Crane Market Size, Share, Trends and Forecast by Product Type, Application, and Region, 2026-2034

Crane Market Size, Share, Trends & Forecast (2026-2034)

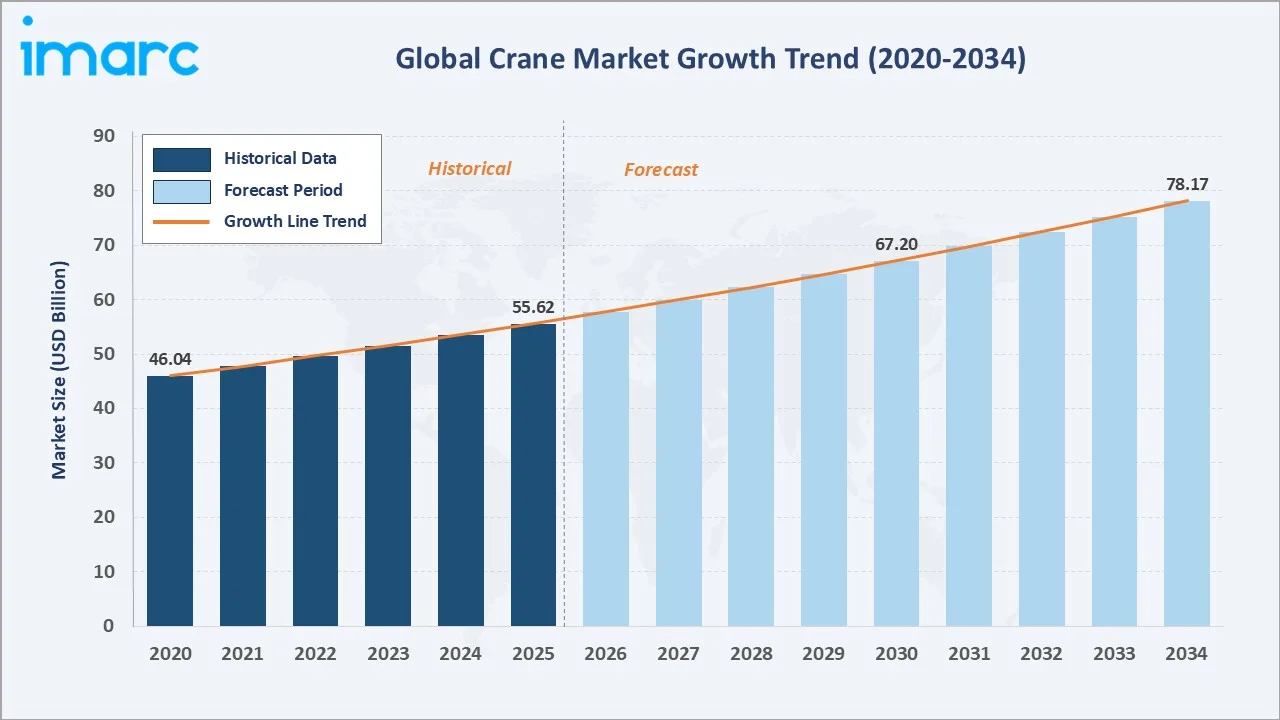

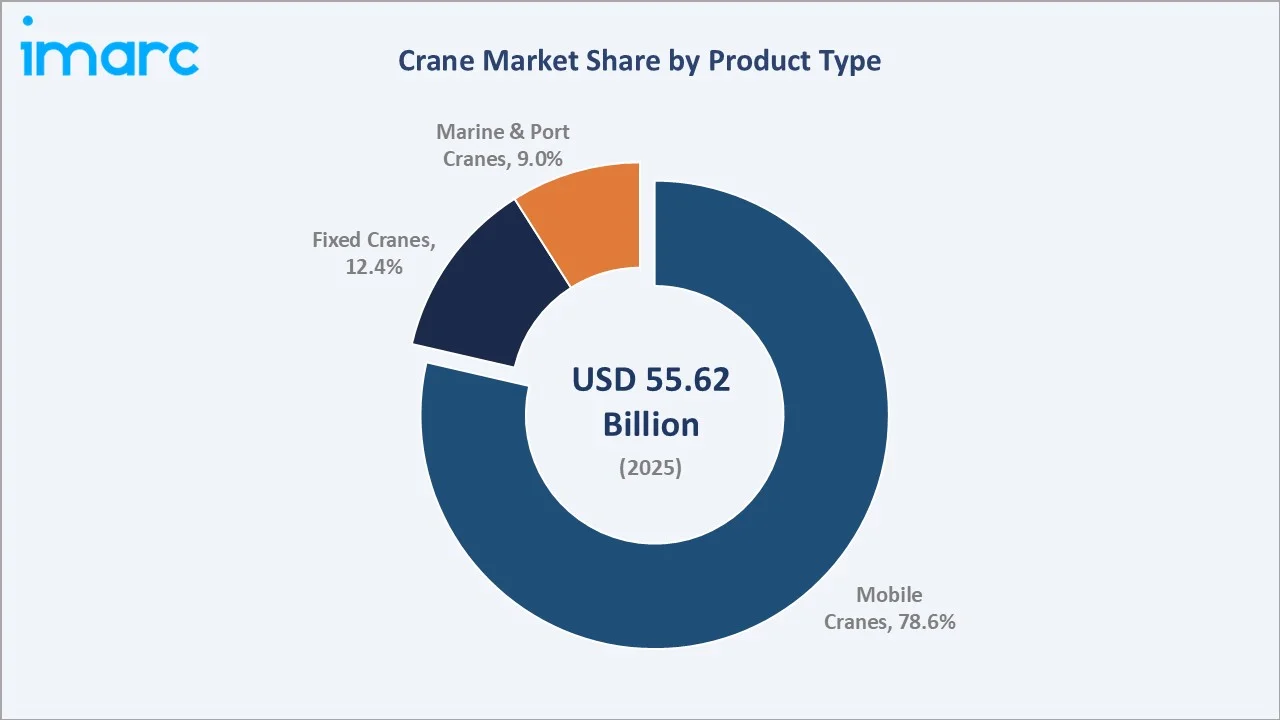

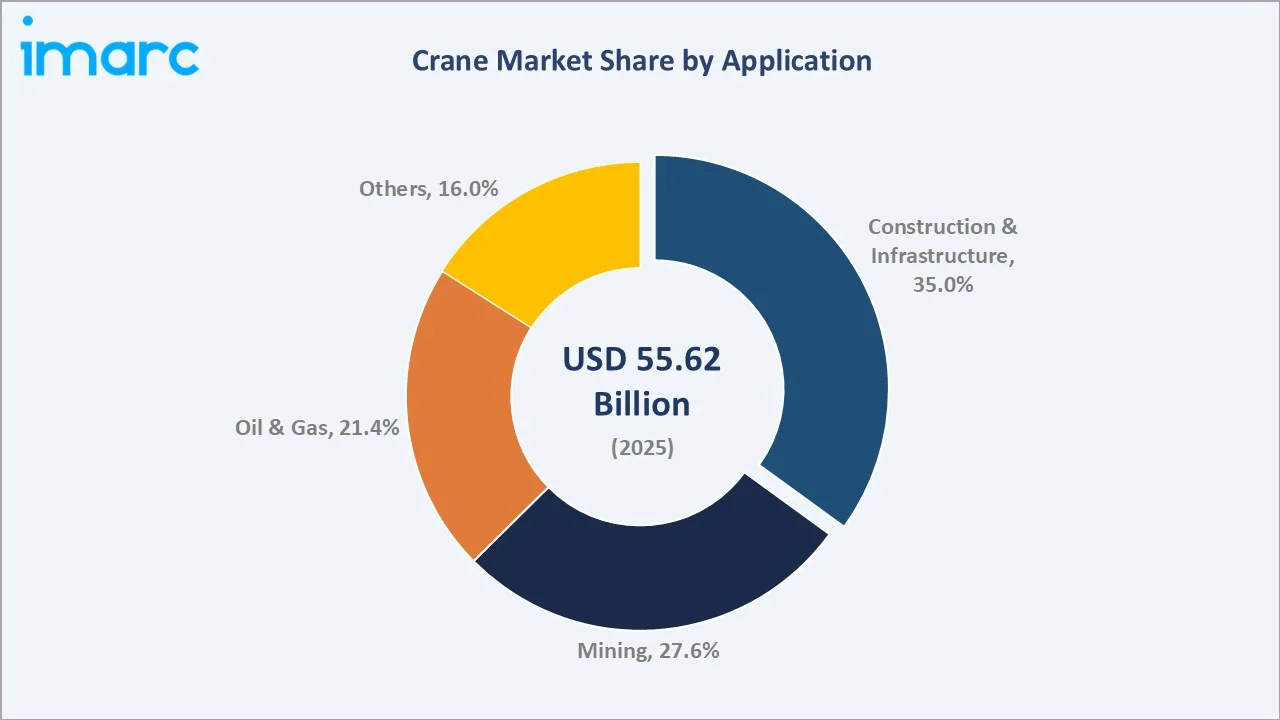

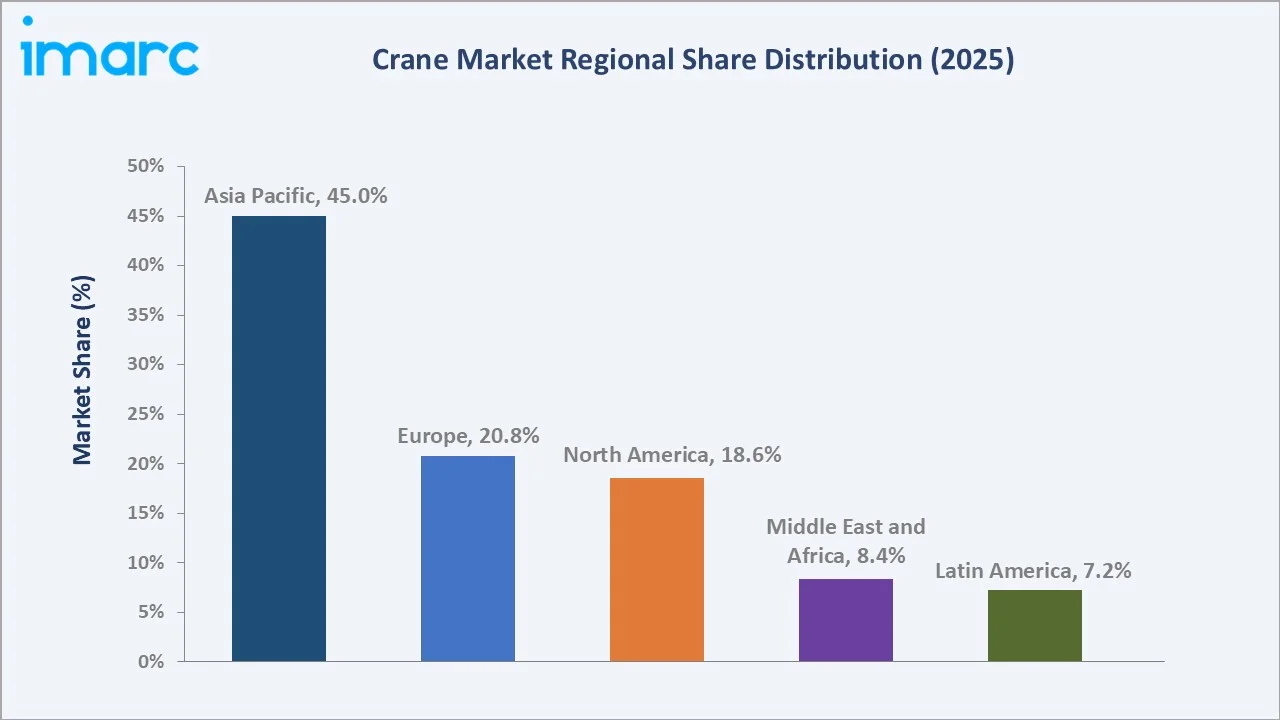

The global crane market reached USD 55.62 Billion in 2025 and is projected to reach USD 78.17 Billion by 2034, growing at a CAGR of 3.85% during 2026-2034. The pipeline of megaprojects, defined as projects costing at least $1 billion, surpassed $3 trillion in 2025. This expanding pipeline of large-scale infrastructure, energy, industrial, and urban development projects is accelerating demand for cranes, as these projects require heavy lifting equipment for material handling, high-rise construction, bridge assembly, port expansion, and installation of large structural components across multiple construction phases. Mobile cranes dominate at 78.6%. Construction and infrastructure lead application at 35.0%. Asia Pacific commands 45.0% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 55.62 Billion |

|

Forecast Market Size (2034) |

USD 78.17 Billion |

|

CAGR (2026-2034) |

3.85% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Mobile Cranes (78.6%, 2025) |

|

Dominant Application |

Construction & Infrastructure (35.0%, 2025) |

|

Leading Region |

Asia Pacific (45.0%, 2025) |

The market expanded from USD 46.04 Billion in 2020 to USD 55.62 Billion in 2025, anchored at USD 67.20 Billion in 2030, and forecast to reach USD 78.17 Billion by 2034. COVID-19's 2020-2021 supply chain disruption created temporary demand compression before a strong recovery from 2022, driven by government infrastructure stimulus programs and the post-pandemic energy sector capital investment rebound.

To get more information on this market, Request Sample

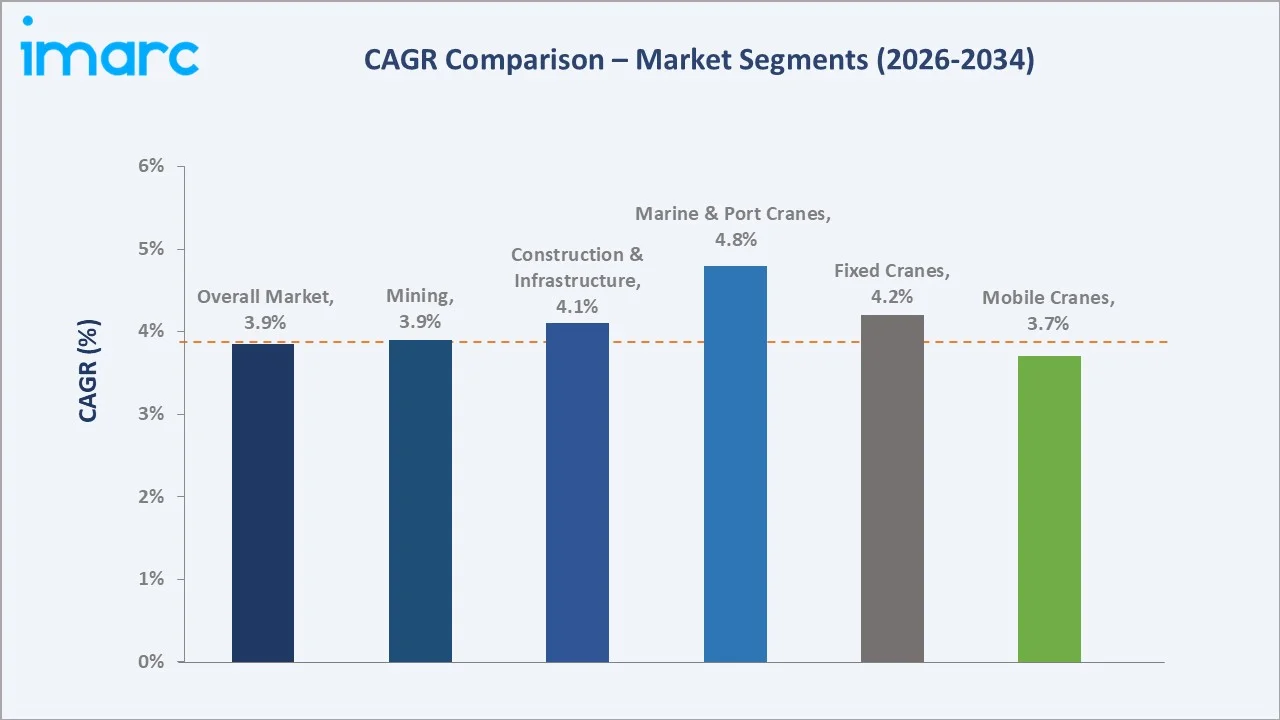

Marine and port cranes grow fastest at ~4.8% CAGR as global container trade expansion, offshore wind energy installation vessel demand, and port automation investment simultaneously drive marine crane procurement. Fixed cranes grow at ~4.2% CAGR through high-rise construction and industrial overhead crane demand in the Asia Pacific's manufacturing and assembly industries. Mobile cranes at ~3.7% CAGR grow steadily through construction activity, driven by the largest installed base requiring both new unit sales and replacement cycles.

Executive Summary

The global crane market reached USD 55.62 Billion in 2025, representing the foundation of global heavy construction, industrial, energy, and maritime material handling. Cranes are essential capital equipment for every major category of physical infrastructure; no bridge, high-rise building, wind turbine, offshore platform, or container ship can be built without cranes, making the industry a structural proxy for global fixed capital formation. The market's 3.85% CAGR reflects the steady compounding of global infrastructure investment, energy transition capital expenditure, and mining industry reinvestment against the backdrop of cyclical construction market volatility. The market is projected to reach USD 78.17 Billion by 2034.

Mobile cranes at 78.6% dominate through their versatility across all application categories. Construction and infrastructure at 35.0% leads application driven by Asia Pacific's construction intensity, North America's infrastructure investment cycle, and Middle East mega-project activity. Asia Pacific at 45.0% leads through China's manufacturing and construction dominance alongside India and Southeast Asia's rapid growth.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Mobile Cranes - 78.6% share (2025) |

|

Dominant Application |

Construction & Infrastructure - 35.0% market share (2025) |

|

Leading Region |

Asia Pacific - 45.0% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Mobile Cranes at 78.6% reflecting the versatility advantage that positions mobile cranes as the default crane type for the majority of global lifting requirements: Mobile cranes' market dominance is structurally sustained by three advantages that fixed and marine cranes cannot replicate. First, deployment flexibility. Second, capacity scalability. Third, ownership economics.

- Construction and Infrastructure at 35.0% as the crane market's fundamental demand anchor driven by global fixed capital formation: Construction and infrastructure's 35.0% application share reflects that cranes are inseparable from physical infrastructure creation; every bridge, building, dam, power plant, and industrial facility requires cranes during construction.

- Asia Pacific at 45.0% through China's manufacturing dominance, combined with India's emerging construction crane market and ASEAN's project-driven growth: Asia Pacific's 45.0% global crane market share reflects China's unique position as simultaneously the world's largest crane consumer and the world's largest crane manufacturer.

Crane Market Overview

The global crane market encompasses the design, manufacture, distribution, rental, operation, and servicing of mechanical lifting equipment across mobile, fixed, and marine product types for applications in construction, mining, oil and gas, port handling, and industrial operations worldwide. Cranes range in capacity from 1-tonne workshop hoists to 5,000-tonne heavy-lift gantry cranes, in mobility from truck-mounted all-terrain cranes to permanently installed overhead traveling cranes, and in technology from manually controlled basic units to AI-guided fully autonomous container handling systems.

The ecosystem integrates high-strength steel and component suppliers, crane OEMs across the premium-to-value spectrum, global dealer and rental networks, EPC project contractors integrating crane equipment into major project delivery, end-user operators, and regulatory bodies enforcing lift plan approval, crane operator certification, and equipment inspection requirements. Macroeconomic factors include rising infrastructure investments, rapid urbanization, industrial expansion, and increasing government spending on transportation, energy, and smart city projects.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

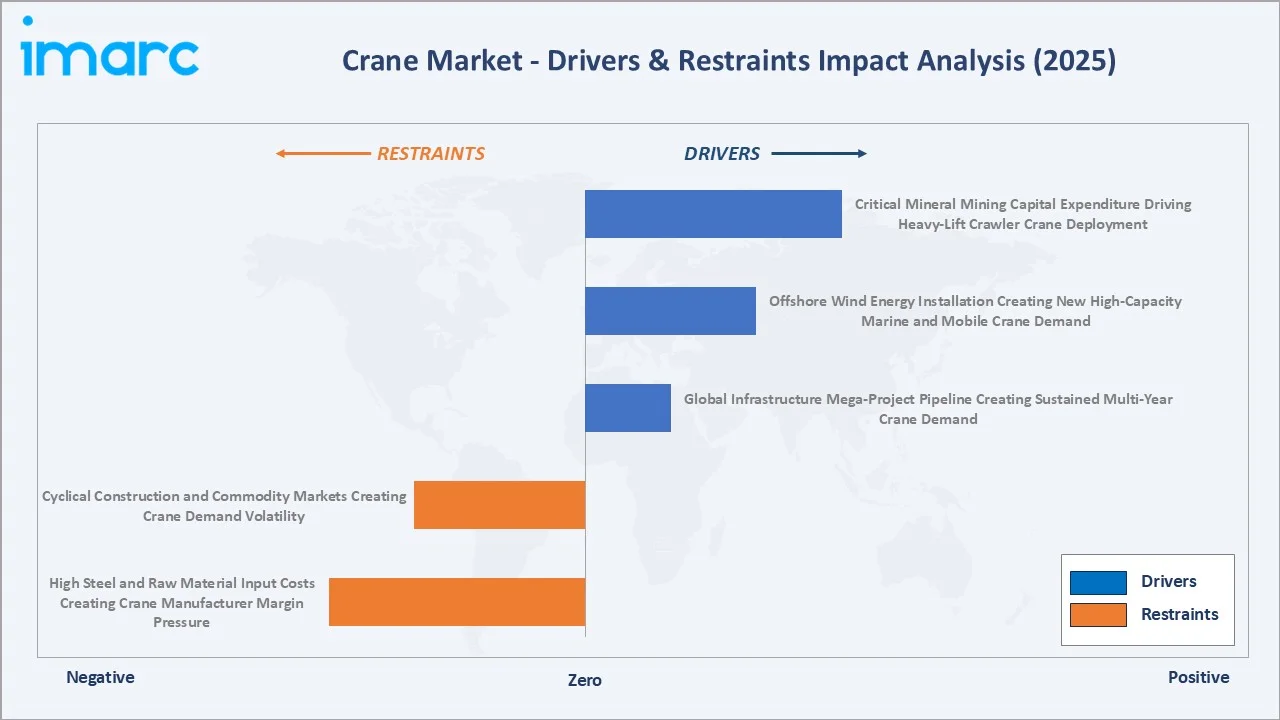

- Global Infrastructure Mega-Project Pipeline Creating Sustained Multi-Year Crane Demand: The pipeline of megaprojects, projects costing at least $1 billion, exceeded over $3 trillion in 2025. This rising pipeline of global infrastructure megaprojects, including airports, rail corridors, smart cities, renewable energy parks, ports, and industrial complexes, is creating sustained long-term demand for cranes across construction and heavy engineering activities. These multi-year projects require high-capacity tower, crawler, mobile, and gantry cranes for lifting heavy materials, steel structures, turbines, and prefabricated components throughout different

- Offshore Wind Energy Installation Creating New High-Capacity Marine and Mobile Crane Demand: The global offshore wind energy sector's 500 GW installation pipeline by 2030 represents the single largest new demand driver for specialized crane equipment. Each offshore wind turbine installation requires specialized heavy-lift vessels equipped with offshore installation cranes.

- Critical Mineral Mining Capital Expenditure Driving Heavy-Lift Crawler Crane Deployment: The energy transition's demand for lithium (battery storage), cobalt (EV batteries), copper (renewable energy wiring and EV motors), nickel (EV battery cathodes), and rare earth elements (permanent magnets for wind turbines and EV motors) is driving unprecedented mining capital expenditure in geographies that have historically had limited crane market development. Each large-scale mining capital project requires heavy-lift cranes during construction, with crawler crane capacity from 200-2,000 tonnes, depending on process equipment lift weights.

Market Restraints

- High Steel and Raw Material Input Costs Creating Crane Manufacturer Margin Pressure: Rising steel and raw material prices are increasing production costs for crane manufacturers, putting pressure on profit margins and limiting pricing flexibility. Higher equipment costs also discourage purchases among construction and industrial contractors, particularly in price-sensitive markets, thereby slowing crane demand and fleet expansion activities.

- Cyclical Construction and Commodity Markets Creating Crane Demand Volatility: The crane market is highly dependent on construction, mining, oil and gas, and infrastructure activities, making it vulnerable to cyclical fluctuations in commodity prices and economic conditions. Slowdowns in real estate development, industrial investments, or energy projects often lead to delayed capital expenditure and reduced equipment rentals or purchases, creating demand volatility for crane manufacturers and rental providers.

Market Opportunities

- Zero-Emission and Hybrid-Electric Crane Development Creating Premium Replacement Demand: The development of zero-emission and hybrid-electric cranes is encouraging fleet modernization across construction, ports, mining, and urban infrastructure projects. Stricter environmental regulations and corporate sustainability targets are increasing demand for low-emission lifting equipment with improved fuel efficiency and reduced operating costs. These advanced cranes are also gaining traction in indoor and urban construction environments where noise and emission restrictions are becoming more stringent.

- Digital Crane Management and Telematics Creating New Service Revenue Streams: Crane OEMs are developing telematics and digital management platforms that create subscription-based service revenue above one-time crane sales. For crane rental companies managing fleets of 500-2,500 cranes, telematics platforms provide operational visibility that improves fleet utilization, reduces unauthorized crane operation, and enables proactive maintenance scheduling that extends crane major overhaul intervals and reduces unplanned downtime.

Market Challenges

- Chinese Manufacturer Competition Pricing Pressure on Western OEM Premium Positioning: Aggressive pricing strategies by Chinese crane manufacturers are intensifying competition in global markets, putting pressure on Western OEMs that traditionally operate in the premium equipment segment. Lower-cost alternatives are reducing pricing power and profit margins for established manufacturers, while also increasing market share competition across emerging and price-sensitive regions.

- Project Execution Delays and Capital Cycle Timing Mismatches Affecting Crane Order Backlog: Large crane orders have 12-24 month delivery lead times from order to delivery, creating timing mismatches with project execution schedules that frequently slip due to permitting delays, contractor financing constraints, and supply chain disruptions.

Emerging Market Trends

1. Zero-Emission and Hydrogen Fuel Cell Crane Technology Entering Commercial Production

The commercialization of zero-emission and hydrogen fuel cell crane technologies is emerging as industries prioritize sustainability and compliance with stricter emission regulations. In October 2025, Konecranes unveiled its Noell Hydrogen Fuel Cell Straddle Carrier at the TOC Americas 2025 event in Panama City, marking its introduction to the Americas and global markets. The company also showcased its E-Hybrid RTG and electric empty container handler, highlighting its ongoing efforts to expand a comprehensive portfolio of low- and zero-tailpipe-emission material handling solutions.

2. Autonomous and Semi-Autonomous Crane Operation Reducing Operator Dependency

The adoption of autonomous and semi-autonomous crane technologies is emerging as companies seek to improve operational efficiency, safety, and productivity. Advanced automation systems, AI-powered controls, collision avoidance technologies, and remote operation capabilities are reducing dependence on skilled crane operators while minimizing human error and downtime. These solutions are gaining traction across ports, warehouses, mining operations, and large-scale construction projects where labor shortages and safety concerns remain significant challenges.

3. Rental Market Consolidation Creating National and International Fleet Management Companies

The consolidation of crane rental companies is leading to the formation of large national and international fleet management operators with broader equipment portfolios and geographic reach. Mergers, acquisitions, and strategic partnerships are enabling rental providers to optimize fleet utilization, expand service capabilities, and offer integrated lifting solutions across multiple industries and project locations. This trend is also improving access to technologically advanced cranes and flexible rental models for contractors and infrastructure developers.

4. Offshore Wind Installation Vessel Market Creating Specialized Heavy-Lift Crane Demand

The global offshore wind capacity target of 500 GW by 2030 is creating strong demand for specialized heavy-lift cranes capable of handling large turbines, monopiles, jackets, and subsea components in harsh marine environments. Increasing investments in offshore wind farms are encouraging crane manufacturers to develop high-capacity lifting systems with enhanced stability, precision, and deep-water operational capabilities. This trend is supporting innovation in floating cranes, pedestal cranes, and vessel-mounted lifting solutions designed for large-scale renewable energy projects.

Industry Value Chain Analysis

The global crane value chain integrates raw material procurement, design and engineering R&D, manufacturing and quality testing, sales through dealer and rental networks, site delivery and commissioning, and after-sales service, parts, and overhaul. Premium OEM value addition is highest in the design and engineering stage. Manufacturing value addition represents 35-45% of the crane selling price for standard products and 50-60% for specialized custom-engineered cranes.

|

Stage |

Key Participants |

|

Raw Material Steel & Components |

High-strength steel suppliers, hydraulic system manufacturers, wire rope and bearing suppliers, engine, battery, and electronic control component providers. |

|

Crane Design & Engineering R&D |

Crane manufacturers’ engineering centers focused on structural design, load optimization, automation systems, telematics, safety technologies, and energy-efficient lifting solutions. |

|

Manufacturing & Quality Testing |

Crane manufacturing facilities, load testing companies, safety inspection agencies, and certification bodies ensure compliance |

|

Sales, Dealer & Rental Network |

OEM dealer networks, crane rental companies, regional distributors, and fleet management providers. |

|

Site Delivery, Installation & Commissioning |

Heavy-haul logistics providers, crane transport specialists, and installation contractors. |

|

After-Sales Service, Parts & Overhaul |

OEM service divisions, spare parts suppliers, predictive maintenance and remote monitoring solution providers, and refurbishment and overhaul service companies. |

|

End-Use Industries |

Construction companies, infrastructure developers, mining operators, oil and gas firms, ports and shipyards, manufacturing plants, renewable energy and utility sector operators. |

The after-sales service, parts, and overhaul tier represents crane OEMs' most strategically important competitive differentiator in mature markets. Each major crane overhaul represents 25-40% of the original crane purchase value in service and parts revenue, creating a substantial aftermarket revenue pool that premium OEMs protect through proprietary parts supply and certified service networks that deter independent service competition.

Technology Landscape in the Crane Industry

Hydraulic System Technology

Advanced hydraulic system technologies are improving lifting precision, load control, operational efficiency, and overall equipment reliability. In March 2026, Liebherr introduced the new 195 HC-LH hydraulic luffing jib crane in the United States, designed to address the demands of modern urban construction projects. These innovations are also supporting automation, remote diagnostics, and smoother operation across construction, mining, port, and industrial applications.

Crane Control and Safety Systems

Advanced crane control and safety systems are improving operational accuracy, load stability, and workplace safety across lifting operations. Technologies such as anti-collision systems, load moment indicators, real-time monitoring sensors, AI-assisted controls, and remote operation platforms are helping operators reduce accidents, prevent overload conditions, and enhance productivity. These systems are also supporting automation, predictive maintenance, and compliance with increasingly stringent industrial safety regulations.

Structural Engineering and Materials Technology

Advancements in structural engineering and materials technology are enabling the development of lighter, stronger, and more durable lifting equipment. The use of high-strength steel, composite materials, optimized boom designs, and fatigue-resistant structures is improving load capacity, fuel efficiency, and operational stability while reducing overall equipment weight. These innovations are also enhancing crane performance in high-rise construction, offshore, mining, and heavy industrial applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Mobile Cranes |

78.6% |

2025 |

|

Application |

Construction and Infrastructure |

35.0% |

2025 |

|

Region |

Asia Pacific |

45.0% |

2025 |

By Product Type

Mobile cranes lead at 78.6% market share (2025). The mobile crane category is led by all-terrain cranes, truck cranes, rough-terrain cranes, and crawler cranes. Mobile cranes' versatility across the construction, mining, and oil and gas applications collectively sustains their absolute market dominance.

To access detailed market analysis, Request Sample

Fixed cranes at 12.4% encompass tower cranes, industrial overhead cranes, and gantry cranes. Marine and port cranes at 9.0% grow fastest at ~4.8% CAGR through offshore wind installation vessel cranes, ship-to-shore container cranes, and floating crane systems for major marine construction projects.

By Application

Construction and infrastructure lead at 35.0% market share (2025). The application encompasses residential, commercial, and industrial building construction, bridge and road infrastructure, power plant construction, and renewable energy construction. Mining at 27.6% represents crane deployments for open-pit and underground mine construction and maintenance, ore processing plant installation, and mining equipment maintenance lifts requiring heavy crawlers.

Oil and gas at 21.4% serves offshore platform construction and maintenance, onshore refinery and petrochemical plant construction and turnaround maintenance, and pipeline construction support. Others at 16.0% encompasses power transmission line construction, shipbuilding and dry dock operations, aerospace assembly, utility infrastructure maintenance, and entertainment and event logistics crane applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Crane Market Drivers & Characteristics |

|

Asia Pacific |

45.0% |

Supported by rapid urbanization, large-scale infrastructure development, industrial expansion, and strong construction activities. |

|

Europe |

20.8% |

Characterized by strong adoption of technologically advanced and energy-efficient cranes, supported by infrastructure modernization, offshore wind projects, and stringent workplace safety and emission regulations. |

|

North America |

18.6% |

Supported by investments in commercial construction, energy infrastructure, logistics facilities, and large-scale industrial projects. |

|

Middle East and Africa |

8.4% |

Driven by megaproject developments, smart city initiatives, oil and gas investments, and expanding transportation and tourism infrastructure. |

|

Latin America |

7.2% |

Supported by mining activities, infrastructure upgrades, renewable energy projects, and industrial construction. |

Asia Pacific's 45.0% market share reflects China's unparalleled position as the crane market gravity center. The region's dual structure of high-volume mass-market crane consumption and growing premium crane adoption creates a market that both global OEMs and Chinese manufacturers serve, albeit at different price-quality tiers.

Europe, at 20.8%, is the market's technology leadership region, setting standards for crane safety systems, environmental performance, and telematics that progressively influence global requirements. North America, at 18.6%, is driven by its infrastructure investment cycle and rental-centric business model that concentrates procurement decisions in fleet operators rather than individual contractors. Middle East and Africa, at 8.4%, reflects mega-project construction activity in the GCC and Africa's urbanization and resource extraction growth. Latin America, at 7.2%, is led by Brazil's oil sector, mining industry, and infrastructure concession program alongside regional urbanization construction.

Competitive Landscape

The global crane market's competitive landscape is distinctive in its geographic bifurcation. Western OEMs dominate the premium-quality, technology-intensive segment, while Chinese OEMs dominate by volume in the mid-market and value segments. This bifurcation reflects fundamentally different competitive advantages: Western OEMs compete on engineering excellence, safety certification, global service network, and telematics ecosystem; Chinese OEMs compete on price, domestic market scale, government-backed export financing, and progressively improving quality credentials.

|

Company Name |

Products |

Market Position |

Core Strength |

|

Liebherr |

LTM Mobile Cranes, LTC Compact Cranes, LRT Rough Terrain Cranes, LG Lattice Boom Cranes, LR Crawler Cranes, LTR Telescopic Crawler Cranes |

Market Leader |

Liebherr has stood for a large, continually developing range of sophisticated products and services. |

|

The Manitowoc Company, Inc. |

All Terrain Cranes, Lattice Boom Crawler Cranes, Tower Cranes, Rough Terrain and Truck Mounted cranes, Carrydeck Industrial Cranes |

Market Leader |

Manitowoc, through its wholly-owned subsidiaries, provides high-quality, customer-focused lifting products and services worldwide. |

|

Tadano Ltd |

All Terrain Cranes, City Cranes, Lattice Boom Crawler Cranes, Rough Terrain Cranes, Telescopic Boom Crawler Cranes, Truck Cranes |

Strong Challenger |

Tadano leads the lifting industry because quality is the highest consideration. Tadano cranes deliver exceptional value, durability, and dependability for all project needs. |

|

Konecranes |

Chain hoist cranes, Rope hoist cranes, Gantry cranes, Portable crane, Wall mounted console cranes, Open winch cranes, Custom cranes |

Established Player |

Konecranes overhead cranes utilise the latest technology to increase the safety and productivity of customers’ businesses. |

|

SANY Group |

Truck Cranes, All-terrain Cranes, Rough-terrain Cranes, Truck-mounted Cranes, Crawler Cranes, Tower Cranes, Loader Cranes |

Established Player |

SANY is one of the world’s largest engineering machinery manufacturers. |

The competitive landscape's most significant structural change of 2020-2025 has been the rapid quality improvement and global ambition of Chinese OEMs. Western OEMs' response represents an attempt to maintain value differentiation through technology before Chinese manufacturers close the gap in these areas as well.

Key Company Profiles

Liebherr

Liebherr is the global crane industry's undisputed technical leader. Liebherr has stood for a large, continually developing range of sophisticated products and services. Exceptionally practical, seasoned and proven engineering, as well as a consistent high-quality level, ensure customer benefit in all product areas.

- Key Products: LTM Mobile Cranes, LTC Compact Cranes, LRT Rough Terrain Cranes, LG Lattice Boom Cranes, LR Crawler Cranes, LTR Telescopic Crawler Cranes.

- Recent Developments: In March 2026, Liebherr launched the 195 HC-LH hydraulic luffing jib tower crane in the United States, specifically developed to meet the demands of modern urban construction environments.

- Strategic Focus: Focused on expanding its portfolio of high-capacity, energy-efficient, and technologically advanced cranes for urban infrastructure, industrial, and heavy-lifting applications worldwide.

The Manitowoc Company, Inc.

Manitowoc is one of the world’s most celebrated makers of crawler cranes. Its cranes have remained at the top of the lifting world for a century, and Manitowoc continues to deliver technological breakthroughs that enhance load charts, increase efficiency, improve transport, simplify erections and earn owners exceptional return on their investments.

- Key Products: All Terrain Cranes, Lattice Boom Crawler Cranes, Tower Cranes, Rough Terrain and Truck Mounted cranes, Carrydeck Industrial Cranes.

- Recent Developments: In April 2025, Manitowoc introduced the Potain MCR 815 tower crane from its China manufacturing facility, expanding its luffing jib crane portfolio with a maximum lifting capacity of 64 tons.

- Strategic Focus: Strengthening its global crane business through product innovation, customer-driven equipment development, and the expansion of high-performance lifting solutions for complex construction and industrial applications.

Market Concentration Analysis

The global crane market exhibits moderate concentration at the premium-segment level and high fragmentation at the total market level. The top 5 global OEMs collectively account for approximately 35-40% of total crane market revenues, a relatively low concentration ratio reflecting the market's geographic diversity, product breadth, and the substantial rental industry revenue captured by fleet operators rather than OEMs. The premium all-terrain crane segment shows higher concentration, with Liebherr, Tadano, and Manitowoc together holding approximately 65-70% of European and North American sales by value.

Chinese manufacturers' growing global market penetration is reducing concentration among Western OEMs. Market concentration within China's domestic market is higher. The global crane market's concentration is expected to gradually increase through 2034 as crane rental industry consolidation concentrates procurement power in fewer larger fleet operators, Chinese OEMs' quality improvements expand their addressable market into previously Western OEM-dominated premium segments, and M&A activity reduces the total OEM count through the acquisition of smaller regional manufacturers.

Investment & Growth Opportunities

Highest Growth Segments

Marine and port cranes (~4.8% CAGR), fixed cranes (~4.2% CAGR), offshore wind installation vessel cranes (~15-20% CAGR for the offshore wind crane subcategory), automated port crane systems (~8-10% CAGR), and crane service and telematics subscription revenue (~12-15% CAGR from growing connected crane base) represent the global crane market's highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Green hydrogen fuel cell crane development represents the emerging technology investment opportunity with the longest commercial runway. Crane OEMs, fuel cell technology companies, and construction site energy management companies investing now in hydrogen-ready crane design and site hydrogen delivery logistics position for leadership in the 2028-2034 commercial scaling of hydrogen crane technology. Public infrastructure project clients in Europe and Australia are actively establishing zero-emission equipment specifications that will mandate hydrogen or battery-electric cranes for specific project categories from 2027-2030.

Investment Themes

- Offshore wind installation crane vessel development for the 500 GW global pipeline: New-generation wind installation vessels each requiring EUR 50-200 Million in crane system investment. Crane technology investment targeting the next-generation turbine size class that the current vessel fleet cannot accommodate will define the offshore wind crane competitive landscape through 2034.

- Port automation crane and digital management system investment for global terminal modernization: Global container port throughput growing at 4-5% annually creates continuous demand for automated port crane system investment. An automated terminal crane system represents one of the crane market's highest-value single transactions, making crane OEMs with port automation software integration capability disproportionately competitive for new greenfield automated terminal development.

Future Market Outlook (2026-2034)

The global crane market is projected to grow from USD 55.62 Billion in 2025 to USD 78.17 Billion by 2034, delivering a 3.85% CAGR over the forecast period. The market's anchor value of USD 67.20 Billion in 2030 represents a crane industry where offshore wind installation vessel crane procurement has created a sustained demand surge for 5,000+ tonne marine crane capacity, zero-emission crane technology (hydrogen fuel cell and battery electric) has crossed commercial viability thresholds for the 60-300 tonne all-terrain crane class, and China's XCMG and Sany have achieved genuine competitive credibility in the 500-1,000 tonne all-terrain crane market.

Three structural forces define the global crane market's growth through 2034 with high confidence: global infrastructure investment sustaining above-GDP growth in crane demand as every major economy deploys stimulus infrastructure capital requiring crane deployment at construction sites that cannot be substituted by any alternative technology; energy transition capital expenditure creating a new structural crane demand category; and the crane-adjacent mining capital expenditure cycle for critical minerals that supports EV manufacturing and renewable energy infrastructure creating 2-3x above-normal mining capex levels through 2034 as the energy transition creates structural mineral demand that existing mine supply cannot satisfy without significant new mine development investment.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including Product Directors and Sales Directors; crane rental fleet managers; construction project crane managers; port crane procurement officers; offshore energy crane engineering specifications managers; and crane operator safety and certification organization representatives.

Secondary Research

Secondary research encompassed European Construction Industry Federation (FIEC) crane market statistics; US Census Bureau construction put in place data; Chinese Construction Machinery Association (CCMA) crane production and export data; individual company annual reports and investor presentations; International Energy Agency (IEA) Renewables 2025 report for offshore wind investment data; Mining Journal and S&P Global Commodity Insights mining capital expenditure projections. Over 65 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up product type and application models calibrated against individual OEM revenue disclosures, Chinese crane production statistics, construction industry investment data, energy sector capex data, and mining sector capital expenditure projections. Key forecast inputs include global construction fixed capital formation growth by region, offshore wind installation schedule and vessel crane requirement modeling, mining critical minerals capex cycle trajectory, and crane fleet replacement demand modeled from global installed crane fleet age distribution data.

Crane Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Mobile Cranes, Marine and Port Cranes, Fixed Cranes |

| Applications Covered | Construction and Infrastructure, Mining, Oil and Gas, Others |

| Regions Covered | Asia Pacific, Europe, North America, Middle East and Africa, Latin America |

| Companies Covered | Liebherr, The Manitowoc Company, Inc., Tadano Ltd, Konecranes, SANY Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, crane market forecast, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global crane market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the crane industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Crane Market Report

The global crane market reached USD 55.62 Billion in 2025, driven by global infrastructure investment programs, offshore wind installation vessel crane deployment for a 500 GW global pipeline, critical mineral mining capex for EV supply chain development, port capacity expansion and automation investment, and China's sustained dominance as the world's largest crane consumer and manufacturer.

The market grows at 3.85% CAGR during 2026-2034, reaching USD 78.17 Billion by 2034, driven by infrastructure investment compounding, offshore wind marine crane procurement, critical mineral mining development, port automation investment, and the electrification replacement cycle as diesel crane fleets are renewed with hybrid and zero-emission platforms meeting tightening emissions regulations in Europe, North America, and the Asia Pacific.

Mobile cranes lead at 78.6% through their versatility across all applications and the world's most diverse capacity range, from 10-tonne city crane trucks to 3,200-tonne crawler cranes.

Construction and infrastructure lead at 35.0% as the fundamental demand anchor; every physical infrastructure project requires crane deployment.

Asia Pacific leads at 45.0% through China's unparalleled position as both the world's largest crane consumer and manufacturer, combined with India's 8-10% CAGR crane market growth under the National Infrastructure Pipeline program and ASEAN construction activity.

Leading companies include Liebherr, The Manitowoc Company, Inc., Tadano Ltd, Konecranes, and SANY Group, among others.

The market is projected to reach approximately USD 67.20 Billion by 2030, with offshore wind marine crane vessel deliveries creating peak marine crane manufacturing demand, India's crane market growth, electrified crane models, and Chinese OEMs achieving genuine competitive credibility in the premium 500-1,000 tonne all-terrain crane market.

Offshore wind's 500 GW global installation pipeline by 2030 is creating the single largest new demand driver for specialized crane equipment in the 2026-2034 forecast period.

Three priority opportunities: offshore wind installation and marine crane vessel system development; crane telematics and energy management software as recurring revenue through the electrification transition; and automated port terminal crane systems for global container throughput growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade