tunnel and glasshouse structures), and silage films (wrapping forage crops for anaerobic fermentation preservation). Each category has distinct performance requirements driving different resin, additive, and film thickness specifications.

The market operates across a global value chain from petrochemical resin production through film extrusion manufacturing, distribution via agricultural input dealers, farm-level installation, and increasing end-of-life recovery and recycling.

The growing emphasis on sustainability is driving the development of biodegradable film alternatives (particularly PBAT/PLA blends for mulch applications) and collection programs for conventional PE film waste, which represents a significant environmental management challenge, particularly in Asia and Latin America.

Market Dynamics

To evaluate market opportunities, Request Sample

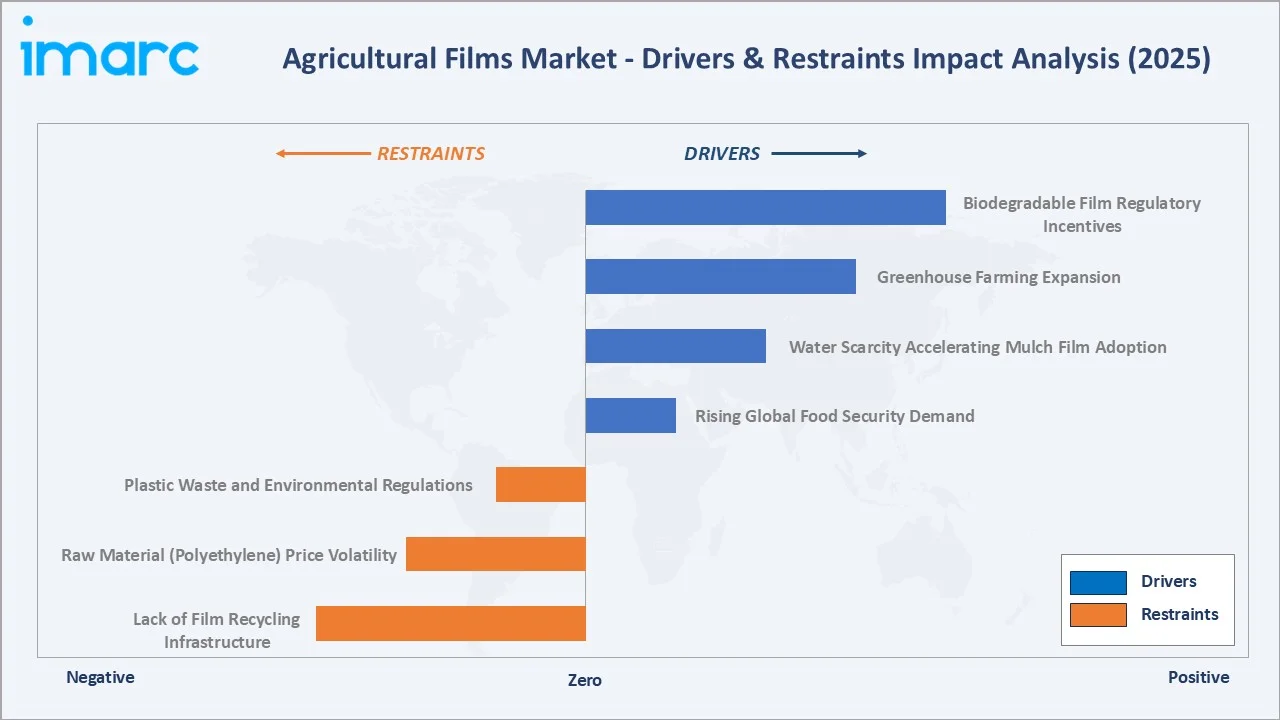

Market Drivers

- Rising Global Food Security Demand: The global population is projected to reach 9.8 Billion by 2050, requiring an approximately 70% increase in food production from current levels. Agricultural films are among the most cost-effective available tools for yield intensification; mulch films increase crop yields by 15–50%, and greenhouse films extend growing seasons by 2–4 months.

- Water Scarcity Accelerating Mulch Film Adoption: According to UNICEF, by 2030, severe water scarcity could displace approximately 700 million people worldwide. Mulch films reduce water use by 25-50% per crop cycle, savings that are economically critical in water-stressed regions.

- Greenhouse Farming Expansion: The global protected agriculture market, encompassing greenhouses, polytunnels, and shade houses, is growing at approximately 6% annually, driven by urbanization, consumer demand for year-round fresh produce, and the economics of controlled-environment agriculture that delivers 10–15× higher yield per hectare than open-field production.

- Biodegradable Film Regulatory Incentives: EU Directives and China's Agricultural Film Recycling Law (effective 2020) are creating regulatory demand for biodegradable mulch film alternatives in high-application-intensity markets.

Market Restraints

- Plastic Waste and Environmental Regulations: Agricultural film plastic waste, where China alone generates approximately 2.5 million tons of plastic film waste annually, is a major environmental management challenge. EU Single-Use Plastics Directive requirements and China's agricultural plastic recovery mandates are creating compliance costs and procurement preference shifts that constrain market growth for conventional PE agricultural films.

- Raw Material (Polyethylene) Price Volatility: LLDPE and LDPE prices are directly correlated with ethylene feedstock costs, which fluctuate with crude oil and natural gas prices. Ethylene price swings in 2020–2022 caused equivalent agricultural film price movements that compressed converter margins and disrupted farmer procurement planning.

- Lack of Film Recycling Infrastructure: Despite growing policy requirements, practical infrastructure for collecting and recycling agricultural films from farm locations is extremely limited, particularly in Asia and Latin America. Film contamination with soil, crop residues, and agrochemicals makes recycling technically challenging.

Market Opportunities

- Biodegradable and Bio-Based Film Development: The biodegradable agricultural film market is growing at ~12% annually and represents a premium-priced growth segment within the broader agricultural film market.

- Silage Film Demand Growth in Emerging Markets: Rising global meat consumption is driving dairy and beef cattle expansion across Latin America, Southeast Asia, and the Middle East, creating growing demand for silage bale wrap and silage pit cover films.

Market Challenges

- Competition from Alternative Technologies: Biodegradable paper mulches, weed fabric textiles, and drip tape-integrated mulch systems are gaining adoption in premium organic and specialty crop farming segments, creating substitute competition for conventional PE mulch films in markets where environmental labelling and organic certification requirements constrain plastic use.

- Agricultural Film Recovery Logistics: The physical characteristics of used agricultural film create fundamental logistics challenges for collection and recycling programs. Overcoming these barriers requires coordinated industry investment in farm collection points, mechanical cleaning systems, and film-to-film recycling capacity that is not yet economically self-sustaining in most markets.

