Air Starter Market Size, Share, Trends and Forecast by Type, End User, and Region 2026-2034

Air Starter Market Size, Share, Trends & Forecast (2026-2034)

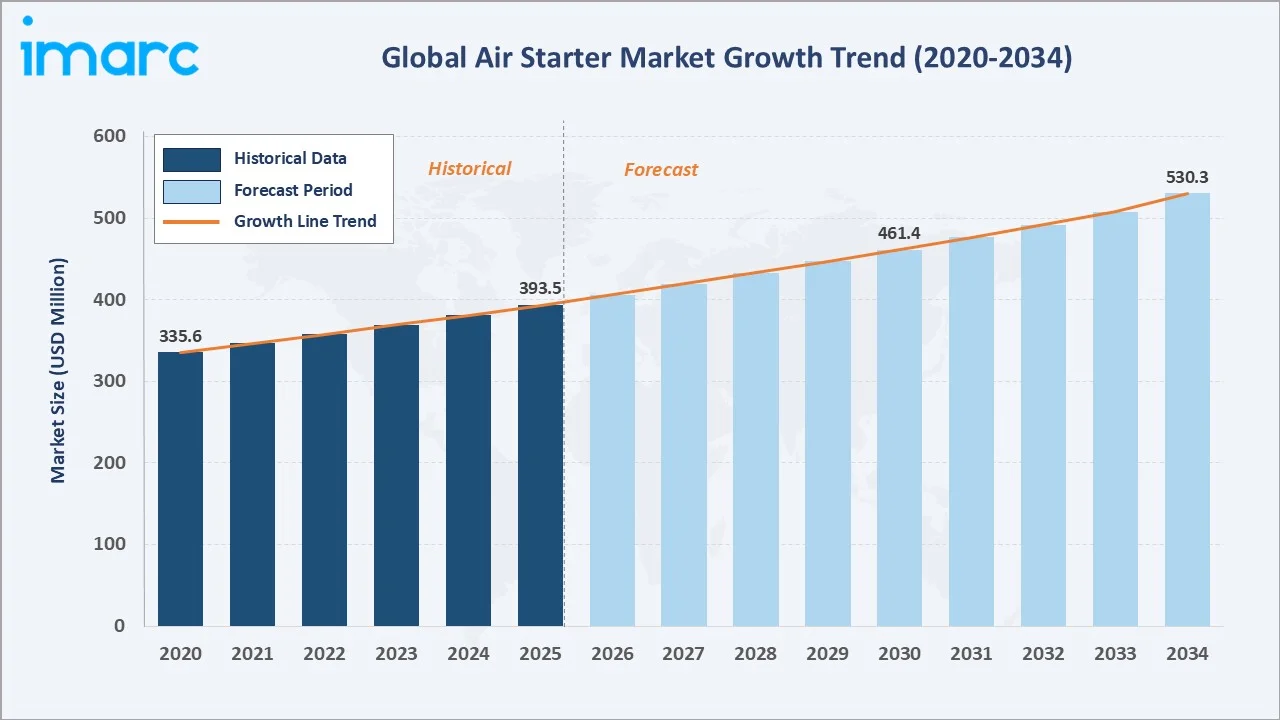

The global air starter market reached USD 393.5 Million in 2025 and is projected to reach USD 530.3 Million by 2034, growing at a CAGR of 3.24% during 2026-2034. Market growth is driven by expanding oil & gas infrastructure, stringent safety regulations mandating compressed-air starting systems in explosive atmospheres, growing marine fleet investment, and increasing mining and power generation capital expenditure.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 393.5 Million |

