Air Freight Market Size, Share, Trends and Forecast by Service, Destination, End User, and Region, 2026-2034

Global Air Freight Market Size, Share, Trends & Forecast (2026-2034)

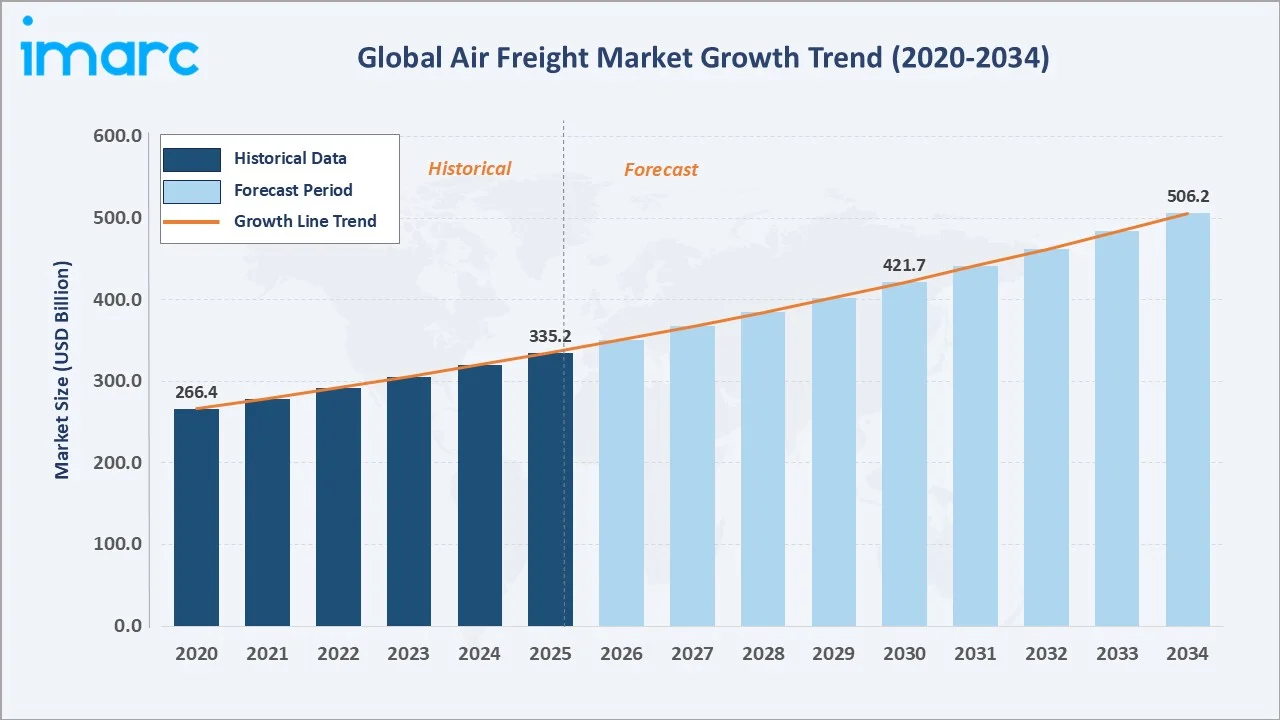

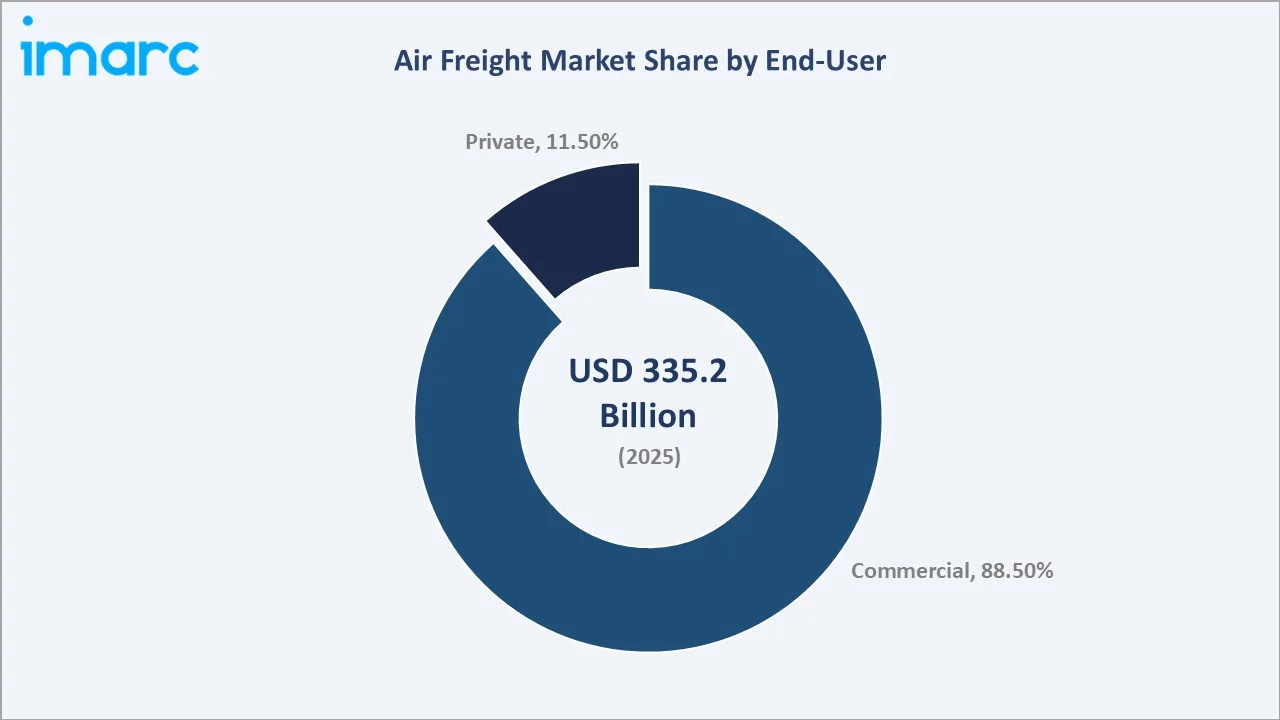

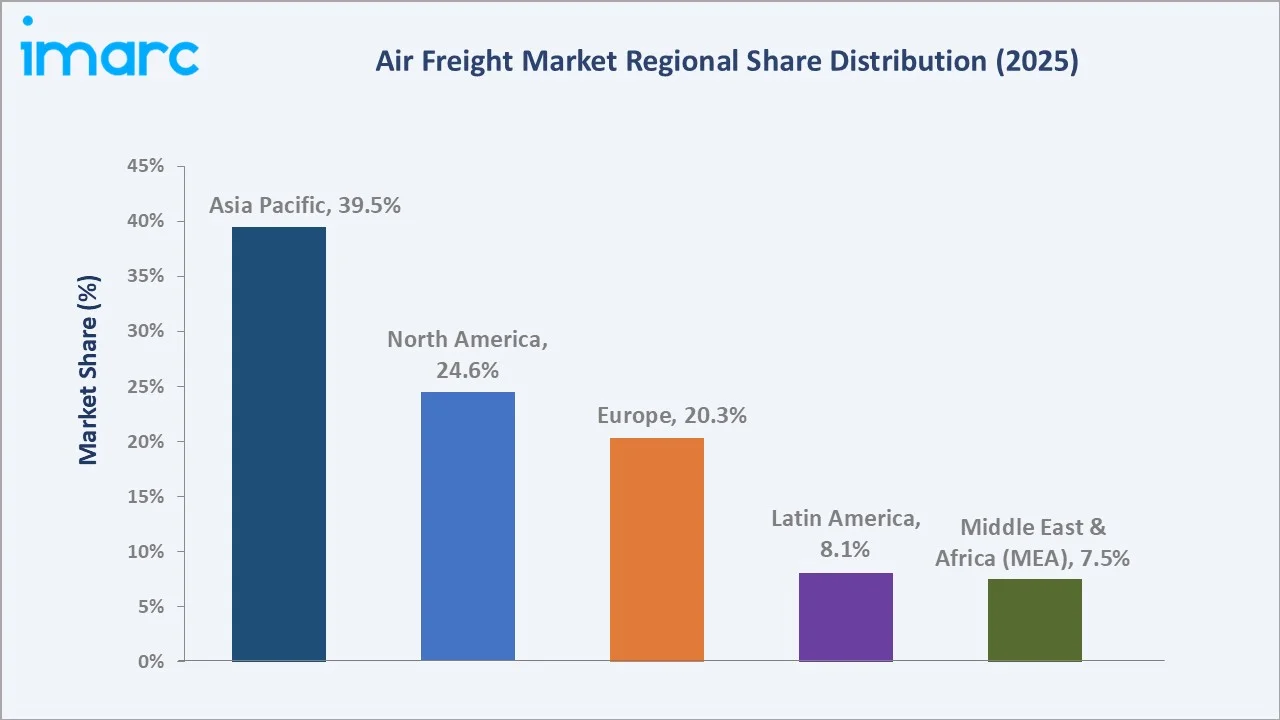

The global air freight market reached a value of USD 335.2 Billion in 2025 and is projected to reach USD 506.2 Billion by 2034, exhibiting a CAGR of 4.7% during the forecast period 2026-2034. Growth is driven by rapid e-commerce expansion, rising demand for time-sensitive and pharmaceutical logistics, and structural shifts in global supply chain strategy. Asia Pacific leads with a 39.5% regional share in 2025. Commercial end users account for 88.5% of revenues, while international routes dominate at 85.1%. The market is projected to reach USD 421.7 Billion by 2030. Key players include FedEx Corporation, United Parcel Service Inc., Deutsche Post AG (DHL), DSV A/S, and Kuehne + Nagel International AG.

Market Snapshot

|

Metric |

Value |

|

Market Size (2020) |

USD 266.4 Billion |

|

Market Size (2025) |

USD 335.2 Billion |

|

Market Size (2030) |

USD 421.7 Billion |

|

Forecast Market Size (2034) |

USD 506.2 Billion |

|

CAGR (2026-2034) |

4.7% |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (39.5%, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Dominant End User |

Commercial (88.5%, 2025) |

|

Dominant Destination |

International (85.1%, 2025) |

To get more information on this market, Request Sample

The market grew from USD 266.4 Billion in 2020 to USD 335.2 Billion in 2025, adding USD 68.8 Billion despite pandemic-induced aviation capacity disruptions. The forecast addition of USD 171 Billion through 2034 is anchored by structural demand from e-commerce trade growth, pharmaceutical supply chain expansion, and manufacturing nearshoring requiring rapid air connectivity.

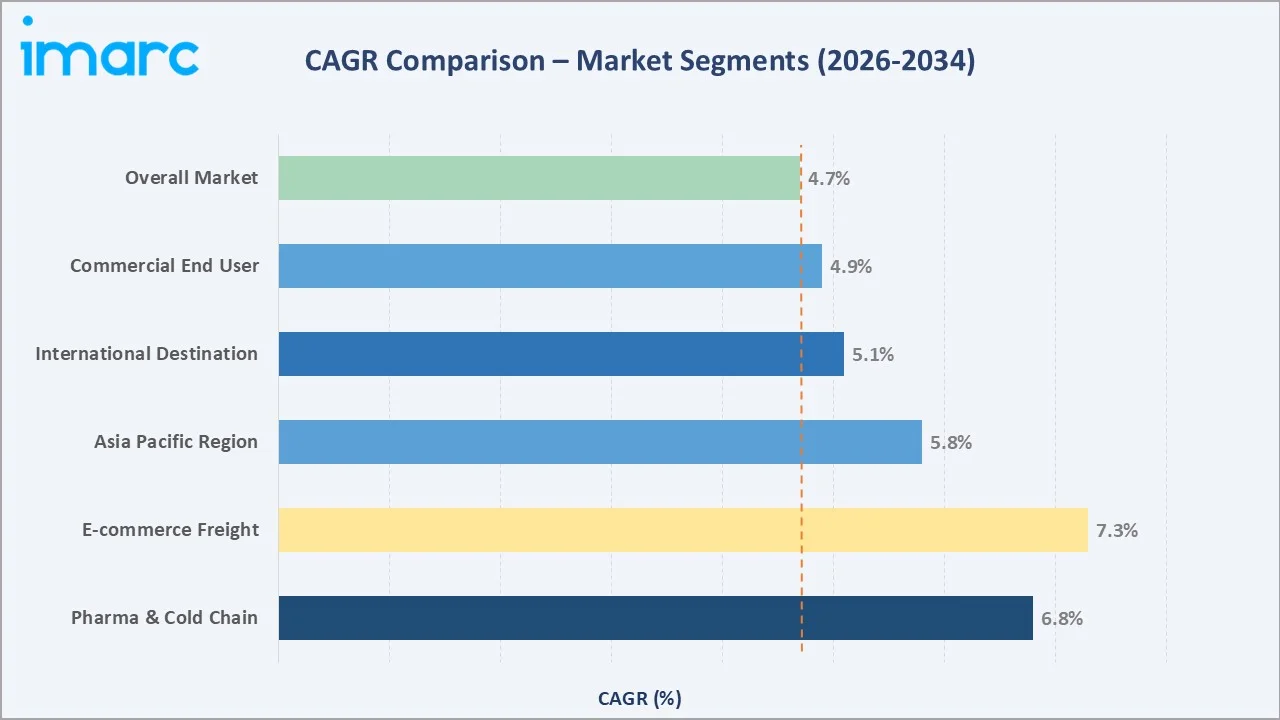

The 4.7% CAGR reflects accelerating demand in high-value sub-segments. E-commerce freight leads at approximately 7.3% CAGR, followed by pharmaceutical cold-chain at 6.8% CAGR, both well above the market average, reflecting structural rather than cyclical demand forces.

Executive Summary

The global air freight market stood at USD 335.2 Billion in 2025, driven by the convergence of accelerating e-commerce trade, pharmaceutical supply chain internationalisation, and the structural shift toward just-in-time logistics by global manufacturers. The market is forecast to reach USD 506.2 Billion by 2034 at a 4.7% CAGR, crossing USD 421.7 Billion by 2030 and adding approximately USD 171 Billion in absolute value over the forecast decade.

Commercial users dominate at 88.5% (2025), reflecting the predominance of B2B freight movements, manufacturing inputs, pharmaceutical shipments, retail inventory replenishment, and e-commerce parcel exports. Private users at 11.5% encompass charter operations and corporate freight. International routes account for 85.1% of revenues, reflecting air freight's competitive advantage in intercontinental lanes where transit time compression from weeks (ocean) to days justifies the cost premium for high-value goods.

Asia Pacific commands 39.5% of the market (2025), underpinned by China's massive export base and the explosive growth of Asian e-commerce platforms. North America follows at 24.6% via robust domestic express networks, while Europe at 20.3% is driven by pharmaceutical exports and intra-EU express demand. Key trends reshaping the market include digital freight platform adoption, sustainable aviation fuel (SAF) programs, pharmaceutical cold-chain expansion, and Middle East hub network development.

Key Market Insights

|

Insight |

Data |

|

Dominant End User |

Commercial – 88.5% (2025) |

|

Dominant Destination |

International – 85.1% (2025) |

|

Leading Region |

Asia Pacific – 39.5% (2025) |

|

Fastest Growing Region |

Asia Pacific (~5.8% CAGR, 2026-2034) |

|

Top Companies |

FedEx, UPS, DHL, DSV, Kuehne+Nagel, Cargolux, Qatar Airways Cargo |

|

Market Opportunity |

E-commerce cross-border freight and pharma cold-chain logistics in Asia |

Key Analytical Observations Supporting The Above Data:

- Commercial Dominance: The 88.5% commercial share (2025) reflects structural dependency of global trade on air freight for high-value, time-sensitive shipments, electronics, automotive parts, pharmaceuticals, where speed premiums justify air economics over sea or land alternatives.

- International Route Leadership: International's 85.1% share reflects air freight's advantage on intercontinental lanes, particularly Asia-to-North America, Asia-to-Europe, and transatlantic routes, where weeks of ocean transit compresses to days via air.

- Asia Pacific Production Hub: Asia Pacific's 39.5% share is anchored by China's export manufacturing base, South Korea and Japan's high-tech electronics exports, and the rapid growth of Southeast Asian manufacturing hubs diversifying global supply chains.

Global Air Freight Market Overview

Air freight encompasses the commercial transportation of goods via aircraft, serving as the world's premier logistics mode for time-sensitive, high-value, and perishable shipments. The market serves manufacturers, retailers, pharmaceutical companies, e-commerce platforms, and commodity traders across 180+ countries. As of 2025, the market is valued at USD 335.2 Billion and handles approximately 65–70 million metric tonnes annually, supporting global trade crossing USD 35 Trillion. Macroeconomic tailwinds, e-commerce expansion, pharma internationalisation, and just-in-time inventory management, sustain long-term demand well above global GDP growth.

Market Dynamics

To evaluate market opportunities, Request Sample

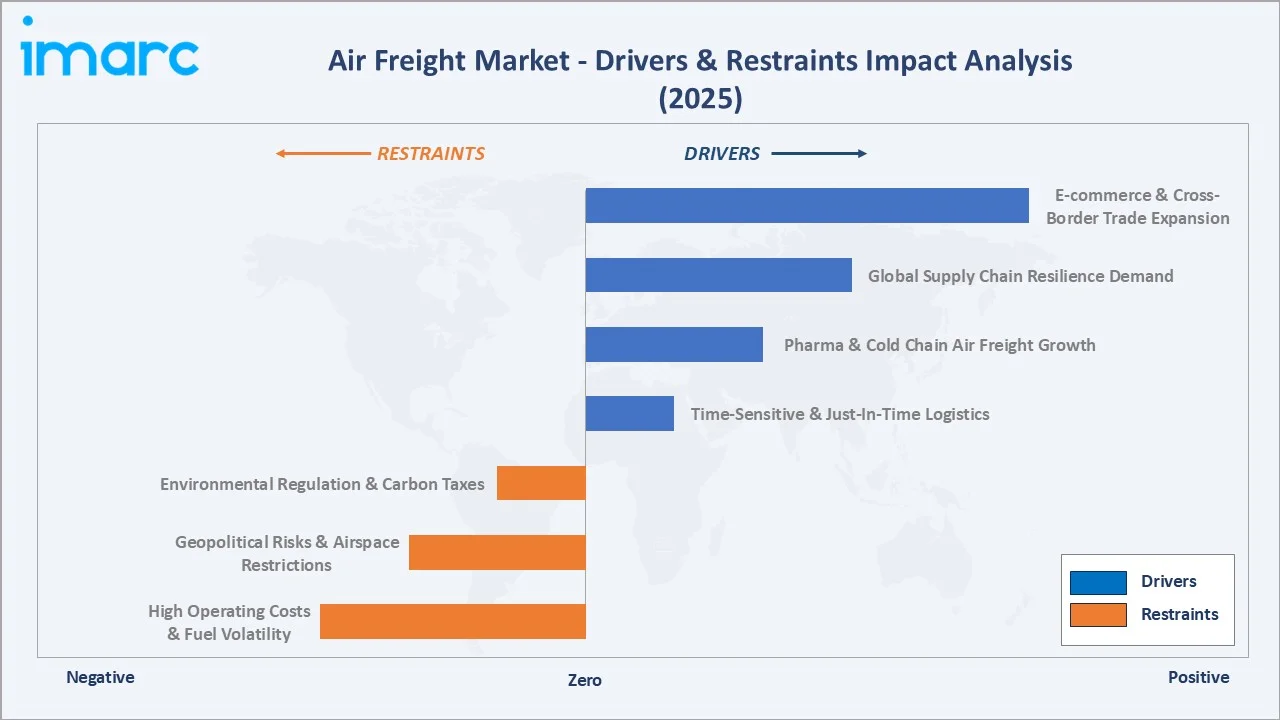

Market Drivers

- E-Commerce and Cross-Border Trade: Global cross-border e-commerce airfreight hit 5.4 million tonnes in 2025. Asian platforms, Alibaba's Cainiao, JD Logistics, Shein, Temu, operate dedicated air charter networks, generating hundreds of millions of parcels monthly on Asia-to-consumer routes.

- Supply Chain Resilience Demand: Post-pandemic supply chain restructuring has elevated air freight as a buffer against maritime disruption. Companies maintain higher air freight shares as insurance against port congestion, Suez and Panama Canal closures, and geopolitical disruption to ocean shipping.

- Pharmaceutical Cold-Chain Growth: Biologics, mRNA vaccines, cell and gene therapy commercialisation are driving pharmaceutical cold-chain air freight. IATA CEIV Pharma now covers 250,000 trade lanes, with 699 companies (including 85 airlines) certified, establishing air freight as the backbone of pharmaceutical supply chains.

- Just-In-Time Manufacturing Logistics: Electronics (semiconductors, smartphones), automotive (EV batteries), and fast fashion companies are structurally increasing air freight for time-critical inventory replenishment, driven by consumer demand for faster availability and inventory optimisation.

Market Restraints

- High Costs and Fuel Volatility: Jet fuel represents 30–40% of cargo operating costs. Air freight is more expensive per kilogram than sea freight, limiting demand to high-value and time-sensitive goods and making the market sensitive to energy price shocks.

- Geopolitical and Airspace Risks: Russian airspace closure since 2022 has materially increased Europe-to-Asia flight times and operating costs. Escalating trade tensions, tariffs, and shifting cargo security requirements create planning uncertainty for network operators.

- Environmental Regulation: EU airports to contain a minimum share of SAF, starting at 2% in 2025, rising to 6% in 2030 and 70% in 2050, creating pricing pressure and potential substitution toward sea freight for less time-sensitive trade lanes.

Market Opportunities

- SAF Green Freight Differentiation: SAF-backed programs from DHL GoGreen Plus, FedEx, and Lufthansa Cargo allow shippers to purchase verified carbon reduction credits. Just 0.6% of all jet fuel usage will come from SAF production in 2025; that percentage will rise to 0.8% the following year. At current price levels, the SAF premium translates into an additional USD 3.6 billion in fuel costs for the industry in 2025.

- Digital Freight Platform Expansion: AI-powered booking platforms (Freightos, Flexport) are reducing transaction costs and improving capacity utilisation. Significant amount of air freight was digitally booked, augmenting this opportunity.

- Emerging Market Airport Infrastructure: Airport expansion programs in India (UDAN scheme), Southeast Asia (Singapore Changi T5, KL KLIA), and the Middle East (Dubai World Central, Doha Hamad) are creating new cargo capacity in underserved high-growth markets.

Market Challenges

- Freighter Capacity Constraints: Boeing and Airbus multi-year delivery backlogs and limited freighter conversion capacity create supply constraints that amplify rate volatility during demand surges and restrict market growth acceleration in peak periods.

- Hub Infrastructure Bottlenecks: Ground handling capacity at Frankfurt, Hong Kong, Chicago O'Hare, and Los Angeles is approaching saturation, creating congestion risk and reducing air freight's service quality advantage over premium sea alternatives.

- Intermodal Competition: China-Europe Belt and Road rail services and ultra-large container vessels with improved transit times offer competitive alternatives for mid-value goods, creating substitution pressure on lower-value air freight segments.

Emerging Market Trends

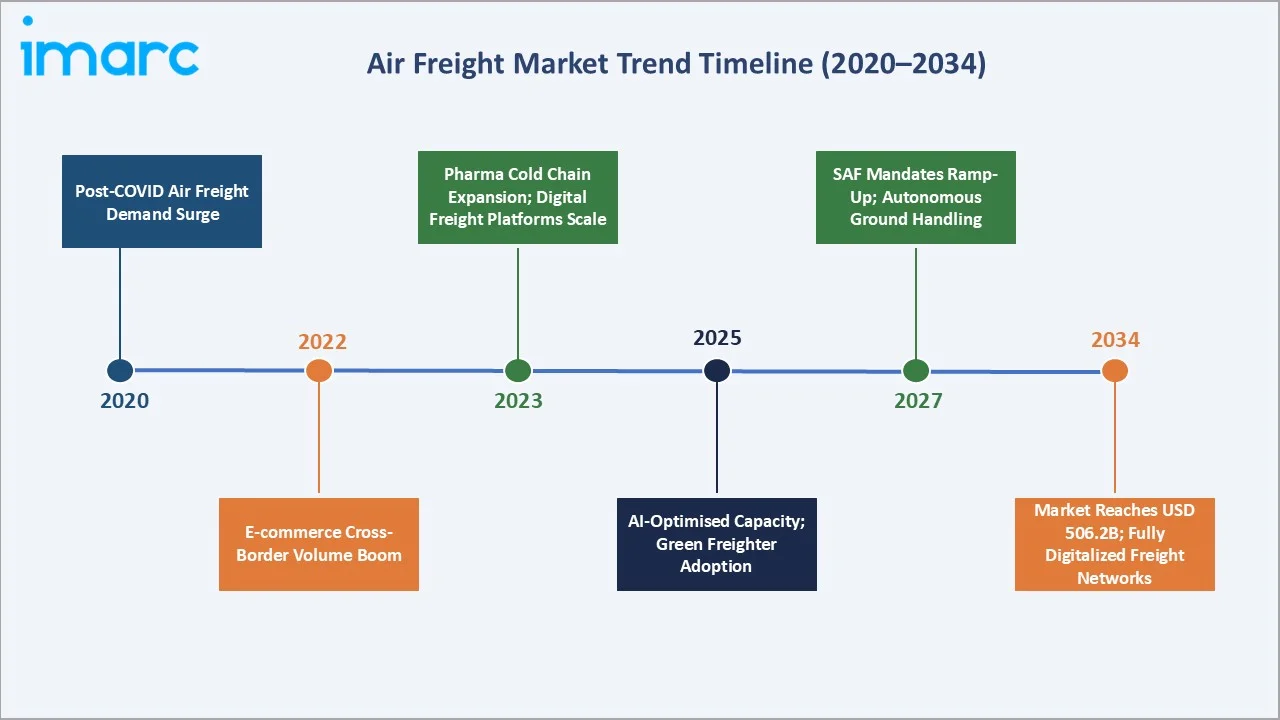

The global air freight market is being reshaped by five converging trends redefining network structures, cargo types, technology adoption, and competitive dynamics through 2034.

1. E-Commerce Freight as a Structural Demand Driver

Cross-border e-commerce has transitioned from a cyclical tailwind to a structural foundation for air freight demand. Asian platforms have established dedicated charter networks and express agreements.

2. Pharmaceutical Cold-Chain Air Logistics Expansion

Commercialisation of mRNA technology, cell therapies, and high-value biologics is driving rapid cold-chain air freight growth. Purpose-built pharmaceutical handling facilities are being deployed at Frankfurt, Singapore Changi, and Dubai, positioning air freight as the irreplaceable backbone of global pharmaceutical distribution.

3. Sustainable Aviation Fuel and Green Freight Programs

DHL GoGreen Plus, FedEx SAF initiatives, and Lufthansa Cargo's Green Fares offer corporate customers verified carbon reduction for freight. SAF production capacity is expected to grow manifold by 2030, progressively reducing air freight carbon intensity and enabling new ESG-aligned commercial propositions.

4. Digitalisation and AI-Powered Freight Optimisation

AI-driven yield management systems at Lufthansa Cargo, IAG Cargo, and Air France KLM Cargo are improving load factors. Blockchain platforms and digital air waybill (e-AWB) adoption reaching approximately 80% penetration in 2025 are reducing documentation errors and clearance delays.

5. Middle East Hub Expansion and Network Reorientation

Qatar Airways Cargo and Emirates SkyCargo are reshaping global air freight network geography through Doha and Dubai hub expansion, capturing growing East-West and South-South freight flows and challenging established European and Asian hub dominance on long-haul trade lanes.

Industry Value Chain Analysis

The air freight industry value chain spans six interconnected stages from cargo origination to final delivery, requiring specialised infrastructure, regulatory expertise, and real-time digital coordination at each stage.

|

Stage |

Key Activities |

Representative Players |

|

Shippers & Consignors |

Cargo preparation, booking, export documentation |

Manufacturers, Retailers, Pharma companies |

|

Freight Forwarders |

Booking, customs clearance, documentation, coordination |

DSV, Kuehne+Nagel, Expeditors, Hellmann, CEVA Logistics |

|

Ground Handling & Trucking |

Palletising, pre-cooling, ramp-side delivery |

Swissport, Menzies Aviation, dnata |

|

Airlines & Cargo Operators |

Freighter and belly operations, capacity management |

FedEx, UPS, DHL, Cargolux, Qatar Airways Cargo |

|

Customs & Compliance |

Import/export clearance, security screening |

CBP, HMRC, customs brokers, IATA CSA agents |

|

Last-Mile Delivery |

Deconsolidation, warehousing, final delivery |

FedEx Express, UPS, DHL Express, Nippon Express |

Freight forwarding is the critical value aggregation stage, with top forwarders controlling approximately 35–40% of total volumes. Digital platforms are progressively disintermediating traditional forwarders on standardised trade lanes, creating structural margin pressure and accelerating consolidation in the forwarding tier.

Technology Landscape in the Air Freight Industry

AI-Powered Capacity Management and Dynamic Pricing

Machine learning models are optimising aircraft load factors, route profitability, and dynamic freight rate pricing in real-time. AI-driven demand forecasting enables pre-positioning of capacity ahead of e-commerce peak seasons, reducing costly last-minute shortfalls by 3–8 percentage points on key trade lanes.

Blockchain and Digital Air Waybill Platforms

IATA's e-AWB initiative has reached approximately 80% digital penetration in 2025. Blockchain platforms including IATA ONE Record enable multi-party shipment data sharing with immutable audit trails, reducing document fraud and clearance delays across complex multi-leg international shipments.

Autonomous Ground Handling and Robotics

Automated cargo handling at Frankfurt Cargo City, Hong Kong Air Cargo Terminals, and Memphis FedEx World Hub reduces labour dependency and enables 24/7 operations. These systems address the critical infrastructure bottleneck constraining throughput at major global cargo hubs.

Cold Chain Monitoring and IoT Technology

Real-time IoT temperature monitoring from va-Q-tec, Envirotainer, and SkyCell enables continuous pharmaceutical cold-chain visibility with automated excursion alerts. GPS-enabled tracking and predictive maintenance for refrigerated ULDs are elevating compliance with WHO and FDA documentation requirements.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Service |

Freight |

74.1% |

2025 |

|

Destination |

International |

85.1% |

2025 |

|

End User |

Commercial |

88.5% |

2025 |

|

Region |

Asia-Pacific |

39.5% |

2025 |

By End User

Commercial users dominate the global air freight market at 88.5% in 2025. This segment encompasses B2B freight movements by manufacturers, retailers, pharmaceutical companies, and e-commerce logistics providers, all shipping high-value or time-sensitive goods where air freight economics are justified. Commercial demand growth is structurally driven by e-commerce platform expansion, pharmaceutical supply chain internationalisation, and just-in-time inventory replenishment requirements by global brands.

Private end users account for 11.5% (2025), covering corporate charter operations, government logistics, humanitarian aid freight, and specialised private cargo movements. The commercial-to-private ratio has remained broadly stable during 2020–2025, with both segments growing in absolute value terms driven by the overall market expansion.

To access detailed market analysis, Request Sample

By Destination

International freight leads at 85.1% in 2025, reflecting air freight's fundamental competitive advantage in intercontinental trade lanes, Asia-North America, Asia-Europe, and transatlantic – where transit time compression from ocean weeks to air days justifies the cost premium for high-value electronics, pharmaceuticals, and fashion goods. International demand growth is structurally linked to global trade liberalisation, e-commerce cross-border expansion, and the increasing time-sensitivity of supply chains.

Domestic air freight at 14.9% is concentrated in large continental economies with geographic constraints or underdeveloped surface infrastructure, notably the United States (domestic express), China (domestic e-commerce), India, and Brazil. India's domestic air freight market is growing fastest within this segment, supported by the UDAN regional connectivity scheme targeting 100 new airports.

Regional Market Insights

Five major regions constitute the global air freight market. Asia Pacific and North America collectively account for 64.1% of revenues in 2025, reflecting manufacturing export volumes and integrated express network density respectively.

Asia Pacific's 39.5% leadership is underpinned by China's export manufacturing base, South Korea and Japan's high-value electronics exports, and the explosive growth of direct-to-consumer e-commerce targeting global markets. India is the fastest-growing market within the region at approximately 7–8% CAGR, driven by electronics manufacturing expansion (Apple, Samsung supply chains) and pharmaceutical exports.

North America's 24.6% share is anchored by FedEx and UPS, whose combined revenues exceeded USD 160 Billion in 2024. Europe's 20.3% reflects its position as the world's largest pharmaceutical manufacturing region, with Frankfurt Airport handling approximately 2.1 million metric tonnes in 2024. The Middle East and Africa at 7.5% is growing through Qatar Airways Cargo and Emirates SkyCargo hub strategies that are repositioning Doha and Dubai as global transit freight centres.

Competitive Landscape

The global air freight market is moderately concentrated. FedEx, UPS, and DHL collectively represent approximately 35–40% of global revenues in 2025. The forwarding tier is more fragmented, with DSV (post-DB Schenker acquisition), Kuehne+Nagel, Nippon Express, and Expeditors controlling approximately 25–30% of forwarded volumes.

|

Company Name |

Key Brand(s) |

Market Position |

Primary Strategy |

|

FedEx Corporation |

FedEx Express |

Global Leader |

Integrated express, e-commerce, SAF commitment |

|

United Parcel Service |

UPS Air Cargo |

Global Leader |

Healthcare logistics, B2B and e-commerce integration |

|

Deutsche Post AG |

DHL Express, DHL Global Forwarding |

Global Leader |

Pharma cold-chain, digital forwarding, GoGreen Plus |

|

DSV A/S |

DSV Air & Sea |

Leader – Forwarding |

M&A growth, digital freight, DB Schenker acquisition |

|

Kuehne+Nagel Intl. |

myKN, CB Air Platform |

Leader – Forwarding |

Pharma specialisation, KN FreightNet digital platform |

|

Cargolux Airlines |

Cargolux |

Leader – Freighter |

Pure freighter operations, Luxembourg hub, specialty cargo |

|

Qatar Airways Cargo |

Qatar Cargo |

Leader – MEA |

Hub expansion, belly & freighter, cold-chain leadership |

|

Nippon Express |

NX Air Freight |

Leader – Asia |

Japan/Asia network, pharma, automotive parts |

|

Expeditors Intl. |

Expeditors |

Established – NA |

Technology-led forwarding, high-margin niche segments |

|

American Airlines |

AA Cargo |

Established – NA |

Belly cargo monetisation, domestic and international routes |

|

ANA Cargo Inc. |

ANA Cargo |

Challenger – Asia |

Japan hub, intra-Asia, perishables and pharma |

Vertical integration, from freight forwarding through airline ownership and ground handling to last-mile delivery is the primary competitive moat for global integrators. FedEx, UPS, and DHL's ability to offer end-to-end tracking, guaranteed transit times, and single-contract coverage across 220+ countries create switching barriers that pure-play airlines and forwarders cannot replicate without significant capital investment.

Key Company Profiles

FedEx Corporation

FedEx Corporation is the world's largest dedicated air freight carrier, operating over 700 aircraft from its Memphis International hub, the North America’s busiest cargo airport. FedEx serves 220+ countries through FedEx Express and TNT networks.

- Recent Developments: FedEx completed its DRIVE transformation in FY2024. Announced USD 1.3 Billion SAF purchase agreement in 2024 to advance net-zero operations by 2040.

- Strategic Focus: E-commerce growth, SAF net-zero 2040, last-mile automation, healthcare logistics expansion, and AI optimisation via FedEx Dataworks.

United Parcel Service Inc.

UPS operates approximately 490 aircraft serving 220+ countries from its Louisville Worldport hub processing approximately 2 million packages daily on an average at peak-hour capacity.

- Recent Developments: UPS acquired Estafeta (Mexico) in 2024 to strengthen Latin American coverage. Launched UPS Premier healthcare program in 2024 with proactive monitoring for biologics.

- Strategic Focus: Healthcare logistics, SME e-commerce via Digital Access Program, SAF investment, and ORION AI routing network efficiency.

Deutsche Post AG (DHL Group)

DHL Group is the world's largest logistics company, with DHL Express, DHL Global Forwarding, and DHL Supply Chain operating across 220+ countries with dominant pharmaceutical and express freight coverage.

- Recent Developments: DHL invested €7 Billion in sustainability (SAF procurement, electric vehicles) in 2021–2025. Launched carrier-neutral air freight booking platform for SME customers.

- Strategic Focus: Pharmaceutical cold-chain (IATA CEIV Pharma globally certified), GoGreen sustainability, Asia Pacific e-commerce expansion, and digital forwarding development.

Cargolux Airlines International S.A.

Cargolux is Europe's largest all-cargo airline, operating 30 Boeing 747 freighters from Luxembourg hub with coverage across 90+ destinations and 50 countries for time-sensitive specialised freight.

- Recent Developments: Announced transition to Boeing 777F freighters from 2026. Signed SAF offtake agreement with Neste in 2023 SAF blend across Luxembourg operations.

- Strategic Focus: Pure freighter network differentiation, pharmaceutical and specialised cargo premium positioning, SAF transition, and emerging African and Middle Eastern route expansion.

Market Concentration Analysis

The global air freight market exhibits bifurcated concentration. At the integrated express and airline level, FedEx, UPS, and DHL represent approximately 35–40% of global revenues in 2025. At the forwarding level, DSV (post-DB Schenker), Kuehne+Nagel, Nippon Express, and Expeditors control approximately significant part of forwarded volumes, with fragmented regional forwarders competing in specialised corridors and cargo categories.

Consolidation is intensifying in the forwarding tier. DSV's €14.3 Billion acquisition of DB Schenker in 2024 is the largest logistics M&A in a while, putting renewed competitive pressure on Kuehne+Nagel and other global forwarders to scale digitally or through acquisition. The market is expected to see 8–12 significant M&A or partnership transactions annually through 2034, driven by digital platform investment, specialty cargo specialisation, and Asia Pacific expansion strategies.

