Anti-Drone Market Report by Type (Detection Systems, and Detection & Disruption Systems), Mitigation Type (Destructive System and Non-Destructive System), Deployment (Ground-based, Handheld, and UAV based), Technology (Anti-Drone Radar, RF Scan, Thermal Image and Others), End Use (Commercial, Military & Defense, and Homeland Security), Region and Competitive Landscape (Market Share, Business Overview, Products Offered, Business Strategies, SWOT Analysis and Major News and Events) 2026-2034

Anti-Drone Market Size:

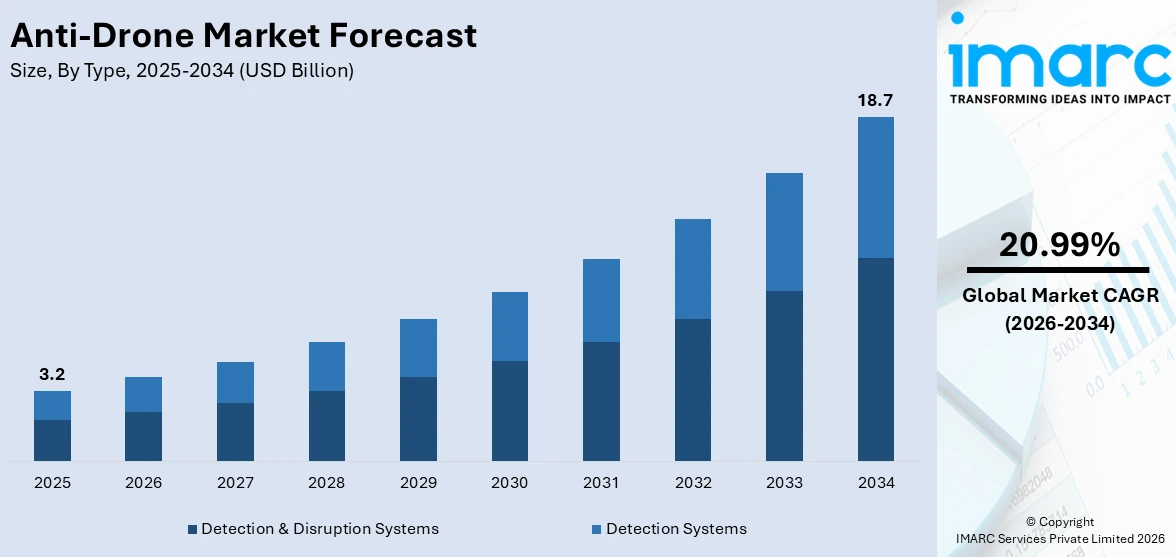

The global anti-drone market size reached USD 3.2 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 18.7 Billion by 2034, exhibiting a growth rate (CAGR) of 20.99% during 2026-2034. Increasing security concerns, advancements in drone technology, rising incidents of unauthorized drone usage, regulatory measures, the need to protect critical infrastructure, and the growing adoption of counter-drone systems are some of the factors propelling the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 3.2 Billion |

|

Market Forecast in 2034

|

USD 18.7 Billion |

| Market Growth Rate 2026-2034 | 20.99% |

Anti-Drone Market Analysis:

- Major Market Drivers: Rising concerns over privacy and security breaches due to unauthorized drone activities are propelling the demand for anti-drone solutions.

- Key Market Trends: Collaborations between government agencies, defense organizations, and private sector companies to develop anti-drone strategies and solutions are gaining traction, driving innovation and market growth.

- Geographical Trends: North America dominates the market due to the presence of stringent regulations, high adoption of advanced technologies, and increasing investments in security infrastructure.

- Competitive Landscape: Some of the major market players in the Anti-Drone industry include Blighter Surveillance Systems Ltd, Cerberus, Skyborne Technologies Pty. Ltd., Dedrone, AI (Israel Aerospace Industries) (Israel), L3Harris Technologies, among many others.

