Anti-venom Market Size, Share, Trends and Forecast by Species, Anti-Venom Type, Mode of Action, End User, and Region, 2026-2034

Anti-venom Market Size, Share, Trends & Forecast (2026-2034)

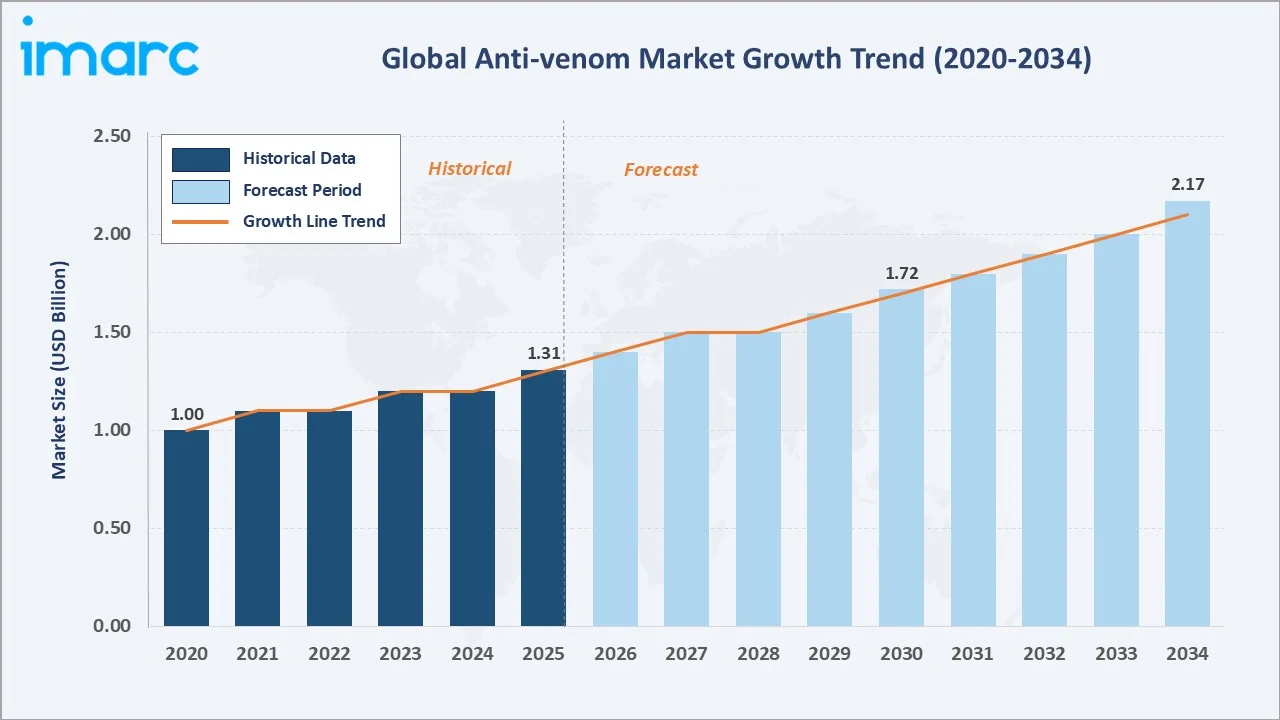

The global anti-venom market reached USD 1.31 Billion in 2025 and is projected to reach USD 2.17 Billion by 2034, growing at a CAGR of 5.57% during 2026-2034. Rising global incidence rates of snakebites and venomous stings, WHO-led envenomation control initiatives, accelerating biotechnology advances in anti-venom production, and expanding healthcare infrastructure in endemic tropical and subtropical regions are the key anti-venom market growth drivers propelling the market forward.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.31 Billion |

|

Forecast Market Size (2034) |

USD 2.17 Billion |

|

CAGR (2026-2034) |

5.57% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

The anti-venom market is expanding globally due to the high prevalence of snakebites, scorpion stings, and other venomous animal encounters, particularly in tropical and rural regions. Anti-venoms, developed from immunized animal plasma or recombinant technologies, are critical for neutralizing venom and reducing morbidity and mortality.

To get more information on this market, Request Sample

The global anti-venom market is underpinned by the persistent global burden of envenomation, which the WHO classifies as a neglected tropical disease affecting 1.8 to 2.7 million people annually. The convergence of increased government-funded procurement programs, technological advances enabling more effective and safer anti-venom formulations, and expanding cold-chain logistics in previously underserved endemic regions collectively sustain above-average growth through the forecast horizon.

Executive Summary

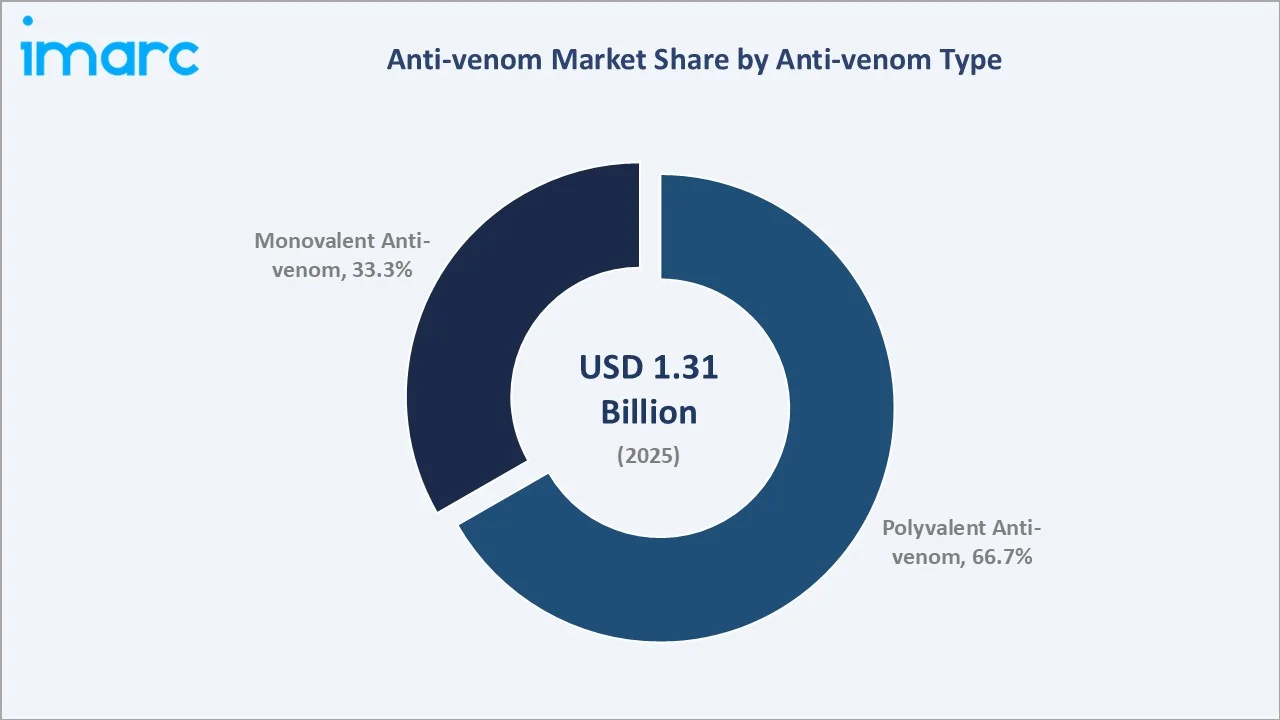

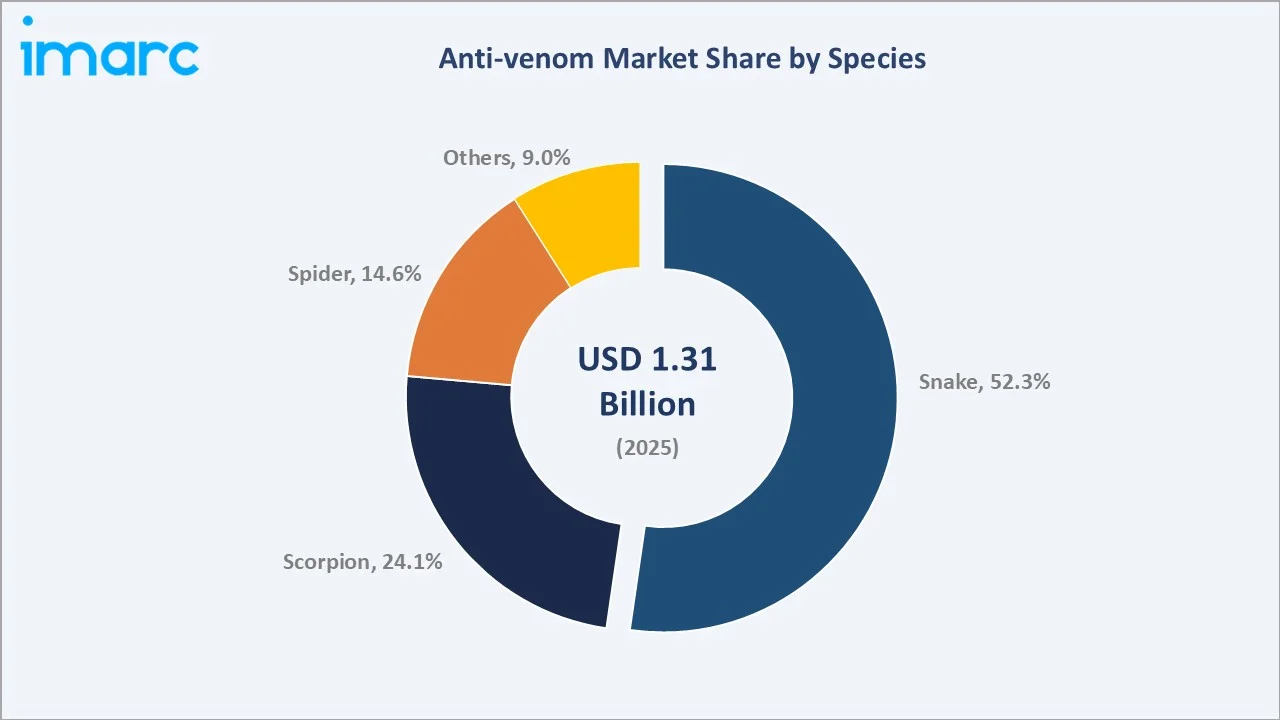

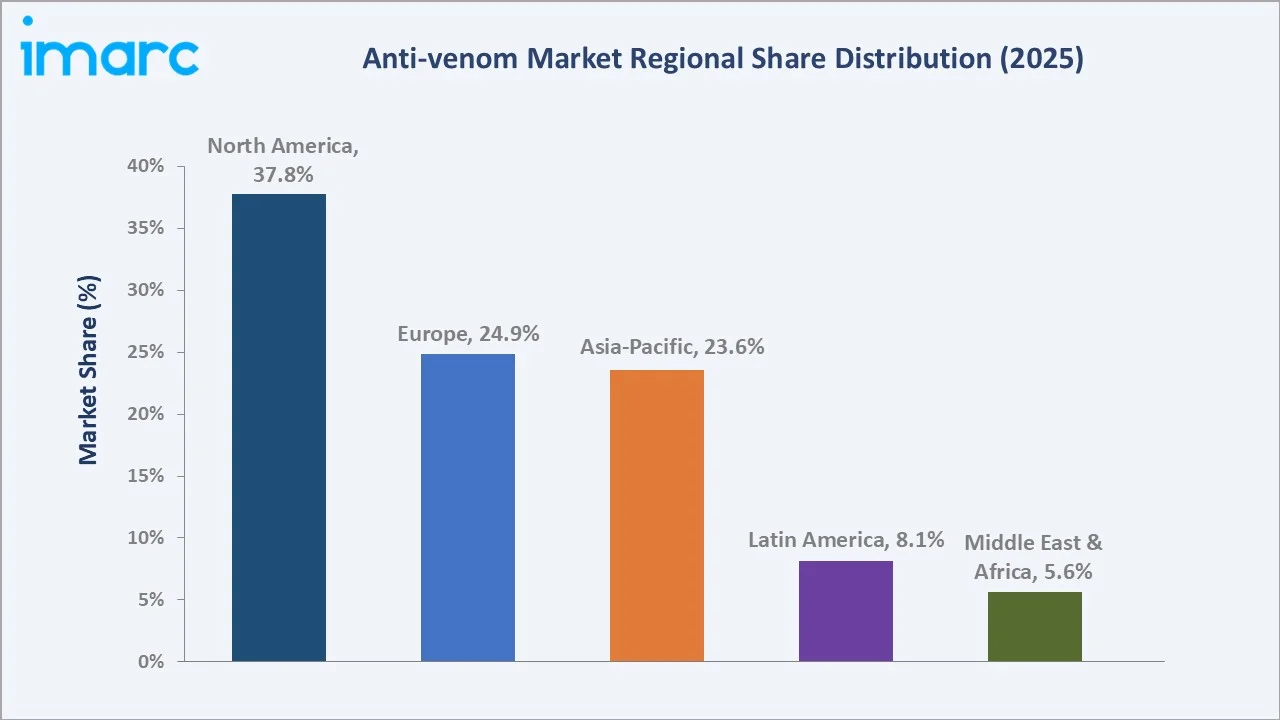

The global anti-venom market was valued at USD 1.31 Billion in 2025 and is forecast to reach USD 2.17 Billion by 2034 at a CAGR of 5.57%. Polyvalent anti-venom dominates with a 66.7% share in 2025, while snake species represent 52.3% of the species breakdown. North America leads regionally at 37.8%, supported by robust emergency care infrastructure and FDA-approved formulations.

WHO's target of halving deaths by 2030 and disability from snakebites, combined with rising biotechnology investment in recombinant and monoclonal antibody-based anti-venoms, defines the anti-venom market outlook through the forecast period. Moreover, rising awareness, government initiatives, and advancements in safer and broad-spectrum formulations are driving growth and innovation in this life-saving segment of the pharmaceutical market.

Key Market Insights

|

Insight |

Data |

|

Largest Anti-venom Type Segment |

Polyvalent Anti-venom – 66.7% share (2025) |

|

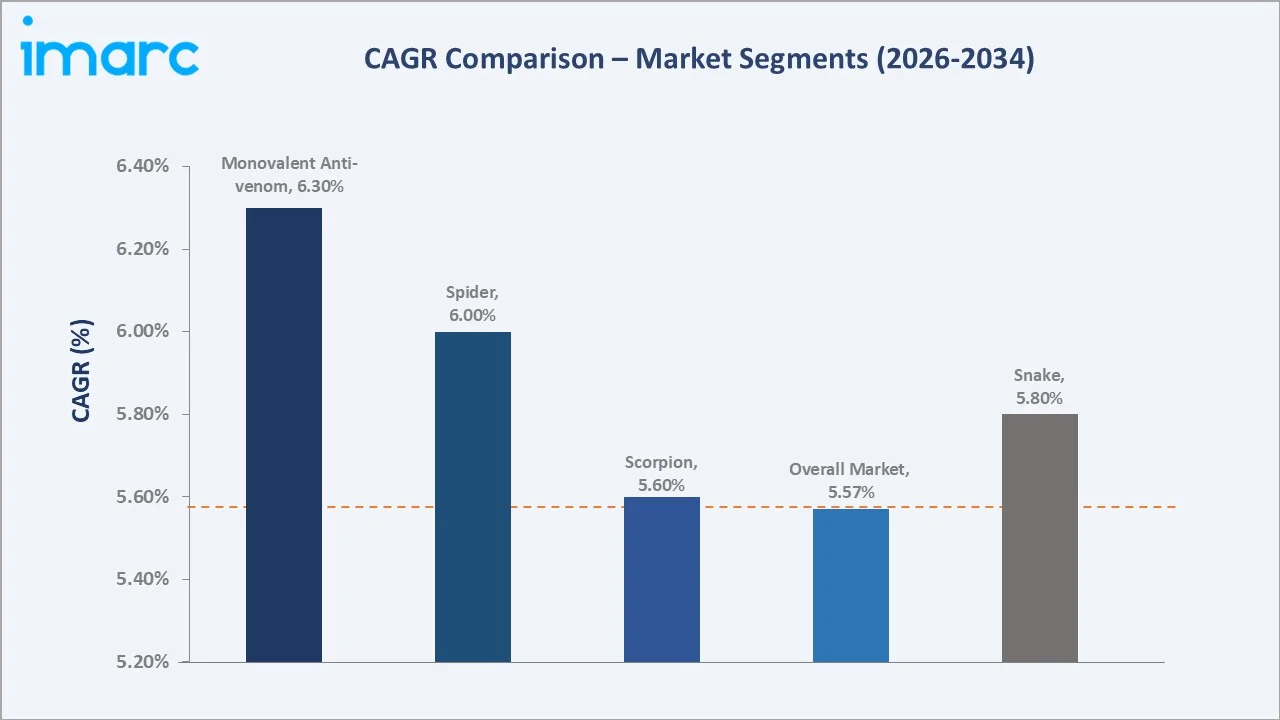

Fastest Growing Anti-venom Type |

Monovalent Anti-venom – ~6.3% CAGR (2026-2034) |

|

Largest Species Segment |

Snake – 52.3% share (2025) |

|

Fastest Growing Species |

Spider – ~6.0% CAGR (2026-2034) |

|

Leading Region |

North America – 37.8% share (2025) |

|

Top Companies |

Mankind Pharma Ltd., CSL Limited, ViNS Bioproducts Ltd., Micropharm |

Key Analytical Observations For 2025:

- Polyvalent Anti-venom (66.7%): Dominates due to broad-spectrum neutralization capability against multiple venom types with a single formulation, making it the preferred choice for emergency settings in endemic regions where the specific envenomating species is often unidentified at the time of treatment.

- Monovalent Anti-venom (33.3%): The fastest-growing type at ~6.3% CAGR, driven by increasing precision medicine approaches in well-equipped hospitals and clinical settings where species identification is feasible, and superior efficacy against specific toxins is prioritized.

- Snake (52.3%): Commands the largest species segment share, reflecting the WHO estimate of 5.4 million annual snakebites globally resulting in 81,000–138,000 deaths, the highest mortality burden of any venomous animal bite category.

- North America (37.8%): Market leadership driven by advanced emergency healthcare infrastructure, FDA-approved polyvalent pit viper anti-venoms, established hospital procurement contracts, and robust public health funding for anti-venom stockpiling across the United States and Canada.

Anti-venom Market Overview

Anti-venom, also known as antivenin or venom antiserum, comprises antibody-based biological products used to counteract the toxic effects of venom from snakebites, scorpion stings, spider bites, and other venomous animal encounters.

Produced primarily through the immunization of horses or sheep with sub-lethal venom doses followed by serum harvesting and antibody purification, anti-venoms are indispensable components of emergency medical care across tropical and subtropical regions globally.

The WHO's classification of snakebite envenomation as a neglected tropical disease in 2017 and subsequent initiative targeting a 50% reduction in snakebite deaths and disability have catalyzed significant government and institutional investment in anti-venom availability, affordability, and supply security.

The anti-venom market forecast reflects the compounding effect of rising envenomation incidence in agricultural communities, climate change expanding the geographic range of venomous species, and accelerating biotechnology innovation enabling next-generation anti-venom formulations with improved safety profiles and longer shelf lives.

Market Dynamics

To evaluate market opportunities, Request Sample

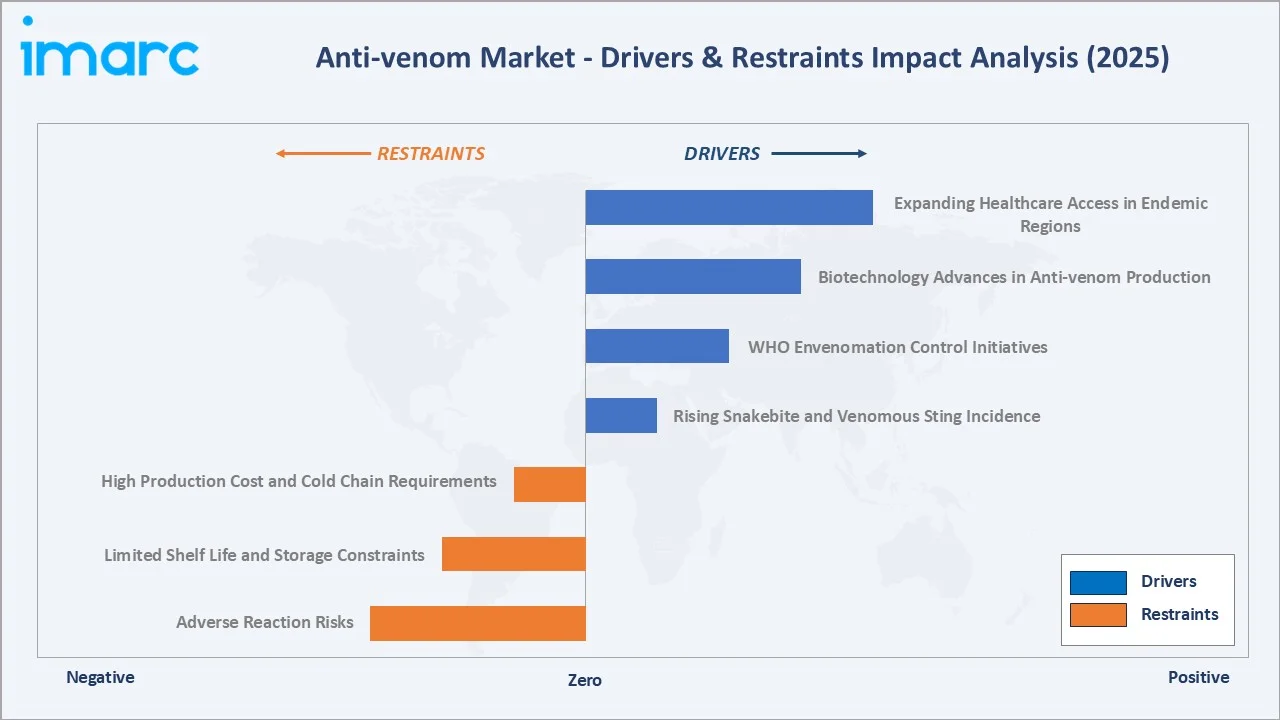

Market Drivers

- Rising Snakebite and Venomous Sting Incidence: The WHO estimates 4.5-5.4 million snakebites occur annually, causing 81,000 to 138,000 deaths. This persistent burden, concentrated in rural South Asian, Sub-Saharan African, and Latin American populations, generates baseline anti-venom demand independent of healthcare system advancement.

- WHO Envenomation Control Initiatives: Under WHO’s 2030 snakebite target has mobilized approximately USD 130 Million from member state commitments and partner organizations for anti-venom procurement, healthcare worker training, and supply chain development in endemic countries, directly expanding institutional anti-venom purchasing.

- Biotechnology Advances in Anti-venom Production: Recombinant DNA technology, monoclonal antibody platforms, and improved fractionation techniques are enabling production of anti-venoms with enhanced potency, reduced adverse reaction profiles, and longer shelf life, driving upgrade cycles in existing hospital formularies.

- Expanding Healthcare Access in Endemic Regions: Government rural health infrastructure investment in India, Brazil, Mexico, and Sub-Saharan Africa is placing anti-venoms into primary healthcare facilities, expanding the distribution footprint substantially beyond major hospitals.

Market Restraints

- High Production Cost and Cold Chain Requirements: Equine-derived anti-venom production involves labor-intensive immunization cycles and complex purification processes, generating high manufacturing costs. Combined with mandatory cold-chain storage at 2–8°C, distribution to remote endemic regions remains logistically challenging and expensive.

- Limited Shelf Life and Storage Constraints: Most anti-venoms have a shelf life of 2–5 years under proper refrigeration, creating stockpile management challenges for national health systems in low-income endemic countries, and contributing to waste and supply gaps.

- Adverse Reaction Risks: Equine-derived anti-venoms carry risks of anaphylaxis and serum sickness in a subset of patients, creating clinical hesitancy in some settings and driving demand for ovine-derived or recombinant alternatives at premium price points.

Market Opportunities

- Recombinant and Monoclonal Antibody Anti-venom Development: Next-generation recombinant anti-venoms produced without animal immunization can eliminate adverse reaction risks, extend shelf life, and enable scalable manufacturing, representing a transformative product innovation opportunity for biotechnology companies.

- Government Procurement Programs in Endemic Nations: India, Brazil, Mexico, Australia, and multiple African nations maintain national anti-venom procurement programs, creating large, predictable revenue streams for qualified manufacturers that achieve WHO prequalification status.

- Climate Change Expanding Venomous Species Range: Temperature warming is extending the geographic range of venomous snake and scorpion species into previously lower-risk temperate regions, creating new market demand in countries with historically limited anti-venom procurement.

Market Challenges

- Market Access and Affordability in Least Developed Countries: The populations bearing the highest snakebite burden often reside in countries with limited healthcare budgets, creating a fundamental mismatch between anti-venom need and purchasing power that constrains commercial market development.

- WHO Prequalification Compliance Barriers: Increasingly stringent WHO prequalification requirements and national regulatory standards are raising compliance costs substantially, disadvantaging smaller regional manufacturers and potentially reducing supply diversity in some endemic markets.

Emerging Market Trends

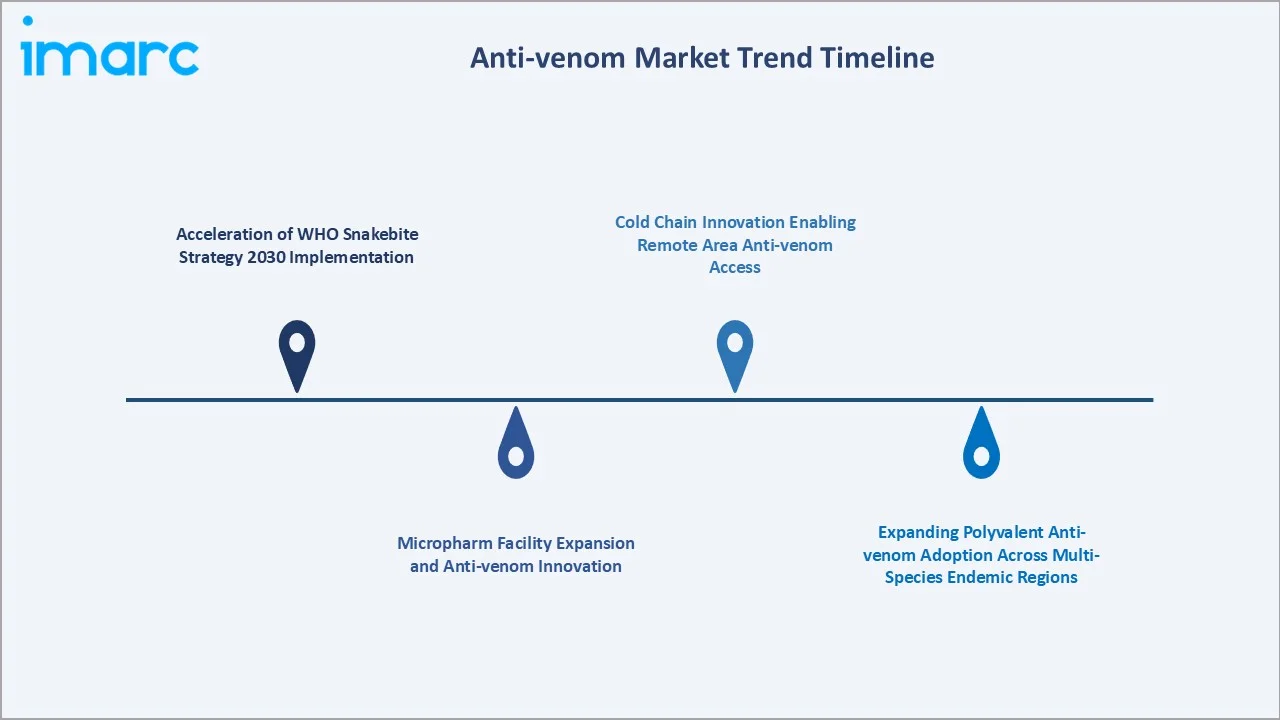

1. Acceleration of WHO Snakebite Strategy 2030 Implementation

The WHO’s targets to halve snakebite deaths and disability by 2030 are mobilizing coordinated investment from governments, international donors, and pharmaceutical manufacturers into anti-venom supply chain development, healthcare worker training programs, and community awareness initiatives across 20 priority endemic countries.

2. Micropharm Facility Expansion and Anti-venom Innovation

In June 2024, Micropharm received MHRA manufacturing licences for its new facility in Cilgerran, North Pembrokeshire, UK, advancing production of Viperfav and Bothrofav species-specific anti-venoms, reflecting the anti-venom market trends toward specialized facility investment. Monoclonal antibody-based platforms are entering early clinical development, representing the next frontier of anti-venom therapy.

3. Expanding Polyvalent Anti-venom Adoption Across Multi-Species Endemic Regions

Healthcare systems in multi-species endemic regions across Sub-Saharan Africa, South Asia, and Latin America are increasingly standardizing on polyvalent anti-venom formulations that provide broad-spectrum protection against the diverse snake and scorpion species. This standardization simplifies hospital formulary management, reduces the logistical complexity of maintaining multiple species-specific products, and enables more efficient WHO procurement programs.

4. Cold Chain Innovation Enabling Remote Area Anti-venom Access

Lyophilized (freeze-dried) anti-venom formulations, which allow storage at ambient temperatures without refrigeration, are gaining traction as a transformative delivery innovation for last-mile healthcare access. Organizations including Médecins Sans Frontières and PATH are supporting field validation of thermostable anti-venom formulations, and regulatory pathways for ambient-temperature anti-venoms are advancing in India, Africa, and Brazil.

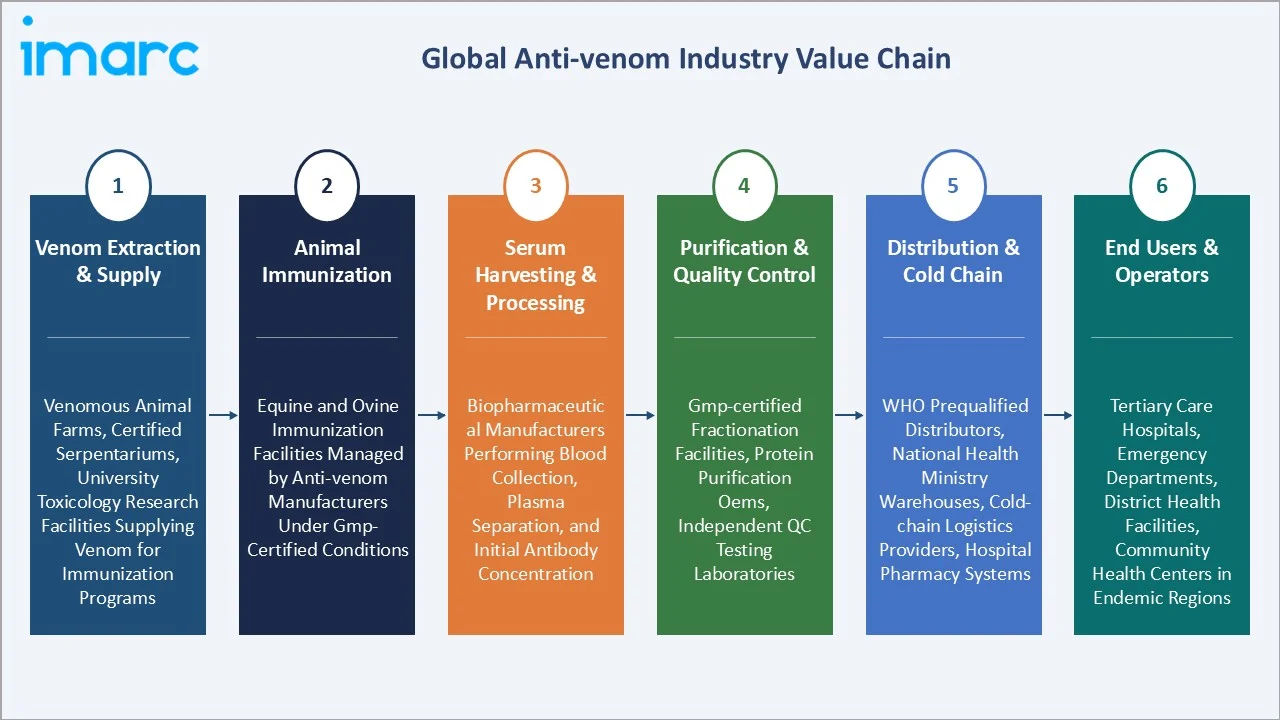

Industry Value Chain Analysis

|

Stage |

Key Players / Examples |

|

Venom Extraction & Supply |

Venomous animal farms, certified serpentariums, university toxicology research facilities supplying venom for immunization programs |

|

Animal Immunization |

Equine and ovine immunization facilities managed by anti-venom manufacturers under GMP-certified conditions |

|

Serum Harvesting & Processing |

Biopharmaceutical manufacturers performing blood collection, plasma separation, and initial antibody concentration |

|

Purification & Quality Control |

GMP-certified fractionation facilities, protein purification OEMs, independent QC testing laboratories |

|

Distribution & Cold Chain |

WHO prequalified distributors, national health ministry warehouses, cold-chain logistics providers, hospital pharmacy systems |

|

End Users & Operators |

Tertiary care hospitals, emergency departments, district health facilities, community health centers in endemic regions |

Technology Landscape in the Anti-venom Industry

Equine-Derived Anti-venom Technology

Equine-derived anti-venom production remains the dominant manufacturing technology globally, accounting for the majority of commercially available polyvalent and monovalent products. The process involves repeatedly immunizing horses with progressively increasing doses of venom, harvesting plasma after peak antibody titers are achieved, and purifying immunoglobulins through ammonium sulfate precipitation and pepsin digestion.

Ovine-Derived Anti-venom Technology

Ovine (sheep-based) anti-venom technology offers an alternative immunoglobulin source with potentially reduced serum sickness risk compared to equine products, as ovine serum proteins are less immunogenic in humans. CroFab, the sheep-derived Crotalidae polyvalent immune Fab anti-venom produced for North American pit viper envenomation by BTG International Inc., now a SERB company, is a commercially established example demonstrating the clinical viability of ovine-derived formulations.

Recombinant Biotechnology-Based Anti-venom

Researchers at the Technical University of Denmark are developing recombinant anti-venom using modern antibody technologies like phage display and human antibody libraries to create safer, more effective, and potentially lower‑cost alternatives to traditional horse‑derived anti-venoms. These approaches eliminate animal immunization, enabling batch-consistent production with scalable manufacturing infrastructure.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Anti-venom Type | Polyvalent Anti-venom | 66.7% | 2025 |

| Species | Snake | 52.3% | 2025 |

| Mode of Action | 🔒 | 🔒 | 2025 |

| End User | 🔒 | 🔒 | 2025 |

| Region | North America | 37.8% | 2025 |

By Anti-venom Type

Polyvalent anti-venom dominates with a 66.7% share in 2025, as they provide broad-spectrum neutralization against venom from multiple species using a single vial. Their lower per-treatment cost relative to maintaining multiple monovalent anti-venom and simpler procurement logistics further reinforce institutional preference, particularly across government hospital networks in Africa, Asia, and Latin America.

To access detailed market analysis, Request Sample

Monovalent anti-venom at 33.3% is the fastest-growing type at ~6.3% CAGR through 2034, driven by expanding precision medicine capabilities. Increasing investment by major manufacturers in developing high-potency monovalent anti-venom products targeting the medically most significant species in North America, Europe, and Australia is expanding the clinical evidence base supporting their adoption in advanced healthcare settings globally.

By Species

Snake species dominates at 52.3% share in 2025, reflecting the WHO estimate of 4.5–5.4 million annual snakebites generating the highest global envenomation mortality burden. Scorpion represents 24.1%, driven by high-burden markets in North Africa, the Middle East, and Mexico, where scorpion envenomation is a major pediatric emergency.

Spider at 14.6% is the fastest-growing species segment at ~6.0% CAGR, driven by CSL opening a USD 1 billion advanced cell‑based influenza vaccine and anti-venom manufacturing facility in Melbourne, Australia, and growing clinical awareness of Latrodectus (black widow) and Loxosceles (brown recluse) envenomation in the Americas and Europe.

Regional Market Insights

North America's market leadership at 37.8% in 2025 reflects advanced emergency healthcare infrastructure, FDA-approved anti-venom availability, and government procurement programs ensuring hospital stockpile adequacy across the United States and Canada.

Asia-Pacific at 23.6% is the most dynamic growth geography, anchored by India's over 1,000,000 snakebites that occur each year, resulting in approximately 58,000 deaths and causing significant disability in nearly four times that number, the highest in any single country. China, Australia, and Southeast Asian nations are also expanding domestic anti-venom production capabilities, further accelerating regional market growth through the forecast period.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

37.8% |

Advanced emergency healthcare infrastructure, robust hospital procurement contracts, government stockpile programs |

|

Europe |

24.9% |

Strong hospital procurement systems, rising awareness of imported tropical snakebite cases, established manufacturing presence |

|

Asia-Pacific |

23.6% |

High snakebite burden in India and Southeast Asia, domestic manufacturer expansion, government procurement programs |

|

Latin America |

8.1% |

Brazil's Instituto Butantan domestic production, scorpion anti-venom in Mexico, high rural snakebite and scorpion sting incidence |

|

Middle East & Africa |

5.6% |

High scorpion sting burden in North Africa and the Arabian Peninsula, donor-funded anti-venom procurement programs |

Competitive Landscape

The global anti-venom market exhibits moderate concentration, with Mankind Pharma Ltd., CSL Limited, ViNS Bioproducts Ltd., and Micropharm collectively holding approximately 50–55% of total global revenue in 2025.

|

Company Name |

Brands/Product Names |

Market Position |

Core Strength |

|

Mankind Pharma Ltd. |

ASVS |

Market Leader |

One of India's largest anti-venom producers; broad polyvalent and monovalent snake coverage |

|

CSL Limited |

Brown snake anti-venom, tiger snake anti-venom, polyvalent snake anti-venom, redback spider anti-venom, box jellyfish anti-venom, and stone fish anti-venom, among others. |

Market Leader |

Snake, spider, and marine anti-venom breadth; Australian/APAC market dominance; advanced biotech manufacturing |

|

ViNS Bioproducts Ltd. |

ASVS, BIOSNAKE, AFRIVEN, ECHIVEN, PCAS, MENASCORP, MENASCORP Plus |

Challenger |

Operates fully automated facilities; commitment to global quality standards |

|

Micropharm |

Favirept, EchiTAbG, Bothrofav, Viperfav |

Strong Challenger |

Viperfav/Bothrofav European vipers; MHRA-licensed manufacturing site; WHO prequalification programs |

Manufacturers are investing in next-generation recombinant and monoclonal antibody platforms and are positioning for the anticipated technology transition that will reshape competitive rankings over the latter portion of the forecast period.

Key Company Profiles

Mankind Pharma Ltd.

Mankind Pharma Ltd. is the parent company of Bharat Serums and Vaccines Limited (BSV), which is one of the global market leaders in anti-venom production. Its anti-venom portfolio spans polyvalent and monovalent snake anti-venoms covering the medically most significant species.

- Product Portfolio: Snake Venom Anti-serum Polyvalent (ASVS)

- Recent Developments: In March 2026, Kerala’s government is exploring a collaboration with Mumbai‑based Bharat Serums and Vaccines Limited to establish a venom collection center in Thrissur and develop region‑specific polyvalent anti-venom tailored to local snake species.

- Strategic Focus: Expanding WHO prequalified portfolio for African snake species; reducing production costs to improve access in low-income endemic markets; developing partnerships with Indian Institute of Science for next-generation anti-venom research.

CSL Limited

CSL Limited’s subsidiary CSL Seqirus, which is a global biotherapeutics leader with an anti-venom portfolio covering Australian snake, spider, and marine species. CSL Seqirus manages the anti-venom product line, supplying the Australian government's national anti-venom stockpile.

- Product Portfolio: Brown snake anti-venom, tiger snake anti-venom, polyvalent snake anti-venom, redback spider anti-venom, box jellyfish anti-venom, and stone fish anti-venom, among others.

- Recent Developments: In December 2025, CSL Seqirus opened a USD 1 billion, world‑class vaccine and anti-venom manufacturing facility in Melbourne. The site will supply Australia’s eleven anti-venoms among other products domestically and globally.

- Strategic Focus: Strengthening Australian market supply security; expanding Asia-Pacific anti-venom access programs; advancing next-generation manufacturing technologies to improve product safety and shelf life.

Market Concentration Analysis

The global anti-venom market exhibits moderate concentration, with the top vendors holding approximately 50–55% of total revenue in 2025. Below the top tier, a diverse mid-market of 15–20 regional manufacturers serves domestic and regional endemic markets, often under government supply agreements that prioritize pricing and local supply security over product innovation.

Micropharm's acquisition of Sanofi Pasteur's equine anti-venom portfolio signals ongoing consolidation among mid-tier manufacturers as WHO prequalification compliance costs rise. AI-assisted toxin informatics and synthetic biology platforms are enabling academic spinouts to advance recombinant anti-venom candidates that could disrupt incumbent manufacturing economics by the early 2030s.

Investment and Growth Opportunities

Fastest Growing Segments

Monovalent anti-venom (~6.3% CAGR), spider anti-venom (~6.0% CAGR), recombinant anti-venom technology platforms (~15–20% CAGR), and thermostable lyophilized formulations for remote area distribution represent the highest-growth investment vectors through 2034. Together, these sub-categories address a combined incremental addressable market of approximately USD 400 Million beyond current base projections by 2030.

Emerging Market Expansion

India, Sub-Saharan Africa, and Southeast Asia collectively represent the largest unmet anti-venom demand opportunity globally. Entry strategies for manufacturers targeting these regions include WHO prequalification pursuit as a prerequisite for donor-funded procurement access, tiered pricing programs aligned with government affordability thresholds, and community health worker training programs.

Venture and Institutional Investment Trends

- Academic-industry partnerships for recombinant anti-venom development are attracting significant grant funding from the Wellcome Trust, Bill & Melinda Gates Foundation, and EU Horizon programs, with multiple pre-clinical stage projects advancing toward first-in-human trials.

- Donor-funded procurement programs from Médecins Sans Frontières, UNICEF, and bilateral development agencies are creating growing institutional anti-venom purchasing volumes in Sub-Saharan Africa, improving market predictability for manufacturers investing in African species-specific anti-venom development.

- Impact investment vehicles and development finance institutions are beginning to view anti-venom manufacturing capacity as a global health security investment, potentially unlocking new funding streams for manufacturer capacity expansion in endemic regions.

Future Market Outlook (2026-2034)

The global anti-venom market is positioned for consistent value growth through 2034. From a base of USD 1.31 Billion in 2025, the market is projected to reach USD 2.17 Billion by 2034, representing total incremental value creation of USD 860 Million at a CAGR of 5.57%. This growth is anchored by the persistent global snakebite burden, WHO 2030 target implementation, and the technology transition from conventional equine-derived products toward advanced recombinant and monoclonal antibody platforms.

Polyvalent anti-venom's share is expected to moderate slightly by 2034 as monovalent precision products gain clinical adoption in advanced healthcare markets, while recombinant anti-venom candidates transition from clinical trials to commercial launch within the latter portion of the forecast window.

Geographic expansion of anti-venom access into rural Sub-Saharan Africa and remote South Asian communities, enabled by thermostable formulations and community health worker distribution networks, represents the primary driver of volume growth beyond current market penetration. North America will maintain revenue leadership while Asia-Pacific is projected to record the highest incremental growth, driven by India's domestic manufacturing expansion and Southeast Asian healthcare infrastructure investment.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 85 industry participants during 2024–2025, including anti-venom manufacturers, hospital pharmacy directors, WHO and national health ministry procurement specialists, emergency medicine clinicians, and institutional investors across North America, Europe, Asia-Pacific, and Latin America, validating market sizing assumptions and technology adoption timelines.

Secondary Research

Secondary research encompassed manufacturer annual reports, FDA 510(k) and BLA databases, EMA product approval registries, WHO prequalification lists, WHO snakebite envenomation epidemiological data, peer-reviewed toxicology and emergency medicine journals, and institutional investor research on biopharmaceutical manufacturers.

Forecasting Models

Market size estimations derived using top-down and bottom-up forecasting incorporating envenomation incidence data by species and region, anti-venom treatment uptake rates by healthcare system tier, average selling prices by product type and geography, and manufacturer revenue disclosures. Base-case CAGR of 5.57% reflects consensus estimates validated against announced procurement programs and anti-venom capacity expansion pipelines through 2034.

Anti-venom Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Species Covered | Snake, Scorpion, Spider, and Others |

| Anti-venom Type Covered | Polyvalent Anti-venom, Monovalent Anti-venom |

| Mode of Action Covered | Cytotoxic, Neurotoxic, Haemotoxic, Cardiotoxic, Myotoxic, and Others |

| End User Covered | Hospitals, Clinics, Ambulatory Surgical Centers |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Mankind Pharma Ltd. , CSL Limited, ViNS Bioproducts Ltd. , Micropharm, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the anti-venom market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global anti-venom market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the anti-venom industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Anti-Venom Market Report

The global anti-venom market reached USD 1.31 Billion in 2025.

The market is projected to grow at a CAGR of 5.57%, reaching USD 2.17 Billion by 2034.

Key drivers include rising global snakebite and venomous sting incidences, WHO Snakebite Strategy 2030 implementation, biotechnology advances in anti-venom production, expanding healthcare access in endemic tropical regions, and growing government procurement programs.

Polyvalent anti-venom dominates with a 66.7% share in 2025, owing to broad-spectrum neutralization capability and suitability for emergency settings where species identification is unavailable.

Monovalent anti-venom is the fastest-growing type at approximately ~6.3% CAGR during 2026–2034, driven by precision medicine adoption and superior efficacy in species-identified clinical settings.

Snake anti-venom leads with a 52.3% species segment share in 2025, driven by the WHO estimate of 4.5–5.4 million annual snakebites generating the highest global envenomation mortality burden.

North America leads the anti-venom market with 37.8% global share in 2025, anchored by advanced emergency care infrastructure, FDA-approved anti-venom availability, and government stockpile programs.

Asia-Pacific at 23.6% is the fastest-growing region, driven by India's dominant snakebite mortality burden, domestic manufacturer expansion by BSV and Serum Institute, and WHO strategy implementation.

Major players include Mankind Pharma Ltd., CSL Limited, ViNS Bioproducts Ltd., and Micropharm.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)