Emerging Market Trends

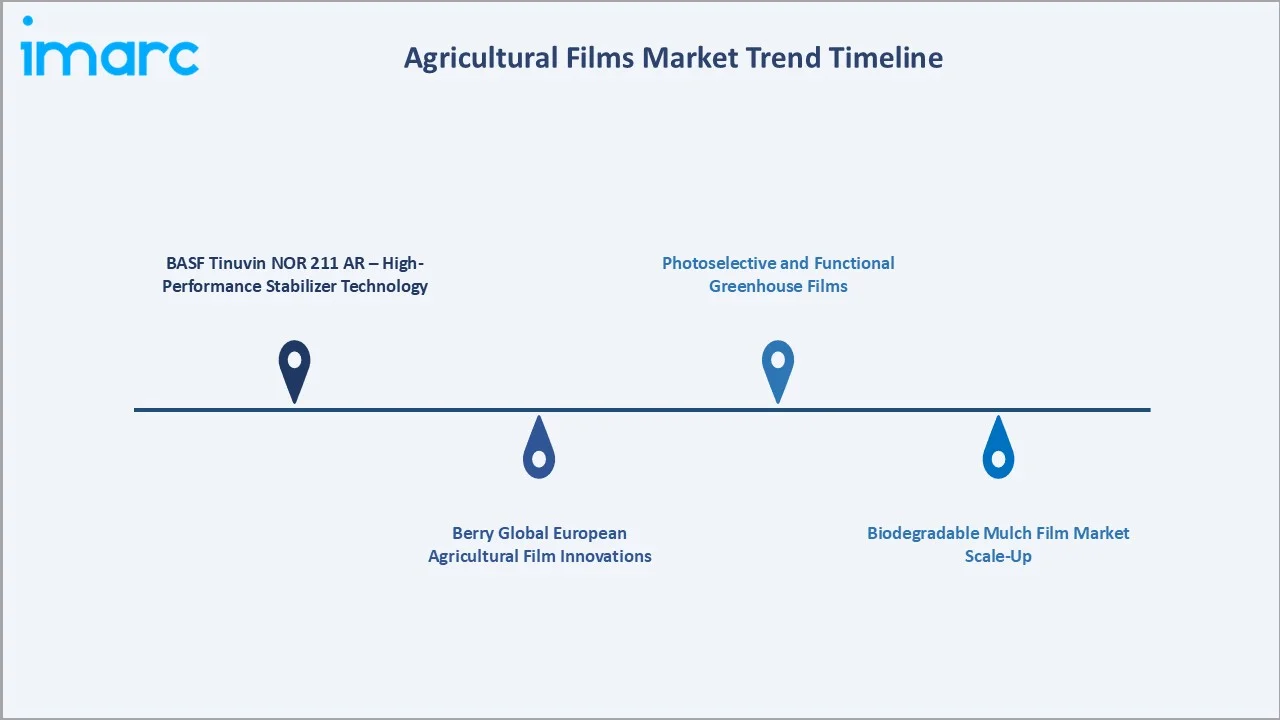

1. BASF Tinuvin NOR 211 AR – High-Performance Stabilizer Technology

In July 2024, BASF launched Tinuvin NOR 211 AR, a new high-performance hindered amine light stabilizer (HALS) developed specifically to support agricultural film converters and resin producers globally in creating films with extended field lifetimes and superior agrochemical resistance.

2. Berry Global European Agricultural Film Innovations

In March 2024, Berry Global's (now part of Amcor plc) European flexible films division showcased its latest agricultural film developments at AMI events in Barcelona and Valencia, presenting new barrier silage films, sustainable greenhouse covers incorporating recycled content, and novel biodegradable mulch film formulations.

3. Biodegradable Mulch Film Market Scale-Up

China's Agricultural Film Recycling Law and EU Directive requirements are accelerating biodegradable mulch film market development. Novamont S.p.A.’s Mater-Bi platform, BASF's ecovio compound, and domestic Chinese PBAT/PLA producers are scaling production to meet growing demand from government-mandated and voluntary-market biodegradable film programs.

4. Photoselective and Functional Greenhouse Films

Wavelength-selective greenhouse films, incorporating photoluminescent dyes that convert UV to PAR (photosynthetically active radiation) wavelengths, NIR-blocking pigments for summer cooling, and blue-light enhancement for vegetative growth promotion, are growing at 8–10% annually in Japan, South Korea, and the Netherlands.

