Applicant Tracking System Market Size, Share, Trends and Forecast by Deployment, Organization Size, Component, End-User, and Region, 2026-2034

Global Applicant Tracking System Market Size, Share, Trends & Forecast (2026-2034)

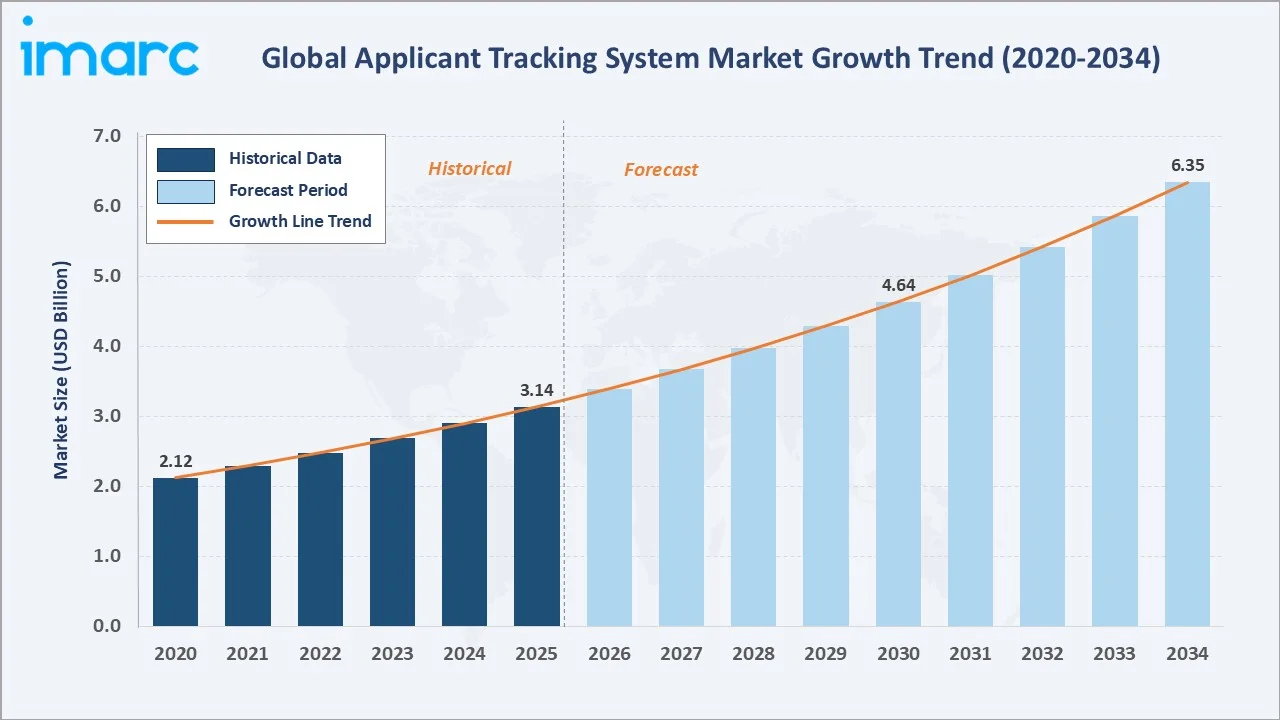

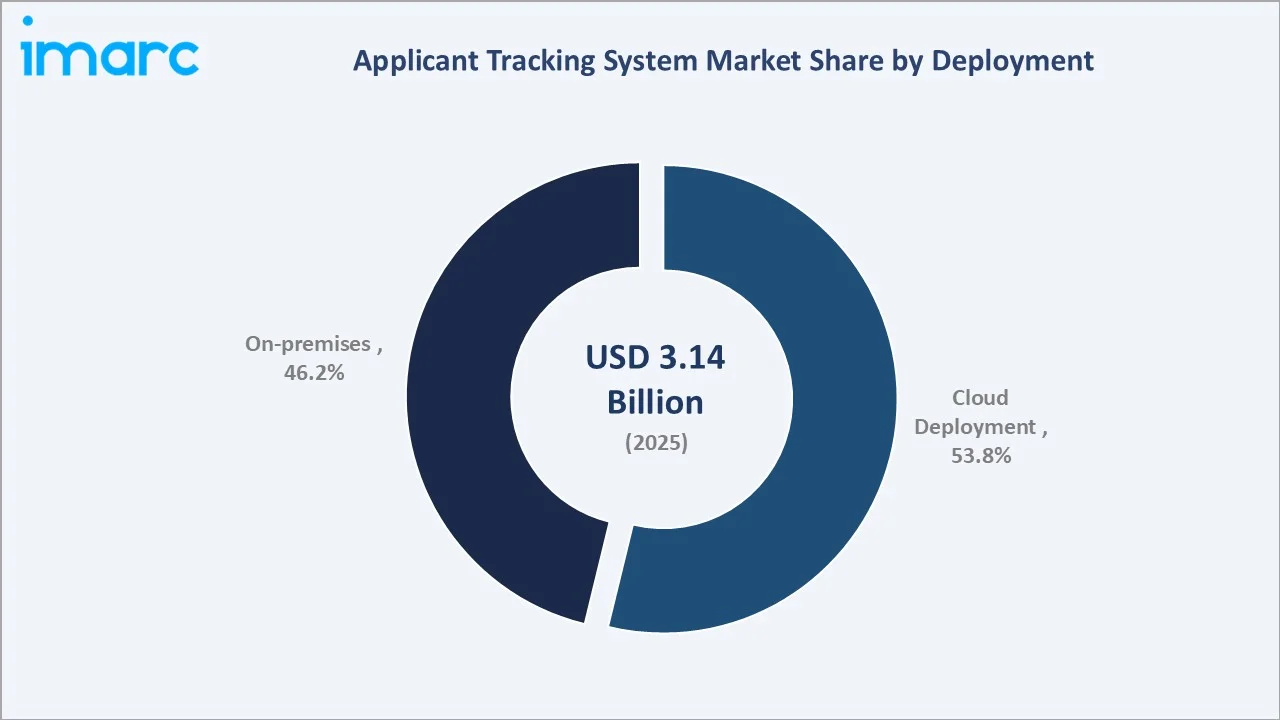

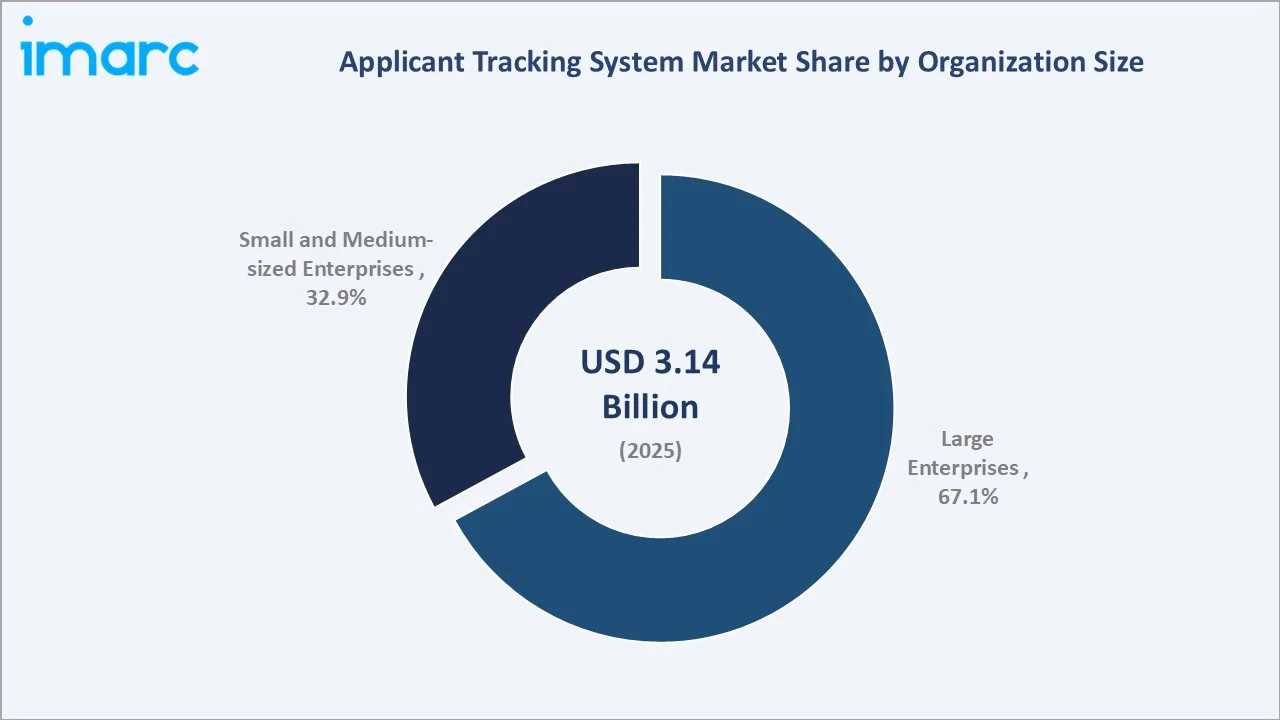

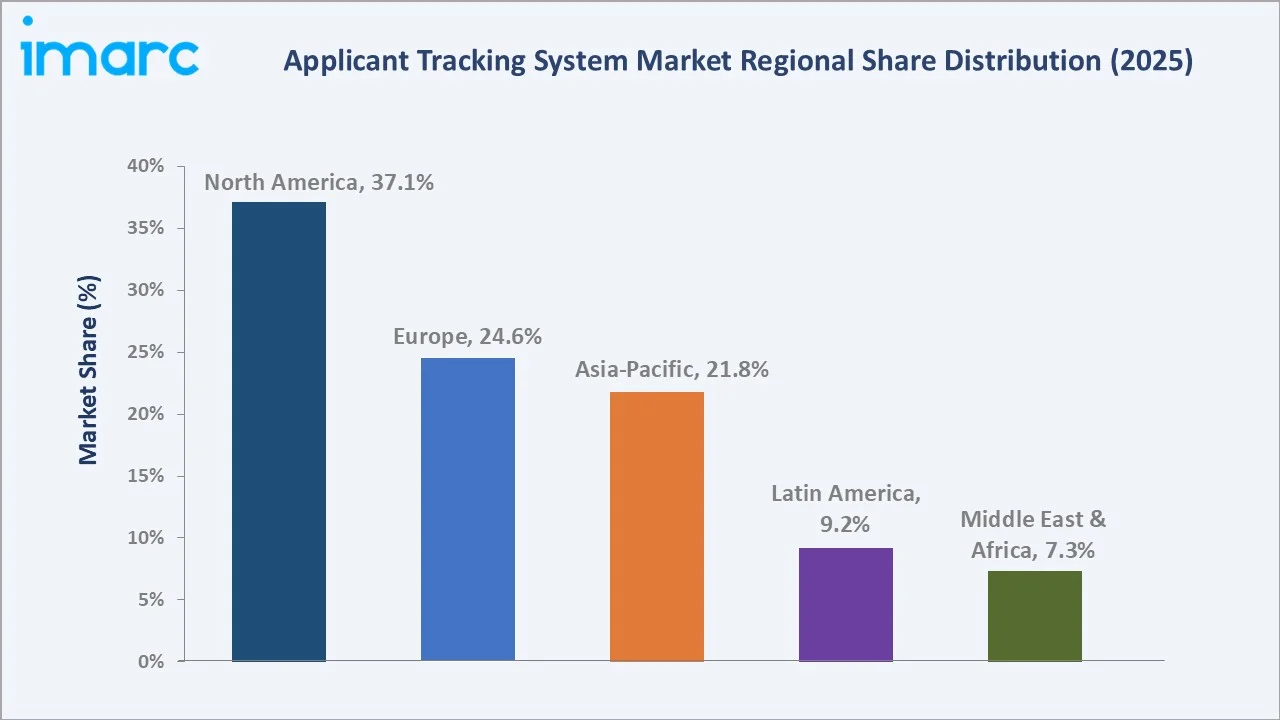

The global applicant tracking system market size was valued at USD 3.14 Billion in 2025 and is projected to reach USD 6.35 Billion by 2034, exhibiting a CAGR of 8.14% during the forecast period 2026-2034. Growing demand for AI-driven, automated recruitment workflows is the primary structural driver, with HR automation now deployed by 27% of companies globally. Cloud-based lead the market with a 53.8% deployment share in 2025, reflecting enterprise preference for SaaS delivery and subscription-based licensing. Large enterprises account for 67.1% of market revenue in 2025, driven by complex, multi-location hiring needs. North America commands a 37.1% regional revenue share, while Asia-Pacific is the fastest-growing regional market, underpinned by rapid enterprise digitization in India, China, and Southeast Asia.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.14 Billion |