| Forecast Market Size (2034) | USD 530.3 Million |

| CAGR (2026-2034) | 3.24% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

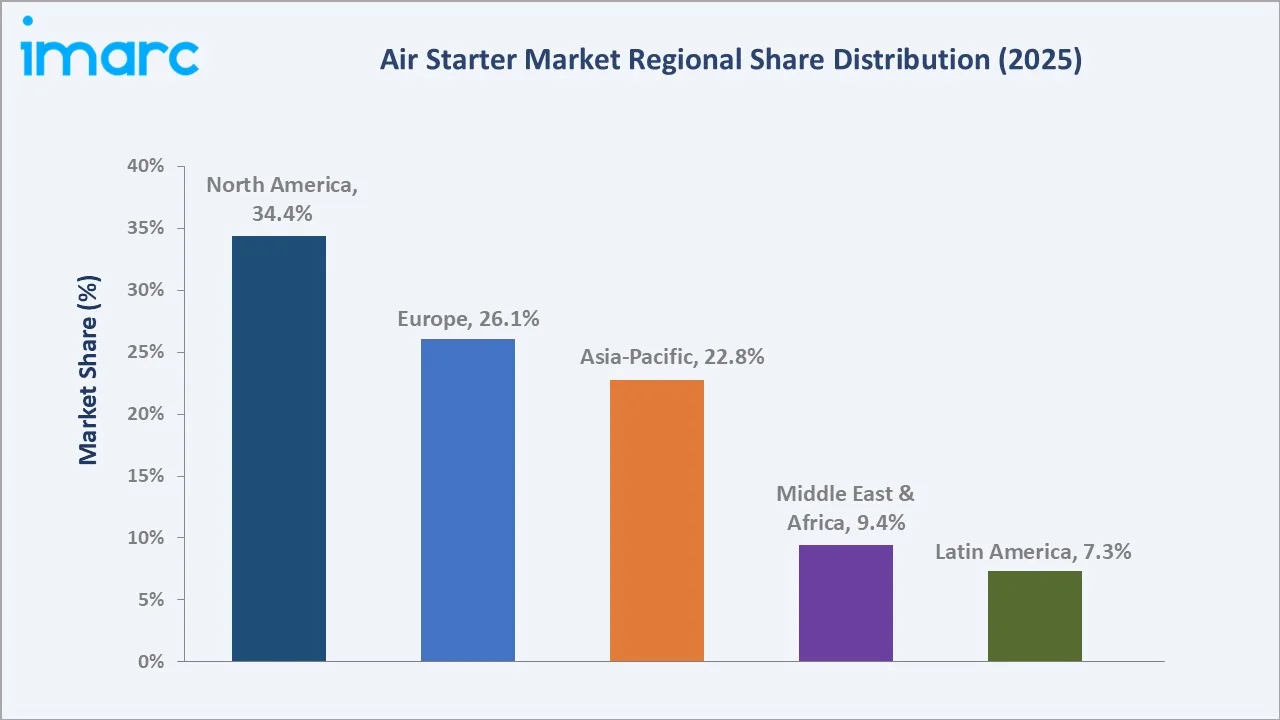

North America's market leadership reflects the region's substantial oil & gas upstream and midstream infrastructure, large installed base of industrial gas turbines and reciprocating engines requiring compressed-air starting, and its mature aftermarket maintenance and parts replacement ecosystem. Turbine air starters' 67.3% dominance underscores their preference in high-power, safety-critical applications across oil & gas, marine, and power generation sectors where electrical starting systems are prohibited by hazardous area classifications.

To get more information on this market, Request Sample

The market's 3.24% CAGR reflects the essential and non-discretionary nature of air starter replacement and new equipment demand tied to the long-lived asset cycles of oil & gas facilities, power plants, and marine vessels, sectors where air starters are the mandated starting technology in ATEX and IECEx classified environments.

Executive Summary

The global air starter market is positioned for steady, demand-led growth across its primary industrial end markets. From USD 393.5 Million in 2025, the market is forecast to reach USD 530.3 Million by 2034, creating incremental value of USD 136.8 Million at a 3.24% CAGR. Growth is underpinned by the structural requirement for compressed-air starting systems in hazardous industrial environments where electrical and hydraulic alternatives cannot safely or practically operate.

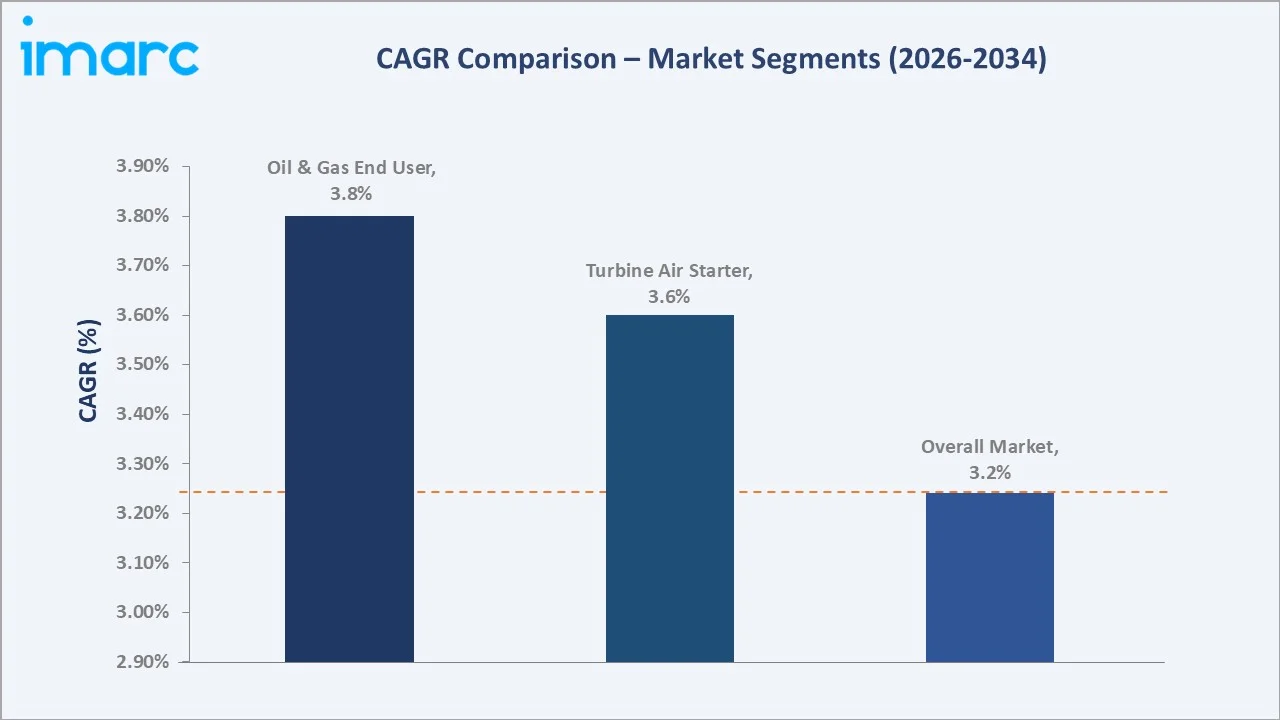

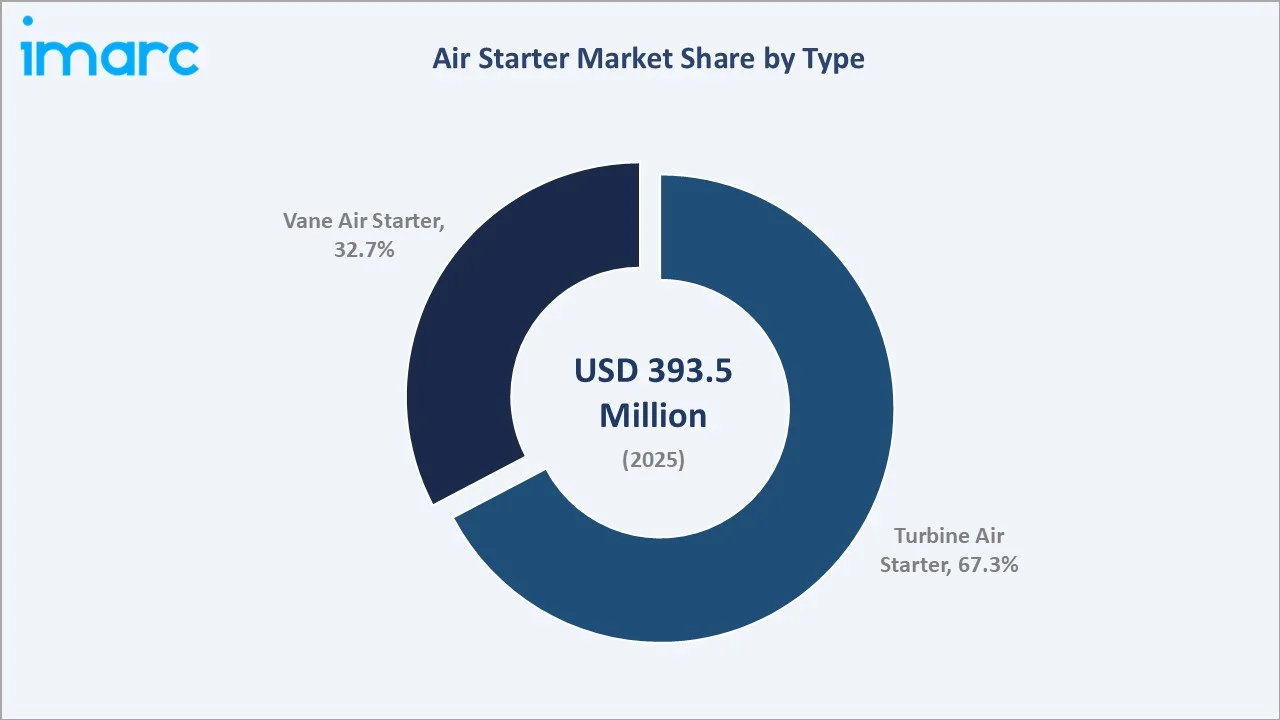

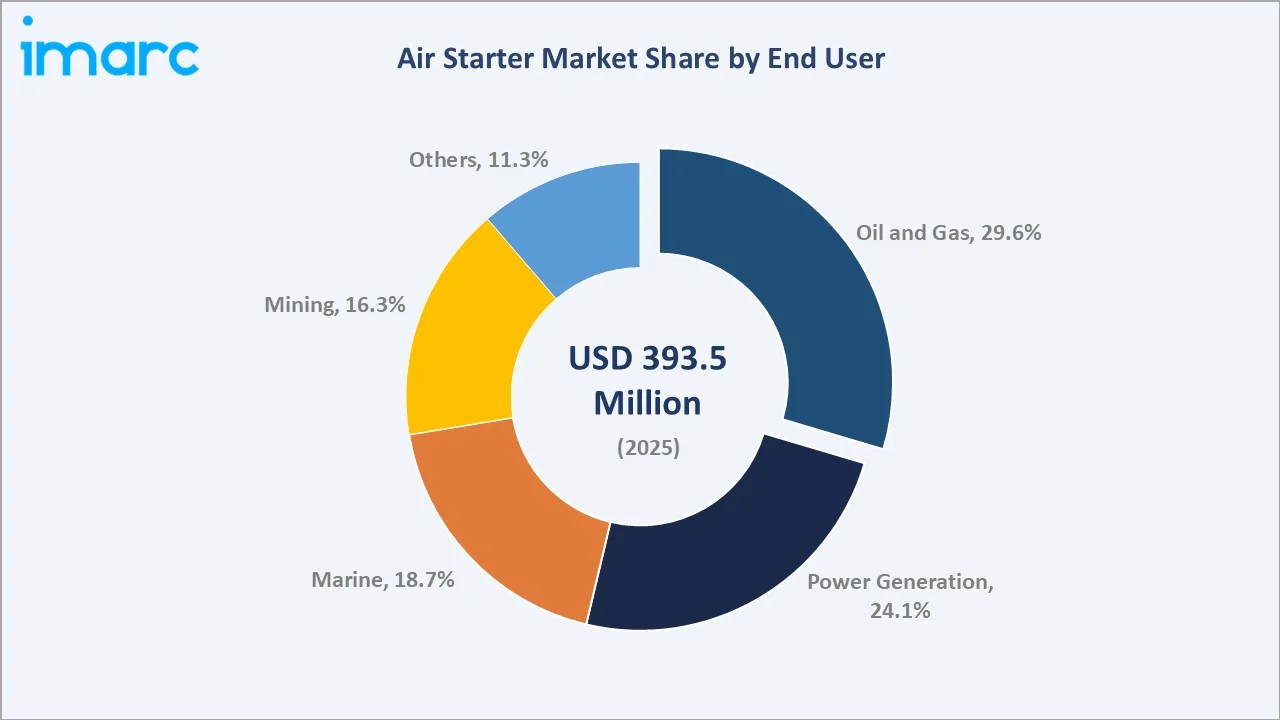

Turbine air starters hold a 67.3% type segment share in 2025, preferred in high-power applications for their high power-to-weight ratio and rapid starting capability. Vane air starters at 32.7% serve medium-duty applications in industrial compressors, gensets, and marine auxiliary engines. Oil & gas leads end-user demand at 29.6%, followed by power generation (24.1%), marine (18.7%), and mining (16.3%).