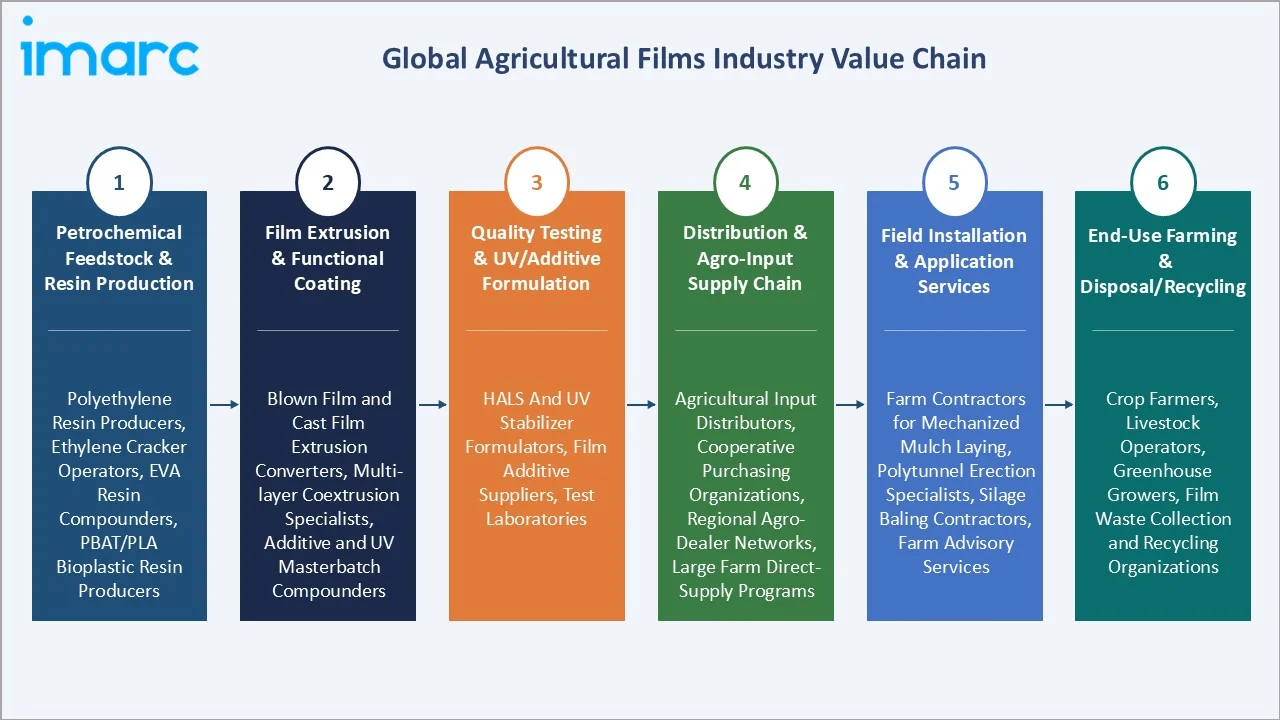

Industry Value Chain Analysis

The agricultural films value chain extends from petrochemical raw material production through functional film manufacturing, agro-input distribution, farm-level deployment, and end-of-life management, with each stage presenting distinct competitive dynamics.

| Stage | Key Players / Examples |

|---|---|

| Petrochemical Feedstock & Resin Production | Polyethylene resin producers, ethylene cracker operators, EVA resin compounders, PBAT/PLA bioplastic resin producers |

| Film Extrusion & Functional Coating | Blown film and cast film extrusion converters, multi-layer coextrusion specialists, additive and UV masterbatch compounders |

| Quality Testing & UV/Additive Formulation | HALS and UV stabilizer formulators, film additive suppliers, test laboratories |

| Distribution & Agro-Input Supply Chain | Agricultural input distributors, cooperative purchasing organizations, regional agro-dealer networks, large farm direct-supply programs |

| Field Installation & Application Services | Farm contractors for mechanized mulch laying, polytunnel erection specialists, silage baling contractors, farm advisory services |

| End-Use Farming & Disposal/Recycling | Crop farmers, livestock operators, greenhouse growers, film waste collection and recycling organizations |

Technology Landscape in the Agricultural Films Industry

Linear Low-Density Polyethylene Film Technology

Linear low-density polyethylene films constitute the dominant agricultural film material at 49.7%. Produced through metallocene or Ziegler-Natta-catalyzed ethylene-alpha olefin copolymerization, LLDPE delivers the flexibility, strength, and processability required for mulch, silage, and greenhouse applications. Modern metallocene-LLDPE grades enable 15–25% film downgauging versus conventional LLDPE, reducing material costs while maintaining field performance.

Mulch Film Functional Technologies

Modern mulch films incorporate black/colored pigments for weed suppression, HALS/UV stabilizers for controlled service life, antioxidants for thermal stability, and IRT dyes for wavelength-selective weed control. Biodegradable mulch films use PBAT/PLA blends as the matrix polymer, delivering controlled soil degradation of 90–180 days under composting or field conditions.

Greenhouse Film Multi-Layer Technology

Advanced greenhouse covers are manufactured as 3–7 layer coextruded structures with LLDPE/EVA skins combined with thermal IR retention additives for nighttime heat retention, anti-fog surfactants that convert condensation to sheet flow, UV-diffusion agents for uniform crop illumination, and multi-season HALS stabilization packages for 3–5 year service lifetimes.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Linear Low-Density Polyethylene | 49.7% | 2025 |

| Application | Mulching | 44.7% | 2025 |

| Region | Asia Pacific | 46.9% | 2025 |

By Type

Linear low-density polyethylene leads with a 49.7% market share in 2025. Its dominance spans all three primary application categories, mulch, greenhouse, and silage wrap, where its superior stretch recovery and puncture resistance versus LDPE justify its higher resin cost.

To access detailed market analysis, Request Sample

Low-density polyethylene at 21.6% remains widely used in standard greenhouse tunnels and low-cost mulch applications, particularly in developing market agricultural sectors. High-density polyethylene at 13.8% serves weed control fabric and heavy-duty mulch applications. EVA (Ethylene Vinyl Acetate) at 8.9% is the premium greenhouse film material, offering superior flexibility at low temperatures and higher IR retention versus pure LLDPE.

By Application

Mulching leads at 44.7%, the single largest agricultural film application globally. Plastic mulch films are deployed on ~20 million hectares worldwide, with the largest deployments in China, Europe, and North America. Mulch films generate consistent annual replacement demand as most products are single-season, creating a large recurring aftermarket that provides revenue stability for manufacturers.

Greenhouse films at 31.5% serve the 5+ million hectares of protected cropping area worldwide with 2–5 year service life greenhouse covers. Silage films at 15.6% serve the global livestock industry's forage preservation requirements; silage bale wrap and pit cover films are growing with expanding dairy and beef cattle operations in Latin America and Asia.

Regional Market Insights

Asia Pacific dominates the global agricultural films market with a 46.9% share in 2025. China's dominant position as both the world's largest agricultural film producer and consumer, deploying over 1.2 million tons annually across mulch, greenhouse, and silage applications, anchors the region's leadership.

Europe's 21.8% share is driven by Mediterranean countries Spain, Italy, and France, which collectively represent the highest per-hectare plastic mulch intensity in the world outside of China. Spain's Almería greenhouses are estimated to produce between 2.5 million and 3.5 million tons of fruits and vegetables annually.

| Region | Share (2025) | Key Growth Drivers |

|---|---|---|

| Asia Pacific | 46.9% | Massive mulch and greenhouse film deployment, expanding horticulture sector, government subsidies for plastic mulching in water-scarce regions |

| Europe | 21.8% | Mediterranean intensive horticulture, biodegradable film regulatory demand, greenhouse flower and vegetable production, sustainable film innovation |

| North America | 17.6% | Berry and vegetable mulch film demand, greenhouse tomato and pepper production, silage film growth with expanding dairy sectors, organic farm film market development |

| Latin America | 8.1% | Vegetable mulch adoption, expanding berry and grape production, growing dairy silage film demand with intensifying livestock operations |

| Middle East & Africa | 5.6% | Water scarcity driving drip-tape integrated mulch adoption, greenhouse food security investment programs, expanding horticulture export production |

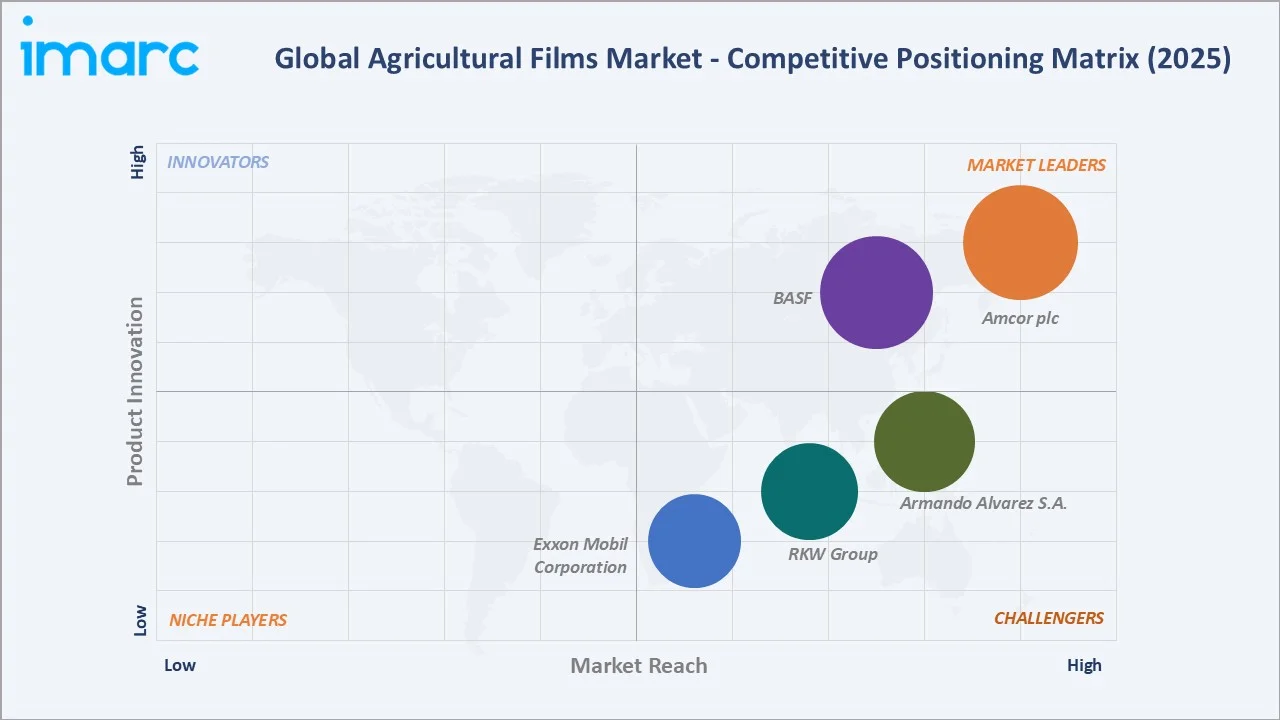

Competitive Landscape

The global agricultural films converting market is fragmented, with 200+ film manufacturers globally, but concentrated at the resin level where major petrochemical producers dominate linear low-density polyethylene and low-density polyethylene supply.

| Company Name | Brand | Market Position | Core Strength |

|---|---|---|---|

| Amcor plc | Parafilm, Silotite, Panda, Total Blockade, Silotite Pro, Baletite | Market Leader | Largest agricultural film portfolio, specialty silage and mulch films, European sustainable film innovations, scale manufacturing efficiency |

| BASF | ecovio, Irganox, Tinuvin NOR 211 AR | Market Leader | Tinuvin HALS/UV stabilizer systems for film producers, ecovio biodegradable compound |

| Armando Alvarez S.A. | Alvaguard, Silvalac, Indasol/Durasol, TRC/Aster, Reytec/Reysun, Reyfilm, Solplast Mulch, Sotrafilm, among others | Strong Challenger | European greenhouse and mulch film leadership, Mediterranean market expertise, multilayer coextrusion capabilities |

| RKW Group | e7 Hytibag, Hermetix, Polydress, Rondotex | Strong Challenger | High-performance mulch and greenhouse films, European biodegradable film development, precision agricultural film solutions |

| Exxon Mobil Corporation | Exceed, Enable, Escorene | Challenger | EXCEED and ENABLE mLLDPE resin platforms, high-performance film resin technology, global petrochemical supply network |

Amcor plc and BASF lead through resin technology differentiation, proprietary additive systems, and global production networks.

Key Company Profiles

Amcor plc

Amcor plc is one of the world's largest producers of agricultural plastic films. Its global agricultural films business spans silage wrap, mulch films, greenhouse covers, and crop protection films, served through manufacturing facilities across North America, Europe, and Asia-Pacific.

- Product Portfolio: Parafilm, Silotite, Panda, Total Blockade, Silotite Pro, and Baletite.

- Recent Developments: In April 2026, Amcor announced the investment of multi-million euros in a new flexographic printing line at its Hardenberg, Netherlands facility to expand industrial and agricultural film packaging capabilities in Europe. Expected to be fully operational in autumn 2026, the line will add capacity for up to 6,000 tons of packaging annually while supporting material-efficient, recycle-ready solutions.

- Strategic Focus: Agricultural film sustainability transformation, silage wrap technology leadership in Europe, expansion of specialty functional greenhouse film offerings, and agricultural film collection and recycling program development.

BASF

BASF is also a leading supplier of polymer additives and biodegradable film compounds to the agricultural film industry. BASF's contribution spans performance additive systems that extend film service life, and ecovio, which is BASF's biodegradable polymer compound enabling certified compostable agricultural mulch films.

- Product Portfolio: Tinuvin NOR 211 AR and Tinuvin 622 HALS stabilizers for agricultural film producers; ecovio biodegradable mulch film compound; Irganox antioxidant stabilizer systems; specialty functional coatings for controlled-environment agriculture applications.

- Recent Developments: In February 2026, BASF showcased advanced plastic additives at Plastindia 2026, including Tinuvin NOR stabilizers that enhance the durability and performance of mulch and greenhouse films under heat, sunlight, and chemical exposure.

- Strategic Focus: High-performance agricultural film additive system development, ecovio biodegradable film compound market expansion in China and EU, sustainability-driven formulation innovation supporting circular economy agricultural film programs.

Market Concentration Analysis

The agricultural films converting market is moderately fragmented, with an estimated 200+ film manufacturers globally. Amcor plc, BASF, Armando Alvarez S.A., and RKW Group collectively hold approximately 35–40% of global agricultural film converting revenue.

However, the upstream resin market is highly concentrated: Dow, ExxonMobil, SABIC, and LyondellBasell collectively supply approximately 70% of global LLDPE and LDPE resin used in agricultural film production.

The competitive landscape is bifurcating between cost-competitive PE film producers and innovation-led suppliers developing functional, biodegradable, and sustainable solutions commanding 20–50% premiums. M&A consolidation among European converters is accelerating, driven by biodegradable film investment requirements and sustainability compliance costs.

Investment & Growth Opportunities

Fastest Growing Segments

Biodegradable mulch films (~12% CAGR), functional greenhouse films (8–10% CAGR), silage bale wrap in emerging markets (~5.5% CAGR), and mulching films in water-scarce regions represent the highest-growth investment vectors through 2034. Together, these sub-segments address a combined incremental addressable market of approximately USD 4 Billion by 2034.

Emerging Market Expansion

India's ambitious expansion of protected horticulture under the National Horticulture Mission, targeting 500,000+ hectares of new greenhouse and tunnel cultivation by 2030, represents a USD 800 Million+ agricultural film opportunity by 2034. Sub-Saharan Africa's growing export horticulture industry, particularly in Kenya, Ethiopia, and Senegal, is creating new demand for greenhouse and mulch film installations supported by development finance institutions.

Venture and Institutional Investment Trends

- Agricultural film collection and recycling programs are receiving EU and member-state government co-funding as Extended Producer Responsibility (EPR) frameworks are implemented, creating infrastructure investment opportunities in film washing, sorting, and PE regrind processing facilities.

- Smart greenhouse film companies incorporating IoT-connected optical sensors, data-driven light management, and precision climate control are attracting agtech venture investment that bridges agricultural film and digital farming markets.

Future Market Outlook (2026-2034)

The global agricultural films market is positioned for consistent, broadly-based growth through 2034. From USD 12.25 Billion in 2025, the market will reach USD 18.56 Billion by 2034, representing incremental value of USD 6.31 Billion at a 4.59% CAGR. Growth will be anchored by the non-discretionary yield and resource efficiency benefits of agricultural films across all farming systems, combined with regulatory-driven demand growth for biodegradable and sustainable film alternatives.

The technology composition will shift meaningfully toward functional, biodegradable, and recycled-content films through 2034, as EU biodegradable mulch mandates, China's film recovery law, and corporate sustainability commitments from food retailers reshape the acceptable film specifications in key markets. Conventional PE mulch films will retain market dominance in volume terms, but the value share of premium functional and sustainable products will grow significantly.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants in 2024–2025, including agricultural film manufacturers, polyethylene resin producers, agro-input distributors, greenhouse operators, and crop farmers across Asia Pacific, Europe, North America, and Latin America. Expert input validated market sizing, technology trends, and regional demand dynamics.

Secondary Research

Secondary research encompassed manufacturer annual reports, FAO food production statistics, European Bioplastics biodegradable film reports, China National Agricultural Film Industry Association data, and trade publications including Plastics Technology, Packaging Europe, and Agri-Film industry journals.

Forecasting Models

Market size estimations used top-down and bottom-up forecasting incorporating global agricultural land use data, plastic mulch penetration rates by crop type and region, greenhouse area expansion projections, silage film consumption per head of livestock, and average film selling price trajectories. A base-case CAGR of 4.59% reflects consensus validated against manufacturer capacity expansion plans and regional agricultural investment programs.

Agricultural Films Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Types Covered |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Low-Density Polyethylene, Linear Low-Density Polyethylene, High-Density Polyethylene, Ethylene Vinyl Acetate, Others |

| Applications Covered | Greenhouse, Silage, Mulching, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Amcor plc, BASF, Armando Alvarez S.A., RKW Group, Exxon Mobil Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the agricultural films market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global agricultural films market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the agricultural films industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Agricultural Films Market Report

The market reached USD 12.25 Billion in 2025 and is projected to grow to USD 18.56 Billion by 2034 at a 4.59% CAGR.

Asia Pacific leads with a 46.9% share in 2025, dominated by China's massive mulch and greenhouse film deployment and India's expanding horticulture sector.

Linear low-density polyethylene leads at 49.7% in 2025, preferred for its superior stretch, puncture resistance, and compatibility with high-performance multi-layer film coextrusion.

Mulching leads at 44.7% in 2025, deployed on 20+ million hectares globally for weed suppression, soil temperature regulation, and irrigation water conservation.

Amcor plc, BASF, Armando Alvarez S.A., RKW Group, and Exxon Mobil Corporation are some of the leading players in the market.

Rising global food security demand, water scarcity driving mulch adoption, greenhouse farming expansion, and biodegradable film regulatory incentives are the primary drivers.

Plastic waste regulations, polyethylene raw material price volatility, and lack of agricultural film recycling infrastructure are the key challenges.

Mulching is the fastest growing application at approximately 5.10% CAGR, driven by intensive vegetable farming expansion in water-scarce regions globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade