Animal Vaccine Market Size, Share, Trends and Forecast by Product, Animal Type, Route of Administration, and Region, 2026-2034

Animal Vaccine Market Size, Share, Trends & Forecast (2026-2034)

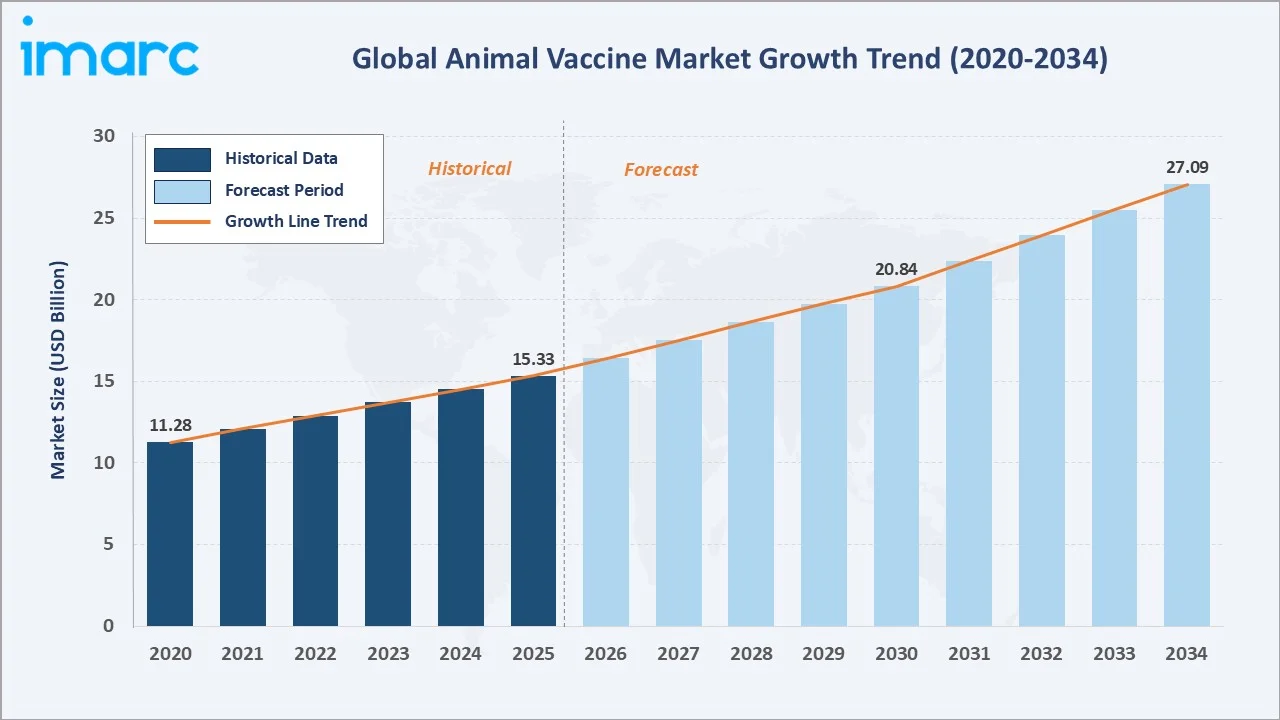

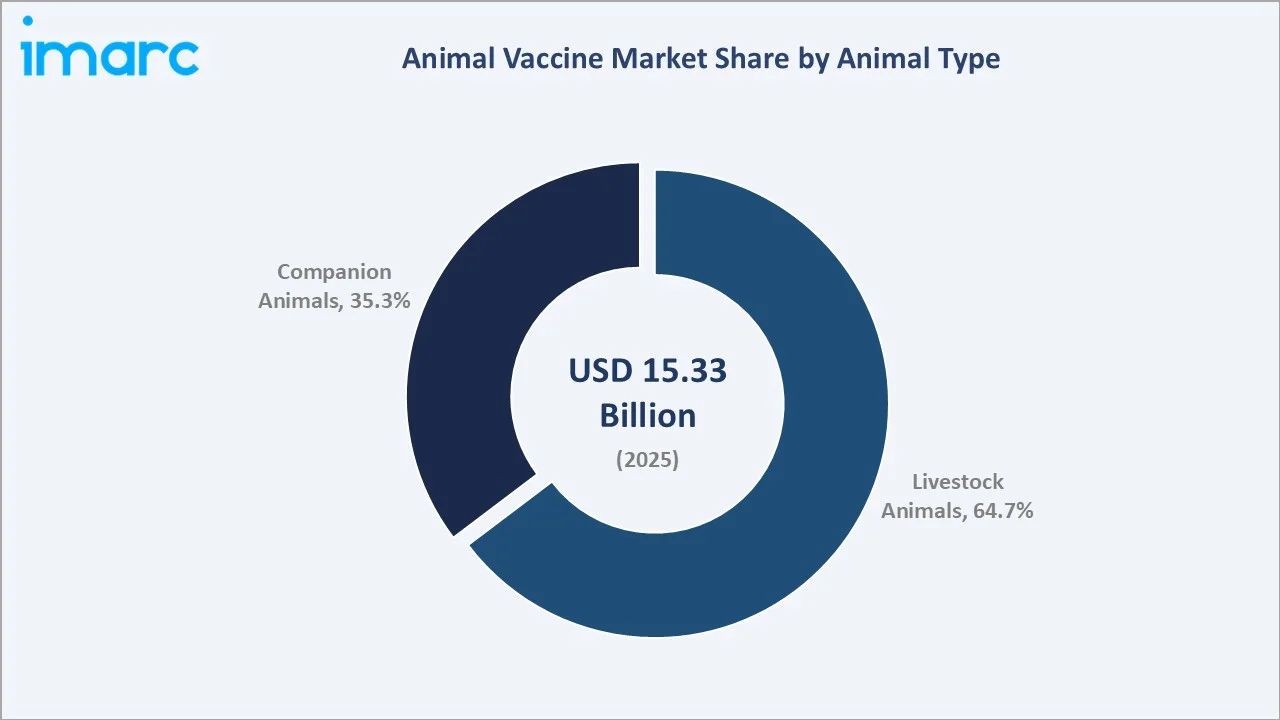

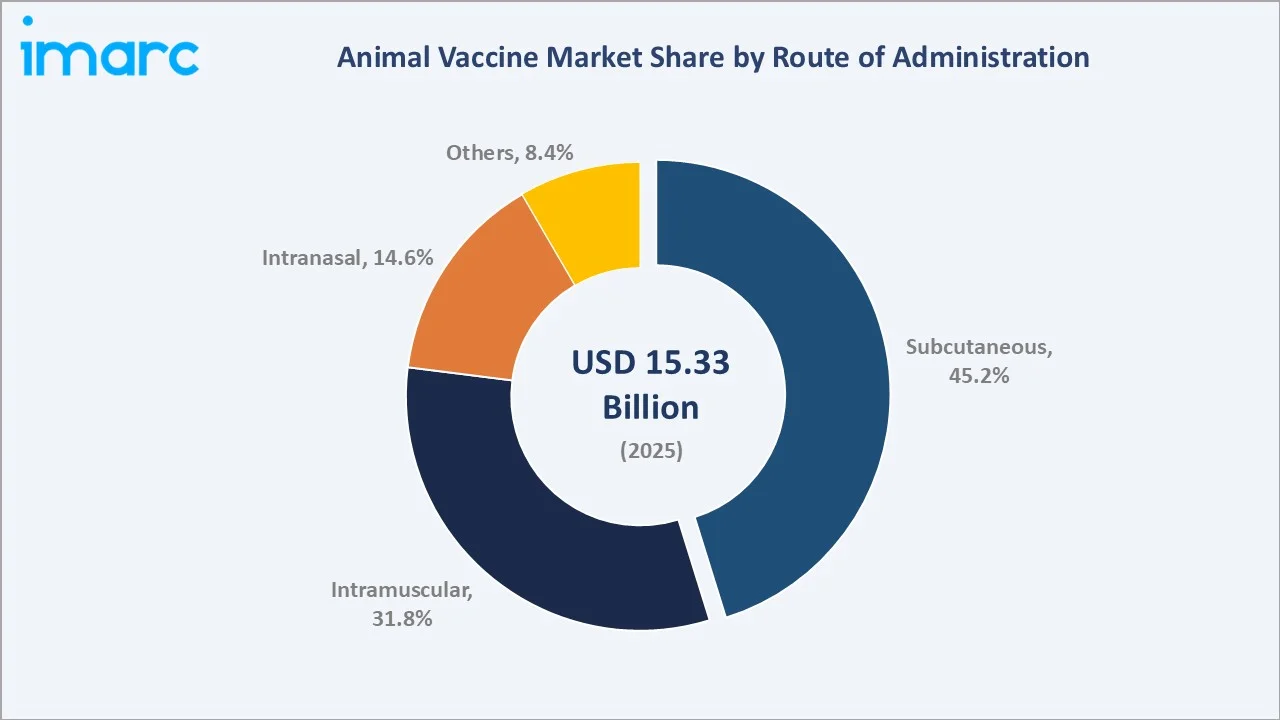

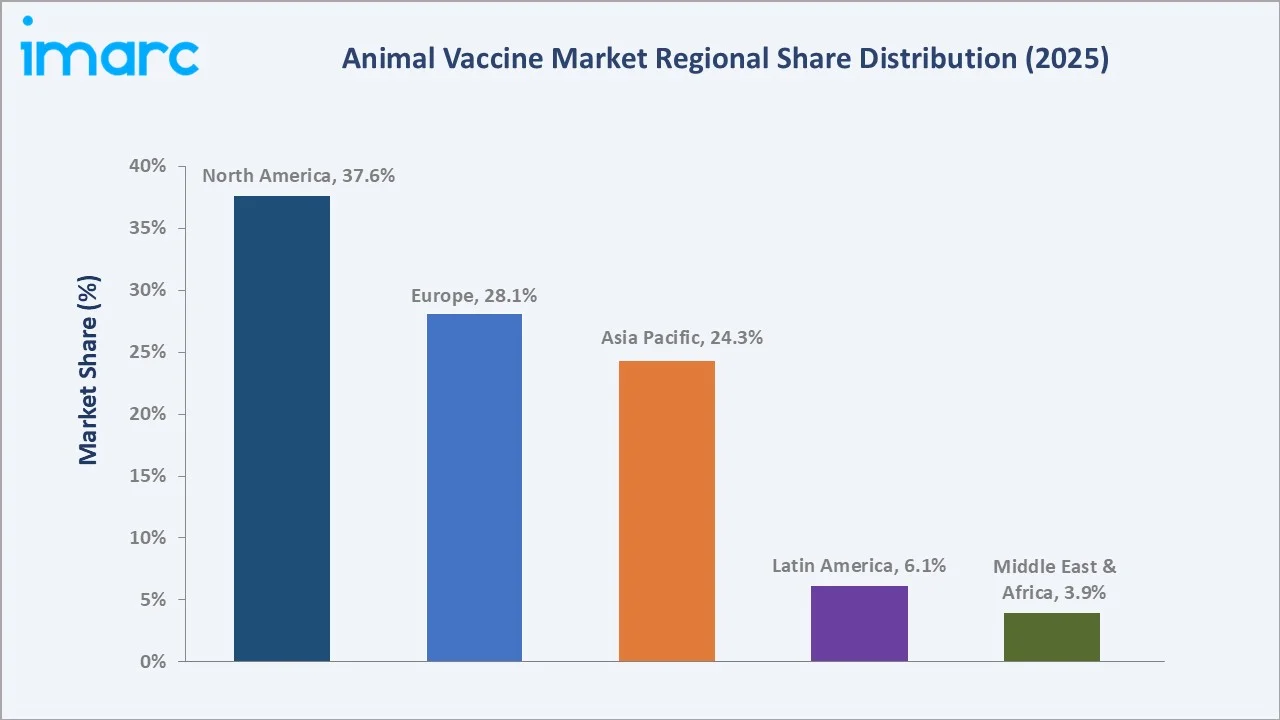

The global animal vaccine market reached USD 15.33 Billion in 2025 and is projected to reach USD 27.09 Billion by 2034, growing at a CAGR of 6.33% during 2026-2034. The market is driven by growing livestock and aquaculture production, rising pet ownership and humanization, increasing awareness of disease prevention, and advancements in vaccine technologies such as recombinant, DNA, and mRNA platforms. Vaccinations for Foot and Mouth Disease (FMD), Brucellosis, Peste des Petits Ruminants (PPR), and Classical Swine Fever (CSF) are covered by 100% central assistance under the Livestock Health and Disease Control Programme (LHDCP) across all Indian states and Union Territories. This government-backed, fully subsidized vaccination initiative boosts demand for animal vaccines. Livestock animals dominate at 64.7%. Subcutaneous administration leads at 45.2%. North America commands 37.6% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 15.33 Billion |

|

Forecast Market Size (2034) |

USD 27.09 Billion |

|

CAGR (2026-2034) |

6.33% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Animal Type |

Livestock Animal (64.7%, 2025) |

|

Dominant Route of Administration |

Subcutaneous (45.2%, 2025) |

|

Leading Region |

North America (37.6%, 2025) |

The market expanded from USD 11.28 Billion in 2020 to USD 15.33 Billion in 2025, anchored at USD 20.84 Billion in 2030, and forecast to reach USD 27.09 Billion by 2034. The COVID-19 pandemic led to lasting changes in demand, with higher rates of pet adoption permanently boosting companion animal vaccine needs, while disruptions in supply chains during the pandemic heightened livestock producers’ focus on disease prevention, driving sustained investment in livestock vaccines.

To get more information on this market, Request Sample

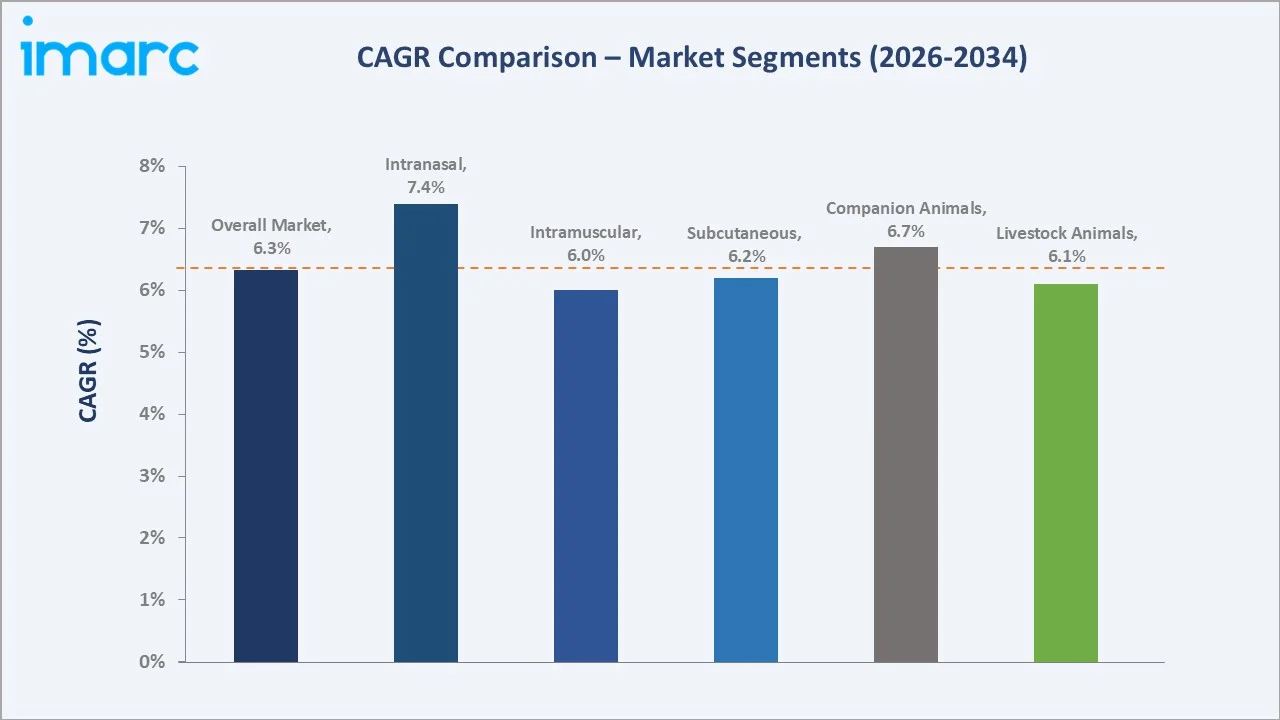

Companion animals grow fastest at ~6.7% CAGR through premiumization toward non-core vaccines and improving digital veterinary health platforms, driving compliance. Intranasal route grows fastest at ~7.4% CAGR through Bordetella bronchiseptica kennel cough vaccines, bovine intranasal respiratory vaccines, and the needle-free mucosal immunity advantages demonstrated for respiratory pathogen vaccines across livestock and companion animal species.

Executive Summary

The global animal vaccine market reached USD 15.33 Billion in 2025, representing the intersection of food security, companion animal welfare, and pandemic preparedness as the three structural demand drivers that collectively sustain robust market growth independent of any single economic cycle. The market is projected to reach USD 27.09 Billion by 2034.

Livestock animals at 64.7% dominate through the volume-intensive vaccination programs across commercial poultry, swine, cattle, and aquaculture. Subcutaneous administration at 45.2% leads through its established suitability for killed/inactivated vaccine delivery for companion animal core vaccines and adjuvanted livestock killed vaccines requiring depot formation. North America, at 37.6%, leads globally through the world's highest pet adoption, requiring vaccinations and favorable regulatory compliance for animal vaccines.

Key Market Insights

|

Insight |

Data |

|

Dominant Animal Type |

Livestock Animal - 64.7% share (2025) |

|

Dominant Route of Administration |

Subcutaneous - 45.2% market share (2025) |

|

Leading Region |

North America - 37.6% market share (2025) |

|

Market Opportunity |

Poultry vaccine commercial programs; swine vaccine launch; India livestock scale-up; mRNA vaccine platforms; non-core companion animal expansion; aquaculture vaccine new species |

Key Analytical Observations Supporting the Above Data:

- Livestock animals at 64.7%: The livestock animals dominate the market because it underpins global food security and trade, with high demand for disease prevention in cattle, poultry, and swine, making vaccination critical for both economic stability and sustainable protein production.

- Subcutaneous at 45.2%: The subcutaneous segment dominates the market because it provides precise, consistent dosing with minimal stress or injury to animals, making it the preferred delivery method for both livestock and companion animal immunizations.

- North America at 37.6%: The North America region dominates the market due to its advanced veterinary infrastructure, high adoption of preventive healthcare, and strong regulatory support, making it a hub for innovation and early implementation of next-generation vaccines.

Animal Vaccine Market Overview

The global animal vaccine market encompasses the research, development, manufacturing, regulatory approval, distribution, and clinical administration of biological products providing active immunological protection against infectious and parasitic diseases across companion animals and production animals. The market includes live attenuated vaccines, inactivated killed vaccines, recombinant subunit vaccines, viral vectored vaccines, DNA plasmid vaccines, and emerging mRNA lipid nanoparticle vaccines.

The ecosystem integrates vaccine R&D centres, vaccine manufacturing companies, cold chain distributors, veterinary prescribers, production animal vaccination programs, and end users. Macroeconomic factors include increasing global demand for meat and dairy products, rising disposable incomes enabling higher spending on pet healthcare, and government initiatives to prevent livestock disease outbreaks.

Market Dynamics

To evaluate market opportunities, Request Sample

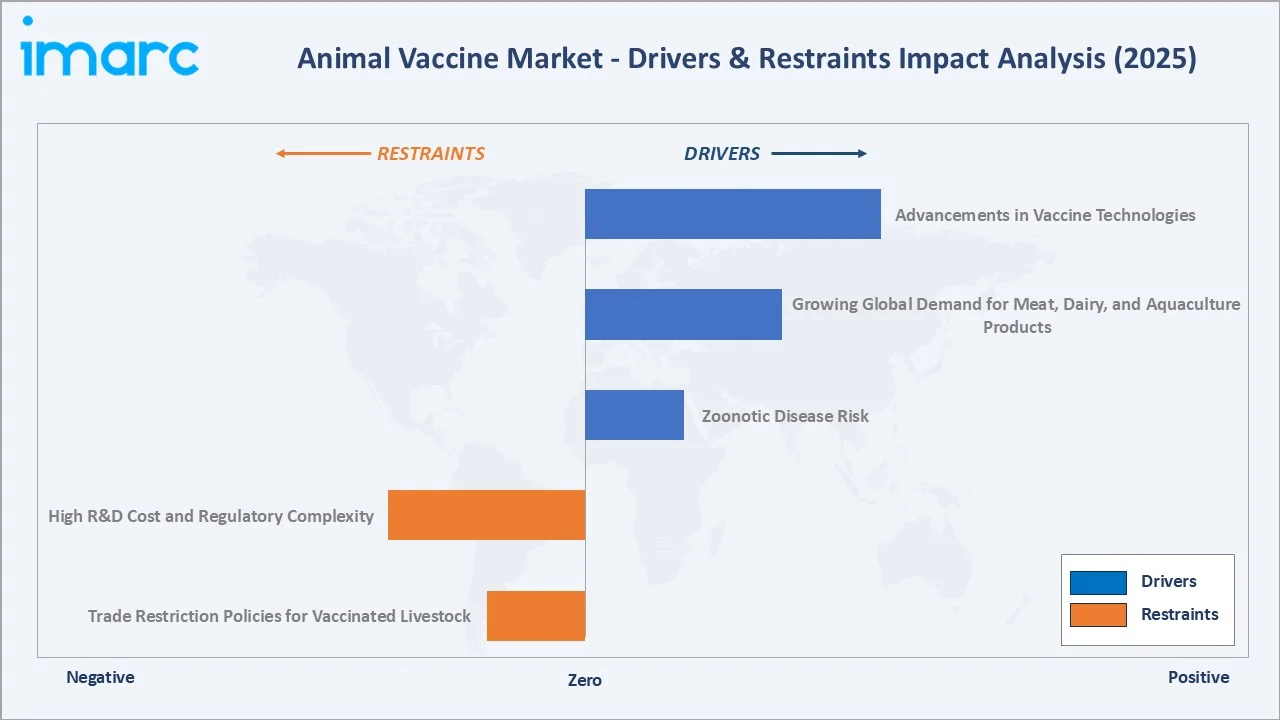

Market Drivers

- Zoonotic Disease Risk: Globally, zoonotic diseases are responsible for around one billion cases of illness and millions of deaths each year. Approximately 60% of newly reported infectious diseases originate from animals, and in the past three decades, over 30 new human pathogens have been identified, with 75% traced back to animal sources. The high prevalence and emerging threat of zoonotic diseases underscore the need for effective vaccination in animals to prevent transmission to humans. This risk boosts demand for livestock and companion animal vaccines, encourages investment in novel vaccine technologies, and strengthens global vaccination programs, thereby expanding the animal vaccines market.

- Growing Global Demand for Meat, Dairy, and Aquaculture Products: Growing global demand for meat, dairy, and aquaculture products is increasing the need to maintain healthy livestock and aquatic populations. Ensuring animal health reduces disease-related losses, improves productivity, and safeguards food supply, leading to higher adoption of vaccines and expansion of the market.

- Advancements in Vaccine Technologies: Advancements in vaccine technologies enable the development of safer, more effective, and species-specific vaccines. Innovations such as recombinant, DNA, RNA, and subunit vaccines allow for rapid response to emerging diseases, improved immune protection, and broader adoption in livestock and companion animals, fueling market growth. In June 2024, Merck Animal Health announced that the U.S. Department of Agriculture (USDA) approved NOBIVAC NXT Canine Flu H3N2, a next-generation vaccine designed to protect dogs from canine influenza. This innovative vaccine uses RNA-particle technology to generate a precise immune response, providing broad protection against multiple viral and bacterial pathogens in companion animals.

Market Restraints

- High R&D Cost and Regulatory Complexity: High R&D costs and regulatory complexity increase the time and investment required to develop new vaccines. Lengthy approval processes, stringent safety and efficacy requirements, and regional regulatory variations raise production costs, delay market entry, and limit the availability of innovative vaccines, thereby slowing overall market growth.

- Trade Restriction Policies for Vaccinated Livestock: Trade restriction policies for vaccinated livestock limit the export and movement of animals, even when vaccinated, due to regulatory or disease-free certification requirements. This creates barriers to market access, reduces incentive for vaccine adoption in certain regions, and adds economic uncertainty for producers, thereby slowing market growth.

Market Opportunities

- mRNA and Nucleic Acid Vaccine Platforms: mRNA and nucleic acid vaccine platforms enable rapid, precise, and customizable vaccine development for livestock and companion animals. These platforms allow faster responses to emerging diseases, improved immune protection, and the creation of next-generation vaccines, opening new avenues for innovation and market growth.

- Digital Health Integration: Digital health integration improves vaccination compliance, monitoring, and record-keeping through apps, reminders, and telemedicine solutions. This technology enhances pet owner engagement, streamlines veterinary workflows, and boosts preventive care adoption, creating new revenue streams and expanding market potential.

Market Challenges

- PRRS Virus Antigenic Evolution Requiring Continuous Vaccine Portfolio Updating: PRRS virus antigenic evolution necessitates frequent updates to vaccine formulations to maintain effectiveness. Continuous viral mutation increases R&D costs, complicates regulatory approval, and can reduce vaccine efficacy if strains are mismatched, creating hurdles for manufacturers and slowing market stability.

- Vaccine Safety and Efficacy Concerns: Vaccine safety and efficacy concerns reduce trust among veterinarians and animal owners, especially if adverse reactions occur or protective outcomes are inconsistent. Such concerns can limit vaccine adoption, slow market growth, and necessitate additional R&D and post-market monitoring to ensure reliable performance.

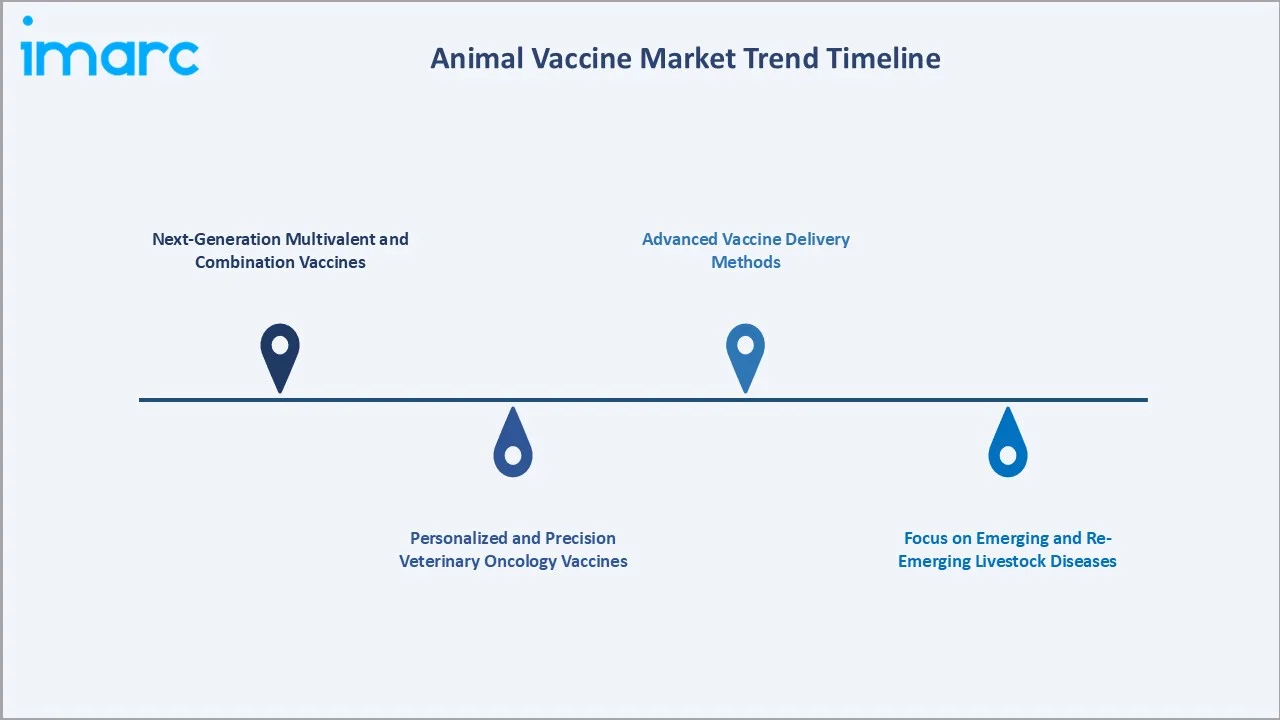

Emerging Market Trends

1. Next-Generation Multivalent and Combination Vaccines

Next-generation multivalent and combination vaccines allow protection against multiple pathogens in a single formulation, reducing the number of injections required. This innovation improves compliance, lowers vaccination costs, and enhances herd and companion animal health, while also enabling efficient disease management and streamlined veterinary practices, driving adoption and market growth.

2. Personalized and Precision Veterinary Oncology Vaccines

Personalized and precision veterinary oncology vaccines leverage genetic, molecular, and immune profiling to tailor cancer vaccines for individual animals. This approach allows for more effective and targeted immune responses, reduced side effects, and improved treatment outcomes, driving innovation in veterinary oncology and creating new growth opportunities in the animal vaccines market.

3. Focus on Emerging and Re-Emerging Livestock Diseases

Focus on emerging and re-emerging livestock diseases drives the development of vaccines targeting newly identified or resurging pathogens. This trend enhances preventive healthcare, reduces economic losses from outbreaks, and strengthens food security, while encouraging innovation in vaccine formulation, rapid response platforms, and expanded coverage for diverse livestock species, thereby boosting market growth.

4. Advanced Vaccine Delivery Methods

Advanced vaccine delivery methods introduce innovative administration routes such as oral, intranasal, and subcutaneous delivery, improving ease of use and animal compliance. These methods enhance immune response, reduce stress during vaccination, and allow mass immunization in livestock and aquaculture, supporting broader adoption and efficiency in preventive animal healthcare, thereby driving market growth.

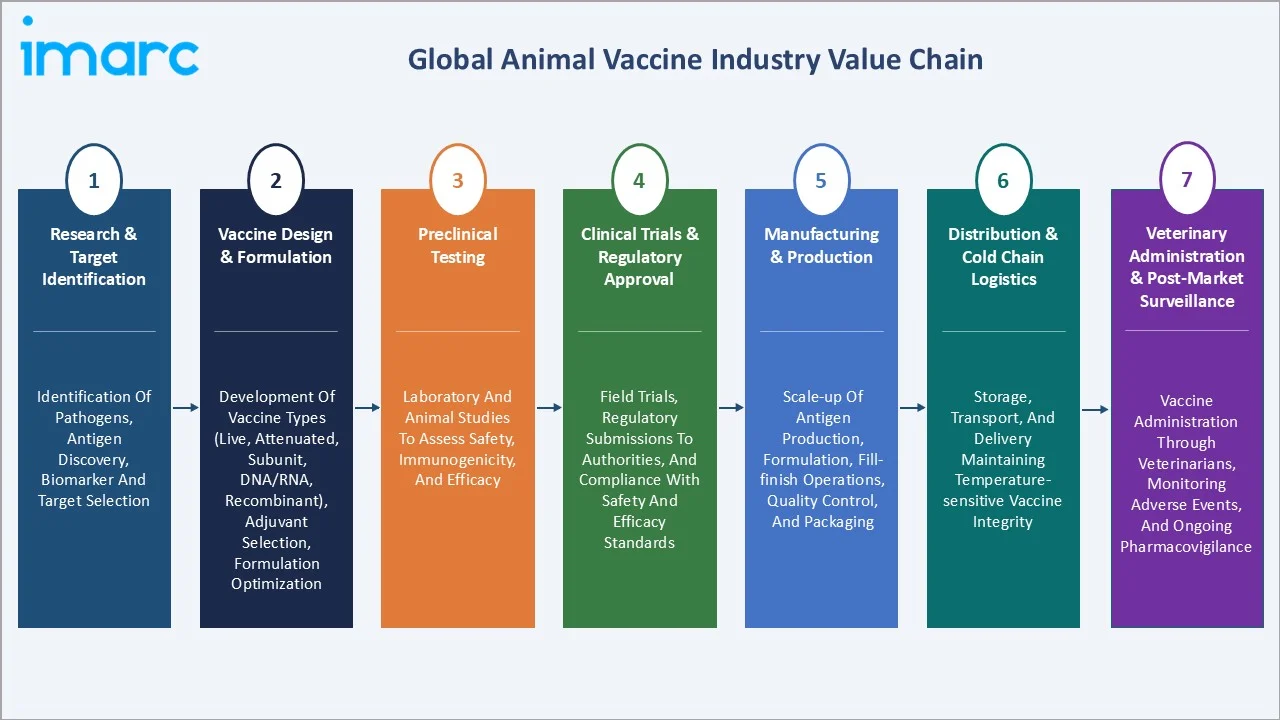

Industry Value Chain Analysis

The global animal vaccine value chain integrates research and target identification, vaccine design and formulation, preclinical testing, clinical trials and regulatory approval, manufacturing and production, cold chain distribution and logistics, and veterinary administration and post-market surveillance. The value chain's commercial structure is dominated by vertically integrated multinational animal health companies that perform most stages in-house, from antigen research through commercial manufacturing and field sales force deployment.

|

Stage |

Key Participants |

|

Research & Target Identification |

Identification of pathogens, antigen discovery, biomarker and target selection. |

|

Vaccine Design & Formulation |

Development of vaccine types (live, attenuated, subunit, DNA/RNA, recombinant), adjuvant selection, formulation optimization. |

|

Preclinical Testing |

Laboratory and animal studies to assess safety, immunogenicity, and efficacy. |

|

Clinical Trials & Regulatory Approval |

Field trials, regulatory submissions to authorities, and compliance with safety and efficacy standards. |

|

Manufacturing & Production |

Scale-up of antigen production, formulation, fill-finish operations, quality control, and packaging. |

|

Distribution & Cold Chain Logistics |

Storage, transport, and delivery maintaining temperature-sensitive vaccine integrity. |

|

Veterinary Administration & Post-Market Surveillance |

Vaccine administration through veterinarians, monitoring adverse events, and ongoing pharmacovigilance. |

The cold chain distribution tier remains the value chain's most operationally challenging segment in developing market contexts. Companion diagnostic integration is creating a diagnostics-vaccination commercial synergy analogous to companion diagnostic-drug pairing in human oncology.

Technology Landscape in the Animal Vaccine Industry

In Ovo Vaccination Technology for Poultry

In Ovo vaccination technology for poultry allows vaccines to be administered directly into eggs before hatching, ensuring early immunity in chicks. This method improves efficiency, reduces handling stress, and enables mass vaccination at scale, supporting high-throughput poultry operations, precise disease control, and enhanced productivity, thereby driving innovation in poultry vaccine delivery and preventive healthcare. In January 2026, Zoetis launched a comprehensive digital resource library to assist poultry producers in maximizing the effectiveness of their vaccine programs through proper handling and administration. Accessible at zoetisus.com/PoultryVaccination, the platform provides best-practice guidance for a variety of vaccination methods, including in Ovo, spray cabinet, field spray, drinking water, wing web, intramuscular, subcutaneous, and intraocular techniques. This support enhances the adoption of high-throughput vaccination techniques and improves operational efficiency in poultry production.

Self-Amplifying RNA (saRNA) and RNA-Particle Technologies

Self-Amplifying RNA (saRNA) and RNA-Particle Technologies enable highly efficient, targeted, and scalable immune responses in livestock and companion animals. These platforms allow for faster vaccine development, reduced antigen doses, and broader protection against multiple pathogens, while supporting next-generation vaccine innovation, rapid response to emerging diseases, and improved disease control strategies, thereby accelerating the adoption of advanced nucleic acid-based vaccines. In May 2026, the Committee for Veterinary Medicinal Products (CVMP) at the European Medicines Agency (EMA) recommended marketing authorization for Nobivac NXT HCPChFeLV, marking the first veterinary vaccine to use self-amplifying RNA (saRNA).

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

🔒 |

🔒 |

2025 |

|

Animal Type |

Livestock Animal |

64.7% |

2025 |

|

Route of Administration |

Subcutaneous |

45.2% |

2025 |

|

Region |

North America |

37.6% |

2025 |

By Animal Type

Livestock animals lead at 64.7% market share (2025). The livestock animals segment addresses large-scale preventive healthcare needs in cattle, poultry, and swine, which are critical for ensuring food security, protecting economic investments, and maintaining global meat, dairy, and egg production. High population density in livestock operations and the significant economic impact of disease outbreaks drive widespread vaccine adoption, making this segment the largest contributor to the market.

To access detailed market analysis, Request Sample

Companion animals at 35.3% grow fastest at ~6.7% CAGR. Companion animals are driving demand because rising pet ownership and the humanization of pets lead owners to prioritize preventive healthcare. This trend boosts vaccination rates, encourages adoption of advanced and specialized vaccines, and increases spending on pet wellness, thereby expanding the market for companion animal vaccines.

By Route of Administration

Subcutaneous leads at 45.2% market share (2025). The subcutaneous route allows precise, consistent delivery of vaccines beneath the skin, ensuring a strong and reliable immune response. This method minimizes stress and injury for animals, simplifies administration in large-scale livestock operations, and is compatible with a wide range of vaccine types, making it the preferred delivery route for both livestock and companion animals.

Intramuscular, at 31.8%, is widely used for both livestock and companion animals, especially for vaccines that require precise dosing or slower antigen release, supporting effective disease prevention and broad adoption across species. Intranasal at 14.6% grows fastest at ~7.4% CAGR through canine Bordetella kennel cough, bovine intranasal respiratory, and expanding needle-free poultry spray vaccination. Others at 8.4% encompasses oral in-feed and in-water poultry, in-Ovo poultry hatchery, and spray delivery routes.

Regional Market Insights

|

Region |

Share (2025) |

Key Animal Vaccine Market Drivers & Characteristics |

|

North America |

37.6% |

Dominates due to high livestock density, advanced animal healthcare infrastructure, strong preventive care programs, and high pet ownership, fostering innovation and early adoption of next-generation vaccines. |

|

Europe |

28.1% |

Driven by stringent regulatory standards, robust livestock and companion animal healthcare, and government-supported vaccination initiatives. |

|

Asia Pacific |

24.3% |

Fueled by the rapid expansion of livestock and aquaculture industries, increasing disposable incomes, and rising awareness of animal disease prevention. |

|

Latin America |

6.1% |

Supported by large-scale livestock production for export markets, increasing vaccination campaigns, and efforts to control endemic diseases. |

|

Middle East and Africa |

3.9% |

Driven by emerging livestock sectors, government disease control programs, and increasing focus on food security and animal health. |

North America, at 37.6%, is driven by its advanced veterinary infrastructure, high livestock and pet population density, strong adoption of preventive healthcare practices, and significant investment in innovative vaccine technologies, making it the largest and most influential market globally. Europe, at 28.1%, is driven by its robust livestock and companion animal healthcare systems, strict regulatory standards, and strong government-supported vaccination programs.

Asia Pacific, at 24.3%, is the fastest-growing region through livestock scale-up and comprehensive poultry vaccination programs. Latin America, at 6.1%, reflects Brazil and Argentina's mandatory export-compliance livestock vaccination programs and growing companion animal markets. MEA, at 3.9%, encompasses commercial livestock vaccination.

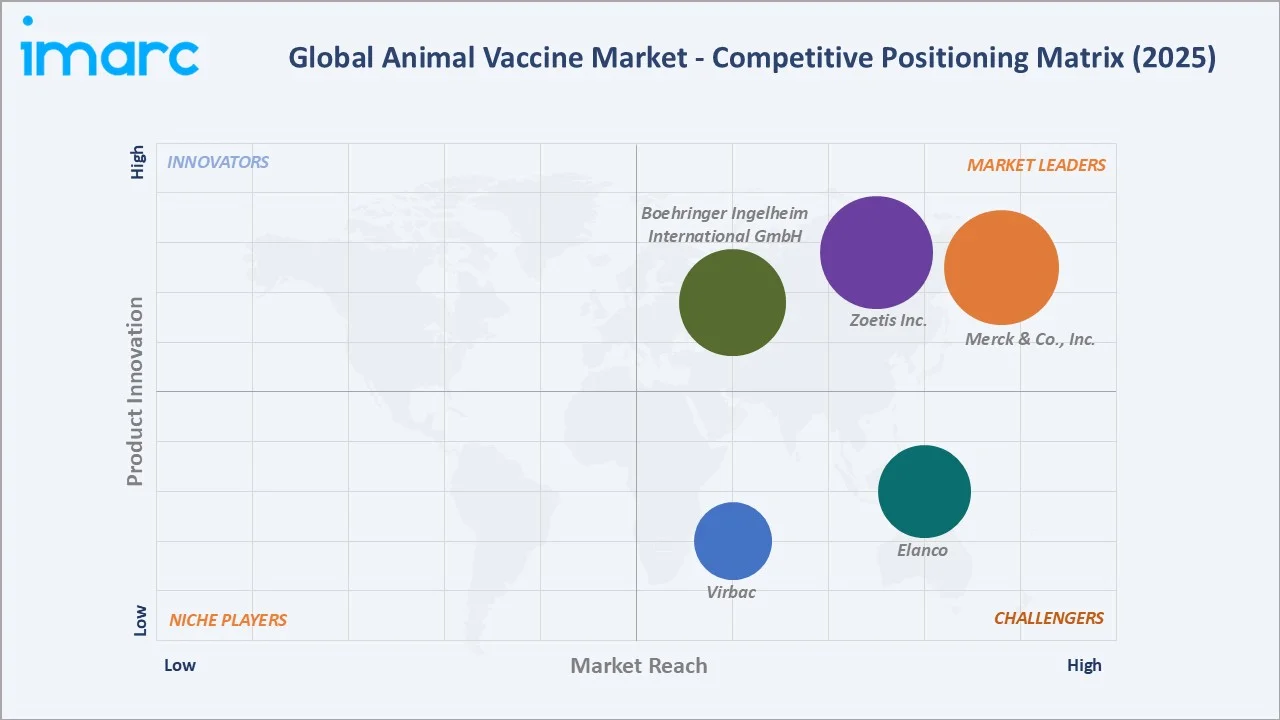

Competitive Landscape

The global animal vaccine competitive landscape is highly concentrated among four integrated multinationals, such as Zoetis Inc., Boehringer Ingelheim International GmbH, Merck & Co., Inc., and Elanco, collectively accounting for approximately 65-70% of global animal vaccine revenue. The competitive landscape is being reshaped by mRNA platform technology.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Merck & Co., Inc. |

Nobivac Tricat Trio, Nobivac Rabies, Nobivac DHPPi, Nobivac KC, Nobivac L4, INNOVAX-ND, Innovax-ND-IBD, Nobilis Coryza, Nobilis E. coli inac |

Market Leader |

Merck Animal Health is a global leader in the animal vaccines market, focusing on developing innovative vaccines for livestock and companion animals, contributing to disease prevention and food safety. |

|

Zoetis Inc. |

Poulvac E. coli, POULVAC ST, Bovi-Shield GOLD FP 5 L5, FluSure XP, Fluvac Innovator, Fostera Gold PCV MH, INFORCE 3 respiratory vaccine |

Market Leader |

Zoetis is the world's largest animal health company and a dominant leader in the global veterinary vaccines market. The company develops, manufactures, and markets products for both companion animals and livestock. |

|

Boehringer Ingelheim International GmbH |

Bovela, BULTAVO 3, Fencovis, INGELVAC CIRCOFLEX |

Market Leader |

Boehringer Ingelheim International GmbH specialize in developing innovative vaccines for both livestock and companion animals, utilizing advanced technologies to support food safety and enhance pet well-being. |

|

Elanco |

NUPLURA PH+, Titanium, Vira Shield, Master Guard, Scour Bos, Para Shield, Parvo Shield, Pili Shield, Prevacent PRRS |

Strong Challenger |

Elanco, specializing in innovative disease prevention for both livestock and pets, has a significant portfolio strengthened by the acquisition of Bayer Animal Health. |

|

Virbac |

CANIGEN DHP, CANIGEN DHPPi/L, RABIGEN Mono, FELIGEN CRP |

Strong Challenger |

Virbac focuses on developing and manufacturing vaccines for both companion and farm animals, with a strong emphasis on disease prevention, virology, and bacteriology. |

Companion animal vaccine competitive dynamics differ structurally from livestock; purchasing decisions are made by veterinary professionals at the point of care, creating prescription-level brand influence by manufacturer sales representatives and continuing education programs.

Key Company Profiles

Merck & Co., Inc.

Merck Animal Health is the animal health division of Merck & Co. Inc., which includes animal vaccines. Merck Animal Health's vaccine portfolio is strongest in companion animal and swine, creating diversified multi-species coverage, complementing its strong position.

- Key Products: Nobivac Tricat Trio, Nobivac Rabies, Nobivac DHPPi, Nobivac KC, Nobivac L4, INNOVAX-ND, Innovax-ND-IBD, Nobilis Coryza, Nobilis E. coli inac.

- Recent Developments: In February 2024, Merck Animal Health announced that the INNOVAX-ILT-IBD vaccine is commercially available as part of its poultry product line. The vaccine received USDA license approval in the United States in 2024.

- Strategic Focus: Innovating and expanding preventive and therapeutic vaccines to protect livestock and companion animals against emerging and endemic diseases.

Elanco

Elanco is one of the largest animal health companies, significantly expanded by the Bayer Animal Health acquisition. Elanco's animal vaccine portfolio was materially strengthened by Bayer's addition of companion animal vaccines.

- Key Products: NUPLURA PH+, Titanium, Vira Shield, Master Guard, Scour Bos, Para Shield, Parvo Shield, Pili Shield, Prevacent PRRS.

- Recent Developments: In May 2026, Elanco Animal Health Incorporated announced the phased launch of Befrena (tirnovetmab), a new anti-IL-31 monoclonal antibody injection designed to treat canine allergic and atopic dermatitis.

- Strategic Focus: Developing innovative and targeted vaccines to enhance livestock and companion animal health while addressing emerging infectious diseases.

Market Concentration Analysis

The global animal vaccine market is highly concentrated at the top, with Zoetis Inc., Boehringer Ingelheim International GmbH, Merck & Co., Inc., and Elanco together accounting for approximately 65-70% of total animal vaccine revenue, reflecting substantial manufacturing barriers, regulatory barriers, and commercial barriers. Concentration is declining at the margins as Virbac and others each hold globally significant positions in specific species or geographic niches that the top-4 multinationals do not equally dominate.

Regional concentration differs from global: the US companion animal vaccine market sees Zoetis Inc., Boehringer Ingelheim International GmbH, Merck & Co., Inc. holding approximately 85-90% market share through direct veterinary sales force dominance. The EU companion animal market is more balanced, reflecting Virbac's distribution strength. Asian livestock markets feature domestic manufacturers holding a disproportionate share through government procurement programs, favouring domestic manufacturing over multinational imports.

Investment & Growth Opportunities

Highest Growth Segments

Companion animals (~6.7% CAGR), intranasal route (~7.4% CAGR), aquaculture vaccines (~10-12% CAGR from growing base), non-core companion animal expansion (Lyme, leptospirosis L4, canine influenza ~10-12% CAGR), ASF vaccine new category (USD 2-4 Billion potential from near-zero), commercial poultry vaccination (USD 1-2 Billion potential if EU/US commercial approval), and mRNA veterinary vaccine platform (~20-25% CAGR from near-zero commercial base) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Veterinary vaccine digital health integration creates a USD 500 Million-1 Billion adjacent revenue opportunity, combining vaccine products with digital compliance platforms that improve companion animal vaccination adherence by 15-25% generates incremental vaccine revenue exceeding digital platform investment by 5-10x. Animal vaccine companies investing in digital clinic engagement platforms, bundling vaccine reminder automation with product purchasing loyalty, create competitive moats that pure-product competitors without equivalent practice management value cannot match.

Investment Themes

- ASF vaccine first-mover commercial advantage for the largest unmet need in global animal vaccinology: Commercial development of a safe, efficacious, broadly applicable ASF vaccine represents the most commercially valuable opportunity in animal vaccines.

- Aquaculture vaccine species expansion targeting shrimp WSSV as the largest single untapped animal vaccine opportunity: Global shrimp aquaculture has no commercially available vaccine despite decades of research, representing the largest blank canvas in animal vaccinology.

Future Market Outlook (2026-2034)

The global animal vaccine market is projected to grow from USD 15.33 Billion in 2025 to USD 27.09 Billion by 2034, delivering a 6.33% CAGR over the forecast period. The market's anchor value of USD 20.84 Billion in 2030 represents an animal vaccine industry at a decisive technology and regulatory inflection point. mRNA veterinary vaccines have achieved commercial scale beyond first conditional approvals, the commercial poultry vaccination policy question has been resolved through Phase III trial regulatory outcomes, and the livestock vaccination mandate has established the commercial infrastructure enabling private-sector animal vaccine market development above the government-funded baseline.

Three structural forces define animal vaccine market growth through 2034 with confidence. Disease burden and emergence of infectious pathogens, advancements in vaccine technologies such as mRNA, DNA, recombinant, and multivalent vaccines enable more effective and rapid immunization solutions, and regulatory and government support encourage adoption and expand market reach globally.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025) including Chief Scientific Officers; Regulatory Affairs Directors; Veterinary Biologics Licensing Officers; Global Medical Directors; Commercial poultry veterinarians; Companion animal veterinary oncologists; Emergency Prevention System coordinators; and patient advocacy representatives.

Secondary Research

Secondary research encompassed veterinary medicinal product authorisation database; World Animal Health 2024 global disease data; livestock population statistics; Pet Ownership Survey 2023; European Pet Food Industry Federation 2024 pet population data; veterinary medicine market data 2024; company annual reports; vaccination research reports; implementation reports 2024; veterinary biologics market data; IQVIA animal health market database. Over 65 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using a species-by-vaccine-category bottom-up model: (i) livestock vaccine revenue; (ii) companion animal vaccine revenue; (iii) aquaculture vaccine revenue. Market growth assumptions calibrated against investor guidance, companion animal veterinary spending data, India government procurement data, investor presentations, and historical animal health product sales.

Animal Vaccine Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Attenuated vaccines, Inactivated vaccines, Subunit vaccines, Toxoid vaccines, Conjugate vaccines, Recombinant vaccines, DNA vaccines |

| Animal Types Covered |

|

| Route of Administrations Covered | Subcutaneous, Intramuscular, Intranasal, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Merck & Co., Inc., Zoetis Inc., Boehringer Ingelheim International GmbH, Elanco, Virbac, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the animal vaccine market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global animal vaccine market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the animal vaccine industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Animal Vaccine Market Report

The global animal vaccine market reached USD 15.33 Billion in 2025, driven by livestock animal vaccines (64.7%) across poultry, swine, cattle, and aquaculture species, combined with growing companion animal vaccines (35.3%) through pet humanisation and digital health platform compliance improvement.

The market grows at 6.33% CAGR during 2026-2034, reaching USD 27.09 Billion by 2034. Growth is driven by companion animal vaccine premiumisation and non-core expansion, HPAI and ASF livestock emergency and commercial vaccine programs.

Livestock animals lead at 64.7% as it addresses large-scale preventive healthcare needs in cattle, poultry, and swine, which are critical for food security, economic stability, and global protein production.

Subcutaneous leads at 45.2% as it provides reliable and consistent immune responses, is easy to administer across large populations, and minimizes stress and injury to both livestock and companion animals, making it the preferred delivery route for vaccines.

North America leads at 37.6% due to its advanced veterinary infrastructure, high livestock and pet populations, strong adoption of preventive healthcare, and significant investment in innovative vaccine technologies, making it the largest and most influential regional market globally.

Leading companies include Merck & Co., Inc., Zoetis Inc., Boehringer Ingelheim International GmbH, Elanco, and Virbac, among others.

The market is projected to reach approximately USD 20.84 Billion by 2030, with mRNA veterinary vaccines achieving commercial scale across canine influenza and cattle respiratory viruses, ASF conditional commercial launch in at least one major market, and European companion animal non-core vaccine penetration growth.

Pet humanisation, treating companion animals as family members with comparable healthcare entitlement, structurally transforms companion animal vaccine markets from core-only commodity vaccination toward comprehensive preventive health programmes, including non-core vaccines generating 40-80% higher revenue per dose than core vaccines.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)