- Challenges and Opportunities: Challenges include the complexity of identifying and mitigating drone threats in urban environments and the risk of collateral damage from anti-drone measures.

To get more information on this market Request Sample

Anti-Drone Market Drivers:

Growing Security Threats

The escalating prevalence of security challenges due to drones has significantly influenced the market. These unmanned aerial vehicles are commonly employed in unlawful endeavors, including contraband smuggling, unauthorized surveillance of protected zones, and executing hostile acts. The surge in such unauthorized drone activities necessitates enhanced solutions for their detection, monitoring, and neutralization. Various sectors, such as defense, law enforcement, critical infrastructure, event coordination, and private businesses, are intensively investing in anti-drone systems to counter the threats associated with unapproved drone entries.

Rising Adoption of Drones

The factor of rising concerns over privacy and security breaches due to unauthorized drone activities is a major driver propelling the growth of the market. As drones become more accessible and capable, the potential for misuse and intrusion into sensitive areas such as government facilities, critical infrastructure, and private properties has heightened. Due to this, there is an increasing demand for effective counter-drone solutions. The number of security incidents involving unauthorized drones has been escalating over the years. For instance, the UK Airprox Board reported over 120 near-miss incidents between drones and aircraft in 2018, highlighting the growing threat to aviation safety. Drones are also extensively used in the agriculture industry for precision spraying. Drones, through precise targeting of pest infestations, can decrease pesticide usage by as much as 90%, thereby minimizing environmental harm and safeguarding beneficial insects.

Increase in Defense Spending

The notable rise in defense spending has profound implications, shaping geopolitical landscapes and fueling advancements in military technology. With nations prioritizing security concerns, heightened defense budgets signify a concerted effort to bolster military capabilities, modernize equipment, and fortify national defense infrastructures. This increase in investment not only fosters innovation within the defense industry but also stimulates economic growth by generating employment opportunities and driving technological advancements with civilian applications. However, it also raises concerns regarding global arms races and potential escalations of conflicts. As defense spending continues to rise, it underscores the evolving geopolitical dynamics and the imperative of maintaining strategic balance in international relations. The U.S. State Department has also granted approval for a drone sale to India worth nearly $4 billion. On the other hand, under the Innovations for Defence Excellence (iDEX) initiative, the Ministry of Defence has awarded a ₹200 crore contract for anti-drone systems to Big Bang Boom Solutions Private Limited (BBBS) for the Indian Army and Indian Air Force (IAF). BBBS stated that this contract is the largest ever signed by the MoD under the iDEX initiative.

Government and Regulatory requirements

Government and regulatory requirements exert a significant influence on various industries, particularly in sectors like aviation and technology. Compliance with these mandates is imperative for companies to operate legally and ensure safety, security, and ethical standards. The stringent regulations often necessitate substantial investments in research, development, and compliance measures, shaping the landscape of innovation and competition within the industry. For example, the global financial sector spends billions annually on compliance costs, with larger banks sometimes spending over $1 billion a year. Moreover, evolving regulations in response to emerging technologies and security threats demand continuous adaptation from businesses, presenting both challenges and opportunities. Companies that effectively navigate the regulatory landscape can gain a competitive edge, while non-compliance risks penalties, reputational damage, and even legal repercussions. Thus, understanding and adhering to government and regulatory requirements are pivotal factors shaping the strategies and operations of businesses across various sectors.

Risk of Unauthorized Drone Activities

The risk of unauthorized drone activities poses a challenge across diverse sectors. Rogue drones can be exploited for malicious purposes such as surveillance, smuggling, or even carrying out targeted attacks, causing security threats. These activities compromise sensitive information and also disrupt operations, endanger public safety, and undermine regulatory compliance. Moreover, the proliferation of drones worsens the difficulty of monitoring and controlling airspace, necessitating robust countermeasures to detect, track, and mitigate unauthorized drone incursions effectively. As such, mitigating the risk of unauthorized drone activities requires a comprehensive approach, including regulatory frameworks, technological solutions, and public awareness campaigns to safeguard against potential threats and ensure the safe integration of drones into society.

