Ambulatory Services Market Size, Share, Trends and Forecast by Service Type, Department, and Region, 2026-2034

Ambulatory Services Market Size and Share:

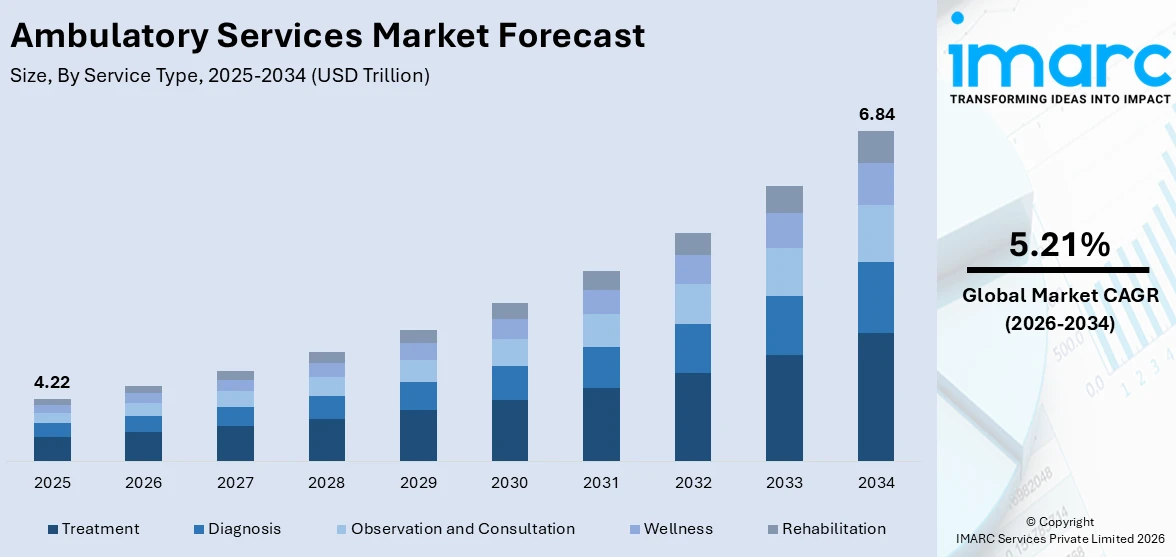

The global ambulatory services market size was valued at USD 4.22 Trillion in 2025. Looking forward, IMARC Group estimates the market to reach USD 6.84 Trillion by 2034, exhibiting a CAGR of 5.21% from 2026-2034. North America currently dominates the market, holding a market share of 45.5% in 2025. The region benefits from highly advanced healthcare infrastructure, extensive insurance coverage under Medicare and Medicaid programs, strong government incentives for cost-efficient outpatient care, and a rapidly aging population increasingly seeking convenient ambulatory alternatives to inpatient services, all of which collectively contribute to the ambulatory services market share.

The global ambulatory services market is experiencing growth driven by the increasing demand for outpatient healthcare services that offer convenience, lower costs, and reduced hospital stays. Patients are seeking quick consultations, minor surgical procedures, diagnostic tests, and preventive care outside traditional hospital settings. Advances in medical technology, including minimally invasive surgical techniques and portable diagnostic equipment, are enabling more procedures to be performed in outpatient facilities safely. Additionally, healthcare providers are expanding ambulatory service offerings to improve patient experience, optimize operational efficiency, and manage rising healthcare expenditures. The growing prevalence of chronic diseases, aging populations, and the focus on early diagnosis and treatment further support the rising adoption of ambulatory services worldwide.

The ambulatory services market in the United States is driven by a combination of advanced infrastructure, favorable reimbursement policies, and a well-established culture of outpatient care. High demand for cost-effective, convenient, and efficient healthcare delivery is encouraging providers to expand ambulatory surgery centers and outpatient clinics. Technological advancements, including integrated electronic health records (EHRs), minimally invasive surgical tools, and telehealth platforms, enhance the quality, safety, and efficiency of outpatient procedures. Reimbursement support from Medicare and commercial insurers further incentivizes healthcare providers to shift appropriate procedures from inpatient to outpatient settings. Reflecting this trend, in 2025, MedCore Partners and GI Alliance opened a new Ambulatory Surgery Center and managed clinic in Kansas City, Missouri, featuring advanced operating rooms, pre-op and recovery suites, and integrated technologies. The facility also offered specialty consultations, pre-surgical evaluations, and post-operative follow-ups, creating a comprehensive outpatient care experience and supporting the broader growth of ambulatory services across the US.

To get more information on this market Request Sample

Ambulatory Services Market Trends:

Development of Large-Scale Specialized Outpatient Facilities

The development of large-scale specialized outpatient facilities is a key factor influencing the market, as healthcare systems increasingly focus on centralizing complex care, enhancing patient access, and integrating advanced treatment options within a single location. Such facilities enable the delivery of high-quality, multidisciplinary care while reducing the reliance on inpatient hospitalization, improving operational efficiency, and fostering collaboration between clinical teams and research programs. For example, in 2024, the University of Kentucky began construction on its new Cancer and Advanced Ambulatory Building in Lexington, a 550,000-square-foot facility designed to house the UK Markey Cancer Center, a Comprehensive Spine Center, and expanded outpatient services. Scheduled for completion by 2027, this building will centralize oncology and spine care, provide state-of-the-art therapies, and support advanced clinical research. Initiatives like this illustrate how investment in specialized, high-capacity outpatient infrastructure enhances patient convenience, improves care coordination, and strengthens access to innovative therapies, driving sustained growth in the Ambulatory Services market globally.

Expansion of Ambulatory Surgery Networks

The expansion of national networks of outpatient surgery centers, which enhance access to specialized care while improving operational efficiency, is impelling the market growth. By creating platforms that consolidate multiple facilities under unified management, healthcare providers can standardize clinical protocols, streamline administrative processes, and leverage shared resources to reduce costs. This model also allows patients to receive high-quality care closer to home, minimizing travel and hospital stays while maintaining clinical excellence. For example, in 2025, Hospital for Special Surgery partnered with General Atlantic to launch a national platform of ambulatory surgery centers, acquiring Legent Health as a foundation for growth. The initiative combined HSS’s clinical expertise with General Atlantic’s scaling capabilities, enabling physician partnerships and operational efficiencies across the network. Such strategic expansion of outpatient surgical platforms illustrates a broader market trend, demonstrating how scalable, coordinated care delivery is driving increased adoption and sustained growth in the market.

Adoption of Minimally Invasive Outpatient Procedures

The increasing adoption of minimally invasive procedures in outpatient settings is a vital factor bolstering the ambulatory services market growth. These procedures allow patients to undergo complex surgeries with shorter recovery times, reduced hospital stays, and lower overall costs, while maintaining high clinical outcomes. Nationwide networks of centers delivering these services enhance patient convenience, optimize scheduling, and expand access to high-quality care. Supporting this trend, Cleveland Clinic partnered with Regent Surgical in 2025 to develop a nationwide network of ambulatory surgery centers specializing in procedures like hip and knee replacements. Patients recover briefly on-site before returning home, combining efficiency with cost-effectiveness. By providing standardized care across multiple locations, this approach improves geographic access to advanced procedures. The widespread adoption of minimally invasive techniques in outpatient facilities exemplifies a broader market shift toward efficiency, patient-centered delivery, and expanded service accessibility.

Ambulatory Services Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global ambulatory services market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on service type and department.

Analysis by Service Type:

- Diagnosis

- Observation and Consultation

- Treatment

- Wellness

- Rehabilitation

Treatment accounts for 38.5% of the market, reflecting its central role in outpatient healthcare delivery. This segment consists of a wide range of therapeutic and procedural interventions that can be performed efficiently outside traditional hospital settings. Key services include ambulatory surgical procedures, where minimally invasive techniques allow patients to undergo operations without overnight hospitalization, and infusion therapies, which provide essential medications such as biologics and antibiotics in outpatient clinics. Chemotherapy administration in ambulatory centers offers convenience and reduces the need for inpatient stays, while pain management interventions, including injections and nerve blocks, enable timely symptom control for chronic conditions. Additionally, same-day specialty consultations with active clinical management allow patients to receive comprehensive care, monitoring, and follow-up in a single visit. These practices exemplify how efficiency, patient convenience, and cost-effectiveness are shaping the adoption and expansion of treatment services globally, reflecting broader ambulatory services market trends.

Analysis by Department:

Access the comprehensive market breakdown Request Sample

- Primary Care Offices

- Outpatient Departments

- Emergency Departments

- Surgical Specialty

- Medical Specialty

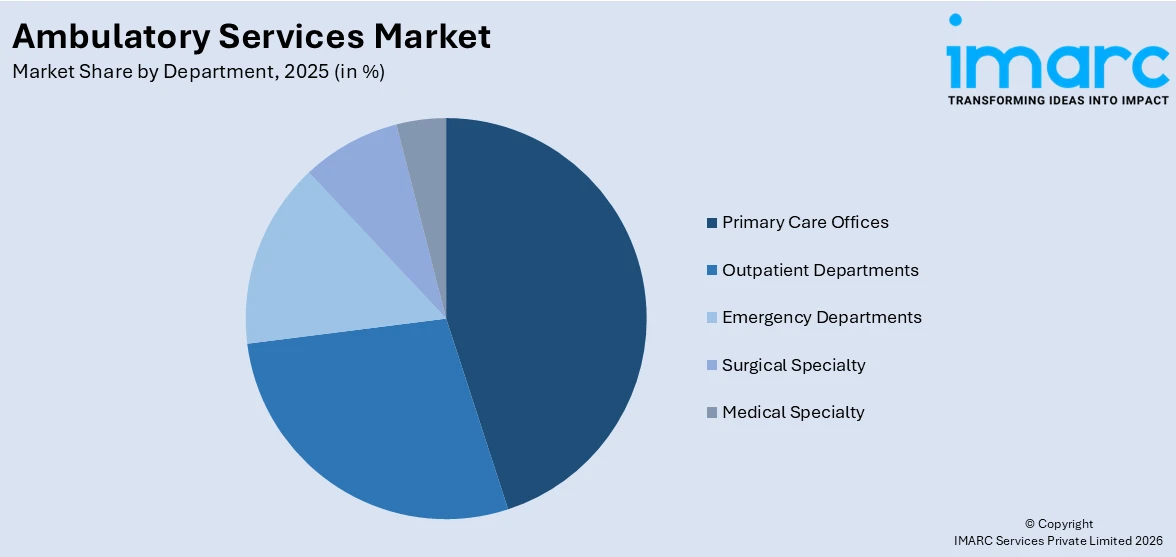

Primary care offices dominate the market, accounting for 42.5% of the overall share, as they constitute the primary entry point into the healthcare system. These facilities provide essential services, including routine wellness exams, chronic disease management, preventive screenings, immunizations, and initial diagnostic evaluations, collectively generating the highest volume of ambulatory patient visits worldwide. They also function as key coordinators within the healthcare ecosystem, directing referrals, overseeing ongoing medication plans, and maintaining long-term patient relationships, which drive frequent engagement across diverse populations. For instance, in 2025, Amazon One Medical partnered with Cleveland Clinic to launch its first primary care office in Avon, Northeast Ohio. This center delivers same- and next-day appointments, 24/7 virtual care, and on-site laboratory services, expanding access to preventive, chronic, and urgent care. By integrating digital and in-person care, the collaboration enhances patient access to coordinated outpatient and specialty services, demonstrating the growing emphasis on seamless, comprehensive ambulatory care delivery. The ambulatory services market outlook emphasizes expanding accessible, coordinated, and patient-centered outpatient care through integrated digital and in-person solutions.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 45.5% of the share, enjoys the leading position in the market. The region’s dominance is anchored by a well-established healthcare infrastructure and widespread adoption of outpatient care models. The region benefits from a network of primary care and specialty facilities that enhance patient access, optimize care delivery, and improve overall health outcomes. For example, in 2025, the Schroeder Ambulatory Centre in Ontario announced its opening on October 1 with 10 clinics offering both primary care and specialty services. The Centre plans to gradually expand its offerings to include surgeries, imaging, and advanced diagnostic procedures, consolidating multiple services under a single roof. This approach aims to provide efficient, equitable, and patient-centered care while improving convenience and continuity for community members. Investments in integrated outpatient facilities like Schroeder Ambulatory Centre exemplify the region’s emphasis on expanding capacity, enhancing service quality, and strengthening patient engagement. The ambulatory services market forecast indicates the dominance of North America driven by expanded outpatient capacity, improved service quality, and enhanced patient engagement.

Key Regional Takeaways:

United States Ambulatory Services Market Analysis

The United States constitutes the largest national market for ambulatory services worldwide, supported by a robust and well-funded outpatient care infrastructure that includes ambulatory surgery centers, primary care offices, specialty clinics, diagnostic imaging facilities, and rehabilitation centers, collectively managing a large volume of patient. The country’s market strength is driven by advanced healthcare delivery models, high adoption of outpatient procedures, and strong investment in facility expansion and technological integration, which together enhance patient access and care efficiency. In 2025, JLL launched a Healthcare Center of Excellence in the United States, led by Brannan Moss, aimed at helping clients optimize medical property portfolios and expand ambulatory services. The center provides data-driven insights and advisory support to hospitals, health systems, and investors, enabling more strategic development of outpatient infrastructure to meet growing demand. By focusing on improving access, operational efficiency, and growth across the sector, this initiative exemplifies how targeted investments and expertise are reinforcing the US leadership in ambulatory care, ensuring comprehensive, patient-centered, and scalable outpatient services nationwide.

Europe Ambulatory Services Market Analysis

The European ambulatory services market constitutes a significant and steadily growing portion of the regional healthcare sector, underpinned by universal healthcare systems that emphasize outpatient care and by EU policies promoting cost-efficient alternatives to inpatient hospitalization. The region’s growth is fueled by investments in specialized outpatient facilities, increasing adoption of minimally invasive procedures, and efforts to enhance patient access and satisfaction. In 2025, Smith+Nephew partnered with Standard Health to inaugurate the UK’s first Orthopaedic Ambulatory Surgery Centre in Poole, providing advanced joint repair and replacement procedures for both NHS and private patients. The center aimed to enhance operational efficiency, patient outcomes, and cost-effectiveness. This initiative was part of a broader strategy to establish 20 additional UK sites by 2030, directly responding to rising demand for orthopedic care. Facilities like this exemplify Europe’s shift toward high-quality, patient-centered outpatient services that reduce hospitalization and optimize resource utilization.

Asia-Pacific Ambulatory Services Market Analysis

The Asia-Pacific ambulatory services market is growing, driven by expanding healthcare infrastructure, increasing urban populations, and government-led modernization initiatives across major economies. China’s vast network of community health centers and outpatient clinics manages billions of patient encounters annually, with sustained investment in primary care capacity fueling continued volume growth. In 2025, Shanghai inaugurated Parkway Medi-Centre Xintiandi, an ambulatory care facility developed by IHH Healthcare, designed to enhance medical tourism and deliver advanced outpatient services. The center hosted an international medical team and supported billing through over 60 global insurers, improving access for expatriates and international patients. Complementing existing hospitals and clinics, this facility aligned with Shanghai’s strategy to attract foreign investment in healthcare while expanding high-quality outpatient services. Initiatives like Parkway Medi-Centre exemplify how the Asia-Pacific region is rapidly scaling integrated ambulatory care to meet rising demand and strengthen its position in the global healthcare landscape.

Latin America Ambulatory Services Market Analysis

The Latin American ambulatory services market is experiencing growth, driven by increasing government investment, rising private sector involvement in outpatient facility development, and a growing middle-class population seeking accessible, cost-effective care. In 2025, Mexico announced a MX$4 billion investment to expand public health infrastructure, including the construction of new hospitals and clinics and the upgrading of existing facilities to enhance access and quality. The government secured 96% of essential medicines for 2025–2026 and introduced digital platforms to monitor distribution, aiming to strengthen healthcare delivery, integrate services across networks, and ensure facilities are fully staffed and equipped. Such initiatives are enhancing outpatient care capacity and supporting the region’s broader healthcare modernization efforts.

Middle East and Africa Ambulatory Services Market Analysis

The Middle East and Africa ambulatory services market is growing, supported by extensive government healthcare modernization initiatives and growing private sector investment in outpatient facilities. In 2024, Burjeel Holdings presented two innovative healthcare solutions at the Global Health Exhibition, including Alkalma, a mental health platform, and Burjeel One, a network of day surgery centers. These programs aimed to broaden access to mental health services and specialized outpatient care across Saudi Arabia, in line with Vision 2030. The first Burjeel One centers, scheduled to open in Riyadh by 2025, planned to integrate advanced technologies to deliver same-day, high-quality medical care, reflecting the region’s commitment to expanding accessible, technologically advanced ambulatory services.

Competitive Landscape:

The ambulatory services market features a moderately consolidated competitive landscape, with large, multi-facility operators dominating alongside regional specialty networks and independent physician-owned centers. Major players leverage scale, brand recognition, and integrated service offerings to attract patients and optimize operational efficiency across multiple locations. Regional networks and specialty providers differentiate through niche expertise, personalized care, and community engagement, addressing specific patient needs in areas such as outpatient surgery, diagnostics, and preventive care. Competitive strategies focus on service diversification, adoption of advanced medical technologies, and partnerships with insurers and healthcare systems. Additionally, the expansion of telehealth, urgent care, and outpatient procedural services enhances market positioning. These dynamics create a mix of competition and collaboration, where established operators pursue acquisitions and strategic alliances to expand geographic reach, improve patient retention, and strengthen their presence within the evolving ambulatory services ecosystem.

The report provides a comprehensive analysis of the competitive landscape in the ambulatory services market with detailed profiles of all major companies, including:

- Envision Healthcare

- HCA Healthcare

- Healthway Medical Group

- Medical Facilities Corporation

- NueHealth

- SCA Health

- Surgery Partners

- Terveystalo

- TH Medical

Latest News and Developments:

- In January 2026, Tampa General Hospital and Mass General Brigham launched a joint ambulatory care network along Florida’s East Coast, expanding access to primary, specialty, and surgical outpatient services. The network aims to provide coordinated, patient-focused care to over two million residents in Martin, St. Lucie, and Palm Beach counties. It will include new facilities like a radiation oncology center and strengthen integrated outpatient services across the region.

- In December 2025, DNV has launched an accreditation program for Ambulatory Surgery Centers (ASCs), aiming to enhance patient safety and quality standards in outpatient surgical care. The program helps ASCs improve operational efficiency, reduce hospital system burden, and maintain continuous quality improvement. This expansion underscores DNV’s commitment to supporting scalable, high-quality healthcare globally.

Ambulatory Services Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Trillion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Service Types Covered | Diagnosis, Observation and Consultation, Treatment, Wellness, Rehabilitation |

| Departments Covered | Primary Care Offices, Outpatient Departments, Emergency Departments, Surgical Specialty, Medical Specialty |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Envision Healthcare, HCA Healthcare, Healthway Medical Group, Medical Facilities Corporation, NueHealth, SCA Health, Surgery Partners, Terveystalo, TH Medical, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the ambulatory services market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global ambulatory services market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter’s Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the ambulatory services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Ambulatory Services Market Size Report

The ambulatory services market was valued at USD 4.22 Trillion in 2025.

The ambulatory services market is projected to exhibit a CAGR of 5.21% during 2026-2034, reaching a value of USD 6.84 Trillion by 2034.

The ambulatory services market is driven by the development of large-scale specialized outpatient facilities, expansion of ambulatory surgery networks, and increasing adoption of minimally invasive procedures, all of which enhance patient access, improve operational efficiency, reduce hospital reliance, and support high-quality, cost-effective, and patient-centered outpatient care.

North America currently dominates the ambulatory services market, accounting for a share of 45.5%. The region benefits from highly advanced healthcare infrastructure, extensive Medicare and commercial insurance coverage, strong regulatory support for ambulatory care expansion, and a large and rapidly aging population generating sustained outpatient care demand.

Some of the major players in the ambulatory services market include Envision Healthcare, HCA Healthcare, Healthway Medical Group, Medical Facilities Corporation, NueHealth, SCA Health, Surgery Partners, Terveystalo, TH Medical, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)