Asia Pacific Online Gambling Market Size, Share, Trends and Forecast by Game Type, Device, and Country, 2026-2034

Asia Pacific Online Gambling Market Size, Share, Trends & Forecast (2026-2034)

The Asia Pacific online gambling market was valued at USD 26.11 Billion in 2025 and is projected to reach USD 59.75 Billion by 2034, exhibiting a CAGR of 9.15% during 2026-2034. Rising smartphone penetration, expanding live in-play sports betting, faster digital payment rails, and the emergence of esports wagering as the primary drivers shaping market growth. As per the National Sample Survey (NSS) conducted from January to March 2025 in India, around 85.5% of homes owned at least one smartphone.

Sports betting leads the game type segment at 46.3%, mobile dominates the device segment at 68.2%, and China commands 36.7% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 26.11 Billion |

|

Forecast Market Size (2034) |

USD 59.75 Billion |

|

CAGR (2026-2034) |

9.15% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

China (36.7%, 2025) |

|

Fastest Growing Region |

India (14.8%, 2025) |

|

Leading Game Type |

Sports Betting (46.3%, 2025) |

|

Leading Device |

Mobile (68.2%, 2025) |

The Asia Pacific online gambling market expanded from USD 16.85 Billion in 2020 to USD 26.11 Billion in 2025, supported by accelerated mobile internet adoption, growing acceptance of digital payments, and progressive regulation in Australia, Japan, and parts of Southeast Asia. Anchored at USD 40.46 Billion in 2030, the forecast to USD 59.75 Billion by 2034 reflects continued migration of wagering and gaming activity to licensed digital platforms across the region.

To get more information on this market, Request Sample

CAGR trajectories across game type, device, and region sub-segments show mobile and India growing materially faster than the overall 9.15% market CAGR, driven by smartphone-led access expansion, rapidly maturing digital payment infrastructure, and a young, sports-engaged player base.

Executive Summary

The Asia Pacific online gambling market is on a steady growth path from USD 16.85 Billion in 2020 to USD 59.75 Billion by 2034. Online wagering has shifted from a niche activity into a mainstream digital entertainment category across regulated markets such as Australia, New Zealand, and parts of Japan. Mobile distribution, faster payment rails, and expanding live in-play sports betting are encouraging households to engage through licensed digital channels rather than traditional retail outlets.

Sports betting dominates game type at 46.3% in 2025, supported by cricket, football, and esports demand across India, Australia, and Southeast Asia. As per IMARC Group, the Australia esports market size reached USD 145.8 Million in 2025. Mobile leads the device segment at 68.2%, fueled by widespread smartphone penetration and app-first product design. China commands 36.7% regional share, led by digital lottery activity and a sizeable grey market.

Key Market Insights

|

Insight |

Data |

|

Leading Game Type |

Sports Betting - 46.3% share (2025) |

|

Second Game Type |

Casino - 38.7% share (2025) |

|

Leading Device |

Mobile - 68.2% share (2025) |

|

Second Device |

Desktop - 24.5% share (2025) |

|

Leading Region |

China - 36.7% share (2025) |

|

Fastest Growing Region |

India - 14.8% share (2025) |

|

Top Companies |

Flutter Entertainment, Entain, Tabcorp, The Lottery Corporation Limited |

Key Analytical Observations Expanding on the Data Above:

- Sports betting at 46.3% is supported by widespread interest in cricket, football, basketball, and esports, with younger consumers gravitating to in-play and pre-match wagering on mobile apps over traditional retail outlets.

- Casino at 38.7% is sustained by live dealer formats, slots, and table game popularity, with operators improving streaming quality and localized content libraries to retain urban users.

- Mobile leadership at 68.2% is reinforced by rising internet penetration and deep smartphone adoption across the region. The China Internet Network Information Center (CNNIC) reported that by December 2024, the country alone had 1,108 Million internet users, providing a vast addressable base for licensed and unlicensed digital wagering platforms.

- Desktop at 24.5% is sustained by professional poker players, serious sports bettors, and live casino enthusiasts who prefer larger screens and stable home broadband connections for longer sessions.

- China at 36.7% reflects the region's vast internet user base, growing digital entertainment spending, and continued expansion of state-run online lottery products through the China Sports Lottery and China Welfare Lottery channels.

Asia Pacific Online Gambling Market Overview

Online gambling refers to wagering and gaming activities, including sports betting, casino games, poker, bingo, and lottery products, conducted via internet platforms or mobile applications. The Asia Pacific market spans highly regulated jurisdictions such as Australia and New Zealand, controlled frameworks in Japan and Singapore, and complex grey markets in China and India where activity occurs through offshore operators or evolving domestic rules.

The regional ecosystem links game and content developers, platform technology vendors, licensed operators, payment gateways and e-wallets, mobile network operators, marketing affiliates, regulators, and end consumers, together enabling the delivery of digital wagering products across mobile and web channels.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- Smartphone and Internet Penetration: Rising mobile broadband uptake, falling data tariffs, and 4G/5G rollout across India, Indonesia, and Vietnam are widening consumer access to licensed and offshore online gambling platforms.

- Live In-Play Sports Betting Expansion: Real-time wagering on cricket, football, and basketball is lifting session frequency and average bet sizes, with operators investing in low-latency streaming and instant settlement.

- Crypto and Digital Wallet Adoption: E-wallets, real-time bank transfers, and selective cryptocurrency rails are reducing payment friction in markets where card-based deposits face restrictions, supporting Asia Pacific online gambling market growth.

- Esports Betting Emergence: Tournament viewership, fantasy gaming, and skin-betting on titles are opening adjacent revenue streams for licensed sportsbooks across the region. The 2026 World Baseball Classic™, which Netflix secured exclusive streaming rights for in Japan, achieved a landmark record in March 2026. The live broadcast of the Japan vs. Australia match became the highest-viewed title on Netflix in Japan. World Baseball Classic matches on Netflix attracted 31.4M viewers across the country.

Market Restraints

- Regulatory and Legal Uncertainty: Many Asia Pacific jurisdictions criminalize or sharply restrict online gambling, creating fragmented operating environments and forcing operators to navigate licensing, advertising, and payment-processing rules market by market.

- Tax and Compliance Cost Pressure: India's GST Council imposed 28% Goods and Services Tax on the full face value of online money gaming deposits effective October 1, 2023, prompting several domestic real-money gaming operators to scale back operations or exit the market in subsequent quarters.

- Responsible Gambling Restrictions: Stricter advertising codes, deposit limits, self-exclusion mandates, and credit-card prohibitions in mature markets, such as Australia, raise compliance investment requirements and dampen near-term acquisition economics.

Market Opportunities

- Regulated Market Expansion: Continued evolution of regulated frameworks in Japan, the Philippines, and selected Southeast Asian markets is creating space for licensed operators to scale products, payment infrastructure, and responsible-play tools.

- Demographic Diversification: Younger, female, and senior demographic segments are increasingly engaging with social casino and skill-based gaming, opening differentiated product lines beyond traditional sports betting.

- Product and Technology Innovation: AI-driven personalization, automated risk management, and integrated live-streaming partnerships are enabling operators to differentiate the user experience while strengthening responsible-play safeguards.

Market Challenges

- Cross-Border Payment Friction: Restrictions on cross-border deposits, fluctuating banking policies, and currency conversion costs constrain operator scalability across multiple Asia Pacific jurisdictions.

- Player Protection Investment: Detecting and mitigating gambling-related harm requires sustained investment in behavioral analytics, age verification, and real-time intervention systems, raising operating cost intensity for licensed players.

- AML and KYC Compliance Burden: Tightening know-your-customer rules and anti-money-laundering reporting requirements increase compliance overheads and create barriers for newer, smaller market entrants.

Emerging Market Trends

1. Mobile-First Sports Betting Boom

Sportsbooks across the region are designing primarily for handheld devices, with simplified registration, streamlined deposits, and one-tap betting interfaces. App-first product design has overtaken traditional desktop experiences, supported by widespread mobile data availability and improved device affordability across emerging markets.

2. Live In-Play Wagering Goes Mainstream

Real-time betting during ongoing matches has become a default feature rather than a premium add-on. Operators are integrating low-latency live streams, instant odds updates, and quick-bet options to capture engaged audiences during peak sports calendars across cricket, football, and basketball.

3. Crypto and Digital Wallet Integration

Operators in the Asia Pacific online gambling market are increasingly supporting e-wallets, instant bank rails, and selective cryptocurrency deposits to navigate card-based restrictions and serve unbanked or underbanked players. In 2023, India had 217 Million e-wallet users, and this number is expected to increase at a CAGR of 23.9% from 2023 to 2027, reaching INR 472.6 Trillion (USD 5.7 Trillion) by 2027.

4. AI-Driven Personalization and Risk Engines

Machine learning (ML) is being embedded across customer journeys, from personalized odds boosts and tailored game recommendations to automated responsible-play interventions. These engines flag at-risk behaviors, tighten anti-fraud controls, and improve lifetime value for licensed operators across mature Asia Pacific markets.

Industry Value Chain Analysis

The Asia Pacific online gambling value chain spans six stages, from game and content development through end-user engagement and compliance monitoring. Platform integration, licensing, and payment infrastructure capture significant value, while marketing affiliates and regulatory frameworks govern downstream activity.

|

Stage |

Key Players / Examples |

|

Game & Content Development |

Game studios, casino software developers, sports data providers offering live odds, content, and probability feeds |

|

Platform & Technology Integration |

Sportsbook engine vendors, white-label platform providers, hosting and infrastructure firms, and KYC/AML solution suppliers |

|

Licensed Operators & Sportsbooks |

Regulated wagering and gaming operators offering branded sportsbook, casino, and lottery products via web and mobile apps |

|

Payment & KYC Providers |

Payment gateway operators, e-wallet providers, banking partners, and identity verification specialists |

|

Marketing & Affiliate Networks |

Performance marketing firms, sports media partners, affiliate aggregators, and search and social advertising channels |

|

End Use & Compliance |

Players, regulatory authorities, responsible-play support organizations, and dispute resolution bodies |

Vertically integrated operators that combine proprietary platforms, in-house data feeds, and licensed retail networks tend to achieve stronger margins and faster product iteration than those reliant on third-party platform providers in the Asia Pacific online gambling industry.

Technology Landscape in the Asia Pacific Online Gambling Industry

Mobile-First Platform Engineering

Lightweight Android and iOS applications, progressive web apps, and responsive HTML5 casino front-ends have become the default delivery model. Operators are investing in load balancing, regional content delivery networks, and lightweight design patterns to support smooth performance on lower-end devices common in emerging Asia Pacific markets.

Live Data, Odds, and Streaming Integration

Sub-second odds updates, live event tracking, and integrated low-latency video are central to in-play product differentiation. Suppliers are delivering enriched data feeds covering minor leagues, esports tournaments, and regional cricket events that resonate with Asia Pacific audiences.

AI for Personalization and Responsible Gambling

Recommendation engines tailor sports markets and casino games to individual preferences, while behavioral analytics identify problematic play patterns. Operators are pairing personalization with cooling-off prompts, deposit caps, and self-exclusion workflows to balance growth with player protection.

Payment, KYC, and Identity Infrastructure

Identity verification stacks combine document scanning, biometric checks, and database matches to comply with regional KYC norms. Operators are integrating multiple e-wallets, bank rails, and selective cryptocurrency options to widen funding flexibility while maintaining audit trails for regulators.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Game Type |

Sports Betting |

46.3% |

2025 |

|

Device |

Mobile |

68.2% |

2025 |

|

Country |

China |

36.7% |

2025 |

By Game Type

Sports betting commands a 46.3% share of the Asia Pacific online gambling market in 2025, supported by deep cultural engagement with cricket in South Asia, football in East and Southeast Asia, and Australian Football League and rugby in Oceania. Operators continue to invest in live in-play markets, micro-betting on individual events, and cash-out functionality to drive session frequency.

To access detailed market analysis, Request Sample

Casino at 38.7% in 2025 covers slots, table games, video poker, and live dealer formats. Live dealer studios designed for Asian audiences, often broadcasting from licensed jurisdictions in the Philippines, are bringing land-based casino experiences to mobile screens with localized presenters and game variants.

By Device

Mobile dominates with 68.2% share in 2025, reflecting the smartphone-first consumer base across Asia Pacific. Affordable Android handsets, mobile-data subscriptions, and operator-led app optimization have collectively shifted wagering activity from desktop to mobile across both mature and emerging markets.

Desktop at 24.5% in 2025 retains relevance among professional poker players, high-frequency sports bettors, and live casino enthusiasts who prefer larger displays, stable home broadband, and multi-table layouts. Operators continue to maintain feature-rich desktop clients alongside their mobile applications.

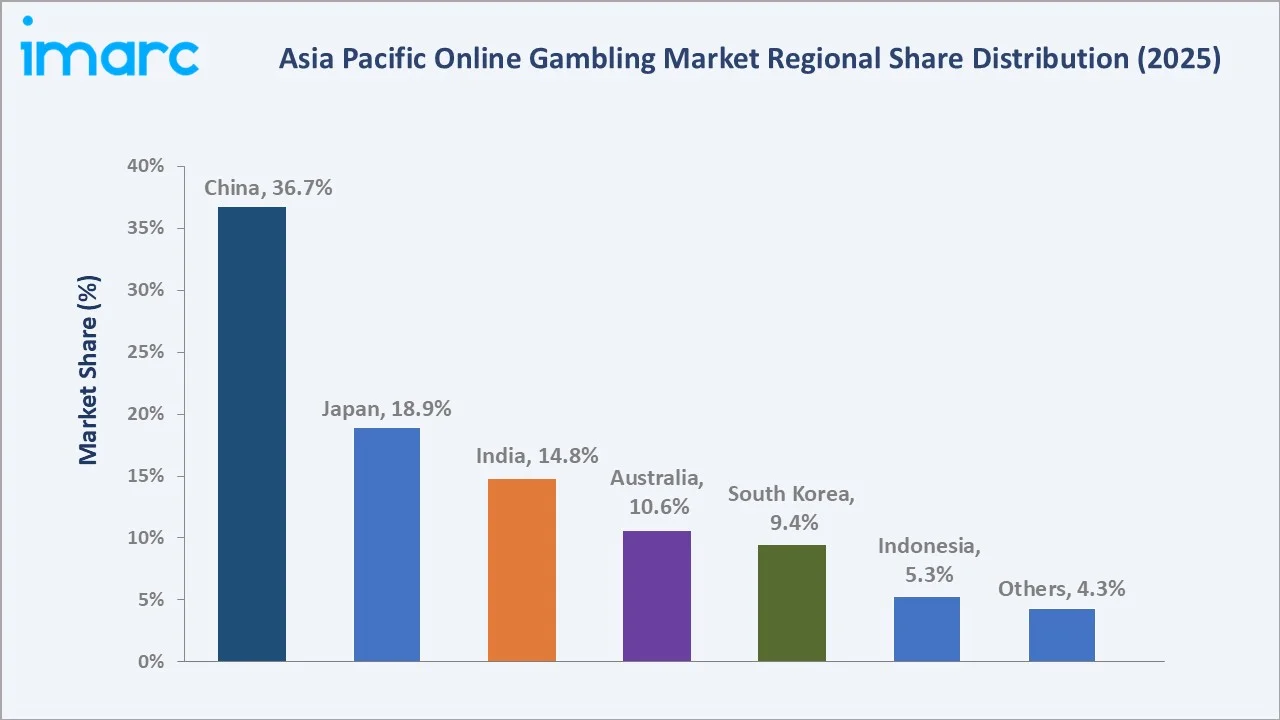

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

China |

36.7% |

Large internet user base, growing digital entertainment spend, and continued expansion of state-run online lottery channels |

|

Japan |

18.9% |

High disposable incomes, mature horse-racing online wagering systems, and an evolving regulatory framework around integrated gaming |

|

India |

14.8% |

Young demographic profile, low-cost mobile data, rising fantasy sports adoption, and active sports viewership across cricket and football |

|

Australia |

10.6% |

High smartphone penetration, established licensed operator base, mature regulatory environment, and strong wagering culture |

|

South Korea |

9.4% |

Strong digital infrastructure, popularity of esports and online lottery products, and high consumer purchasing power |

|

Indonesia |

5.3% |

Expanding internet access, large youth population, and increasing mobile commerce uptake supporting digital wagering interest |

|

Others |

4.3% |

Growing tourism economies, emerging digital payment systems, and improving regional connectivity supporting online entertainment uptake |

China at 36.7% leads the Asia Pacific online gambling market in 2025, supported by the world's largest online consumer base, established state lottery digitization, and a sizeable grey market for offshore wagering. Despite stringent regulations on private gambling, the region's scale and digital payment maturity sustain its leadership position.

India at 14.8% is the highest-growth region through 2034, driven by a young population, rising mobile data consumption, fantasy sports adoption, and broader regulatory clarity around skill-based gaming. Expanding digital payment adoption and increasing smartphone penetration are further supporting user engagement across online gaming platforms.

Competitive Landscape

The Asia Pacific online gambling market is moderately fragmented, with global wagering and gaming groups operating regional brands alongside domestic licensed operators. Brand strength, product depth, payment integration, and responsible-play capabilities are key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Flutter Entertainment |

Sportsbet |

Leader |

Multi-brand digital wagering portfolio, focus on scale and product breadth across regulated markets |

|

Entain |

Ladbrokes, Neds |

Leader |

Multi-jurisdictional regulated operations, omni-channel reach, and responsible-play investments |

|

Tabcorp |

TAB |

Challenger |

Australia-focused wagering, retail-digital integration, and regulated market specialization |

|

The Lottery Corporation Limited |

The Lott, Keno |

Challenger |

Online lottery and Keno digitization, large licensed retail-digital network, and recurring-revenue subscription products |

Key players include Flutter Entertainment, Entain, Tabcorp, and The Lottery Corporation Limited, among others.

Key Company Profiles

Flutter Entertainment

Flutter Entertainment is one of the world's largest sports betting and gaming operators, with its primary Asia Pacific exposure delivered through the market-leading Sportsbet brand in Australia.

- Product Portfolio: Sportsbet (Australia online wagering), with supporting global brands across the Group's wider international portfolio in regulated markets.

- Recent Developments: The company has continued to strengthen its digital wagering ecosystem through ongoing investments in platform technology, customer engagement features, and responsible gaming capabilities across regulated markets.

- Strategic Focus: Multi-brand digital wagering portfolio, focus on scale and product breadth across regulated markets, supported by deep investment in product technology and responsible-play capabilities.

Entain

Entain is a global sports betting, gaming, and interactive entertainment group operating multiple regional brands across Asia Pacific, with regulated activity in Australia and presence through proprietary technology and brand portfolios.

- Product Portfolio: Ladbrokes and Neds, supported by a proprietary technology stack.

- Recent Developments: The company IS investing in its wagering platforms through enhancements in live betting functionality, digital product innovation, and responsible gaming capabilities across its betting brands. These developments are aimed at improving user engagement, platform efficiency, and long-term customer retention in regulated online betting markets.

- Strategic Focus: Multi-jurisdictional regulated operations, omni-channel customer reach, and a focus on safer-gambling tools and compliance investment.

The Lottery Corporation Limited

The Lottery Corporation Limited operates licensed lottery and Keno gaming services through an extensive retail and digital distribution network. The company continues to strengthen customer engagement through digital platform expansion, mobile accessibility, and integrated gaming offerings.

- Product Portfolio: The Lott (umbrella brand for major draw games and instant scratch products) and Keno, distributed through licensed retail outlets, online platforms, and mobile applications, including subscription and syndicate products.

- Recent Developments: The company has continued to expand its online lottery business through stronger digital sales, broader subscription and syndicate offerings, and ongoing investments in mobile platforms and player-focused digital engagement capabilities.

- Strategic Focus: Online lottery and Keno digitization, large licensed retail-digital network, and recurring-revenue subscription products that anchor long-duration customer relationships.

Market Concentration Analysis

The Asia Pacific online gambling market is moderately fragmented, with the top operators (Flutter Entertainment, Entain, Tabcorp, and The Lottery Corporation Limited) in regulated jurisdictions accounting for a notable share of licensed online wagering activity.

Barriers to entry include licensing requirements in regulated markets, deep customer-acquisition spend in mature countries, technology platform investment, and the integrated payment, content, and risk-management infrastructure required to scale a sportsbook or casino product.

Consolidation is being driven by global operators acquiring or expanding regional footprints, technology platform partnerships, and cross-jurisdictional brand rollouts. Scale advantages in product engineering, payment integrations, and responsible-play tooling continue to reinforce the position of established players.

Investment & Growth Opportunities

Fastest-Growing Segments

Mobile at 68.2% expands faster than desktop at 24.5% through 2034, supported by smartphone-led access. Sports betting at 46.3% remains the largest game type segment, driven by strong cricket and football wagering activity.

Emerging Markets

India at 14.8% is the standout high-growth region, supported by young demographics and digital payment expansion. Indonesia, Vietnam, and the Philippines also represent material long-term opportunities as digital infrastructure and consumer purchasing power evolve.

Venture & Investment Trends

Capital is concentrated in mobile-first sportsbook platforms, AI-driven trading and risk-management engines, integrated payment and KYC stacks, and esports betting infrastructure. Strategic investment is also expanding into responsible-play technology and regional content production for live casino studios.

Future Market Outlook (2026-2034)

The Asia Pacific online gambling market is forecast to expand from USD 26.11 Billion in 2025 to USD 59.75 Billion by 2034 at a CAGR of 9.15%, adding roughly USD 33.64 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: continued mobile-led consumer migration to licensed digital channels; broader integration of esports and fantasy products into mainstream sportsbook portfolios; regulatory evolution in markets, such as India, Japan, and Thailand; and ongoing investment in AI-powered personalization and responsible-play tooling.

By 2034, mobile-first sports betting and live casino are expected to remain the dominant product categories, while regulated payment and identity infrastructure becomes a key differentiator for licensed operators across the Asia Pacific region.

Research Methodology

Primary Research

Primary research included structured interviews with senior executives at licensed wagering operators, sportsbook platform vendors, payment and KYC suppliers, regulators, and affiliate networks across Australia, Japan, India, and Southeast Asia, validating segment sizing, regional splits, and competitive dynamics.

Secondary Research

Secondary sources included regulatory filings, government statistical agency releases, central bank payments data, listed-operator annual and quarterly reports, investor presentations, and reputable business and trade publications covering the Asia Pacific gaming and wagering industry.

Forecasting Models

Market forecasts combined top-down and bottom-up modelling using internet and smartphone penetration, average revenue per active player, regulatory trajectories, and operator-level disclosures. Scenario analysis addressed regulatory tightening, tax shifts, and digital-payment evolution.

Asia Pacific Online Gambling Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Game Types Covered |

|

| Devices Covered | Desktop, Mobile, Others |

| Countries Covered | China, Japan, India, South Korea, Australia, Indonesia, Others |

| Companies Covered | Flutter Entertainment, Entain, Tabcorp, The Lottery Corporation Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Asia Pacific Online Gambling Market Report

The Asia Pacific online gambling market was valued at USD 26.11 Billion in 2025, supported by mobile-led adoption, sports betting demand, and digital payment expansion across the region.

The market is projected to grow at 9.15% CAGR from 2026 to 2034, reaching USD 59.75 Billion, driven by smartphone penetration, in-play betting, and esports wagering uptake.

Sports betting leads at 46.3% in 2025, supported by cricket, football, and basketball wagering across India, Australia, and Southeast Asia, with strong live in-play engagement.

Mobile dominates at 68.2% in 2025, fueled by smartphone-led access, app-first product design, and falling mobile data costs across the region's major consumer markets.

China leads at 36.7% in 2025, driven by its vast internet user base and digital lottery activity, while India at 14.8% is the fastest-growing region through 2034.

Leading players include Flutter Entertainment, Entain, Tabcorp, and The Lottery Corporation Limited, among others.

Smartphone penetration, app-first sportsbook design, faster mobile internet, and digital payment adoption are pushing wagering activity from desktop and retail to mobile channels.

E-wallets, real-time bank rails, and selective cryptocurrency options reduce payment friction in markets with card restrictions, supporting Asia Pacific online gambling market growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)