Anti-Drone Market Opportunities:

Innovation in Technology

The drive for innovation in technology is propelling market growth by addressing the challenge of collateral damage. Advanced technologies such as AI-driven detection systems, precision-guided countermeasures, and non-kinetic methods are being developed to neutralize rogue drones with minimal risk of unintended harm to surrounding assets or individuals. These innovations enhance the effectiveness and reliability of anti-drone solutions, bolstering their appeal to a wider range of customers across various sectors. As the demand for safer and more precise anti-drone technologies continues to rise, the market is witnessing accelerated growth driven by ongoing advancements in technology aimed at mitigating the risk of collateral damage and ensuring the safe integration of drones into airspace. Aligned with Prime Minister Narendra Modi’s goal to position India as a global drone hub by 2030, the initiative to pursue drone pilot training promises promising career prospects in drone technology. During the inauguration of "Drone Yatra 2.0" in Chennai last year, Union Information and Broadcasting Minister Anurag Singh Thakur underscored the necessity for a minimum of 100,000 pilots by 2023, envisioning an annual employment worth ₹6,000 crores in the burgeoning drone sector.

Partnership and Collaboration of Players

The collaboration and partnership among various players are driving the growth of the market. By joining forces, companies can use each other's strengths and resources to develop the best anti-drone solutions that address threats effectively. Strategic alliances between technology providers, defense contractors, and regulatory authorities facilitate the integration of advanced capabilities and regulatory compliance. Additionally, partnerships enable broader market reach, accelerating the adoption of anti-drone technologies across different sectors and geographical regions. As collaboration becomes increasingly prevalent in the industry, it fosters innovation and drives market competitiveness. ACL Digital, a subsidiary of the ALTEN group, has entered into a groundbreaking partnership with PhoenixAI.tech, a provider of advanced drone technology solutions. Having a workforce of 57,100+ spread across more than 30+ countries, this collaboration aims to redefine AI-powered drone solutions and services.

Market Development in Emerging Regions

Market development in emerging regions is driving the expansion of the market. As countries in Asia, Latin America, and Africa experience rapid urbanization and industrialization, the demand for anti-drone solutions is increasing to reduce security threats and protect critical infrastructure. Government initiatives aimed at improving national security and regulatory frameworks to manage drone proliferation further stimulate market growth in these regions. Moreover, the adoption of anti-drone technologies in emerging economies presents opportunities for market players to establish a foothold and capitalize on untapped market potential.

Investment in Security

Investment in security is a driving force behind the growth of the market. As security concerns rise, governments, businesses, and critical infrastructure operators are allocating resources to protect against unauthorized drone activities. This investment includes the deployment of advanced anti-drone systems capable of detecting, tracking, and neutralizing rogue drones effectively. Additionally, companies are investing in research and development to innovate new technologies and enhance existing solutions to combat evolving drone threats. The increasing recognition of the importance of safeguarding airspace from malicious drone incursions is driving investment in anti-drone security measures, propelling the growth of the market. Safety and security drones offer numerous benefits, including extended drone range and high-resolution sensors tailored for specialized tasks.

Key Technological Trends & Development:

Machine Learning and Artificial Intelligence (AI) Powered

Machine learning and artificial intelligence (AI) are important in driving advancements within the anti-drone market. AI-powered systems enable real-time analysis of drone behavior patterns, improving detection accuracy and reducing false alarms. Machine learning algorithms continuously refine detection capabilities by learning from past incidents, ensuring adaptability to evolving threats. Additionally, AI-driven countermeasures enable swift and precise neutralization of rogue drones. Integrating machine learning and AI into anti-drone solutions improves their effectiveness in complex environments. A robotics company, named Grene Robotics, headquartered in Hyderabad has introduced a cutting-edge autonomous anti-drone system, using artificial intelligence technology. This system offers protection for critical infrastructures such as nuclear facilities and oil rigs, as well as expansive coverage, capable of protecting entire cities from various types of drones with its 360-degree protection. Notably, this marks the debut of such an innovative system developed within India.

Advanced RF Technologies

Advanced radio frequency (RF) technologies are driving significant advancements in the anti-drone market. By using sophisticated RF sensors and communication systems, anti-drone solutions can detect, track, and neutralize unauthorized drones with precision and efficiency. These technologies enable the detection of drones across multiple frequency bands, including Wi-Fi, Bluetooth, and cellular signals. Moreover, advancements in RF signal processing algorithms and machine learning enable real-time analysis of drone behavior patterns, improving detection accuracy and reducing false positives. As security concerns rise, the demand for advanced RF-based anti-drone solutions continues to rise, positioning RF technologies as key drivers in shaping the future of drone defense strategies. The Special Operations Forces Acquisitions, Technology, and Logistics (SOF AT&L) office has awarded PDW a $6.9 million contract. This contract entails the delivery of Blackwave, PDW’s radio system specifically designed to guarantee dependable drone operation in environments characterized by radio frequency (RF) interference and erratic GPS signals.

Hybrid Anti-Drone Technology

Hybrid anti-drone technology refers to the integration of multiple complementary methods and systems to improve the effectiveness of counter-drone measures. This approach combines various technologies such as radar, radio frequency (RF) detection, electro-optical sensors, acoustic sensors, and jamming or interception systems. By combining different techniques, hybrid anti-drone solutions offer improved detection rates, increased coverage, and enhanced mitigation capabilities against a wide range of drone threats. This integrated approach allows for greater adaptability to different environments and scenarios, ensuring comprehensive protection for critical infrastructure, events, and public spaces. Hybrid anti-drone technology represents an excellent strategy to address the challenges posed by unauthorized drone activities, offering a robust defense solution against emerging threats in today's airspace landscape. In response to swarm drone attacks, an Indian Army officer and a jawan have collaboratively developed an integrated anti-drone system. This innovative solution that took an approx. of 8-10 months to develop combines an indigenous jammer with an upgraded Russian-origin Schilka Weapon System to effectively counter swarm drone threats. The hybrid anti-drone system provides a comprehensive defense mechanism against swarm drone attacks.

Multiple Surveillance Technologies

Multiple surveillance technologies encompass the usage of diverse sensor systems and monitoring methods to enhance situational awareness and security measures. This approach integrates various surveillance techniques such as video surveillance, radar systems, thermal imaging, LiDAR (Light Detection and Ranging), and acoustic sensors. By employing a combination of these technologies, organizations can achieve comprehensive coverage and detection capabilities across different environments and scenarios. This multi-faceted approach enables more effective monitoring of critical infrastructure, borders, public spaces, and other sensitive areas, providing early detection and response to potential threats. The integration of multiple surveillance technologies enhances security measures, offering a layered defense strategy to mitigate risks and ensure the safety of assets, personnel, and the public. Zhejiang University has developed an advanced anti-drone system named ADS-ZJU. This innovative system combines 3 different types of passive surveillance devices, including audio, video, and radio frequency, which can localize as well as detect intruding UAVs within 100 m area while integrating multiple passive surveillance technologies to achieve drone detection, localization, and radio frequency jamming capabilities. By combining these technologies, ADS-ZJU provides comprehensive protection against unauthorized drone activities.

Anti-Drone Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on type, mitigation type, deployment, technology, and end use.

Breakup by Type:

- Detection Systems

- Detection & Disruption Systems

Detection & disruption systems account for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the type. This includes detection systems and detection & disruption systems. According to the report, detection & disruption systems represented the largest segment.

Detection and disruption systems help to combat the rising threat of rogue drones. Detection technologies, such as radar and optical sensors, pinpoint unauthorized drones in the airspace. These systems use various methods like jamming signals, directed energy, or net cannons to neutralize these intruders swiftly and effectively. Their integration into security frameworks bolsters protection against potential threats posed by drones, whether in sensitive areas like airports, stadiums, or critical infrastructure sites. As the drone industry expands, so does the need for advanced countermeasures. Detection and disruption systems remain important in ensuring airspace safety and security, propelling innovation and investment in the anti-drone market. By 2020, the United States had registered more than 1.7 million drones. During the same year, China dominated the global drone production market, contributing to 79.8% of the total output.

Breakup by Mitigation Type:

- Destructive System

- Non-Destructive System

Destructive system hold the largest share in the industry

A detailed breakup and analysis of the market based on the mitigation type have also been provided in the report. This includes destructive and non-destructive system. According to the report, destructive system accounted for the largest market share.

Among the array of countermeasures, destructive systems claim the largest share in the industry. These systems, ranging from jamming signals to directed energy weapons, are crucial in neutralizing rogue drones swiftly and effectively. Their prominence underscores the urgent need for robust defense mechanisms against potential threats posed by drones. As the drone industry continues to expand, the demand for advanced anti-drone technologies, particularly destructive systems, remains high, driving innovation and investment in this rapidly evolving sector. As of October 2022, the United States had approximately 865,505 registered drones.

Breakup by Deployment:

- Ground-based

- Handheld

- UAV based

Ground-based hold the largest share in the industry

A detailed breakup and analysis of the market based on the deployment have also been provided in the report. This includes ground-based, handheld, and UAV based. According to the report, ground-based accounted for the largest market share.

Ground-based systems claim the largest share in the anti-drone industry. These systems, anchored on terrestrial infrastructure, include various technologies like radar, radio frequency scanners, and optical sensors to detect and counter unauthorized drones effectively. Ground-based solutions provide versatility and scalability. This makes them indispensable for protecting critical infrastructure, public events, and sensitive areas. Their prominence underscores the significance of terrestrial defenses in mitigating the evolving threats posed by drones. As the demand for anti-drone solutions continues to rise, ground-based systems remain at the forefront, driving innovation and investment in the industry to ensure robust protection against aerial intruders. As per 6Wresearch, the Indian UAV market is set to expand at a CAGR of 18% from 2017 to 2023 in revenue terms. While long-range UAVs will continue to dominate, medium and mini-UAVs are expected to experience significant growth as well.

Breakup by Technology:

- Anti-Drone Radar

- RF Scan

- Thermal Image

- Others

Anti-drone radar holds the largest share in the industry

A detailed breakup and analysis of the market based on the technology have also been provided in the report. This includes anti-drone radar, RF scan, thermal image, and others. According to the report, anti-drone radar accounted for the largest market share.

Anti-drone radar systems command the largest share in the industry. These systems detect and track unauthorized drones with precision, providing crucial situational awareness for effective countermeasures. They also employ advanced radar technology. Their widespread adoption shows their effectiveness in safeguarding critical infrastructure, public spaces, and events from potential threats posed by drones. With the increasing popularity of drones, the demand for anti-drone radar systems is expected to remain robust, driving innovation and investment in the sector. As a cornerstone of drone defense strategies, anti-drone radar systems play an important role in ensuring airspace security and mitigating the risks associated with unauthorized drone activities. The Defence Research and Development Organisation has tasked Bharat Electronics Limited (BEL), Larsen & Toubro, and the Adani Group with developing anti-drone technology.

Breakup by End Use:

Access the comprehensive market breakdown Request Sample

- Military & Defense

- Commercial

- Homeland Security

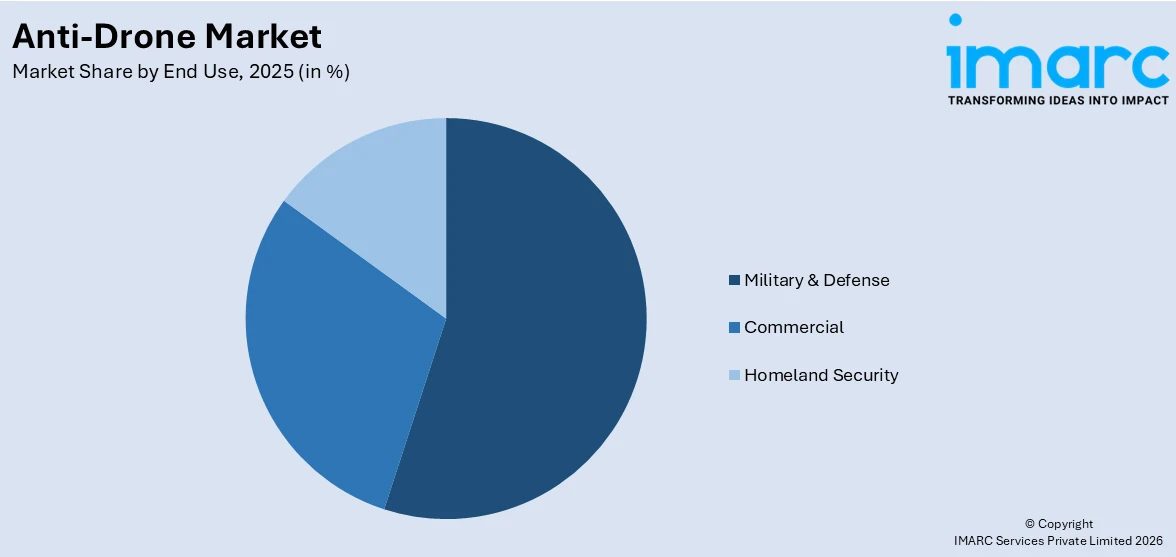

Military & defense hold the largest share in the industry

A detailed breakup and analysis of the market based on the end use have also been provided in the report. This includes military & defense, commercial, and homeland security. According to the report, military & defense accounted for the largest market share.

Military and defense sectors dominate the industry, holding the largest share in anti-drone technology. With growing concerns over security threats posed by drones, governments worldwide prioritize investments in defense capabilities. Military entities heavily rely on advanced anti-drone systems to protect strategic assets, troops, and infrastructure from aerial threats. These systems encompass a wide range of technologies, including radar, jamming, and directed energy weapons, tailored to counter diverse drone threats effectively. As the need for robust defense against drones continues to escalate, the military and defense sectors remain at the forefront, driving innovation and shaping the evolution of anti-drone technology. Statistics from the Stockholm International Peace Research Institute (SIPRI) reveal that India leads the global UAV import rankings with 22.5%. Primarily for military use, these figures indicate India's significant reliance on drone imports. Additionally, commercial drone imports are experiencing substantial growth, reflecting diverse applications beyond military contexts.

Breakup by Region:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East

- Africa

North America leads the market, accounting for the largest anti-drone market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Latin America (Brazil, Mexico, and others); the Middle East; and Africa. According to the report, North America accounted for the largest market share.

North America emerges as the dominant force in the anti-drone market, boasting the largest market share. The anti-drone market in North America is segmented into the USA and Canada. In 2017, the US military expenditure reached approximately $810 billion, compared to $760 billion in 2016. With robust technological advancements and a proactive approach toward security, the region leads in the development and deployment of anti-drone solutions. Key players in North America continually innovate to address evolving threats posed by drones, driving the market growth. The region's expansive defense infrastructure, coupled with increasing investments in counter-drone technology, solidifies its leadership position. As drone-related incidents continue to rise globally, North America remains at the forefront, shaping the landscape of anti-drone solutions and safeguarding critical assets against airborne threats.

Analysis Covered Across Each Country:

- Historical, current, and future market performance

- Historical, current, and future performance of the market based on product and end-user

- Competitive landscape

- Government regulations

Leading Key Players in the Anti-Drone Industry:

Key players in the market are driving innovation and market growth through strategic partnerships, investments in research and development, and the development of advanced technologies. They are using expertise and resources to develop comprehensive anti-drone solutions and collaborating with industry stakeholders, government agencies, and research institutions. Additionally, they actively engage in regulatory advocacy to establish clear guidelines, fostering trust and facilitating wider adoption of anti-drone solutions. By continuously advancing their offerings and advocating for responsible usage, key players not only expand their market presence but also ensure the safety and security of airspace environments globally, shaping the future of drone defense strategies.

The market research report has provided a comprehensive analysis of the competitive landscape covering market structure, market share by key players, market player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant, among others. Detailed profiles of all major companies have also been provided. This includes business overview, product offerings, business strategies, SWOT analysis, financials, and major news and events. Some of the key players in the market include:

- Blighter Surveillance Systems Ltd

- Cerberus, Skyborne Technologies Pty. Ltd.

- Dedrone

- IAI (Israel Aerospace Industries) (Israel).

- L3Harris Technologies

- Leonardo S.p.A.

- Rafael Advanced Defense Systems (Israel)

- Rohde & Schwarz

- RTX, Raytheon

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Analysis Covered for Each Player:

- Market Share

- Business Overview

- Products Offered

- Business Strategies

- SWOT Analysis

- Major News and Events

Latest News:

- February 15, 2024: The UK Government has declared that a coalition led jointly by the UK and Latvia will be established to provide significant drone capabilities to Ukraine. This initiative will involve supplying thousands of drones, including first-person view (FPV) drones, which have shown high effectiveness in combat situations.

- November 20, 2023: Montgomery County Office of Homeland Security and Emergency Management (MCOHSEM) announced the deployment of DroneShield's DroneSentry System for the IRONMAN Triathlon Championships 2023 in Woodlands, Texas for the second year in a row.

- December 28, 2023: To address the increasing threat of loitering munitions, the U.S. Army aims to procure 6,000 Coyote Block II anti-drone interceptors, along with potentially acquiring 700 Block III variants equipped with non-kinetic payloads. Additionally, the service branch plans to purchase hundreds of launchers and radar systems.

Anti-Drone Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Detection Systems, Detection & Disruption Systems |

| Mitigation Types Covered | Destructive System, Non-Destructive System |

| Deployments Covered | Ground-based, Handheld, UAV based |

| Technologies Covered | Anti-Drone Radar, RF Scan, Thermal Image, Others |

| End Uses Covered | Military & Defense, Commercial, Homeland Security |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East, Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Blighter Surveillance Systems Ltd, Cerberus, Skyborne Technologies Pty. Ltd., Dedrone, IAI (Israel Aerospace Industries) (Israel)., L3Harris Technologies, Leonardo S.p.A., Rafael Advanced Defense Systems (Israel), Rohde & Schwarz, RTX, Raytheon, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global anti-drone market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global anti-drone market?

- What is the impact of each driver, restraint, and opportunity on the global anti-drone market?

- What are the key regional markets?

- Which countries represent the most attractive anti-drone market?

- What is the breakup of the market based on the type?

- Which is the most attractive type in the anti-drone market?

- What is the breakup of the market based on the mitigation type?

- Which is the most attractive mitigation type in the anti-drone market?

- What is the breakup of the market based on the deployment?

- Which is the most attractive deployment in the anti-drone market?

- What is the breakup of the market based on technology?

- Which is the most attractive technology in the anti-drone market?

- What is the breakup of the market based on the end use?

- Which is the most attractive end use in the anti-drone market?

- What is the competitive structure of the market?

- Who are the key players/companies in the global anti-drone market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the anti-drone market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global anti-drone market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the anti-drone industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)