Investment & Growth Opportunities

Fastest Growing Segments

E-commerce cross-border freight, pharmaceutical cold-chain air logistics, and time-sensitive electronics express freight are the highest-growth investment vectors through 2034. These three segments collectively address a total addressable air freight market exceeding USD 200 Billion by 2034, offering premium margin profiles for specialised operators.

Emerging Market Opportunities

India presents the largest single-country opportunity, driven by Apple and Samsung supply chain expansion, pharmaceutical export growth, and UDAN domestic aviation investment. Latin America's nearshoring boom is creating structural demand on US-Mexico and US-Brazil corridors for automotive parts, electronics, and consumer goods. Vietnam, Bangladesh, and Indonesia are rapidly developing as air freight origin markets for garment and electronics exports.

Technology and Innovation Investment Trends

- Digital Freight Platforms: AI-powered booking platforms (Freightos, Flexport) are attracting huge investments of air freight revenues still booked via manual and phone-based processes.

- SAF Production Infrastructure: SAF production facilities are attracting multi-billion dollar investment driven by US Inflation Reduction Act tax credits, EU ReFuelEU mandates, and airline sustainability commitments.

- Cold-Chain Technology: Smart ULD sensors, active temperature-control containers, and real-time monitoring platforms are attracting investment as pharmaceutical cold-chain air freight grows substantially.

- Autonomous Ground Handling: Robotics investment for air cargo terminals addresses labour cost escalation and hub throughput bottlenecks, with the global air cargo terminal automation market growing rapidly.

Future Market Outlook (2026-2034)

The global air freight market is poised for robust expansion through 2034. This trajectory significantly exceeds projected global GDP growth, reflecting the structural shift of commerce toward faster logistics for high-value and time-sensitive goods.

AI-powered network optimisation, SAF supply security, and pharmaceutical cold-chain differentiation will define competitive advantage over the next decade. Asia Pacific's share is projected to approach 42–44% by 2034, as India's manufacturing export surge and Southeast Asia's continued industrial development add to China's established volumes. Companies investing now in digital platforms, SAF supply chains, and specialised cold-chain capabilities will be best positioned to capture premium market segments through 2034.

Research Methodology

Primary Research

Primary research included structured interviews with over 150 industry participants in 2024–2025, comprising air freight carriers, freight forwarders, shippers (electronics, pharmaceutical, retail), airport authority representatives, and regulatory officials across North America, Europe, Asia Pacific, and the Middle East.

Secondary Research

Secondary research encompassed IATA World Air Transport Statistics, ICAO air transport data, World Bank trade databases, company annual reports, trade publications (Air Cargo World, The Loadstar), and industry associations including TIACA and FIATA. Over 280 primary statistical sources were triangulated for market size validation.

Forecasting Models

Market size estimations used a bottom-up cargo volume model combined with top-down revenue analysis, incorporating yield projections, route network capacity growth, fuel cost scenarios, and end-market demand forecasts by industry vertical. Scenario analysis across base, optimistic, and conservative cases was conducted to account for geopolitical risk and demand volatility.

Air Freight Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Services Covered | Freight, Express, Mail, Others |

| Destinations Covered | Domestic, International |

| End Users Covered | Private, Commercial |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | FedEx Corporation, United Parcel Service, Deutsche Post AG, DSV A/S, Kuehne+Nagel Intl., Cargolux Airlines, Qatar Airways Cargo, Nippon Express, Expeditors Intl., American Airlines, ANA Cargo Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the air freight market from 2020-2034.

- The air freight market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the air freight industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Air Freight Market Report

The global air freight market was valued at USD 335.2 Billion in 2025 and is projected to reach USD 506.2 Billion by 2034.

The market is forecast to grow at a CAGR of 4.7% during 2026-2034, driven by e-commerce expansion, pharmaceutical cold-chain demand, and rising time-sensitive global logistics requirements.

Commercial end users dominate at 88.5% in 2025, encompassing manufacturers, retailers, pharma firms, and e-commerce platforms shipping high-value, time-sensitive international freight globally.

International freight leads at 85.1% in 2025, reflecting air freight's advantage in intercontinental trade where transit time compression from ocean weeks to air days justifies the cost premium.

Asia Pacific leads with 39.5% in 2025, driven by China's export manufacturing base, Asian e-commerce platform growth, and high-tech electronics exports from South Korea and Japan.

Key drivers include cross-border e-commerce expansion, pharmaceutical cold-chain demand, just-in-time supply chain requirements, emerging market manufacturing growth, and post-pandemic supply chain resilience building.

Asia Pacific is both the largest and fastest-growing region, with India leading within the region at approximately 7–8% CAGR, driven by electronics manufacturing exports and pharmaceutical logistics.

Leading companies include FedEx Corporation, United Parcel Service, Deutsche Post AG, DSV A/S, Kuehne+Nagel Intl., Cargolux Airlines, Qatar Airways Cargo, Nippon Express, Expeditors Intl., American Airlines, and ANA Cargo Inc.

The global air freight market is projected to reach USD 421.7 Billion by 2030, reflecting steady compound growth from the 2025 base of USD 335.2 Billion.

Commercial air freight covers B2B trade shipments by manufacturers, retailers, and e-commerce platforms (88.5%), while private covers corporate charters and government freight (11.5%).

Key opportunities include e-commerce cross-border freight platforms, pharmaceutical cold-chain infrastructure, SAF production programs, digital freight forwarding platforms, and Asia Pacific airport infrastructure.

Key challenges include high fuel costs and volatility, geopolitical airspace restrictions, environmental carbon taxes, freighter capacity constraints, hub infrastructure bottlenecks, and intermodal competition.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade