Aluminium Cans Market Size, Share, Trends and Forecast by Application and Region 2026-2034

Global Aluminium Cans Market Size, Share, Trends & Forecast (2026-2034)

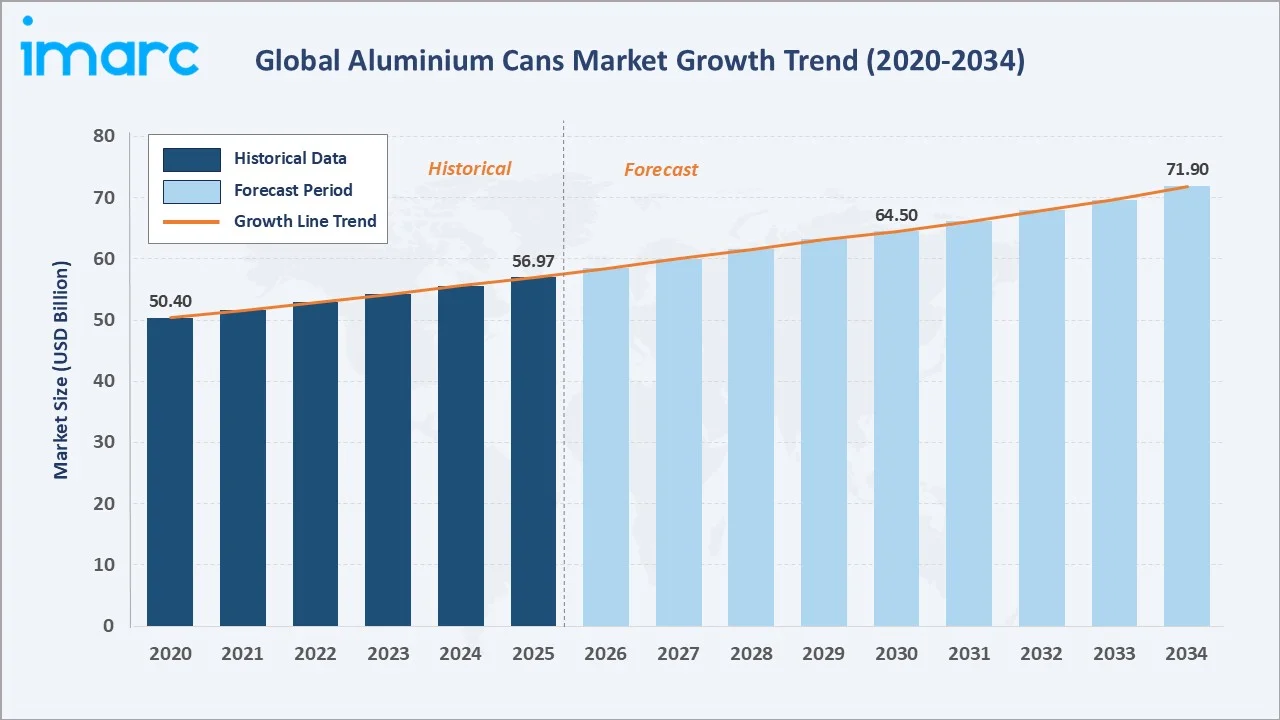

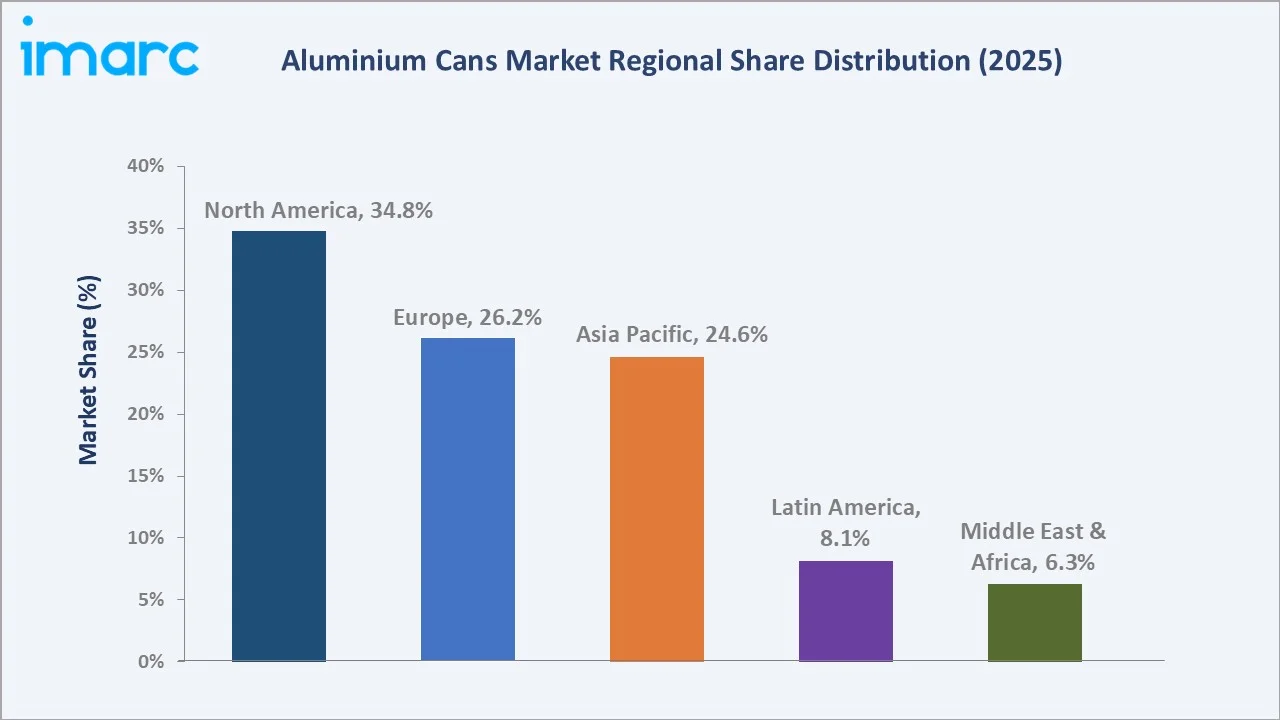

The global aluminium cans market reached USD 56.97 Billion in 2025 and is projected to reach USD 71.9 Billion by 2034, exhibiting a CAGR of 2.5% during 2026-2034. Growth is driven by sustainable packaging demand, the craft beverage boom, rising canned food consumption, and the shift away from single-use plastics. Beverages lead with a 72.6% share. North America leads regionally at 34.8%. The market is projected to reach USD 64.5 Billion by 2030. Key players include Ball Corporation, Crown Holdings, ALTEMIRA, Toyo Seikan, and Canpack S.A.

Market Snapshot

|

Metric |

Value |

|

Market Size (2020) |

USD 50.4 Billion |

|

Market Size (2025) |

USD 56.97 Billion |

|

Market Size (2030) |

USD 64.5 Billion |

|

Forecast Market Size (2034) |

USD 71.9 Billion |

|

CAGR (2026-2034) |

2.5% |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (34.8%, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Dominant Application |

Beverages (72.6%, 2025) |

|

Second Largest Application |

Food (18.4%, 2025) |

To get more information on this market, Request Sample

The market grew from USD 50.4 Billion in 2020 to USD 56.97 Billion in 2025. The forecast addition of USD 14.9 Billion through 2034 is underpinned by aluminium's infinite recyclability credentials, beverage category premiumisation, and a global regulatory push against single-use plastic packaging.

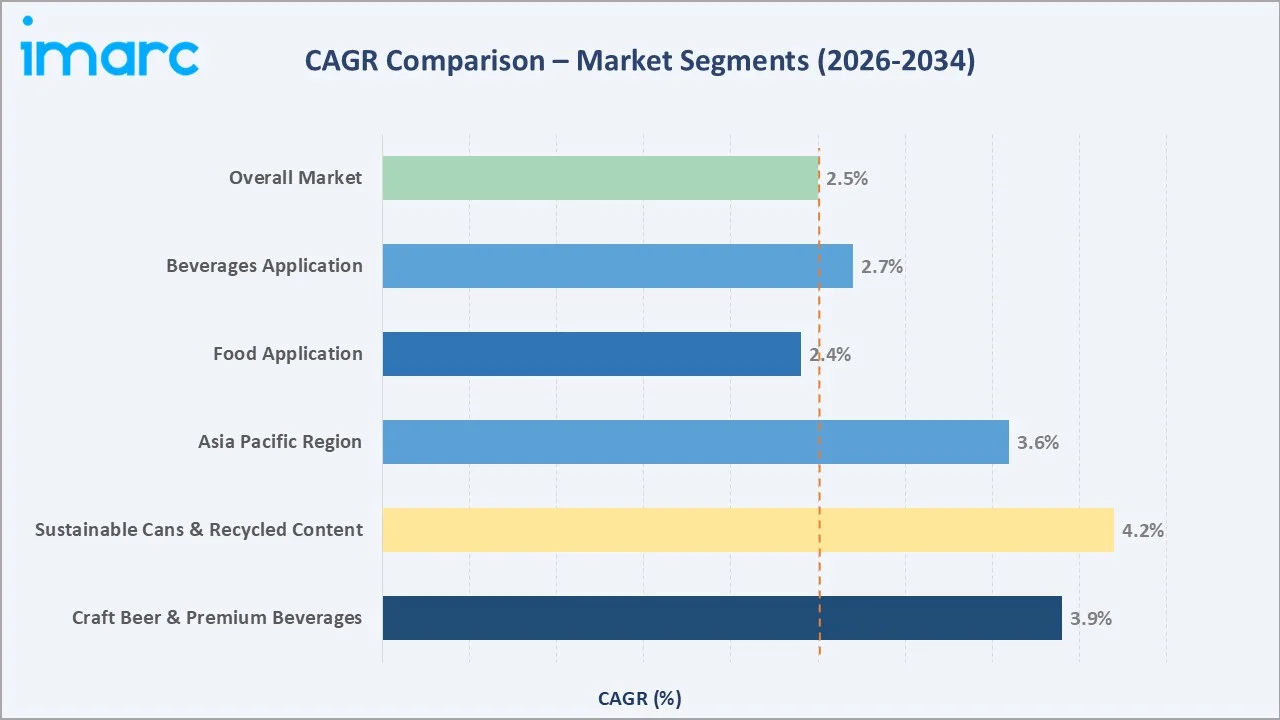

The 2.5% CAGR reflects steady sustainability-backed expansion. Sustainable recycled-content cans grow at approximately 4.2% CAGR and Asia Pacific at approximately 3.6% CAGR, both outpacing the market average on structural demand tailwinds.

Executive Summary

The global aluminium cans market stood at USD 56.97 Billion in 2025, driven by sustainability demand, craft and premium beverage growth, and regulatory restrictions on single-use plastics globally. The market is forecast to reach USD 71.9 Billion by 2034 at a 2.5% CAGR, crossing USD 64.5 Billion by 2030.

Beverages dominate at 72.6% in 2025, driven by carbonated soft drinks, beer, energy drinks, and RTD alcoholic beverages favouring aluminium over glass and PET for sustainability and consumer experience. Food at 18.4% serves canned vegetables, soups, seafood, and pet food. Others at 9.0% encompasses aerosols, personal care, and industrial specialty applications.

North America leads regionally at 34.8% (2025), driven by the United States' deeply entrenched can culture across beverages and food. Europe at 26.2% is accelerating aluminium can adoption through extended producer responsibility (EPR) regulations and single-use plastics directives. Asia Pacific at 24.6% is the fastest-growing region, driven by urbanisation, rising FMCG penetration in China, India, and Southeast Asia, and rapid growth in energy drink and RTD beverage categories.

Key Market Insights

|

Insight |

Data |

|

Dominant Application |

Beverages – 72.6% (2025) |

|

Second Largest Application |

Food – 18.4% (2025) |

|

Leading Region |

North America – 34.8% (2025) |

|

Fastest Growing Region |

Asia Pacific (~3.6% CAGR, 2026-2034) |

|

Top Companies |

Ball Corp., Crown Holdings, ALTEMIRA, Toyo Seikan, Canpack |

|

Market Opportunity |

Sustainable recycled-content cans and Asia Pacific FMCG expansion |

Key Analytical Observations Supporting the Above Data:

- Beverages Segment Leadership: Beverages' 72.6% dominance (2025) reflects aluminium's superior chilling properties, light barrier protection for flavour preservation, portability, and consumer preference for the tactile can experience in beer, energy drinks, and RTD cocktails, categories that are growing at above-market rates globally.

- Food Application Growth: Food at 18.4% benefits from aluminium's hermeticity, shelf-life extension of 2–5 years versus ambient alternatives, and compatibility with retort sterilisation. Pet food canning is a high-growth sub-category as pet ownership and premium pet food spending rise across North America, Europe, and Asia Pacific.

- North America's Structural Advantage: North America's 34.8% share reflects approximately 100 billion U.S. aluminium cans consumed annually, Ball and Crown's dominant domestic capacity, and a beverage industry that overwhelmingly standardises on 12 oz aluminium formats across beer, CSD, and energy drink categories.

Global Aluminium Cans Market Overview

Aluminium cans are rigid metal containers manufactured via the draw and ironing (DWI) process, serving beverages, food, and specialty products requiring hermetic sealing and consumer portability. The market covers manufacturing, coating, printing, and distribution of slim, sleek, and standard formats for beverage and food manufacturers across 100+ countries. As of 2025, the market is valued at USD 56.97 Billion. Key tailwinds include anti-plastic regulation, aluminium's circular economy credentials, beverage premiumisation, and Asia Pacific urbanisation.

Market Dynamics

To evaluate market opportunities, Request Sample

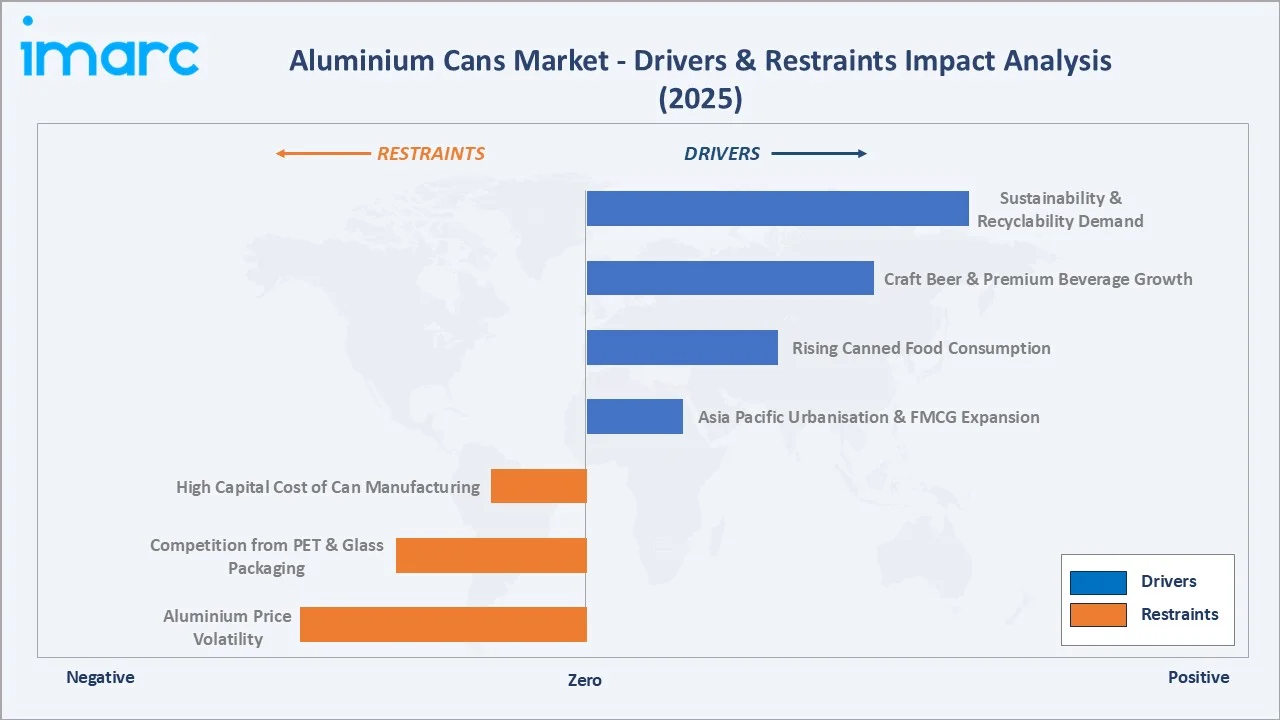

Market Drivers

- Sustainability and Recyclability Demand: Aluminium's infinite recyclability, producing approximately 95% energy savings versus primary production, is a decisive sustainability advantage as EPR regulations, deposit return schemes (DRS), and corporate net-zero commitments mandate higher recycled content and recyclability in packaging. The EU's SUP Directive and U.S. state-level bottle bill expansions are structurally favouring aluminium over single-use plastic.

- Craft Beer and Premium Beverage Growth: The global craft beer market and premium RTD beverage categories are growing significantly, with aluminium cans being the dominant packaging format. Over 78% of U.S. craft breweries now can their products, and global energy drink volumes, led by Red Bull, Monster, and Celsius, are growing at approximately 7% CAGR, directly driving aluminium can demand.

- Rising Canned Food Consumption: Post-pandemic shift toward shelf-stable food and growing consumer confidence in canned nutrition has sustained elevated food can volumes. Canned protein (seafood, poultry, beans) and ready-meal categories are particularly growing in North America and Europe, supporting the 18.4% food application segment.

- Retail and E-Commerce Packaging Requirements: Online grocery and direct-to-consumer beverage channels are increasingly requiring packaging that withstands handling, transit, and ambient storage – all areas where aluminium cans outperform glass and PET, driving structural channel-led demand growth in developed and emerging markets alike.

Market Restraints

- Aluminium Price Volatility: Primary aluminium prices are linked to LME (London Metal Exchange) spot rates, which are subject to energy cost fluctuations, production disruptions, and trade tariff policies. Significant price spikes, as seen in 2021–2022, compress can manufacturer margins and increase cost-of-goods for beverage brands, creating demand sensitivity in price-competitive food and lower-value beverage segments.

- Competition from PET and Glass Packaging: PET bottles and glass continue to compete strongly in premium spirits, still water, and certain juice categories where visual differentiation, resealability, and consumer perception favour non-aluminium formats. PET's cost advantage in large-format (1L+) applications limits aluminium can penetration in these segments.

- High Capital Cost of Manufacturing: Aluminium can manufacturing requires significant capital investment in DWI lines (USD 50-100 Million per line), coaters, decorators, and end-manufacturing equipment. High minimum efficient scale and barrier entry costs limit new entrant competition but also restrict capacity expansion responsiveness to regional demand growth.

Market Opportunities

- High Recycled Content and Certified Sustainable Cans: Brands and retailers are increasingly requiring can suppliers to provide verified recycled aluminium content (70%+ recycled content cans) and carbon-footprint-certified packaging. Ball Corporation's certified 90%+ recycled content cans and ALTEMIRA's sustainable can programs command price premiums of 5–15% in retail markets.

- Slim and Sleek Can Format Premiumisation: The shift toward slim (250ml, 330ml) and sleek (355ml) can formats for energy drinks, RTD cocktails, hard seltzers, and functional beverages is a high-growth market sub-segment. These premium formats command 15–25% higher per-unit revenues versus standard 355ml cans.

- Emerging Market Penetration in Asia Pacific and MEA: Per-capita aluminium can consumption in India, Southeast Asia, and Africa remains far below North American levels (approximately 676 cans/year per household), creating a structural long-run growth opportunity as income growth, urbanisation, and modern retail infrastructure expand addressable markets.

Market Challenges

- Global Can Supply-Demand Imbalances: The 2020–2021 can shortage, driven by pandemic-accelerated at-home beverage consumption, led to significant capacity additions, creating oversupply in North America and Europe during 2023–2024. Managing the cycle from shortage to excess capacity requires careful capital allocation by manufacturers and creates pricing pressure in the near term.

- Aluminium Tariffs and Trade Policy Risk: U.S. Section 232 aluminium tariffs and EU-U.S. trade policy on primary aluminium create input cost uncertainty for can manufacturers. Import dependencies on primary aluminium from Australia, Canada, and Norway expose North American and European manufacturers to trade policy risk that is difficult to fully hedge through recycled content sourcing.

- Coating and Liner Migration Regulations: Tightening EU and FDA regulations on internal can coatings, particularly BPA (Bisphenol A) migration limits in food-contact applications, require ongoing reformulation investment by cans manufacturers. Transition to BPA-NI (non-intent) liners adds formulation complexity and cost, particularly for food can applications.

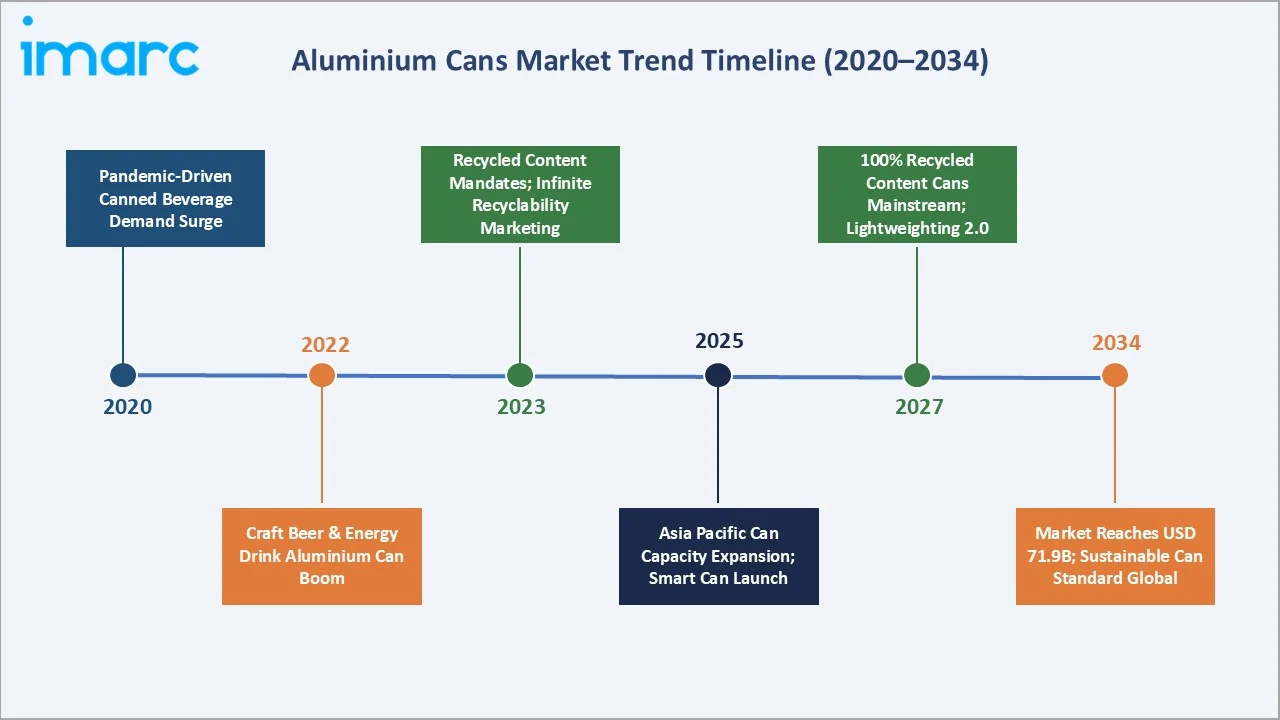

Emerging Market Trends

Five converging trends are redefining production technology, sustainability standards, product formats, and competitive dynamics in the global aluminium cans market through 2034.

1. Infinite Recyclability and Circular Economy Leadership

Aluminium's infinite recyclability, with global can recycling rates of approximately 75% in 2025, positions the aluminium can as the circular packaging format of choice for FMCG brands. DRS expansions across Germany, Scandinavia, the UK, and Australia are structurally improving recovery rates and feeding certified recycled aluminium back into can sheet production.

2. Craft Beer and Hard Seltzer Market Expansion

The global craft beer market and the rapid rise of hard seltzers, RTD cocktails, and functional beverages are driving above-market beverage can demand. Over 78% of U.S. craft breweries now package in cans, with segment expansion into Europe and Asia Pacific creating new demand for smaller-run, high-decoration specialty formats.

3. Sustainable Can Certification and Verified Recycled Content

FMCG brands require chain-of-custody verified recycled aluminium under ASI certification. Ball, Crown, and ALTEMIRA have all launched certified sustainable can lines. The sustainability premium in European retail creates positive margin incentives for producers investing in certified recycled content supply chains.

4. Lightweighting and Can Design Innovation

Can body weight has reduced significantly over two decades through continuous lightweighting. The weight of two-piece aluminium cans has drastically been reduced from the original 85 grams to approximately 15 grams today. Sleek and slim premium formats are enriching manufacturer revenue mix through higher per-unit revenues.

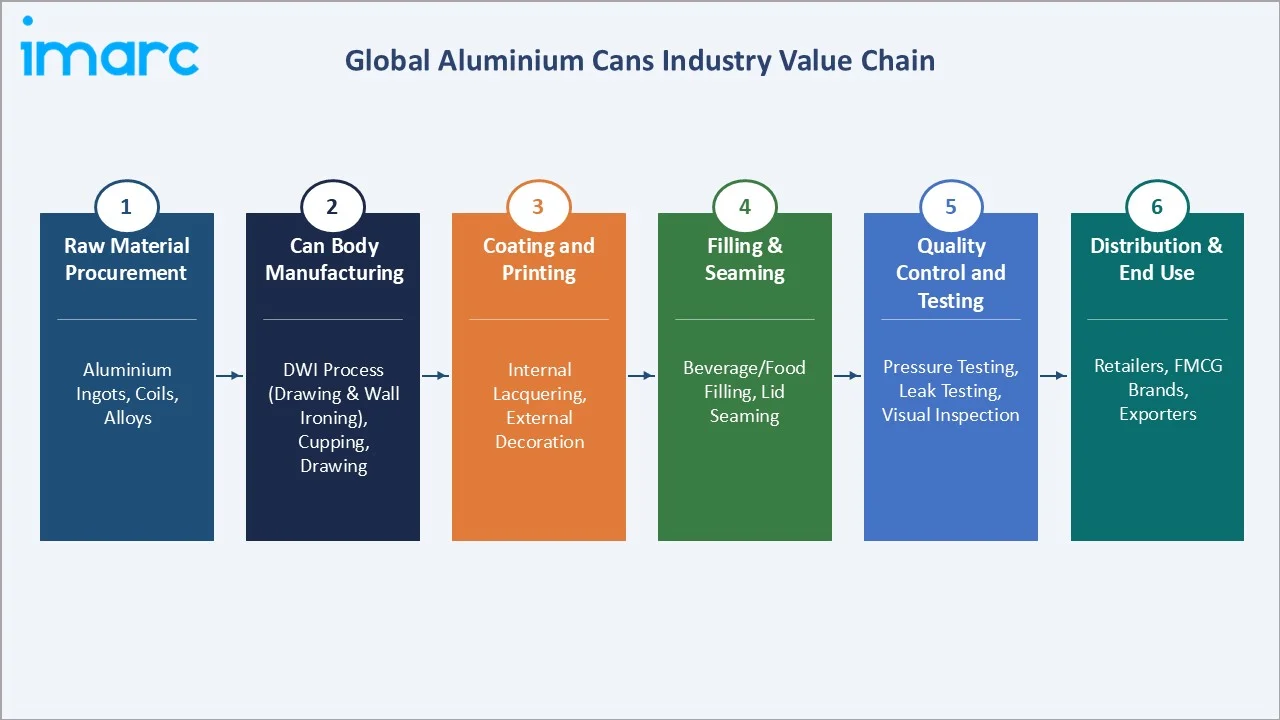

Industry Value Chain Analysis

The aluminium cans industry value chain spans six integrated stages from raw material procurement to end-use, with sustainability credentials and recycled content certification increasingly critical at each stage.

|

Stage |

Key Activities |

Representative Players |

|

Raw Material Procurement |

Bauxite mining, aluminium smelting, rolling mill coil production |

Alcoa, Rio Tinto |

|

Can Body Manufacturing |

DWI process, cupping, drawing, ironing, trimming to final dimensions |

Ball Corp., Crown Holdings, ALTEMIRA, Toyo Seikan |

|

Coating & Printing |

Internal lacquering, external basecoat, offset/lithographic printing |

Sherwin-Williams, PPG, can manufacturers |

|

Filling & Seaming |

Beverage/food filling, lid placement, double seaming, pasteurisation |

AB InBev, Coca-Cola, PepsiCo, Nestlé, food processors |

|

Quality & Compliance |

Internal coating integrity, pressure testing, fill accuracy, traceability |

SGS, Bureau Veritas, internal QC teams |

|

Distribution & End Use |

Retailer distribution, DTC e-commerce, foodservice, export |

Walmart, Carrefour, Amazon, foodservice distributors |

Can body manufacturing is the primary value creation point, transforming commodity aluminium coil into decorated, specification-compliant packaging at 8–15% margins over material costs. Digital printing advances now enable short-run, high-personalisation can decoration for craft and premium brands, expanding the accessible customer base for can manufacturers.

Technology Landscape in the Aluminium Cans Industry

Advanced DWI Manufacturing and Lightweighting

Next-generation DWI lines operate at high speed production with 2,200-3,000 cans per minute. Advanced 3004 and 3104 aluminium alloys with higher strength-to-weight ratios enable further lightweighting, cutting material costs and embodied carbon, while servo-controlled bodymakers provide real-time gauge adjustment minimising scrap.

Digital Can Printing and Closed-Loop Recycling

Industrial inkjet printing enables short-run, variable-data decoration without litho tooling costs, serving craft breweries via Ball's Revolution Can and Crown's Mass Customisation platforms. Closed-loop recycling re-melts UBCs into new can sheet within 60 days, achieving 70–90% recycled content. Novelis and Hydro deploy blockchain mass-balance tracking to certify chain-of-custody sustainability for EPR-compliant customers.

BPA-Free Internal Coatings and Food Safety

The BPA-NI transition under EU Regulation 10/2011 and FDA guidance requires significant reformulation investment. Advanced spray systems achieve 100% coating coverage at 3,000+ cans per minute, ensuring food safety compliance while maintaining retort sterilisation compatibility essential for food can applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

Beverages |

72.6% |

2025 |

|

Region |

North America |

34.8% |

2025 |

By Application

Beverages dominate at 72.6% in 2025, driven by CSD, beer, energy drinks, and fast-growing RTD alcoholic beverage categories. Aluminium's chilling performance, flavour barrier properties, light weight, and 100% recyclability make it the preferred format for sustainability-focused beverage brands.

Food at 18.4% serves canned vegetables, soups, seafood, pet food, and ready meals. Aluminium's hermeticity, sterilisation compatibility, and multi-year shelf life are essential for shelf-stable food. Premium pet food canning and consumer preference for convenient canned proteins support segment growth. Others at 9.0% covers aerosols, personal care, and industrial specialty applications.

To access detailed market analysis, Request Sample

Regional Market Insights

Five major regions contribute to the global aluminium cans market. North America and Europe collectively account for 61.0% of revenues in 2025, reflecting their mature beverage can cultures, established recycling infrastructure, and dominant global can manufacturing capacity.

North America's 34.8% share reflects the United States' annual can consumption, Ball and Crown Holdings' dominant production capacity, and extensive DRS infrastructure. Over 9,000 U.S. craft breweries predominantly package in aluminium cans, and energy drink volume growth sustains above-average demand in this mature market.

Europe at 26.2% is accelerating aluminium can adoption through the EU SUP Directive, EPR regulations rewarding recyclability, and premiumisation of beer and RTD segments. Germany's Pfand, Scandinavia's Pantamera, and the UK's emerging DRS strengthen aluminium's circular economy positioning. Asia Pacific at 24.6% grows fastest, with China's huge energy drink market, India's modern retail expansion, and Southeast Asian urbanisation driving structural FMCG demand.

Competitive Landscape

The global aluminium cans market is moderately concentrated. Ball Corporation and Crown Holdings collectively represent approximately nearly half of global aluminium can production capacity in 2025, creating a duopoly-influenced competitive structure at the global level. Regional and specialty players including ALTEMIRA, Toyo Seikan, Canpack, Orora Beverage, and Silgan compete effectively in specific geographies and product categories.

|

Company Name |

Key Brand(s) |

Market Position |

Primary Strategy |

|

Ball Corporation |

Ball |

Global Leader |

Sustainable cans, lightweighting, DRS partnerships |

|

Crown Holdings |

Crown |

Global Leader |

Beverage & food cans, M&A growth, premium formats |

|

ALTEMIRA Group |

ALTEMIRA |

Leader – Asia |

Sustainable aluminium, European market focus |

|

Toyo Seikan Co., Ltd. |

Toyo Seikan |

Leader – Asia |

Japan/Asia Pacific, food cans, lightweight tech |

|

Canpack S.A. |

Canpack |

Challenger – Europe |

Eastern Europe growth, export markets, craft beer |

|

Orora Beverage |

Orora |

Established – Pacific |

Australia/NZ beverage cans, sustainability program |

|

CCL Container Inc. |

CCL |

Established – NA |

Specialty aerosol and food cans |

|

Silgan Containers |

Silgan |

Established – NA |

Steel and aluminium food cans, long-run volumes |

|

Nampak Ltd. |

Nampak |

Challenger |

Africa beverage can specialist, DRC, Nigeria, Kenya |

|

Tecnocap Group |

Tecnocap |

Emerging |

Specialty closures and cans |

|

SAPIN |

SAPIN |

Emerging |

Metal food, aerosol, and industrial cans-Saudi Arabia & UAE/MENA |

Scale economies in DWI manufacturing, long-term beverage brand supply agreements, and certified sustainable aluminium supply chain control are the primary competitive moats for Ball Corporation and Crown Holdings. Regional challengers compete on proximity to customer production sites, flexible minimum order quantities for craft and premium customers, and lower overhead cost structures in developing market geographies.

Key Company Profiles

Ball Corporation

Ball Corporation is the world's largest aluminium packaging company, producing approximately 107 Billion recyclable cans annually and leading the industry on sustainable can certification and lightweighting innovation.

- Recent Developments: Ball Corporation completed the divestiture of its Aerospace segment to BAE Systems in 2024, refocusing entirely on packaging. Ball launched its EVA (End-to-End Value Analysis) program in 2024 to optimise customer total cost of packaging.

- Strategic Focus: Sustainable can certification, lightweighting R&D, Asia Pacific capacity expansion, and craft and premium beverage format growth

Crown Holdings

Crown Holdings is the world's second-largest metal packaging company with aluminium beverage and food can operations around 40 countries. Its SuperEnd lid technology saves approximately 10% aluminium versus standard ends.

- Recent Developments: Crown Holdings divested its European tinplate packaging business in 2021 to sharpen focus on aluminium beverage and food can growth segments. Expanded India aluminium can capacity in FY2024.

- Strategic Focus: Premium beverage can growth, SuperEnd lightweighting adoption expansion, India and Southeast Asia market penetration, and digital printing platform for craft and limited-edition brands.

ALTEMIRA Holdings Co., Ltd.

ALTEMIRA is a leading independent aluminium can manufacturer, based in Tokyo, with a capital of 100 million Japanese Yen.

- Recent Developments: ALTEMIRA achieved ASI (Aluminium Stewardship Initiative) certification across its manufacturing network, enabling supply of verified sustainable cans to customers in Japan and Vietnam.

- Strategic Focus: Asian market share consolidation, certified sustainable aluminium can supply, craft and premium beverage format growth, and innovative can recovery programme development.

Toyo Seikan Co., Ltd.

Toyo Seikan is Japan's largest and Asia Pacific's leading metal packaging company, producing aluminium cans, steel cans, and pouches across Japan and Southeast Asia.

- Recent Developments: Toyo Seikan is focusing on expanding aluminium can capacity to serve Southeast Asia's growing energy drink and RTD beverage sectors, targeting significant volume growth in the region.

- Strategic Focus: Southeast Asia capacity expansion, lightweight aluminium technology adoption, food can BPA-NI coating transition, and recycled content certification under Japan's aluminium recycling framework.

Market Concentration Analysis

Ball Corporation and Crown Holdings collectively control nearly half of global aluminium can production capacity. The top five players- Ball, Crown, ALTEMIRA, Toyo Seikan, and Canpack, account for more than half of market revenues, with regional specialists competing in specific geographies and specialty product categories.

The market is more fragmented at the regional level, with dozens of players serving local demand in Asia, Africa, and Latin America. Can manufacturing's capital intensity, long-term supply agreements, and logistics proximity requirements create natural geographic fragmentation.

Investment & Growth Opportunities

Fastest Growing Segments

Sustainable recycled-content cans, slim and sleek premium formats for RTD and craft beverages, and BPA-free food-grade cans are the highest-growth vectors through 2034.

Emerging Market Opportunities

India is the largest emerging market investment opportunity, with approximately 8% annual can demand growth driven by Red Bull, Monster, and beer can adoption. Vietnam, Indonesia, Thailand, and Sub-Saharan Africa offer similar structural growth opportunities as canned beverage penetration rises from very low bases.

Technology and Innovation Investment Trends

- Closed-Loop Recycling Infrastructure: Investment in UBC (used beverage can) collection, sorting, and re-rolling infrastructure is being funded by can manufacturers, aluminium producers, and EPR levy funds in Europe, Japan, and increasingly in U.S. state DRS programmes, creating sustainable feedstock supply chains.

- Digital Can Printing Platforms: Industrial inkjet digital can printing platforms enabling short-run, variable-data decoration are attracting investment from Ball (Revolution Can), Crown (Mass Customisation), and independent digital printing service providers targeting the craft brewery market.

- BPA-Free Food Can Coatings: Continued R&D investment in acrylic and polyester-based BPA-NI internal coatings meeting EU and FDA food safety standards is required across the industry, creating opportunities for specialty coating companies (Valspar/Sherwin-Williams, PPG) and can manufacturers investing in coating technology differentiation.

Future Market Outlook (2026-2034)

The global aluminium cans market is poised for steady, sustainability-driven expansion through 2034. This growth reflects aluminium cans' uniquely advantaged competitive positioning in an era of intensifying packaging sustainability regulation globally.

By 2034, aluminium's circular economy credentials will be structural market advantages as EPR regulations and DRS mandates require 75–90% packaging recyclability in the EU, U.S., and Japan. The shift away from single-use plastics is expected to deliver sustained aluminium can volume gains across all geographies through the forecast decade.

Asia Pacific is projected to reach approximately 28–30% of global revenues by 2034, driven by India's scaling can market and Southeast Asia's beverage penetration growth. Companies investing now in Asia Pacific capacity, certified sustainable aluminium, premium formats, and BPA-free food can technology will be best positioned for the next decade.

Research Methodology

Primary Research

Primary research included structured interviews with over 120 industry participants in 2024–2025, comprising can manufacturers, beverage brand procurement managers, aluminium producers, food processors, recycling operators, and regulatory officials across North America, Europe, Asia Pacific, and Latin America.

Secondary Research

Secondary research encompassed CMI statistics, Aluminium Association data, European Aluminium reports, company annual reports, trade publications (The Canmaker, Packaging Digest), and regulatory databases including EU SUP Directive implementation tracking and FDA food contact guidance. Over 200 statistical sources were triangulated for market size validation.

Forecasting Models

Market size estimations used a bottom-up can volume model combined with top-down value analysis, incorporating aluminium price assumptions, per-capita consumption growth by region, format mix shift trajectories, and recycling rate improvements. Scenario analysis across base, optimistic, and conservative cases accounts for aluminium price volatility and regulatory pace uncertainty.

Aluminium Cans Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Billion Units |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Applications Covered | Beverages, Food, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Ball Corporation, Crown Holdings, ALTEMIRA Group, Toyo Seikan Co., Ltd., Canpack S.A., Orora Beverage, CCL Container Inc., Silgan Containers, Nampak Ltd., Tecnocap Group, SAPIN, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the aluminium cans market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global aluminium cans market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the aluminium cans industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Aluminium Cans Market Report

The global aluminium cans market was valued at USD 56.97 Billion in 2025 and is projected to reach USD 71.9 Billion by 2034.

The market is forecast to grow at a CAGR of 2.5% during 2026-2034, driven by sustainability regulations, craft and premium beverage growth, and rising canned food demand globally.

Beverages dominate at 72.6% in 2025, driven by carbonated soft drinks, beer, energy drinks, and RTD alcoholic beverages that increasingly prefer aluminium for its recyclability and chilling properties.

Food accounts for 18.4% in 2025, serving canned vegetables, soups, seafood, pet food, and ready meals requiring hermeticity, long shelf life, and compatibility with retort sterilisation processes.

North America leads with 34.8% in 2025, driven by the United States' annual can consumption, craft beer expansion, and well-established deposit return scheme infrastructure.

Key drivers include sustainability and recyclability demand, craft beer and premium beverage growth, rising canned food consumption, Asia Pacific FMCG expansion, and regulatory shift away from single-use plastics.

Asia Pacific is the fastest-growing region at approximately 3.6% CAGR, driven by China's energy drink market, India's can adoption acceleration, and Southeast Asia's rising FMCG beverage penetration.

Leading companies include Ball Corporation, Crown Holdings, ALTEMIRA Holdings, Toyo Seikan Co., Ltd., Canpack S.A., Orora Beverage, CCL Container Inc., Silgan Containers, Nampak Ltd., Tecnocap Group, and SAPIN.

The global aluminium cans market is projected to reach USD 64.5 Billion by 2030, reflecting steady compound growth from the 2025 base of USD 56.97 Billion at the market's 2.5% CAGR.

Aluminium offers infinite recyclability (versus PET's quality degradation), superior chilling properties, 100% light barrier, lower transport weight, and increasingly mandated sustainability credentials under EPR regulations.

Key opportunities include recycled-content sustainable can certification, slim and sleek premium format growth, India and Southeast Asia capacity investment, digital can printing for craft markets, and BPA-free food can coating technology.

Key challenges include aluminium price volatility, competition from PET and glass in certain categories, high capital costs of DWI manufacturing, near-term North American capacity oversupply, and BPA-NI coating reformulation requirements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)