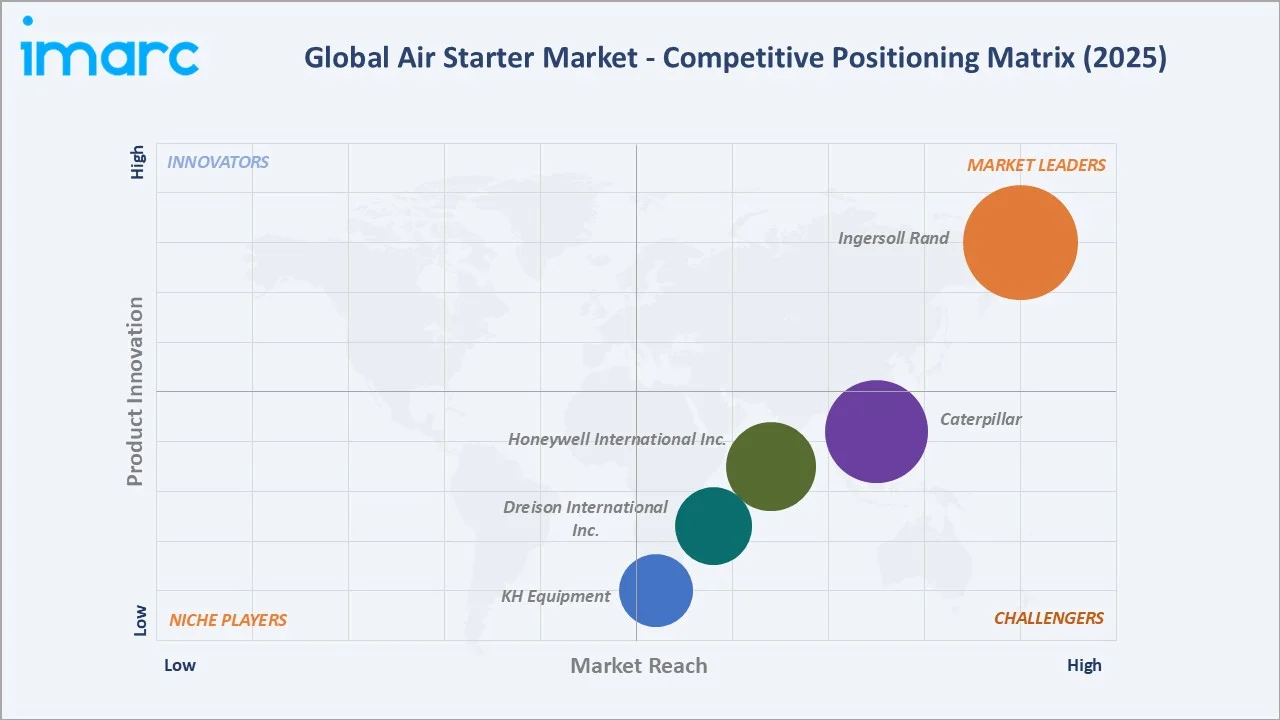

Key players, including Ingersoll Rand, Caterpillar, Honeywell International Inc., Dreison International, Inc., and KH Equipment, compete through product breadth, ATEX/IECEx certification coverage, aftermarket service networks, and engineering customization capabilities for application-specific starting torque and air consumption requirements.

Key Market Insights

| Insight | Data |

|---|---|

| Largest Type Segment | Turbine Air Starter – 67.3% share (2025) |

| Fastest Growing Type | Turbine Air Starter – ~3.60% CAGR (2026-2034) |

| Largest End-User Segment | Oil and Gas – 29.6% share (2025) |

| Fastest Growing End User | Oil and Gas – ~3.80% CAGR driven by upstream capex growth |

| Leading Region | North America – 34.4% share (2025) |

| Top Companies | Ingersoll Rand, Caterpillar, Honeywell International Inc., Dreison International, Inc., and KH Equipment |

Key Analytical Observations:

- Turbine air starters command a 67.3% market share in 2025. Their dominance reflects their critical role in starting large gas turbines, diesel engines, and reciprocating compressors in oil & gas refineries, power plants, marine vessels, and mining applications. Turbine starters generate high torque from a compact, lightweight package, making them irreplaceable in weight- and space-constrained installations where electrical equivalents would be impractical or hazardous.

- Vane air starters at 32.7% (2025) serve medium-duty starting applications where lower starting torque is sufficient, industrial air compressors, gensets, and auxiliary marine engines typically rated below 500 kW.

- Oil & gas dominates end-user demand at 29.6% (2025), driven by the large global installed base of gas turbine compressor trains, emergency generator sets, and reciprocating compressors across upstream, midstream, and downstream facilities that require periodic air starter replacement on lifecycle cycles of 3–7 years.

- North America's 34.4% (2025) regional leadership reflects the US Gulf of Mexico upstream infrastructure, large North American onshore shale gas compression fleet, substantial midstream pipeline compressor station network, and the region's mature industrial air starter aftermarket supply ecosystem.

Air Starter Market Overview

An air starter uses compressed air to crank and start industrial engines and gas turbines via a turbine wheel or vane rotor that drives the engine crankshaft or turbine spool. Air starters are the mandated starting technology in ATEX and IECEx-classified hazardous areas where electrical spark ignition risk prohibits electric starters, including oil & gas refineries, offshore platforms, and underground mining environments.

The market serves five primary end-user verticals: oil & gas, power generation, marine, mining, and other industrial applications. The aftermarket includes replacement starters, repair kits, and service contracts, representing an estimated 40–45% of total market revenue, generating stable, recurring income streams for established suppliers.

Market Dynamics

To evaluate market opportunities, Request Sample

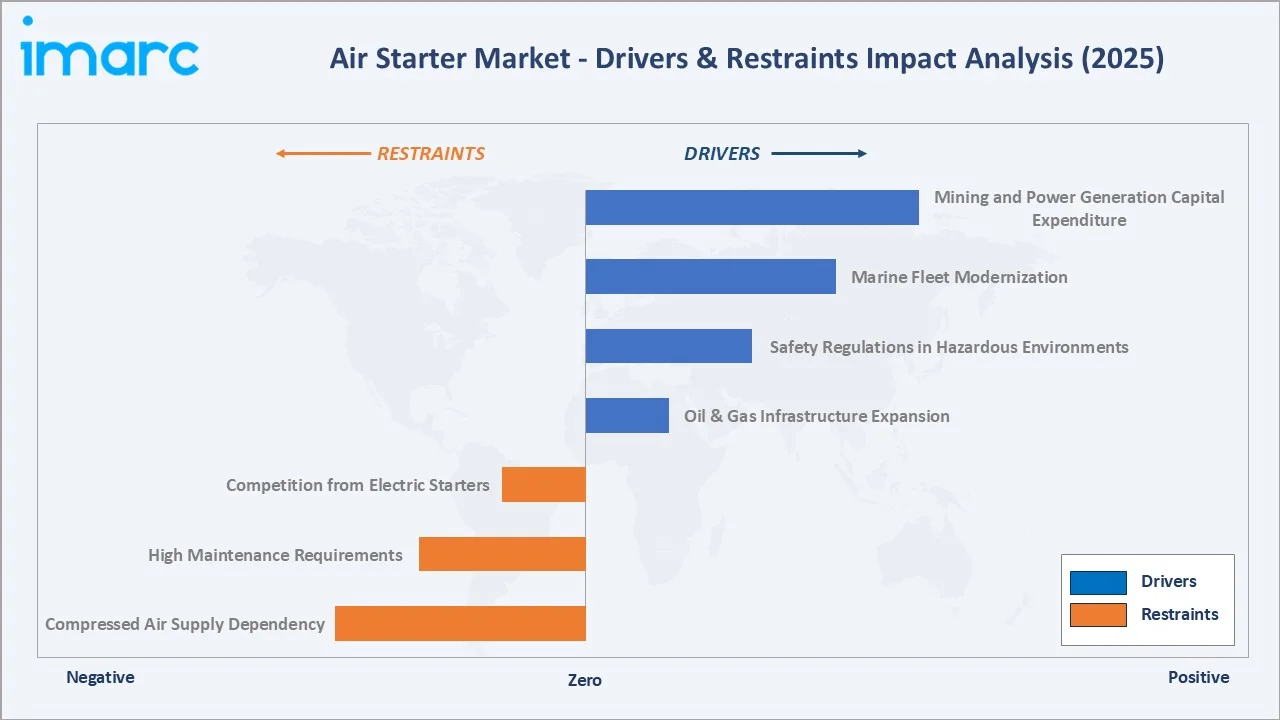

Market Drivers

- Oil & Gas Infrastructure Expansion: Global upstream oil & gas capital expenditure is recovering to pre-pandemic levels, with the IEA estimating USD 570 Billion in upstream investment in 2025. Each new gas turbine compressor station, LNG liquefaction train, or offshore platform installation incorporates multiple air starter units.

- Safety Regulations in Hazardous Environments: ATEX Directive (EU), NEC 505 (North America), and IECEx standards mandate the use of non-electrical starting systems in classified hazardous areas, environments where flammable gases, vapors, or combustible dust create explosion risks.

- Marine Fleet Modernization: The global commercial shipping fleet, estimated at 112,500 vessels as of January 2025, requires ongoing maintenance and replacement of air starters for main engines and auxiliary generators. New vessel construction programs, particularly in LNG carriers, offshore support vessels, and bulk carriers, are generating incremental air starter demand.

- Mining and Power Generation Capital Expenditure: Global mining investment is growing at approximately 5% annually, driven by copper, nickel, cobalt, and lithium demand for energy transition. Underground mining equipment requires air starters for diesel engine starting where ATEX compliance is mandatory.

Market Restraints

- Competition from Electric Starters: In non-hazardous industrial applications, electric starters offer advantages including simpler installation, lower maintenance burden, and easier remote monitoring integration. As battery and motor technology improves, electric starting systems are increasingly competitive in medium-duty applications where air starters previously had a performance advantage.

- High Maintenance Requirements: Air starters require periodic inspection of vanes, turbine blades, bearings, and air control valves, with typical service intervals of 1,000–3,000 operating hours for heavy-duty applications. Maintenance in remote or offshore locations is logistically challenging and costly, creating operational friction for end users.

- Compressed Air Supply Dependency: Air starters require a reliable source of compressed air at specified pressure (typically 90–150 psi) and volume. In facilities where compressed air infrastructure is unavailable, the capital cost of installing dedicated air receivers and supply piping adds high cost to air starter adoption.

Market Opportunities

- LNG Infrastructure Growth: The global LNG supply chain expansion, driven by European energy security demand and Asian LNG import terminal construction, is creating sustained air starter demand in liquefaction trains, regasification terminals, and LNG carrier vessels.

- Aftermarket and Maintenance Services: The estimated 40–45% aftermarket share of air starter revenues is growing steadily as the global installed base of air starters ages. Extended maintenance contracts, certified rebuild programs, and original-equipment-equivalent spare parts programs provide recurring, high-margin revenue streams that are less cyclical than new equipment sales.

Market Challenges

- Cyclicality of Oil & Gas Capital Expenditure: Air starter demand in the oil & gas segment, which accounts for 29.6% of end-user demand, is directly correlated with upstream capital expenditure cycles. Oil price volatility-driven capex reductions can cause sharp demand contractions in the new equipment segment, creating revenue volatility for suppliers heavily exposed to greenfield oil & gas project demand.

- Specialist Technical Knowledge Requirements: Air starter selection, installation, and maintenance require specialized knowledge of compressed air system engineering, ATEX hazardous area classification, and engine-specific starting torque profiles. The shortage of qualified pneumatic systems engineers constrains air starter adoption in underdeveloped regions.

Emerging Market Trends

1. ST2000 Inline Turbine Technology Advancement

Ingersoll Rand's ST2000, launched in March 2023, features a single-stage solid billet aluminum inline turbine motor delivering 70 hp in a 40-pound package with optimized air consumption. Covering engines from 15 to 150 liters, the ST2000 sets the industry benchmark for power density and air efficiency that competitors are targeting in their R&D programs.

2. IoT-Enabled Predictive Maintenance Integration

Air starter suppliers are developing smart monitoring accessories that attach to existing starter housings, measuring vibration signatures, air pressure, cycle count, and temperature to predict maintenance requirements before failure. Connected monitoring transforms air starters from passive mechanical components into data-generating assets within industrial IoT platforms.

3. ATEX and IECEx Certification Scope Expansion

Leading suppliers are expanding their ATEX, IECEx, and region-specific hazardous area certification scope to cover a broader range of air starter models across all temperature classes and equipment protection levels. Certification leadership is a strategic differentiator in oil & gas, petrochemical, and offshore markets where procurement specifications mandate specific certification types.

4. Lightweight Composite Materials for Marine Applications

Marine applications are driving demand for lightweight air starter designs using composite housings and aluminum alloys to reduce vessel topside and engine room weight budgets. LNG carrier and offshore vessel space constraints create demand for compact, high-power turbine starters with reduced installation envelopes.

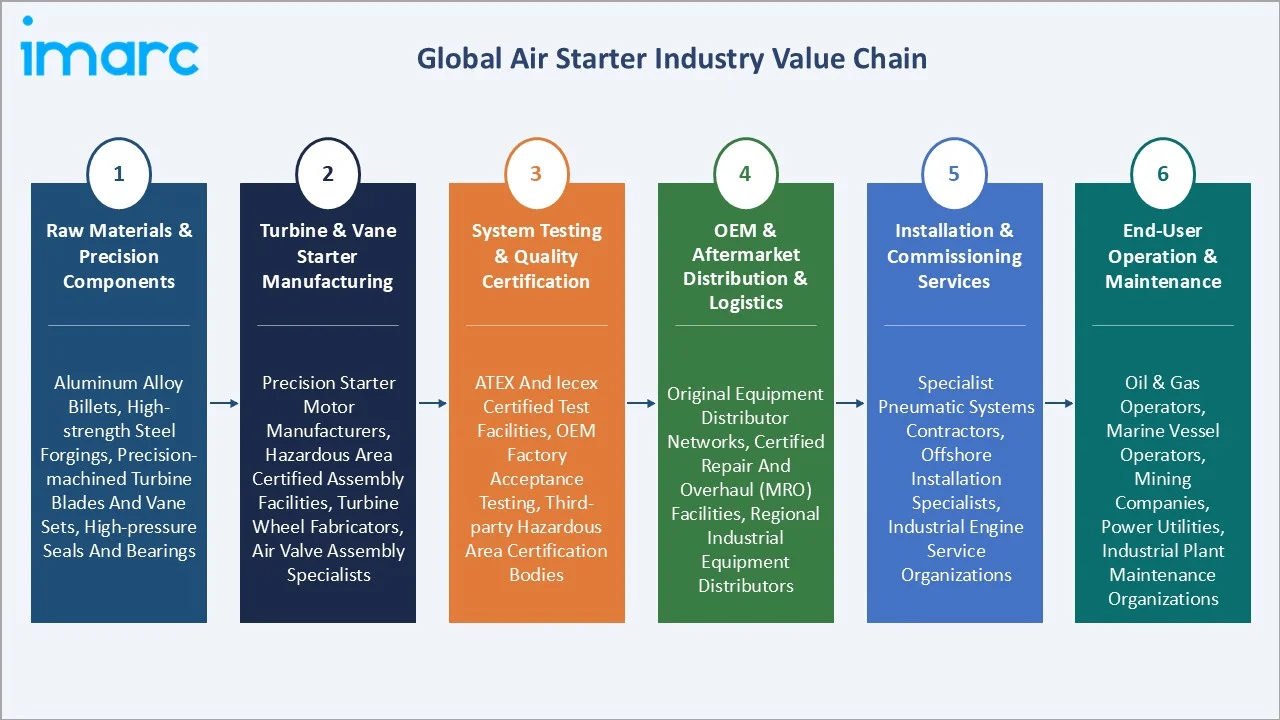

Industry Value Chain Analysis

The air starter value chain extends from precision component manufacturing through hazardous area certified assembly, OEM and aftermarket distribution, and specialist installation and maintenance services in demanding industrial and offshore environments.

| Stage | Key Players / Examples |

|---|---|

| Raw Materials & Precision Components | Aluminum alloy billets, high-strength steel forgings, precision-machined turbine blades and vane sets, high-pressure seals and bearings |

| Turbine & Vane Starter Manufacturing | Precision starter motor manufacturers, hazardous area certified assembly facilities, turbine wheel fabricators, air valve assembly specialists |

| System Testing & Quality Certification | ATEX and IECEx certified test facilities, OEM factory acceptance testing, third-party hazardous area certification bodies |

| OEM & Aftermarket Distribution & Logistics | Original equipment distributor networks, certified repair and overhaul (MRO) facilities, regional industrial equipment distributors |

| Installation & Commissioning Services | Specialist pneumatic systems contractors, offshore installation specialists, industrial engine service organizations |

| End-User Operation & Maintenance | Oil & gas operators, marine vessel operators, mining companies, power utilities, industrial plant maintenance organizations |

Technology Landscape in the Air Starter Industry

Turbine Air Starter Technology

Turbine air starters use a single- or multi-stage axial turbine wheel driven by compressed air at 90–150 psi inlet pressure to generate high rotational torque. Modern single-stage designs deliver superior air efficiency over earlier multi-stage equivalents. Torque outputs range from 100 to 1,500+ ft-lbs, covering engines from 5 to 100+ liters displacement in oil & gas, marine, and power generation applications.

Vane Air Starter Technology

Vane air starters use retractable carbon or composite vanes rotating eccentrically inside a cylindrical housing. Compressed air pressure differentials across the vanes generate torque transmitted through a gear reduction drive. Operating at 80–120 psi inlet pressure, vane starters are suited to facilities with lower compressed air system pressures. Their torque output (50–500 ft-lbs) serves medium-duty gensets, auxiliary marine engines, and industrial compressors.

Aftermarket Rebuild and Overhaul Technology

Air starters are highly rebuildable; OEM and third-party turbine, vane, bearing, and seal kits enable field or workshop rebuild to as-new specification at 30–50% of new unit cost. Ingersoll Rand's certified repair network set the industry aftermarket standard, creating recurring, high-margin revenue that complements new unit sales.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Turbine Air Starter | 67.3% | 2025 |

| End User | Oil and Gas | 29.6% | 2025 |

| Region | North America | 34.4% | 2025 |

By Type

Turbine air starters lead with a 67.3% market share in 2025. Their dominance reflects the high-power starting requirements of the market's primary end-user verticals, oil & gas compressor turbine drivers, marine main engines, mining haul trucks, and gas turbine generators, where only turbine starters provide the required torque at competitive weight and size.

To access detailed market analysis, Request Sample

Vane air starters represent 32.7% of the market in 2025, serving medium-duty starting applications where turbine starters' higher cost and air consumption cannot be economically justified. The vane starter segment is dominated by established aftermarket supply from regional distributors and specialist rebuild shops serving the large installed base of vane starters in industrial facilities.

By End User

Oil and gas dominates end-user demand at 29.6% in 2025. The global oil & gas industry operates an estimated 250,000+ air-starter-equipped engines and turbines across upstream, midstream, and downstream facilities. Replacement cycles of 3–7 years per unit create a large, predictable recurring demand base that anchors the market's growth trajectory.

Power generation represents 24.1% of end-user demand, driven by the large global installed base of gas turbine and diesel generating sets. Marine accounts for 18.7%, with new vessel construction and fleet maintenance creating consistent demand. Mining at 16.3% reflects the mandatory use of air starters in underground diesel equipment across ATEX-classified environments.

Regional Market Insights

North America leads the global air starter market with a 34.4% share in 2025. The region's dominance reflects its large oil & gas infrastructure base, substantial industrial engine installed base, and the presence of the world's largest air starter manufacturer, Ingersoll Rand, whose North American production and distribution operations serve both domestic and export markets.

Europe's 26.1% share is anchored by its large North Sea and Norwegian Continental Shelf oil & gas operations, the world's largest concentration of maritime shipping registrations requiring marine engine air starters, and the region's strict ATEX regulatory environment that mandates certified air starters in all classified industrial zones.

| Region | Share (2025) | Key Growth Drivers |

|---|---|---|

| North America | 34.4% | Large oil & gas infrastructure installed base, major air starter manufacturer presence, substantial shale gas compression fleet, mature aftermarket replacement demand cycle |

| Europe | 26.1% | North Sea oil & gas operations, large marine fleet maintenance demand, stringent ATEX regulatory requirements driving certified air starter adoption, industrial manufacturing sector MRO demand |

| Asia-Pacific | 22.8% | Australian LNG infrastructure, Southeast Asian oil & gas expansion, Chinese and Indian power generation investment, growing mining sector capex |

| Middle East & Africa | 9.4% | GCC oil & gas capital projects, large midstream compressor station installations in Saudi Arabia and UAE, growing power generation infrastructure |

| Latin America | 7.3% | Brazilian oil & gas deepwater operations, mining equipment demand in Chile, Peru, and Colombia, growing LNG infrastructure investment |

Competitive Landscape

The global air starter market is moderately fragmented. Ingersoll Rand holds the dominant global position, estimated at 25–30% of revenues, through its comprehensive turbine and vane starter product portfolio, global service network, and established OEM relationships with major engine and gas turbine manufacturers.

| Company Name | Brand | Market Position | Core Strength |

|---|---|---|---|

| Ingersoll Rand | Ingersoll Rand | Market Leader | Extensive global service network, broad OEM coverage, internationally certified portfolio |

| Caterpillar | Cat | Strong Challenger | Deep OEM integration across major engine platforms, mining and oil & gas foothold |

| Honeywell International Inc. | Honeywell | Challenger | Aerospace-grade engineering pedigree, advanced turbine starting expertise |

| Dreison International, Inc. | Pow-R-Quik | Challenger | North American aftermarket expertise, custom engineering for demanding applications |

| KH Equipment | Austart | Challenger | Dominant Asia-Pacific presence, mining and marine specialization, OEM supply relationships |

The competitive landscape below the market leader includes several established niche players with regional and application-specific strengths.

Key Company Profiles

Ingersoll Rand

Ingersoll Rand is one of the global market leaders in air starter systems. The company offers the most comprehensive air starter product range globally, covering turbine and vane starters for engine displacements from 2 liters to 150+ liters across all major industrial end markets.

- Product Portfolio: ST400, ST900, ST2000 turbine air starters; pneumatic starting systems for industrial, marine, oil & gas, and mining applications; certified rebuild and overhaul service programs.

- Recent Development: Ingersoll Rand reported Q1 2026 revenue of USD 1.85 billion, up 8% year-on-year, with orders rising 5% to USD 1.98 billion. Growth was supported by strong Precision and Science Technologies performance, where revenue increased by 10%.

- Strategic Focus: ST2000 global market penetration, IoT-enabled predictive maintenance integration, global OEM and aftermarket service network expansion, and compressed air system portfolio broadening through strategic acquisitions.

Caterpillar

Caterpillar is one of the global leaders in construction, mining, and energy equipment with a significant air starter business serving its own engine ecosystem and the broader industrial market.

- Product Portfolio: Proprietary air starters for Cat C175 and ACERT diesel engines, Cat gas turbine starting systems for power generation, aftermarket air starter kits for Cat engine platforms in mining and oil & gas applications.

- Recent Developments: Caterpillar reported first-quarter 2026 sales and revenues of USD 17.4 billion, up 22% year-on-year, mainly driven by USD 2.3 billion in higher sales volume and USD 426 million in favorable pricing.

- Strategic Focus: Captive engine ecosystem air starter optimization, mining sector OEM integration, aftermarket parts and service revenue growth, and air starter product development aligned with Cat's Tier 4 Final and Stage V emission-compliant engine platforms.

Market Concentration Analysis

The air starter market is moderately fragmented. Ingersoll Rand holds an estimated 25–30% revenue share, with the other top players (Caterpillar, Honeywell International Inc., Dreison International, Inc., KH Equipment) collectively accounting for approximately 55–60% of global revenues in 2025.

M&A activity is gradually consolidating the market. Ingersoll Rand's ~8–10 acquisitions in 2024 included businesses that complement its air treatment and gas management capabilities alongside core air starter demand. The market's moderate fragmentation creates ongoing consolidation opportunities as leading players seek to acquire regional distributors and certification-holding manufacturers to broaden their geographic and application coverage.

Investment & Growth Opportunities

Fastest Growing Segments

Turbine air starters (~3.60% CAGR), LNG infrastructure starting systems, offshore oil & gas aftermarket replacement, and IoT-enabled smart air starters represent the highest-growth investment vectors through 2034. Together, these sub-segments address a combined incremental addressable market of approximately USD 90 Million by 2034 within the global air starter ecosystem.

Emerging Market Expansion

Africa, Southeast Asia, and South America collectively represent a USD 40+ Million incremental opportunity by 2034. Local content requirements in these markets favor regional partnership strategies, with global suppliers licensing manufacturing rights or establishing joint ventures with local industrial equipment distributors to qualify for major oil & gas project procurement programs.

Venture and Institutional Investment Trends

- Global LNG infrastructure investment exceeding USD 100 Billion through 2030 creates a sustained pipeline of high-value turbine air starter procurement, as each LNG liquefaction train incorporates multiple high-power air starters for compressor turbine starting.

- Mining sector electrification paradox: while some surface mining operations are transitioning to electric haul trucks, underground mining continues to require diesel-powered equipment with air starters due to ATEX requirements and the impracticality of battery-electric systems in deep underground environments.

- Aftermarket service contract models are attracting institutional interest as they provide recurring revenue with high retention rates; air starter MRO customers typically re-sign with OEM service providers due to certification and parts availability advantages.

Future Market Outlook (2026-2034)

The air starter market is positioned for steady growth through 2034. From USD 393.5 Million in 2025, the market will reach USD 530.3 Million by 2034, representing incremental value of USD 136.8 Million at a 3.24% CAGR. Growth is anchored by non-discretionary replacement demand in oil & gas, marine, and mining facilities, combined with greenfield LNG and power generation infrastructure demand.

Turbine air starters will extend their market share lead as the proportion of high-power industrial engine applications grows relative to medium-duty vane starter applications. IoT connectivity and predictive maintenance integration will become standard features in new turbine starter generations by 2030, creating digital service revenue streams alongside hardware sales.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 85 industry participants in 2024–2025, including air starter engineers, oil & gas procurement managers, marine vessel operators, mining equipment maintenance managers, and industrial distributors across North America, Europe, and Asia-Pacific. Expert input validated market sizing, technology trends, and end-user adoption dynamics.

Secondary Research

Secondary research encompassed supplier annual reports, ATEX and IECEx regulatory documentation, IEA oil & gas investment statistics, IMO fleet data, mining industry capex reports, and trade publications including Offshore Technology, Marine Propulsion, and Hydrocarbon Processing.

Forecasting Models

Market size estimations used top-down and bottom-up forecasting incorporating global industrial engine and gas turbine installed base data, air starter replacement cycle assumptions by end-user vertical, average unit selling price trajectories, and new equipment demand from identified capital project pipelines. A base-case CAGR of 3.24% reflects consensus validated against OEM order book disclosures and capital project pipeline data.

Air Starter Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| S cope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Vane Air Starter, Turbine Air Starter |

| End Users Covered | Oil and Gas, Power Generation, Mining, Marine, Others |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Ingersoll Rand, Caterpillar, Honeywell International Inc., Dreison International Inc., KH Equipment, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the air starter market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global air starter market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the air starter industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Air Starter Market Report

The market reached USD 393.5 Million in 2025 and is projected to reach USD 530.3 Million by 2034 at a 3.24% CAGR.

North America leads with a 34.4% share in 2025, driven by its large oil & gas infrastructure and major air starter manufacturer presence.

Turbine air starters lead with a 67.3% share in 2025, preferred for high-power applications in oil & gas, marine, and power generation sectors.

Oil and gas is the largest end user at 29.6% in 2025, driven by the global installed base of gas turbine compressors and reciprocating engines requiring air starting.

Ingersoll Rand, Caterpillar, Honeywell International Inc., Dreison International, Inc., and KH Equipment, are some of the leading players in the market.

Air starters are mandated in ATEX and IECEx hazardous areas where electrical systems pose ignition risks. They also offer advantages in weight, starting torque, and compressed air infrastructure compatibility in industrial applications.

Oil & gas infrastructure expansion, safety regulations in hazardous environments, marine fleet modernization, and mining and power generation capital expenditure are the primary drivers.

Competition from electric starters in non-hazardous zones, high maintenance requirements, compressed air supply dependency, and oil & gas capex cyclicality are key challenges.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)