|

Forecast Market Size (2034) |

USD 6.35 Billion |

|

CAGR (2026-2034) |

8.14% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (37.1% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Leading Deployment |

Cloud (53.8%, 2025) |

|

Leading Organization Segment |

Large Enterprises (67.1%, 2025) |

The global applicant tracking system market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by AI-powered recruiting, cloud adoption, and increasing compliance mandates.

To get more information on this market, Request Sample

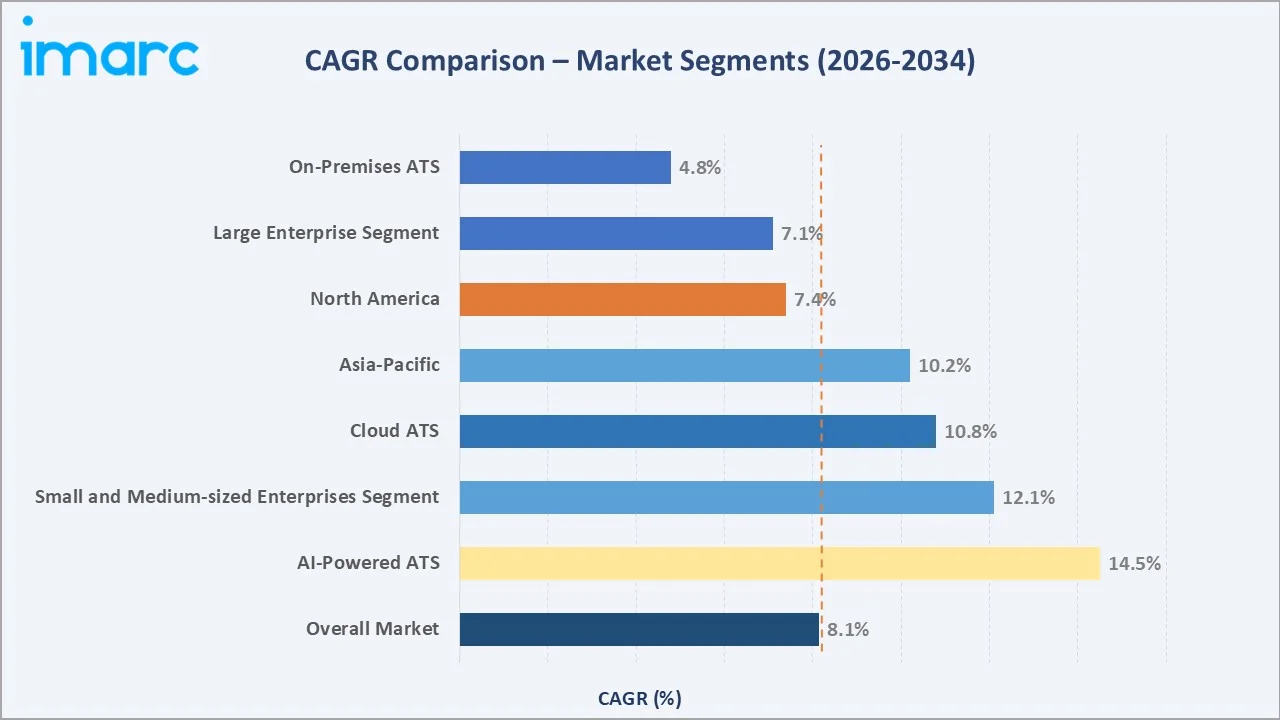

Segment-level CAGR comparisons highlighting AI-powered ATS and the SME organization segment as the two fastest-growing sub-categories within the global applicant tracking system industry analysis through 2034.

Executive Summary

The global applicant tracking system market, valued at USD 3.14 Billion in 2025, is projected to reach USD 6.35 Billion by 2034 at 8.14% CAGR, driven by AI, cloud computing, and the growing strategic role of talent acquisition.

Cloud deployment holds 53.8% of the market and grows fastest due to subscription models and continuous updates, while on-premises retains 46.2%, favored by highly regulated industries. Large enterprises generate 67.1% of market revenue in 2025, reflecting their high hiring volumes and the complexity of multi-geography recruitment. Small and Medium-sized Enterprises at 32.9% represent the fastest-growing organization segment, as affordable cloud ATS platforms expand accessibility below the traditional enterprise adoption threshold.

North America leads globally with a 37.1% share in 2025, anchored by technology-mature enterprises and a robust HR-tech vendor ecosystem including Workday, Oracle, and iCIMS. Europe follows at 24.6%, driven by GDPR compliance mandates requiring audit-ready, structured recruitment platforms. Asia-Pacific accounts for 21.8% but is projected to post the highest regional growth rate through 2034, fueled by rapid enterprise digitization across India, China, and Southeast Asia.

Key Market Insights

|

Insight |

Data |

|

Largest Deployment Segment |

Cloud Deployment – 53.8% share (2025) |

|

Leading Organization Segment |

Large Enterprises – 67.1% share (2025) |

|

Leading Region |

North America – 37.1% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific – ~10% CAGR through 2034 |

|

Top Companies |

Workday, Oracle, SAP SE, iCIMS, Greenhouse Software, SmartRecruiters |

|

Market Opportunity |

AI-driven ATS and SME cloud adoption in emerging markets |

- Cloud Deployment at 53.8% market share in 2025 reflects enterprise preference for elastic, subscription-based platforms that support dispersed hiring managers, real-time analytics, and rapid feature deployment through continuous SaaS update cycles.

- Large enterprises at 67.1% market dominance in 2025 are driven by complex multi-geography hiring needs, sophisticated workforce planning requirements, and integration demands across HCM, payroll, and learning management platforms.

- North America's 37.1% revenue leadership is underpinned by the presence of leading ATS vendors, early adoption of AI-powered recruiting, and stringent EEOC compliance frameworks mandating structured, auditable hiring workflows.

- Asia-Pacific is projected to grow at approximately 10% CAGR through 2034, driven by India's rapidly expanding IT sector employing over 5 million professionals, China's enterprise technology modernization, and growing MNC hiring activity across Southeast Asia.

- AI-powered capabilities, including resume parsing, chatbot pre-screening, and talent rediscovery, are now the primary ATS vendor differentiation factors, with Workday's Spring 2025 Release featuring over 350 product enhancements addressing AI-driven talent workflows.

Global Applicant Tracking System Market Overview

An applicant tracking system (ATS) automates and centralizes the recruitment lifecycle—from job posting and resume parsing to candidate screening, interview scheduling, offer management, and onboarding. Modern ATS platforms integrate with HRIS, payroll, background checks, video interviews, and analytics, evolving into strategic talent intelligence hubs. Used across industries like BFSI, IT, healthcare, retail, and government, enterprise-grade ATS now includes AI matching, diversity screening, predictive analytics, and regulatory reporting.

Growth is driven by hybrid/remote work, tightening labour markets, rising recruitment costs, and complex multi-jurisdictional compliance.

Market Dynamics

To evaluate market opportunities, Request Sample

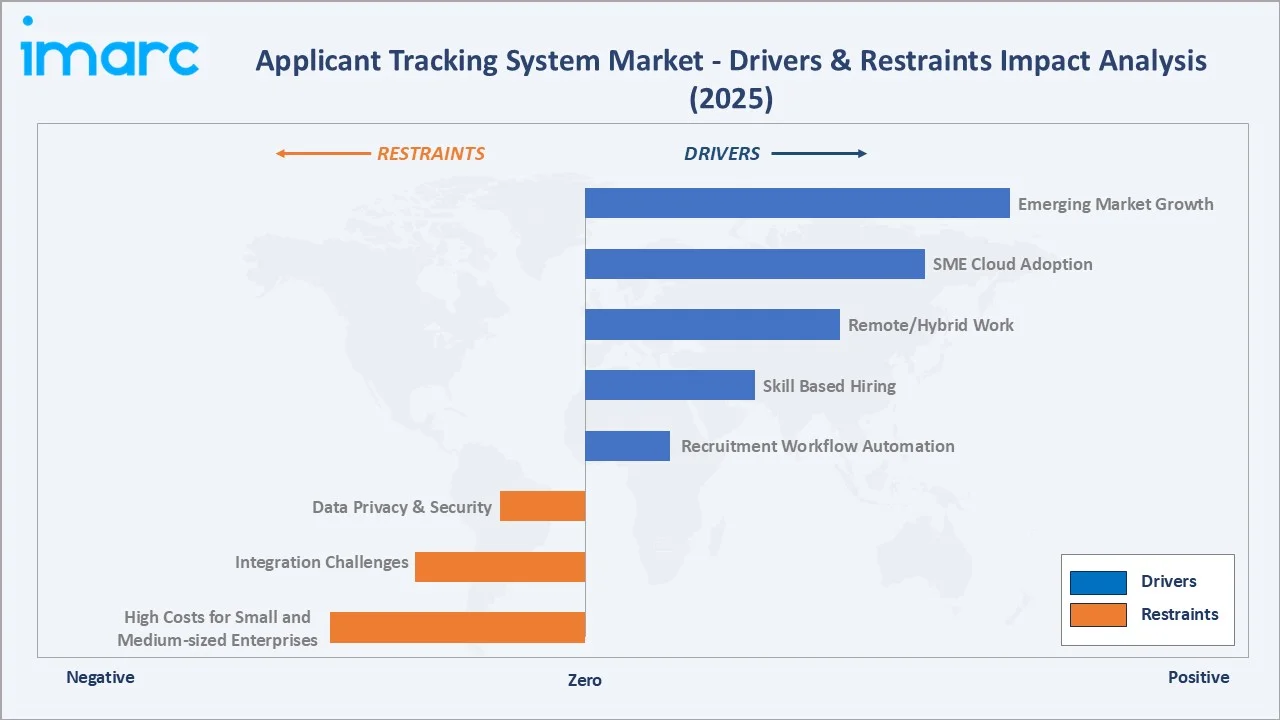

Market Drivers

- Recruitment Workflow Automation: ATS platforms cut time-to-fill by 40–60%, letting HR teams handle higher applicant volumes efficiently.

- Regulatory Compliance: Platforms support EEOC, GDPR, and global diversity mandates with structured, auditable hiring processes.

- Remote/Hybrid Work: Cloud-based ATS enable location-agnostic recruiting across multiple geographies and time zones.

Market Restraints

- High Costs for Small and Medium-sized Enterprises: Enterprise ATS setup involves significant licensing, customization, integration, and training expenses, straining SME budgets.

- Integration Challenges: Connecting cloud ATS with legacy HRIS, ERP, and payroll systems requires technical expertise and costly customizations.

- Data Privacy & Security: Handling sensitive candidate data across jurisdictions creates compliance complexity for multinational organizations.

Market Opportunities

- SME Cloud Adoption: Affordable cloud ATS for Small and Medium-sized Enterprises taps a large, underpenetrated market.

- Emerging Market Growth: Asia-Pacific, Latin America, and the Middle East—especially India, Indonesia, Brazil, and the UAE—offer major greenfield ATS opportunities through 2034.

- Generative AI Innovation: LLM-powered features like automated job descriptions, conversational screening, and AI interview design are the next key differentiation layer.

Market Challenges

- Vendor Consolidation Pressure: Enterprise preference for integrated HCM suites gives Workday, Oracle, and SAP SuccessFactors a competitive edge, challenging standalone ATS vendors.

- Candidate Data Management: Large-scale hiring generates vast applicant datasets, creating GDPR and CCPA compliance challenges for ATS vendors and enterprises.

Emerging Market Trends

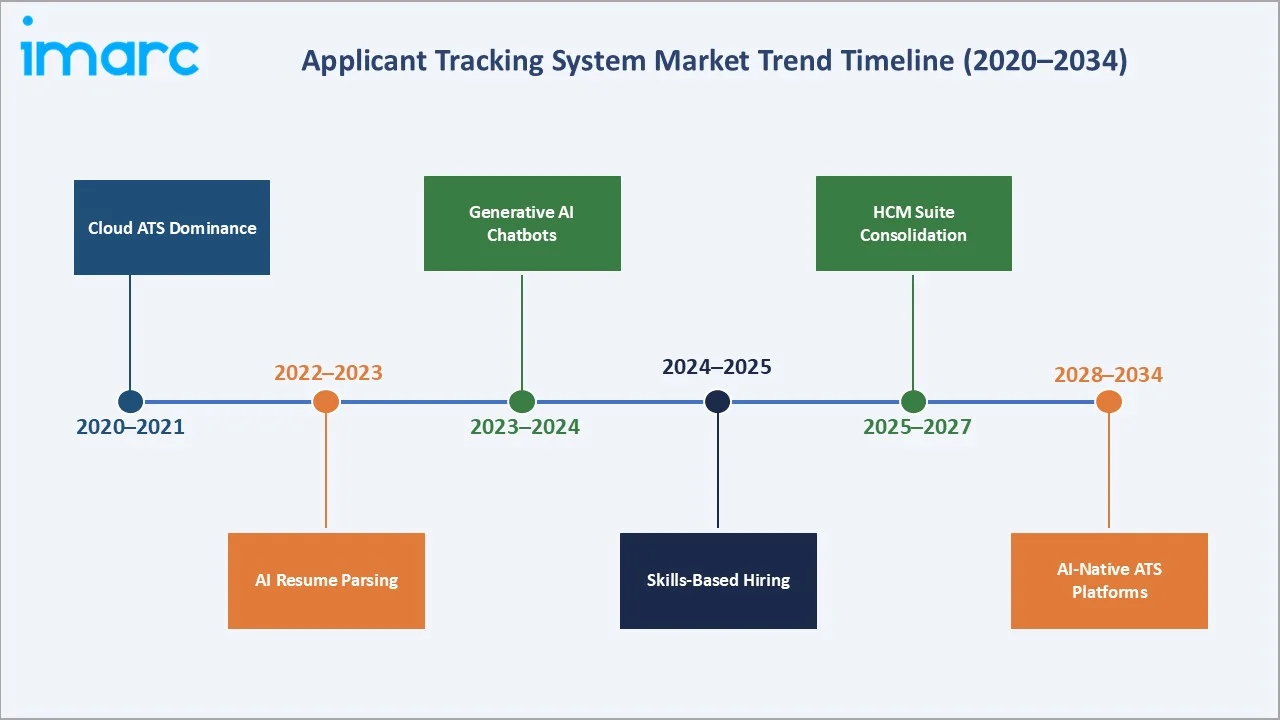

1. Generative AI Redefining ATS Product Architecture

Generative AI and large language models are transforming ATS platforms from applicant databases into predictive talent intelligence engines. Bullhorn's Amplify suite, launched at Engage Boston 2025, delivered early-user results of a 51% rise in job submissions and 85% candidate satisfaction, establishing AI capability as the primary ATS selection criterion.

2. Skills-Based Hiring Displacing Credential-Based Recruitment

Organizations are shifting from degree-and-title credential filtering to competency-based hiring, requiring ATS platforms to support skills taxonomies, assessment integrations, and anonymous screening workflows. This shift expands the addressable talent pool, reduces systemic bias, and improves quality-of-hire metrics – particularly relevant in tight labour markets where traditional credential filters exclude qualified candidates.

3. HCM Suite Consolidation and Platform Integration

Enterprises increasingly prefer unified HCM platforms that integrate ATS, performance management, learning, and payroll on a single data model. Oracle's cloud services revenue rose 21% in Q1 2025, reflecting enterprise appetite for integrated platform architectures. This shift favors large suite vendors and creates pricing pressure on standalone ATS providers.

4. Mobile-First Candidate Experience Optimization

Over 60% of global job applications are now submitted via mobile devices. ATS vendors are investing heavily in mobile-optimized application flows, one-tap apply integrations with job boards, and SMS-based candidate communication to reduce drop-off rates. iCIMS's 2025 Summer Release specifically introduced SEO and translation assistants for global career sites, reflecting the growing importance of mobile-accessible, multilingual candidate interfaces.

5. DEI Compliance and Structured Hiring Automation

Regulatory pressure combined with corporate ESG commitments is driving demand for ATS features that anonymize resumes, track diversity pipeline metrics, flag bias in job descriptions, and generate EEOC and diversity audit reports automatically. DEI-focused capabilities have become a standard enterprise ATS feature requirement across North America and Europe, with the EU AI Act's provisions on automated recruitment decision-making expected to further formalize requirements through 2026–2027.

Industry Value Chain Analysis

The applicant tracking system value chain spans five integrated stages from technology infrastructure providers through enterprise end-users. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements that shape the overall industry structure.

|

Stage |

Key Players / Description |

|

Technology Infrastructure |

Cloud providers (AWS, Microsoft Azure, Google Cloud) supply the hosting, compute, storage, and global data center infrastructure underpinning all SaaS ATS deployments. |

|

ATS Software Vendors |

Core platform developers (Workday, Oracle, SAP, iCIMS, Greenhouse, SmartRecruiters, Zoho) design, build, and maintain ATS software and deliver it as SaaS |

|

System Integrators |

Implementation partners (Accenture, Deloitte, IBM Consulting) deploy and customize enterprise ATS platforms, integrate with HRIS and ERP systems, and provide ongoing support. |

|

HR Tech Ecosystem Partners |

Job boards (Indeed, LinkedIn), background screening firms, video interview platforms, assessment providers, and analytics tools that integrate with core ATS via open APIs |

|

End-User Organizations |

Large enterprises, Small and Medium-sized Enterprises, staffing agencies, and government bodies across BFSI, IT, healthcare, retail, and manufacturing that purchase and deploy ATS solutions |

ATS software vendors occupy the highest-value strategic position in the value chain, capturing subscription revenue, professional services fees, and platform ecosystem royalties. However, this position faces structural pressure from two directions: enterprise clients internalizing software development to reduce vendor dependency, and cloud hyperscalers (AWS, Microsoft) offering competing HR AI services directly on their platforms.

Technology Landscape in the Applicant Tracking System Industry

Artificial Intelligence and Natural Language Processing

AI is the defining technology transformation in the ATS industry. Resume parsing accuracy has improved from approximately 75% in 2019 to over 95% with modern NLP models. Conversational AI chatbots now handle candidate pre-screening, FAQ support, and interview scheduling with minimal recruiter intervention. Workday's Spring 2025 Release and iCIMS's Summer 2025 Release both feature AI-driven candidate rediscovery and intelligent matching, setting a new baseline for enterprise ATS capability. Generative AI features – automated job description generation and LLM-based interview question design – represent the next capability tier.

Cloud and SaaS Architecture

Cloud-native ATS platforms represent 53.8% of the market in 2025, enabled by multi-tenant SaaS architectures that support elastic scaling, automated feature updates, and global data center redundancy. Open API frameworks facilitate seamless integration with job boards, background check providers, video interview tools, and analytics platforms, enabling ATS vendors to position their platform as the hub of a broader HR technology ecosystem. Oracle's cloud services revenue growth of 21% in Q1 2025 reflects the structural enterprise shift toward subscription cloud consumption.

Data Analytics and Workforce Intelligence

Advanced reporting dashboards provide real-time visibility into recruitment funnel metrics – application-to-hire conversion rates, source-of-hire efficiency, diversity pipeline composition, and cost-per-hire tracking. Workforce planning modules use historical ATS data combined with business growth projections to forecast future talent demand by skill category, geography, and time horizon. Predictive analytics models assess offer acceptance probability and first-year retention likelihood using behavioral and assessment data.

Security, Compliance, and Data Governance

Enterprise ATS platforms have invested significantly in security and compliance infrastructure in response to GDPR, CCPA, and emerging AI regulation requirements. Modern platforms support candidate consent management, automated data retention scheduling, right-to-erasure workflows, and audit trail generation for regulatory review. IBM's sale of its talent acquisition suite to Infinite Computer Solutions in October 2024 highlighted the commercial pressure on vendors to maintain enterprise-grade data security certification across multiple jurisdictions.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Deployment Mode | Cloud | 53.8% | 2025 |

| Organization Size | Large Enterprises | 67.1% | 2025 |

| Component | Software | 60.8% | 2025 |

| End-User | IT and Telecommunication | 27.9% | 2025 |

| Region | North America | 37.1% | 2025 |

By Deployment

Cloud deployment commands a 53.8% majority share in the global applicant tracking system market in 2025, reflecting the industry-wide standardization of SaaS delivery as the preferred ATS architecture. Cloud ATS benefits from lower total cost of ownership – eliminating on-premises server infrastructure investment – faster implementation timelines of weeks versus months for on-premises, and the ability to access continuous feature updates without software upgrade projects.

To access detailed market analysis, Request Sample

On-premises at 46.2% in 2025 retains relevance in highly regulated industries, including government, defense, and financial services, where data sovereignty requirements mandate local data storage and restrict cloud hosting across national borders. Large enterprises with substantial IT infrastructure and internal development capabilities also favor on-premises deployments for the greater customization control they afford. On-premises growth is expected to decelerate to below 4% CAGR through 2034 as cloud migration accelerates across all verticals.

By Organization Size

Large enterprises accounted for 67.1% of global ATS revenue in 2025, driven by high recruitment volumes, multi-site operations, and complex integrations with HRIS, payroll, and assessment tools. Enterprise deployments often involve SAP or Workday HRIS, background screening, video interviews, and skills assessments, with contracts ranging from USD 50,000 to 500,000+ annually.

Small and Medium-sized Enterprises represent 32.9% of the market but are the fastest-growing segment (~12% CAGR through 2034). Platforms like Zoho Corporation and ApplicantStack offer affordable, easy-to-deploy solutions, with free tiers and integrations with major job boards, enabling small teams to automate hiring without enterprise IT resources.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

37.1% |

Digital-first enterprises, EEOC/OFCCP compliance mandates, leading ATS vendor ecosystem, and high-volume enterprise hiring |

|

Europe |

24.6% |

GDPR compliance-driven ATS adoption, multi-language requirements, SME digitization, EU AI Act provisions shaping product roadmaps |

|

Asia-Pacific |

21.8% |

India's IT sector expansion, enterprise digitization in China and SE Asia, growing MNC presence, and rising cloud penetration |

|

Latin America |

9.2% |

Expanding mid-market, rising cloud penetration, and cross-border hiring growth in Brazil, Mexico, and Colombia |

|

Middle East & Africa |

7.3% |

Saudi Vision 2030 nationalization policies, increasing HR digitization, and growing GCC enterprise demand |

North America leads the global applicant tracking system market with 37.1% share in 2025, driven by Fortune 500 enterprises, vendor headquarters (Workday, Oracle, iCIMS, Greenhouse), and strict regulations (EEOC, OFCCP, CCPA). Europe holds 24.6%, where GDPR compliance and the EU AI Act are key purchasing drivers, with Germany, the UK, and France as the largest markets.

Asia-Pacific accounts for 21.8% and is the fastest-growing region (~10% CAGR through 2034), led by India’s IT sector, China’s tech modernization, Southeast Asia’s expanding industries, and Japan’s workforce challenges; local vendors like Zoho Corporation compete in the SME segment. Latin America holds 9.2%, driven by Brazil, Mexico, and Colombia, with cloud adoption and cross-border hiring fueling demand. Middle East & Africa at 7.3% grows steadily, supported by Saudi Arabia’s Vision 2030 and HR digitization in GCC enterprises.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Workday, Inc. |

Workday Recruiting |

Leader |

End-to-end HCM+ATS, AI talent rediscovery, Spring 2025 350+ enhancements |

|

Oracle Corporation |

Oracle Recruiting Cloud |

Leader |

ERP-native cloud HCM, 25 languages, 150+ country compliance, 21% cloud growth Q1 2025 |

|

SAP SE |

SAP SuccessFactors |

Leader |

ERP-native ATS, dominant EMEA presence, manufacturing, and public sector strength |

|

iCIMS |

iCIMS Talent Cloud |

Challenger |

AI-driven candidate search, 4,000+ clients, 180 countries, 2025 Summer Release |

|

Greenhouse Software |

Greenhouse ATS |

Challenger |

Structured hiring methodology, DEI tools, Real Talent AI fraud detection (2025) |

|

SmartRecruiters |

SmartRecruiters ATS |

Challenger |

Global-first platform, compliance-driven, multi-language career sites |

|

Jobvite |

Jobvite ATS |

Challenger |

Social recruiting, mobile-first, candidate relationship management |

|

Zoho Corporation |

Zoho Recruit |

Emerging |

Affordable SME-focused ATS, built-in CRM, multi-board job posting |

|

ClearCompany |

ClearCompany ATS |

Emerging |

SME-oriented structured hiring, performance management integration |

|

ApplicantStack |

ApplicantStack ATS |

Emerging |

Small business ATS, job posting automation, low-cost entry-level platform |

The global applicant tracking system market has a barbell structure. At the enterprise level, Workday, Oracle, and SAP SuccessFactors dominate through integrated HCM suites, while iCIMS and Greenhouse compete as specialized challengers. The SME segment is highly fragmented, with vendors like Zoho Corporation, ApplicantStack, and ClearCompany serving niche sub-segments. Mid-market consolidation, exemplified by IBM’s 2024 sale of its talent acquisition suite to Infinite Computer Solutions, highlights ongoing M&A activity reshaping the landscape.

Key Company Profiles

Workday, Inc.

Workday offers Workday Recruiting as a core module of its unified Human Capital Management suite, providing end-to-end talent acquisition capabilities on a single data model shared with Workday HCM, Learning, and Payroll. The platform is the market-leading enterprise ATS for large and mid-sized enterprise deployments globally.

-

Product Portfolio: Workday Recruiting, Workday Skills Cloud, Workday People Analytics, VNDLY Contingent Workforce Management.

-

Recent Developments: In March 2025, Workday rolled out its Spring 2025 Release, featuring over 350 product enhancements across HR and finance, with AI-powered talent rediscovery, personalized onboarding experiences, and intelligent job recommendations as key ATS upgrades.

-

Strategic Focus: Workday's strategy centers on deepening AI capability across its entire HCM platform, with recruiting intelligence as a primary investment area. The company is expanding its Skills Cloud as a cross-platform competency framework, positioning Workday Recruiting as the data layer connecting talent acquisition, performance, learning, and succession planning on a unified talent intelligence architecture.

Oracle Corporation

Oracle Recruiting is a core component of Oracle Cloud HCM, serving enterprise clients globally with AI-assisted candidate matching, mobile-optimized candidate experiences, and deep integration with Oracle's ERP and payroll ecosystems. Oracle's cloud business is the fastest-growing segment of the company.

- Product Portfolio: Oracle Recruiting Cloud, Oracle HCM Cloud, Oracle Talent Management, Oracle Workforce Management.

- Recent Developments: In April 2025, Oracle was named a Leader in the 2025 Gartner Magic Quadrant for Talent Acquisition (Recruiting) Suites for Oracle Fusion Cloud Recruiting and Oracle Fusion Cloud Recruiting Booster.

- Strategic Focus: Oracle's ATS strategy leverages its dominant ERP installed base to cross-sell Oracle Recruiting to existing Oracle Fusion Cloud HCM customers. The company is investing in AI-powered talent intelligence features and expanding global compliance coverage across 150+ countries to support multinational enterprise requirements.

iCIMS

iCIMS Talent Cloud is a purpose-built enterprise ATS platform serving over 4,000 customers across 180 countries. iCIMS is one of the largest independent ATS vendors by customer count, occupying a strong position in the US large enterprise and mid-enterprise market.

-

Product Portfolio: iCIMS Talent Cloud (ATS + CRM), iCIMS Video Studio, iCIMS Scheduling, iCIMS Apply Network.

-

Recent Developments: In July 2025, the iCIMS 2025 Summer Release introduced AI-driven candidate search, SEO and translation assistants for global career sites, improved interview scheduling and feedback tools, and expanded growth in the iCIMS Apply Network across employer and candidate interfaces.

-

Strategic Focus: iCIMS's strategy focuses on AI capability depth within a best-of-breed talent acquisition platform, avoiding HCM suite expansion to maintain specialist positioning. The iCIMS Apply Network and ecosystem integrations with 700+ HR technology partners are central to its platform differentiation strategy.

Market Concentration Analysis

The global applicant tracking system market exhibits a bi-modal concentration structure. At the enterprise tier, the top five vendors – Workday, Oracle, SAP SuccessFactors, iCIMS, and Greenhouse – collectively account for an estimated 55–60% of enterprise ATS revenue in 2025. This concentration reflects the high switching costs associated with enterprise ATS implementations, the strategic advantage of HCM suite vendors over standalone platforms in procurement bundling, and the significant multi-year implementation investments that create structural customer retention.

The small and medium-sized enterprises market remains highly fragmented globally, with a large number of competing vendors across regions and verticals. Mid‑market consolidation is underway, for example, Infinite Computer Solutions acquires IBM’s Talent Acquisition Suite (including BrassRing) to expand its HR software portfolio— illustrating M&A pressure on standalone mid‑tier ATS providers. This dynamic of consolidation at the enterprise level and fragmentation at the SME level is expected to persist through 2030 before AI‑native ATS entrants begin reshaping the competitive landscape.

Investment & Growth Opportunities

Fastest-Growing Segments

AI-powered ATS is the fastest-growing market segment, projected at ~14.5% CAGR through 2034. Bullhorn’s Amplify suite shows strong early results, with a 51% increase in job submissions, 22% higher fill rates, and 85% candidate satisfaction, highlighting the value of AI-native ATS. The SME segment, growing at ~12% CAGR by customer count, is the fastest-growing user base.

Emerging Market Expansion

India, Indonesia, Brazil, Saudi Arabia, and the UAE are key greenfield markets for ATS growth through 2034. India’s IT sector alone employs over 5 million professionals, creating a large enterprise ATS opportunity. Expansion of cloud infrastructure by AWS, Microsoft, and Google in Asia‑Pacific and the Middle East is lowering adoption barriers, while local compliance and language requirements favor vendors with regional presence.

Venture and Strategic Investment Trends

Private equity and strategic investments highlight confidence in ATS's growth. Workday is expanding AI and skills intelligence, while Oracle’s 21% cloud revenue growth shows strong returns on HCM investments. Adjacent areas—skills intelligence, candidate experience analytics, diversity data, and AI interview tools—offer acquisition opportunities for ATS vendors aiming to broaden their offerings.

Future Market Outlook (2026-2034)

The global applicant tracking system market is forecast to expand from USD 3.14 Billion in 2025 to USD 6.35 Billion by 2034 at a CAGR of 8.14%, representing a near-doubling of market value underpinned by cloud adoption acceleration, AI capability integration across all price tiers, and expanding geographic penetration in high-growth emerging markets. The market is entering a phase where ATS technology is transitioning from a recruitment operational tool to a strategic talent intelligence platform embedded in enterprise workforce planning.

By 2034, the applicant tracking system market will evolve from structured hiring tools into predictive talent intelligence platforms. Generative AI will become a baseline feature by 2027–2028, shifting competition toward data quality, workflow depth, and customer success. HCM suite consolidation will reduce standalone ATS adoption in enterprises, while AI-native, no-code, voice-first ATS startups will disrupt the SME segment from 2026. The market will consolidate into three tiers: integrated HCM suites like Workday, Oracle, and SAP for enterprises, specialist talent platforms such as iCIMS, Greenhouse, and SmartRecruiters for mid-enterprises, and generative AI-first platforms targeting Small and Medium-sized Enterprises.

Research Methodology

Primary Research

Primary research encompassed structured interviews with HR technology industry stakeholders, including ATS product directors, enterprise HR technology buyers, talent acquisition leaders, staffing industry executives, implementation consultants, and institutional investors in HR technology. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments across all major geographic regions.

Secondary Research

Secondary sources include CareerPlug's 2025 Candidate Experience Report, Workday Investor Relations fiscal 2025 results, Oracle Q1 2025 earnings disclosures, Gartner HR Technology Hype Cycle 2024, SHRM Talent Acquisition research publications, LinkedIn Global Talent Trends 2025, company annual reports, SEC filings, and trade publications including HR Dive, Recruiting Daily, and ERE Media. Industry conferences, including HR Tech Conference 2024 and Bullhorn Engage Boston 2025, provided primary market intelligence inputs.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, enterprise digital transformation adoption curves by region, HR technology penetration rates by organization size, and historical applicant tracking system market evolution patterns from 2015 to 2025. Scenario analysis covering base, optimistic, and conservative forecasting cases was performed to account for macroeconomic uncertainty and technology adoption rate variance.

Applicant Tracking System Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Deployments Covered | On-premises, Cloud |

| Organization Sizes Covered | Small and Medium-sized Enterprises, Large Enterprises |

| Components Covered | Software, Services |

| End-Users Covered | BFSI, IT and Telecommunications, Government and Public Sector, Retail, Manufacturing, Healthcare and Life Sciences, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Argentina, Colombia, Chile, Peru, Turkey, Saudi Arabia, Iran, United Arab Emirates |

| Companies Covered | Workday, Inc., Oracle Corporation, SAP SE, iCIMS, Greenhouse Software, SmartRecruiters, Jobvite, Zoho Corporation, ClearCompany, ApplicantStack, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the applicant tracking system market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global applicant tracking system market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the applicant tracking system industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Applicant Tracking System Market Report

The global applicant tracking system market was valued at USD 3.14 Billion in 2025, driven by growing demand for automated recruitment, cloud adoption, and AI-powered talent acquisition tools.

The market is projected to reach USD 6.35 Billion by 2034, growing at a CAGR of 8.14% during 2026-2034, driven by cloud expansion, AI integration, and emerging market SME adoption.

Cloud deployment leads with a 53.8% share in 2025, driven by lower total cost of ownership, faster implementation, and continuous feature updates through SaaS delivery models.

Large enterprises account for 67.1% of ATS revenue in 2025, reflecting their high hiring volumes, complex HCM integration requirements, and multi-geography recruitment operational needs.

North America dominates with a 37.1% share in 2025, anchored by technology-mature enterprises, leading ATS vendors headquartered in the region, and strict EEOC compliance requirements.

Key drivers include recruitment automation demand, AI-powered candidate screening, remote work normalization, HR compliance requirements, and cloud technology cost and accessibility advantages.

Asia-Pacific is the fastest-growing, projected at approximately 10% CAGR through 2034, driven by India's IT sector, China's enterprise digitization, and rising SME cloud adoption across Southeast Asia.

Leading companies include Workday, Oracle, SAP SE, iCIMS, Greenhouse Software, SmartRecruiters, Jobvite, Zoho Corporation, ClearCompany, and ApplicantStack.

AI enables resume parsing, chatbot pre-screening, bias detection, predictive candidate scoring, and talent rediscovery, reducing time-to-fill and improving hiring quality at scale across all organization types.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade