Asteroid Mining Market Size, Share, Trends and Forecast by Asteroid Type, Phase, Application, and Region, 2026-2034

Asteroid Mining Market Size and Share:

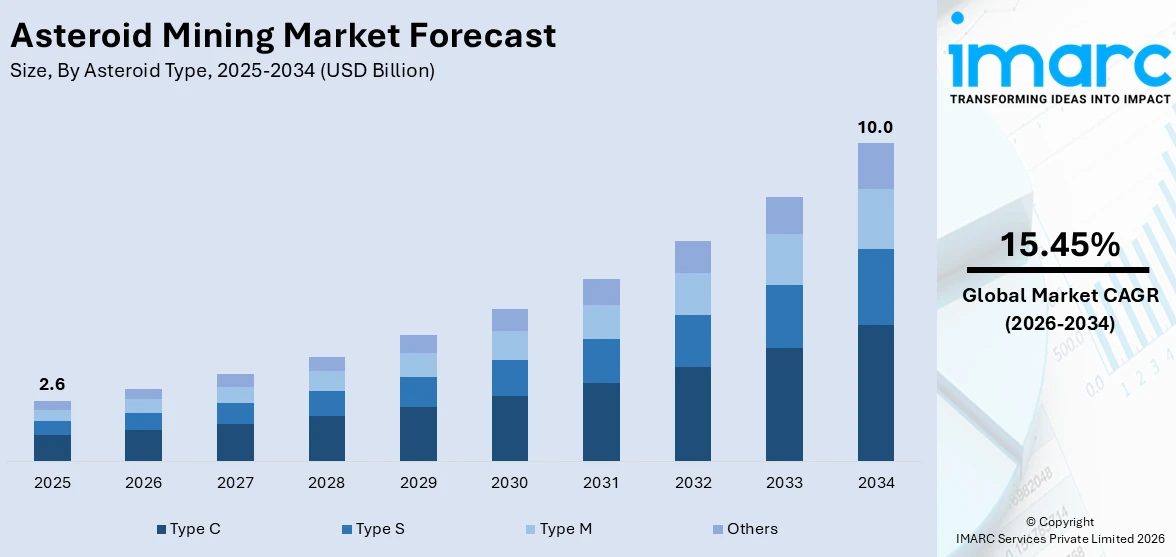

The global asteroid mining market size was valued at USD 2.6 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 10.0 Billion by 2034, exhibiting a CAGR of 15.45% from 2026-2034. North America currently dominates the market in 2025. At present, space exploration developments are largely propelling the market growth. Moreover, increased worldwide demand for rare earth elements (REEs) is a crucial factor impelling the market growth. Apart from this, the rise in private sector investment is expanding the asteroid mining market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 2.6 Billion |

|

Market Forecast in 2034

|

USD 10.0 Billion |

| Market Growth Rate 2026-2034 | 15.45% |

The asteroid mining industry is constantly transforming, driven by a number of dominant trends shaping its growth. One of the most crucial trends is the growing role of private firms in space exploration. These firms are constantly investing in research and development (R&D), sending missions, and refining technology to make asteroid mining advanced. Through cost reduction, increased autonomy in spacecraft, and better means of extracting resources, they are expanding the frontiers of what can be achieved in space mining. With private companies leading the way, the market is becoming increasingly competitive as new players enter and play their part in the development of asteroid mining technology.

To get more information on this market Request Sample

The market in the United States for asteroid mining is experiencing robust growth due to rising investments by the government and private enterprise participation. The government is constantly providing support to space exploration efforts by institutions such as NASA, which is working on new technologies and sending missions that are dedicated to asteroid exploration and resource mapping. In addition to government initiatives, private industry is investing heavily in asteroid mining, with companies consistently developing spacecraft technology and methods of resource recovery. Public and private investment combined is fueling the market asteroid mining market growth. The demand for rare earth elements and other strategic minerals is also a major driver. AstroForge, a company located in California, is propelling its ambitions to commercialize space mining with the inaugural private mission outside the Earth-moon system. Its spacecraft, Vestri, will attach to a secret near-Earth asteroid to evaluate the quality of its metals, such as cobalt, nickel, and precious metals. These resources are essential for the shift to clean energy, especially for battery and renewable energy systems. The mission, set to launch in October 2025, intends to assess the resources of the asteroid and ultimately extract and bring back one to two tons of materials to Earth.

Asteroid Mining Market Trends:

Technological Advancements in Space Exploration

Space exploration developments are largely propelling the market growth. Agencies and companies are continuously enhancing spacecraft technology, propulsion systems, and automated mining methods. They are evolving more effective approaches to exploit resources from asteroids using advanced robotics, machine learning (ML), and artificial intelligence (AI) to maneuver the complicated space environment. New technologies in spacecraft are facilitating cheaper, quicker missions to find and extract asteroids, making resource extraction progressively viable. These developments are making asteroid mining cheaper and less time-consuming, and thus more attractive to private companies and government space agencies. As technology advances, the industry is reaping the benefits of advances in spacecraft autonomy, deep-space communication networks, and resource recovery methods, which are facilitating long-term exploration and development of asteroid mining ventures. For instance, in 2025, NASA and private space companies will allocate $10 billion in funding to support AI-driven space advancement and launch machine-aided space exploration. This is expected to further improve space mining activities.

Increased Demand for Rare Earth Elements

One of the most important asteroid mining market trends is the increased worldwide demand for rare earth elements (REEs). With the growing electric vehicles (EVs), renewable energy technologies, and sophisticated electronics, the demand for REEs like lithium, cobalt, and nickel is growing. Asteroids contain these key materials in abundance, and corporations are increasingly looking for methods of extracting them from asteroids. By accessing asteroid resources, companies are seeking to decrease the reliance on mining on Earth, which is increasingly difficult as a result of environmental issues and limited availability. The rising dependence on technology and renewable energy is steadily generating more need for these vital materials, thereby increasing the economic potential of asteroid mining. Since this demand continues, additional investments are being made in R&D, which is moving at a faster pace to explore asteroids as a source of these resources. The IMARC Group stated that the global rare earth elements market size is projected to attain USD 37.06 Billion by 2033.

Growing Private Sector Investment

Private sector investment is playing an ever-more important role in offering a favorable asteroid mining market outlook. Venture capital companies and private firms are continuously investing in space exploration programs and understanding the long-term benefits of harvesting valuable resources from asteroids. Space startups and mature aerospace firms are creating strategic partnerships, working with governments, and leading innovative solutions to lower the expensive cost of space missions. These investments are facilitating the creation of the infrastructure necessary for asteroid mining, including launching spacecraft, creating mining operations, and processing resources in space. While private companies keep pouring in massive investments, the asteroid mining market is picking up speed, with new players joining the market and facilitating the large-scale viability of operations. Increased financial investment is speeding up technological advancements and bringing asteroid mining a step closer to being an industry that can operate commercially. In 2024, AstroForge, a startup from the US aiming to mine asteroids, secured $40 million to initiate its third mission in 2025, joining Intuitive Machines' IM-3 lunar mission.

Asteroid Mining Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global asteroid mining market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on asteroid type, phase, and application.

Analysis by Asteroid Type:

- Type C

- Type S

- Type M

- Others

Type C stands as the largest component in 2025, holding 73.2% of the market. Type C asteroids, referred to as carbonaceous asteroids, are some of the most frequently encountered types within the asteroid belt. Made mainly of carbon-heavy substances, silicates, and water, these asteroids are highly valuable for asteroid mining because of their plentiful resource possibilities. They are thought to be among the oldest traces of the solar system, consisting of primitive materials that can offer an understanding of the initial phases of planet formation. The carbon-based makeup of Type C asteroids suggests they might be abundant in water, which could be crucial for upcoming space missions as a resource for life support and rocket fuel via electrolysis. The possibility of obtaining valuable resources from Type C asteroids is considerable. They are recognized for having vital elements like carbon, nitrogen, and hydrogen, which may act as fundamental components for life or be utilized in different industrial uses.

Analysis by Phase:

- Spacecraft Design

- Launch

- Operation

Spacecraft design leads the market with 46.8% of market share in 2025. The design phase of the spacecraft focuses on defining the key goals and establishing the overall mission requirements for the spacecraft. This stage typically entails market segmentation according to mission type, including satellite launches, crewed missions, or deep-space exploration. It involves determining the spacecraft's abilities like payload capacity, propulsion mechanisms, and energy requirements. In this phase, mission planners and design firms examine existing technologies, the environmental factors of the intended location, and regulatory limitations. The mission profile and budget for the spacecraft are set, offering a clear pathway for future design endeavors. Important market players in this stage could consist of aerospace research institutions, government space organizations, and private space exploration companies. With the growth of space exploration, the need for tailored mission concepts is rising, especially in fields like asteroid mining.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

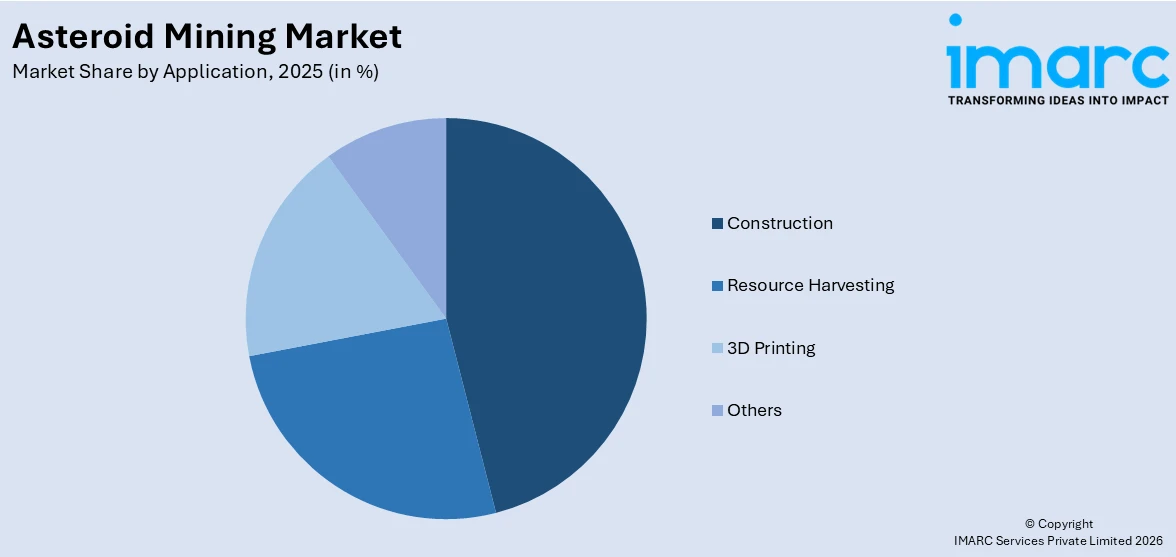

- Construction

- Resource Harvesting

- 3D Printing

- Others

The construction segment in the context of space applications is focused on the use of extraterrestrial materials to build infrastructure either on the Moon, Mars, or in orbit. Market segmentation in this area is primarily driven by advancements in construction technologies that allow for the use of local resources, such as lunar regolith or Martian soil, to create structures in space. This approach, known as in-situ resource utilization (ISRU), reduces the need for launching materials from Earth, significantly lowering costs.

Resource harvesting in space refers to the extraction of valuable materials from asteroids, the Moon, or other celestial bodies, which could be utilized for various industrial and energy purposes. The market segmentation in this area is driven by the increasing need for rare minerals, such as platinum, gold, and rare earth elements, which are critical for technology manufacturing and renewable energy sectors. Companies involved in space mining are focusing on developing efficient extraction and processing technologies to mine asteroids and lunar surfaces.

3D printing in space is becoming an increasingly important application, particularly for manufacturing components and tools on long-duration missions, such as those involving asteroid mining, construction on the Moon, or Mars exploration. Market segmentation in this field revolves around the ability to manufacture objects directly in space using available materials, reducing the reliance on resupply missions from Earth. Companies are developing 3D printing technologies that can use lunar regolith, Martian soil, or even materials brought from Earth to create a variety of structures and parts on demand.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share. The asteroid mining sector in North America is experiencing rapid growth as both private and public sectors become more engaged in space exploration. Firms are persistently enhancing their space technologies, emphasizing the creation of effective spacecraft and resource retrieval techniques. These firms are leading initiatives to transform asteroid mining into a commercially feasible industry through advancements in propulsion systems, mining tools, and automation technologies. With substantial investments from private companies, the market is growing increasingly competitive, and fresh entrants are persistently introducing creative solutions to enhance the cost-effectiveness and sustainability of asteroid mining. This continuous technological advancement is driving the market. A significant factor in North America is the increasing need for vital minerals like rare earth elements, platinum, and water, which are plentiful on asteroids.

Key Regional Takeaways:

United States Asteroid Mining Market Analysis

The United States holds 80% share in North America. Increasing space missions are significantly driving asteroid mining adoption as more launches and explorations demand new sources of rare minerals and materials. For instance, more than 80 launches entered into space from Kennedy and Cape Canaveral in 2024, and 2025 promises to convey even more government and commercial missions to the Eastern Range. This surge in space launches, alongside the involvement of private companies like SpaceX and Blue Origin, provides a strong foundation for innovation in asteroid mining technologies. The continued support from NASA and other government agencies for space missions and exploration strengthens America's position as a key player in the market. Consequently, the active space mission environment is accelerating the adoption of asteroid mining technologies, aiming to enhance space exploration capabilities and secure essential materials for future interplanetary ventures.

Asia Pacific Asteroid Mining Market Analysis

The Asia-Pacific region’s asteroid mining market is driven by significant investments from emerging space agencies and private companies, particularly in Japan, China, and India. In 2018, Japan established a USD 940 million fund to support space startups, fueling innovation and exploration in space-related technologies. Additionally, Japan is sponsoring research in robotics, including the Space Capable Asteroid Robotic Explorer (Scar-E), a first-of-its-kind climbing robot with potential asteroid mining applications. This robot, developed through a collaboration between Japan’s Tohoku University and the Asteroid Mining Corporation, highlights Japan’s commitment to advancing asteroid mining technologies. Government-backed space missions, as well as growing industrial applications for extraterrestrial resources, further drive the development of the market in this region.

Europe Asteroid Mining Market Analysis

Europe’s asteroid mining market is supported by strong governmental backing, with the European Space Agency (ESA) allocating over USD 15 billion to its space budget in 2024. This substantial investment enables the continued development of space exploration technologies, including asteroid mining. The active operation and development of space stations also provide critical platforms for testing and deploying mining technologies in orbit. These efforts are complemented by Europe’s focus on sustainability, with asteroid mining offering an alternative to traditional terrestrial resource extraction that reduces environmental impact. Europe's growing interest in advanced space technologies is positioning the region as a leader in the asteroid mining sector.

Latin America Asteroid Mining Market Analysis

Limited resources on Earth are declining with the growing world population, fuelling asteroid mining adoption in the region. According to the Natural Resources Defence Council, 27 to 43% of the land in Peru, Bolivia, Chile, and Ecuador is being affected by the rampant forest loss. As terrestrial reserves diminish, the urgent need for alternative resource sources encourages investment in asteroid mining technologies. This trend reflects the growing recognition that space-based resources can help meet increasing material demands sustainably.

Middle East and Africa Asteroid Mining Market Analysis

The Middle East and Africa are experiencing a growing interest in asteroid mining, driven by the increasing demand for critical minerals like cobalt, lithium, nickel, and platinum. These minerals are crucial for industries like electronics, semiconductors, electric vehicles, and solar power, particularly due to their role in battery production, including lithium-ion batteries. However, the extraction of these minerals in regions like the Democratic Republic of Congo, which accounts for about 70% of global cobalt production as of 2023, has been marred by reports of human rights violations, including child and forced labor. With rising global demand, prices are expected to escalate, presenting a significant challenge, especially for developing nations. While alternatives like deep-sea mining have been proposed, they come with environmental risks, including potential harm to aquatic ecosystems. In this context, asteroid mining offers a promising alternative to terrestrial extraction, potentially alleviating some of these challenges while supporting the region’s commitment to technological innovation and sustainability.

Competitive Landscape:

Market players in the industry are actively involved in advancing space exploration and resource extraction technologies. Companies are developing spacecraft and mining technologies aimed at extracting valuable materials such as platinum, rare earth metals, and water from asteroids. These players are focusing on improving propulsion systems, refining mining techniques, and investing in automation to make asteroid mining more cost-effective. Additionally, they are collaborating with governmental agencies like NASA, which supports asteroid exploration missions. According to the asteroid mining market forecasts, as private sector investment continues to grow, new companies are expected to enter the market, contributing innovative solutions and increasing competition, which accelerates the pace of technological advancements in this emerging industry.

The report provides a comprehensive analysis of the competitive landscape in the asteroid mining market with detailed profiles of all major companies, including:

- Asteroid Mining Corporation Limited

- Moon Express Inc.

- OffWorld

- Shackleton Energy Company

- SpaceFab.US Inc.

- Trans Astronautica Corporation

Latest News and Developments:

- May 2025: China launched its Tianwen-2 spacecraft aboard a Long March 3B rocket to retrieve asteroid samples, targeting near-Earth asteroid Kamoʻoalewa about 10 Million miles away; the mission marked a milestone in asteroid mining as China aimed to return rock samples by 2027.

- March 2025: China University of Mining and Technology unveiled the nation's first homegrown space mining robot, which adapted to asteroid terrains and microgravity for advanced resource extraction. The six-legged prototype, inspired by insect claws, passed preliminary reviews and marked a key step in asteroid mining technology.

- February 2025: AstroForge revealed its second asteroid mining mission target, 2022 OB5, and announced a future launch partnership with Stoke Space. The Odin spacecraft was scheduled to launch in February aboard SpaceX’s Falcon 9 as a secondary payload on the IM-2 lunar lander mission.

- February 2025: Karman+ raised USD 20 Million in seed funding to advance asteroid mining aimed at fuelling the space economy, with support from Plural, Hummingbird, and other investors; the funds were allocated to develop its first tech demo and missions slated for 2027, targeting near-Earth asteroids for sustainable space resources.

- January 2025: AstroForge disclosed its Mission 2 target as asteroid 2022 OB5 and confirmed Odin would reach it 300 days post-launch, marking a pivotal move in asteroid mining. The company also finalized a multi-launch deal with Stoke Space and overcame earlier manufacturing setbacks to swiftly build the Odin spacecraft.

Asteroid Mining Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Asteroid Types Covered | Type C, Type S, Type M, Others |

| Phases Covered | Spacecraft Design, Launch, Operation |

| Applications Covered | Construction, Resource Harvesting, 3D Printing, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Asteroid Mining Corporation Limited, Moon Express Inc., OffWorld, Shackleton Energy Company, SpaceFab.US Inc., Trans Astronautica Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the asteroid mining market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global asteroid mining market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the asteroid mining industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Asteroid Mining Market Report

The asteroid mining market was valued at USD 2.6 Billion in 2025

The asteroid mining market is projected to exhibit a CAGR of 15.45% during 2026-2034, reaching a value of USD 10.0 Billion by 2034

Key factors driving the market include advancements in space exploration technologies, the rising global demand for rare earth elements, and increased private sector investment. These developments are facilitating more efficient and cost-effective asteroid mining operations, making resource extraction from space increasingly viable

North America currently dominates the asteroid mining market. The region is benefiting from significant technological advancements and private sector investments.

Some of the major players in the asteroid mining market include Asteroid Mining Corporation Limited, Moon Express Inc., OffWorld, Shackleton Energy Company, SpaceFab.US Inc., Trans Astronautica Corporation, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)