Ammonia Crackers Market Size, Share, Trends and Forecast by Type, Capacity, Product Type, Application, and Region, 2026-2034

Ammonia Crackers Market Size and Share:

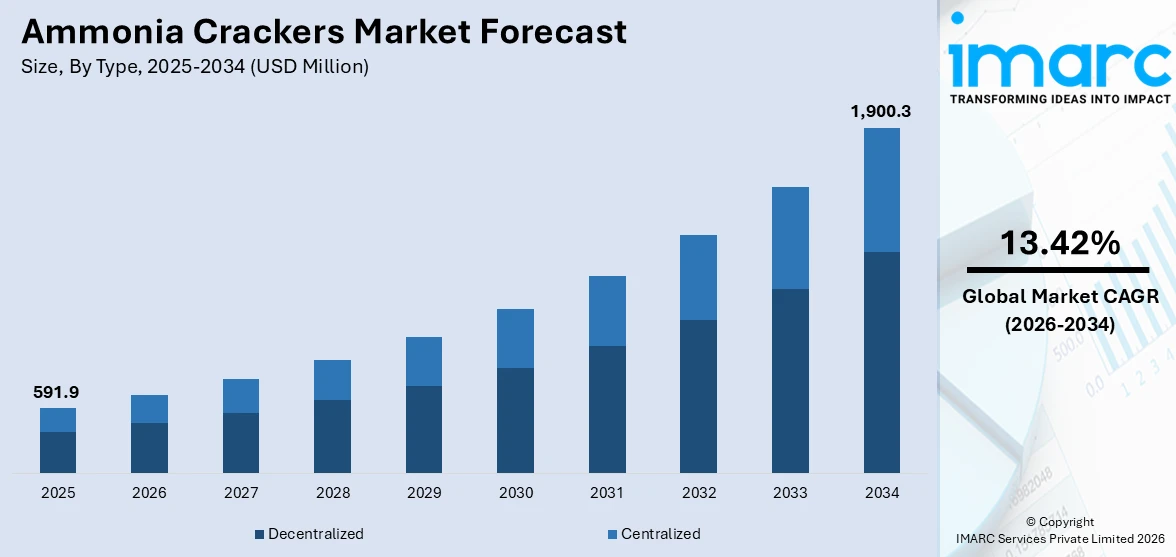

The global ammonia crackers market size was valued at USD 591.9 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 1,900.3 Million by 2034, exhibiting a CAGR of 13.42% from 2026-2034. Asia Pacific currently dominates the market, fueled by expanding demand for hydrogen as a clean fuel, rising use of ammonia as a hydrogen carrier, growing industrial decarbonization programs, and widespread application in metal processing and semiconductor industries. Incentives provided by governments to low-emission technologies also add to market expansion.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 591.9 Million |

| Market Forecast in 2034 | USD 1,900.3 Million |

| Market Growth Rate 2026-2034 | 13.42% |

A major driver of the global ammonia crackers market is the growing demand for hydrogen as a clean energy source, driven by global decarbonization and carbon neutrality goals. Hydrogen's zero-emission combustion is making it more popular, but there are major logistical obstacles in storing and transporting it. Ammonia, containing 17.6% hydrogen by weight, is increasingly used as an efficient hydrogen carrier due to its higher energy density and easier handling compared to liquid hydrogen. Ammonia crackers serve an essential function by re-converting ammonia back into hydrogen at the end user, facilitating safer and more efficient transportation across industries such as transport, power generation, and heavy industry.

To get more information on this market Request Sample

In the U.S., the ammonia crackers market is primarily driven by the growing emphasis on clean energy transition and hydrogen adoption across transportation, power, and industrial sectors with 81.50% market share. With the U.S. hydrogen market producing approximately 10 million metric tons annually, ammonia crackers play a vital role in converting ammonia into hydrogen for various applications. Growing investment in hydrogen infrastructure, coupled with government policies towards energy independence and decarbonization, increases the potential of the market. Ammonia's efficiency as a carrier of hydrogen over long distances and large scales of distribution adds further impetus to the requirement for ammonia crackers. The growing funding by the U.S. government for developing hydrogen economies and programs to bolster domestic supply chains also adds to the increasing demand for ammonia cracker technologies.

Ammonia Crackers Market Trends:

Growing Demand for Hydrogen in Clean Energy Applications

The rising demand for hydrogen in clean energy applications is driven by its potential as a clean, efficient, and versatile energy carrier. As global efforts intensify to reduce carbon emissions, hydrogen is gaining traction for use in fuel cells, power generation, and energy storage. Governments and industries are investing in hydrogen technologies to support decarbonization, especially in hard-to-abate sectors like transportation and heavy industry. Green hydrogen, produced via electrolysis using renewable energy, is particularly favored for its low environmental impact. Additionally, hydrogen can be blended with natural gas or used to produce synthetic fuels, enhancing its role in transitioning to a sustainable energy system. These factors collectively contribute to the growing adoption of hydrogen in clean energy initiatives.

Advantages of Ammonia as a Hydrogen Carrier

Ammonia offers significant advantages as a hydrogen carrier, positioning it as a practical solution for large-scale hydrogen storage and transportation. With its high hydrogen density and ease of liquefaction, ammonia can be transported efficiently over long distances without the need for high-pressure or cryogenic conditions. Its well-established global infrastructure further supports widespread adoption. Importantly, ammonia can be decomposed to release hydrogen at the point of use, making it suitable for off-grid and mobile applications. Recent research has demonstrated ammonia conversion rates as high as 99.4%, with hydrogen yields ranging from 84% to 99.5%, ensuring high efficiency in hydrogen recovery. This hydrogen meets ISO 14687:2019 purity standards, expanding its applicability in fuel cells and green energy systems. These attributes make ammonia a scalable, cost-effective solution for the global hydrogen economy.

Industrial Applications of Hydrogen

Hydrogen plays a crucial role in various industrial applications due to its versatility and clean energy potential. It is primarily used in the production of ammonia for fertilizers through the Haber-Bosch process, which accounts for a significant portion of global hydrogen demand. Hydrogen is also essential in petroleum refining, where it is used for hydrocracking and desulfurization to produce cleaner fuels. Additionally, hydrogen serves as a reducing agent in the production of metals like steel, offering a cleaner alternative to traditional methods that rely on coal. In recent years, hydrogen has gained traction in fuel cells for clean energy applications, including transportation and stationary power generation, contributing to the transition to low-carbon energy systems. These industrial uses highlight hydrogen’s growing role in sustainable development.

Ammonia Crackers Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global ammonia crackers market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, capacity, product type, and application.

Analysis by Type

- Centralized

- Decentralized

Decentralized ammonia crackers hold the largest market share of 60% due to their ability to provide localized hydrogen production, reducing reliance on centralized infrastructure. This decentralization is crucial for industries operating in remote or energy-scarce regions, where transporting hydrogen from large-scale plants is costly and inefficient. Decentralized systems offer the flexibility to produce hydrogen on-demand, making them ideal for applications in industries such as transport, agriculture, and chemical manufacturing. Furthermore, decentralized ammonia cracking reduces the need for extensive pipeline networks and high-capital investments required for centralized facilities. With the global push toward clean and sustainable energy solutions, the demand for decentralized ammonia crackers has surged, as they align with goals of reducing CO2 emissions and increasing energy security by enabling localized, green hydrogen production.

Analysis by Capacity

- Large-Scale (>1,000 Nm3/hr)

- Medium Scale (250-1,000 Nm3/hr)

- Small-Scale (<250 Nm3/hr)

Small-scale ammonia crackers (<250 Nm³/hr) account for 45% of the market share due to their versatility and cost-effectiveness in decentralized hydrogen production. These systems are ideal for smaller, local operations where large-scale infrastructure isn't feasible. They are increasingly used in industries that require on-site hydrogen production for specific applications like fuel cells or industrial processes, particularly in remote areas or where energy infrastructure is limited. Their compact design makes them suitable for a range of industries, including agriculture, transport, and chemicals, where hydrogen is needed for specific, localized uses. Additionally, the lower capital investment required for small-scale ammonia crackers makes them an attractive option for businesses seeking to adopt clean energy solutions without significant upfront costs. This has led to their widespread adoption in regions focused on hydrogen as a sustainable energy carrier.

Analysis by Product Type

Access the comprehensive market breakdown Request Sample

- Catalytic Crackers

- Electrochemical Crackers

- Plasma-Assisted Crackers

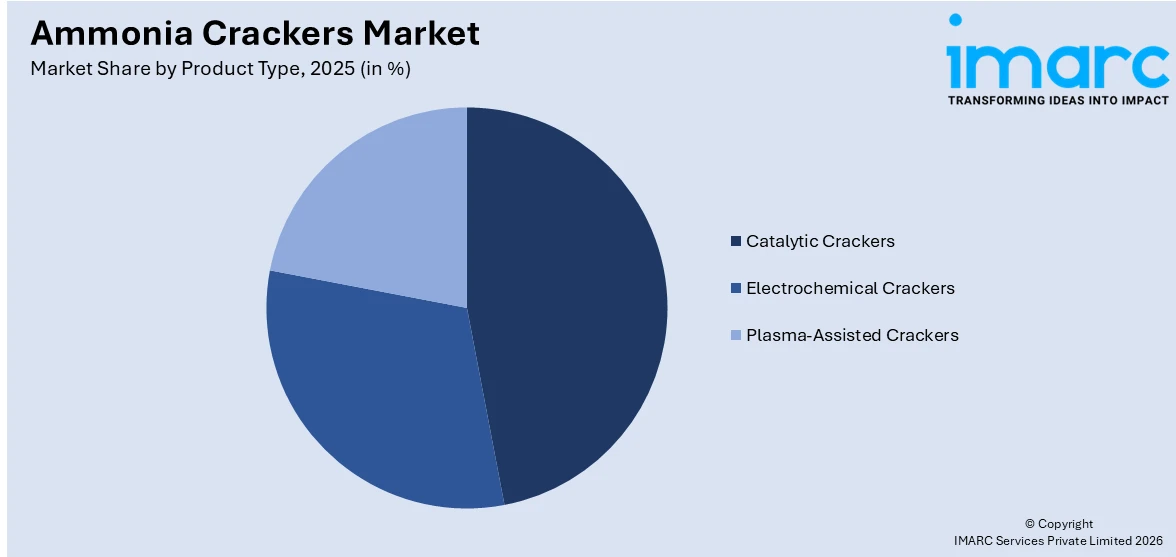

Catalytic crackers dominate the ammonia crackers market with a 47.5% market share due to their efficiency in producing high-purity hydrogen. These systems use catalysts to break down ammonia into hydrogen and nitrogen, ensuring a cleaner, more controlled reaction compared to other cracking methods. The ability to operate at lower temperatures and pressures makes catalytic crackers more energy-efficient, reducing operational costs and enhancing their appeal for large-scale commercial use. As industries focus on reducing carbon footprints, catalytic crackers provide a more sustainable solution for hydrogen production. Their application in industries like refining, chemicals, and energy further strengthens their market dominance, as these sectors increasingly turn to hydrogen for cleaner fuel and raw materials. The widespread adoption of catalytic ammonia cracking aligns with the growing demand for clean energy solutions across various industries.

Analysis by Application

- Heat Treatment

- Metal Industry

- Oil and Gas

- Mobility

- Power Generation

- Others

Heat treatment represents the largest market share in the ammonia crackers market due to its significant role in various industrial processes. Ammonia crackers are used to produce hydrogen, which is essential in heat treatment applications, particularly in the automotive, aerospace, and manufacturing industries. Hydrogen produced through ammonia cracking is utilized as a reducing agent in heat treatment processes, helping to improve material properties such as strength, hardness, and durability. The increasing demand for high-performance materials and the growing need for precision in manufacturing drive the need for hydrogen in heat treatment. Furthermore, hydrogen is favored due to its cleaner burning properties compared to traditional fuels, aligning with the industry's focus on reducing carbon emissions. As industries seek more sustainable and efficient processes, ammonia crackers for hydrogen production in heat treatment applications are witnessing increased adoption.

Regional Analysis:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East

- Africa

Asia-Pacific is the leading region in the ammonia crackers market due to several key factors. The region has a rapidly growing demand for hydrogen as a clean energy source, particularly in industries such as refining, chemicals, and heavy transport. Many countries in Asia-Pacific are investing in ammonia cracking technologies to support their hydrogen supply chains, driven by their commitment to reducing carbon emissions and achieving energy security. Additionally, the region benefits from established ammonia production infrastructure, facilitating the integration of ammonia cracking systems. The presence of major energy import hubs and the ongoing shift towards sustainable energy solutions further solidify Asia-Pacific's dominance in this market. Strong governmental support for green energy projects and clean hydrogen initiatives also plays a significant role in driving market growth.

Key Regional Takeaways:

North America Ammonia Crackers Market Analysis

The North American ammonia crackers market is experiencing substantial growth, driven by the increasing demand for hydrogen as a clean energy source. Ammonia crackers play a crucial role in the production of hydrogen from ammonia, which is gaining traction in industries such as oil refining, chemicals, and transportation. The market is particularly strong in the United States, where the adoption of ammonia cracking technology is bolstered by the need for hydrogen in refining processes and the energy transition toward cleaner fuels. Technological advancements, along with investments from major industry players, are accelerating the commercialization of ammonia cracking systems. Companies are focusing on improving efficiency, reducing costs, and scaling up production to meet the rising demand for hydrogen. The Midwest region, with its robust industrial infrastructure, is becoming a key hub for ammonia cracker installations. Additionally, the region's proximity to renewable energy sources and strategic import hubs contributes to the growth of the market, supporting its role in the hydrogen supply chain.

United States Ammonia Crackers Market Analysis

The United States ammonia crackers market is experiencing notable growth, driven by increasing demand for clean hydrogen across transportation, industrial, and energy sectors. A strong emphasis on reducing carbon emissions and enhancing domestic energy production has accelerated the integration of ammonia crackers into hydrogen supply chains. Industries such as metal processing, electronics, and fuel cell manufacturing are adopting ammonia-based hydrogen solutions to ensure reliable and scalable energy access. Supportive federal initiatives and funding for hydrogen infrastructure further stimulate market development. The flexibility of ammonia crackers to produce hydrogen on-site enhances their appeal in decentralized energy systems. Additionally, the availability of technical expertise and advanced manufacturing capabilities contributes to innovation and localized deployment. Strategic collaborations among energy companies, equipment manufacturers, and government agencies are encouraging investments in ammonia cracking technologies. The United States also benefits from a robust industrial base, enabling the integration of crackers into both traditional and emerging hydrogen applications. The market outlook remains strong with rising interest in clean hydrogen pathways.

Europe Ammonia Crackers Market Analysis

The European ammonia crackers market is progressing steadily because of the aggressive decarbonization plans and shift towards hydrogen-based energy solutions in the region. Ammonia is being envisioned as a central carrier for hydrogen transportation, particularly from renewable energy surplus regions. The increasing demand for clean mobility and energy independence has raised interest in cracking technologies. Refining, chemical, and steel industries are looking at ammonia crackers to fulfill sustainability objectives. Moreover, existing infrastructure and the availability of solid regulatory support promote the use of ammonia-based hydrogen solutions. Public-private partnerships also promote innovation and commercialization. The focus on integrating crackers with renewable ecosystems will be expected to drive the long-term market outlook.

Asia Pacific Ammonia Crackers Market Analysis

Asia Pacific is a prominent region in the ammonia crackers market, driven by rising energy demand, industrial expansion, and clean fuel adoption. Countries such as China, Japan, and South Korea are actively investing in hydrogen infrastructure where ammonia crackers play a central role. The flexibility of ammonia as a hydrogen carrier supports large-scale and cross-border energy applications. Regional policies promoting cleaner industrial practices and the decarbonization of energy systems are accelerating technology deployment. Ammonia crackers are increasingly used in sectors such as power generation, transportation, and manufacturing. As governments continue to invest in low-emission technologies, the market outlook remains promising.

Latin America Ammonia Crackers Market Analysis

In Latin America, the ammonia crackers market is gradually emerging, supported by the region's growing focus on alternative energy and industrial decarbonization. Interest in hydrogen technologies is increasing among sectors such as mining, refining, and heavy manufacturing. Ammonia is being evaluated as a viable hydrogen carrier due to its transport efficiency. The development of renewable energy projects in select countries is expected to complement ammonia cracking efforts. Market expansion remains moderate but is likely to gain momentum as hydrogen strategies become more defined.

Middle East and Africa Ammonia Crackers Market Analysis

The Middle East and Africa (MEA) region is undergoing emerging advancements in the ammonia crackers market, supported by rising need for exporting hydrogen via ammonia. Regions with high renewable and natural gas resources are investigating ammonia as a carrier for green and blue hydrogen. Infrastructure investment and pilot projects are starting to define regional market potential. Increasing collaborations with international energy players signal a strategic drive toward integrating ammonia crackers into larger hydrogen value chains.

Competitive Landscape:

The competitive landscape is characterized by the presence of both established players and emerging participants focusing on improvement and efficiency. Competition is driven by the development of advanced cracking technologies, including compact reactor designs and high-performance catalysts. Companies are actively investing in R&D to enhance hydrogen yield and energy efficiency. Strategic collaborations, collaborative pilot projects and technology licensing are common approaches to expand market reach and improve offerings. The market also sees differentiation based on system scalability, integration capabilities with renewable sources, and after-sales support. Customization and modular system designs are increasingly influencing competitiveness, particularly as demand grows for decentralized and mobile hydrogen production solutions across various industrial sectors.

The report provides a comprehensive analysis of the competitive landscape in the ammonia crackers market with detailed profiles of all major companies, including:

- Air Liquide

- AMMPOWER

- AMOGY Inc

- Duiker Combustion Engineers

- Haldor Topsoe A/S

- KBR Inc

- Lindberg/MPH

- MVS Engineering Pvt. Ltd.

- Nuberg GPD

- Siemens Energy

- thyssenkrupp AG

Latest News and Developments:

- In March 2025, AFC Energy established the world's first portable ammonia cracking module, Hy-5, that generates grey hydrogen at £10/kg ($12.70/kg). On track for 2026 delivery, the system can generate up to 500kg/day and is a plug-and-play "fuel as a service" proposition. Hy-5 provides competitive hydrogen pricing while avoiding high upfront costs and infrastructure requirements of traditional electrolysers, making it suitable for transportation applications, off-grid EV charging, and industry.

- In January 2025, Syzygy Plasmonics and Lotte Chemical successfully established the world's largest all-electric ammonia cracking system at Ulsan, South Korea, with 81% energy efficiency and 99% conversion. The achievement proves that ammonia can be used as a carrier for hydrogen, and clean ammonia imports can supply hydrogen to Korea, Japan, and Eastern Europe. The test opening the door to comer.

- In December 2024, Air Liquide been conferred a €110 million grant for its ENHANCE project in Antwerp-Bruges, Belgium from the European Innovation Fund. The project involves the production of low-carbon and renewable hydrogen from ammonia, the first big industrial project of this kind in Europe. Air Liquide will construct a renewable ammonia cracking facility and hydrogen liquefier, enabling decarbonization in refining and transport sectors while cutting CO₂ emissions by more than 300,000 tonnes per year.

- In December 2024, Air Liquide will begin its first pilot ammonia cracker in the Port of Antwerp in Q1 2025, which is an essential highlight for the commercialization of ammonia cracking equipment. This investment underpins low-carbon ammonia value chains in Europe. Several projects in Antwerp and Rotterdam are underway, with midstream player VTTI providing third-party access to ammonia crackers. This technology might become an essential source of electrolytic hydrogen in key import hubs.

- In June 2024, H2SITE designed the most effective ammonia cracker based on membrane reactor technology for the Ammogen Project in Birmingham, UK. The system yields 200 kg of green hydrogen on a daily basis for mobility purposes. The novel technology integrates ammonia cracking and hydrogen separation, with more than 98% hydrogen recovery under mild temperatures. This project confirms the membrane reactor technology and lays the foundation for scalability in future large-scale applications for import terminals and maritime purposes.

Ammonia Crackers Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Centralized, Decentralized |

| Capacities Covered | Large-Scale (>1,000 Nm3/hr), Medium Scale (250-1,000 Nm3/hr), Small-Scale (<250 Nm3/hr) |

| Product Types Covered | Catalytic Crackers, Electrochemical Crackers, Plasma-Assisted Crackers |

| Applications Covered | Heat Treatment, Metal Industry, Oil and Gas, Mobility, Power Generation, Others |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East, Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Air Liquide, AMMPOWER, AMOGY Inc, Duiker Combustion Engineers, Haldor Topsoe A/S, KBR Inc, Lindberg/MPH, MVS Engineering Pvt. Ltd., Nuberg GPD, Siemens Energy, thyssenkrupp AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the ammonia crackers market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global ammonia crackers market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the ammonia crackers industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Ammonia Crackers Market Report

The ammonia crackers market was valued at USD 591.9 Million in 2025.

The ammonia crackers market was valued at USD 1,900.3 Million in 2034, exhibiting a CAGR of 13.42% during 2026-2034.

Key factors driving the ammonia crackers market include the growing demand for low-carbon hydrogen, advancements in ammonia cracking technology, the need for sustainable energy solutions, and the increasing adoption of ammonia as a hydrogen carrier for transportation and industrial applications. These factors support the transition to cleaner energy sources globally.

Asia-Pacific leads the ammonia crackers market due to its strong industrial growth, government support for hydrogen adoption, and increasing recognition of ammonia as a hydrogen carrier. Countries like China, Japan, and South Korea are investing in ammonia cracking infrastructure to meet rising energy demands, enhance sustainability, and support low-carbon goals.

Some of the major players in the ammonia crackers market include Air Liquide, AMMPOWER, AMOGY Inc, Duiker Combustion Engineers, Haldor Topsoe A/S, KBR Inc, Lindberg/MPH, MVS Engineering Pvt. Ltd., Nuberg GPD, Siemens Energy, thyssenkrupp AG, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)