Airport Retailing Market Size, Share, Trends and Forecast by Product, Airport Size, Distribution Channel, and Region, 2026-2034

Airport Retailing Market Size and Share:

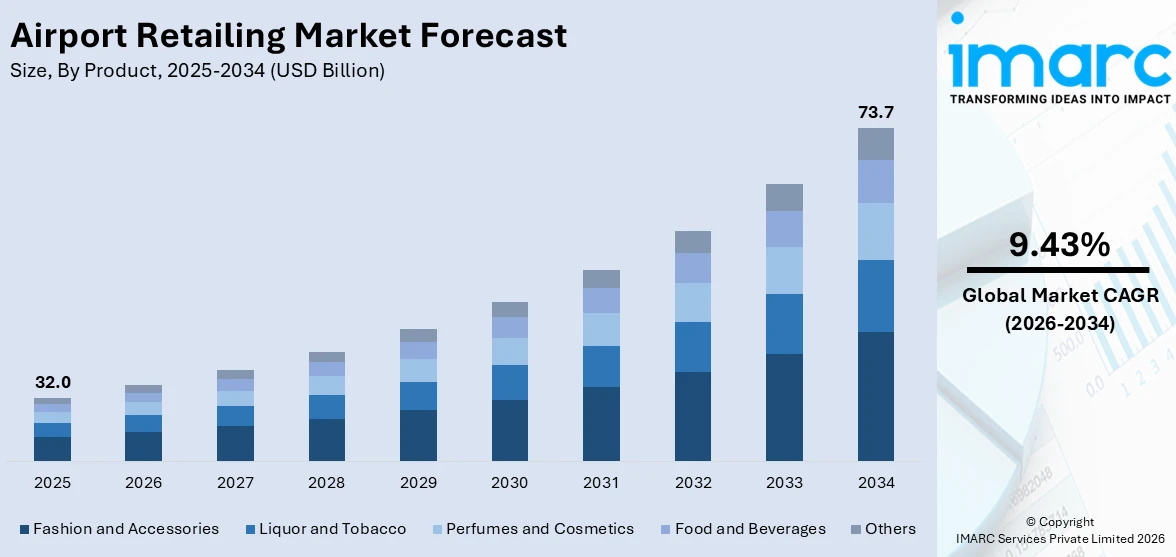

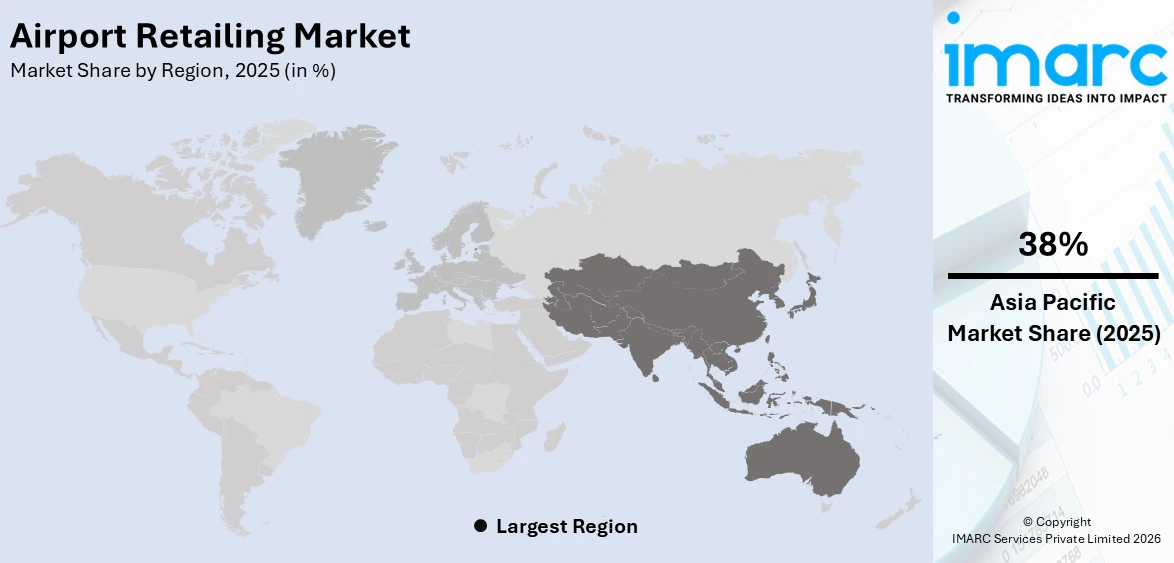

The global airport retailing market size was valued at USD 32.0 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 73.7 Billion by 2034, exhibiting a CAGR of 9.43% from 2026-2034. Asia-Pacific currently dominates the market, holding a market share of 38% in 2025. The region benefits from extensive networks of high-traffic international and domestic airports, strong travel demand driven by tourism and business activity, and ongoing investments in terminal modernization with expanded commercial retail zones, all contributing to the airport retailing market share.

The airport retailing market is driven by the constant increase in air travel, thereby increasing the consumer base for retail business in airport terminals. The increase in urbanization and rising disposable incomes in both developed and developing countries triggers the desire for discretionary spending by passengers during their transit time. The development of airport infrastructure worldwide, including the development of new terminals and commercial areas, provides additional retail space and attracts major brands to showcase themselves to a diverse and affluent group of people. Additionally, the increasing affinity for luxury and branded products among the global middle class fuels the demand for fashion, cosmetics, and specialty products in airport retailing environments.

The United States with a share of 87.80% has emerged as a major region in the airport retailing market owing to many factors. The country hosts some of the busiest airports globally, generating substantial passenger volumes that directly support retail revenue within terminals. In March 2025, Fraport USA secured a 23-year agreement with the Maryland Department of Transportation to manage and redesign retail concessions across approximately 18,000 m² at Baltimore/Washington International Airport. The growing trend of experiential retailing, where airports are designed as destinations offering premium dining, shopping, and entertainment, is encouraging travelers to engage in discretionary purchases. Rising international tourism to the United States and a strong domestic travel culture further contribute to steady consumer traffic through airport retail outlets, strengthening the airport retailing market outlook.

To get more information on this market Request Sample

Airport Retailing Market Trends:

Digital Transformation in Airport Retail

The digital transformation of airport retailing is reshaping how travelers discover, evaluate, and purchase products within terminal environments. Airports are increasingly adopting omnichannel retail strategies that integrate online pre-ordering platforms with physical store pickups, enabling passengers to browse and reserve products before arriving at the terminal. In 2025, Changi Airport Group launched a tender to partner with digital agencies to strengthen its e‑commerce and loyalty platforms, aiming to enhance seamless mobile engagement and targeted promotions for shoppers. Self-service kiosks and interactive digital signage provide personalized product recommendations based on travel destinations, loyalty profiles, and purchase history, creating tailored shopping experiences. Mobile applications developed by airport operators and retailers facilitate seamless navigation through retail zones, offer real-time promotions, and support digital wallet payments that reduce transaction times. Augmented reality features allow travelers to virtually try on fashion accessories and cosmetics, enhancing engagement without requiring physical interaction.

Expansion of Luxury Retail Offerings

The expansion of luxury retail offerings at airports reflects the evolving expectations of international travelers who seek premium shopping experiences during transit. Major airports are dedicating larger proportions of their commercial space to high-end fashion houses, designer accessories, premium cosmetics, and exclusive duty-free boutiques, transforming terminals into curated retail destinations. In April 2025, Vancouver International Airport unveiled its newly renovated Vancouver Duty Free spanning approximately 30,000 ft² with a curated mix of global luxury brands and exclusive Fragrance Haute Parfumerie offerings, elevating the airport’s retail experience for international travelers. This trend is supported by the increasing purchasing power of global travelers, particularly those from emerging economies who view airport shopping as an opportunity to access international luxury brands at competitive prices. Additionally, exclusive airport-only product collections and limited-edition releases create urgency and differentiation, encouraging travelers to make purchases they cannot replicate elsewhere, bolstering the airport retailing market trends.

Sustainability-Driven Retail Practices

Sustainability-driven retail practices are gaining prominence within airport commercial environments as both operators and travelers prioritize environmental responsibility. Airports are increasingly incorporating eco-friendly retail concepts, including stores that feature sustainably sourced products, recyclable packaging, and reduced plastic usage across merchandise and food service operations. In September 2025, Coty Travel Retail and Gebr. Heinemann launched the “My Fragrance Garden” sustainability pop‑up at Copenhagen and Berlin Brandenburg airports, showcasing eco‑designed packaging, fragrance refills, and upcycled ingredients to engage environmentally conscious travelers. Several airports have introduced dedicated sustainability-focused retail zones that showcase local artisans, organic food producers, and environmentally conscious fashion brands, appealing to travelers who align their purchasing decisions with their values. These initiatives enhance brand reputation while attracting the growing segment of environmentally aware consumers, supporting the airport retailing market forecast.

Airport Retailing Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global airport retailing market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product, airport size, and distribution channel.

Analysis by Product:

- Liquor and Tobacco

- Perfumes and Cosmetics

- Fashion and Accessories

- Food and Beverages

- Others

Fashion and accessories account for 31% market share, covering a broad range of products such as designer clothing, handbags, watches, jewelry, sunglasses, scarves, and travel-related fashion accessories offered through various airport retail outlets. The dominance of this category is justified by the aspirational purchasing habits of international travelers, who perceive airport shopping as a convenient opportunity to purchase global fashion brands, often at duty-free prices. The carefully designed shopping environments within airport terminals, featuring flagship stores and brand boutiques, provide an immersive shopping experience that promotes impulse buying and higher average transaction values. Furthermore, the increasing impact of social media and fashion awareness among younger generations also supports the sustained demand for fashionable accessories and high-end apparel during travel. Airport retailers are constantly updating their product offerings with seasonal ranges and airport-exclusive merchandise, keeping consumers engaged and promoting repeat business among regular travelers.

Analysis by Airport Size:

- Large Airport

- Medium Airport

- Small Airport

Large airport leads the market with a share of 61%, serving as primary international gateways, handling millions of passengers annually and offering extensive commercial retail infrastructure that accommodates a diverse range of product categories. The significant foot traffic at these facilities provides retailers with consistent access to a broad and affluent consumer base, including business travelers and international tourists with higher disposable incomes. In June 2025, Fraport unveiled a 12,000 square meters retail zone with 64 stores in the new Terminal 3 at Frankfurt Airport, reinforcing its position as a major European retail hub and enhancing the shopping experience for millions of global travelers. These airports typically feature expansive duty-free shopping areas, luxury brand outlets, and curated retail zones designed to maximize passenger engagement during extended layovers and transit times. The scale of operations at large airports allows for greater investment in store design, technology integration, and customer service enhancements that elevate the retail experience.

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Direct Retailers

- Convenience Stores

- Specialty Retailers

- Departmental Stores

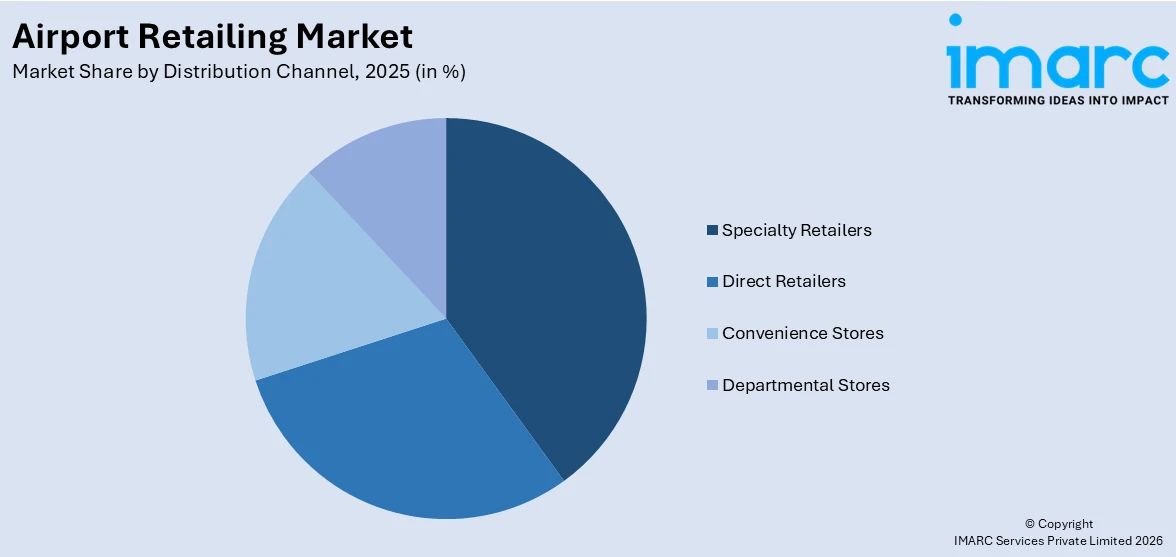

Specialty retailers dominate the market, with a share of 36%, operating focused store formats that cater to specific product categories such as luxury fashion, premium cosmetics, electronics, confectionery, and regional souvenirs. The market leadership of specialty retailers is based on their capacity to provide carefully selected and high-quality product offerings that match the shopping interests of international travelers looking for unique and high-quality products during their transit. Specialty retailers use their expertise in exclusive brands and products to differentiate shopping experiences and make them distinct from general merchandise stores. The positioning of specialty retail stores in highly visible locations within terminals, close to boarding gates and in departure lounges, maximizes exposure to passenger flow. Specialty retailers also benefit from partnerships and concessions with airport operators that offer favorable leasing terms and support, allowing them to maintain competitive pricing and attractive store displays that maximize consumer engagement.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia-Pacific, accounting for 38% of the share, enjoys the leading position in the market. The region's dominance is driven by the rapid expansion of air travel infrastructure across major economies, including China, India, Japan, South Korea, and Southeast Asian nations, where rising middle-class populations and growing disposable incomes are fueling significant increases in both domestic and international passenger volumes. Asia-Pacific airports are undergoing extensive modernization and expansion programs that incorporate world-class commercial retail facilities, attracting leading global brands to establish flagship stores within terminal environments. The region's strong tourism ecosystem, supported by favorable visa policies and growing inbound travel from neighbouring countries, creates a diverse consumer base for airport retail operators. Furthermore, the cultural emphasis on gift-giving and the popularity of luxury and duty-free shopping among Asian travelers drive higher per-passenger spending within airport retail outlets, consolidating the region's leading market position.

Key Regional Takeaways:

North America Airport Retailing Market Analysis

North America is a major contributor to the overall airport retailing market, due to the presence of a large number of busy international and domestic airports in the region. The United States and Canada are the major contributors to the market performance in the region. The major airport hubs in the region are continuously investing in the development of commercial retail infrastructure in their airports. The trend of developing airports as lifestyle destinations, with retail environments that combine luxury fashion, duty-free shopping, premium dining, and specialty product stores, is increasing passenger engagement and boosting spending per passenger. The use of advanced digital retail technology, such as contactless payment systems, mobile-based pre-ordering systems, and personalized promotion tools, is simplifying the shopping process and improving conversion rates at retail outlets in airport terminals. The steady recovery and growth in the number of passengers in the aviation industry is boosting consumer traffic in airport retail environments.

United States Airport Retailing Market Analysis

The United States represents a significant force in the airport retailing market, underpinned by its extensive network of high-traffic international and domestic airports that collectively serve hundreds of millions of passengers each year. The country's airport retail landscape is characterized by a sophisticated mix of duty-free shops, luxury brand boutiques, quick-service dining outlets, and specialty retail stores that cater to the diverse preferences of both domestic and international travelers. Ongoing infrastructure investments across major airport hubs are expanding commercial retail space and introducing innovative store formats that enhance the passenger shopping experience. The growing adoption of technology-driven retail solutions, including self-checkout systems, mobile ordering platforms, and personalized digital promotions, is transforming how travelers interact with airport retail offerings. Additionally, the resurgence of international travel to and from the United States continues to strengthen consumer traffic through airport retail zones, with leisure and business travelers contributing to steady demand for fashion, cosmetics, electronics, and specialty food products. Airport operators are also prioritizing partnerships with premium and emerging brands to diversify product offerings and capture evolving consumer preferences.

Europe Airport Retailing Market Analysis

Europe maintains a prominent position in the global airport retailing market, supported by its dense network of major international airports that serve as critical transit hubs connecting intercontinental travel routes. The region's airport retail sector benefits from a well-established tradition of duty-free shopping, with travelers from within and outside Europe actively seeking premium products at competitive prices during their journeys. In July 2025, Amsterdam Airport Schiphol and Lagardère Travel Retail opened the airport’s largest duty‑free flagship store under the new ‘Today Duty Free’ retail concept, significantly upgrading the shopping experience for international passengers. European airports are distinguished by their curated retail environments that blend luxury fashion, artisanal food products, fine wines, and locally sourced specialty goods, creating a distinctive shopping experience tailored to the region's cultural diversity. Airport modernization programs across major hubs in Germany, France, the United Kingdom, and other nations are expanding commercial retail footprints and incorporating technology-enabled shopping solutions.

Asia-Pacific Airport Retailing Market Analysis

Asia-Pacific leads the global airport retailing market growth, driven by the region's rapid growth in air passenger traffic and significant investments in airport infrastructure development. Countries such as China, India, Japan, and South Korea are expanding their airport capacities with modern terminal facilities that prioritize commercial retail integration, offering travelers access to international luxury brands, duty-free outlets, and culturally relevant specialty products. The region's growing middle-class population, combined with increasing outbound tourism and a strong cultural affinity for luxury goods and gift purchasing, supports elevated per-passenger spending at airport retail establishments. Digital payment adoption is particularly advanced across Asia-Pacific airports, enabling seamless transactions that enhance the shopping experience. Furthermore, government initiatives promoting tourism and aviation sector development across Southeast Asian nations are creating new retail opportunities.

Latin America Airport Retailing Market Analysis

Latin America presents a growing opportunity in the airport retailing market, supported by increasing air travel connectivity and expanding airport infrastructure across key economies including Brazil and Mexico. The region's rising middle-class population and growing interest in international travel are driving higher passenger volumes through major airport hubs, creating expanded opportunities for retail operators. Duty-free shopping remains a significant draw for both domestic and international travelers seeking competitively priced fashion, cosmetics, and electronics. Airport modernization projects across the region are enhancing commercial retail spaces and attracting international retail brands. Additionally, the growth of low-cost carriers is broadening the traveler base and increasing exposure to airport retail offerings.

Middle East and Africa Airport Retailing Market Analysis

The Middle East and Africa region is experiencing steady growth in airport retailing, driven by the strategic positioning of major Gulf airports as global transit hubs and the expansion of aviation infrastructure across African nations. Airports in the Middle East, particularly those in the United Arab Emirates and Saudi Arabia, are renowned for their extensive luxury retail offerings and world-class duty-free shopping experiences that attract premium-spending international travelers. The growing tourism sector across both subregions, supported by government diversification strategies and visa facilitation programs, is increasing passenger traffic and retail spending. Africa's emerging aviation market, with airport development projects in several nations, presents new opportunities for retail expansion.

Competitive Landscape:

The competitive landscape of the airport retailing market is characterized by the presence of established global travel retail operators alongside regional players that collectively shape the industry's strategic direction. Leading market participants are focused on expanding their concession portfolios across major international airports through competitive bidding processes and strategic partnership agreements with airport authorities. Players are investing in store renovation and redesign initiatives to create premium retail environments that enhance passenger engagement and drive higher spending. The integration of digital retail technologies, including e-commerce platforms, mobile applications, and data analytics, is enabling operators to personalize shopping experiences and optimize inventory management. Additionally, mergers and acquisitions within the travel retail sector are consolidating market positions and enabling companies to achieve economies of scale across multiple geographies, allowing them to better serve the evolving demands of an increasingly diverse global traveler base.

The report provides a comprehensive analysis of the competitive landscape in the airport retailing market with detailed profiles of all major companies, including:

- Airport Retail Group LLC

- Autogrill S.p.A.

- China Duty Free Group Co. Ltd. (China International Travel Service Co. Ltd.)

- DFS Group Ltd. (LVMH Moët Hennessy Louis Vuitton)

- Dubai Duty Free

- Dufry AG

- Duty Free Americas Inc.

- Flemingo International Ltd.

- Gebr. Heinemann SE & Co. KG

- Japan Airport Terminal Co. Ltd.

- KING POWER International

- Lagardère Travel Retail (Lagardère Group)

Latest News and Developments:

- In February 2025, the Adani Group announced expansion of its airport retail operations, planning to operate over 310 stores, including 270 retail outlets and 40 F&B units across eight airports. The move aims to increase non-aeronautical revenue, extend retail beyond airports to highways and malls, and compete with Tata Group and Reliance.

- In February 2025, Dubai Duty-Free announced plans to seek strategic retail partners for the new Al Maktoum International Airport (DWC) to enhance passenger shopping experiences. The operator reported Dh7.901 billion in 2024 sales, over 20.733 million transactions, and 13.7 million customers, aiming to expand exclusive brands and integrate innovative retail technologies.

Airport Retailing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Liquor and Tobacco, Perfumes and Cosmetics, Fashion and Accessories, Food and Beverages, Others |

| Airport Sizes Covered | Large Airport, Medium Airport, Small Airport |

| Distribution Channels Covered | Direct Retailers, Convenience Stores, Specialty Retailers, Departmental Stores |

| Region Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Airport Retail Group LLC, Autogrill S.p.A., China Duty Free Group Co. Ltd. (China International Travel Service Co. Ltd.), DFS Group Ltd. (LVMH Moët Hennessy Louis Vuitton), Dubai Duty Free, Dufry AG, Duty Free Americas Inc., Flemingo International Ltd., Gebr. Heinemann SE & Co. KG, Japan Airport Terminal Co. Ltd., KING POWER International, Lagardère Travel Retail (Lagardère Group), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the airport retailing market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global airport retailing market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the airport retailing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Airport Retailing Market Size Report

The airport retailing market was valued at USD 32.0 Billion in 2025.

The airport retailing market is projected to exhibit a CAGR of 9.43% during 2026-2034, reaching a value of USD 73.7 Billion by 2034.

The airport retailing market is driven by growing global air passenger traffic, increasing disposable incomes, expansion of airport infrastructure with dedicated commercial retail zones, rising demand for duty-free and luxury products among international travelers, the integration of digital retail technologies enhancing shopping convenience, and the growing preference for premium fashion, cosmetics, and specialty items during transit.

Asia-Pacific currently dominates the airport retailing market, accounting for a share of 38%. The region benefits from rapidly expanding air travel infrastructure, rising middle-class populations, strong tourism ecosystems, and cultural preferences for luxury and duty-free shopping.

Some of the major players in the airport retailing market include Airport Retail Group LLC, Autogrill S.p.A., China Duty Free Group Co. Ltd. (China International Travel Service Co. Ltd.), DFS Group Ltd. (LVMH Moët Hennessy Louis Vuitton), Dubai Duty Free, Dufry AG, Duty Free Americas Inc., Flemingo International Ltd., Gebr. Heinemann SE & Co. KG, Japan Airport Terminal Co. Ltd., KING POWER International, Lagardère Travel Retail (Lagardère Group), etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade