Asia Pacific Metal Casting Market Size, Share, Trends and Forecast by Process, Material Type, End Use, Component, Vehicle Type, Electric and Hybrid Type, Application, and Country, 2026-2034

Asia Pacific Metal Casting Market Summary:

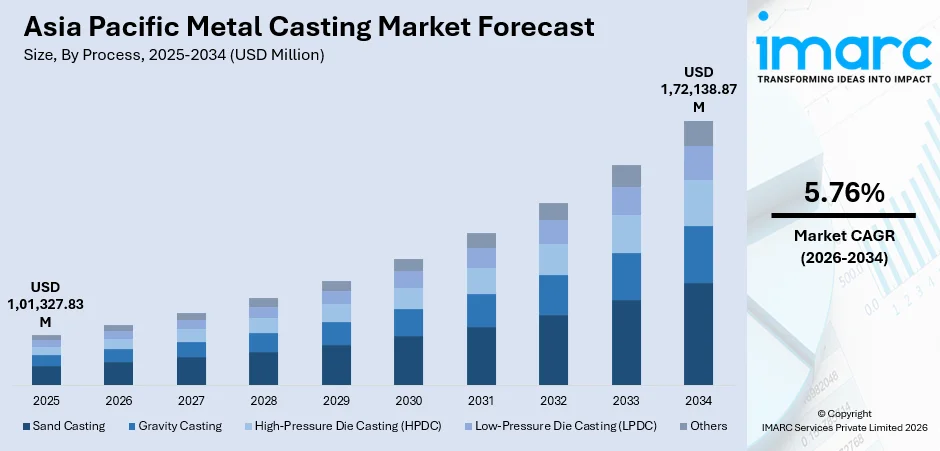

The Asia Pacific metal casting market size was valued at USD 1,01,327.83 Million in 2025 and is projected to reach USD 1,72,138.87 Million by 2034, growing at a compound annual growth rate of 5.76% during 2026-2034.

The Asia Pacific metal casting market is experiencing robust expansion driven by rapid industrialization, surging automotive production, and extensive infrastructure development across the region. Growing adoption of lightweight casting materials for electric and hybrid vehicles, coupled with advancements in high-pressure die casting and digital foundry technologies, is reshaping manufacturing capabilities. Government initiatives promoting domestic manufacturing, expanding construction activities, and rising demand for precision-engineered components across diverse industrial applications are further strengthening the Asia Pacific metal casting market share.

Key Takeaways and Insights:

- By Process: Sand casting dominates the market with a share of 45% in 2025, driven by its versatility, cost-effectiveness, and ability to produce large and complex components across diverse industrial applications.

- By Material Type: Cast iron holds the largest market share at 38% in 2025, supported by its exceptional strength, durability, and widespread use in automotive engine blocks, industrial machinery, and construction applications.

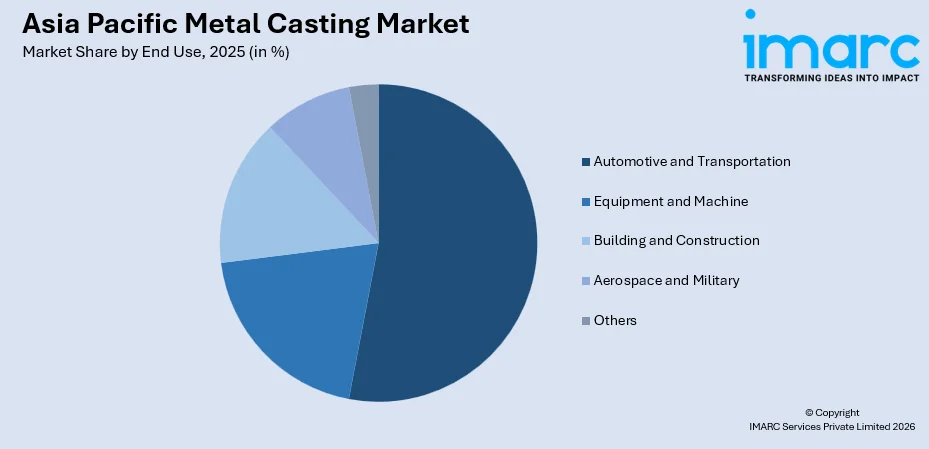

- By End Use: Automotive and transportation lead the market with a 53% share in 2025, fueled by growing vehicle production, demand for lightweight components, and the rapid expansion of electric and hybrid vehicle manufacturing.

- By Component: Cylinder head accounts for the largest share at 22% in 2025, owing to its critical role in engine performance and the consistent demand for both internal combustion and hybrid engine architectures.

- By Vehicle Type: Passenger cars represent the leading segment with a 68% share in 2025, reflecting strong consumer demand and rising vehicle ownership across major Asia Pacific economies.

- By Electric and Hybrid Type: Hybrid electric vehicles hold the largest share at 46% in 2025, driven by favorable government policies and growing consumer preference for fuel-efficient hybrid powertrains.

- By Application: Engine parts dominate with a 44% share in 2025, supported by sustained production of internal combustion and hybrid vehicles requiring precision-cast engine components.

- Key Players: The Asia Pacific metal casting market is moderately fragmented, with leading manufacturers investing in advanced casting technologies, expanding production capacity, forming strategic partnerships, and diversifying product portfolios to strengthen market positioning across automotive and industrial segments.

To get more information on this market Request Sample

The Asia Pacific metal casting market is advancing steadily as the region consolidates its position as the global hub for automotive manufacturing, industrial production, and infrastructure development. Countries such as China, India, Japan, and South Korea are driving demand for both ferrous and non-ferrous cast components across a wide range of applications. The transition toward electric mobility is creating significant demand for lightweight aluminum and magnesium castings, particularly for battery housings, motor cases, and structural vehicle parts. For instance, in March 2025, Ryobi Limited introduced an ultra-large die casting machine with a clamping force of 6,500 tons at its Kikugawa Plant in Shizuoka Prefecture, Japan, enabling prototype manufacturing of large automobile chassis parts and structural components. Rising investments in smart foundry technologies, sustainable casting practices, and regional manufacturing capacity are positioning the market for sustained long-term growth.

Asia Pacific Metal Casting Market Trends:

Rising Adoption of Mega-Casting and Integrated Die Casting Technologies

Asia Pacific is witnessing a significant shift toward mega-casting and integrated die casting, particularly for electric vehicle structural components. Chinese automakers including NIO, Xpeng, and Zeekr have adopted gigacasting for rear floor modules using presses exceeding tons of clamping force. Equipment manufacturers such as LK Technology and Yizumi have reported strong demand for ultra-high-tonnage machines. This trend is reducing component counts, cutting assembly time, and enabling lighter vehicle architectures, supporting Asia Pacific metal casting market growth. In 2025, UBE Machinery Corporation, Limited, the main entity of the UBE Group's machinery sector, has increased its range of die casting machines capable of executing giga casting, a die casting method that seamlessly molds body structure components for battery electric vehicles (BEVs), among others, utilizing aluminum alloy.

Growing Demand for Lightweight Aluminum and Magnesium Castings

The shift toward vehicle lightweighting is accelerating demand for aluminum and magnesium die castings across the region. Automakers are replacing traditional steel and iron components with advanced aluminum alloys to improve fuel efficiency and battery range in electric vehicles. This is being driven by expanding EV production and tightening emission standards across the region. In 2025, GDCTECH organized a significant global conference on Aluminum and Magnesium Die Casting Technology from December 4 to 6, 2025, in Pune. The three-day large-scale event will unite industry leaders, specialists, and innovators for the sharing of ideas, technological progress, and collaborative prospects.

Integration of Industry 4.0 and Smart Foundry Technologies

Asia Pacific foundries are increasingly integrating digital technologies such as casting simulation software, AI-driven quality control, and IoT-enabled predictive maintenance to improve production efficiency. These technologies are reducing cast defects, improving mold design accuracy, and enabling more consistent, sustainable manufacturing across regional foundries. In 2025, GlobalFoundries (GF) India effectively conducted its premier technical conference, TeknIka 2025, highlighting the firm’s India Foundry Connect Program. Aimed at expediting the transition from design to production for India's fabless semiconductor startups, the program offers access to state-of-the-art Product Design Kits (PDKs), GlobalShuttle™ Multi Project Wafer (MPW) fabrication services, IP libraries, and engineering support.

Market Outlook 2026-2034:

The Asia Pacific metal casting market is positioned for sustained growth, underpinned by robust automotive manufacturing, expanding EV adoption, and rising infrastructure investments. The market generated a revenue of USD 1,01,327.83 Million in 2025 and is projected to reach a revenue of USD 1,72,138.87 Million by 2034, growing at a compound annual growth rate of 5.76% during 2026-2034. Increasing domestic manufacturing capabilities, advancing foundry digitalization, and supportive government policies are expected to drive higher revenue streams and foster a more competitive, innovative, and sustainable casting landscape across the region.

Asia Pacific Metal Casting Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Process |

Sand Casting |

45% |

|

Material Type |

Cast Iron |

38% |

|

End Use |

Automotive and Transportation |

53% |

|

Component |

Cylinder Head |

22% |

|

Vehicle Type |

Passenger Cars |

68% |

|

Electric and Hybrid Type |

Hybrid Electric Vehicles (HEV) |

46% |

|

Application |

Engine Parts |

44% |

Process Insights:

- Sand Casting

- Gravity Casting

- High-Pressure Die Casting (HPDC)

- Low-Pressure Die Casting (LPDC)

- Others

Sand casting leads the market with a revenue share of 45% of the total Asia Pacific metal casting market in 2025.

Sand casting continues to hold a dominant position in the Asia Pacific metal casting market due to its versatility, low tooling costs, and ability to accommodate a wide range of metals and component sizes. The process is particularly favored for producing large and complex parts for automotive, industrial machinery, and construction applications. Its adaptability to both ferrous and non-ferrous metals makes it an essential method for mass production and custom manufacturing. Furthermore, the recyclability of sand used in the process aligns with growing sustainability goals across the region.

The expanding infrastructure development and industrial machinery sectors across China, India, and Southeast Asia are driving consistent demand for sand-cast components. Sand casting is widely used for producing engine blocks, pump housings, valve bodies, and structural parts that require high strength and durability. As governments invest in transportation networks, energy systems, and urban development, the need for reliable and cost-effective cast components produced through sand casting is expected to remain strong throughout the forecast period.

Material Type Insights:

- Cast Iron

- Aluminum

- Steel

- Zinc

- Magnesium

- Others

Cast iron leads with a share of 38% of the total Asia Pacific metal casting market in 2025.

Cast iron remains the most widely used material in the Asia Pacific metal casting market, valued for its excellent castability, wear resistance, and mechanical strength. The material is extensively utilized in the production of automotive engine components, industrial machinery parts, and construction hardware. Its ability to absorb vibrations and withstand high temperatures makes it ideal for engine blocks, brake discs, and heavy-duty industrial applications. The well-established supply chain for cast iron across the region further supports its continued market leadership.

Despite growing interest in lightweight materials like aluminum and magnesium, cast iron continues to be essential for applications demanding high durability and structural integrity. The material's cost-effectiveness compared to non-ferrous alternatives ensures strong demand from price-sensitive markets in India and Southeast Asia. Moreover, hybrid vehicles that retain internal combustion engines alongside electric drivetrains continue to require cast iron components, sustaining demand even as the automotive sector transitions toward electrification.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Automotive and Transportation

- Equipment and Machine

- Building and Construction

- Aerospace and Military

- Others

Automotive and transportation exhibit a clear dominance with a 53% share of the total Asia Pacific metal casting market in 2025.

The automotive and transportation sector is the primary driver of metal casting demand in Asia Pacific, supported by the region's position as the world's largest vehicle production hub. Countries like China, Japan, India, and South Korea collectively produce a significant share of global automobiles, generating massive demand for cast components including engine blocks, transmission cases, cylinder heads, and structural parts. The rapid growth of electric and hybrid vehicle manufacturing is further expanding the scope of casting applications.

The increasing focus on vehicle lightweighting and fuel efficiency is reshaping casting requirements, with automakers increasingly turning to advanced aluminum and magnesium die castings for structural and powertrain components. Government policies promoting domestic auto manufacturing, such as India's Production Linked Incentive scheme with a budgetary outlay of INR 25,938 crore for advanced automotive technology products, are further boosting demand for precision-cast automotive components across the region.

Component Insights:

- Alloy Wheel

- Clutch Casing

- Cylinder Head

- Cross Car Beam

- Crank Case

- Battery Housing

- Others

Cylinder head leads with a share of 22% of the total Asia Pacific metal casting market in 2025.

Cylinder heads remain a critical cast component in the automotive sector, essential for sealing combustion chambers and housing intake and exhaust valves. Their complex geometry and demanding performance requirements make casting the preferred manufacturing method. In Asia Pacific, the sustained production of internal combustion engine vehicles alongside growing hybrid vehicle volumes ensures continued strong demand for precision-cast cylinder heads made from both aluminum and cast iron alloys.

As the automotive industry transitions toward electrification, hybrid powertrains that combine conventional engines with electric motors continue to require high-quality cylinder heads. This dual demand from both traditional and hybrid vehicle segments supports the cylinder head component's market leadership. Foundries are investing in advanced casting techniques such as low-pressure and gravity casting to produce cylinder heads with improved thermal efficiency, reduced weight, and enhanced durability to meet evolving emission and performance standards.

Vehicle Type Insights:

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

Passenger cars exhibit a clear dominance with a 68% share of the total Asia Pacific metal casting market in 2025.

Passenger cars form the largest vehicle type segment in the Asia Pacific metal casting market, driven by rising urbanization, increasing disposable incomes, and expanding consumer demand for personal mobility. China, Japan, India, and South Korea are among the world's top passenger vehicle producers and consumers, generating substantial demand for cast components including engine blocks, transmission housings, wheel hubs, and structural parts. The growing availability of affordable compact and mid-range vehicles is further supporting casting demand.

The ongoing electrification of passenger vehicles is creating new casting requirements, particularly for battery housings, motor cases, and lightweight structural components. Automakers are increasingly adopting aluminum die castings to reduce vehicle weight and extend battery range. The proliferation of hybrid passenger vehicles, which require both traditional engine castings and new electrified powertrain components, is further expanding the range of casting applications within this segment.

Electric and Hybrid Type Insights:

- Hybrid Electric Vehicles

- Battery Electric Vehicles

- Plug-In Hybrid Electric Vehicles

Hybrid electric vehicles lead with a share of 46% of the total Asia Pacific metal casting market in 2025.

Hybrid electric vehicles are the dominant segment within the electrified vehicle category, reflecting the transition strategy adopted by many Asia Pacific automakers who are gradually shifting from conventional to fully electric powertrains. HEVs require a comprehensive range of cast components for both their internal combustion engines and electric drivetrains, including cylinder heads, engine blocks, transmission cases, and electric motor housings. This dual requirement makes HEVs a particularly casting-intensive vehicle type.

Government incentives and emission regulations across Japan, South Korea, China, and India are encouraging the adoption of hybrid vehicles as a practical pathway toward cleaner mobility. Japanese automakers such as Toyota and Honda have been at the forefront of hybrid vehicle technology, driving demand for precision-cast aluminum and iron components. The growing consumer acceptance of HEVs as a bridge technology between conventional and fully electric vehicles is expected to sustain strong casting demand throughout the forecast period.

Application Insights:

- Body Assemblies

- Engine Parts

- Transmission Parts

- Others

Engine parts exhibit a clear dominance with a 44% share of the total Asia Pacific metal casting market in 2025.

Engine parts represent the largest application segment for metal castings in the automotive and transportation sector, encompassing critical components such as engine blocks, cylinder heads, intake manifolds, and exhaust components. The continued production of internal combustion and hybrid vehicles across Asia Pacific sustains strong demand for precision-cast engine parts. Foundries are employing advanced casting technologies to produce engine components with tighter tolerances, improved thermal performance, and reduced weight.

While the long-term shift toward battery electric vehicles may gradually reduce demand for traditional engine castings, the near-to-medium term outlook remains positive due to the sustained production of hybrid vehicles and the large installed base of conventional engine vehicles requiring replacement parts. Additionally, the growing complexity of hybrid engine architectures is driving demand for higher-value, more precisely engineered cast engine components, supporting revenue growth within this application segment.

Country Insights:

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

China is the dominant force in the Asia Pacific metal casting market, accounting for the largest share of regional output. As the world's largest automotive and machinery manufacturing hub, China's foundries produce vast quantities of both ferrous and non-ferrous castings for domestic and export markets. Government initiatives such as Made in China 2025 have facilitated foundry modernization, encouraging automation and green casting technologies.

Japan maintains technological leadership in precision casting, with strong research and development investments supporting innovation in high-pressure die casting and lightweight alloy development. The country's automotive and electronics industries drive demand for high-quality casting solutions.

India's metal casting market benefits from a growing automotive sector, large-scale infrastructure development, and a thriving foundry ecosystem. Government support through programs like Make in India and the PLI scheme for auto components is encouraging investment in advanced casting capabilities.

South Korea's casting market is supported by its robust automotive industry, with leading manufacturers investing in aluminum die casting to produce components for hybrid and electric vehicles.

Australia's casting industry serves mining, construction, and defense sectors, with growing interest in precision-engineered components for specialized industrial applications.

Indonesia is emerging as a competitive manufacturing destination, attracting foreign direct investment in casting facilities due to its strategic geographic location, growing domestic demand, and favorable labor costs.

Market Dynamics:

Growth Drivers:

Why is the Asia Pacific Metal Casting Market Growing?

Expanding Automotive Production and Electric Vehicle Manufacturing

The Asia Pacific region is the global epicenter of automotive manufacturing, with China, Japan, India, and South Korea collectively producing a dominant share of the world's vehicles. The rapid growth of electric and hybrid vehicle production is generating significant new demand for precision metal castings, particularly lightweight aluminum components for battery housings, motor cases, and structural parts. Automakers are increasingly investing in advanced die casting technologies to meet the requirements of next-generation vehicle architectures. The expanding electric vehicle ecosystem is fundamentally reshaping casting demand patterns. Manufacturers are transitioning from traditional iron-based castings to aluminum and magnesium alloys that reduce vehicle weight and improve energy efficiency. The proliferation of hybrid powertrains, which require both conventional engine components and electrified drivetrain parts, is further expanding the total addressable market for metal castings across the automotive value chain.

Large-Scale Infrastructure Development and Industrialization

Governments across Asia Pacific are investing heavily in infrastructure development, including transportation networks, energy systems, and urban construction projects. These initiatives are driving substantial demand for durable metal castings used in construction equipment, industrial machinery, pipes, valves, and structural components. China's New Infrastructure strategy and India's Bharatmala and Sagarmala programs are boosting procurement of heavy-duty cast components for roads, ports, and logistics networks. The ongoing industrialization across Southeast Asian economies, including Indonesia, Vietnam, and Thailand, is further expanding the market for metal casting products. Rising investments in manufacturing capacity, coupled with growing demand for industrial machinery and equipment, are creating new opportunities for foundries to supply precision-engineered cast components across diverse industrial applications throughout the region.

Supportive Government Policies and Manufacturing Incentives

Proactive government policies across Asia Pacific are strengthening domestic manufacturing capabilities and encouraging investment in advanced casting technologies. India's Production Linked Incentive scheme for the automobile and auto components sector, with a budgetary outlay of INR 25,938 crore, has attracted over INR 25,000 crore in committed capital investment, supporting the expansion of advanced automotive component manufacturing including casting operations. China's Made in China 2025 initiative continues to promote foundry modernization through automation, green technologies, and digital integration. Similarly, Thailand's Industry 4.0 strategy and Indonesia's efforts to attract foreign direct investment in manufacturing are encouraging capacity expansion and technological upgrades across the region's casting sector. These policy frameworks are helping to build more competitive, efficient, and sustainable foundry operations.

Market Restraints:

What Challenges the Asia Pacific Metal Casting Market is Facing?

Rising Raw Material Costs and Supply Chain Volatility

Fluctuating prices of key raw materials such as aluminum, iron ore, and alloy metals create cost uncertainties for foundries across Asia Pacific. Supply chain disruptions and geopolitical tensions can further exacerbate material availability challenges. These cost pressures strain profit margins, particularly for small and medium-sized foundries that lack the purchasing power to hedge against price volatility, limiting their ability to invest in capacity expansion and technology upgrades.

Stringent Environmental and Emission Regulations

Tightening environmental regulations are requiring foundries to invest significantly in pollution control systems, energy-efficient melting technologies, and waste management infrastructure. Compliance with evolving emission standards increases operational costs and capital expenditure requirements. Smaller foundries, particularly in developing economies, face challenges in meeting these regulatory demands, potentially leading to capacity constraints and consolidation within the industry.

Competition from Alternative Manufacturing Technologies

The metal casting industry faces growing competitive pressure from alternative manufacturing methods such as forging, machining, and additive manufacturing. Advanced composite materials and polymer-based solutions are increasingly being explored as substitutes for traditional cast metal components in select applications. These alternatives, combined with rising competition from emerging low-cost producers in Vietnam and Bangladesh, create pricing pressure and challenge established foundries to continuously innovate and move up the value chain.

Competitive Landscape:

The Asia Pacific metal casting market is moderately fragmented, with a mix of large multinational manufacturers and numerous regional foundries competing across diverse segments. Companies are focusing on expanding production capacity, investing in advanced die casting and simulation technologies, and forming strategic partnerships with automotive OEMs to secure long-term supply contracts. Competition is intensifying as manufacturers seek to differentiate through lightweight material expertise, digital foundry capabilities, and sustainability practices. Vertical integration strategies, including securing upstream access to raw materials and downstream machining and assembly services, are becoming increasingly important for maintaining competitive positioning. The ongoing transition toward electric vehicle components is prompting established players to diversify their product portfolios and invest in new casting technologies to capture emerging growth opportunities.

Asia Pacific Metal Casting Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Processes Covered | Sand Casting, Gravity Casting, High-Pressure Die Casting, Low-Pressure Die Casting, Others |

| Material Types Covered | Cast Iron, Aluminum, Steel, Zinc, Magnesium, Others |

| End Uses Covered | Automotive and Transportation, Equipment and Machine, Building and Construction, Aerospace and Military, Others |

| Components Covered | Alloy Wheels, Clutch Casing, Cylinder Head, Cross Car Beam, Crank Case, Battery Housing, Others |

| Vehicle Types Covered | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles |

| Electric and Hybrid Types Covered | Hybrid Electric Vehicles, Battery Electric Vehicles, Plug-In Hybrid Electric Vehicles |

| Applications Covered | Body Assemblies, Engine Parts, Transmission Parts, Others |

| Countries Covered | China, Japan, India, South Korea, Australia, Indonesia, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Asia Pacific Metal Casting Market Report

The Asia Pacific metal casting market size was valued at USD 1,01,327.83 Million in 2025.

The market is expected to grow at a compound annual growth rate of 5.76% during 2026-2034 to reach USD 1,72,138.87 Million by 2034.

Sand casting, holding the largest revenue share of 45%, remains the most widely used casting process in Asia Pacific due to its versatility, cost-effectiveness, ability to handle diverse metals, and suitability for producing large and complex components.

Key factors driving the Asia Pacific metal casting market include expanding automotive and EV production, large-scale infrastructure development, supportive government manufacturing policies, growing demand for lightweight components, and advancing foundry technologies.

Major challenges include rising raw material costs and supply chain volatility, stringent environmental and emission regulations, competition from alternative manufacturing technologies, skilled labor shortages, and pricing pressure from emerging low-cost producers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)