Agriculture Sprayers Market Size, Share, Trends and Forecast by Type, Source of Power, Usage, and Region, 2026-2034

Agriculture Sprayers Market Size, Share, Trends & Forecast (2026-2034)

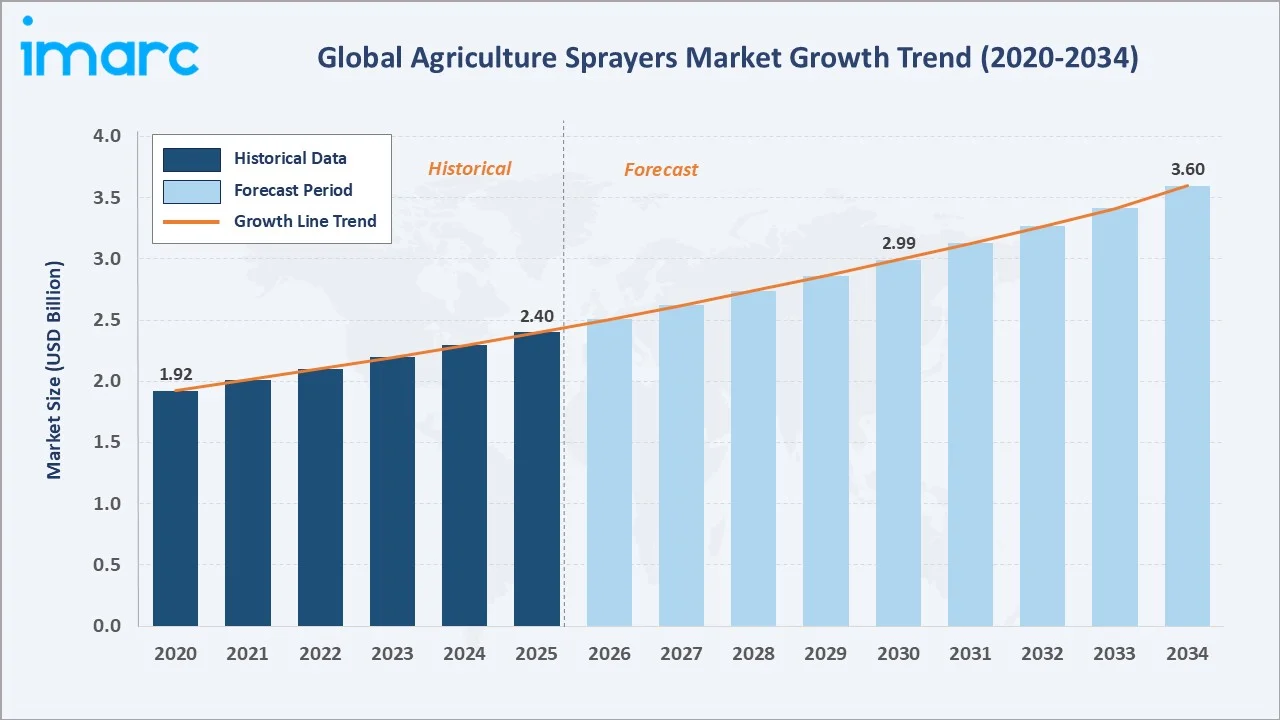

The global agriculture sprayers market reached USD 2.40 Billion in 2025 and is projected to reach USD 3.60 Billion by 2034, growing at a CAGR of 4.51% during 2026-2034. Growth is driven by rising crop protection demand, precision agriculture adoption, battery-operated sprayer proliferation, and government mechanization subsidies.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 2.40 Billion |

| Forecast Market Size (2034) | USD 3.60 Billion |

| CAGR (2026-2034) | 4.51% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

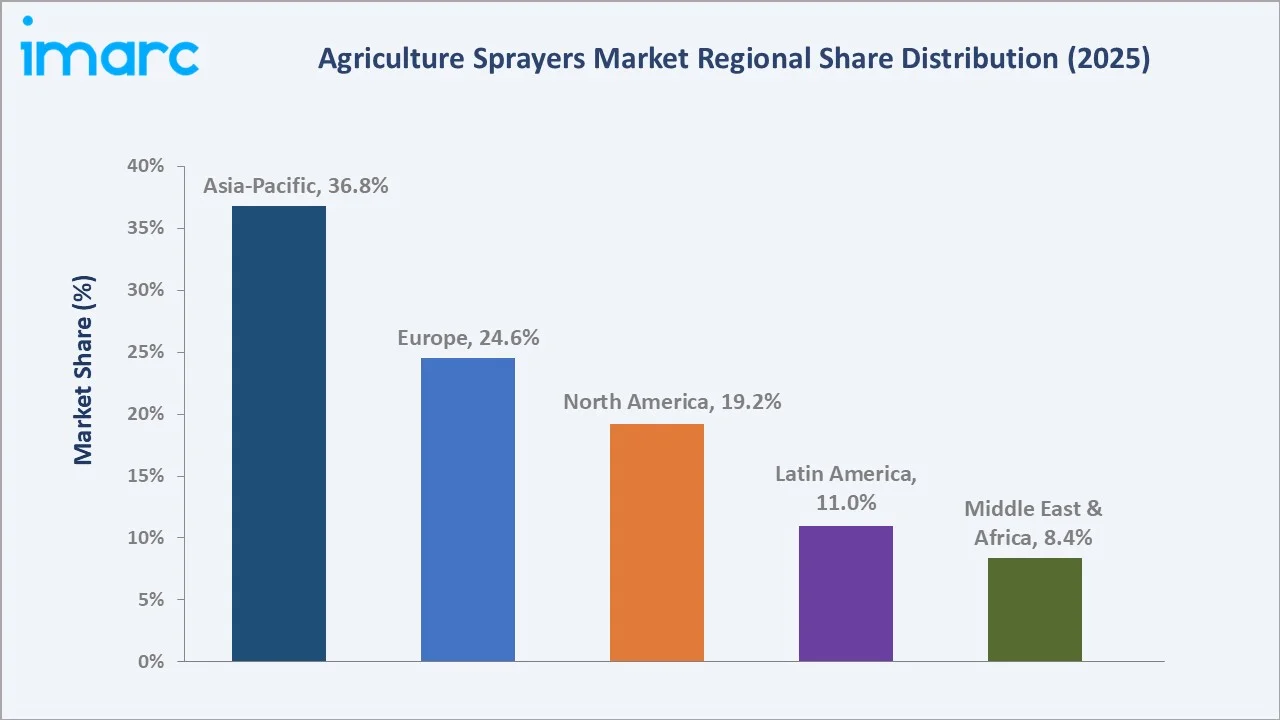

Asia-Pacific's 36.8% dominance is underpinned by India and China's vast smallholder farming populations, rapid battery knapsack sprayer adoption, and growing agricultural drone deployments. High-pressure sprayers lead the type segment due to their broad applicability across row crops, orchards, and specialty crops where high-pressure uniform coverage is essential for effective pesticide and fertilizer delivery.

To get more information on this market, Request Sample

The market's 4.51% CAGR reflects non-discretionary crop protection requirements across global farmland. With crop losses from pests, diseases, and weeds estimated at 20–40% of potential yield, sprayer equipment represents one of farming's highest-ROI capital investments, sustaining demand across all economic cycles and farming scales.

Executive Summary

The global agriculture sprayers market is on a steady growth trajectory, driven by crop protection demand, precision agriculture adoption, and a technology transition toward battery, solar, and drone-based platforms. From USD 2.40 Billion in 2025, the market will reach USD 3.60 Billion by 2034, generating USD 1.20 Billion in incremental value at a 4.51% CAGR.

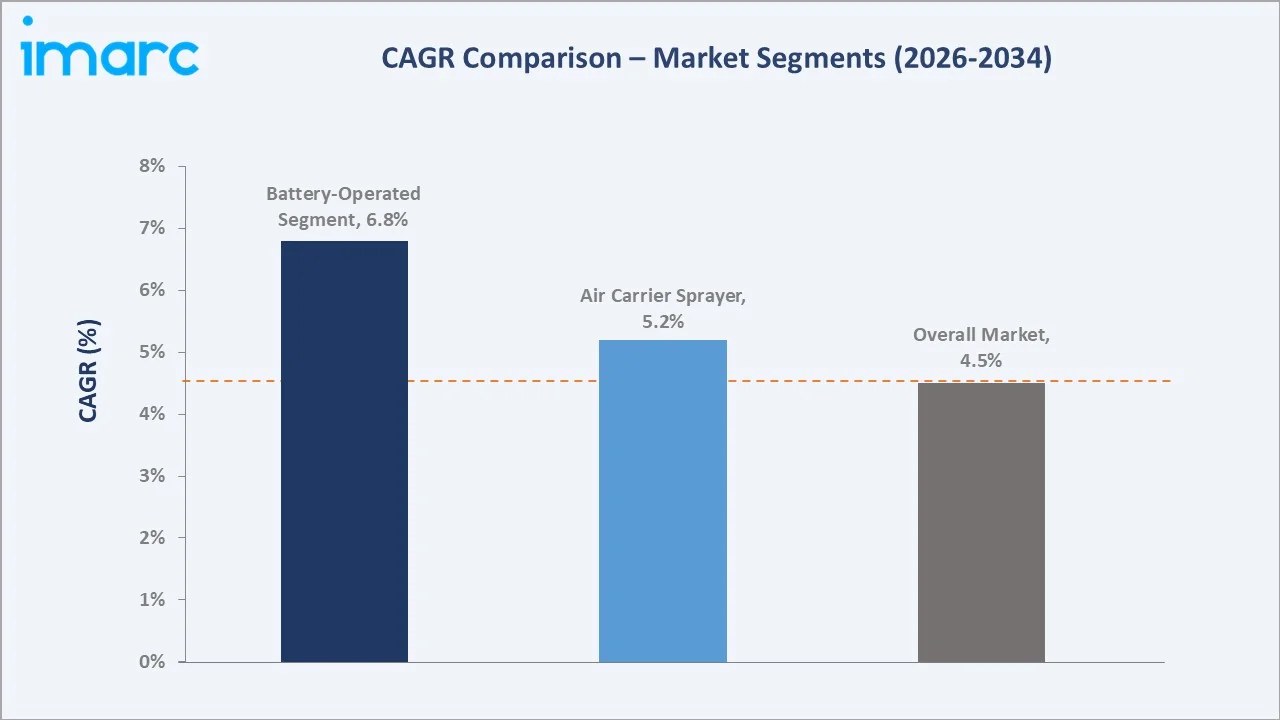

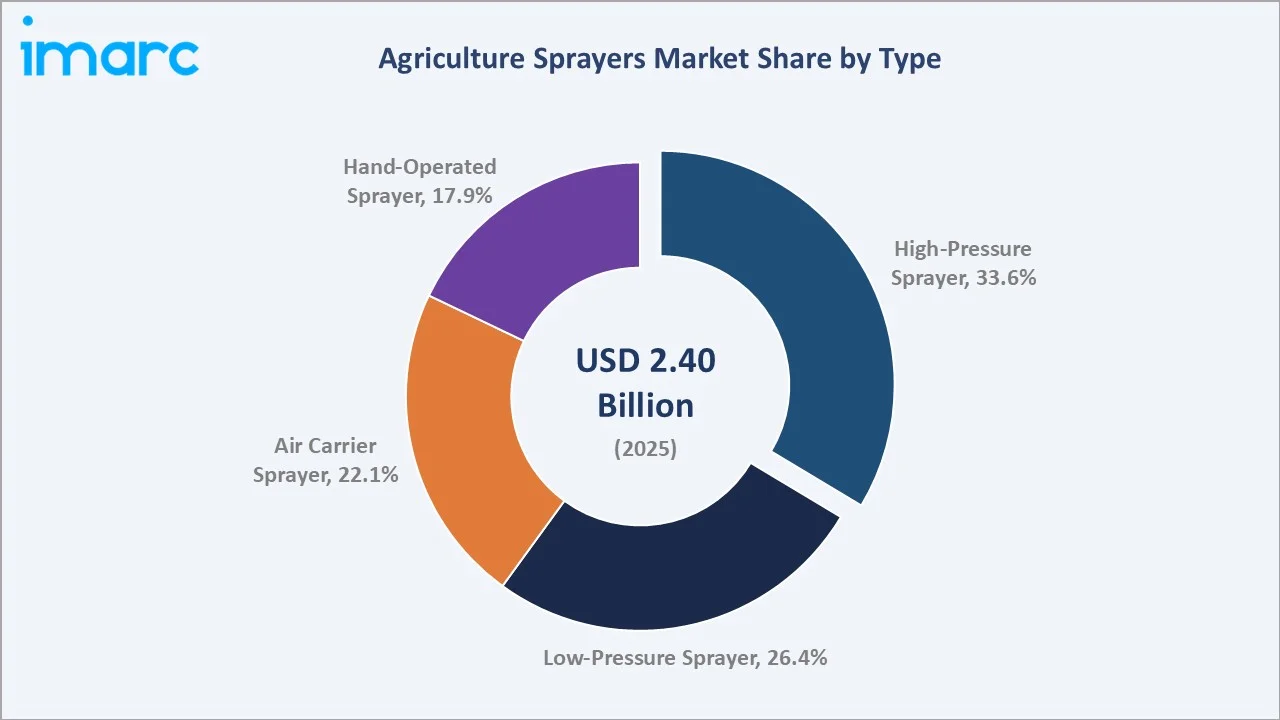

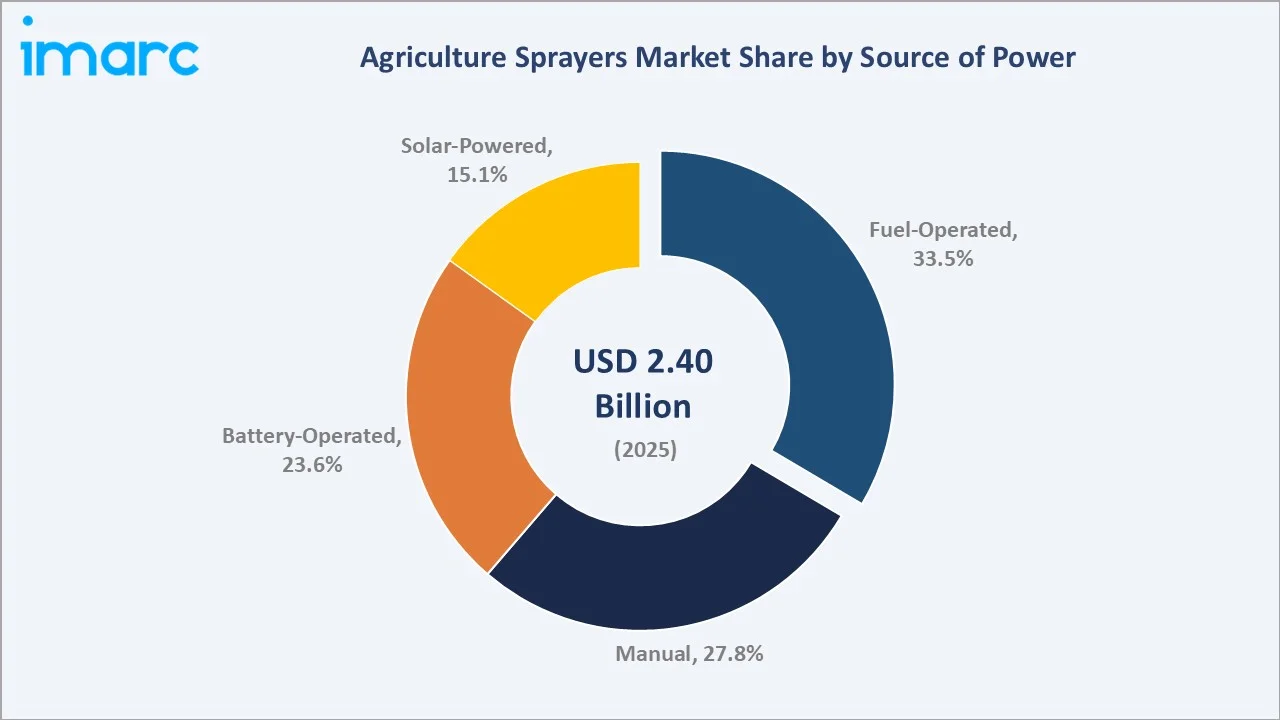

High-pressure sprayers lead the type segment at 33.6%, serving large-scale commercial farming globally. Battery-operated power sources at 23.6% are growing fastest at approximately 6.80% CAGR, propelled by the rapid proliferation of rechargeable knapsack sprayers across India, Southeast Asia, and Sub-Saharan Africa, where grid access is improving but fuel supply chains remain unreliable.

Key players, including AGCO Corporation, Deere & Company, CNH Industrial N.V., KUBOTA Corporation, and EXEL Industries, compete through product portfolio breadth, precision application technology, global dealer networks, and autonomous and AI-powered spraying system development.

Key Market Insights

| Insight | Data |

|---|---|

| Largest Sprayer Type | High-Pressure Sprayer – 33.6% share (2025) |

| Fastest Growing Type | Air Carrier Sprayer – ~5.20% CAGR (drone integration) |

| Largest Power Source | Fuel-Operated – 33.5% share (2025) |

| Fastest Growing Power Source | Battery-Operated – ~6.80% CAGR (2026-2034) |

| Leading Region | Asia-Pacific – 36.8% share (2025) |

| Top Companies | AGCO Corporation, Deere & Company, CNH Industrial N.V., KUBOTA Corporation, EXEL Industries |

Key Analytical Observations:

- High-pressure sprayers command a 33.6% share (2025), serving the broadest range of agricultural applications. Operating at 10–300 PSI, these systems deliver fine atomization for dense canopy penetration.

- Battery-operated sprayers at 23.6% (2025) are growing fastest at approximately 6.80% CAGR. Declining lithium-ion costs, expanding rural electrification, and farmer preference for emission-free operation are driving adoption.

- Fuel-operated sprayers retain a 33.5% share (2025) anchored by the large installed base of tractor-mounted and self-propelled diesel machines in North America, Europe, and Latin America.

- Solar sprayers at 15.1% (2025) share address off-grid rural markets where neither reliable electricity nor fuel supply exists. Solar-charging integrated backpack sprayers extending battery operating time by 20–30% during daylight hours are gaining adoption in Sub-Saharan Africa and South Asia, driving the solar segment's ~4.90% CAGR.

Agriculture Sprayers Market Overview

Agriculture sprayers are mechanical devices used to apply liquid solutions, pesticides, herbicides, fungicides, and liquid fertilizers to crops, soil, and livestock. They range from hand-operated pump units for subsistence farmers to GPS-guided self-propelled machines and UAV drone sprayers covering thousands of hectares.

The market spans four primary categories: high-pressure field sprayers, low-pressure orchard sprayers, air carrier sprayers for dense canopies, and hand-operated knapsack sprayers.

The market is undergoing fundamental transformation from manual and fuel-powered systems to precision, sensor-equipped, connected platforms. Variable Rate Application (VRA), GPS boom section control, and real-time canopy sensing enable chemical reduction with improved application accuracy.

Drone sprayers, while still a small volume share, are growing rapidly in Asia-Pacific, where regulatory frameworks are established, and pilot programs demonstrate operational advantages.

Market Dynamics

To evaluate market opportunities, Request Sample

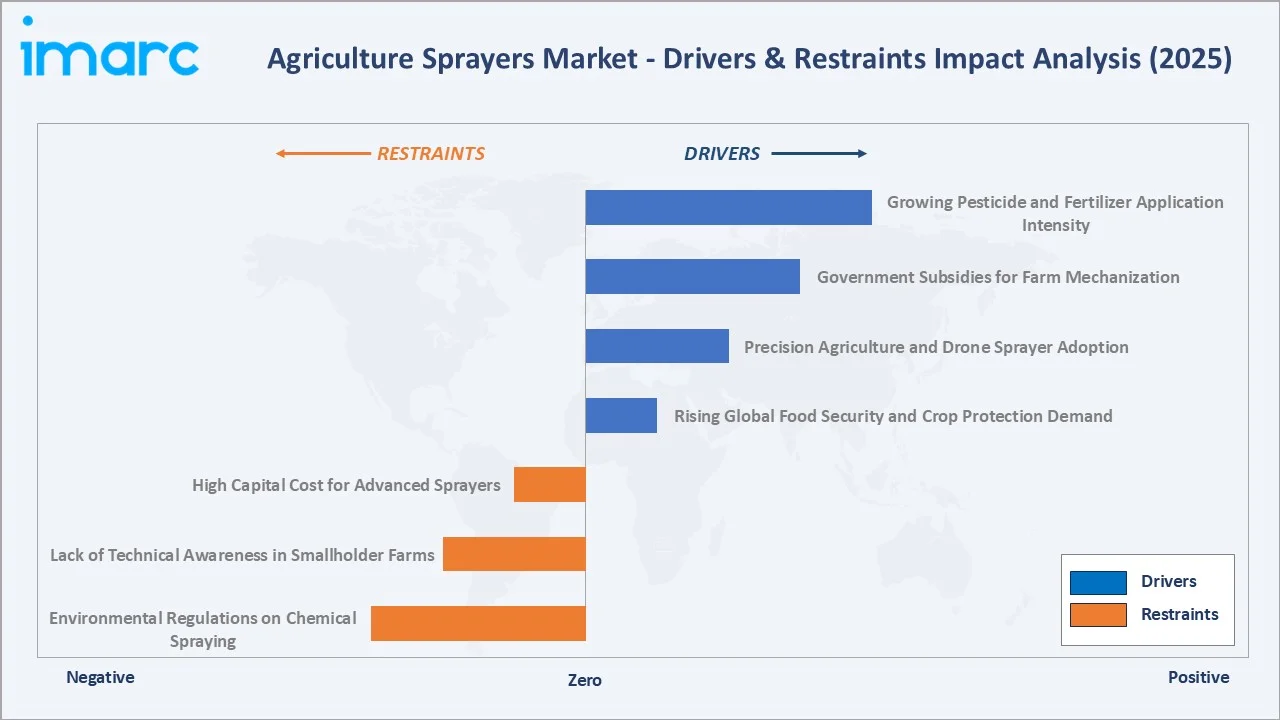

Market Drivers

- Rising Global Food Security and Crop Protection Demand: With crop losses from pests, diseases, and weeds estimated at 20–40% of potential yield globally, crop protection investment generates returns of USD 6.5 per dollar spent. Growing incidence of new pest threats is increasing spraying frequency per crop cycle, driving consistent sprayer equipment demand across all farm-scale categories.

- Precision Agriculture and Drone Sprayer Adoption: Precision agriculture is expected to grow at 9.8% from 2026-2034, with GPS-guided VRA systems and boom section control becoming standard on new commercial sprayers.

- Government Subsidies for Farm Mechanization: India's Sub-mission on Agriculture Mechanization provides 50-80% subsidies on agriculture machinery prices for small and marginal farmers, with state-level top-ups in major farming states. China's agricultural subsidy system similarly supports equipment purchases.

- Growing Pesticide and Fertilizer Application Intensity: The global agrochemicals market size was valued at USD 307.2 Billion in 2025, and it is expected to reach USD 406.2 Billion by 2034. As high-value specialty crop acreage expands globally, per-hectare application intensity and sprayer utilization rates increase, directly driving equipment demand.

Market Restraints

- High Capital Cost for Advanced Sprayers: Backpack sprayers typically cost USD 50–500, while tractor-mounted boom sprayers range from USD 5,000–25,000 and UAV/drone sprayers from USD 3,000 to over USD 20,000. This is constraining adoption among medium-scale farmers in developing markets where agricultural lending infrastructure is limited.

- Lack of Technical Awareness in Smallholder Farms: Effective sprayer use requires understanding nozzle selection, pressure, travel speed, and chemical mixing protocols. In developing markets, limited access to agronomic advisory services results in suboptimal application practices that reduce perceived ROI and constrain willingness to invest in higher-specification equipment.

- Environmental Regulations on Chemical Spraying: EU Sustainable Use of Pesticides Directive, buffer zone requirements, and precision application mandates impose compliance costs on conventional broadcast spray equipment. Restrictions near water bodies and populated areas in European jurisdictions require investment in drift-reduction nozzles and operator exposure controls, adding system complexity and cost.

Market Opportunities

- Agricultural Drone Sprayer Global Expansion: The agricultural drone sprayer market (~USD 3,463.8 Million, growing at 26.85% during 2026-2034) is expanding as regulatory frameworks develop in India, Brazil, the US, and Europe.

- Smart Connectivity and IoT-Enabled Sprayer Services: Connected sprayer platforms generating application data for farm management software, enabling remote diagnostics and compliance reporting, are creating subscription-based software revenue streams for manufacturers.

Market Challenges

- Dealer Network Gaps in Remote Regions: Agricultural sprayer maintenance requires trained technicians, spare parts, and calibration equipment. In remote farming regions of Sub-Saharan Africa, Central Asia, and Pacific Islands, the absence of service networks constrains adoption of technically complex sprayers, limiting viable commercial products to simpler hand-operated and basic battery-operated models.

- Calibration and Training Requirements: Modern precision sprayers require regular calibration of nozzles, flow meters, and section control systems to maintain application accuracy. This operational complexity creates barriers for farmers transitioning from manual to mechanized crop protection, requiring sustained technical support investment from manufacturers and distributors.

Emerging Market Trends

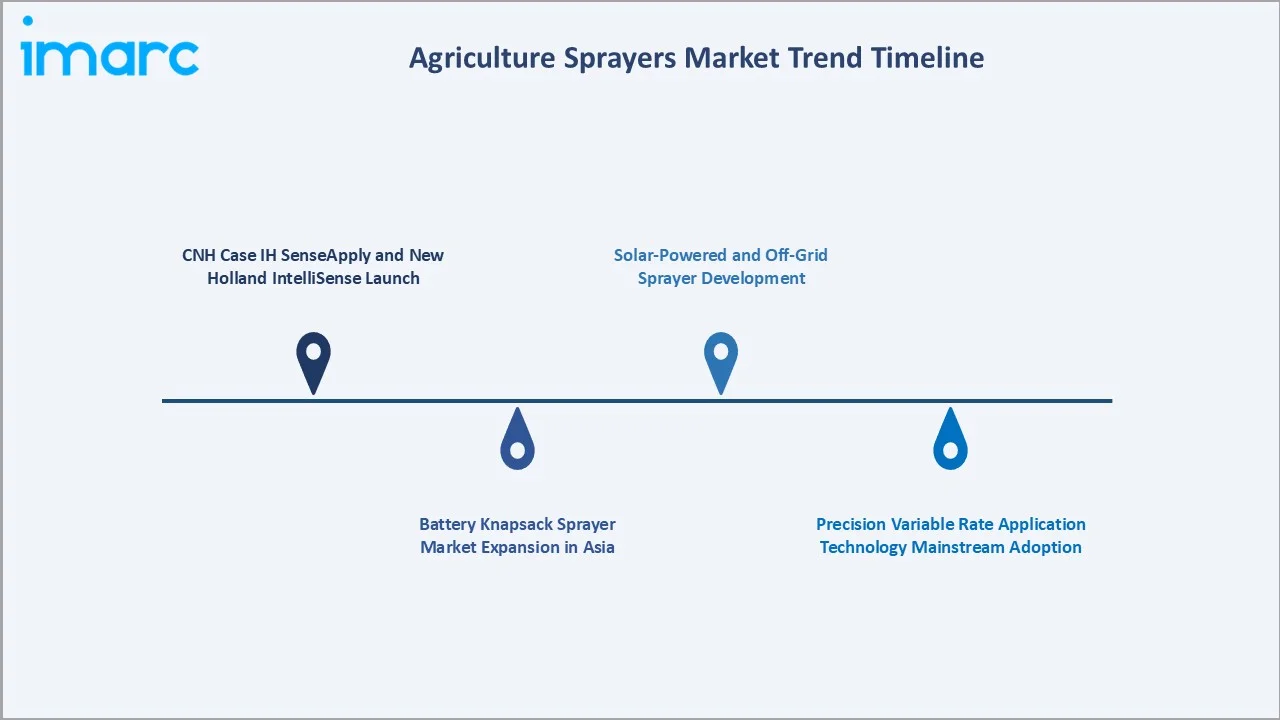

1. CNH Case IH SenseApply and New Holland IntelliSense Launch

CNH introduced built-in AI-powered sprayer technology across its Case IH, New Holland and Miller sprayer portfolios, combining machine learning and cameras for real-time crop analysis and automated spraying. The system identifies weeds on bare soil and precisely applies water, herbicides and fertilizers, helping farmers reduce chemical use and input costs while improving productivity and sustainability.

2. Battery Knapsack Sprayer Market Expansion in Asia

The battery-operated agricultural sprayer market in Asia-Pacific is experiencing structural growth as lithium-ion battery costs decline and rural electrification expands. Chinese manufacturers producing 16–20 liter rechargeable knapsack sprayers at USD 50–80 are displacing fuel-powered alternatives across India, Bangladesh, Vietnam, and Indonesia.

3. Precision Variable Rate Application Technology Mainstream Adoption

Variable Rate Application (VRA) with individual nozzle pulse-width modulation and GPS prescription maps is transitioning from premium-only to standard specification on new commercial self-propelled sprayers in North America and Europe. John Deere's See & Spray and AGCO's Fendt Rogator 900 series represent the current commercial state of the art.

4. Solar-Powered and Off-Grid Sprayer Development

Solar-integrated sprayer systems, combining photovoltaic panels with battery packs for continuous off-grid operation, are growing at approximately 8–10% annually in Sub-Saharan Africa, South Asia, and Pacific farming regions where consistent fuel supply and grid access remain unreliable. These systems address the 15.1% solar sprayer segment, which is growing to serve smallholder farmers globally who currently lack access to reliable mechanized crop protection.

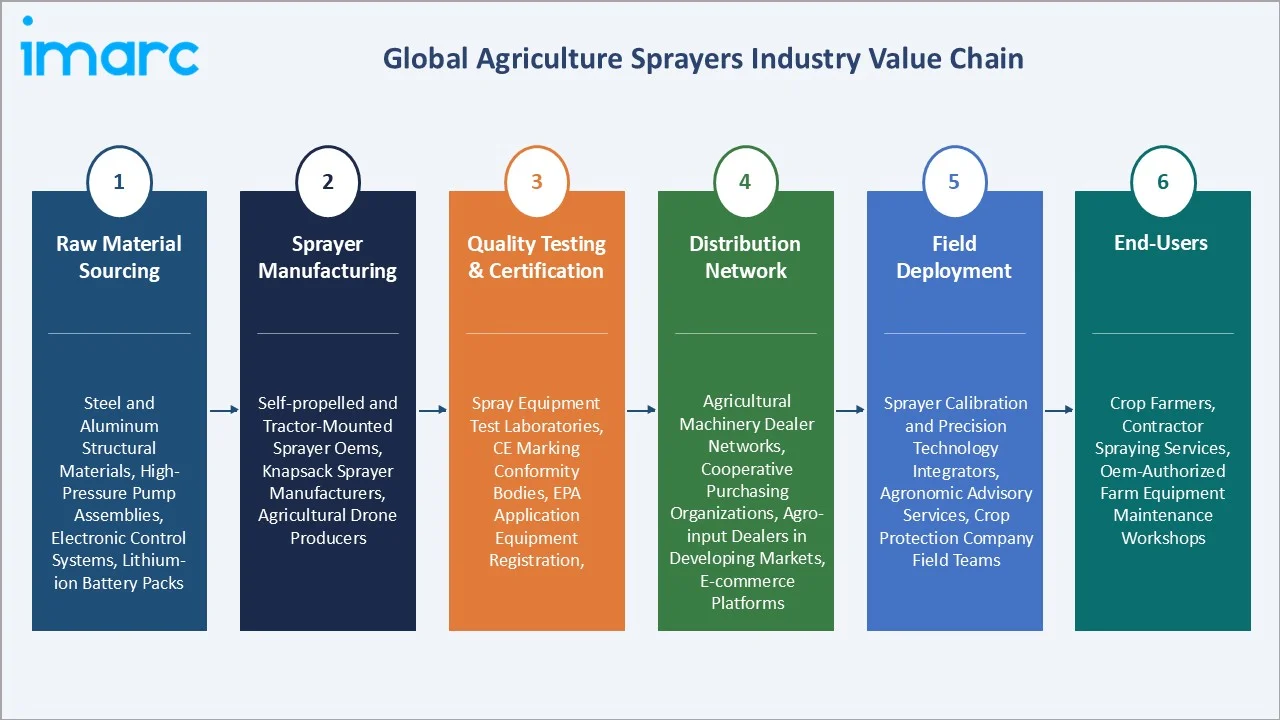

Industry Value Chain Analysis

The agriculture sprayers value chain extends from raw material sourcing through precision manufacturing, dealer distribution, and farm-level operation, with growing importance of digital services at the end-user stage.

| Stage | Key Players / Examples |

|---|---|

| Raw Material Sourcing | Steel and aluminum structural materials, high-pressure pump assemblies, electronic control systems, lithium-ion battery packs |

| Sprayer Manufacturing | Self-propelled and tractor-mounted sprayer OEMs, knapsack sprayer manufacturers, agricultural drone producers |

| Quality Testing & Certification | Spray equipment test laboratories, CE marking conformity bodies, EPA application equipment registration |

| Distribution Network | Agricultural machinery dealer networks, cooperative purchasing organizations, agro-input dealers in developing markets, e-commerce platforms |

| Field Deployment | Sprayer calibration and precision technology integrators, agronomic advisory services, crop protection company field teams |

| End-Users | Crop farmers, contractor spraying services, OEM-authorized farm equipment maintenance workshops |

Technology Landscape in the Agriculture Sprayers Industry

High-Pressure Self-Propelled Sprayer Technology

High-pressure self-propelled sprayers operate at boom widths of 24–48 meters, tank capacities of 2,000–6,000 liters, and speeds of 16–25 km/h. John Deere's Hagie STS and CNH's Case IH Patriot integrate GPS auto-steer, section control, variable rate nozzle management, telematics, and machine vision-based selective application. Ground clearance of 1.2–1.8 meters enables late-season canopy entry in corn, sunflower, and sugarcane applications.

Battery and Solar Knapsack Sprayer Technology

Battery knapsack sprayers use 12V–16V lithium-ion packs powering submersible diaphragm pumps delivering 0.8–1.5 L/min at 2–4 bar pressure. Modern 20-litre models weigh 6–7 kg empty and provide 4–6 hours continuous operation per charge, with DC charging. Solar-assisted models integrate 5–10W photovoltaic panels into the backframe, extending operating time by 20–30% during daylight operation.

Agricultural Drone Sprayer Technology

Agricultural drone sprayers carry 10–50 liter tanks and use centrifugal or pressure atomizer nozzles to spray at 1.5–3 meters above canopy, achieving 30–80 hectares per hour. Active rotor downwash forces droplets into dense canopies, improving penetration versus ground-based equipment. RTK-GPS autonomous flight enables obstacle avoidance, terrain following, and pre-programmed field boundary compliance.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | High-Pressure Sprayer | 33.6% | 2025 |

| Source of Power | Fuel-Operated | 33.5% | 2025 |

| Usage | Field Sprayers | 23.7% | 2025 |

| Region | Asia-Pacific | 36.8% | 2025 |

By Type

High-pressure sprayers lead at 33.6% in 2025, spanning large-scale field crop production in North America, European arable farming, and Asian rice and cotton cultivation. Operating pressures of 3–6 bar achieve adequate droplet velocity and canopy penetration across a USD 50–400,000 price spectrum from backpack compression units to self-propelled commercial machines.

To access detailed market analysis, Request Sample

Low-pressure sprayers at 26.4% serve orchard, vineyard, and specialty crops where reduced pressure minimizes drift. Air carrier sprayers at 22.1% are essential for high-canopy orchards and hop gardens, using airstream projection for dense foliage penetration. Hand-operated sprayers at 17.9% serve the smallholder segment globally, particularly across Africa and South Asia.

By Source of Power

Fuel-operated sprayers retain a 33.5% share anchored by the large installed base of diesel tractor-mounted and self-propelled sprayers in commercial farming across North America, Europe, and Latin America. Diesel engines provide the power density required for large-tank, high-pressure, wide-boom operations not yet achievable by battery technology at equivalent commercial performance.

Manual sprayers at 27.8% serve smallholder farming across Africa, South Asia, and Latin America where motorized equipment remains cost-prohibitive. Battery-operated at 23.6% is the fastest-growing segment at ~6.80% CAGR. Solar sprayers at 15.1% are gaining traction in off-grid markets, with their combined share of battery and solar projected to exceed 50% of the market by 2034.

Regional Market Insights

Asia-Pacific leads with a 36.8% market share in 2025. China's growing drone sprayer commercial ecosystem, India's 120+ million smallholder farms supported by government mechanization subsidies, and Southeast Asia's expanding commercial horticulture sector collectively create the world's largest and most diverse agriculture sprayer demand base.

Europe's 24.6% share is driven by large commercial farm scale, stringent EU pesticide reduction regulations mandating precision application investment, and a sophisticated farmer base in Germany, France, and the UK adopting high-specification self-propelled precision sprayers.

| Region | Share (2025) | Key Growth Drivers |

|---|---|---|

| Asia-Pacific | 36.8% | India's farm mechanization subsidies, China's drone sprayer ecosystem, Japan and South Korea precision orchard spraying |

| Europe | 24.6% | Large commercial arable farm scale, EU precision pesticide reduction mandates driving smart sprayer investment, specialist orchard and vineyard sprayer demand |

| North America | 19.2% | Large self-propelled precision sprayer market, US and Canadian corn and soybean belt commercial spraying volumes |

| Latin America | 11.0% | Brazil's large soybean, corn, and sugarcane sector, growing precision agriculture investment in Argentina and Chile's specialty crop sectors |

| Middle East & Africa | 8.4% | Sub-Saharan Africa smallholder mechanization programs, GCC greenhouse and vertical farm spraying, Egyptian cotton farming, South Africa's commercial crop protection sector |

North America at 19.2% represents the world's most advanced self-propelled sprayer market, where AGCO Corporation, Deere & Company, and CNH Industrial N.V. compete on AI-powered technology at the USD 200,000–400,000 price tier.

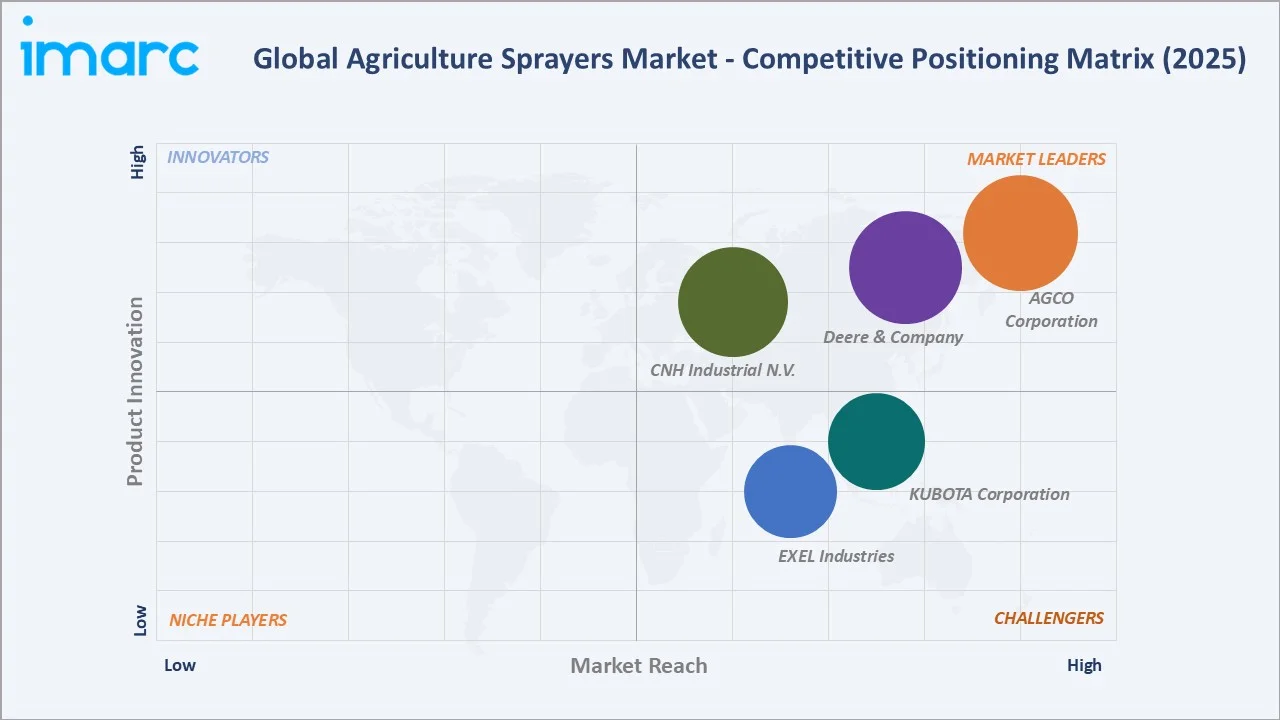

Competitive Landscape

The agriculture sprayers market exhibits a dual-tier competitive structure. In the high-value self-propelled precision segment, AGCO Corporation, Deere & Company, and CNH Industrial N.V. collectively hold approximately 40–45% of global revenue.

| Company Name | Brands/Products | Market Position | Core Strength |

|---|---|---|---|

| AGCO Corporation | MF 500R, Fendt Rogator 900 | Market Leader | Fendt Rogator and Challenger precision sprayers, VRA technology, North America and European commercial farm coverage |

| Deere & Company | R4023 Sprayer, 400 and 600 Series, Hagie STS, Frontier 3-pt Sprayers, LS20 Liquid System, See & Spray | Market Leader | John Deere R Series, See & Spray machine vision, ExactApply individual nozzle control, Operations Center data platform |

| CNH Industrial N.V. | Case IH, New Holland, Miller | Market Leader | Case IH Patriot/SenseApply, New Holland Guardian/IntelliSense, precision automation leadership, global coverage |

| KUBOTA Corporation | Kverneland, Great Plains Manufacturing | Strong Challenger | Asia-Pacific dealer dominance, paddy and vegetable sprayer strength, drone sprayer partnerships in Japan and India |

| EXEL Industries | Tecnoma, Nicolas Sprayers, Berthoud, CMC, Matrot, Hardi, Evrard, Agrifac, Exxact Robotics | Strong Challenger | Berthoud and Hardi brand portfolio, European precision sprayer leadership, orchard and arable technology breadth |

In the broader knapsack and hand-operated segment, the larger volume category, the market is highly fragmented among hundreds of Asian manufacturers competing primarily on price.

Key Company Profiles

AGCO Corporation

AGCO Corporation is one of the global leaders in agricultural equipment with a strong position in precision sprayer technology through its Fendt Rogator product portfolio.

- Product Portfolio: MF 500R, Fendt Rogator 900, and others.

- Recent Developments: In May 2025, AGCO expanded its PTx precision agriculture network by integrating PTx solutions, including sprayers, into more than 50 additional Fendt and Massey Ferguson dealerships across the US and Canada within one year.

- Strategic Focus: Digital farm management integration, export market growth in Latin America and Australia, and sustainable pesticide reduction solutions aligned with EU Farm-to-Fork strategy requirements.

Deere & Company

Deere & Company is one of the world's largest agricultural equipment manufacturers and a global technology leader in precision spraying through the John Deere R Series and See & Spray machine vision platform.

- Product Portfolio: R4023 Sprayer, 400 and 600 Series, Hagie STS, Frontier 3-pt Sprayers, LS20 Liquid System, and See & Spray.

- Recent Developments: In November 2025, John Deere’s See & Spray technology was used across more than 5 million acres, reducing non-residual herbicide use by nearly 50% and saving almost 31 million gallons of herbicide mix.

- Strategic Focus: See & Spray scale-up, ExactApply nozzle rollout, Operations Center precision farming ecosystem, North America and European market leadership, and autonomous sprayer roadmap within John Deere's 2030 autonomous equipment vision.

Market Concentration Analysis

AGCO Corporation, Deere & Company, and CNH Industrial N.V. together hold approximately 40–45% of global commercial sprayer revenue. The broader market, including knapsack categories, is highly fragmented with hundreds of Asian manufacturers.

Vertical integration is increasing: Deere & Company’s Bear Flag Robotics acquisition and AGCO Corporation’s Precision Planting platform create proprietary data ecosystems generating switching costs beyond the equipment itself.

Investment & Growth Opportunities

Fastest Growing Segments

Battery-operated sprayers (~6.80% CAGR), agricultural drone sprayers (26.85% CAGR), and precision VRA systems represent the highest-growth vectors through 2034, addressing a combined incremental market of approximately USD 700 Million.

Emerging Market Expansion

Sub-Saharan Africa, where 50+ million hectares rely on manual spraying, is the largest underserved market. Government-backed programs in Ethiopia, Nigeria, Ghana, and Kenya are creating structured demand through subsidy and extension service channels for affordable battery and solar sprayer mechanization.

Venture and Institutional Investment Trends

- Precision application startup investment exceeded USD 500 Million globally in 2024, with AI nozzle targeting companies, autonomous sprayer platforms, and spray management SaaS businesses attracting venture capital from agtech investors and strategic corporates including Corteva, BASF, and Bayer.

- Agricultural drone sprayer companies in China, India, and the US are attracting venture and government funding as drone spraying regulatory frameworks are implemented in key agricultural markets.

Future Market Outlook (2026-2034)

The global agriculture sprayers market will reach USD 3.60 Billion by 2034 from USD 2.40 Billion in 2025, adding USD 1.20 Billion at a 4.51% CAGR. Battery-operated and solar sprayers will grow their combined share from approximately 38.7% to over 50% by 2034. Drone sprayers will transition from early adoption to mainstream in Asia-Pacific, with meaningful penetration in Latin America and Africa by 2030.

Machine vision-powered targeted application will become standard on all new commercial self-propelled sprayers by 2030, enabling 40–60% chemical use reduction versus current broadcast application, fundamentally transforming the economics of precision crop protection and compelling OEM investment in AI-augmented platform capabilities.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 85 industry participants in 2024–2025, including sprayer manufacturers, precision technology companies, agrochemical field teams, agricultural machinery dealers, and farmers across Asia-Pacific, Europe, North America, and Latin America.

Secondary Research

Secondary research encompassed manufacturer annual reports, FAO agricultural mechanization statistics, AEM and CEMA equipment association data, precision agriculture adoption surveys, and trade publications including Precision Agriculture Magazine, Top Crop Manager, and Agri-Fax.

Forecasting Models

Market size estimations used top-down and bottom-up forecasting incorporating global arable land area, sprayer penetration rates by category and region, average selling price trajectories, replacement cycle assumptions, and government subsidy program data. A base-case CAGR of 4.51% reflects consensus against manufacturer capacity plans and national mechanization targets.

Agriculture Sprayers Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | High-Pressure Sprayer, Low-Pressure Sprayer, Air Carrier Sprayer, Hand Operated Sprayer |

| Sources of Power Covered | Manual, Battery-Operated, Solar Sprayers, Fuel-Operated |

| Usages Covered | Field Sprayers, Orchard Sprayers, Gardening Sprayers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AGCO Corporation, Deere & Company, CNH Industrial N.V., KUBOTA Corporation, EXEL Industries, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the agriculture sprayers market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global agriculture sprayers market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the agriculture sprayers industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Agriculture Sprayers Market Report

The market reached USD 2.40 Billion in 2025 and is projected to reach USD 3.60 Billion by 2034 at a 4.51% CAGR.

Asia-Pacific leads with a 36.8% share in 2025, driven by India's government subsidies, China's drone sprayer adoption, and Southeast Asia's growing commercial horticulture.

High-pressure sprayers lead at 33.6% in 2025, serving large-scale commercial farming across field crops, orchards, and specialty crops globally.

Fuel-operated leads at 33.5% in 2025, as it is dependable, powerful, and versatile, especially in large-scale farming operations

Battery-operated sprayers are growing fastest at approximately 6.80% CAGR, driven by declining battery costs and smallholder farmer adoption in Asia and Africa.

AGCO Corporation, Deere & Company, CNH Industrial N.V., KUBOTA Corporation, and EXEL Industries are some of the leading players in the market.

CNH Industrial launched Case IH SenseApply and New Holland IntelliSense in 2025, AI machine vision systems enabling species-specific herbicide targeting with 50–70% chemical savings.

High capital costs for advanced sprayers, technical awareness gaps in smallholder markets, and environmental regulations on chemical spraying are key challenges.

Agricultural drone sprayers are growing at 26.85%+ CAGR, particularly in China and India, enabling precision spraying in terraced, sloped, and access-constrained farmland.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)